Pendal Concentrated Global Share Fund Hedged – Class R (APIR: RFA0031AU, ARSN: 098 376 151)

On 23 September 2021, the existing units of the Pendal Concentrated Global Share Fund Hedged (Fund) were reclassified as ‘Pendal Concentrated Global Share Fund Hedged – Class R’. The name of the Fund did not change and there were no changes to the terms of the class or your rights as an investor.

What do you need to do?

No action is required. You will be able to continue to invest or withdraw from the Fund.

An updated Product Disclosure Statement (PDS) was issued on 23 September 2021 and made available on www.pendalgroup.com.

Here are the main factors driving the ASX this week according to our head of equities Crispin Murray. Reported by portfolio specialist Chris Adams

INFLATION concerns eased last week and there were implications for central bank messaging.

There had been concern that higher inflation would prompt central banks to shift messaging more aggressively towards potential rate hikes.

That seems to be allayed for now.

This came via statements from central banks, a US labour report that indicated a return of supply, and the firming chances of Jay Powell being appointed for a second term at the Fed.

Bond yields fell in response. In combination with a decent US earnings season and good news on Pfizer’s antiviral pill, the S&P 500 rose 2.03% and the S&P/ASX 300 gained 1.91%.

US equities have had a strong run, up 9.17% for the quarter to date.

Australian equities have lagged, up only 2.02%. This reflects our skew to resources and the need to digest new capital issuance.

While they might pause for breath in the near term, equity markets should remain sell-supported into the year’s end.

Central banks outlook

Various statements from central banks went a long way to calming the market’s concerns about how quickly rates will need to rise.

The Fed announced it would begin tapering asset purchases by US$15 billion per month, implying that Quantitative easing would end in mid-June 2022.

This is in-line with expectations and was a dovish statement given speculation that the rate might have been accelerated.

Chair Powell was at pains to talk down inflationary fears. He noted that “transitory” did not necessarily mean “short-lived” — rather they were not expecting “permanently higher inflation”, ie a wage-price spiral. They did give themselves room to adjust their plans.

Pendal Focus Australian Share Fund

Now rated at the highest level by Lonsec, Morningstar and Zenith

A strong showing for the Republicans in gubernatorial elections in Virginia and New Jersey is seen as beneficial for Powell’s chances of securing a second term as Fed Chair.

The view is that the Biden Administration will not want to appoint a potentially less-predictable candidate to the Fed at this point.

The Bank of England caught the market on the hop when it kept rates stable. A 15bp rise had been signalled and widely expected. The BoE pushed back against the market projection for rate increases — citing signs of slowing economic momentum — and made the case for transitory inflation.

The market is still pricing in a 15bp move for December and is split as to whether the following one will be February or May.

So at this point major central banks are signalling a lagged response to rising inflationary pressure.

This also flowed through into a lower trajectory for projected ECB rate rises.

The RBA also adjusted its messaging.

The three-year yield target was removed as expected. The possibility of a rate rise in 2023 was also mentioned for the first time.

The Reserve noted that the labour market was stronger than expected, but border re-opening should provide additional supply.

This remains to be seen.

The market is still wary of inflationary pressures, particularly in housing. Nevertheless, there was relief that the RBA didn’t take a dogmatic stance towards the target for a first hike in 2024.

Economic outlook

The dominant narrative at this point is that global growth is accelerating following a hit from the Delta strain and disrupted supply chains.

Bottlenecks persist but there are signs the situation is improving.

This was reinforced by US payroll data, which showed 531,000 jobs were added in October, versus 450,000 expected.

The previous month was also revised upwards by 235,000 new jobs. The private sector added 604,000 new jobs, which was good, while the government sector shed 73,000 jobs.

Sustainable and

Responsible Investments

Fund Manager of the Year

The underemployment rate fell from 4.8% to 4.6%. Wages grow rose 0.4% to 4.9% year-on-year.

The household survey showed the labour force rose 104,000 after falling 183,000 in September.

However the participation rate remain a key variable in the outlook for wage inflation. It was 63% pre-pandemic, fell to 60% during the economic downturn and is now steady at 61.6%.

The St Louis Federal Reserve estimates there have been more than 3 million retirements in excess of what would normally be expected. This represents more than half the 5 million people who left the workforce since the beginning of the pandemic.

The resulting tight labour market can be seen in the ratio of employed workers to each new job opening, which is at its lowest point since measurement began in 2001.

So the outlook for inflation and bond yields — and the effect on growth stock premiums in the equity market — will be very tied to wage growth in the US.

This continues to move higher and is probably the key macro factor to watch in the coming year.

That said, it is worth noting that given the high rates of inflation, current real wage growth is negative.

This helps explain a backlash against the Democrats last week and a rising incidence of industrial action in the US.

Covid and vaccines

New daily cases in the US continue to flatten.

One factor to watch here will be the combination of waning immunity from vaccines and the onset of colder weather. We are seeing the number of people getting a third jab picking up quickly.

We are also watching the situation in China, which is going it alone in pursuit of zero-Covid. This could see an impact on economic growth — and potential demand for commodities.

The more important news was that Pfizer published data on its anti-viral pill, which so far in trials is indicating an 85% reduction in severe cases.

