Here are the main factors driving the ASX this week according to Pendal investment analyst GRAEME PETRONI. Reported by investment specialist Chris Adams

- The Fed and BoE cut rates by 25bps, the RBA remains unchanged

- Economists modelling various scenarios for Trump’s policies

- Find out about Pendal Focus Australian Share Fund

IT was a big week for markets following the US election.

The S&P 500 rose 4.69% on pro-growth policies around tax cuts and deregulation.

Bond markets stabilised after sharp moves higher in the lead up to the election, with the outcome suggesting a lower trajectory for US rates.

Trade tensions dragged on Europe, while China benefited from optimism in the lead up to the NPC meeting, which ultimately failed to deliver on expectations.

The Australian market echoed the US with respect to financials, tech and cyclical industrials outperforming, while taking a more cautious approach to resources – with the S&P/ASX 300 closing the week up 2.23%.

While macro moves dominated, there was a fair amount of news flow, particularly from bank reporting season.

Banks reported solid results but without any further follow through on the positive thematics that had been building around margins and balance sheet.

US election

The US election is widely regarded as having been won on the economy. The catch cry “are you better off than you were four years ago?” clearly resonated.

It looks likely to be a clean sweep of the popular vote, electoral college, Senate and House, potentially giving Trump a mandate for reform. However, the House is close and the Senate lead is slim, which may put some constraints on passing legislation.

Trump talked about some big policies throughout his campaign, like a significant lift in tariffs (50-60% on China, 10-20% rest of world), tight immigration controls (15-20 million deportations) and lower taxes (extend 2017 cuts, no taxes on social security, overtime and tips).

But in his post-election speech, there was no mention of tariffs or China and references to immigration were dialled down (“we’re going to have to let people come into our country… but they have to come in legally”).

This illustrates significant uncertainty on the extent to which Trump’s campaign policies are implemented.

Economists have modelled various scenarios.

If tariffs are limited to 20% for China and 5% for the rest of world, and if net migration only moderates to 500,000 per annum, the inflationary impact is contained to 0.5 percentage points (ppt).

There is also a negative growth impact, but this would potentially be offset by taxes and deregulation.

The end outcome for the Federal Reserve (the Fed) is estimated to be two to three fewer cuts in 2025, potentially implying US cash rates don’t fall much below 4%.

However, this will depend on the degree to which campaign policies are pursued.

The directional impact of Trump policies is clear: bad for bonds, supportive for equities (at least in the near term), some volatility risks, positive for financials, and negative for property, resources and US homebuilders.

Markets have moved a long way in a short space of time and there are still a lot of unknowns to play out.

US interest rates

The Fed played a straight bat, continuing with a 25-basis-point (bp) rate cut (4.50%-4.75%) and making only minor changes to statement wording.

In response to questions about post-election policy impacts, Chairman Powell made it clear that the Fed would not pre-empt changes, saying “we don’t guess, we don’t speculate, and we don’t assume”.

On the outlook, Powell noted that the labour market had cooled and that the Fed was alert to any further deterioration.

There was also confidence expressed that inflation would reduce to target.

Against this, economic growth has been stronger than expected, and Powell said the Fed was starting to think about when to slow the pace of cuts.

This suggests consecutive cuts for now, slowing into 2025.

Pendal Focus Australian Share Fund

Now rated at the highest level by Lonsec, Morningstar and Zenith

US economic data

US economic data remains reasonably strong, though there are some mixed signals for the labour market:

Initial jobless claims were benign, with 221k per consensus, continuing to moderate.

-

The Michigan Consumer Sentiment Survey was published, covering the two weeks before the election. The index resumed its uptrend, lifting from 70.5 to 73.0 over the month (above consensus of 71.0). This was despite a 0.5 ppt dip in current conditions to 64.4 – more than offset by a surge in expectations to 78.5.

-

The ISM Services Index lifted from 54.9 in September to 56.0 in October, which was above consensus of 53.8 and could suggest a pickup in the economy. However, the index appears more consistent with stability in Services spend rather than an acceleration. And within the ISM Services data, the price paid index remains supportive of a moderation in inflation.

