Here are the main factors driving the ASX this week according to our head of equities Crispin Murray. Reported by portfolio specialist Chris Adams.

Find out about Crispin’s Pendal Focus Australian Share Fund

Find out about Crispin’s sustainable Pendal Horizon Fund

HIGHER-than-expected US inflation data, combined with a hawkish tone from European and Australian central banks, have helped push equity markets down through the May lows.

US bonds have sold off, with a “bear flattening” of the curve as 2-year yields rose 41bps and 10-year yields rose 22bps (at Friday’s close). Risk aversion saw the US dollar and gold hold up, while equities fell.

The S&P 500 was off 5% last week, the NASDAQ lost 5.6% and the Euro STOXX 50 was down 4.9%. For the year-to-date the S&P 500 is -17.6%, the NASDAQ -27.3% and the Euro STOXX 50 -18.5%.

A record low in the University of Michigan Consumer Sentiment index (which goes back to 1978) and evidence that consumer longer-term inflation expectations are on the rise add to the sense of foreboding.

The market increasingly fears high interest rates and a recession.

The RBA’s 50bp rate hike triggered recession fears domestically. This prompted some shorting of domestic banks by international investors and saw the Australian market sell off even before Friday’s move.

The banks sector fell 10.6% last week. The S&P/ASX fell 4.3% and is down 5.5% in so far in 2022.

The US Fed meets this week and the market is pricing an 80% chance of a 75bp hike.

The rationale is they need to “get in front of the curve” and restore confidence that inflation will be subdued.

There is a growing view the Fed has to choose between allowing inflation to stay high or triggering a recession. This translates to either rating or earnings risk for equities.

The combination of rates up, oil up and US dollar up is not good for equity markets.

Our view is the risk/reward trade-off remains skewed to the downside for now.

Pendal Focus Australian Share Fund

Now rated at the highest level by Lonsec, Morningstar and Zenith

Economics and policy

The May CPI print was only 0.1% worse than expected. However the underlying components were considered more negative.

Some key points to note:

- Headline inflation rose to 8.6% year-on-year — a new high for this cycle and up from 8.3% last month. Energy accounted for was 0.3% of the 1% month-on-month increase. Gas prices are up a further 10% this month.

- The Median CPI across all categories was +0.58% m-o-m. This was the highest-ever print, as was the y-o-y median. This reflects the breadth of pricing pressure.

- Core CPI rose 0.63% m-o-m versus 0.5% expected. It’s running at 6% y-o-y, down from 6.2% last month.

- Core goods inflation picked up m-o-m, goods CPI +0.7% m-o-m versus +0.2% last month. New and used auto prices picked up as car manufacturing remained constrained.

- Core services inflation rose 0.6% m-o-m. Airfares remained strong, up 12.6% m-o-m.

- Shelter (50% of services inflation) did not decelerate as expected, rising 0.6% m-o-m.

One key issue is that goods inflation is not coming off quickly enough to offset the rise of services inflation.

The rent component was expected to decelerate, but did not. Some private measures of rent indicate this will continue to rise. This needs to be watched since it comprises 40% of core CPI.

The problem for policy makers is that inflation expectations are beginning to step up.

This puts more pressure on the Fed to break the wage-price feedback loop by slowing the economy and creating slack in the labour market. The Atlanta wage tracker is staying flat at 6.5% and hasn’t yet shown signs of falling back.

The University of Michigan Consumer Sentiment index weighed on markets, falling to levels not seen since the early 1980s. The disconnect here is that people are still spending despite a low confidence level.

There appears to be an emerging divergence between lower and higher income consumers. The former are hit harder by inflation and the removal of stimulus payments.

This is evident in feedback from consumer stocks, where luxury and premium products are continuing to see good demand.

Europe

The European Central Bank met and sent a clear hawkish shift in their outlook. They noted CPI was now expected to be above the target range through 2024, despite lowering the outlook for economic growth. They also signalled the risk to CPI expectations was to the upside.

Sustainable and

Responsible Investments

Fund Manager of the Year

The signal is for rates to increase 25bps in July. The market is now expecting 50bp in September and possibly another 50bp in October, with rates peaking at 1.75%.

This means the market is now seeing 125bps tightening this year, versus 50bps only four weeks ago.

It is worth bearing in mind that inflation isn’t expected to peak before September, at around 9.3%.

Using the old rule of thumb that rates need to reach the inflation level, there still seems risk to the upside.

The market’s other issue was the lack of any specific mechanism to avoid the “fragmentation risk” of widening spreads from Eurozone “periphery” economies.

This is already occurring with Italian 10-year yields now at 3.98% versus Germany at 1.58% — a spread of 240bp. This is a 100bp widening from the start of the year when German bonds were -0.18% and Italian 1.19%.

The ECB believes it has the tools to prevent this becoming a problem. But lack of detail opens the door to the market testing the level at which the ECB will act.

Markets

The rally over the last fortnight lacked conviction, with low breadth compared to previous market returns.

We are now breaking through the May lows in US equities. The near-term outlook is not constructive given:

- US bond yields have risen to cycle highs on the tail of a break-out in German bonds

- The most bombed-out tech names are rolling over again

- Mega-cap tech look to be rolling over; these have propped the overall index up

- The US dollar index is testing new highs

- Oil price – the source of a lot of problems – refuses to soften given supply issues

The risk-off signal is also apparent in speculative tech and also in cryptocurrencies, where Bitcoin is falling on liquidity concerns.

Tightening cycles often trigger some form of financial shock, which can create a capitulation in the market. This often marks the low.

In this context, there are specific areas we are watching for signs of further strain:

- Peripheral bond spreads in Europe (indicates pressure on the Euro as ECB forced to raise rates into downturn)

- Credit spreads (indicates evidence of recession risk)

- US$/Yen and Japanese bond yields (indicates evidence market losing confidence in yield curve control)

- CNY/USD (reflecting pressure on Chinese economy from higher energy and food prices)

- Crypto, first real test of how liquid this is in a bear market

- Performance of banks versus market

Technically, if the S&P breaks through the May low the next resistance is at 3500.

Beyond that, the pre-Covid level was 3250.

If we get into this territory it would represent a material tightening of total financial conditions which may see a moderation in the market’s view of how far the Fed needs to tighten.

