Here are the main factors driving the ASX this week according to our head of equities Crispin Murray. Reported by portfolio specialist Chris Adams.

Find out about Crispin’s Pendal Focus Australian Share Fund

Find out about Crispin’s sustainable Pendal Horizon Fund

SEVERAL themes are emerging from Australia’s reporting season:

- The Australian economy is in good shape with a strong outlook

- Companies that have been challenged for some time by Covid disruptions are responding well and positively surprising the market

- Labour availability and inventory management have been a challenge for some companies

- US-based businesses are seeking to put through material price rises

Globally, the valuation de-rating of growth companies and concern over the Ukraine weighed on equity markets last week. The S&P 500 fell 1.5% and the NASDAQ was down 1.7%.

A generally good menu of corporate results helped support the local market, which ended up 0.2%.

Year to date, the S&P/ASX 300 is -2.9% versus -8.6% for the S&P 500 and -13.3% for the NASDAQ.

This week’s action underpins our view that Australian equities are generally more defensive in the current environment.

Macro-economic news

Inflation

There was little newsflow last week. Our view remains that financial conditions — including asset markets — need to tighten further for any real chance of inflation cooling.

Headline inflation data may moderate in coming months due to the base effect. But US economic momentum looks to be strengthening.

Pendal Focus Australian Share Fund

Now rated at the highest level by Lonsec, Morningstar and Zenith

For example, company survey data from researcher Evercore ISI indicates the US economy continues to pick up following the most recent Covid wave.

This is supported by Bank of America credit card data and air travel sales. Housing is staying resilient despite mortgage rates moving higher. This may reflect pent-up demand and supply constraints.

Meanwhile monetary policy remains loose. This is not consistent with the need to bring inflation down, which is becoming a political imperative given the mid-term elections in November.

Fed Chair Powell is still yet to be officially confirmed for another term. The process has been delayed by wrangling in the Senate over the appointment of Sarah Bloom Raskin to a key regulatory role at the Fed.

If this situation drags on it raises an outlying risk that Powell may not be confirmed if he is failing to quell inflation. This is arguably putting more than the usual political pressure on the Fed.

Ukraine

There are two very different perspectives on the Russia-Ukraine stand-off.

The first is that Putin is almost certain to invade in the next couple of weeks and is trying to engineer a pretence to do so via claims of an unwarranted act from Ukraine.

The other is that the US is overstating the risk to put pressure on Putin and reframe Biden’s image.

The outcome remains to be seen.

Sustainable and

Responsible Investments

Fund Manager of the Year

History suggests any sell-off in risk assets in response to military action will be relatively short lived.

If a solution is found, it could see the oil price back down to about $80 very quickly — particularly if the market starts to price in the possibility of a new deal with Iran.

This would give Biden some relief on the inflation issue, with high fuel prices becoming an acute political problem.

Australia

The domestic economic looks primed for a period of strength thanks to a combination of:

- Pent-up demand supported by excess savings

- Border re-opening as cases numbers fall

- Labour market and wage strength

- Renewal of immigration

- Policy — rates remain low and we are likely to see a stimulatory pre-election budget

Employment-to-population ratios continue to climb. There is little evidence of the “great resignation” seen in the US.

The job market also looks strong, based on Seek’s job ads data, which continues to climb to 10-year highs.

Immigration is also recovering quite quickly, helped by a near-term boost from returning students.

This all bodes well for aggregate corporate earnings, which can help protect the domestic equity market from the valuation de-rating seen elsewhere.

Markets

The rotation away from growth continues.

Speculative tech names declined again after a recent small bounce. Meanwhile mining stocks continue to climb.

It was interesting to note some positive noise on gold last week. The gold price is up 5.8% for the month and has broken out a recent technical range, helped by geopolitical concerns.

This needs to be watched. Gold miners have been material underperformers for almost two years and when they do run, they tend to do so sharply.

There is a lot of debate on the link between real rates and gold. There has been a strong negative correlation in recent years (as real rates rise, gold underperforms). This has helped entrench bearish sentiment recently.

There is an argument that relationship held in the Quantitative Easing era where gold was a hedge against deflation.

Now there is a view we may see correlations between gold and real rates return to the pre-GFC era, when gold was held as a hedge against inflation.

Flows in gold ETFs are only now just beginning to turn positive, so sentiment is not over extended. Iron ore fell 11.8% as Beijing clamped down on speculative activity by traders. But underlying demand and economy strength appear to be constructive, supporting a price in the low US$100 range.

About Crispin Murray and Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia. Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Wages are the next battleground for policy. Pendal’s TIM HEXT explains how it will play out and what it means for investors

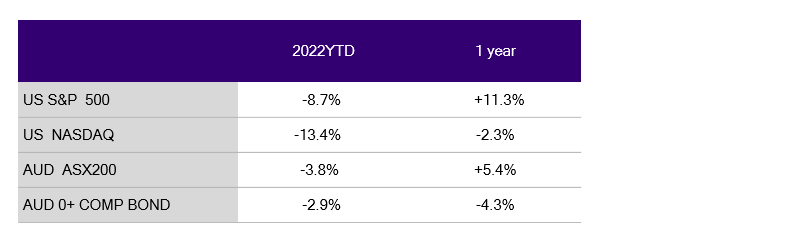

THE upcoming federal election will determine if it’s a good year for the Australian Labor Party, which for some reason adopted the US spelling more than a century ago.

No matter the election result, it will finally be a good year for labour at least.

This year has not started well for asset owners, though a late 2021 surge means the one-year picture is better.

