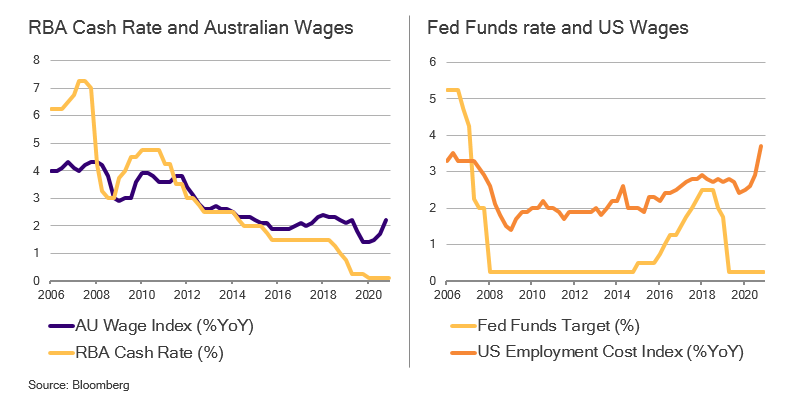

GLOBAL fixed income markets have been marching to a common theme lately.

Inflation data have been on an upward trend and there seems to be consensus that inflation will climb higher still.

Market pricing for rate rises from major central banks is outpacing what the policy makers themselves are saying.

Inflation will be going higher over the next couple of quarters. That theme is global since the driving forces behind the trend are global.

Supply chain disruptions coupled with higher goods demand have affected us all. As lockdowns lift and consumption normalises, there will be a handover from goods inflation to services inflation.

There is an assumption that rising wage pressures will be an equally global theme.

That is not the case. As RBA Assistant Governor Lucy Ellis pointed out this week, market fixation with labour market patterns offshore is leading to an overly optimistic outlook for wage developments in Australia.

Labour force participation rates in the US have been slow to recover since the depths of the pandemic. That same degree of sluggish return to work need not apply to Australia.

Initiatives such as JobKeeper have been instrumental in maintaining a link between employers and workers.

In the US, the fiscal response was aimed at generous unemployment benefits. So generous at first, in fact, that many workers chose to quit their jobs so they could access a better income stream.

Find out about

Pendal’s Income and Fixed Interest funds

Another difference is the health policy response in handling the pandemic.

In the US, despite attempts at various lockdown measures, Covid has unfortunately run rampant in the community. In Australia, a zero-Covid strategy until very recently has produced a far better population health outcome.

While the US vaccination rate seems to have stalled around the 60% mark, Australia’s vaccination rates continue to climb. New South Wales passed 92% this week.

For the US, this translates to slower re-entry into the labour force by workers who are still legitimately fearful of contracting the virus.

The resulting picture differs for wage pressures in Australia and the US.

Sure, both central banks are willing to let things run hotter for longer. But the heat is far more intense in the US.

Nevertheless, the market prices a matched pace of rate hikes for Australia and the US in 2022. Either the Fed will need outpace the market, or the RBA will prove the market wrong.

Higher yield prospects bring on more corporate issuance

Likely driven by the fear of rate hikes translating into higher refinancing rates next year, the pace of corporate issuance has been heavy so far this month, especially offshore.

European and US credit markets have seen higher-than-typical new issuance volumes in the past two weeks.

Despite continued inflows into both sectors, the supply deluge has been weighing on credit spreads — and hence the secondary market performance of many of these new deals.

In Australia the new issue pipeline has also been solid — about $3.5 billion of benchmark deals hit the market this week.

Issuers have ranged from utilities and banks to commercial and industrial real estate investment companies.

Contrary to the offshore credit climate, however, demand appetite remains very robust in Australia. Most deals have been able to price at the tighter end of price guidance and perform well in the secondary market.

Emerging market volatility

The higher yield environment would usually be a particular headache for emerging markets, especially accompanied by a climbing greenback and slowing China.

On the whole, emerging market hard currency sovereign debt has been resilient in the face of yield climbs so far this month, with yield-related widening in spreads broadly in line with global high yield.

This is because most emerging market central banks have been proactive and keenly aware of inflation pressures.

They have no desires to invite an ugly currency-inflation spiral. Moreover, the global economy is still in good shape, in spite of China’s property-driven slow-down.

The key driver of volatility for emerging market sovereign risk has been the volatility in Turkey and in particular around the currency.

This volatility stems from the Turkish’s president’s unorthodox views on the relationship between inflation and interest rates — and hence the high turnover of the leadership of the Turkish central bank.

A noteworthy improvement now versus the last Lira crisis in 2018 is the composition of the country’s external debt rollover risk.

A lot of the maturing debt is held by the government or institutions that have historically exhibited high roll-over rates even in times of crisis.

Our portfolios currently have no exposure to the Turkish Lira — or any other high-beta local emerging market risk.

Our income strategies employ a tactical allocation to the USD emerging market sovereign index. Turkey is a component of that.