Australia

The RBA rose 50bps rather than the expected 25-40bp. Like many other central banks the Reserve seems to realise the need to get back to neutral quickly. Rate expectations have now risen for the balance of the year. This has weighed on the ASX, with banks hit on economic concerns and REITs over the increase in funding costs.

After a multi-year cease fire, global long/short funds chose to put the short back on Australian banks, on the premise the economy is going to slow and that housing will follow.

We have been here before and it has historically been a losing trade.

The rationale, from an international perspective, is grounded in the fact that Australian house prices have more than doubled the growth rate of the US over the past 30 years.

There are explanations for this, including the impact of immigration and lack of supply.

But the simple narrative for now is that Australian mortgage rates are set to rise from around 2% to potentially over 5%. In the near term that means risk for housing and the banks.

This saw Westpac (WBC) -13.1% last week, Commonwealth Bank (CBA) -10.9%, National Australia Bank (NAB) -10.3% and ANZ (ANZ) -7.7%. Year-to-date the banking sector has now performed in line with the market.

Discretionary retail is the other sector particularly vulnerable to the rise in mortgage rates.

This is translating through to underperformance in JB Hi-Fi (JBH, -10%), Wesfarmers (WES, -7.4%) and certain small caps.

About Crispin Murray and Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia. Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

As bond yields rise investors can expect “some very good opportunities”, says Bill Bellamy, Director of Income Strategies at Pendal’s US-based investment manager TSW

- Bond yields high enough to consider investing

- Fundamental analysis is critical the further out the yield curve

- Find out about Pendal’s income and fixed interest funds

THE jump in bond yields this year has been stark, particularly in the high-yield end of the market.

US double-B rated bonds, for example, yielded 3.2 per cent at the start of the year and are now around 6 per cent.

But is that enough to make bond markets investable, given inflation rates globally are running at multi-decade highs?

Is it enough to look at high-yield investments, given the risk-reward trade off?

“Fixed income is, in our view, certainly much more investable today than it’s been for a while,” says Bill Bellamy, Director of Income Strategies at Pendal Group’s US-based investment manager TSW (Thompson, Siegel and Walmsley LLC).

“But we’re probably not totally done with this corrective phase and there is still room to go with yields. As they rise, there are going to be some very good opportunities.”

“Because the market has priced in a lot of the US Federal Reserve tightening that we think is coming, it’s time to take a look at fixed income markets once again,” Bellamy says.

Investing in fixed income involves interest rate risk, duration risk, industry risk and security specific risk.

But its main role in a portfolio is to provide ballast for stability.

“Investors want the ballast,” Bellamy says. “And investors can scale into the market as yields move higher.

“You may not pick the bottom, but you’ll get a better yield than what we’ve seen for some time.”

Returns don’t have to be spectacular because that’s not what investors use fixed income for — or as Bellamy puts it: “we’re trying to hit singles and doubles, not triples and home runs.”

While the philosophy across fixed income markets is the same, as investors move out the yield curve and go beyond investment grade to high-yield double B rated bonds, or single B or triple C, it becomes more of an individual credit picker’s market. It is an area of expertise for Bellamy.

Income cushion

High-yield bonds offer an income cushion that investment grade bonds and Treasuries do not, he says. The main risk in high yield is default risk.

“In high yield bonds, you need to do fundamental analysis of the underlying credits ultimately going into a portfolio.

“You need to know what the ultimate risk is in the event of a problem at corporate level. You need to know anything that could impair your ability to get your money back,” Bellamy explains.

Find out about

Pendal’s Income and Fixed Interest funds

That groundwork understanding the ultimate asset of a high-yield bond isn’t just a safety check. It also unveils mis-priced assets.

“Is the market efficient in that respect? We don’t think so,” Bellamy says. “We believe the ratings agencies leave a lot of opportunities in the high yield market especially as you go out the risk spectrum.

“That’s particularly so when an issuer might have one or two issues outstanding. That’s really where you can uncover some opportunities from an investment perspective.”

“When investing in fixed income, we believe that income wins over time. We try to outyield the indices in the most efficient way possible.

“We are a big believer in getting paid for the risks we are taking.”

About Bill Bellamy

Bill Bellamy is Director of Income Strategies at Pendal Group’s US-based investment manager TSW (Thompson, Siegel and Walmsley LLC). Bill has been with TSW for 19 years. He is a graduate of Cornell University, BS and Duke University, MBA. He previously worked for Merrill Lynch Capital Markets as an Assistant Vice President, Clayton Brown & Associates as a Vice President, First Union Capital Markets as a Vice President and Trusco Capital Management as a Vice President. Bill is a Chartered Financial Analyst.

About Pendal’s Income & Fixed Interest team

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia. The team won Lonsec’s Active Fixed Income Fund of the Year award in 2021 and Zenith’s Australian Fixed Interest award in 2020.

Find out more about Pendal’s fixed interest strategies here

About Pendal Group

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Here are the main factors driving the ASX this week according to our head of equities Crispin Murray. Reported by portfolio specialist Chris Adams.

Find out about Crispin’s Pendal Focus Australian Share Fund

Find out about Crispin’s sustainable Pendal Horizon Fund

BETTER-than-expected economic data and signs of Beijing winding back Covid restrictions are fuelling concerns that inflation may not fall as quickly as some hoped.

This has prompted a rebound in commodity prices. It’s also seen US 10-year bond yields rise 20bps to 2.94%, down from a peak of 3.19%.

The move in bonds triggered a sell-off in US equities late last week. The S&P 500 finished down 1.2%. The S&P/ASX 300 was up 0.8%.

Cautious sentiment was reinforced by JP Morgan CEO Jamie Dimon’s reference to the “hurricane… right out there down the road coming our way” as a result of higher rates and quantitative tightening.

Elon Musk’s “superbad feeling about the economy” and need to cut 10% of Tesla’s workforce did not help.

The S&P 500 has rallied 7% off its lows and many sentiment indicators have shifted back from “oversold” to more neutral.

The near-term market direction is likely to be driven by this week’s inflation data and the potential for earnings surprises.

We believe we are in a holding pattern for now.

Rate expectations have shifted materially. Whether they will moderate or go higher still will be determined by the economy over the next three months. It’s just too early to call.

Soft landing or recession

Going back to 1929, the average US soft-landing bear market has been -26% — and for a recession

-41%.

