What does the new monthly CPI indicator mean for investors? Pendal’s TIM HEXT explains

STARTING in October, Australian investors will finally get a monthly snapshot of inflation data.

This is very welcome news to all, particularly the RBA which relies on data to set policy.

The new monthly CPI indicator has a number of shortcomings, which will likely be addressed over the next few years by more budget or better technology.

Some basic facts are:

- Only 43% of the basket is updated live every month. These are items where electronic data points are easily collected such as supermarkets, airlines, rents and home construction costs

- 10% are administrative prices that reset annually – so they are effectively accounted for every month, eg education in February, private health insurance in April and council rates in September.

- The remaining 47% are collected quarterly – but not all in the same month of the quarter. That is, they’re spread across the three months of a quarter. I presume this is a resourcing issue since collection is harder.

Find out about

Pendal’s Income and Fixed Interest funds

The latter point will make predicting monthly numbers difficult at first.

At Pendal we’re now building out our models to help predict monthly movements, given markets will respond.

For example, utility costs are going up sharply. But they will only be collected in the final month of the quarter – and so will impact at the same time as quarterly numbers.

Restaurant meals though – another inflation pinch point – will appear in the monthly number prior to the quarterly number.

On average, two thirds of the CPI basket is effectively now monthly.

This helps make an already lagging indicator lag less.

It causes issues when the RBA bases policy on data that’s an average three months behind. This was shown late last year when the official quarterly CPI numbers were slow to pick up the rising monthly inflation.

Inflation bonds will continue to index off the quarterly CPI, which is still the ultimate source of truth.

Inflation bonds remain very cheap and despite a likely tailing off in goods inflation in the months ahead.

Services inflation will remain stubbornly higher in the medium term, whether measured monthly or quarterly.

Adviser Sam is invested

in making our world

A better place.

Watch as Sam meets a

mum rebuilding her life

thanks to responsible

investing

About Tim Hext and Pendal’s Income & Fixed Interest boutique

Tim Hext is a Pendal portfolio manager and head of government bond strategies in our Income and Fixed Interest team.

Tim has extensive experience in banking, financial markets and funding including senior positions with NSW Treasury Corporation (TCorp), Westpac Treasury, Commonwealth Bank of Australia, Deutsche Bank, Bain & Co and Swiss Bank Corporation.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia.

Find out more about Pendal’s fixed interest strategies here

About Pendal

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

In 2023, Pendal became part of Perpetual Limited (ASX:PPT), bringing together two of Australia’s most respected active asset management brands to create a global leader in multi-boutique asset management with autonomous, world-class investment capabilities and a growing leadership position in ESG.

In October Australia will move from quarterly to monthly reporting of inflation data. Pendal assistant portfolio manager ANNA HONG explains what that means

AUSTRALIA moves to monthly Consumer Price Index releases in October, bringing us in line with other major developed economies.

The decision, announced by the Australian Bureau of Statistics on Tuesday, heralds a new era for investors.

Why is up-to-date inflation data important?

Price stability is crucial in the allocation of resources.

Prices are economic signals. Large fluctuations change the expectations of businesses and individuals, leading to potential misallocation of resources.

Price stability is therefore one of the core objectives of central banks around the world.

It’s also why most central banks are now taking the full-throttle approach with rate hikes – they want to rein in inflation.

Because the CPI influences monetary policies, financial markets use it as a bellwether for the direction of monetary policy actions.

In 2022 this has led to markets swinging between fears of runaway inflation and fears of recession.

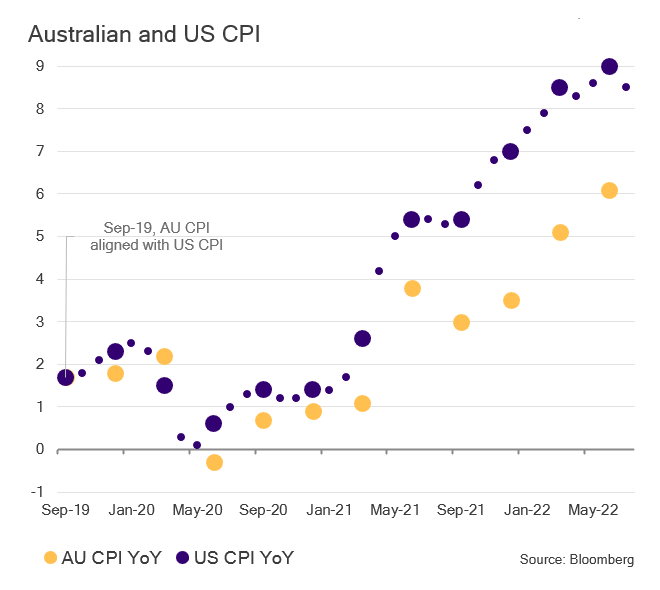

In Australia CPI data is traditionally released quarterly, compared to the US where it is monthly.

Hence, in between quarterly AU CPI releases, financial markets have largely looked to the US CPI numbers as a guide.

Problems arise because the direction of US CPI numbers does not always align with the AU CPI outlook.

This move to fill the calendar gap with timelier AU CPI data will help the RBA with policy decisions and give the markets better direction.

What are the changes?

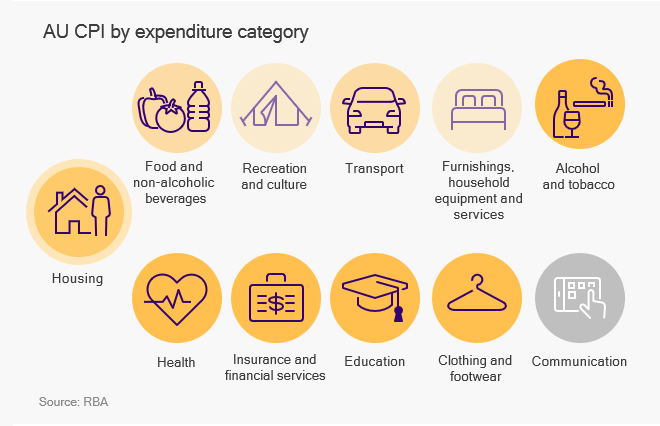

Same: The new monthly CPI will include all items within the quarterly CPI basket. The weights on each of the categories for the monthly CPI will also align with the quarterly CPI.