We expect political developments in Turkey to continue punctuating sovereign credit spreads with bouts of volatility, but current market pricing is also compensating investors for that volatility.

Our exposure remains highly liquid and our investment process tunes into left-tail risks.

These are aspects of our investment philosophy that will help us to de-risk promptly and efficiently out of emerging markets when warranted.

About Amy Xie Patrick and Pendal’s Income and Fixed Interest team

Amy is Pendal’s Head of Income Strategies. She has extensive expertise and experience in emerging markets, global high yield and investment grade credit and holds an honours degree in economics from Cambridge University.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia. The team oversees some $20 billion invested across income, composite, pure alpha, global and Australian government strategies.

Find out more about Pendal’s fixed interest strategies here

About Pendal Group

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

Economics rather than environmentalism can explain much of the global renewables boom, says Regnan’s head of research, Alison George.

- Pollution, consumer preferences driving shift to renewables

- Economics are clear: renewables now cheapest in all key regions

- Pursuit of net zero would turbo-charge this trend

THE transition to a renewable energy system is a mega-trend that will drive investment returns for decades.

Renewables are expected to account for 70 per cent of the $US530 billion spent on all new generation capacity in 2021, says the International Energy Agency.

But with almost every part of the global economy touched by the transition, picking investment opportunities can be daunting.

Successful investing in the transition is made even more difficult by noisy debate and political point-scoring about the best path to net-zero carbon emissions.

But beyond the noise, much of global shift to renewable energy can be explained by underlying forces that are with us today and offer some quite understandable and investable opportunities, says Alison George, head of research at Regnan, a global leader in sustainable investing.

“There’s a whole lot of change happening in energy systems — all from three key drivers,” says George.

“Emissions are important, but in developing countries it’s air pollutants that are key to changes happening now, with climate concerns coming up behind.”

Then there’s changing consumer preferences and technological advancement.

Sustainable and

Responsible Investments

Fund Manager of the Year

“The shifts that are occurring in the energy system are a combination of those three factors playing out over time.”

Focusing on these three drivers can give investors a much clearer understanding of how the transition will affect their portfolios.

“In China and India, they are much more concerned with the very real problem of air pollution, which is causing significant numbers of extra deaths right now,” says George.

“Similarly, Australia’s love of home solar panels is not just about incentives — it’s about people liking the idea of being in control of their own power, playing to a personal independence narrative.

“It’s not just a decarbonisation preference — it’s a consumer preference.

“Historically energy was a low-engagement purchase, then all these apps came along so you can see how much power you are generating and connect it all up.”

George says the advancement in technology, which will ultimately allow households to trade energy the same way they trade stocks, via an app on their phone, will further drive the interest in renewables.

‘It’s not environmental, it’s economic’

Even global scale changes like the phasing out of coal-fired power stations can be explained by underlying economic drivers.

“Even without new commitments from governments, energy coal is already on the way out.

“It’s not environmental – it’s economic.

Find out about

Regnan Global Equity Impact Solutions Fund

“In the US there has been a huge changeover from coal to gas that was entirely economically driven because of the shale gas revolution.

“Suddenly the US had an abundant source of cheap gas and that has led to a lot of very economically rational coal to gas switching.”

This combination of an energy transition being driven by factors other than climate change allows investors to think differently about how they play the transition.

One implication is that the policy debate and regulatory overlay is perhaps less important than traditional economics.

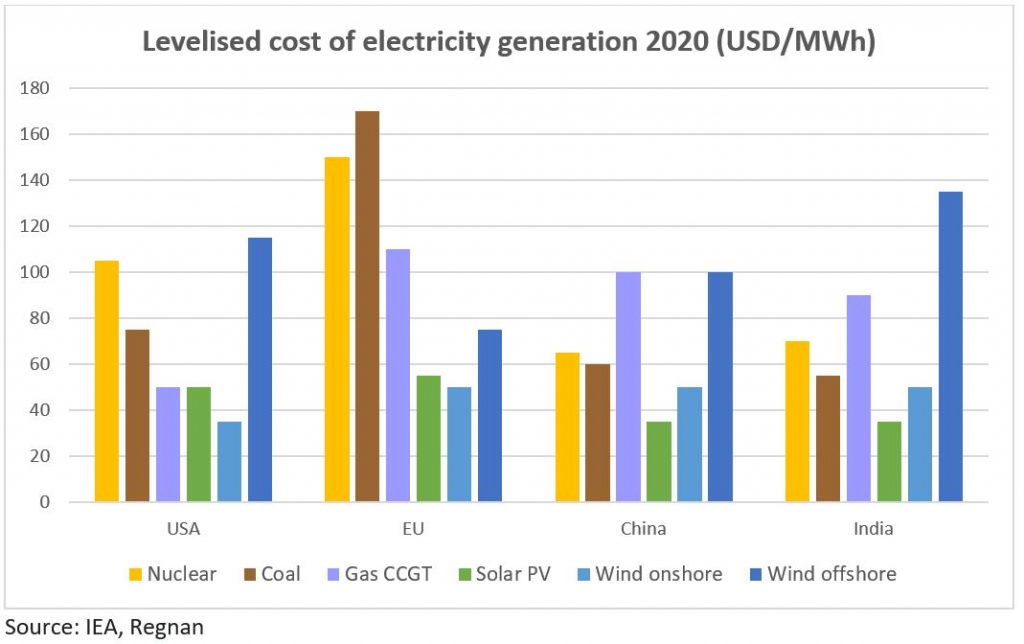

The International Energy Agency says renewable energy is now the cheapest way to lift energy production in all key regions.