-

Non-farm productivity increased 2.2% (annualised) in the third quarter. This slightly missed consensus of 2.5% but the prior history was revised up, pointing to strong post-Covid productivity gains. Within the data, unit labour costs increased 1.9% (annualised) in the quarter, which is a potential concern for inflation. But the index has tended to be heavily revised over time and other indicators point to a softening of the labour market.

-

Initial jobless claims were benign, with 221k per consensus, continuing to moderate.

UK interest rates

As widely expected, the Bank of England Monetary Policy Committee cut the official rate 25bp to 4.75%.

Growth and inflation forecasts for 2025 lifted sharply following the UK Budget.

While guidance was retained for a gradual approach to policy easing, this is now subject to “evolving data” rather than “absent material developments”.

This suggests a pause in December and modest pace of cuts through 2025.

However, trade tensions could pose a risk to growth and increase the case for cuts over the course of 2025.

Australian interest rates

The RBA left the cash rate unchanged at 4.35% (in line with consensus) and made minimal changes to its outlook.

From the RBA’s perspective, restrictive policy settings are having their intended effect, with inflation moderating.

Household consumption has slowed, but with an offset from public spend.

The RBA made the point that local rates had never risen as much as in other developed countries, and even with cuts offshore (from the US, UK, EU, Canada, New Zealand), rates here remain less restrictive.

Reflecting this, it noted that inflation hasn’t moderated as sharply as offshore and labour markets remained relatively tight.

The market continues to debate when the local rate-cutting cycle will begin – whether early or mid-2025.

The RBA is not expecting inflation to reach the top of its band until late 2025, with the middle to be reached in late 2026.

But there is potential for US tariffs on China to have a negative flow through domestically, depending on China’s response.

China policy

If the US imposed the full 60% tariff on China, the impact to China is estimated at -2ppt of GDP.

This would fall to sub -0.5ppt in the event of a 20% tariff, with the potential for this to be offset by currency depreciation and fiscal policies. However, we have yet to see a fiscal response.

On Friday, the National People’s Congress (NPC) Standing Committee announced a RMB 10 trillion increase in the local government debt resolution over the next four years.

This should reduce local government interest costs and gradually improve infrastructure investment.

But there was nothing on the RMB 2 trillion worth of fiscal initiatives that had been speculated on in the press to cover bank recapitalisation and stimulate consumption.

Perhaps this is not surprising; the NPC is designed to approve pre-proposed policies – not launch new ones.

Policymakers will review fiscal budgets at the Economic Work Conference in December. Any announcement would then be communicated at the Two Sessions meetings in March 2025.

Given domestic weakness, in addition to any export threats, there is clear pressure to act.

US reporting season

Some 84% of S&P 500 companies have reported, with the largest stock – Nvidia – yet to come.

The frequency of beats returned to a more normal 51%, down on recent quarters.

Consensus EPS revisions are also back to a more normal trend.

Typically, consensus is downgraded as the year progresses, which we’re starting to see again for the “S&P 493”, excluding the Mag 7 stocks.

By sector, tech and financials were among the better performers while real estate, materials and energy struggled.

Markets

Australian non-bank financials reacted more positively than banks to the US election result, given more direct earnings leverage.

Effectively, the election helped solidify a 60-80bp move in bonds, which had yet to be reflected in share prices.

Among the banks, ANZ and CBA fared slightly better as they previously had more to lose from a fall in cash rates, given ANZ’s unhedged exposure to US institutional deposits and CBA’s very profitable domestic deposit book.

As a sector, banks could yet benefit from a rotation away from resources given disappointment on China stimulus, but reporting season was not particularly inspiring.

Bank reporting

Heading into results, the market was looking for upside on margins and/or the balance sheet, but neither came through.

Core margins were flat to down slightly, with guidance for similar outcomes given the ongoing mix shift in business deposits and emerging mortgage competition.

Credit quality deteriorated, most notably for NAB, where provisions are now being released to offset problem loans instead of being released to profits, as was hoped.

Capital initiatives were piecemeal, with sizeable buybacks appearing a 50/50 proposition given stretched payout ratios and the limit now being reached on optimisation initiatives.

Overall, there was nothing untoward, but no bottom-up catalysts for further sector outperformance.

About Graeme Petroni and Pendal Focus Australian Share Fund

Graeme is an analyst with Pendal’s Australian equities team. He has more than 20 years of experience covering the banking, insurance and diversified financials sectors. Graeme is a CFA Charterholder and holds bachelor’s degrees in Commerce and Law from the University of Sydney.