Markets

The US equity market may be a touch over-bought in the near term. But there are positive signals for the outlook into the year’s end:

- Bond yields look to have peaked near term as supply chain issues improve

- Market breadth is improving in the US, with the small cap Russell 2000 breaking higher after an eight-month consolidation and outperforming the broader market

- We are seeing US consumer discretionary stocks break out versus consumer staples. This is a signal of consumer confidence, though we are yet to see this in Australia.

In the US, 89% of companies have reported quarterly earnings.

Market eps is up 38% year-on-year. While a deceleration from previous quarters, this is well ahead of the +27% consensus expectation.

About 60% of companies have beaten expectations by a standard deviation or more, versus a long-term average of 49%.

Given the headwinds of supply chain and Delta this is a very good outcome.

The S&P/ASX 300 did well last week despite a drag from resources, which is the now the worst-performing area for the year to date.

About Crispin Murray and Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia. Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Find out more about Pendal Focus Australian Share Fund here.

A weekly income and fixed interest snapshot from Pendal assistant portfolio manager ANNA HONG

It’s been a topsy-turvy week.

Monday started with the after-shocks of the latest Australian CPI print which featured core inflation numbers that convincingly beat forecasts.

The lead-up to Tuesday’s Melbourne Cup race at 3pm was unusually nerve-wracking as many in the markets waited for Governor Lowe’s statement at 2.30pm.

It marked the continuing removal of extraordinary monetary policy in Australia. As expected, the RBA announced the termination of Yield Curve Control.

Finally we had Friday’s release of the Statement of Monetary Policy (SoMP).

The RBA pushed back against market sentiment, which is pricing in a 2022 rate hike.

Find out about

Pendal’s Income and Fixed Interest funds

The RBA maintains its central scenario of a 2024 rate hike, though it will no longer defend the 0.10% YCC target for April 2024.

The key drivers of the scenario are unemployment and inflation. Unemployment was only marginally revised lower since the forecast scenario expects a gradual tightening of the labour market.

Inflation was revised upwards. But the inflation forecast has largely discounted surges experienced in other countries. The RBA says the impact of supply chain disruptions is less evident in Australian CPI.

But there is strong evidence to suggest otherwise.

Unemployment — one of the key lynchpins — has rebounded remarkably.

Businesses regained confidence and started hiring in late September, readying themselves for the end of lockdown.

In the foreseeable future, laggard industries such as accommodation, air & transport services and construction will very likely pick up as the economy continues to re-open.

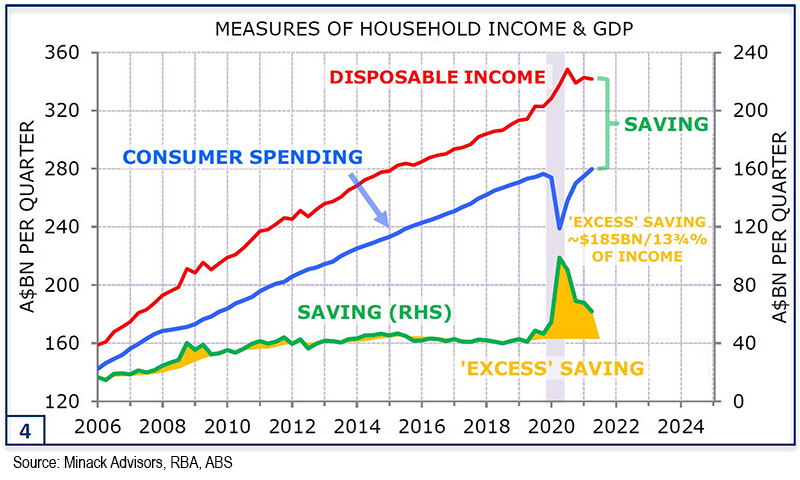

Australian consumers, flushed with cash, are on the same page as businesses.

The major banks are reporting that internal high-frequency consumer spending data demonstrates a strong recovery in consumer spending.

This may continue as disposable income grows and savings are unwound.

Market Implications

Even before the SoMP was released, the impact on housing credit could already be felt.

Westpac led the charge, raising fixed rate home loans by between 10 basis points (0.10%) and 21 basis points (0.21%). CBA followed with rate hikes to its home loan products, shortly after SoMP.

Before the SoMP, financial markets fully priced in a hike by July 2022 — with almost four increases priced by the end of 2022.

Markets eased off post-SoMP — but remained sceptical. Markets held firm to their pricing in of 2022 rate hikes.

Time will tell which side is right.

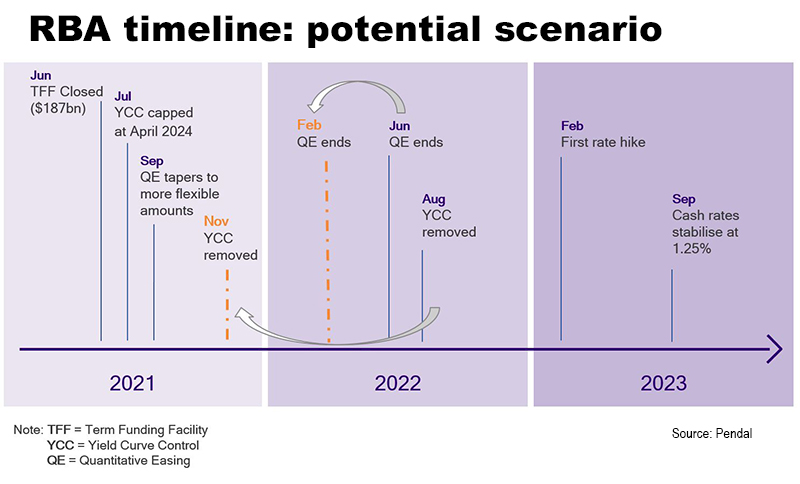

Here is Pendal’s time-line of potential RBA moves.