“If you need more supply, the next megawatt will be renewable.

As the graph below shows, solar is the cheapest option in China and India. In the US and EU, it’s onshore wind.

The nuclear option

Economics also explain why nuclear is being left behind renewables, despite being low carbon, George says.

“Nuclear is expensive in relative terms, even in developing economies where input costs like labour and land are lower.”

That’s why nuclear doesn’t get much of a boost, even under the most ambitious decarbonisation scenarios.

“Renewables are already the best bet. It doesn’t matter what scenario we look at, renewable investment is a runaway car — it’s happening of its own accord.

“That is the key expectation that people should have.”

“Pursuit of net zero would only accelerate these trends, while also bringing hydrogen into the picture.

“There is a still a big gap between current policies and what is needed to achieve the net zero commitments being made by countries around the world.

“This represents a huge investment opportunity – worth a cumulative US$27 trillion by 2050 according to the IEA.

“Solar, wind and especially batteries would all be winners from increased environmental ambition, turbo charging current trends as more energy comes from electricity and renewables get a larger share of an even bigger electricity pie.

“Electricity networks would also require substantial increased investment.”

About Alison George

Alison George is Regnan’s head of research. She has deep experience in ESG, responsible investment and active ownership. Alison oversees Regnan’s research frameworks, processes and outputs, ensuring it remains at the forefront of industry practice and meets evolving clients needs.

About Regnan

Regnan is a responsible investment leader with a long and proud history of providing insight and advice to investors with an interest in long-term, broad-based or values-aligned performance.

Building on that expertise, in 2019 Regnan expanded into responsible investment funds management, backed by the considerable resources of Perpetual Group.

The Regnan Global Equity Impact Solutions Fund invests in mission-driven companies we believe are well placed to solve the world’s biggest problems.

The Regnan Credit Impact Trust (available in Australia only) invests in cash, fixed and floating rate securities where the proceeds create positive environmental and social change. Both funds are distributed by Perpetual Group in Australia.

Find out about Regnan Global Equity Impact Solutions Fund

Find out about Regnan Credit Impact Trust

For more information on these and other responsible investing strategies, contact Head of Regnan and Responsible Investment Distribution Jeremy Dean at jeremy.dean@regnan.com.

There are plenty of so-called ‘climate-aware’ companies to invest in — some 60 per cent of the ASX300 (by market cap) now have net zero commitments. But how do you judge the right ones? EDWINA MATTHEW explains

- Not all net zero commitments are the same

- Strategy and governance, disclosures and analysis of targets are critical, plus transition implications for workers

- Red flags include board sceptics, indirect impact from value chains and lack of progress

Some 60 per cent of the ASX300 (by market cap) now have net-zero commitments.

That’s a reflection of accelerating global progress on climate change.

Almost 90 per cent of global emissions are now covered by net-zero commitments from nations — up from about 75 per cent before the recent COP26 climate change conference.

Financial institutions are also forming initiatives — such as the Glasgow Financial Alliance for Net Zero announced at COP26 — to accelerate the transition away from fossil fuels.

So Australian investors have plenty of opportunity to invest in “climate-aware” companies.

The question is: how do you judge which companies are best placed to deliver on their net-zero commitments?

“Investors and the public are sceptical about the credibility and veracity of many net-zero commitments,” says Edwina Matthew, Head of Responsible Investments at Pendal Group.

“Investors need to ensure the companies they invest in are walking the talk.

“That means having a clear and credible climate strategy in place that is based on delivering actual real-world decarbonisation, and not just ‘virtual’ reductions from carbon offsets and asset divestment.”

Below Edwina lists some key things to look for.

Sustainable and

Responsible Investments

Fund Manager of the Year

Examine a company’s net zero targets

A company needs targets that span the life of its transition plan – including intermediate (typically 2030) and long-term (2050) targets. They need to be science-based and aligned to the Paris Agreement.

Companies should also be clear in their disclosures about whether their targets are across “scope 1, 2 and 3 emissions” — and what percentage of its assets and emissions are covered by those targets.

What are Scope 1, 2 and 3 emissions? They are the three factors an organisation should consider to understand its carbon footprint.