Here are the returns in AUD:

Of course these are nominal returns. If we look at it in real returns (including inflation) the picture is 3.5% worse. Spending power is going backwards.

This week we are seeing further evidence of the next battleground for policy — wages.

Wages will be under pressure on two fronts.

Firstly, workers who are feeling cost-of-living pressures are more likely to push for higher increases.

Secondly, there is a window in Australia we have not seen for a very long time where limited migration means worker shortages. Unions are not going to miss their chance.

Teachers and nurses have already begun their bargaining dance and transport workers have now joined them.

Expect a lot more of this as the NSW government (and others) 2.5% wage policy comes under attack. First introduced by Mike Baird a decade ago they got away with it given private sector wages were 2.5% or even lower.

The next year or even two will not be that kind. Collective agreements and awards underpin the majority of wages.

Watching with keen interest will be the RBA.

Wages are the ultimate lagging indicator but the clock is now ticking.

We think the market will be right about rate rises this year, likely beginning in August — though five hikes is probably one too far.

It is important to keep some perspective though. If by December we have a strong economy, wages at 3.5%, unemployment at 3.5% and inflation at 3% then it should be smiles all round.

Capital has had a much better decade — even during Covid — than labour. So a reversal for several years should be applauded.

Ultimately a strong economy, spurred on by pent-up savings and re-openings, should mean risk markets take rate hikes in their stride.

Mistakes happen late cycle and that will be a number of years away.

Investors should take advantage of higher bond yields in the next few years to start building up some defensive positions.

At 2.5% (zero real yields plus 2.5% inflation) I will stop calling bonds expensive.

History suggests, though, it is too early to call them cheap.

Find out about

Pendal’s Income and Fixed Interest funds

About Tim Hext and Pendal’s Income & Fixed Interest boutique

Tim Hext is a Pendal portfolio manager and head of government bond strategies in our Income and Fixed Interest team.

Tim has extensive experience in banking, financial markets and funding including senior positions with NSW Treasury Corporation (TCorp), Westpac Treasury, Commonwealth Bank of Australia, Deutsche Bank, Bain & Co and Swiss Bank Corporation.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia.

Find out more about Pendal’s fixed interest strategies here

About Pendal

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

In 2023, Pendal became part of Perpetual Limited (ASX:PPT), bringing together two of Australia’s most respected active asset management brands to create a global leader in multi-boutique asset management with autonomous, world-class investment capabilities and a growing leadership position in ESG.

The US Federal Reserve is expected to start raising rates next month. Pendal’s TIM HEXT explains how the rate hike cycle is likely to play out in Australia

The March 16 US Federal Reserve meeting is now a month away.

A tightening is a given. Market pricing suggests 50bp to get things started and then 25bp every meeting this year (there are another six).

If correct this would mean it will take less than a year to get back to almost 2.5%. It took three years in the last hiking cycle (Dec15-Dec18).

Obviously 7.5% inflation focuses a central banker’s mind and stopping to see if hikes are working along the way is not on the cards.

The US Fed has often done this as Greenspan showed in the 2004 to 2006 relentless hiking cycle.

This is partly because the US largely has a long-dated fixed rate mortgage market, so cash rates have less importance.

Overall, financial conditions are more influenced by long-term interest rates which may or may not go up with rate hikes.

In the 2004 to 2006 cycle cash rates went from 1% to 5% but 10-year bonds from only 4% to 5%.

What about us?

Australia is very different.

Rate hikes are passed on almost instantly. Traditionally, floating rates make up 80% of the market, though recently that fell to 50%.

However most of the wall of fixed rates from last year will roll off in 2023, offering only limited respite.

Find out about

Pendal’s Income and Fixed Interest funds

Therefore the RBA is more likely to move more cautiously.

Like my local bus service, rate moves tend to come in twos.

This year that should be August and September and then November and December. This at least gives a little time to see the impact on housing and confidence.

The next CPI, due in late April, will again be strong but with an election and post-election uncertainty (hung parliament anyone?) the RBA will likely wait till after the Q2 CPI in July.

Strangely enough that CPI could offer some inflation respite. Goods prices will be tapering by then and a childcare subsidy will knock 0.3% off headline CPI.

What comes next

Attention now turns to the terminal rate — in other words how high do cash rates need to go to slow the economy enough to bring inflation back to target and GDP growth back to capacity.

Nirvana for the RBA would be inflation at 2.5%, GDP growth at 3% and wages growth at 3.5%.

I wrote about this in our last quarterly report, but it’s fair to say a zero real rate and 2.5% inflation rate leads to 2.5% as a reasonable estimate.

A lot would need to go right before we get there but this decade feels different to the last, mainly due to fiscal policy being unleashed.

Finally, asset owners should start thinking about where they get back into fixed interest markets.

Bonds are a defensive instrument but the last few years it has been hard to avoid the awkward fact that they were expensive on any long-term measures.

Back above 2.5% though this changes and we expect some rebalancing back into bonds for long-term asset owners, especially those managing retirement incomes.

About Tim Hext and Pendal’s Income & Fixed Interest boutique

Tim Hext is a Pendal portfolio manager and head of government bond strategies in our Income and Fixed Interest team.

Tim has extensive experience in banking, financial markets and funding including senior positions with NSW Treasury Corporation (TCorp), Westpac Treasury, Commonwealth Bank of Australia, Deutsche Bank, Bain & Co and Swiss Bank Corporation.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia.

Find out more about Pendal’s fixed interest strategies here

About Pendal

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

In 2023, Pendal became part of Perpetual Limited (ASX:PPT), bringing together two of Australia’s most respected active asset management brands to create a global leader in multi-boutique asset management with autonomous, world-class investment capabilities and a growing leadership position in ESG.