Here are the current scenarios for each of these “book-end” soft-landing and recession paths:

1) The path to a soft landing

- Building inventories mean consumer price rises ease off

- Chinese re-opening eases product supply, also helping inflation

- Wages ease as a lack of stimulus means companies no longer need to pay up to induce workers to return. Companies begin to stop hiring and even lay off workers. Tesla and Amazon’s recent comments are pertinent in this regard

- Commodity prices stop rising

- As a result, the Fed doesn’t need to go harder than what’s already priced in the forward curve

2) The path to recession

- Inflation remains resilient as the economy doesn’t slow sufficiently

- Companies continue to catch up to the cost impost they are wearing

- Housing costs keep rising

- The labour market stays tight as service jobs continue to recover, workers seek compensation for higher prices and so wage growth doesn’t slow

- Supply shortages combined with the return of China continue to underpin higher commodity prices

- This leads to the Fed remaining hawkish, triggering a recession

The path should become more apparent in coming months.

Pendal Focus Australian Share Fund

Now rated at the highest level by Lonsec, Morningstar and Zenith

The risk-reward at this point favours caution. The Fed still cannot afford for financial conditions to loosen — which would be the case if equities rallied too far.

The key caveat is that Australian equities remain well placed in this environment and continue to hold up reasonably well.

Economics and policy

Monthly US payroll data was solid — 390k new jobs versus 318k expected.

The rate of new jobs has eased from the 600k level, but it’s generally considered too high to be consistent with an easing of inflationary pressure.

The three-month moving average remains at 408k. The market believes a level of 100k-150k new monthly jobs is needed.

Participation picked up 0.1%, but this is not enough. This gap helps explain tightness in the labour market with unemployment at 3.6%. There is material deviation by age cohort, with participation rates in the 55-and-over range remaining stubbornly low.

Average hourly earnings growth of 0.3% month-on-month was a bit lower than expected. The annual rate of 5.2% remains too high, though the three-month moving average has fallen into the 4-5% range. We need to see it drop into the 3-4% range.

The latest ISM manufacturing data was too strong for the market, rising to 56.1 versus consensus 54.5. Services ISM was marginally softer at 55.9 versus consensus of 56.5, but this clearly remain the strong part of the economy.

The orders backlog component fell back to pre-pandemic levels, indicating supply chains are improving. This reflects the build in retailer inventory we have been hearing about from companies.

Overall there is nothing here to reduce the likelihood of back-to-back 50bp moves from the Fed in June and July.

It also reduces the likelihood of a pause in rate hikes in September.

Oil

Oil markets saw a lot of action last week.

OPEC+ announced it would bring forward an increase in oil supply. Initially this was seen positively as a thawing of relations between Saudi and the US.

But the more you dug into it, the more it looked like another hollow effort to make it appear as though something was being done about high US fuel prices.

OPEC is bringing forward a slated September supply increase to July and August.

This equates to an extra 200k or so barrels per day for two months — allocated across all of OPEC+, including Russia. Many of these nations are unable to produce the extra barrels, so not all of that will come onto the market.

It is also apparent that Libya and Venezuelan production has been weaker than expected. Any agreement with Iran to potentially unlock another 500k bpd is still forthcoming.

Russian supply is estimated to be 1m bpd less than pre-invasion. The prospect of China re-opening could add 1m bpd of demand.

The risk of fuel prices to the economy is high.

US inventories are low. Globally they are being propped up by strategic petroleum reserve releases, but this is not sustainable.

An extremely tight refining market caps all this off. The NYMEX 3-2-1 spread — the gap between a price of three barrels of oil and the two barrels of petrol and one of diesel which can be refined from it — is multiples of its historical average.

Sustainable and

Responsible Investments

Fund Manager of the Year

This implies fuel prices at the pump are equivalent to US$175 oil. This is a challenge for the consumer and does not help the inflation outlook.

Australian Energy markets

There is increasing focus on Australian power prices.

A combination of outages and supply issues at coal-fired plants — plus cold weather and a limited supply of solar at this time of year — have left the domestic market relying on gas to fill the void.

This comes at a time of limited gas supply and a high global price. Wholesale prices have surged in response. The NSW average price is $200 — almost double the previous highest prices over the past 15 years.

In the near term this affects only a few commercial buyers, since most are on contract.

Consumers are protected for now. The main effect is on power providers reliant on purchasing power on the National Electricity Market. Smaller players are looking to shed customers and load as a result.

However the medium-term effects could be material.

Some analysis suggests it could translate to power price rises of 9% in Sydney in FY23 and 30% in FY24. The situation would be worse in Queensland and marginally better in Victoria.

Clearly, this is politically unpalatable and raises the risk of intervention in the industry.

Understanding the flow-on effects for the economy and corporate earnings is key here.

Markets

The consensus view that peak inflation meant peak bond yields was challenged last week.

We remain wary of this view. History suggests that in most cycles rates end up rising above inflation. If the latter isn’t below 3% in a reasonable time frame we still may see rate and bond yields head higher.

The issue for markets remains that central bankers will want to be seen to be hawkish until it is clear inflation is beaten — which will not help sentiment.

Commodities maintain their defensiveness. This partly reflects the oil issue flagged above — but also the belief that China appears to be reopening. Copper remains the best proxy for this sentiment, and rose 6% last week. The Australian market continues its resilient performance with energy and resources leading the way. Financials and utilities fell last week, relating mostly to stock-specific issues.

About Crispin Murray and Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia. Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Monetary policy will have to work harder to keep inflation in check if the new Labor government is still putting extra dollars into pockets, writes Pendal’s TIM HEXT

THE federal election was an exciting moment for all Australians, but a week later our fascination with politics is probably again confined to those in Canberra.

This time last week I was an expert in the comings and goings of seats like Fowler and Gilmore. In a month I won’t be able to tell you where they are, let alone who the local member is.

One thing that’s clear, though, is fiscal policy will stay expansionary under Labor.

The new government’s additional spending adds $19 billion to the budget while its aspirational revenue plan only takes off $11.5 billion.

Budget numbers were supercharged during Covid, so $19 billion is barely noticed. But let’s stop and think about the impact.

Let’s remember that a public sector deficit is a private sector surplus – more money is entering the private sector than is taken out.

When the RBA tightens by 1%, the interest bill on the $3 trillion debt goes up by $30 billion. However, two thirds of debt is lent by Australians – so $18 billion is a transfer between borrowers and savers within Australia.