Pendal Focus Australian Share Fund is Crispin Murray’s flagship Aussie equities strategy. It is a high-conviction equity fund with a 16-year track record of strong performance in a range of market conditions. The Fund features our highest conviction ideas and drives alpha from stock insight over style or thematic exposures.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Near-zero interest rates have depressed returns in financial services for years. But with further rate cuts unlikely, it might be time to revisit the sector, says Pendal’s Graeme Petroni.

- Outlook for rates poses challenges for investors

- Financials one of the few sectors that can benefit from higher rates

- 10 to 40 per cent earnings upside for every 100-basis point rate rise

THE financial services sector is an important driver of overall stock market returns in Australia, making up nearly a third of the entire market’s capitalisation.

While the past few months have seen a return to favour for the big banks and other financials, it comes after five years of lacklustre share market returns.

“The biggest macro driver of returns has been interest rates,” says Petroni, who covers the financial services sector for Pendal’s Australian equities team.

“But we’re at an interesting juncture where interest rates have fallen to zero.

“It probably can’t get any worse. And that brings scope for significant share price recovery across the sector.”

Impact of rates on financials

Financial services react differently than most companies to higher interest rates, which make borrowing more expensive and slow business activity.

Higher rates allow many of the financial companies to earn increased interest income on their cash holdings. Banks can also benefit directly as they rebuild margins compressed by low lending and deposit rates.

“Financials across the board will perform well in a rising interest rate environment,” says Petroni.

Leverage to rising interest rates can be anywhere from 10 to 40 per cent earnings upside for every 100 points of rate rises, he says.

Portfolio strategy

But building a portfolio that can benefit from rising rates is not simply a matter of buying the whole sector. Each company is affected differently and each has its own idiosyncrasies.

Petroni says the three ASX companies most exposed to a rising rate environment are insurer QBE, British bank-holding company Virgin Money UK and stock market registrar Computershare.

Pendal Focus Australian Share Fund

Now rated at the highest level by Lonsec, Morningstar and Zenith

Insurers benefit from rising rates because of the government bond investments they hold to back their commitments to policyholders. Typically, fixed income makes up more than 75 per cent of an insurer’s portfolio, he says.

For QBE, the yield on its portfolio is now below 1 per cent — the lowest on record — meaning a 100 basis point lift in interest rates could flow through to a 15 to 20 per cent lift in QBE’s earnings.

Virgin Money UK — formed when National Australia Bank spun off its British bank businesses — is another positioned to gain from rising rates.

Bank earnings suffer from near zero interest rates because the difference between what they can charge for loans and what they have to pay on deposit accounts gets squeezed.

Computershare — which administers shareholdings for listed companies — benefits from higher rates because it invests money that it holds temporarily while distributing dividends. A 100-basis point rise in rates could lift Computershare earnings by 15 per cent.

Risks to consider

There are risks. Looming inflation is a problem for insurers because they set aside reserves based on projections of future payouts. Inflation can drive these higher.

Computershare’s clients are unlikely to allow higher interest rate earnings to flow to the bottom line without demanding their share.

And strong competition for market share among banks often eats away margin gains from higher rates.

“There are a wide range of companies in the financial services sector and they each have their own individual issues,” says Petroni.

“But they all have had a large exposure to falling interest rates — and that has been the dominant reason why they have underperformed.”

And his number one pick?

“The one that we like the most is QBE,” he says.

“The reason being is it is not just an interest rate story — it’s also benefiting from strong price rises. In the last result, the interim CEO said market conditions were better than they’ve experienced in more than a decade. Pretty strong words.”

About Graeme Petroni and Pendal Focus Australian Share Fund

Graeme is an analyst with Pendal’s Australian equities team. He has more than 20 years of experience covering the banking, insurance and diversified financials sectors. Graeme is a CFA Charterholder and holds bachelor’s degrees in Commerce and Law from the University of Sydney.

Pendal Focus Australian Share Fund is Crispin Murray’s flagship Aussie equities strategy. It is a high-conviction equity fund with a 16-year track record of strong performance in a range of market conditions. The Fund features our highest conviction ideas and drives alpha from stock insight over style or thematic exposures.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Significant features: The Fund is an actively managed portfolio of fixed interest securities. It is designed for investors who want income and diversification across a broad range of fixed interest securities and are prepared to accept some variability of returns. The Fund invests primarily in Australian dollar denominated investment grade fixed interest securities, including government securities, semi-government securities, supranational securities and credit securities and holds cash.