Different: Due to the complexities and timing of collecting and collating data, not every item in the CPI basket will be updated every month.

Prices will be carried forward for items without newly collected information — assuming zero change from the last period when the fresh price was collected.

Will it be useful?

There will still be gaps between monthly and quarterly releases.

But the monthly data has been designed to capture the bulk of information within the quarterly data.

Every category of prices will see an update in the monthly releases apart from Communication.

Non-volatile goods prices such as Alcohol and Tobacco and Housing will be fully or mostly accounted for.

Categories with items that experience more volatile price changes – such as Recreation and Culture – will be representative. Though not all series within those categories will get a price refresh in the monthly updates.

What it means for investors

ABS mapping of historical data shows the monthly release will closely track the quarterly.

That is positive news.

This will be a tailwind helping the RBA achieve a soft-landing by providing policymakers with the information needed to identify key inflection points before over-correcting with rate hikes.

It will also give markets better information on potential policy decisions, reducing the need to second-guess the Reserve Bank as demonstrated by aggressive pre-emptive selloffs between Q3 2021 and Q2 2022.

Those circumstances will be supportive of bonds at current levels, allowing them to perform as an income-generating, defensive asset in a balanced portfolio.

Find out about

Pendal’s Income and Fixed Interest funds

About Anna Hong and Pendal’s Income and Fixed Interest team

Anna Hong is an assistant portfolio manager with Pendal’s Income and Fixed Interest team.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia. In 2020 the team won the Australian Fixed Interest category in the Zenith awards.

With the goal of building the most defensive line of funds in Australia, the team oversees A$22 billion invested across income, composite, pure alpha, global and Australian government strategies.

Find out more about Pendal’s fixed interest strategies here

About Pendal Group

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Here are the main factors driving the ASX this week according to our head of equities Crispin Murray. Reported by portfolio specialist Chris Adams.

Find out about Crispin’s Pendal Focus Australian Share Fund

Find out about Crispin’s sustainable Pendal Horizon Fund

THE reluctant rally continues with the S&P 500 up 3.3% last week and the S&P/ASX 300 gaining 1.4%. They are now down 9.3% and 3.7% respectively for 2022.

The US market is now up more than 15% from its low and the rally has lasted 32 days.

Key drivers include:

- Positioning: Systematic and institutional investors have been sitting on their biggest equity underweights in years.

- Lower volatility: This leads to increased participation by systematic investors

- Better sentiment: Job data has helped quell the view that the economy is facing imminent recession.

- Strong US earnings season: Hasn’t validated the pre-season market de-rating

- Lower commodity prices: Particularly in US gas which is helping dampened inflation expectations

- Early signs of goods inflation slowing as supply chains free up

A small shift in fundamental view — that things are not as bad as feared — has prompted a material shift into equities by various systematic approaches. This caught institutional investors off-guard.

This is the nature of bear market rallies — sharp and often short. We now find ourselves at a key point.

In the short term we’re likely to have a quiet couple of weeks ahead of the Jackson Hole central banking conference on August 25-27.

We suspect the market will be range-bound given it is high summer in the north, there are limited new data releases, we are near a large technical resistance level for the S&P 500 and it appears the sharp move in systematic investors has played out.

Beyond that there remains a wide distribution of outcomes:

- Inflation rolls over, the economy has a mild recession at worse, earnings declines are limited and the easing cycle starts at the back-end of 2023. In this scenario the market may consolidate, but ultimately moves higher.

- Inflation proves more persistent, driven by tight labour market and higher energy prices as the economy runs too hot and China re-opens. Central banks need to continue to tighten into the downturn and earnings decline more significantly, taking equities lower.

There is probably enough evidence to indicate the latter scenario does not take us to new lows.

The key to the call remains the main drivers of inflation: the job market (particularly job ads and wage pressures), corporate pricing power and commodity markets.

Economics and policy

US year-on-year CPI (8.5%) and PPI (9.8%) were lower than expected.

But one month does not create a trend — and there was enough in the data for both inflation bulls and bears to validate their outlooks.

Pendal Focus Australian Share Fund

Now rated at the highest level by Lonsec, Morningstar and Zenith

Core CPI (5.9%) was 0.3% month-on-month, a lot lower than recent months. But it is at 0.5% excluding the more idiosyncratic categories such as used cars and airline tickets.

Core goods inflation is falling away reasonably quickly. Energy represents 34% of current inflation and is heading down as petrol prices drop.

Forward indicators of inflation — including the Crude Non-farm Materials ex Energy PPI which is a directional indicator for the Finished Goods (ex-energy and food) PPI — are moving in the right direction.

Freight rates also continue to decline.

All this underpinned more positive sentiment in market last week.

But in the medium term, categories such as direct rent and owner’s equivalent rent become more important. While these have begun to decelerate, it is marginal at this point and is still running above 8%.

Unit labour costs also remain too high, while there is no sign of a turn in the Atlanta wage tracker.

This means the Fed has had to re-iterate its vigilance on inflation.

China

There is some hope that cumulative stimulus measures will begin to drive economic recovery, particularly as we head into Autumn when construction activity should pick up.

We are cautious on calling this too soon. Some key lead indicators remain negative, notably property stock performance.

Credit data continues to be weaker than expected, reflecting low demand given the zero-Covid policy.

Australia

The market continues to grind higher, helped last week by BHP’s (BHP) bid for OzMinerals (OZL) which fired up the resource sector.

Adviser Sam is invested

in making our world

A better place.

Watch as Sam meets a

mum rebuilding her life

thanks to responsible

investing

Small caps also continue their recovery, outperforming the S&P/ASX 300 by 8% QTD. This is helped by a combination of short covering and a position squeeze.

There is an emerging view that the government and RBA are looking to deliver a soft landing by allowing inflation to run a bit hotter than normal — on the premise that commodity prices should stop rising, and immigration can ultimately resolve labour shortages.