- Scope 1 greenhouse gas emissions come directly from sources controlled by a company

- Scope 2 are indirect emissions associated with the purchase of electricity, steam, heat or cooling

- Scope 3 result from assets not controlled by a company, but indirectly impacted by its value chain

Investors also need to look out for how carbon offsets are used in their net zero plan and also whether there is reasonable consideration of transition implications for their workforce and communities.

To mitigate risks of ‘green-washing’, investors need to not just look at the company’s targets but also look at the governance and incentive structures and disclosure practices.

Is there clear evidence that a company’s climate transition plan is incorporated into its corporate strategy and risk management systems?

Red flags to watch out for

There are also red flags for investors, Matthew says.

“One is having net zero implementation responsibilities sitting solely in a sustainability or ESG role rather than being incorporated into relevant executive and business line responsibilities.

Also look out for climate sceptics on boards or lobbying against change via industry associations.

“Investors should also assess whether scope 3 emissions are sufficiently considered. While it’s an iterative process that should be refined over time, there should be demonstrable evidence of progress.”

Find out about

Pendal Horizon Sustainable Australian Share Fund

Climate transition plan

Companies should have a climate transition plan with detailed analysis of material risks and opportunities.

There should be evidence the analysis is used to inform business decisions (including relevant capital allocation), resourcing and expertise and sometimes links to remuneration.

Investors should ask themselves if the board has sufficient skills. Is there stakeholder engagement? What is the track record of achieving previous transition strategies and targets?

Disclosures

Investors need to also pay close attention to disclosures.

Does a company produce reporting in line with the Task Force on Climate Related Financial Disclosures (TCFD)? How regular and comprehensive are they?

Does a corporate clearly outline the most material climate-related risks and opportunities for its business? How robust is the analysis that sits behind these views?

“We want to make sure their net zero plan is credible. It should be practical but adequately ambitious to align with key stakeholder expectations,” Matthew says.

“Without doubt the private sector on the whole is stepping up to the net zero call to action and this is a very important development.

“As investors, the onus is now on us to pay attention to the detail and progress of individual net zero plans.

“Through company engagements, we are working with companies to address any shortfalls and accelerate real economy decarbonisation.”

About Edwina Matthew

Edwina Matthew is Pendal’s Head of Responsible Investments. Edwina is responsible for maintaining our leadership position in the provision of sustainable and ethical investment products.

Edwina is actively involved in the implementation of the UN-supported Principles for Responsible Investment. She also represents the company in working groups with a number of industry associations and initiatives relating to responsible investment.

About Pendal Group

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

We believe sustainability considerations ultimately drive higher and more stable investment returns over the long term.

Pendal Group has a proud heritage in responsible investing, extending back decades. Our specialist responsible investing business Regnan includes highly experienced ESG research and engagement experts and offers a growing range of investment strategies.

Some of our responsible investing strategies

The federal government estimates $20 billion of funding is needed to hit net zero emissions by 2050. But it could be triple. TIM HEXT explains what that means for investors

You probably don’t spend much time pondering our federal and state government arrangements.

But after running the NSW debt program for ten years as a general manager of TCorp (NSW Treasury Corporation) — which involved regularly explaining the arrangements to offshore investors — I know state governments are more important than federal governments.

The only reason people gathered on the sheep paddocks of southern NSW in the first place was to discuss defence and foreign affairs.

Covid has demonstrated the importance of the states to the population. In day-to-day life, Australians now should well understand that premiers are more important than prime ministers.

Therefore it’s interesting to watch Prime Minister Morrison trying to reclaim ascendency in recent times, as we move towards a federal election due by May.

Whether it be vaccine rollouts, new infrastructure and now climate policy, the prime minister’s main job seems to be repackaging state initiatives as his own.

That’s nothing new. But it appears people are now onto it — and the spin doctors are having to work harder.

Why does this matter for investors?

Well, the states are like you and me. They have to either earn or borrow money to spend it. They must live within their means.

On the other hand, the federal government — via the Reserve bank — has the ability to create money. They don’t need to borrow or earn it. The only constraint on federal spending is inflation.

Pendal Sustainable Australian Fixed Interest Fund

An Aussie bond fund that aims to outperform its benchmark while targeting environmental and social outcomes via a portion of its holdings.

Central bankers and economists used to push back on this. But after the past two years the cat is out of the bag.

Now the challenge is how to finance all the required climate initiatives.

Federal/state fiscal arrangements are complex — and in the relatively new area of climate policy thay are largely untested.

The federal government’s “Technology Investment Roadmap” estimates $20 billion of funding is needed to hit net zero emissions by 2050.

The cost may be closer to $60 billion based on estimates from countries that are less optimistic on the whole technology vibe.

I suspect much of this will come via guarantees of private projects rather than direct funding.

This is the European model and leads the world. Projects would need backing from the federal government, though, since state funding is already stretched.

Let’s hope federal and state governments can get back on the same page and work out a joint approach to climate policy.

States are already leading the execution, but the federal government will need to step up and do the heavy lifting on financing. (They already have the Australian Renewable Energy Agency and the Clean Energy Finance Corporation in place.)