Only one third of the interest leaves the country and goes into the pockets of foreigners. So the Labor spending plans on a dollar-for-dollar basis roughly negate the 1% rate rise. I understand this is not a straight comparison since rate rises have second-round impacts to economic activity and wealth more so than fiscal policy.

Find out about

Pendal’s Income and Fixed Interest funds

Also it does matter whether the money is entering or leaving pockets with a propensity to borrow or save.

But this does show that monetary policy will have to work harder to keep inflation in check if the government is still putting extra dollars into pockets.

If all goes well for Labor the global economy will open up quickly in the next few years, helping the supply side catch up to the strong demand side.

If not, they face a growing problem of entrenched inflation, spurred on by their fiscal policy pushing demand. Rates will then have to hit restrictive levels – which nearly always turns into recession, just in time for the 2025 election.

As bond managers we are constantly monitoring the interplay between demand and supply in the economy.

We will shortly publish an in-depth piece on the inflation outlook. For now though, inflation is here to stay and long bond duration remains vulnerable.

About Tim Hext and Pendal’s Income & Fixed Interest boutique

Tim Hext is a Pendal portfolio manager and head of government bond strategies in our Income and Fixed Interest team.

Tim has extensive experience in banking, financial markets and funding including senior positions with NSW Treasury Corporation (TCorp), Westpac Treasury, Commonwealth Bank of Australia, Deutsche Bank, Bain & Co and Swiss Bank Corporation.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia.

Find out more about Pendal’s fixed interest strategies here

About Pendal

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

In 2023, Pendal became part of Perpetual Limited (ASX:PPT), bringing together two of Australia’s most respected active asset management brands to create a global leader in multi-boutique asset management with autonomous, world-class investment capabilities and a growing leadership position in ESG.

Here are the main factors driving the ASX this week according to portfolio manager Jim Taylor. Reported by portfolio specialist Chris Adams

A BOUNCE in US equities last week was underpinned by reassuring words from JPMorgan Chase CEO Jamie Dimon and a positive take on some Fed rhetoric.

At the same time, emerging caution on the near-term outlook for US companies seems to be taken positively as a sign of moderating demand — which may ease inflationary pressure and potentially the rate of tightening.

Nevertheless, the risk of recession remains front of mind — investor surveys place the chance at about 55%.

The S&P 500 gained 6.6% and the NASDAQ 6.9% last week. The S&P/ASX 300 was up 0.5%.

There is more data coming out that suggests supply chain stresses are abating while pressure on employers is seen to be falling.

China’s Premier Li Keqiang held an extraordinary conference call across multiple layers of government flagging near-term risk to the Chinese economy. This wasn’t sufficient to de-rail a strong week for the Australian Resources sector (+2%).

Find out about

Pendal Focus

Australian Share Fund

Crispin Murray,

Head of Equities

Fedspeak

Fed watchers sifted through the May FOMC meeting minutes and recent comments — and formed the view that tightening may pause in September.

Fed minutes showed “all participants concurred that the US economy was very strong, the labour market was extremely tight, and inflation was very high”. With risks of more inflation “skewed to the upside”, “participants agreed that the Committee should expeditiously move the stance of monetary policy toward a neutral posture”.

They also noted policy may need to move beyond neutral to a “restrictive” stance.

“Most” participants judged 50bp rate hikes would be appropriate at the next couple of meetings. However “a number” said data had begun to indicate inflation “may no longer be worsening”.

Atlanta Fed president Raphael Bostik said he supported an expeditious return of monetary policy to a more “neutral” stance to bring down inflation. But policymakers must “proceed carefully in tightening policy”, being mindful of the uncertain effects of the pandemic, the war in Ukraine and supply constraints on the economic outlook.

Policymakers were unsure how quickly higher borrowing costs would bite demand, said Kansas City Fed president Esther George.

St Louis Fed president James Bullard — who has been the leading hawk — called for the Fed to frontload rates and get them to 3.5% by year-end.

This would enable them to ease in 2023 and 2024 if inflation is under control. He didn’t see a recession, but did see some businesses getting “punched in the face” as consumers substituted basic necessities for luxuries.

US data and inflation

April personal spending rose 0.9% month-over-month versus an expected 0.7%.

The American consumer remains resilient — despite low confidence surveys — and is benefiting from wage gains and the gradual draw down of accumulated savings and handouts. This gives the market a degree of comfort.

The PCE Price Index (which measures costs Americans pay for a variety of different items) edged up 0.2% month-over-month and 6.3% year-over-year.

Meanwhile the core PCE indicator (the Fed’s preferred inflation gauge which excludes food and energy and is used to make monetary policy decisions) advanced 0.3% on a seasonally adjusted basis.

The annual rate eased from 5.2% in March to 4.9%, in line with expectations.

Several drivers of inflation are showing signs of easing, though the pace of normalisation remains the obvious question mark:

- Wages: Wage growth (as measured by month-on-month changes in total hourly earnings) is moderating as participation rates normalise.

- Employment: Pressure on companies to hire has passed the peak. This can be seen in surveys of hiring intentions and expected worker compensation. It can also be seen in anecdotes such as PayPal announcing staff lay-offs as a result of lower top-line growth and the need to prevent material operating deleveraging.

- Profit margins: As demand abates, abnormally high-profit margins will have to revert to more normal levels.

- Housing: While inventory of completed homes is very low a lot of supply is coming through which will ameliorate price rises and flow into reduced pressure on rentals — a key component of the inflation spike we have witnessed. In April, US new home sales fell 16.6% m/m to 591,000 — far short of the 748,000 expected. Unsold inventory of new houses jumped 34,000 m/m and 127,000 y/y to 444,000 seasonally adjusted — the highest since May 2008. Inventories jumped from 6.9 months of supply to 9 months.

New Zealand

The RBNZ raised rates 50bps to 2%, as expected. The Monetary Policy Committee is in a real hurry, with a very high likelihood of successive 50bp hikes in July and August. They flagged a peak Official Cash Rate (OCR) of about 4%, up from 2.6% only six months ago.

Sustainable and

Responsible Investments

Fund Manager of the Year

They couldn’t be any clearer on their intent: “A larger and earlier increase in the OCR reduces the risk of inflation becoming persistent, while also providing more policy flexibility ahead in light of the highly uncertain global economic environment.”

China

China’s cabinet introduced 33 policies to support consumer spending and businesses as the economic fallout from the zero-Covid policy bites deeper.