This timeline was first created in May. The arrows represent changes after recent RBA actions.

About Anna Hong and Pendal’s Income and Fixed Interest team

Anna Hong is an assistant portfolio manager with Pendal’s Income and Fixed Interest team.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia. In 2020 the team won the Australian Fixed Interest category in the Zenith awards.

With the goal of building the most defensive line of funds in Australia, the team oversees A$22 billion invested across income, composite, pure alpha, global and Australian government strategies.

Find out more about Pendal’s fixed interest strategies here

About Pendal Group

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Extraordinary monetary policy is ending. TIM HEXT explains what it means for investors

THE RBA’s abandonment of Yield Curve Control (YCC) — capping yields on three-year and shorter bonds to a target rate — was confirmed in its post-meeting statement, released half an hour before the Melbourne Cup.

Extraordinary monetary policy is in decline.

The RBA’s Term Funding Facility — which provided three-year funds to banks at 0.1% to help lower rates in the real economy — was closed in June and will wind down into 2023.

Quantitative Easing (QE) was reduced from $5 billion to $4 billion a week in August.

Now YCC is terminated. This leaves QE, to be reviewed in February, as the last extraordinary measure.

QE in Australia has always been more about matching the QE offshore central banks are doing to stop higher rates here and limit a higher currency.

The RBA will be comfortable with current AUD levels. It will be looking to the US Federal Reserve’s tapering plans announced shortly before deciding whether to abandon or merely reduce QE in February.

We think abandonment is more likely.

Find out about

Pendal’s Income and Fixed Interest funds

What next for rates?

The bigger question for the real economy is when do they actually hike rates?

Markets are pricing 1% by the end of 2022. Dr Lowe, in a post-meeting webinar, said hikes were highly unlikely in 2022. He was still thinking 2024 as likely, though he acknowledged 2023 was now live.

Normally such guidance would see everyone jump on the apparent cheapness of short rates. After all, the RBA sets the cash rate levels.

Right now though, the RBA seems to be playing catchup and markets think another “mark to market” will be needed next year. Their forecasting credibility is in question.

It all centres around the inflation and wages outlook.

Until this week the RBA was forecasting 1.5% underlying CPI by June 2022. There was a near-record upgrade to 2.25% this week.

This was a huge miss. While globally things are changing fast, it’s fair to say previous forecasts were not their finest hour. A decade of overestimating inflation seems to have given way to constant underestimation.

Our view for the past six months has been a first hike in February 2023 with cash rates peaking at 1.25% in late 2023.

We held this view through lockdown and for now maintain this view.

Market pricing means our bias to short duration has changed to a bias for long duration for now.

But we think inflation will be higher and more persistent than the RBA does, so we’ll happily turn neutral or even bearish should rates rally too far in November.

Dr Lowe may think late 2022 rate hikes are highly unlikely, but it would be a mistake to price them out.

About Tim Hext and Pendal’s Income & Fixed Interest boutique

Tim Hext is a Pendal portfolio manager and head of government bond strategies in our Income and Fixed Interest team.

Tim has extensive experience in banking, financial markets and funding including senior positions with NSW Treasury Corporation (TCorp), Westpac Treasury, Commonwealth Bank of Australia, Deutsche Bank, Bain & Co and Swiss Bank Corporation.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia.

Find out more about Pendal’s fixed interest strategies here

About Pendal

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

In 2023, Pendal became part of Perpetual Limited (ASX:PPT), bringing together two of Australia’s most respected active asset management brands to create a global leader in multi-boutique asset management with autonomous, world-class investment capabilities and a growing leadership position in ESG.

Here are the main factors driving the ASX this week according to portfolio manager Jim Taylor. Reported by portfolio specialist Chris Adams

There’s plenty going at the moment.

At a headline level, the S&P/ASX 300 shed 1.13% last week, while the S&P 500 was up 1.35%.

Domestic inflation data prompted a large divergence between US and Australian bond yields. US earnings season maintained a good trajectory, though supply chain issues are making themselves felt.

Commodity prices took a hit on some policy announcements in China.

The market is doing what it does best — testing the resolve and conviction of key constituents. The RBA’s response to recent moves will be important to watch in this context.

Covid and vaccines

There are indications Delta waves may be peaking in recent hot spots such as Romania and Singapore. This is consistent with the experience of other countries.

The issue of vaccine availability in the world’s poorest countries is one to watch.

While almost 60% of the world’s population have had two vaccine does, parts of Africa, Eastern Europe and emerging Asia are running well below that figure.

News that Merck has agreed to license drug makers globally to produce its oral antiviral medicine Molnupiravir without royalties could be a material benefit to countries that are vaccine constrained.

Economics and policy

There were a couple of quarterly data points out of the US last week.

US GDP grew 2% sequentially in the third quarter (seasonally adjusted), down from 6.7% growth in the previous quarter. As a result, annualised growth for 2021 is now running at 4.98% (down from 5.82%).