Here are the main factors driving the ASX this week according to our head of equities Crispin Murray. Reported by portfolio specialist Chris Adams.

Find out about Crispin’s Pendal Focus Australian Share Fund

Find out about Crispin’s sustainable Pendal Horizon Fund

THE challenge for central banks — particularly in the US — is that the economy is growing well above trend, with little slack in labour markets.

They need to engineer a tightening of financial conditions to resolve this and at least slow the economy back to trend growth rates.

This is yet to be achieved, which means they need markets to adjust further.

This is why we remain wary of equity markets in the near term. We are not expecting a major bear market, but believe we remain in a correction phase.

We also remain mindful that Australian equities should fare better than the US, reflecting its sector mix and less need to tighten. The S&P/ASX 300 is down 3.2% year-to-date versus -7.2% for the S&P 500 and -11.8% for the NASDAQ.

US inflation data came in higher than expected last week. In combination with further evidence of wage pressure, this saw an increase in the number of expected US rate hikes this year.

Concerns over the Russia-Ukraine crisis also drove oil prices higher, adding to future inflationary pressure as well as geopolitical risk.

Pendal Focus Australian Share Fund

Now rated at the highest level by Lonsec, Morningstar and Zenith

The S&P 500 fell 1.8% and the NASDAQ lost 2.2% last week. Australia fared better with the S&P/ASX 300 up 1.3%.

This was partly a catch-up on the overseas rally in the previous week, but also reflected reasonable results in the local financial sector.

Economics and policy

US inflation data came in worse than expected last week. Headline CPI was at 7.5% and the underlying core measure at 6% annual growth.

Current consensus is a peak of 7.9% headline and 6.4% core inflation in February. The latter would be the highest reading since 1984. It is then expected to ease as a result of base effects and easing supply chain pressure.

Prices of goods have been rising at 11% annualised, which has been the key driver of inflation. For example, of the 6% growth in core CPI, a disproportionately large 2.7% is coming from used cars and new vehicles.

The unwinding of components such as these are underpinning expectations of a deceleration in inflation after February.

However we are also seeing services inflation start to rise, reaching its highest levels since 2007. The pathway here will be something to watch.

There is also a broadening of inflationary factors. The median three-month CPI component is running at an annualised rate of 5.9% — its highest level since data was first recorded in 1983.

Key components such as rents (17% of the core PCE index) are yet to rise since measured rent is below signals of what spot rents are doing. For example, the Zillow measure of rents is up close to 14% versus the 4% in the PCE calculation.

This is all adding to concern that inflation may prove harder to contain.

Concerns over the threat of a wage-price spiral was reinforced by the Atlanta wage tracker, which moved over 5% annualised growth, the highest level in 20 years.

Sustainable and

Responsible Investments

Fund Manager of the Year

The issue here is one of the pathway and changing expectations. The market is still implying that annualised inflation drops below 3% by the end of 2022. There are reasons to be wary of this expectation:

- The US economy is growing well above trend (nominal GDP >10%)

- Commodity prices are still rising

- The housing market remains strong

- Labour market are very tight

- Real wages are declining, requiring labour to seek increases to catch up

- Money supply growth is still well over 10%

- Real rates still negative

- Companies are clearly stating a need to push prices higher to compensate for higher costs.

The key point is the size of the disconnection between policy conditions and the economic environment.

We can see this in the Goldman Sachs Financial Conditions Index which captures contributing factors beyond just rates. This remains at a 39-year low.

This stance is grounded in the view that inflation will fall as supply chains improve; high levels of debt mean the economy will be sensitive to small adjustments in rates; and the belief that real rates can stay negative.

This means central banks need to do more to drive bond yields, the US dollar and credit spreads higher and/or equities lower – since these are all contributors to total financial conditions. This means either tightening faster than expected or going higher than expected – or seeing signs that the economy is rolling over quicker than expected.

None of these scenarios are benign for any asset class, though within equities there is scope for variance in outcomes.

With real rates still needing to move higher, this remains a difficult environment for growth stocks. So shorter duration, cash generating names will be more defensive which we have seen in the Australian market this week.

Part of the reason equities can be a bit more defensive is that equity risk premiums have stayed at reasonable levels through this cycle.

A more positive data point was that Chinese loan growth was larger than expected. This reflected more issuance of local government bonds which are likely to underwrite greater infrastructure spend in China over the next few months.

The Chinese economy remains fragile, particularly the small-to-medium enterprise (SME) sector. However this should lead further easing of policy — with two key policy meetings towards the end of March — which can help underpin the resource sector.

Markets

Resources and financials helped the market last week. They are leading to an emerging theme of large cap outperformance.

About Crispin Murray and Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia. Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Australia’s national border will finally re-open on February 21. TIM HEXT explains how the economy will respond

THIS week brought news of the re-opening of our borders on February 21 – to fully vaccinated visitors anyway.

Fingers crossed Covid does not bring new surprises.

It will take time for business-as-usual to resume. We will be watching numbers closely to see if it’s a trickle or flood — or more likely something in between.

The surge in inflation over the past year has been led more by supply side than demand side — so this should potentially bring some relief in labour markets over time.

Globally, goods supply bottle-necks should also ease, though not as quickly as some would hope.

So where does this leave inflation? Well, it’s complicated.

Goods markets inflation is likely already peaking about now. An increase in labour supply should reduce wage pressures over the medium term, but 2022 should still see a sellers (employee) market.