Investments are selected based on a range of financial, sustainable and ethical characteristics The Fund aims to allocate capital to issuers and securities that align to our sustainability themes: climate stability, human basics and innovation for good (the Sustainability Objective).

The Fund invests in securities issued by issuers that have passed Pendal’s sustainability assessment. Our sustainability assessment process is a qualitative assessment conducted at a security and issuer level. It seeks to identify issuers that, in our view, have strong sustainability credential for investment and aims to avoid issuers that we consider to have poor sustainability outcomes.

Fund Objective: The Fund aims to provide a return (before fees, costs and taxes) that exceeds the Bloomberg AusBond Composite 0+ Yr Index by 0.75% p.a. over rolling 3 year periods.

What can investors do when bonds stop performing how they’re supposed to in portfolios? Pendal’s Vimal Gor has been thinking about this – and has some answers

- Use tested strategies to achieve diversification and yield

- Alternative duration is a new way of thinking about asset allocation

- Find out more about Pendal’s fixed interest strategies

What can investment managers do when key attributes of bond investing — yield, diversification from equities — are low, asks Pendal’s Vimal Gor.

“You take market factors that already exist … and build a new asset allocation process around them,” says Vimal, who has pioneered “alternative duration” investing in Australia for several years.

The idea is to identify factors in different trading environments — such as momentum, volatility, skew (which involves the implied volatility of options) — and use a strategy that takes advantages of these factors to achieve desired outcomes.

“We think the uptake of this sort of alternative duration thinking is going to be very material in the next few years,” says Vimal, who recently began specialising in this space.

A five-person team, headed up by Vimal, is focused on bringing new thinking and new opportunities to income clients.

(Vimal was previously head of Pendal’s Income and Fixed Interest team — then known as Bond, Income and Defensive Strategies).

Investors can consider alternatives to the bond market to achieve the attributes they want in their portfolios, says Gor. That means thinking about alternative duration.

Duration in fixed income markets is a measure of the sensitivity of the price of a bond to changes in interest rates.

“Global government bonds have been in a long-term bull market for 30 years. Yields have fallen as nominal GDP and inflation has fallen.

Find out about

Pendal’s Income and Fixed Interest funds

“Ultimately, as global government bonds approach zero, the efficiency and effectiveness of fixed income as a diversifier to equities in a portfolio is dampened because they have less negative correlation to equities in a time of stress, and that’s one of the main reasons you want global bonds.

New way of thinking

Three years ago, Pendal embarked on a project to better understand how to achieve the attributes that global government bonds traditionally performed, including diversification.

“How do we approach the asset allocation problem when government bonds aren’t as useful as the used to be?”

Gor and his team’s approach was to rethink what the post-Covid economic and market environment was like.

“It’s a new way of thinking about asset allocation. We took market factors that already exist … and built a new asset allocation process around them.”

That meant identifying factors in different trading environments – momentum, volatility, skew (which involves the implied volatility of options) – and using a strategy that takes advantages of those factors to achieve desired outcomes.

“For example, intraday momentum is a systematic strategy that works very well in periods of drawdowns. Foreign exchange carry works very well in periods when equity markets are going up.

“By identifying these factors, and their risk-return characteristics, we are able to blend them in a portfolio to get a specific outcome.”

Traditionally, investors approach portfolio construction by blending assets to achieve a 60 per cent growth assets, 40 per cent defensive assets, for example. That mix determines what an investor’s profile is.

“We are coming at it from looking at what outcome profile would we like, and how do we get there by bolting together these factors which have very long track records. It’s a very different way of approaching asset allocation.

“We use strategies based on different factors in the multi-asset markets and apply and change them as we go through the cycle, depending on the environment.”

About Vimal Gor and Pendal’s Alternative Duration boutique investment team

Vimal Gor is Pendal’s Head of Alternative Duration.

Vimal’s new five-person team focuses on bringing new thinking and new opportunities to income clients.