The more important point to watch in terms of questions over monetary policy was the Employment Cost Index, which measures total compensation to workers including salaries, wages and benefits.

Pendal Focus Australian Share Fund

Now rated at the highest level by Lonsec, Morningstar and Zenith

This grew at its fastest pace in more than 30 years, rising 1.3% quarter-on-quarter. It is up 3.7% from a year earlier.

This headline increase was driven by a 1.5% spike in wage growth over the quarter, versus 0.9% growth in Q2.

The question is: does this start to slow in the current quarter as labour supply rebounds? If it doesn’t, the market is likely to lose faith in the “transitory” inflation narrative and the Fed will come under pressure to start hiking rates sooner.

European Central Bank president Christine Lagarde acknowledged that inflation will be higher for even longer than first thought. But she maintained the increase will be temporary, so a policy response would be premature.

She identified higher energy prices, a global mismatch between recovering demand and supply and one-off effects of a German sales tax as three factors temporarily driving inflation.

There are reports that Chinese banks are starting to ease credit controls in response to government concerns about the potential effect of a slowing property sector on the broader economy.

Banks in some areas have accelerated issuing home loans and lowered mortgage rates. The credit environment for property developers is also improving.

Australian bond yields

Australian 10-year government bond yields rose 29bps last week to 2.09% — versus an 8bp fall in the US equivalent.

Three factors drove the recent rise in yields:

- This shift began as New Zealand inflation data for the quarter came in at 2.2% versus 1.5% expected. This was treated as a lead indicator for Australia — and so it proved

- Australian headline CPI was in line with the expected 0.8% quarter on quarter and 3% year on year. But underlying CPI — the trimmed mean which is the RBA’s preferred indicator of inflation — rose 0.7% vs 0.5% expected. This was driven largely by housing construction and auto fuel prices. It is now sitting at 2.1% year on year versus 1.9% expected.

- The spike in bond yields is seen as a sign that the RBA is stepping back from yield-curve control given recent data — and may formally abandon it.

The market is aggressively pricing in both the end of yield curve control and rate hikes prior to the RBA’s previous target of 2024.

The RBA meeting on Melbourne Cup Day will be keenly watched in this regard.

Sustainable and

Responsible Investments

Fund Manager of the Year

Markets outlook

US earnings season continues to play out well — 63% of companies have so far beat earnings estimates.

That said, the market is not rushing to upgrade outlooks. Revisions to fourth-quarter and FY22 earnings and margins have been very modest.

Supply chain issues are evident. Apple said supply chain issues cost it US$6 billion in sales for the quarter, with a bigger impact coming in the current quarter.

Iron ore fell 10.9% and copper lost 2% as Beijing stepped in to control the price of coal.

China’s National Development and Reform Commission set a target price and price ceiling for domestic coal at the pit-head until May 2022.

It is also looking for downstream sale prices to be controlled, but will let local governments set their prices.

The focus is alleviating pressure on coal prices for power production. The thermal coal price has almost halved from its highs, but is still up more than 100% since the start of year.

Australian equities had a flat start last week, but sold off on bond market volatility in the last two days.

About Jim Taylor and Pendal Focus Australian Share Fund

Drawing on more than 25 years of experience investing in top-performing Australian companies and a background in accounting, Jim manages our Long/Short Fund and co-manages our Imputation Fund. He is a Chartered Accountant with membership of the Australian Institute of Chartered Accountants.

Pendal Focus Australian Share Fund is managed by Crispin Murray. The fund has beaten its benchmark in 12 years of its 16-year history (after fees), across a range of market conditions. Find out more about Pendal Focus Australian Share Fund here.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

It’s been one of the biggest months in bonds ever. An unravelling expected over six months happened in three days. Pendal portfolio manager TIM HEXT explains what’s going on

SUNDAY is Halloween and I’m tempted to dress up as the bond market.

It’s been a scary month. 10-year yields are up 0.6%. Three-years are up almost 1%. Holders of a Composite Bond Strategy will be down around 5% on what are supposed to be safe investments.

So what happened?

The first reason is globally central banks are talking tapering and potentially higher rates.

The RBA was supposed to be different though. They have been very firm in expressing a willingness to be behind the curve and the need to see both inflation and wages at target (2.5% and 3%).

Even in early October they thought they could wait till 2024 at the earliest. Last week they even bought bonds to support their yield curve control (YCC) at 0.1% for the April 2024.

Then the great unravelling began.

The Q3 underlying inflation numbers came out at 0.7% — above the RBA and market expectation of 0.5%.

The market was cautious but surely one number would not see the RBA abandon its guidance and YCC?

It seems the RBA has done just that — the final nail in the bond coffin.

Find out about

Pendal’s Income and Fixed Interest funds

Find out about

Pendal’s Income and Fixed Interest funds

Either the RBA is ghosting the market (ask your nearest Millenial if you don’t know what that means) or next Tuesday will bring a massive about turn from the RBA.

Today (Friday) they were noticeably absent.

The April 2024 bond they are supposedly targeting with yield curve control at 0.1% last traded at 0.7%.

And no word. Nothing.

No doubt they are revising up their inflation forecasts to be published next week, which will provide the cover for the change of view.

Radio silence this week though means the market is left to second guess their inaction.

Today has seen another 0.25% sell-off to seal one of the biggest months in bonds ever — and not from the good side.