On the other side housing inflation (particularly rents) will likely pick up again with population growth.

Find out about

Pendal’s Income and Fixed Interest funds

In most locations the flat-lining of the population has masked an under-supply of housing. This could again become an issue by 2023.

Inflation will ebb and flow in 2022 before settling down in the medium term not too far from the RBA target.

Longer term we stand by the view that inflation will be structurally around 1% higher this decade than last – nearer 2.5% than 1.5%.

Unfortunately market pricing is already there so the opportunity that markets gave us in 2021 is largely gone.

Our attention has now turned to the path of real yields as the big story in 2022.

(My colleague Amy Xie Patrick has just recorded a short podcast on this).

A combination of surging business investment, reduced monetary stimulus and sustainability initiatives should see real rates get back to zero over the year.

This will put upward pressure on yields, though for now they have probably moved enough.

The RBA will take comfort from the border re-opening.

I suggest unions and employees in general take advantage of the current squeeze to lock in some decent wage hikes now, for the years ahead.

About Tim Hext and Pendal’s Income & Fixed Interest boutique

Tim Hext is a Pendal portfolio manager and head of government bond strategies in our Income and Fixed Interest team.

Tim has extensive experience in banking, financial markets and funding including senior positions with NSW Treasury Corporation (TCorp), Westpac Treasury, Commonwealth Bank of Australia, Deutsche Bank, Bain & Co and Swiss Bank Corporation.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia.

Find out more about Pendal’s fixed interest strategies here

About Pendal

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

In 2023, Pendal became part of Perpetual Limited (ASX:PPT), bringing together two of Australia’s most respected active asset management brands to create a global leader in multi-boutique asset management with autonomous, world-class investment capabilities and a growing leadership position in ESG.

Here are the main factors driving the ASX this week according to our head of equities Crispin Murray. Reported by portfolio specialist Chris Adams.

Find out about Crispin’s Pendal Focus Australian Share Fund

Find out about Crispin’s sustainable Pendal Horizon Fund

EQUITY markets bounced last week after overselling — but underlying news flow indicates further tightening, which remains a headwind for markets:

- Both the European Central Bank and the Bank of England signalled a more hawkish policy direction

- US employment and average earnings growth were far stronger than expected

- Oil prices continue to rise as “OPEC Plus” nations signalled they were sticking to their plan despite high oil prices

- US bond yields hit new cycle highs; the 10-year government bond yield reached 1.92%

The S&P/ASX 300 gained 2% and the S&P 500 1.6% last week.

So far this year the latter is now down 5.5% and the NASDAQ has lost 9.8%. The S&P/ASX is down 4.5%, reinforcing our view that the Australian market should be more defensive in this environment.

The first three weeks of January saw hedge funds de-leveraging and the market cutting growth positions. This phase has played out for now. The market is likely to be more focused on earnings in the near term.

The bull case from here relies on slowing growth and easing supply chain pressure resolving the inflationary pressures without requiring a significant economic slowdown.

The bear case is that rates are still low, inflationary pressures are rising (oil, wages, rents, company pricing power) and the market begins to raise its view on where terminal rates are.

Last week’s news flow shifts probability to the latter. We think the market’s expectations are still playing out. Hence we remain cautious in the near term.

One CEO we spoke to last week said companies could not rely on the hope that inflationary was transitory.

They needed to act as though inflation was here to stay — which meant price increases.

Pendal Focus Australian Share Fund

Now rated at the highest level by Lonsec, Morningstar and Zenith

If most companies are thinking this way it means more inflationary pressure is in the pipeline.

The market also seems to be more discerning now the initial de-risking has played out.

We saw this in the divergence between Facebook and Amazon last week. Features such as pricing power, control over costs, earnings predictability, strong cash flow, low gearing and the ability to do capital management are likely to be rewarded in this environment.

This reinforces our view that in 2022 beta could be lower than previous years and alpha will be a major differentiator.

Policy and economics

The key notion underpinning central bank thinking is the realisation that the combination of emergency policy measures, substantial fiscal expansion and supply chain disruption has triggered a significant rise in inflation — and they need to stop stimulating as quickly as possible.

This means normalising rates in a shorter timeframe than previously thought. The next step would be an increase in the terminal rates they are targeting, though we are not seeing this yet.

European Central Bank

President Christine Lagarde followed the Fed’s suit as the ECB made a sharp hawkish turn in tone. The bank removed references to rate increases this year being “highly unlikely” and emphasised the strength of the economy.

This is in response to year-on-year Eurozone inflation rising to 5.3% and a shift upwards in longer-term inflationary expectations 2%.

The fact that interest rates sit at -0.5% highlights the disconnection between policy and the underlying economy.

The consensus expects an announcement in March that Quantitative Easing ends from June. This suggests EUR200 billion less QE in 2022 versus 2021 and rate hikes to follow in September and December.

This triggered a sell-off in European bonds. German Bund yields increased from 0% to 0.2% and the Euro rose against other currencies.

Sustainable and

Responsible Investments

Fund Manager of the Year

Bank of England

The BoE has been the most hawkish of the major central banks, raising rates 25bp with four out of nine members calling for a 50bp hike. It also announced quantitative tightening.

This highlights a policy of front-ending tightening and reflects the wage pressure that is already evident (it’s forecast to hit 5% for 2022).

The BoE is effectively prepared to break the economy’s strong growth to reduce the hit to real incomes form inflation and power price increases.

This is something to be mindful of for UK-exposed companies on the ASX this year. The GBP also sold off versus the EUR.