Otherwise state credit ratings will deteriorate and the federal government will end up footing the bill anyway.

This is an increasing focus for us when assessing the credit ratings of semi governments and the positioning in our government bond portfolios.

We have also recently finished our wider ESG assessment of the states and will publish a piece on this in our upcoming Australian Quarterly.

About Tim Hext and Pendal’s Income & Fixed Interest boutique

Tim Hext is a Pendal portfolio manager and head of government bond strategies in our Income and Fixed Interest team.

Tim has extensive experience in banking, financial markets and funding including senior positions with NSW Treasury Corporation (TCorp), Westpac Treasury, Commonwealth Bank of Australia, Deutsche Bank, Bain & Co and Swiss Bank Corporation.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia.

Find out more about Pendal’s fixed interest strategies here

About Pendal

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

In 2023, Pendal became part of Perpetual Limited (ASX:PPT), bringing together two of Australia’s most respected active asset management brands to create a global leader in multi-boutique asset management with autonomous, world-class investment capabilities and a growing leadership position in ESG.

Most investors are now aware of climate change risks. But biodiversity preservation may be an even bigger and more immediate issue. EDWINA MATTHEW explains

Countries representing 90 per cent of global GDP are now covered by net-zero targets, highlighted at the recent COP26 climate change conference in Glasgow.

We will soon know if those targets are sufficiently ambitious to keep global warming to 1.5 degrees — meeting the Paris Agreement adopted at COP21 in 2015.

But net zero emissions by 2050 is not the whole story.

As Glasgow was ramping up for COP26, the southern Chinese city of Kunming was just winding down after another COP (or Conference of the Parties) which focused on conserving biological diversity.

At COP15, 195 countries pledged to reverse biodiversity loss by 2030 at the latest and agree on a framework to protect species and their habitats.

Biodiversity may not be as attention-grabbing as climate change. But it is a critical part of the overall solution and directly impacts many industries.

Agriculture. Medicine. Insurance. Real estate. Tourism. To name a few.

Half of the world’s total GDP — or some US$44 trillion of economic value generation — is moderately or wholly dependent on nature and its services, according to the World Economic Forum.

“Climate change is a very complicated issue, but biodiversity is on a whole other level,” says Pendal’s Head of Responsible Investments, Edwina Matthew.

Sustainable and

Responsible Investments

Fund Manager of the Year

Twin crises

Climate change and biodiversity loss are inter-related, “twin crises”, says Matthew.

Climate adaptation strategies such as protecting and restoring natural habitats offer defence against the physical impacts of climate change.

Nature-based solutions are also part of the broader universe of carbon removal projects underlying the carbon credits or offsets that are part of net zero strategies.

But climate change itself is destroying our natural capital (soil, air, water and living organisms) and biodiversity ecosystems — as seen in Australia’s Black Summer bushfires.

“Encouragingly, governments, business and investors are starting to understand that nature and climate can’t be separated — and that nature-related impacts and dependencies need to be considered alongside climate-related exposures,” says Matthew.

“We need to invest in mutually reinforcing solutions. A 1.5-degree pathway cannot be achieved without major investments in natural capital.”

Industries threatened by biodiversity loss

Agriculture is the most obvious example of an industry threatened by loss of biodiversity.

The agriculture sector accounts for a quarter of Australia’s exports (and employs 60 per cent of the world’s working poor).

Scientists estimate $US577 billion of annual crop production is at risk from loss of pollinators like bees.

The Worldwide Fund for Nature says 60 per cent of the world’s coffee varieties are in danger of extinction due to climate change — a sector with more than US$80 billion in global sales.

Nearly half of all medicines are derived from natural sources.

“We’re also starting to see scientists linking the transmission of animal disease to humans because of a breakdown in biodiversity buffers,” says Matthew. “We had SARS, now we have COVID.”

The UK Treasury’s Dasgupta Review on the Economics of Biodiversity released earlier this year says the “devastating impacts of COVID-19 and other emerging infectious diseases — of which land-use change and species exploitation are major drivers — could prove to be just the tip of the iceberg if we continue on our current path”.

Find out about

Pendal Horizon Sustainable Australian Share Fund

Much of global tourism is linked to natural attractions. The Great Barrier Reef brings in $A1.5 billion a year in tourism and fishing.

The loss of wetland buffers for flood-prone areas can expose real estate and insurance companies to higher risk.

Nature also helps regulate the climate itself — as we acknowledge in the development of nature-based carbon offsets.

What it means for investors

Just as investors now understand the risks posed by climate change, so too natural capital and biodiversity considerations are starting to creep into the investor engagement and corporate reporting agenda.

“It’s twofold,” says Matthew.

“It’s about understanding biodiversity loss as a top-down, systemic issue — as a threat to the global economy — as well as understanding and managing bottom-up, company-specific natural capital and biodiversity-related exposures.

“It’s also about holding companies to account for their impacts, as we do for climate. What role do they play in adverse outcomes for biodiversity and natural capital? How are companies embedding these considerations into their own governance structures and risk management frameworks?