The package of about US$30 billion was extensive. It includes measures to boost infrastructure spending and rural road building; improve supply chain disruptions; provide cash subsidies to maintain staff levels; provide VAT rebates; and reduce taxes on car purchases.

Markets

There was plenty of commentary and results coming out of US companies last week.

It wasn’t all good news. But in conjunction with better economic data the market has gravitated to the view that after 50bps in July and August the Fed might be inclined to take a breather and see how the tightening is manifesting.

Sentiment was bolstered by Jamie Dimon’s remark that if the US does go into recession, it is likely to be moderate due to underlying strength in the economy and consumer.

There were also comments in this vein from Bank of America CEO Brian Moynihan. He noted consumers were buoyed by strength in household balance sheets right across the income spectrum — and they continued to grow.

Moynihan also noted credit card debt was rebounding from its lows (though it remains well below the pre-Covid level) and mortgage loan-to-value ratios remain in the 50%-60% range.

It wasn’t all one way traffic on the commentary front.

US social media company Snap fell 33% on reduced revenue and earnings guidance for the current quarter after issuing guidance a month ago. “The macroeconomic environment has fallen further and faster than we had anticipated,” management said. Other digital media businesses fell 5-20% in sympathy.

Commentary from US retailers was mixed.

Dollar Tree and Nordstrom were strong. But a mix shift in consumption saw a blow-out in inventories at Walmart and Target. Gap also reported a big miss.

Clearly there is no consistent playbook from the retailer’s perspective in this environment. Pivots in consumer demand are tough for retailers to keep up with.

Inflows resumed into equity funds globally after a run of outflow weeks. There was US$21 billion of inflows — the biggest amount in 10 weeks — mainly into US equities.

The Australian market lagged the US after several weeks of outperformance. Energy (+2%) and Materials (+1.7%) led. Technology (-3.4%) was the worst performer.

Stock moves were much more idiosyncratic than they have been for quite a few weeks.

BHP (BHP, +3.9%) merged its oil and gas business into the newly named Woodside Energy (WDS, +4.8%). Tabcorp (TAH, +2.2%) demerged its lotteries and keno division in The Lottery Corporation (TLC, +2.1%). The likelihood of further M&A activity remains high.

Incitec Pivot’s (IPL, -6.4%) 1H FY22 result missed EBITDA expectation by 8% as both the fertiliser and explosives divisions didn’t exhibit the operating leverage that has been evident in peer results. The big news was the proposed spin-off of the fertiliser business, which they have been trying to offload without success for many years. Fertiliser peers globally have retreated from the highs earlier in the year, which has impacted IPL as well.

About Jim Taylor and Pendal Focus Australian Share Fund

Drawing on more than 25 years of experience investing in top-performing Australian companies and a background in accounting, Jim manages our Long/Short Fund and co-manages our Imputation Fund. He is a Chartered Accountant with membership of the Australian Institute of Chartered Accountants.

Pendal Focus Australian Share Fund is managed by Crispin Murray. The fund has beaten its benchmark in 14 years of its 18-year history (after fees), across a range of market conditions. Find out more about Pendal Focus Australian Share Fund here.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

After the evolution of Coalition fiscal spending habits during the pandemic, Australia’s new Labor government won’t be a big change, says Pendal’s Anna Hong

ON THE economic front, Australians will be largely unaffected by the change of federal government — at least in the near term, says Pendal’s Anna Hong.

That’s because key economic policies between Australia’s two major parties are mostly aligned, says Hong, an assistant portfolio manager from Pendal’s Income and Fixed Interest team.

However, there will be an increase in fiscal spending by the Albanese government.

Labor will increase fiscal spending by a net $7.4 billion in areas such as home equity schemes and electric car discounts, as you can see in this table:

Labor’s Fiscal Plan

| Net Budget Impact | -$7.4bn | |

| Revenue + Savings | $11.5bn | |

| Spending | $18.9bn | |

| Key Spends | Childcare subsidies | $5.4bn |

| Aged care | $2.5bn | |

| Medicare | $0.75bn | |

| Electric car discount | $0.47bn | |

| Home equity scheme | $0.31bn |

“This will prop up demand without fixing the supply issues, nudging inflation higher,” says Hong. “It will make the RBA work harder to counter the loose fiscal policy.”

The federal budget will remain in deficit for the rest of the decade — under either party.

“The stumbling block to Labor’s policies may be in generating planned revenue and savings.

“Many items on their list — such as multinational tax revenue — are easy to promise but notoriously difficult to achieve.

“Overall, the change of government is more of the same for the economy and the budget.

“The difference will be in the changes many Australian voters are focused on – climate policy, federal integrity, and gender equity — as Pendal’s Rajinder Singh outlines here.

“Australians want action and will watch this space closely.”

Find out about

Pendal’s Income and Fixed Interest funds

About Anna Hong and Pendal’s Income and Fixed Interest team

Anna Hong is an assistant portfolio manager with Pendal’s Income and Fixed Interest team.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia. In 2020 the team won the Australian Fixed Interest category in the Zenith awards.

With the goal of building the most defensive line of funds in Australia, the team oversees A$22 billion invested across income, composite, pure alpha, global and Australian government strategies.

Find out more about Pendal’s fixed interest strategies here

About Pendal Group

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Has inflation peaked and if so, what’s next for fixed interest investors? Here’s a view from our head of government bond strategies TIM HEXT

AMONG the many adages I’ve heard in my career “sell in May and go away” always sticks in my mind.

The quote apparently originated in London and said in full: “sell in May and go away and come back on St Leger Day” (in September). The “go away” referred to very long summer holidays enjoyed by rich stockbrokers.

In the US equity market November-to-April outperforms May-to-November over time.

Going back more than a century the Dow’s average return is apparently 5.2% for November-to-April, compared to 2.1% for May-to-October.

In Australia the numbers are 5.1% and 2.4%. The term could be recoined as “buy in November and sit back”, but that wouldn’t rhyme.

The calm in the storm

This May has been the calm in the storm. But no one can agree if it’s the eye of the storm or if we’re actually through it.

Markets are clutching at any sign inflation has peaked.

In the US it likely has on both on a monthly and year-on-year basis — but will be slow to come down.

In Australia we are unlikely to see a repeat of the Q1 2.1% quarterly CPI number. But base effects mean annual inflation will peak closer to 6% (currently 5.1%) in Q3 (released in late October).