US employment

US payrolls came in at +467,000 new jobs versus +125,000 expected. This strong number was reinforced by material positive revisions to recent months and resilient average earnings data.

All this highlights that the Omicron wave has had limited impact on the economy and makes the Fed’s job of slowing inflationary pressures harder.

There was also a significant re-allocation of jobs in 2021. This reflects a shift in seasonal adjustments which meant the labour market was growing far more consistently through the year than previously thought.

Compared to previous recessions, the unemployment rate has returned to original levels far more quickly after the post-Covid shock. But the impact on the participation rate is far worse.

While the initial decline in participation was greatest in the 16-24 year age cohort, it is now evenly spread across all age cohorts.

It is impossible to isolate the drivers. But key contributors are considered to be rising wealth, a desire to change careers leading to re-training and education, health considerations and lifestyle choices. Whatever the reasons, it is creating a substantial labour bottleneck, driving wages higher.

Data released in the US last week shows civilian worker wages are up 4% from last year.

Another survey showed all private-sector wage growth of 5%, while leisure and hospitality wages were up 8.9% year-on-year. Wage growth is critical to watch. It is the factor that can turn supply chain inflation into more structural inflation

The bottom line is that pressures driving inflation are not yet showing any signs of abating.

Covid outlook

New case number and hospitalisations continue to fall. The BA.2 variant appears to be 30% more transmissible, but no more severe.

The US has seen case numbers halve and hospitalisations fall 25%. Fatalities have fallen 80%, mostly due to immunity that has built up in the community from vaccines and prior infections. The death rate among those who have had vaccine boosters is 99% lower than the unvaccinated.

The ability for health systems to largely weather the Omicron wave is likely to reduce the use of restrictions in future waves. We should now see a re-opening boost heading into the northern hemisphere spring.

Markets

Brent crude rose 1.2% last week and was up after the “OPEC plus” meeting.

It is now at its highest point since 2014. The Australian dollar oil price is almost back to its 2008 peak.

Oil inventories are below pre-Covid levels.

It is hard to see what might change this, given continued demand recovery, OPEC sticking to careful supply increases, some concern they are limited in their ability to respond and the ESG overlay combined with a steep backwardation limiting new supply. All this adds to the inflationary pressure still in the economy.

The credit markets serve as indicators of stress in the economy. Spreads have widened but are nowhere near the stress we saw in the 2020 sell-off. This reflects good economic growth, cheap and available funding, and lower corporate gearing.

The market also watches the yield curve, which continues to flatten. Higher yields generally mean lower P/E ratings for equities and underperformance of growth stocks. This is a very different environment to what we have seen for the last few years.

In this vein, it was interesting to note the divergence in stock performance in the US last week.

The FAANGM stocks are longer performing in unison. Stock analysis and stock picking are becoming increasingly important since relentlessly increasing valuation ratings no longer overwhelm earnings trends.

About Crispin Murray and Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia. Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

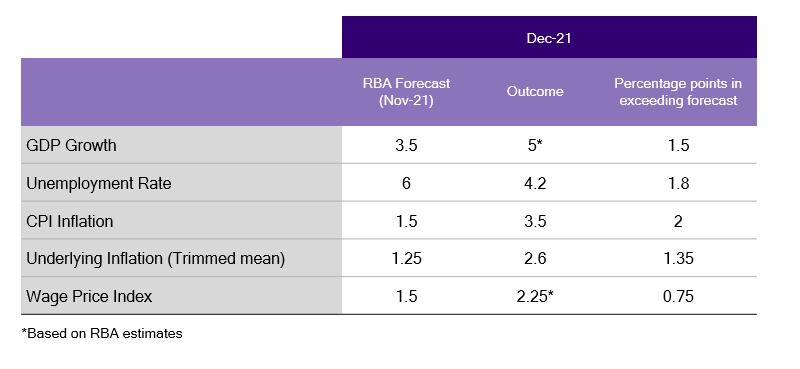

What are the implications for investors from this week’s RBA statement? Where might Dr Lowe go next? Pendal’s ANNA HONG explains

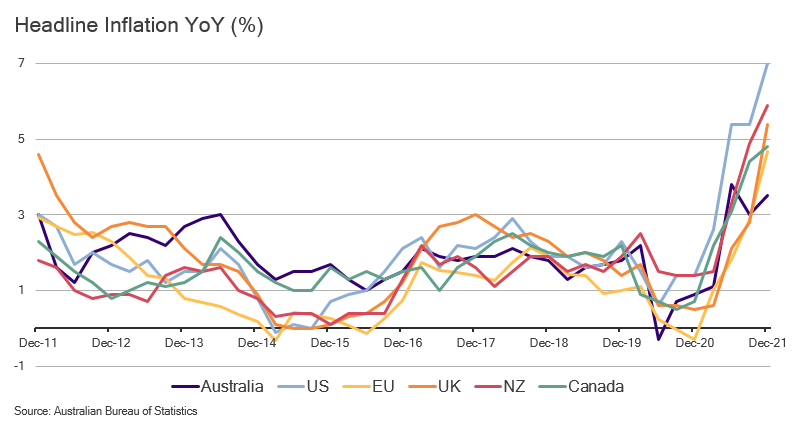

ON A global scale, the picture looks pretty clear — inflation is here.

Here is a comparison of year-on-year headline inflation growth:

- United States 7%

- United Kingdom 5.4%

- Eurozone 4.7%

- Canada 4.8%

- New Zealand 5.9%

- Australia 3.5%

Australian inflation appears modest in comparison to other regions.

But after the RBA has repeatedly reiterated a target inflation band of 2% to 3%, the market is understandably confused.