We expected this to unravel slowly over the next six months. It has happened in three days.

I have always said the RBA is like an oil tanker not a speedboat.

Unless a crisis hits like March 2020 they move slowly and gradually communicate the whole time. I now need a new analogy.

Once the dust settles and momentum slows, bonds will be something we have not seen in a long while — cheap.

However with even the RBA confused and wrong-footed, now is not the time.

On a final note, 10-year real yields are now positive.

If you have deep pockets lock some away. I doubt you’ll regret that one.

About Tim Hext and Pendal’s Income & Fixed Interest boutique

Tim Hext is a Pendal portfolio manager and head of government bond strategies in our Income and Fixed Interest team.

Tim has extensive experience in banking, financial markets and funding including senior positions with NSW Treasury Corporation (TCorp), Westpac Treasury, Commonwealth Bank of Australia, Deutsche Bank, Bain & Co and Swiss Bank Corporation.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia.

Find out more about Pendal’s fixed interest strategies here

About Pendal

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

In 2023, Pendal became part of Perpetual Limited (ASX:PPT), bringing together two of Australia’s most respected active asset management brands to create a global leader in multi-boutique asset management with autonomous, world-class investment capabilities and a growing leadership position in ESG.

The income game has changed and Pendal’s income strategies have evolved to look very different to traditional income portfolios. Pendal portfolio manager AMY XIE PATRICK explains

LOW YIELDS and skinny corporate bond coupons are not the makings of a traditional income portfolio.

That’s the challenge that many bond-only income products face today.

A 30-year bond bull market has been a massive boon for income portfolios heavily reliant on credit. In a falling yield environment, you can reap the full benefits of corporate bond yields — and many investors have pushed into riskier and high-spread exposures.

This has been very supportive for credit as an asset class. But the game is now changing.

The 30-year bond bull-run has come to a close. Inflation is the market zeitgeist. Any traditional income portfolio will lack the necessary levers to confront it.

Rising bond yields need to be hedged. Those hedges eat into the already scant levels of income such portfolios are now generating.

A rising yield environment will also cause more dispersion in the performance of credit. Portfolios that have loaded up on lower quality offerings in recent years are likely to see more headwinds.

That’s why Pendal’s income strategies look very different to those traditional income portfolios.

Find out about

Pendal’s Income and Fixed Interest funds

Other levers needed

High-quality credit serves as an essential income building block, but the overall portfolio needs other levers to manoeuvre through different market environments.

If the environment is inflationary, there need to be other sources of income besides fixed rate credit.

The Pendal Monthly Income Plus Fund currently has a 19% allocation to Australia equities, with room to add further.

This is not only a way to help the portfolio keep up with the reflation narrative. The income from equity dividends frees us from relying heavily on accruals from fixed rate instruments.

As a result, the Monthly Income Plus Fund’s exposure to interest rate risk is the lowest it’s been for more than five years.

Importantly, should sentiment suddenly turn more bearish, de-risking will be far easier in equities than in credit due to its liquidity advantage.

In the Pendal Dynamic Income Fund, a 20% allocation to floating rate emerging market sovereign exposure helps generate additional income, while capturing the spread compression opportunity as investors seek portfolio diversification from asset classes such as Emerging Markets.

Similarly, the Dynamic Income Fund’s interest rate exposure is currently minimal.

Having non-traditional levers to gain additional exposure to income and market upside has given us the luxury to not chase lower quality credit deals when they come to the market.

Instead, cognisant of the rising yield environment, we are running higher-than-normal cash balances that are waiting to be deployed at more attractive yield (and hence income) levels.

Flexibility via multiple levers, a focus on quality, and agility on interest rate exposures are the makings of a resilient income portfolio.

About Amy Xie Patrick and Pendal’s Income and Fixed Interest team

Amy is Pendal’s Head of Income Strategies. She has extensive expertise and experience in emerging markets, global high yield and investment grade credit and holds an honours degree in economics from Cambridge University.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia. The team oversees some $20 billion invested across income, composite, pure alpha, global and Australian government strategies.

Find out more about Pendal’s fixed interest strategies here

About Pendal Group

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

Most investors are now aware of climate change risks. But biodiversity preservation may be an even bigger and more immediate issue. EDWINA MATTHEW explains

Countries representing 90 per cent of global GDP are now covered by net-zero targets, highlighted at the recent COP26 climate change conference in Glasgow.

We will soon know if those targets are sufficiently ambitious to keep global warming to 1.5 degrees — meeting the Paris Agreement adopted at COP21 in 2015.

But net zero emissions by 2050 is not the whole story.

As Glasgow was ramping up for COP26, the southern Chinese city of Kunming was just winding down after another COP (or Conference of the Parties) which focused on conserving biological diversity.

At COP15, 195 countries pledged to reverse biodiversity loss by 2030 at the latest and agree on a framework to protect species and their habitats.

Biodiversity may not be as attention-grabbing as climate change. But it is a critical part of the overall solution and directly impacts many industries.

Agriculture. Medicine. Insurance. Real estate. Tourism. To name a few.

Half of the world’s total GDP — or some US$44 trillion of economic value generation — is moderately or wholly dependent on nature and its services, according to the World Economic Forum.

“Climate change is a very complicated issue, but biodiversity is on a whole other level,” says Pendal’s Head of Responsible Investments, Edwina Matthew.