“And to what extent are they dependent on natural capital for their own business? How do they think about biodiversity loss and related policy and regulatory trends and shifts in key stakeholder expectations?

“A lot of the learnings we’ve had from climate change are starting to play out in the natural capital space.”

The good news is, companies are starting to respond.

“We are seeing efforts in mining, property and finance to build understanding around dependencies and impacts in business models and supply chains.”

Biodiversity and land management reporting is already a feature in some company public disclosures.

“Just last month BHP acknowledged evolving stakeholder expectations about its efforts to achieve nature-positive outcomes during an ESG investor roundtable.”

The newly launched Taskforce on Nature-related Financial Disclosure — supported by the United Nations and endorsed by G7 ministers and financial institutions — is setting up a risk management and disclosure framework for organisations to report and act on nature-related risks.

The taskforce supports a shift in global financial flows away from “nature-negative” outcomes toward “nature-positive” outcomes.

Opportunities

Similar to the transition to a “low-carbon economy”, a transition to a “nature-positive economy” also offers economic opportunities.

There is potential for almost 400 million jobs and some $US10 trillion in annual business value by 2030 across three socioeconomic systems (food, land and ocean use; infrastructure and the built environment and energy and extractives) according to WEF.

Pendal clients are exploring how they can direct capital to support nature-positive outcomes, Matthew says.

“They have a fiduciary and financial interest in the wellbeing of the economy as a whole. They expect active managers like Pendal to exercise our ownership rights on behalf of our clients to encourage the protection of natural capital.

“They are also seeking opportunities for how they can allocate capital to support and scale nature-positive outcomes.”

Pendal will “continue to work with our clients and other stakeholders to build understanding around biodiversity loss and access to nature-positive investment solutions to help tackle the next sustainable investment challenge,” Matthew says.

About Edwina Matthew

Edwina Matthew is Pendal’s Head of Responsible Investments. Edwina is responsible for maintaining our leadership position in the provision of sustainable and ethical investment products.

Edwina is actively involved in the implementation of the UN-supported Principles for Responsible Investment. She also represents the company in working groups with a number of industry associations and initiatives relating to responsible investment.

About Pendal Group

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

We believe sustainability considerations ultimately drive higher and more stable investment returns over the long term.

Pendal Group has a proud heritage in responsible investing, extending back decades. Our specialist responsible investing business Regnan includes highly experienced ESG research and engagement experts and offers a growing range of investment strategies.

Some of our responsible investing strategies

What are the major factors driving global equities investments in this volatile period? And which plays should investors be considering right now? Pendal’s head of global equities, Ashley Pittard, explains in this fast podcast

Listen to the podcast above or read the transcript below

Interviewer Sean Aylmer: Ashley, there’s incredible volatility in Wall Street at the moment, particularly among the tech stocks. What is going on?

Ashley Pittard, Pendal’s head of global equities: It really comes down to a couple of key points. The key points are:

- Inflation: Is a transitory or is it frustratingly structural?

- In addition to that, you have the Federal Reserve tapering

- You have long-term interest rates increasing

- You have a debt ceiling negotiations in the US that are dragging on

- In addition to that, you have China’s increasing regulatory risk. China also has real estate issues with regards to their largest developer.

All of that together creates uncertainty and that uncertainty is creating volatility in companies that have re-rated over the last five years to valuation levels that are very, very high.

Interviewer: Inflation – is it transitory or is it structural?

Ashley Pittard: I get back to what Fed chair Powell said. He originally thought inflation was transitory, but it’s now becoming frustrating.

When you step back, you look at wage growth in the US which is compounding at 3-4%. You’ve got higher energy prices. We’re actually near an oil price of $80. And you’ve got massive higher transportation costs — an example is the UK’s with their fuel and transport issues.

All of those issues, in addition to commodity prices that are at near-term highs, are all contributing to inflation that I believe will be more longer-term in nature then transitory.

So it’s interesting now that we’re starting to see the Federal Reserve think that way.

Find out about

Pendal Concentrated Global Share Fund

Interviewer: How big a worry is China — be it the regulatory risk or real estate issues particularly around Evergrande?

Ashley Pittard: There’s no doubt China is a massive risk. The reason it’s a massive risk is because they’re trying to redistribute wealth. And whenever you try and redistribute wealth, people that have the wealth usually lose out.

So where is the majority of wealth situated in China? It is in the large property businesses. And more importantly, these large technology companies. As we’ve seen over time, restrictions being put in place which means the market will start giving a significantly lower valuation to these businesses on the tech side.

With regards to the real estate side, in addition to lowering house prices, these development companies have significant amounts of debt. And if you have debt, you can start getting into a situation that is very reminiscent of what we saw in the US housing market probably a decade ago now.

So the risk in China is very, very high because you’re redistrubuting wealth, the P/Es have to come down because of the increasing risk. And then you also have this debt burden associated with a reduction or slowing in property development, which is very reminiscent of what we saw a decade ago in the US.