As you can see below, actual data for Q4 2021 exceeded that target — and the RBA is forecasting inflation in the higher part of the target range through to 2024.

Yet the Reserve is saying “no rate hike in the near-term”.

Never before has the RBA been so wrong, so quickly.

This week the central bank was forced to revise its February forecasts to match the market since the data showed that the market was correct.

That led to a stand-off on Tuesday after the RBA statement. The front end of the yield curve rallied but without commitment. Yes, lower for just a bit longer…wait, but how much longer?

The RBA provided a few breadcrumbs for the market to follow.

Dr Lowe’s National Press Club speech made it clear the Reserve was not working off “a specific definition as to what ‘sustainably in the target range’ means”.

It will depend instead on the rate, trajectory, outlook, and drivers of the inflation. In a nutshell – it will be all be about wages.

Why do wages keep Dr Lowe up at night?

In the past 10 years wages growth alongside goods prices have been the main reasons inflation stayed below target.

The RBA appears to be pre-empting the dampening effects of the border re-opening.

It remains worried about the impact on wages if the number of temporary visa holders returns to the pre-pandemic levels. See graphs below.

What are the implications?

The RBA’s preparedness to miss the Q1 and probably Q2 global rate hike party, means conditions for mortgage holders, share markets and owners of short bonds remain supportive.

The picture for long bonds is less clear.

We expect real rates to rise in the months ahead, which is very likely to move nominal yields higher as well.

About Anna Hong and Pendal’s Income and Fixed Interest team

Anna Hong is an assistant portfolio manager with Pendal’s Income and Fixed Interest team.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia. In 2020 the team won the Australian Fixed Interest category in the Zenith awards.

With the goal of building the most defensive line of funds in Australia, the team oversees A$22 billion invested across income, composite, pure alpha, global and Australian government strategies.

Find out more about Pendal’s fixed interest strategies here

About Pendal Group

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

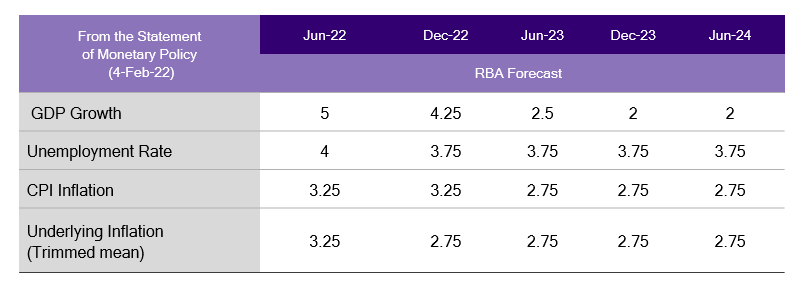

The Reserve Bank of Australia has confirmed its shift from hawk to dove — and savers will be going further backwards, says Pendal’s TIM HEXT

FOR most of modern inflation targeting, introduced in 1993, the RBA has leaned on the hawkish side — quick to hike when inflation loomed, slower to cut when it fell.

For years inflation languished below 2% and rates were slowly and reluctantly reduced.

However Covid has brought about a major reset at the RBA.

The Reserve is now possibly the most dovish of the developed market central banks and seems prepared to be one of the few to sit out inflation-led hikes.

Then again, they might argue Australia’s 3.5% inflation (in the US it has been nudging 7%) means there is less need for speed here.

The February statement did see the RBA cut its losses on some woefully low inflation forecasts.

The Reserve now expects underlying inflation to be 3.25% this year and 2.75% in 2023.

Unemployment is expected below 4% this year… we are likely almost there now. Full employment is here.

With these new forecasts you may be forgiven for thinking the RBA would conclude inflation was sustainably within its 2-3% band. Well think again.

Referring to inflation at the end of the statement, the RBA says it’s “too early to conclude that it is sustainably within the target band”.

Everyone stand down, time is on our side.

They then cite wages and supply side problems as items to watch in 2022.

Find out about

Pendal’s Income and Fixed Interest funds

Clearly having been so wrong in recent forecasts, they are loathe to jump on board now.

Having only recently assured everyone rates weren’t likely to move in 2022, they don’t want to do a sharp turn.

But what we can really conclude is that the RBA is happy to sit out global rate hikes for now — and certainly doesn’t feel it is behind the curve.

Time will tell.

It’s great news for mortgage holders, share markets and holders of short bonds.

It’s more mixed for long bonds.

Not great news for the AUD. And definitely not great news for savers who are going backwards, seeing prices go up by 3% a year but savings flat-line.

About Tim Hext and Pendal’s Income & Fixed Interest boutique

Tim Hext is a Pendal portfolio manager and head of government bond strategies in our Income and Fixed Interest team.

Tim has extensive experience in banking, financial markets and funding including senior positions with NSW Treasury Corporation (TCorp), Westpac Treasury, Commonwealth Bank of Australia, Deutsche Bank, Bain & Co and Swiss Bank Corporation.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia.

Find out more about Pendal’s fixed interest strategies here

About Pendal

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

In 2023, Pendal became part of Perpetual Limited (ASX:PPT), bringing together two of Australia’s most respected active asset management brands to create a global leader in multi-boutique asset management with autonomous, world-class investment capabilities and a growing leadership position in ESG.

Here are the main factors driving the ASX this week according to our head of equities Crispin Murray. Reported by portfolio specialist Chris Adams.

Find out about Crispin’s Pendal Focus Australian Share Fund

Find out about Crispin’s sustainable Pendal Horizon Fund

LAST week’s Fed statement was bland, but the press conference that followed was not.