In this context banks don’t face downside risk on bad debts and some of the consumer-exposed stocks may now be pricing in too much downside.

As in the US, this is contingent on commodity prices staying subdued and labour markets loosening.

Markets

It was interesting that US bond yields couldn’t break the 2.51% low of August 8 in response to the lower CPI number.

June’s hot CPI number coincided with the peak in bond yields (3.5% on June 14). Since then we’ve seen a 100bp move down, before a 33bp rise, closing the week at 2.83%.

Bonds could trade back towards 3% for several reasons:

- Economic data is surprising on the upside. The Fed is likely to be uncomfortable without further slowing, given inflation remains too high.

- The Total Financial Conditions index has begun to loosen, reflecting more confidence in the economy. This works against the Fed’s goals, which may lead them to signal rates stay higher for longer.

- Quantitative tightening beginning to kick in, which will potentially act as a headwind to lower yields.

- Yield curve inversion is implying too quick a reversal in US rates, particularly given economy and FCI trends

Given this, we do not expect to see bond yield moves lower — and they may move higher within a trading band.

This does not necessarily mean bad news for equities, but it makes further moves higher harder.

Given the moves seen so far we expect a period of consolidation coming soon.

About Crispin Murray and Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia. Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Consumers and business can only be out of step for so long — and 2023 will see a reckoning, writes Pendal’s head of government bond strategies TIM HEXT

WE ALL exist in the same economy — but you’d be forgiven for thinking otherwise.

This week we had new consumer and business sentiment data.

Early last year consumer confidence boomed as escaped from lockdowns with money in our pockets.

Sentiment hit an all-time high of 118 in the April 2021 Westpac-Melbourne Institute Consumer Confidence survey.

Now we have resumed our gloomy outlook. Weighed down by rising prices and rate hikes we’ve plunged to 81 — not far off the March 2020 low.

For business, however, it’s hardly looked better.

The NAB Business Survey sees business conditions at 20, not far off the April 2021 high of 30 (it averages around 5).

Business outlook, as measured by confidence, is a more modest 7, nearer the long-term averages.

Find out about

Pendal’s Income and Fixed Interest funds

What’s going on?

Clearly while we’re worrying about the future we’re still spending our pent-up savings.

Rate hikes of 1.75% to date have been manageable. But the next 1% this year will start to bite — heavily for some.

Tight supply of goods and services means businesses are able to pass on higher costs, maintaining margins and seeing conditions as strong.

Of course, consumers and business can only be out of step for so long — and 2023 will see a reckoning.

For now pessimists are winning the day as markets price in rates topping out early next year.

Growth will slow, but whether the landing is soft or hard is a guessing game that will be heavily debated.

Challenging times for everyone but particularly for central banks trying to bring down inflation without a recession.

However it does mean bonds are back — and their role as insurance in these highly uncertain times should not be underestimated.

About Tim Hext and Pendal’s Income & Fixed Interest boutique

Tim Hext is a Pendal portfolio manager and head of government bond strategies in our Income and Fixed Interest team.

Tim has extensive experience in banking, financial markets and funding including senior positions with NSW Treasury Corporation (TCorp), Westpac Treasury, Commonwealth Bank of Australia, Deutsche Bank, Bain & Co and Swiss Bank Corporation.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia.

Find out more about Pendal’s fixed interest strategies here

About Pendal

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

In 2023, Pendal became part of Perpetual Limited (ASX:PPT), bringing together two of Australia’s most respected active asset management brands to create a global leader in multi-boutique asset management with autonomous, world-class investment capabilities and a growing leadership position in ESG.

Here are the main factors driving the ASX this week according to our head of equities Crispin Murray. Reported by portfolio specialist Chris Adams.

Find out about Crispin’s Pendal Focus Australian Share Fund

Find out about Crispin’s sustainable Pendal Horizon Fund

JULY’S more positive tone was tested last week by a combination of:

- US Fed officials rolling back a perceived “pivot” signal from Chair Powell the previous week

- Strong US employment data (which is ironically poor news in the current environment)

- China-Taiwan tensions

The first two points saw bond yields gain 34bp at the short end and 18bp for 10-year Treasuries. The yield curve is now more negative than it was in 2007 and the US dollar has started rallying again.

Despite this, equities ground out small gains, led again by growth stocks.

The S&P 500 rose 0.4% and S&P/ASX 300 gained 1.1%.

This resilience is surprising. We suspect it has as much to do with the market’s previous negative positioning and sentiment as any fundamentals.

The recovery has prompted some breaks in the previous bearish consensus.

We have seen a highly rated US technical analyst turn positive on the premise that the oil price and bond yields have peaked.

Energy is critical to the outlook.

A bounce-back in the oil price would kick-start stagflation concerns; a continued fall would help drive bond yields lower.

Locally, the focus will shift to stock specifics as reporting season kicks off this week.

US economics

US payroll data and household survey came in well ahead of expectations.

Pendal Focus Australian Share Fund

Now rated at the highest level by Lonsec, Morningstar and Zenith

This suggests the job market remains strong despite weakening lead indicators, a technical “recession” signal and headlines about tech companies laying off workers:

- The US economy is averaging more than 400,000 new jobs a month over three and six months. The three-month average has fallen from 600,000 — though it needs to come down to 50,000-75,000 to be consistent with looser wage pressure.

- Total US payrolls are back to pre-pandemic levels, though leisure and hospitality roles are 7% lower. The overall unemployment rate is at its lowest since 1969.

- Three-month average wage growth (measured by average hourly earnings) has ticked up and remains stuck with a 5-handle. This needs to fall back to the 3% range to help inflation back to 2%.

- The participation rate was down month on month and remains stubbornly low versus pre-pandemic. Older workers are still showing reluctance to return to work.

There are early signs that the ratio of job openings to the number of unemployed is rolling over. But we have a long way to go to normalise and reduce pressure on wages.

These are all co-incident or lagging indicators.

It’s highly likely a weakening economy will start to flow into jobs in the next few months.