Interviewer: So bringing that all to portfolio construction, what does it mean in terms of investing in global markets at the moment?

Ashley Pittard: We think that you want to be different. What do I mean by that? You want to be contrarian. If you look over the last five years, the best sectors to be in globally have been technology and pharmaceuticals. They are at all-time highs as a per cent of the index — and also their stock prices.

We believe, as inflation becomes more structural, that you want to be concentrated in a portfolio of financial and energy plus aerospace exposure.

So effectively we believe you want to be in re-opening plays and contrarion plays as inflation becomes frustratingly higher for longer and not transitory – just like Chairman Powell said.

About Ashley Pittard and Pendal Concentrated Global Share Fund

Ashley Pittard leads Pendal’s Global Equities investment boutique. He is responsible for setting the strategy, processes and risk management for the boutique and its funds including Pendal Concentrated Global Share (COGS) Fund.

Ashley has more than 24 years of finance experience, including roles in petroleum economics, global energy investment analysis and 20 years as a global equities fund manager.

Pendal COGS Fund is an actively managed, concentrated portfolio of global shares diversified across a broad range of global sharemarkets.

Find out more about Pendal Concentrated Global Share Fund

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Investors concerned about the banking crisis and recession fears in the US may be missing out on finding investment opportunities in other parts of the world, says Pendal’s CLIVE BEAGLES

- US banking crisis creating opportunities elsewhere

- UK banks trade at steep discounts

- Browse Pendal’s global equities funds

MARKETS are watching the US closely as its banking system reels from the impact of higher interest rates on regional bank bond portfolios.

Three US banks have been shuttered during the rolling crisis and regional bank shares have been volatile as markets weigh up the prospect of further failures.

But the crisis has also swept up banks and markets outside the US, which may offer opportunities for investors who can keep calm amid the noise.

Clive Beagles, a senior fund manager at Pendal’s UK-based asset manager affiliate J O Hambro, has similar things to say about British bank stocks.

“Many of the UK banks are posting returns on equity of close to 20 per cent in the first quarter,” says Beagles.

“But they all trade at a discount to book value — some of them at 0.4 or 0.5. That includes big names like Natwest and Lloyds.

“Discounts to book value for that kind of return on equity just look silly.”

Beagles says the US market is acting like a “rotating firing squad” that seems to be picking a different name every other day to sell off.

But he believes the banks that are failing in the US are smaller players which are not globally significant.

“The differential between how the US has been regulating their banks and how the UK and Europe are regulating banks is becoming ever clearer — which is frustrating because they have been dragged down a bit by the noise.

Is everyone else still catching cold when America sneezes?

Beagles says the underlying concern many investors have is of a global recession triggered by a downturn in the US.

“There’s an old assumption that when the US sneezes everyone else catches a cold. But I do slightly wonder if it’s going be different this time.

“If this is a crisis, it’s the first one we’ve had where the US dollar is going down rather than up.

“Normally, you head to the dollar for safe haven status.”

Beagles believes the US dollar weakness indicates something different is going on from the usual global contagion. It could point to a period where the US is one of the slower-growing economies in the developed world rather than its traditional role as one of the fastest.

“The banks are just a microcosm of that — they will need more capital and need to be more tightly regulated in a slower US.”

Beagles also cautions against comparisons to previous banking crises.

“In 2008, UK banks had tier-one capital ratios of 4 per cent. Today they have tier-one ratios of 14 per cent.”

Tier-one capital refers to bank’s most reliable and highest-quality capital. A higher tier-one capital ratio generally suggests a bank is better equipped to absorb losses and maintain its financial stability.

“In 2008, there were something like £400 billion more loans than there were deposits — today it’s the other way around.

“The UK as an economy is under-geared rather than over-geared.”

About Clive Beagles

Clive Beagles is a senior fund manager with Pendal Group’s UK-based asset manager, J O Hambro Capital Management. Clive is one of the UK’s most highly respected equity income managers. He has 32 years of industry experience and co-manages the JOHCM UK Equity Income Fund.

About Pendal Group

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

A rotation from growth to value will take years to play out for a generation of investors that has only known low interest rates, says senior fund manager CLIVE BEAGLES

- Rotation from growth to value underway

- Corporate activity could be next trigger

- Investors slow to embrace change

A STOCKMARKET rotation from growth to value could take years to fully play out, with corporate action likely to be the next catalyst for investors, says senior fund manager Clive Beagles.

Many investors sold down high-growth stocks like big US tech firms over the past year as higher interest rates reduced the future value of their earnings.

But despite a dramatic selldown that shaved trillions from market values, investors are only at the start of a reorientation in markets that could last up to three years, believes Beagles, an UK equity income manager with our London-based sister company J O Hambro.

“There’s a generation of fund managers who have only ever lived in a world of zero interest rates and very low discount rates and it’s taking them a long time to recognise that this is a regime shift,” he says.