Fed chair Jerome Powell did not deliver a soothing message and the more hawkish tone of his comments raised market expectations around monetary tightening.

The bond yield curve flattened, the US dollar rallied and the US equity market fell in response. However a rebound on Friday saw the S&P 500 finish the week up 0.8%.

The Australian equity market rode the same wave, with the additional distortion of BHP’s index re-weighting exaggerating swings. The S&P/ASX 300 ended down 2.8%.

We remain cautious in the near term. The withdrawal of liquidity combined with the Fed’s aim of slowing economic growth suggests there may yet be more downside.

But we also expect markets to be punctuated by sharp bounce backs as we saw on Friday. This is partly because selling is amplified by the effect of investor hedging, which then unwinds.

It’s important to keep a close watch on the trifecta of rates, oil prices and the US dollar. When all three are rising it usually means a stiff headwind for equities.

However the underlying growth environment remains strong and supportive of earnings. The selling has also been largely indiscriminate, ultimately driving good alpha opportunities.

The Fed’s hawkish message

Chair Powell struck a hawkish tone in his press conference, prompting a sell-off in two-year notes and a flattening of the yield curve. His key messages were:

- This tightening cycle is very different to the last one in 2018. Back then higher rates quickly led to a slump in economic activity and the need for a swift “pivot”. This time inflation is higher, the employment market tighter and the economy stronger. As a result more tightening will be needed.

- The risk is to the upside in terms of the Fed’s inflation expectations.

- The prospect of rate rises is “live” at every meeting this year. This could imply more than the four hikes previously expected.

- The Fed remains data dependent. This has been a consistent message, but the nuance is that their bias is now towards tightening. They would need to see sufficient evidence of slowing to change tack.

- Rates will be the primary tool for tightening. There had been some debate that quantitative tightening would play a larger role to help manage the risk of an inverted yield curve. But the Fed is now clearly saying it needs to see rates higher.

Pendal Focus Australian Share Fund

Now rated at the highest level by Lonsec, Morningstar and Zenith

The market has moved to price in five hikes in response.

The March, May, June, September and December meetings are expected to yield rate rises. At this point the market expects quantitative tightening to begin at the July meeting, while the November meeting coincides with mid-term elections.

The market suspects there will be evidence of a slowing economy or inflation (or both) by that point.

The market is not used to such frequent hiking. But this should be considered in the context of the very low starting point and the fact that monetary policy is still likely to be stimulatory until we go beyond a 2% rate.

The Fed’s goal is to stop stimulating an economy that does not require it. It is looking to get rates back to a “neutral” setting of 2% to 2.5% and shrink the balance sheet from US$9 trillion to US$6 trillion (it was US$3 trillion pre-pandemic).

The essential question – and driver of current uncertainty – is whether this will to be too much tightening or insufficient to achieve the Fed’s aim.

One way to consider this is that the risk balance is asymmetrical.

Higher inflation is considered to be a greater problem than over-tightening, since it would de-anchor inflation expectations and could require a recession for resolution.

It would also condemn Powell and the board to history as the team that lost control of inflation after four decades.

Given this, the goal outlined above is the point at which the Fed will believe they are not making the inflation problem any worse. If it transpires that they have over-tightened and the economy slows too much, they can quickly fall back and pivot as they did in January 2019.

The upshot is that the “Fed put” that helped underpin market confidence has shifted.

The market was conditioned to expect a soothing message from the Fed after equities fell some 10%. Now the perception seems to be that it would take something closer to a 20% fall and widening credit spreads to prompt Fed intervention.

This shift in perception changes the mindset of the market.

The impact of rates on the economy

One of the key questions is how quickly rate rises would affect the economy.

There is a view that the high degree of leverage means small rate increases will affect the economy quickly. But as Chair Powell detailed, this cycle is different to the last. Specifically:

- US household leverage is much lower

- Banks are better capitalised and loan growth is picking up

- There is still a lot of surplus liquidity

- Employment and wages are stronger, supporting income growth

Academic analysis suggests that when you net off the negative for borrowers with the positive for savers, the impact of rates is very mild and only kicks in with a lag.

The impact on investment intentions is also likely to be minimal. Lower rates did not trigger substantially more investment and higher rates are unlikely to choke it off.

There is plenty to underpin a resilient outlook for business investment.

Sustainable and

Responsible Investments

Fund Manager of the Year

This includes the transition away from carbon, good pricing power, the need for more resilient supply chains, the need to deal with labour shortages and the effect of technology on business models.

The areas where tightening may have a disproportionate impact are sentiment and access to capital.

Aggregate financial conditions – how loose or tight an environment is – include not just the level of rates, but also money supply, equity markets, credit spreads, the US dollar and energy prices.

With the US dollar and oil rising as equities fall, we have already seen a meaningful tightening in financial conditions. In time this will begin flowing through to the real economy.

That said, we suspect pent-up Covid demand, the need for inventory re-build and tight labour markets will mean growth and inflation are more resilient.

Conditions also remain relatively loose in a historical context, compared to where we have been over the past decade.

Australian outlook

Australia had its own wake-up call with worse-than-expected quarterly inflation numbers.

The RBA’s preferred trimmed mean measure hit the middle of the 2% to 3% target band two years ahead of forecast.

Since rents, grocery items and new housing prices are all rising and supply constraints remain, it is hard to see inflation easing back.

Wage growth is running at just above 2% and the RBA believes wages rising more than 3% are necessary to be consistent with inflation staying in the target band.