Sustainable and

Responsible Investments

Fund Manager of the Year

Twin crises

Climate change and biodiversity loss are inter-related, “twin crises”, says Matthew.

Climate adaptation strategies such as protecting and restoring natural habitats offer defence against the physical impacts of climate change.

Nature-based solutions are also part of the broader universe of carbon removal projects underlying the carbon credits or offsets that are part of net zero strategies.

But climate change itself is destroying our natural capital (soil, air, water and living organisms) and biodiversity ecosystems — as seen in Australia’s Black Summer bushfires.

“Encouragingly, governments, business and investors are starting to understand that nature and climate can’t be separated — and that nature-related impacts and dependencies need to be considered alongside climate-related exposures,” says Matthew.

“We need to invest in mutually reinforcing solutions. A 1.5-degree pathway cannot be achieved without major investments in natural capital.”

Industries threatened by biodiversity loss

Agriculture is the most obvious example of an industry threatened by loss of biodiversity.

The agriculture sector accounts for a quarter of Australia’s exports (and employs 60 per cent of the world’s working poor).

Scientists estimate $US577 billion of annual crop production is at risk from loss of pollinators like bees.

The Worldwide Fund for Nature says 60 per cent of the world’s coffee varieties are in danger of extinction due to climate change — a sector with more than US$80 billion in global sales.

Nearly half of all medicines are derived from natural sources.

“We’re also starting to see scientists linking the transmission of animal disease to humans because of a breakdown in biodiversity buffers,” says Matthew. “We had SARS, now we have COVID.”

The UK Treasury’s Dasgupta Review on the Economics of Biodiversity released earlier this year says the “devastating impacts of COVID-19 and other emerging infectious diseases — of which land-use change and species exploitation are major drivers — could prove to be just the tip of the iceberg if we continue on our current path”.

Find out about

Pendal Horizon Sustainable Australian Share Fund

Much of global tourism is linked to natural attractions. The Great Barrier Reef brings in $A1.5 billion a year in tourism and fishing.

The loss of wetland buffers for flood-prone areas can expose real estate and insurance companies to higher risk.

Nature also helps regulate the climate itself — as we acknowledge in the development of nature-based carbon offsets.

What it means for investors

Just as investors now understand the risks posed by climate change, so too natural capital and biodiversity considerations are starting to creep into the investor engagement and corporate reporting agenda.

“It’s twofold,” says Matthew.

“It’s about understanding biodiversity loss as a top-down, systemic issue — as a threat to the global economy — as well as understanding and managing bottom-up, company-specific natural capital and biodiversity-related exposures.

“It’s also about holding companies to account for their impacts, as we do for climate. What role do they play in adverse outcomes for biodiversity and natural capital? How are companies embedding these considerations into their own governance structures and risk management frameworks?

“And to what extent are they dependent on natural capital for their own business? How do they think about biodiversity loss and related policy and regulatory trends and shifts in key stakeholder expectations?

“A lot of the learnings we’ve had from climate change are starting to play out in the natural capital space.”

The good news is, companies are starting to respond.

“We are seeing efforts in mining, property and finance to build understanding around dependencies and impacts in business models and supply chains.”

Biodiversity and land management reporting is already a feature in some company public disclosures.

“Just last month BHP acknowledged evolving stakeholder expectations about its efforts to achieve nature-positive outcomes during an ESG investor roundtable.”

The newly launched Taskforce on Nature-related Financial Disclosure — supported by the United Nations and endorsed by G7 ministers and financial institutions — is setting up a risk management and disclosure framework for organisations to report and act on nature-related risks.

The taskforce supports a shift in global financial flows away from “nature-negative” outcomes toward “nature-positive” outcomes.

Opportunities

Similar to the transition to a “low-carbon economy”, a transition to a “nature-positive economy” also offers economic opportunities.

There is potential for almost 400 million jobs and some $US10 trillion in annual business value by 2030 across three socioeconomic systems (food, land and ocean use; infrastructure and the built environment and energy and extractives) according to WEF.

Pendal clients are exploring how they can direct capital to support nature-positive outcomes, Matthew says.

“They have a fiduciary and financial interest in the wellbeing of the economy as a whole. They expect active managers like Pendal to exercise our ownership rights on behalf of our clients to encourage the protection of natural capital.

“They are also seeking opportunities for how they can allocate capital to support and scale nature-positive outcomes.”

Pendal will “continue to work with our clients and other stakeholders to build understanding around biodiversity loss and access to nature-positive investment solutions to help tackle the next sustainable investment challenge,” Matthew says.

About Edwina Matthew

Edwina Matthew is Pendal’s Head of Responsible Investments. Edwina is responsible for maintaining our leadership position in the provision of sustainable and ethical investment products.

Edwina is actively involved in the implementation of the UN-supported Principles for Responsible Investment. She also represents the company in working groups with a number of industry associations and initiatives relating to responsible investment.

About Pendal Group

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

We believe sustainability considerations ultimately drive higher and more stable investment returns over the long term.

Pendal Group has a proud heritage in responsible investing, extending back decades. Our specialist responsible investing business Regnan includes highly experienced ESG research and engagement experts and offers a growing range of investment strategies.

Some of our responsible investing strategies

ASX small caps have outperformed the top 100 companies over the past year. But investors need to be increasingly aware of ESG factors which often go under-reported. Pendal’s LEWIS EDGLEY and DAMIEN DIAMANT explain

SMALL CAPS provide a chance for investors to diversify portfolios away from the more mature behemoths that dominate the top end of town.