Find out about

Pendal’s Income and Fixed Interest funds

We have just finished a deep dive into inflation which we will release shortly as part of our Australian Investor Quarterly newsletter.

As the inflation narrative settles down, all eyes will turn to the impact of inflation and interest rates on growth.

Share markets remain vulnerable to earnings downgrades and weakening growth numbers.

This becomes reflexive, though, as equity weakness in turn causes confidence to fall which may eventually take some pressure off rising interest rates thereby supporting equities.

We may well spend the northern summer rolling around in this cycle of volatility, heading eventually nowhere as the dynamics try to work themselves out.

What it means for investors

As a fixed interest portfolio manager it means we must look to harvest more tactical trades than big-picture moves for the next few months.

We continue to think short-dated inflation bonds are cheap in outright real yields but also in break-evens (inflation expectations).

The picture for duration and credit is less clear though we do have some positions based on cash rates “only” getting to 2% this year as opposed to markets pricing closer to 2.75%.

With both bond markets and equity markets trashed in the last four months I will ignore the “sell in May and go away” advice as coming way too late — wishing someone had instead advised me this year to “Sell on New Years Day and go away.”

About Tim Hext and Pendal’s Income & Fixed Interest boutique

Tim Hext is a Pendal portfolio manager and head of government bond strategies in our Income and Fixed Interest team.

Tim has extensive experience in banking, financial markets and funding including senior positions with NSW Treasury Corporation (TCorp), Westpac Treasury, Commonwealth Bank of Australia, Deutsche Bank, Bain & Co and Swiss Bank Corporation.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia.

Find out more about Pendal’s fixed interest strategies here

About Pendal

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

In 2023, Pendal became part of Perpetual Limited (ASX:PPT), bringing together two of Australia’s most respected active asset management brands to create a global leader in multi-boutique asset management with autonomous, world-class investment capabilities and a growing leadership position in ESG.

Here are the main factors driving the ASX this week according to our head of equities Crispin Murray. Reported by portfolio specialist Chris Adams.

Find out about Crispin’s Pendal Focus Australian Share Fund

Find out about Crispin’s sustainable Pendal Horizon Fund

THE MARKET is at an interesting near-term juncture.

The S&P 500 has lost ground seven weeks in a row and is now off about 20% from its peak. It has re-tested and held recent lows.

Expiring options may reduce volatility and we may see some month-end rebalancing towards equities in a low-liquidity environment due to next Monday’s US Memorial Day holiday.

A near-term bounce may be possible and counter-trend moves can be material.

However we don’t think we’ve seen the low point for this cycle. The market is yet to work through the effect of a slowing economy on corporate earnings.

The S&P 500 fell 3% last week as the market continued to worry about the potential for recession.

This was compounded by some poor earnings results out of US retailers. The issue here was not weaker consumption, but the mix shift from goods to services and a rising cost impost.

This emphasises the market’s vulnerability should a slowdown occur and begin to affect earnings.

US 10-year government bond yields fell 14bp. The positive correlation between bonds and equities appears to have broken down as the focus moves to risk aversion and a flight to safety.

We also saw a fall in the US dollar. This was probably a consolidation after a big run. It helped commodities and resource stocks, as did more signs of Chinese easing.

Australia again remains the market for these times.

The S&P/ASX 300 was up 1.2% for the week. It’s down only 2.5% for the calendar year to date, versus -17.7% for the S&P 500 and -27.2% for the NASDAQ.

Two key issues driving the market

We see two primary issues driving the outlook for markets.

The first issue is whether the US economy slows down or slips into recession.

Looking at recent bear markets, a recession has tended to lead to bigger drawdowns – such as in 2000-2002 and 2007-2009.

Pendal Focus Australian Share Fund

Now rated at the highest level by Lonsec, Morningstar and Zenith

Current investor surveys indicate a 50-55% probability of recession.

This comes down to views on what the Fed sees as acceptable inflation and what they will need to do to achieve it. There are two scenarios here:

- The positive scenario: Financial conditions have tightened enough, the economy is already slowing, inflation pressures are beginning to ease and therefore bonds have peaked and aggressive monetary tightening (and therefore recession) will not occur. A variant of this view is that the Fed will live with inflation in the mid to high 2s — rather than go for 2% — to avoid pushing the economy into recession

- The negative scenario: The economy will prove more resilient to rising rates, with consumers bolstered by excess savings and the labour market remaining tight. This will force the Fed to do more tightening and ultimately “break” the economy to control inflation. Proponents point to unemployment of 3.5% needing to rise to around 4.25% to create sufficient slack to ensure wages don’t reinforce inflationary pressures. The US has never been able to engineer such a rise in unemployment without it being associated with a recession.

The second major issue is whether the Chinese economy deteriorates or sees a policy-driven rebound.

Again, there are two scenarios:

- The positive view: China is close to peak Covid lockdown and the combination of re-opening and additional infrastructure stimulus will trigger a recovery, generate good commodity demand, and underpin resource stocks.

- The negative scenario: The economy is in far worse shape than the market realises. Lower rates reflect the financial vulnerability of property developers, stimulus will be ineffective due to low confidence, high input costs and inability to execute due to Covid restrictions.

Economics and policy

There is a lot of debate about whether we have seen peak inflation and peak bond yields.

Official data such as retail sales is signalling that the consumer remains strong, though there are signs the economy is slowing. For example, the Economic Surprise index – which shows the degree to which economic data is beating or missing estimates – is deteriorating in most countries. Consumer confidence is also weak and is at 40-year lows in the UK.

Sustainable and

Responsible Investments

Fund Manager of the Year

The combined effects of higher mortgage rates and fuel prices have reached levels consistent with previous consumer slowdowns. This indicator tends to lead by around 12 months.

Total financial conditions – which includes rates, equities and credit spreads – have tightened to a reasonable degree and should lead to a headwind of 1.3% of US GDP growth by Q3 2022.

We are also seeing signs that corporate pricing power – while still at high levels – may be easing.

There are signs that consumers are under some stress – particularly at the lower income end – with credit outstanding rising rapidly. This may support current consumption but is unsustainable.

Freight shipping rates are beginning to drop and there are early signs of a fall in US trucking rates.

That said, the freight rate may be a misleading signal due to a drop-off in Chinese exports. It’s unclear how much of this is a genuine de-bottlenecking of supply chains.

All this indicates the economy is responding to tighter financial conditions. It is slowing down and this is beginning to reduce inflation pressures.