Vimal was previously head of Pendal’s Income and Fixed Interest (I&FI) team (formerly known as Bond, Income and Defensive Strategies). Pendal I&FI is one of the most experienced and well-regarded fixed income teams in Australia. In 2020 the team won the Australian Fixed Interest category in the Zenith awards.

Find out more about Pendal’s fixed interest strategies here

About Pendal Group

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Significant Features: The Pendal Focus Australian Share Fund is an actively managed concentrated portfolio of Australian shares.

Fund Objective: The Fund aims to provide a return (before fees, costs and taxes) that significantly exceeds the S&P/ASX 300 (TR) Index over the medium to long term.

Here are the main factors driving the ASX this week according to portfolio manager Jim Taylor. Reported by portfolio specialist Chris Adams

RECENT trends persisted last week, although news flow was relatively quiet.

US and Australian 10-year government bond yields rose 15bps for the week, prompting further rotation from long-duration growth plays.

Commodity prices continued their climb. Brent crude oil rose 3.9% and copper 2.1%. There was some relief for iron ore, which gained 9.7% after recent plunges.

Gas and electricity prices continue to surge in the US, the EU and Asia. They are at record levels in the UK and EU, while volumes in storage are materially below historical averages. Moscow stepped in late last week, saying it was prepared to take steps to calm energy markets.

US payrolls data on Friday asked more questions than it answered in terms of the pace of tapering and rate rises.

The S&P/ASX 300 gained 1.86% and the S&P 500 0.83%.

Covid outlook

New case numbers continue to improve in US and most places around the world.

Singapore is an outlier, walking back some re-opening measures after a material resurgence in cases.

Severity of infection is proving far lower in vaccinated people. About 98% of recent Covid cases experienced either no symptoms — or only mild effects — in the 28 days before becoming positive.

Pfizer has asked the FDA to approve the vaccine for 5-to-11-year-olds. The FDA took about 30 days to approve the Pfizer vaccine for 12-to-15-year-olds.

Israel last week became the first country to effectively make vaccine boosters mandatory.

Pendal Focus Australian Share Fund

Now rated at the highest level by Lonsec, Morningstar and Zenith

Six months after a second vaccine dose, Israelis now require a third dose to retain a fully immunised “green pass” allowing entry into restaurants, gyms and other venues.

Over the past two months Israel has provided boosters to 39% of its population, significantly ahead of all other countries.

The case count there has been pushed down by 54% over the past two weeks. Health outcomes appear materially better than for those with just two doses.

Economics: US outlook

Friday’s US employment had been eagerly awaited for some read-through to Fed policy. But there was not enough clarity to read one way or the other.

There were expectations that September non-farm payrolls would see a material rebound given a reduction in unemployment benefits, the return to school after summer break and continued vaccinations.

But the headline came in weaker than expected with 194,000 jobs added versus consensus expectations of 500,000.

That said, the previous two months were revised up by 169,000 jobs. There was also a distortion from government jobs, which have been volatile and fell by 123,000.

Private payrolls were up 317,000 month-on-month. Hiring in tech-related service sectors remained strong. Leisure and hospitality was less buoyant (up 74,000) reflecting difficulties in recruitment.

The question is whether this meets the definition of “decent” economic momentum Powell flagged in September to keep tapering on track.

A key point of debate remains around the extent to which displaced workers are retiring or re-training rather than returning to old jobs.

Earlier explanations for lack of labour — such as the effect of benefits or the summer break — seem to be falling by the wayside.

The jobless rate fell to 4.76%, down from 5.2%. The modest pace of hiring will be enough to push the US towards full employment, since the labour force participation rate for prime-aged workers fell.

Average hourly earnings rose 0.62% month-on-month, ahead of a 0.4% expectation. The means the question of the Fed needing to tighten sooner rather than later remains live, although a mix shift of more growth in lower-paid hospitality jobs may see wage growth ease going forward.

Economics: Australia and New Zealand

The RBA left policy settings unchanged, as expected, including the cash rate target, the 2024 yield target and the pace of Quantitative Easing purchases.

The RBA maintained its positive medium-term view while noting ongoing disruptions from lockdowns in Sydney and Melbourne.

Pendal Focus Australian Share Fund

A high-conviction equity fund with 16 years of strong performance in a range of market conditions

The RBNZ lifted its official cash rate by 25bp to 0.5%, also in line with expectations. It maintained a moderate, hawkish bias, noting that “further removal of monetary policy stimulus is expected over time”.