Given the rigid Australian labour market, wages should be slower to rise than in the US, possibly giving the RBA cover to delay a rate hike beyond the market’s expectation of May.

That said, surveys indicate labour shortages and with unemployment falling and higher headline inflation, it is likely we will see wages move higher and the RBA raise rates.

As flagged last week, Australia is in a better place than the US in terms of the need to tighten. Inflation and wages are lower and we didn’t have the same degree of stimulus last year.

Australia is also among the more defensive equity markets at this stage of the cycle, given:

- The market composition is better suited to rising rates, with more financials and resources and less long-duration tech

- A lower valuation

- Less need for tightening

- A weaker currency

How Covid is impacting investors

Australian Covid-related mortality rates are at a high point, but the trend in new cases and hospitalisations is beginning to turn downwards. This is also the case in the UK and US.

In the latter, case numbers are down in 45 states. This is coinciding with evidence that retail and travel activity is beginning to pick up again following largely self-imposed lockdowns.

European cases are on the rise again.

Denmark, which was early into the Omicron wave, has seen a re-acceleration led by the Omicron Ba.2 sub-variant.

Early assessments suggest this sub-variant is about 1.5 times more transmissible than Omicron, but no more severe.

The UK has not seen a surge in the sub-variant yet. But if Denmark proves to be a lead for other countries, it will reinforce the disruption to the economy and supply chains.

Market outlook

The last leg of the US sell-off came with very high volumes, which signalled a degree of short-term capitulation as investors de-risked following a 7% drop.

Measures of the proportion of stocks declining are at extreme levels, suggesting the market may be oversold on a near-term view.

This could indicate a pause in the market, particularly given strength in recent economic data and what should be a constructive US earnings season.

We do not expect a sharp bounce-back at this stage and there is scope for further falls as rates begin to rise. At this point we remain wary of the degree of beta investors will want.

There was an interesting shift in equity markets last week.

As expectations around rates increased, long-duration growth stocks were underperforming. But as the Fed emphasised the goal of slower growth we saw more cyclical sectors hit last week.

In the global tech sector semiconductors had outperformed software by some 40% since October 2021. About a third of that move unwound last week.

Real-time surveys in the US highlight how consumers have become more cautious. Anecdotally this is also true in Australia, which could have a bearing on company outlooks in the upcoming earnings season.

This partly reflects the flattening yield curve but may also signal that the worst of the valuation de-rate in good quality software names is over.

A strong result from Microsoft highlighted strong enterprise demand for software as business models evolve. This is particularly material in the financial sector where the rise of the payment companies has sharpened the focus of banks.

The call between value and growth is more nuanced now.

Value’s outperformance over the past two months is in line with the vaccine-related rebound in late 2020 and early 2021.

But on a long-term basis the relative move still looks muted. Within value we are wary of the more cyclical end due to a backdrop of slowing growth and high leverage as credit spreads widen.

A final interesting observation: this is the first market sell-off to coincide with rising bond yields since the Quantitative Easing era started.

This reinforces the point Powell made about this cycle being different. It goes to the core issue that strategies that have worked in the past 11 years may not work this cycle.

There should be a lot of alpha opportunities in this type of market.

Largely indiscriminate macro-related selling means there has been little differentiation between stocks that are likely to reverse once strong fundamentals become evident, and those that will not.

We have been in a multi-year period where rating has been the dominant driver of returns. There is now the strong possibility that individual company earnings return to the fore.

About Crispin Murray and Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia. Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

What does today’s inflation spike mean for investors? Here’s a quick snapshot from Pendal’s head of government bond strategies TIM HEXT

THIS WEEK’S inflation numbers were extremely strong.

Headline at 1.3% on a quarterly basis and 3.5% annual. Underlying inflation at 1% or 2.6% annual.

Unusually there were almost no negative contributions.

New dwellings, food and fuel were the main drivers but the real surprise came from a wider range of goods which normally see little if any inflation.

Clothing, footwear, furnishings and a wide range of everyday items are going up by around 3 to 5% annually.

Some of that of course is supply related and might come down if things normalise later in the year. But for now that is all speculation.

The RBA once again has been railroaded on its forecasts and will need to address this number in next week’s meeting.

Find out about

Pendal’s Income and Fixed Interest funds

The only thing they can still hang their dovish hat on is wages — but given labour shortages that may move quicker in the year ahead.

Markets actually took the numbers in their stride.

That’s likely because most knew a higher number was a good chance — but also against the current backdrop of risk-off in equities and credit.

Four rate hikes are priced for 2022 with the first in May.

The RBA would have thought that too aggressive, but now may be forced to admit the market has been better at reading the economy.

Although this week’s numbers give support to concerns around inflation, we still don’t expect an unhinging of inflation from the medium term 2% to 3% band.

For investment markets that would not be a bad result.

After all, 2% to 3% is still considered low — and business investment and the economy in general can easily handle that.

About Tim Hext and Pendal’s Income & Fixed Interest boutique

Tim Hext is a Pendal portfolio manager and head of government bond strategies in our Income and Fixed Interest team.

Tim has extensive experience in banking, financial markets and funding including senior positions with NSW Treasury Corporation (TCorp), Westpac Treasury, Commonwealth Bank of Australia, Deutsche Bank, Bain & Co and Swiss Bank Corporation.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia.

Find out more about Pendal’s fixed interest strategies here

About Pendal

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

In 2023, Pendal became part of Perpetual Limited (ASX:PPT), bringing together two of Australia’s most respected active asset management brands to create a global leader in multi-boutique asset management with autonomous, world-class investment capabilities and a growing leadership position in ESG.