This belief can be seen in forward pricing of inflation, where both break even yields and the 5-year inflation swap have rolled over since late April.

This could be positive for the equity market since it’s in line with the first scenario outlined above.

However there are still two key unknowns:

- This slowing could be the prequel to a recession. A slow-down and a recession will look the same initially. It will also probably result in negative earnings revisions, which the market will not like as we saw last week in the US.

- The second unknown is whether this will equate to inflation falling enough to allow the Fed to declare victory.

Fed Chair Powell has stressed that the labour market is resilient enough to weather tightening policy.

While this sounds reassuring, the question is whether a resilient labour market is consistent with inflation falling to target levels. If it is not, policy needs to tighten even more.

The labour force is very tight and this is driving wage growth. Some measures suggest we need to see employment decline by at least 1% to reduce wage pressure.

China

Economic surveys indicate the Chinese economy is weak. Q2 GDP is expected to decline 1.5% to 2%, with growth for the year coming in between 3% and 4%.

Beijing has responded with a larger-than-expected cut in its 5-year loan prime rate.

China bears see this as a move to prop up private developers who are facing a funding squeeze, thereby preventing deterioration rather than providing stimulus.

The more bullish view is that while this may not be a sizeable move, it is a very strong signal that the government will support property, similar to November 2014. Then it was the precursor to a big bounce in Chinese growth sentiment in 2015.

We remain cautious on a China recovery.

The property market appears to be deflating, but prices remain very high and developers are still too leveraged. At best the market stays flat, but the risk is to the downside, so any infrastructure related stimulus will only be offsetting this.

The other challenge is the lack of transparency over the extent of Covid and the real level of restrictions.

Europe

The ECB struck a more hawkish tone in response to poor inflation data. The market is now being primed for a first rate rise in July, with a possible 50bp move straight up. This is unlikely, but helped the Euro bounce off its lows against the US dollar.

Australia

There is little to read into the election outcome at this point. A majority government provides more clarity than a minority.

We are also likely to see more emphasis on reducing carbon emissions in coming years, which will have an impact on corporate disclosures and investment.

US earnings

Overall quarterly earnings were good. Full-year earnings lifted from about 5% to 11% growth.

However the outlook looks overly optimistic, with 9% eps growth expected in CY23 despite a slowdown.

Last week demonstrated the impact earnings headwinds can have. Broadline retailers missed earnings expectations as a result of freight costs and the mix shift in consumption.

Walmart and Target have joined Amazon in highlighting material gross margin pressure.

Underlying sales have not been particularly disappointing. But the impact of the unexpected mix shift caused problems as spending moved away from home, consumer electronics and sporting goods to travel, toys and luxury goods.

Inventories are also building in areas such as home furnishings and consumer electronics, while unit demand growth is dropping. This crimps a company’s ability to push through price rises.

The share of “private label” sales are rising. This is partly due to improved product availability as labour issues improve. It may also indicate consumers are “trading down” as real income falls – potentially a signal of softer consumption.

The overall impact were large hits to stocks in the previously defensive consumer staples sector.

This highlights the difficulty in identifying defensive pockets in this environment

Markets

We may be seeing a near-term low in the US equity market.

Historically, bear market bounces average a 15% gain over 30-40 days.

This does not signal the market has hit its lows for the cycle. Most technical signals have not indicated a degree of panic or capitulation. For example put/call ratio data has not yet moved into 99th percentile level – a usual indicator of capitulation. Nor have we seen high volumes in stocks being sold down.

Retail investors are yet to give up on the bull market.

The triple-leveraged NASDAQ ETF is still seeing large net inflows – despite being down over 60% year-to-date. Interestingly energy-related ETFs – among the best performing year to date – are seeing negligible inflows by comparison.

The high proportion of “buy” ratings on the market leaders of the past few years is another sign that we are yet to see capitulation.

We see scope for short, sharp bear-market rallies, but remain defensively positioned overall. We don’t believe it is yet the time to reload on high beta, illiquid names.

The Australian market last week saw a good bounce in the resource sector (+3.8%) on China optimism. The Technology (+5%) sector bounced as Xero’s management clarified a post-result message and emphasised confidence in improved margins and cash flow over time. Consumer staples (-3.3%) lagged, following the US lead.

About Crispin Murray and Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia. Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

The latest wages data shows surprisingly modest growth in some sectors. But wages are the ultimate lagging indicator and that will soon change, says our head of government bond strategies TIM HEXT

DESPITE increasing anecdotal evidence of rising wages, the latest data shows the price of labour grew a modest 0.7% in the March quarter.

Over the year wage growth was 2.4%, according to the Wage Price Index (WPI) released yesterday.

Only one sector nudged over 3% annually and none grew at or near 1% for the quarter.

In some areas this was not surprising. But in industries such as construction and retail trade this flies in the face of worker shortages.

This will change, since we’ve really only fully opened up this year.

Wages are the ultimate lagging indicator — and patience is required.

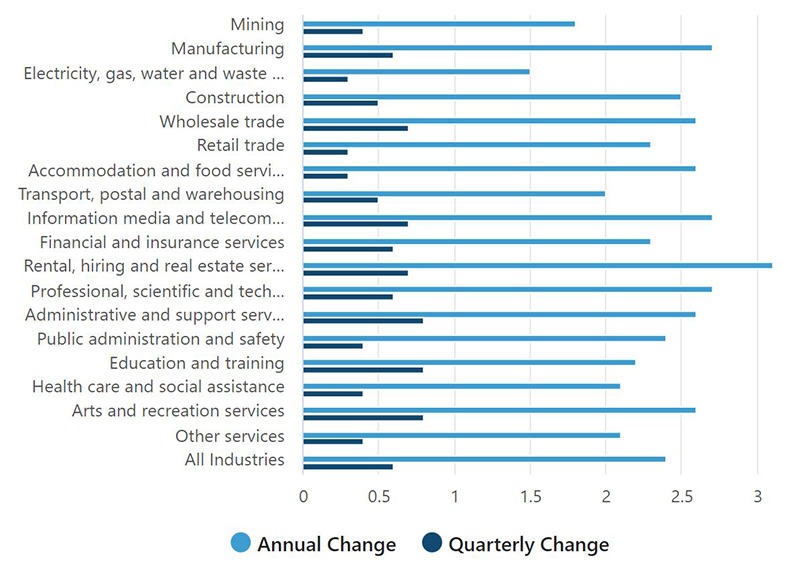

Annual and quarterly changes, WPI Mar 2022 (total hourly rates of pay excluding bonuses, per industry):

Earlier this year the Reserve Bank had WPI front and centre when trying to ignore rising inflation and pressure to raise rates.