APRA announced an increase in the minimum serviceability buffer of 0.5% (from 2.5% to 3%) The market had generally expected APRA would wait until early 2022. Clearly regulators appear more concerned about risks in the housing market than anticipated.

The message is that while banks are “well capitalised and lending standards have generally remained sound”, action is being taken to offset the “heightened risks for the financial system from lending at very high levels of indebtedness”.

Basically regulators are worried about households taking on too much debt relative to incomes at a time of record low rates. The increase in serviceability buffers will be effective from the end October.

Elsewhere, business surveys and consumer sentiment survey results have fallen as a result of lockdowns, but importantly they remain high compared to pre-Covid levels.

Markets

Bond yields rose materially last week. Commodity prices also rose which, in combination, underpinned a continued rotation away from growth.

A rebound in iron ore provided some much-needed respite for the major miners.

Energy (+4.49%) and Financials (+3.27%) did best, while Health Care (-0.26%) and Technology (+0.25%) lagged.

Worley (WOR, +9.8%), AGL (+7.9%), Woodside (WPL, +6.7%), Origin (ORG, +6.5%), Santos (STO, +6.0%) and Oil Search (OSH, +5.37%) all had a strong week as energy prices continued to climb. The oil price benefited from news that the US are unlikely to tap strategic fuel reserves.

Higher bond yields supported the financials, particularly QBE (QBE, +8.1%), IAG (IAG, +6.8%) and Challenger (CGF, +5.4%).

Insurers had good news with a federal court ruling that was largely in their favour in the second test case for Business Interruption (BI) related claims from Covid.

The outcome was seen as more commercial-friendly then consumer-friendly, which differs from many judgements globally. An appeal is set down for November 21 with further clarity expected on December 21.

About Jim Taylor and Pendal Focus Australian Share Fund

Drawing on more than 25 years of experience investing in top-performing Australian companies and a background in accounting, Jim manages our Long/ Short Fund and co-manages our Imputation Fund. He is a Chartered Accountant with membership of the Australian Institute of Chartered Accountants.

Pendal Focus Australian Share Fund has beaten its benchmark in 12 years of its 16-year history (after fees), across a range of market conditions. Find out more about Pendal Focus Australian Share Fund here

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

As Australia embarks on take two of the post-covid re-opening sequence, focus is turning to reducing risk in our overheated housing market. ANNA HONG explains

IN A MOVE that surprised no one, Australia’s financial system regulator APRA took steps to cool the housing market on Wednesday.

The decision to tackle house prices with macro-prudential instead of monetary tools reflects the reality that we are still in a tentative economic situation despite rocketing house prices.

This week Australia edged towards take two of the post-covid, re-opening sequence.

NSW firmed up its re-opening date of October 11. Victoria pushed forward with a roadmap out of lockdown despite rising case numbers.

We are opening up just in time to face global supply chain issues that are already creating havoc — and may worsen with potential delivery strikes.

Against this backdrop of uncertainty, RBA governor Phil Lowe reiterated the central bank’s dovish stance earlier in the week.

His main objective was to reduce unemployment and boost wages and prices.

That leaves APRA with the heavy lifting on cooling the housing market.