They are often driven by very different themes to the macro factors that typically affect the ASX100.

Pendal Smaller Companies portfolio manager Lewis Edgley points to successful technology businesses, innovative online retailers and companies producing materials used in batteries such as lithium, cobalt and nickel.

“These are new-world businesses that offer exposure to disruptive business models — much more so than the large cap index,” says Edgley.

Small caps are further up the risk return spectrum relative to their large cap counterparts. But they provide access often to undiscovered companies that can present outsized returns relative to their risk profiles.

The ASX Small Ordinaries index (which measures companies in the top 300 minus the top 100) — outperformed the ASX100 over the past year.

“Small caps are generally under-researched relative to their large cap counterparts, while offering more attractive growth prospects” he says.

“We find many opportunities to invest alongside business founders and management teams that have significant shareholdings, which creates a strong alignment of interest with investors.”

Find out about

Pendal Smaller

Companies Fund

New opportunities

Small caps also offer a continual flow of new opportunities.

“About 20 per cent of the Small Ords listed in the last five years. That amount of refresh in our investable universe means the small cap sector is never stale.

“In the last two years our team has evaluated literally hundreds of new IPOs, the majority of which don’t make the cut… In the last month alone, we’ve had nearly 10 IPOs worth more than $1 billion each come across our desk.

“Investors need to be discerning about which to participate in. Some are blatantly opportunistic, just trying to take advantage of bull market conditions and the broader market’s willingness to discount risks.

“By sticking to our proven investment process we expect to do well on the select few IPOs we’ve recently supported.”

ESG a factor to watch

For all the opportunities, the sector is not without risk. Environmental, Social and Governance (ESG) issues are a significant emerging factor that small cap investors need to watch.

Unlike large companies, small caps often do not have the resources or expertise to measure and report on ESG risks. They can go unheralded in company reports.

“Most of the companies we talk to are not sufficiently resourced to have a fully enunciated plan in terms of how they are going on their ESG journey,” says Edgley.

“We work with companies to provide our insights on what is important from an ESG perspective. We share what we think is important and help them formulate a framework so they can set sensible and realistic targets.

“We find many small caps are doing a number of things that would already rate them well on an ESG screen — but they’re not actually recording and reporting on them.”

City Chic Collective (ASX:CCX)

Pendal small cap investment analyst Damien Diamant gives the example of fashion retailer City Chic Collective (ASX:CCX), an ecommerce company held in the Pendal Smaller Companies Fund.

“We spent time with the company running through their supply chain and actions they’re taking to ensure they have a positive impact on communities.

For example CCX — which focuses on plus-sized fashion — has moved to ban raw materials sourced from high-risk regions, such as cotton from Xinjiang.

Xinjiang cotton is regarded as high-quality, but human rights campaigners say it is produced by forced labour.

CCX has also focused on water and waste management, sustainable packaging and recycling.

“We’re happy with the progress made to date” says Diamant. “As a smaller company there are obviously limitations to the resources that go into developing a detailed ESG reporting framework.

“But they have a strong awareness of the risks and are taking a proactive response to ethical trade.”

The small caps team is further integrating ESG into its investment process, says Edgley.

“We’ll continue to work closely with our investee companies to gain a deeper understanding of their priorities in this emerging space,” he says.

“We’re fortunate to have the support of a dedicated Responsible Investment team at Pendal. Their insights and guidance have been invaluable as we embark on this ESG journey.”

About Lewis Edgley and Patrick Teodorowski

Lewis and Patrick are co-managers of Pendal Smaller Companies Fund.

Portfolio manager Lewis Edgley co-manages Pendal’s Australian smaller companies and micro-cap funds and conducts analysis on a range of smaller companies. He joined the Pendal Smaller Companies team in 2013 as an analyst, before being promoted to the role of portfolio manager in 2018. Lewis brings 20 years of industry experience with previous roles spanning equities research, as well as commercial and investment banking roles at Westpac and Commonwealth Bank.

Portfolio manager Patrick Teodorowski co-manages Pendal’s smaller companies and micro-cap funds and conducts analysis on a range of smaller companies. He joined Pendal in 2005 and developed his career as a highly regarded small cap analyst. Patrick holds a Bachelor of Commerce (1st class Honours) from the University of Queensland and is a CFA Charterholder.

About Pendal Smaller Companies Fund

Pendal Smaller Companies Fund is an actively managed portfolio investing in ASX and NZX-listed companies outside the top 100. Co-managers Lewis Edgley and Patrick Teodorowski look for companies they believe are trading below their assessed valuation and are expected to grow profit quickly. Lewis and Patrick together have more than 40 years of investment experience.

Find out about Pendal Smaller Companies Fund

Find out about Pendal MicroCap Opportunities Fund

Find out about Pendal MidCap Fund

About Pendal Group

Pendal is a global investment management business focused on delivering superior investment returns through active management.

In 2023, Pendal became part of Perpetual Limited (ASX:PPT), bringing together two of Australia’s most respected active asset management brands.

Here are the main factors driving the ASX this week according to our head of equities Crispin Murray. Reported by portfolio specialist Chris Adams

MARKETS enjoyed a good, broad-based rally last week. This was despite a continued rise in bond yields and ongoing concern about Chinese growth.