But the starting point is higher and the amount of slack needed is rising. This makes the Fed’s job harder.

Fed speak

Some outer members of the Fed worked this week to rectify the interpretation of Powell’s press conference, re-iterating the priority of fighting inflation.

Combined with the employment data this moved the short end of the yield curve in particular.

The market is back to pricing an implied 67bp rate hike for September.

The Fed’s initial plan is to slow growth below trend — which should loosen the job market, leading to lower wage growth and inflation.

Adviser Sam is invested

in making our world

A better place.

Watch as Sam meets a

mum rebuilding her life

thanks to responsible

investing

It’s important to remember that equity markets form part of the overall total financial conditions index, which has an impact on the pace of economic growth.

The Fed had shifted this sufficiently to be consistent with 1% GDP growth — in line with the aim of a soft landing.

However the reaction to Powell’s press conference last week meant total financial conditions were beginning to ease.

The Fed needed to check that move to keep conditions conducive to below-trend growth.

US Inflation Reduction Act

This US$430 billion bill — intended to fight climate change, lower drug prices and raise some corporate taxes — has been further amended and is now highly likely to be passed in next few weeks.

The most relevant component is an emphasis on clean-energy investments, including increased subsidies for electric vehicles.

This is tied to requirements that companies source components from countries with free-trade agreements with the US, to prevent reliance on China. This should be a boon for the Korean battery industry.

It remains to be seen whether the capacity to deliver this exists. But for the moment sentiment towards electric vehicles and battery materials has improved.

Bank of England

The UK highlights the policy conundrum that emerges as stagflation takes hold.

The Bank of England now predicts five quarters of recession with inflation peaking above 13% this year and remaining above 9% next year.

The need to quash inflation takes precedence, so the BOE raised rates 50bps despite predicting recession.

The UK is facing a crisis in power prices, which is not the case in the US or Australia.

This is a reminder that energy prices are a critical factor in determining where all markets go.

Taiwan

Markets remained relatively sanguine around the tensions attached to Speaker Nancy Pelosi’s visit to Taiwan.

The view among most geopolitical experts is that Beijing is not confident in the success of any invasion and will not yet start to impose a blockade — the likely first step.

Sustainable and

Responsible Investments

Fund Manager of the Year

That said, there is a widespread view among western military experts that neither Taiwan nor the US is sufficiently prepared for any cross-Strait attack.

This is quite different to the preparation that had been happening in Ukraine for the past few years.

Pelosi’s visit and the Chinese reaction may be a catalyst for action to rectify this — which may also trigger Beijing to act before those preparations are in place.

This remains the single biggest long-term geopolitical risk for markets.

Markets

The big debate is whether the market’s rebound is a bear market rally or whether we have put in the lows for this cycle.

At this point the rebound is almost bang on the average bear market rally (in terms of rebound and length) in the S&P 500 since 1950.

The market breadth of the rally is not yet consistent with a change in trend.

The rule of thumb is you need to see 90% of stocks above the 50-day moving average to signal a change in market direction. We are at 73%. However this could continue to climb.

The yield curve is also sending a negative signal.

Its inversion is signalling recession, which would lead to a decline in earnings and pull the markets lower.

The challenge to this perspective is the unusual speed and scale of the increases and the market’s current confidence that inflation will be brought back down, which is reflected in long bond yields.

The bull case for equity markets is:

- They have bounced off long-term technical support levels

- Oil prices have peaked, with demand weakening

- Bond yields have peaked, helped by lower commodity prices

The importance of oil

The positive case is underpinned by the view that oil prices won’t bounce back.

We see this as a potential negative surprise for markets. There are several reasons why oil could behave differently in this cycle:

- Inventories are low, despite tapping the US Strategic Petroleum Reserve (SPR). The latter probably has capacity for three more months of contributions to supply, with the run rate falling in that time.

- Spare capacity is very limited, as shown by OPEC increasing output by only 100,000 barrels per day for September. There is no buffer for demand recovery or for any geopolitical shock.

- Europe plans to tighten sanctions on Russian oil in December, which could limit access to 0.01 to 1.5m bpd

- China at some point will re-open its economy, increasing oil demand by 500K to 1m bpd

- Oil demand may surprise on the upside due to fuel oil. This is the first downturn where alternate fuel prices (notably gas and coal) are far higher than oil. This is likely to see some substitution to oil — not away from it as is normally the case. The US gas market has remained surprisingly tight despite the closure of the Freeport LNG export facility.

This may not play out for a few more months, given US SPR is still being released, China is set to run with zero covid for another few months and the global economy is slowing.

For time being the weaker oil/lower bond signal could remain in place, but it is something to watch.

Australia

The S&P/ASX 300 is now down only 4.1% in 2022. This followed a US rotation to tech, away from energy last week.

Defensive sectors such as staples continue to perform as cash is put into market reluctantly.

We continue to see a bounce-back in small-cap performance which appears correlated to market direction.

About Crispin Murray and Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia. Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Did this week’s RBA statement this week signal fewer rate hikes ahead? Probably not, says Pendal’s head of government bond strategies TIM HEXT

THE RBA statement this week played a reasonably straight bat.

Who can blame them given all the criticism and the upcoming review? They seem less keen to take on the market.

But it’s also reasonable in a highly uncertain and complex world that you maintain maximum flexibility.

Anyone with a strong opinion on the economy at the moment is likely displaying misplaced bravado.

What we do know is rates are going to hit neutral this year. Another 1% of hikes can be expected, moving the cash rate to 2.85%.

Whether it’s four lots of 25bp across four meetings or 50bp at fewer meetings is only of interest to short-end traders.

Hence the RBA’s line that “the Board expects to take further steps in the process of normalising monetary conditions over the months ahead, but it is not on a pre-set path”.

Sounds like an opportunity for everyone to interpret this with their own confirmation bias — which on Tuesday seemed to be fewer hikes, not more.

I think that’s reading too much into it.

Find out about

Pendal’s Income and Fixed Interest funds

Much like the US Fed, the RBA will be keeping a close eye on overall monetary conditions.

As asset owners we must remember the “central bank put” is now also a “central bank call”.