Property obsession

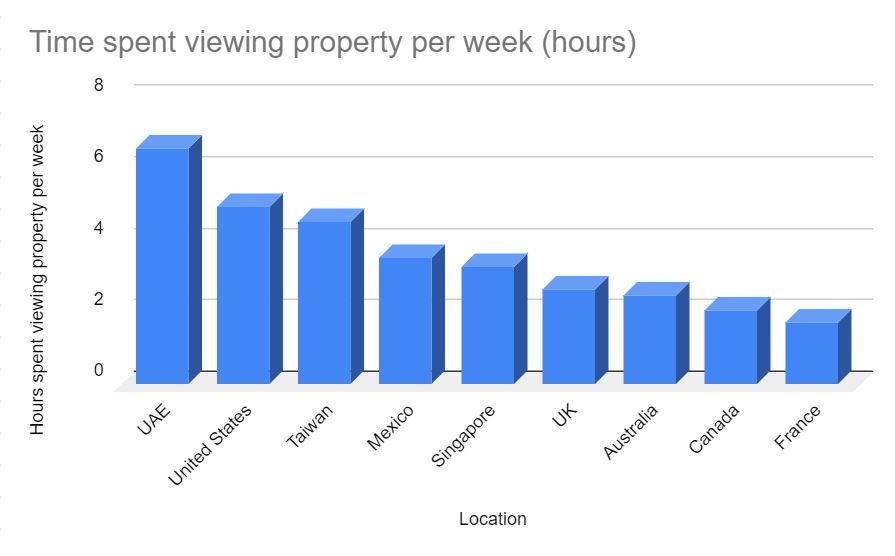

Australia’s obsession with property certainly isn’t new.

We spend an average of 2.5 hours a week researching property — even when we’re not in the market, according to HSBC data from 2019:

That’s twice the time spent at the gym (1.08 hours) and three times as much as we talk to our parents (0.88 hours).

Under such benign housing credit conditions — low rates, greater certainty on repayments with the fixing of rates thanks to the Term Funding Facility, lockdowns coupled with income from JobKeeper — it’s not surprising that we’re ploughing money into property.

On Wednesday APRA sent a letter to the banks, instructing them to increase the minimum interest rate buffer applied to new home loan applications.

The serviceability buffer will increase from 2.5 per cent to 3 per cent.

“While the banking system is well capitalised and lending standards overall have held up, increases in the share of heavily indebted borrowers, and leverage in the household sector more broadly, mean that medium-term risks to financial stability are building,” said APRA chairman Wayne Byres.

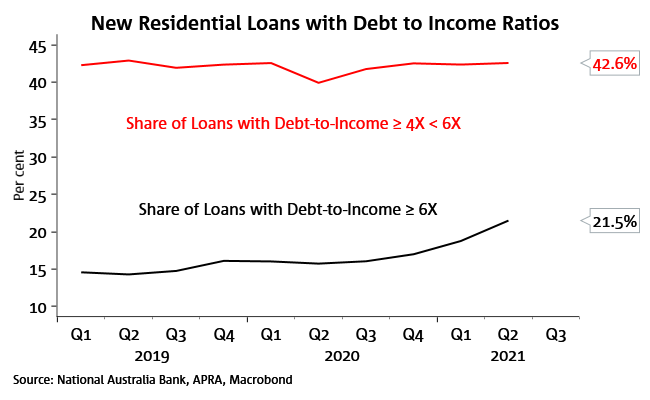

APRA wants to reduce maximum borrowing capacity, since a fifth of new loans now have more than a 6:1 ratio of debt-to-income, as this NAB chart shows:

The implications

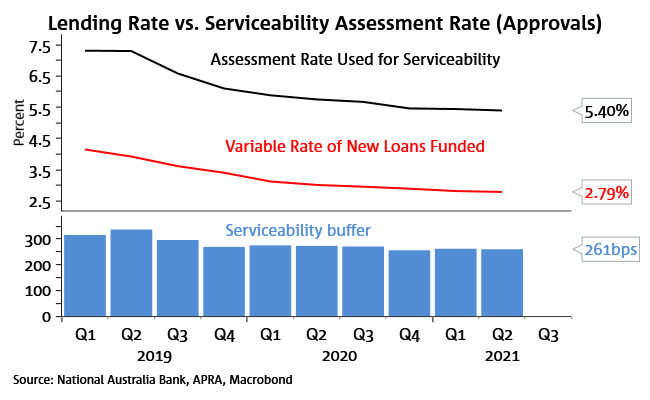

This increase in serviceability buffer reduces the borrowing capacity of borrowers by 5 to 6 per cent, again shown in this NAB chart:

Only time will tell if the latest measures put a dent in the housing market.

History has shown these may be mere bumps in the road instead of a large-scale correction.

But it’s just the first shot across the bow from APRA.

About Anna Hong and Pendal’s Income and Fixed Interest team

Anna Hong is an assistant portfolio manager with Pendal’s Income and Fixed Interest team.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia. In 2020 the team won the Australian Fixed Interest category in the Zenith awards.

With the goal of building the most defensive line of funds in Australia, the team oversees A$22 billion invested across income, composite, pure alpha, global and Australian government strategies.

Find out more about Pendal’s fixed interest strategies here

About Pendal Group

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.