Unless we got strong wage growth, inflation would eventually come back, the RBA said.

But in May — as they threw in the towel and hiked rates — the RBA referenced broader measures of wages:

“The outlook for broader measures of labour costs had also been revised up; average earnings were expected to increase at a faster pace than the WPI, as firms turned to bonuses, allowances and other measures to attract and retain workers,” the RBA said in its May board minutes.

They also highlighted the great inertia of wage growth:

“While the inertia arising from multi-year enterprise agreements and current public sector wages policies would continue to weigh on aggregate wages growth in the near term, a period of faster growth in labour costs overall was in prospect.”

The main battleground this year will be public sector agreements across the big employment areas of health, education and transport.

Find out about

Pendal’s Income and Fixed Interest funds

The public sector employs around 20% of the workforce. These are state government responsibilities and for now at least the governments largely have a 2.5% wage cap.

However unions quite rightly point out that a 5% inflation rate is seeing real wages fall. With staff shortages in key areas they are in a good position to extract wage rises closer to 5% than 2.5%.

Maybe for teachers and nurses they can offer 2.5% and a “thank you” bonus of 2% for their efforts through Covid, keeping their policy “intact”.

The RBA expect the WPI to hit 3% by year end and 3.5% by the end of 2023.

Chances are we hit these levels sooner.

Let’s remember this is a good thing overall. It does however add to the narrative that inflation will struggle to fall back to target anytime in the next few years.

What it means for fixed interest investors

Investors should still be looking to inflation bonds ahead of nominal bonds.

In our portfolios we have been adding inflation risk, which has cheapened up in May.

Inflation will moderate next year but levels above 3% look like being more entrenched over the next two to three years, helped by wages eventually nearing 4% growth.

About Tim Hext and Pendal’s Income & Fixed Interest boutique

Tim Hext is a Pendal portfolio manager and head of government bond strategies in our Income and Fixed Interest team.

Tim has extensive experience in banking, financial markets and funding including senior positions with NSW Treasury Corporation (TCorp), Westpac Treasury, Commonwealth Bank of Australia, Deutsche Bank, Bain & Co and Swiss Bank Corporation.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia.

Find out more about Pendal’s fixed interest strategies here

About Pendal

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

In 2023, Pendal became part of Perpetual Limited (ASX:PPT), bringing together two of Australia’s most respected active asset management brands to create a global leader in multi-boutique asset management with autonomous, world-class investment capabilities and a growing leadership position in ESG.

Where are the opportunities emerging in fixed interest? Here are the latest insights from Pendal’s head of government bond strategies TIM HEXT

SO FAR 2022 has been an extraordinary year for markets.

This past week was perhaps the first where you could draw breath.

I am normally hesitant to forecast too far ahead given elevated uncertainties. “Conviction” is generally a positive word, but at times like this the negative simile of “entrenched” can be dangerous.

So let’s summarise where we are up to (at end of Monday, May 16):

| Data point | Market Pricing |

| Cash rates — Dec 2022 | 2.7% |

| Cash rates — Dec 2023 | 3.6% |

| 3-year govt bond | 2.83% |

| 10-year govt bond | 3.38% |

| 5-year inflation break-even (implied inflation) | 2.55% |

| 10-year inflation break-even | 2.35% |

Several things stand out in the above numbers.

Find out about

Pendal’s Income and Fixed Interest funds

First and most importantly the RBA is tightening because inflation is now well above its target band — and likely to stay there until mid-2024.

Below are our best guesses for the headline inflation rates going forward. They are conservative and risks are probably to the upside.

| Period | Estimate Quarterly Headline CPI | Estimated Annual Headline CPI |

| Current (Q1 2022) | 2.1% (actual) | 5.1% (actual) |

| Q2 2022 | 1.2% | 5.6% |

| Q3 2022 | 1.1% | 5.7% |

| Q4 2022 | 1.3% | 5.7% |

| Q1 2023 | 0.9% | 4.5% |

| Q2 2023 | 0.8% | 4.1% |

| Q3 2023 | 0.8% | 3.8% |

| Q4 2023 | 0.7% | 3.2% |

The fuel excise relief pushes Q2 2022 down 0.4%. But Q4 2022 gains back 0.4% when the full-rate duty returns (if indeed it ever does).

Clearly forecasting inflation over a year out involves some guesswork.

We assume goods prices moderate with some supply chain easing but service prices continue to rise above target with wages and strong employment.

When we look at the two tables above, the most glaring mispricing or opportunity is in 5-year inflation bonds.

Current breakeven pricing — ie the inflation rate that would make you neutral about owning them versus nominal bonds — is near the RBA target of 2.5%.

However for at least the next two years CPI is averaging close to 4.5%.

Unless you think inflation in the following three years will be around 1%, this is just wrong. And we haven’t even included the extra carry from owning these bonds.

A brief lull in inflation concerns has seen these 5-year inflation bonds cheapen and we have been adding them to our nominal portfolios.

Market expectations

As for market expectations on cash rates, like most observers I think they are a bit too high.

I think they will get to 2% this year, not 2.7%.

By mid next year inflation should be moderating, so it’s unlikely they will need to push above 3%.

Needless to say the mortgage fixed-rate cliff and variable rates 3% higher should be enough to drop the economy down a few gears. We get wage and employment data in the days ahead which will again recalibrate expectations.

About Tim Hext and Pendal’s Income & Fixed Interest boutique

Tim Hext is a Pendal portfolio manager and head of government bond strategies in our Income and Fixed Interest team.

Tim has extensive experience in banking, financial markets and funding including senior positions with NSW Treasury Corporation (TCorp), Westpac Treasury, Commonwealth Bank of Australia, Deutsche Bank, Bain & Co and Swiss Bank Corporation.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia.

Find out more about Pendal’s fixed interest strategies here

About Pendal

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

In 2023, Pendal became part of Perpetual Limited (ASX:PPT), bringing together two of Australia’s most respected active asset management brands to create a global leader in multi-boutique asset management with autonomous, world-class investment capabilities and a growing leadership position in ESG.