That is, if bonds, equities and credit spreads rally too much without a significant easing in inflation pressures, they will lean against the easing of conditions.

The rally of the past month suggests this is in danger of happening — so expect more hawkish speeches from officials, especially in the US.

RBA officials will have time over summer to sit back and see the impact of hikes on the economy.

I suspect the hikes will not have a big impact yet — but will do so next year.

This is when 30% of total mortgages come off 2% fixed rates onto 5%-plus floating rates.

However, while goods price inflation will be falling, services inflation will be becoming more embedded in the economy, courtesy of labour shortages.

This will limit any further rallies in bonds.

They are not expensive, but recent rallies mean they are no longer cheap.

Adviser Sam is invested

in making our world

A better place.

Watch as Sam meets a

mum rebuilding her life

thanks to responsible

investing

About Tim Hext and Pendal’s Income & Fixed Interest boutique

Tim Hext is a Pendal portfolio manager and head of government bond strategies in our Income and Fixed Interest team.

Tim has extensive experience in banking, financial markets and funding including senior positions with NSW Treasury Corporation (TCorp), Westpac Treasury, Commonwealth Bank of Australia, Deutsche Bank, Bain & Co and Swiss Bank Corporation.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia.

Find out more about Pendal’s fixed interest strategies here

About Pendal

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

In 2023, Pendal became part of Perpetual Limited (ASX:PPT), bringing together two of Australia’s most respected active asset management brands to create a global leader in multi-boutique asset management with autonomous, world-class investment capabilities and a growing leadership position in ESG.

A re-assessment of fixed income securities and yields — and their defensive qualities — have made bonds attractive again. Here’s a quick overview from Pendal’s head of client solutions DALE PEREIRA

AFTER a decade of strong returns, bond markets have been challenging for investors over the past year.

Returns have not been kind.

But in recent few months a re-assessment of fixed income securities and yields — and their defensive qualities — have made bonds attractive again.

Bond returns don’t predict future returns – they reflect what has happened. That’s where the opportunity lies: they may be showing negative returns now, but the future looks a lot brighter.

Why bond yields are up

Markets are forward-looking – prices reflect where the economy is heading.

Bonds typically lead equities in terms of market reaction.

From the end of 2021 and into the first half of 2022, bond yields moved in line with expectations of future rate rises – which in turn reflected inflation expectations.

But markets often over-react when extrapolating good and bad news. And that’s the case now.

The market has likely priced in too many rate rises. It’s priced in a good chance that central banks around the world won’t be able to control inflation. (Though recently that pricing has started to dissipate, making yields less volatile.)

This means the bond market is at a much better entry point for investors.

But aren’t central banks already lifting interest rates?

They are, but remember bonds are priced on expectations.

We’ve seen a big jump in yields because investors initially expected things could get out of control with supply-chain problems and higher prices.

Find out about

Pendal’s Income and Fixed Interest funds

There was plenty going on – Covid restrictions in China, the war in Ukraine, soaring oil prices and an energy crisis. It wasn’t long ago that people were talking about oil at $US200 a barrel.

Hence, central banks have acted aggressively.

In Australia we’ve seen consecutive 50-point rate hikes – the fastest rate-rise path in our history.

Other countries such as the US, UK, Canada and New Zealand have been even more aggressive.

Central banks understood their objective and acted to curtail inflation expectations. If they hadn’t, inflation expectations could quite easily have become reality.

What’s the prognosis for inflation?

In recent weeks there are early signs that inflationary pressures may be dissipating.

The flipside to reduced economic activity and price pressures is the prospect of a recession.

That’s an environment when bonds outperform.

Why bonds could be a good investment now

If inflation has peaked — and we’re now only expecting moderate inflation – that’s a good environment for bonds, since the starting point is a higher yield.

Coupon payments (and income) is higher. Plus there’s limited downside risk in terms of capital loss.

If we head into a recession, there’s a call option on bonds. That means the issuer can redeem the bond before its maturity date.

So the asset from which you are getting a coupon is at least in line with long-term inflation.

And it will appreciate in value if we do head into a recession.

What about corporate bonds?

Until recently, many corporate bond investment strategies were hit with a double whammy of interest rate risk and credit risk.

Adviser Sam is invested

in making our world

A better place.

Watch as Sam meets a

mum rebuilding her life

thanks to responsible

investing

Corporate bonds are more susceptible to an economic growth slow-down and potential recession. Investors may worry that companies won’t be able to repay their debt.

The market has anticipated this and re-priced corporate bonds.

The riskiest companies don’t have a strong balance sheet. They may be operating in an environment where margins are under pressure because costs are going up while sales are flat or falling.

But that’s the worst-case scenario.

In Australia there are many investment-grade corporates with strong balance sheets.

How to invest in the bond market now?

Investors should consider a “barbell” approach.

At one end of the barbell, consider buy high-quality government bonds for duration.

Australia looks like a good place to re-enter the market. If investors already hold government bonds, now is not the time to sell because that would lock in losses.

Look for actively managed portfolios, because opportunities depend on choosing the right maturities of a government bond.

For example 5-and-10-year bonds — which take into consideration medium-term impacts of inflation and growth — now present interesting opportunities that active managers can exploit.

At the other end of the barbell, investors should consider investment-grade bonds which represent quality companies with good cash flows.

In Australia the level of default in investment grade bonds is much lower than the US, because of our higher-quality balance sheets.

Investors can also look for floating rate investments issued by corporates.

This means investors are less impacted by rate rises. They get an increase in income every quarter as the cash rate rises.

Floating rates haven’t been a good investment in recent years as interest rates tended down.

But in this environment they can outperform term deposits since investors pick up extra accrual as rates rise.

Sustainable and

Responsible Investments

Fund Manager of the Year

Other opportunities can be found in the fast-growing impact or “use-of-proceeds” bonds, often known as green, social or sustainable bonds.

Strong tailwinds in climate, regulation and human behaviour change mean there is increasing demand for these types of bonds — and not enough issuance.

This dynamic is likely to continue.

Dedicated strategies can find strong returns along while aligning with client principles.