The diminishing probability of a hike in US corporate taxes helped sentiment. So, too, did generally supportive US earnings.

The S&P/ASX 300 rose 0.72% and the S&P 500 1.67%.

COVID and vaccines

Case trends in the US and Asia are generally headed in the right direction, though there are concerning signs in Europe.

A renewed wave in the UK suggests it may be following the same path as Israel, where case numbers picked up as vaccine protection waned.

German cases are also increasing. Some Eastern European countries, where vaccination rates are low, are also seeing a surge. Romania is a case in point.

There is also an outbreak in Singapore, which is notable since 81% of the population is vaccinated.

We may be at an inflection point for a renewed surge in cases, led by Europe. The critical relationship between vaccinations and fewer severe infections and hospitalisations continues to hold, but needs to be watched.

Pfizer released results from its first booster trial.

A sample of 10,000 vaccinated people showed five new Covid infections among the half who received the booster and 109 in the remainder who had a placebo.

Importantly, there were no severe infections in either group. This reinforces the idea that while a vaccine’s ability to prevent infection wanes, its ability to prevent severe infection may be more enduring.

Economics and policy

It was generally a good week for data. Flash PMIs, a leading indicator of activity, came in better than expected in Japan and the EU.

In the US, the manufacturing flash PMI was weakened by supply chain factors, but strength in the services PMI more than made up for it. This is important, since the service sector — which is benefiting from re-opening — is roughly five times larger than manufacturing in the US.

Pendal Focus Australian Share Fund

A high-conviction equity fund with 16 years of strong performance in a range of market conditions

It is worth watching US credit growth. This was persistently disappointing in the post-GFC era, one symptom of the lacklustre recovery.

It has remained muted in this cycle due to excess household savings accrued during Covid. But US bank results suggest we might be seeing credit growth building. If this occurs it will further support the sustainability of economic growth.

So the demand environment remains firm.

If this coincides with alleviation of supply chain pressure, it should be a positive environment for equities.

Inflation and yields

The inflation issue remains very live.

The UK is seen as something of a bellwether. September inflation data in the UK was a little softer than expected, but forward expectations are rising sharply. The market is pricing in a 21bp rate increase in November as the Bank of England needs to be seen to react to rising inflationary expectations.

Longer-term indicators of US inflation — such as house prices, wages and retailer pricing power — continue to rise. So too are prices in the service sector.

This is flowing through into a continued re-pricing of the short end of the bond curve.

US two-year government bond yields have doubled from about 20bps to 46bps in October, reflecting expectation of tightening. The consensus view is that when tapering begins it will do so at the higher end of the range (about US$20 billion per month) and the first rate hike will come in June.

Policy moves

Negotiations around President Biden’s reconciliation bill are nearing a conclusion. The final package looks likely to be around US$1.8 trillion rather than the original US$3.5 trillion plan.

The debate over how it is funded has been interesting. Democrat senator Kyrsten Sinema of Arizona refused to withdraw an objection to any change in corporate, capital gains or personal tax rate. If corporate tax hikes don’t eventuate — which is now quite possible — US earnings expectations could rise 5 per cent.

In China, beleaguered property developer Evergrande paid interest on its first bond, due just before the end of a 30-day grace period. It has avoided default for this week. But another payment is due Friday and there are more after that.

Meanwhile Beijing is dealing with another Delta outbreak — 10 of 31 provinces have reported cases. Restrictions have been imposed, potentially providing another economic drag.

Sustainable and

Responsible Investments

Fund Manager of the Year

The central government is telling provinces to accelerate their issuance of government bonds, to use up the 39% of annual allocation they have remaining for 2021. The spending is unlikely to make an impact this quarter, but is supportive of Chinese growth in coming years.

This week the European Central Bank will meet. At this point the market is pricing a 40bp hike in rates by the end of 2023. It will be interesting to see if there is any push-back by the Bank — or if it acknowledges building inflationary pressure.

Markets

While inflation pressures remain significant, there is a case for nearer-term stability in bond yields as China remains in a slumber, global Covid cases start to rise again and supply chain pressures ease.

This would support a rotation back to growth.

We retain a material growth exposure with companies targeted at corporate or institutional end markets, rather than the consumer.

US earnings

About a quarter of the US market has reported quarterly earnings so far. Some 65% have beaten consensus expectation by more than one standard deviation. If this holds it will be another strong quarter with earnings running 8% ahead of estimates.

Revenue growth has exceeded expectations in 57% of companies compared to a long-term average of 35%.

The market is focused on labour costs, which are rising. But to date most companies have indicated they can offset this via higher prices.

While the quarter looks strong, this has not flowed through to large consensus upgrades for CY22, since the market remains wary of supply chains and labour costs.

It’s worth noting that social media company Snap Inc’s result highlighted a second-order effect of supply chain issues: companies with less product to sell are scaling back advertising.

This may provide read-through for Google and Facebook, which are yet to report.

Australia

Stocks leveraged to Chinese supply chains started to do better, reflecting our observation last week that signals such as power availability and freight rates were improving.

We saw a disconnection in commodity markets. Oil remained well supported but there were corrections in other commodities. It is worth noting technical signals that some commodities such as aluminium have peaked for now.

About Crispin Murray and Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia. Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Find out more about Pendal Focus Australian Share Fund here.