ESG (environment, social and governance) has a different meaning in bonds compared to equities. Capital can be ring-fenced for specific projects or uses and the main elements of credit risk and duration risk can be managed.

About Dale Pereira and Pendal’s Income & Fixed Interest boutique

Dale is Pendal’s head of client solutions. He works with investment managers and product teams to position our investment capabilities in the most effective and relevant way for clients across all channels.

Dale joined Pendal in 2011 as a portfolio specialist with responsibility for fixed interest and alternative strategies.

About Pendal’s Income & Fixed Interest team

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia. The team won Lonsec’s Active Fixed Income Fund of the Year award in 2021 and Zenith’s Australian Fixed Interest award in 2020.

Find out more about Pendal’s fixed interest strategies here

About Pendal Group

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Here are the main factors driving the ASX this week according to portfolio manager Jim Taylor. Reported by portfolio specialist Chris Adams

MARKETS took a glass-half-full view last week, despite data showing inflation was still running hotter than central banks would like.

This was in stark contrast to recent market action.

There were two reasons for this more positive stance:

First, the market interpreted Fed Chair Powell’s remarks after last week’s 0.75 percentage point rate rise as leaving the door open to a more moderate pace of tightening.

The reaction suggests the Fed may have restored a degree of credibility in the market’s eyes.

Second, comments from several big US companies during reporting season suggest that while the economic slowdown is real, it isn’t derailing corporate earnings at this stage.

The S&P 500 gained 4.3% last week, while the S&P/ASX 300 was up 2.3%. Commodity prices rallied, while US 10-year bond yields fell 38bps.

Australia

Last week’s inflation data was seen as enough to support today’s 50bp rate increase, but not sufficient to warrant the 75bp “shock and awe” move that many feared.

CPI inflation rose 1.8% in the June quarter — slightly less than the 1.9% consensus expectation and down on the 2.1% gain in Q1.

Annual CPI growth was 6.1%, up on the 5.5% of Q1 and the strongest growth since 1990.

Trimmed mean CPI — the RBA’s preferred measure — rose 1.5% over the quarter, in line with consensus. It is at 4.9% for the year versus 4.7% expected. This remains well above the RBA’s 2-3% target.

Price growth was broad-based with sharp rises in food, transport and housing costs.

Find out about

Pendal Focus

Australian Share Fund

Crispin Murray,

Head of Equities

US Fed

The Fed raised its target band by 75bps to 2.25-2.5%.

The decision was unanimous and returns rates to a range the Fed considers neutral — though some observers disagree.

The market wanted to hear there was some chance hikes get throttled back. People saw enough in the accompanying statement to deliver this hope.

Chair Powell flagged some softening in spending and production. But he pointed out that labour markets remain strong and inflation elevated.

The Fed would need to see growth and inflation slowing to ease the pace of hikes, he said. Hence the market’s positive reaction to the data print of negative GDP growth in Q2, slipping the US into technical recession.

That said, Powell reiterated that failure was not an option in achieving price stability.

He could not rule out another out-sized rate hike for September, depending on the data. He wanted to see “compelling evidence” of slowing inflation in the core Personal Consumption Expenditures price index.

Powell also noted the natural rate of unemployment was likely a lot higher today than prior to the pandemic. At 3.6% the labour market looks extremely tight — and hence a generator of primary inflation.

US GDP

The US economy contracted 0.9% in the June quarter after falling 1.6% in Q1 — signalling a recession.

But it does not feel like a recession, given strength in the jobs market and an unemployment rate of only 3.6% in the past four months. This remains a key factor to watch.

Unemployment benefit applications last week were the highest this year, which may signal a shift.

Consumer spending rose 1% annualised, down from 1.8% in the previous quarter.

The slowing pace of inventory restocking was a big draw-down on economic growth. Changing consumption patterns have left many retailers with excess stock that needs to be discounted and cleared.

Most economists have growth in the September quarter and for calendar 2022 — so the current contraction is not expected to continue.

US inflation

A few other data points indicate that inflation remains high.

The Employment Cost index rose faster than expected, up 1.3% for Q2 and 5% year-on-year.

However the market is seeing signs of near-term softening in labour markets and at this stage seems happy to look through this print.

The Core Personal Consumption Expenditure index (which excludes food and energy) rose 4.8% in June, up from 4.7% in May. Prices rose 0.6% in June, following several months of 0.3% increases. Consensus expected a 0.5% gain.

One positive is that US petrol prices have now fallen for more than 40 days straight.

Markets

Last week was strong across the board.

Every major equity index except Japan made gains, while commodities and bonds were both stronger.

It topped a strong month. The S&P 500 gained 9.2%, the NASDAQ lifted 12.4% and the S&P/ASX 300 moved ahead 6%.

US mega-cap stocks caught a strong bid, reflected in growth outperforming value.

So far 56% of US companies have reported Q2 results.

About 75% have delivered better than expected EPS results, versus an 81% average over the past year and 77% over five years.

Sustainable and

Responsible Investments

Fund Manager of the Year

Overall, earnings are on track to rise 6% — the slowest rate since the end of 2020.

Amazon delivered an unexpected loss for the quarter — though sales for the quarter were up 7% to US$121bn versus $119bn expected.

Management guided to $125-130bn of sales next quarter, versus $126bn consensus. Crucially, management indicated it was getting costs under control and productivity at fulfilment centres was improving.

Revenue grew 33% for Amazon Web Services and advertising was up 18%, continuing the theme that the stronger franchises are taking revenue from the weaker franchises. Amazon shares were up 29% in July — their best month since October 2009.

Intel shares tanked after missing quarterly profit and revenue expectations. Revenue fell 22% — the biggest drop in a decade. The chip-maker flagged weaker PC sales and poor execution on a rollout of a new generation of chips for data centres.

Microsoft’s 12% revenue growth fell short of expectations. However an upbeat outlook saved the day, with management expecting double-digit growth in sales and operating income for FY23.

Apple revenue rose 2%, driven by stronger-than-expected demand for iPhones. Sales rose 2% while the market was expecting a 3% fall. CEO Tim Cook said he was seeing pockets of softness but expected even stronger year-on-year revenue growth next quarter.

Google’s parent Alphabet reported sales up 13% on the previous comparable period. It was the slowest growth in two years as advertising decelerated in many areas. Net income was down 14%. The company has slowed down hiring plans.

Meta (previously Facebook) reported a decline in revenue versus the previous comparable period for the first time and a third sequential fall in operating profits. Ad revenue declined 18% and pricing fell after recent strong gains. Meta also flagged slower hiring.

Shopify’s stock fell 14% after cutting 10% of its global staff in response to the reversal of sales back to physical retail.

Australia

In Australia materials (+5%) led the market higher as miners dominated the leader board, led by the lithium and EV-related names.

Real estate (+3.9%) was also strong.

Health care (-0.8%) lagged, as did consumer discretionary (-0.3%).

About Jim Taylor and Pendal Focus Australian Share Fund

Drawing on more than 25 years of experience investing in top-performing Australian companies and a background in accounting, Jim manages our Long/Short Fund and co-manages our Imputation Fund. He is a Chartered Accountant with membership of the Australian Institute of Chartered Accountants.

Pendal Focus Australian Share Fund is managed by Crispin Murray. The fund has beaten its benchmark in 14 years of its 18-year history (after fees), across a range of market conditions. Find out more about Pendal Focus Australian Share Fund here.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Here are the main factors driving the ASX this week according to our head of equities Crispin Murray. Reported by portfolio specialist Chris Adams.

Find out about Crispin’s Pendal Focus Australian Share Fund

Find out about Crispin’s sustainable Pendal Horizon Fund

THE market is seeing signs of inflation easing, the economy slowing and policy having an effect.

As a result, concerns over the extreme tail risk of substantial central bank overtightening may be receding.

It remains a challenging environment. The key questions around where inflation settles, the path of rate hikes and the economic impact are still unanswered.

Energy remains a wildcard. But at this point there is a reduced probability of some of the most negative projected scenarios.

The market bounce continued last week.

The S&P 500 gained 2.6% and the S&P/ASX 300 3.6%. This was despite more bad news on economic growth and the European Central Bank (ECB) striking a more aggressive stance than expected with a 50bp rate hike.

At this point bad news is seen as good news. Weaker growth is seen as helping drive inflation lower, bringing forward an expected peak in rates and bond yields.

US 10-year government bond yields are now 66bps lower than the June high, which is helping support the equity market. The S&P 500 is up about 8% from its lows. We are also seeing a rotation back to longer-duration sectors.

Oil prices, bond yields and the US dollar all remain tightly correlated and a key driver of markets. Recent falls in yields and oil and a pause in US dollar gains are all helpful for equities.

Early US corporate earnings signals are supportive. It was interesting to see Netflix bounce about 25 per cent despite weaker subscription numbers.

Where to next for markets?

It is too early to call whether we have seen a bottom or if this is another bear market rally.

Pendal Focus Australian Share Fund

Now rated at the highest level by Lonsec, Morningstar and Zenith

Technical measures of market breadth and volumes are not indicating a sustainable turn in sentiment.

Seasonally, August and September are typically soft months for equities.

That said, a market moving higher on bad news suggests some stale positioning and the squeeze could continue.

Bear markets don’t tend to end until policy direction shifts. It would also be unusual to see markets bottom before the extent of any earnings recession is known.

The challenge is that bear market rallies and squeezes can be large.

The average NASDAQ bear market rally since 1985 has been 30% — and the NASDAQ is only up 11% from its recent low.

The S&P/ASX 300 is now down 7.2% for the year to date. Technology is off 27%, consumer discretionary is down 17.6% and REITs has lost 16.8%. This leaves plenty of scope for these sectors to squeeze higher during reporting season.

This week will bring a lot of new information including a Fed meeting, the US Q2 GDP print and a raft of US earnings results.

Macro and policy outlook

Europe

The ECB raised rates 50bps — the first hike in 11 years — in response to a worse-than-expected inflation print of 8.6% year-on-year. The market was not expecting such a big move, only ascribing a 25% chance.

Adviser Sam is invested

in making our world

A better place.

Watch as Sam meets a

mum rebuilding her life

thanks to responsible

investing

The market’s reaction was positive.

This could be partly because the ECB stated there was no change to the ultimate expected terminal rate. There was also likely some relief that the bank was catching up to the reality of dealing with inflation.

Given the likely slump in the European economy, there is a view the ECB has only a small window politically to raise rates — and therefore they are better to front load.

The ECB also provided the latest “tool” to manage the “fragmentation” risk of bond spreads blowing out in the periphery and creating the next Euro crisis.

The Transmission Protection Instrument (TPI) represents a form of Quantitative Easing in an era of rate tightening and Quantitative Tightening. The purpose is to prevent the upcoming recession from putting pressure on the Euro.

It is said to have no budget limit on the purchases or periphery bonds (refers to being “proportionate”) or any need to negotiate some economic reform package.

There is no stated threshold for use, which will be determined by the European Council. It will also likely relate to circumstances beyond the country’s control, so the current Italian political crisis is unlikely to trigger its use.

As with most European tools, this is deliberately vague. We suspect the market will want to test this at some point.

United States

It is almost unanimously expected that the Federal Reserve will hike rates 75bps this week. Speculation about a 100bp hike has dwindled along with the latest inflation expectations data.

The Fed is maintaining a hawkish tone.

We suspect they would rather wait for more firm evidence of slowing inflation over next two months – remembering they do not meet in August – than ease up too early and risk another embarrassing U-turn.

The curve of expected future policy rates shifted down 15bps last week. It now has rates peaking at the end of 2022, rather than the previous end of Q1 2023.

Sustainable and

Responsible Investments

Fund Manager of the Year

This is a big shift from where we were a month ago. It is likely the economy will need to be a lot weaker for this to happen.

Elsewhere there were limited data releases last week.

Regional Fed manufacturing indices were soft. But the Flash US Manufacturing PMI was better than expected at 52.3 vs 52.7 in June.

Interestingly the Services PMI was weak at 47 vs 52.7 in June, with the pricing component notably lower.

Overall, it painted a constructive picture of inflation easing.

Energy markets

Gas resumed flowing through the Nordstream pipeline from Russia to Europe after maintenance, calming some fears.

It is running at 40% capacity. This enables Germany to build enough reserves for winter – but only just. It remains vulnerable to any change in the Russian approach.

We now have the perverse situation where the West has imposed sanctions to constrain Russia’s ability to sell oil, but is desperately hoping Moscow keeps supplying gas.

Germany suffered the ignominy of asking the rest of Europe to reduce gas consumption 15%. Greece and Spain refused. The latter drew on Germany’s own Euro crisis era rhetoric noting that “unlike other countries, we haven’t been living above our means in terms of energy”.

Oil and gas will be key to determining whether sentiment around inflation continues to improve.

The growing consensus is that weak global growth will see oil prices fall below US$90, relieving pressure on headline inflation and consumer inflationary expectations.

This would allow softer Fed rhetoric perhaps as early as September.

The alternate view is that supply constraints, an end to strategic petroleum reserve (SPR) releases and Chinese re-opening could drive energy prices higher even as the global economy slows.

This would leave central banks facing an impossible choice.

China

Chinese equities have rallied since May on the easing of Covid restrictions.

However sentiment has turned more negative.

This is partly driven by the mortgage strike in relation to unfinished homes and also by the lack of any meaningful stimulus. Measures enacted recently really only serve to offset the negative impact from housing weakness.

At this point, it appears growth with be sluggish for the next few months. It is hard to see China as a big driver of any improvement in sentiment towards global growth in the near term.

The US dollar continues to drag the Chinese Yuan (CNY) higher, affecting its ability to compete with Korea and Japan. There is a risk we may see another step down in the CNY, which would likely be negative for commodities.

Australian market

Last week’s broad ASX rally was led by tech (+7.3%), financials (+4.5%) and small caps (+5.8%).

Small cap resources had a good bounce (+6.9%) after a sharp fall in recent weeks (about -33% since April).

This is symptomatic of being oversold and the market chasing beta into the bounce, rather than a shift in fundamentals.

We are seeing small signs of rotation from consumer defensives to discretionary. This was helped by an upgrade from JB Hi-Fi (JBH, +10.1%).

This will be something to watch in reporting season. We note Nine Entertainment (NEC) as a good example of stock that has been heavily de-rated without any sign of earnings softening.

About Crispin Murray and Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia. Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Bonds are back. Here Pendal’s head of income strategies AMY XIE PATRICK explains why

- Ten-year bond rates close to 4 per cent

- Benchmark returns for other asset classes higher

- Negative correlation between bonds and risk assets has re-emerged

INVESTORS have struggled to earn good returns from fixed income assets in recent years.

But yields on government bonds have risen over the past year — and the negative correlation between bonds and risk assets has re-emerged.

That reflects the narrative around a recession in the United States, Europe and possibly even Australia, says Pendal’s head of income strategies Amy Xie Patrick.

“The bond story of recent years has been flipped on its head,” says Xie Patrick.

“Buying 10-year government bonds in Australia can get you nearly 4 per cent. At the height of the pandemic, it was 50 basis points.

“Now the credit risk-free rate is 4 per cent, which raises the bar for other asset classes.”

Those other assets might be riskier fixed income instruments including junk bonds and private sector debt, or other asset classes such as equities and alternatives.

When government bonds yields have risen so much, so quickly, the economics of all other investments change.

“You can get credit-risk free, 10-year yields in Australia for 10 per cent. That sounds pretty good,” Xie Patrick says.

Investors should consider buying high-quality sovereigns, such as United States or Australian bonds, which are free from credit risk, says Xie Patrick.

Find out about

Pendal’s Income and Fixed Interest funds

Changing attitude to bonds

Investors have been hesitant to include bonds in portfolios in recent years — but that’s changing, says Xie Patrick.

“For the last three years equity yields were much higher than bond yields. Investors were better off sitting in equities and collecting the dividend.”

But fears of a recession have changed all that. Xie Patrick points out that it isn’t central banks around the world that will trigger a recession. Rather, it’s tumbling consumer sentiment that reflects inflation.

“You’re filling up your petrol tank and the cost at the bowser just keeps going up. Grocery bills are so much higher and feeding a family is becoming expensive. None of that is good for consumer sentiment,” she says.

Private sector sentiment is critical to economic growth because confidence leads to higher spending. The most recent Westpac-Melbourne Institute of consumer confidence in Australia (PDF) – the long-time benchmark – this month fell to its lowest level since the beginning of the pandemic.

In the US, the benchmark measure from the University of Michigan has hit a record low.

No quick turn-around

Consumer sentiment isn’t going to improve quickly, Xie Patrick says.

“High levels of inflation tends to lead consumer sentiment by six to 12 months, so even if inflation has peaked, we’ve still got six to 12 months of poor consumer sentiment. That’s not great.”

This adds to the argument why bonds are back.

One lingering question for investors is whether four per cent is a good return, given inflation is currently higher than that.

“To put that value into perspective, inflation markets infer that over ten years inflation will be, on average, around two-and-a-half per cent, which is the Reserve Bank’s inflation target,” Xie Patrick says. “Ten-year bonds are yielding a nominal rate of four per cent.”

“By owning a 10-year Australian bond, you are taking effectively no credit risk, keeping up with the two-and-a-half per cent long-term rate of inflation and then getting another one-and-a-half per cent.

“You’re getting paid to own something without credit risk and keep up with inflation.

“The value proposition for bonds is really back.”

About Amy Xie Patrick and Pendal’s Income and Fixed Interest team

Amy is Pendal’s Head of Income Strategies. She has extensive expertise and experience in emerging markets, global high yield and investment grade credit and holds an honours degree in economics from Cambridge University.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia. The team oversees some $20 billion invested across income, composite, pure alpha, global and Australian government strategies.

Find out more about Pendal’s fixed interest strategies here

About Pendal Group

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.