The gap between average valuations of US and UK-based companies is evidence of how far the changeover has left to go, he says.

UK shares are trading at an average price earnings ratio roughly half their US counterparts as the war in Ukraine overshadows a robust local economy and better-than-expected company reporting season.

“The UK has the greatest exposure to the value factor of any developed market,” he says.

Value gap may trigger corporate activity

This relative value is starting to trigger corporate activity, says Beagles.

The UAE’s First Abu Dhabi Bank is reported to have been considering an all-cash bid for banking icon Standard Chartered.

Anglo-Dutch energy giant Shell has been mulling a move to the US.

Cement and concrete producer CRH unveiled plans to move its main listing from London to New York, sending its shares up 7 per cent on the day of the announcement.

Adviser Sam is invested

in making our world

A better place.

Watch as Sam meets a

mum rebuilding her life

thanks to responsible

investing

“This could be the sort of thing that jolts investors into realising quite how ridiculous this valuation gap between the UK market and other parts of the world has become,” says Beagles.

“Standard Chartered is an interesting example. As far back as 50 years ago, it was one of jewels in the crown of the UK market — listed in London but exposed to high growth markets in Asia with a very interesting geographical footprint.

“It has been struggling for years and is now trading on about half its book value. First Abu Dhabi trades at two times book value — so you can see what they are trying to do.”

Reports of Shell considering a move to the US markets also indicate that corporate activity can be the catalyst to realise investment opportunities.

“In terms of the geographical footprint, there’s not much to choose between Britain’s BP and Shell and their US peers Exxon and Chevron.

“But the US peers trade on anywhere between 50 to 75 per cent premiums. There’s no logic to it.”

Trend to value has years to play out

Beagle says this indicates the trend towards value stocks has some years to play out.

“It is taking investors a while — the UK has been deemed to be this sort of Jurassic Park market where companies go to die for some time.

“This is why I come back to: does it need one of our banks to get bid for? Does it need one our big oil companies to get bid for?

“If you have two or three come along in quite short order that might be the thing — investors have been very slow to embrace the change.”

Beagles says the recent corporate earnings season in the UK saw a mix of solid results and muted outlook statements.

But he says better-than-expected dividends indicate that corporate Britain is in good health.

“That’s the ultimate manifestation of business confidence, isn’t it? It reflects strong balance sheets and demonstrates what companies really think about the world.

“Consumer confidence in the UK is almost at a one year high, so despite all the misery they read in the newspapers, people are just getting on with their lives.

“Retail spending has generally come in better than people would have expected, and we’ve still got this massive cushion of £270 billion in savings.

“There’s a little bit of noise about currency, with sterling rallying off its lows, and there’s a little bit of noise around interest costs for companies that are heavily levered – but overall things are looking pretty good.”

About Clive Beagles

Clive Beagles is a senior fund manager with UK-based asset manager, J O Hambro Capital Management. Clive is one of the UK’s most highly respected equity income managers. He has 32 years of industry experience and co-manages the JOHCM UK Equity Income Fund.

About Pendal Group

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

The British share market shows why it’s important to look past the headlines and see the world objectively, says Pendal’s Clive Beagles.

IT’S easy to forget that newspaper headlines are designed to do only one thing: sell newspapers.

If long-term investors needed a reminder of the importance of looking past the headlines, consider the UK, says Pendal’s Clive Beagles.

Recent commentary on the UK has focused on political instability, energy market disruption and the prospect of a real GDP recession in 2023.

Yet UK shares are the best-performing developed market in the world this year — and still offer strong value, healthy dividends and the prospect of growth, says Beagles, a senior fund manager at Pendal’s UK-based asset manager J O Hambro.

Consider this: the FTSE All-Share Index — a measure of the biggest 600 companies on the London Stock Exchange — trades at about the same market cap as Apple.

“It’s crackers,” says Beagles. “One is a two product company — the other is an extraordinarily diverse index in all sorts of industries.

“And yet which one have investors got more money in?”

It’s a reminder of the importance of looking through the noise in investment markets and trying to see the world objectively, he says.

UK issues milder than they appear

Many of the perceived problems facing the UK are milder than they appear, says Beagles.

The recent chaos in political leadership is likely to settle down to an era of more predictable politics, with the extremes of both sides reined in by the shambles of three Prime Ministers in two months.

“In any case, we have left the EU so we might as well try and make the best of it — many of the government’s policies about accelerating deregulation were exactly what we need to do.”

The energy crisis triggered by the Russia Ukraine war is dissipating as European governments co-operate to find alternative gas suppliers and build stockpiles.

“And obviously we can’t rely on the weather, but it’s 19° here this weekend in the middle of November. Each week that goes by like that means accumulated gas reserves are being built up for the winter.”

Sustainable and

Responsible Investments

Fund Manager of the Year

Look to nominal GDP

Even the prospect of recession in 2023 is not as simple as it appears, says Beagles.

“There’s far too much focus on real GDP as opposed to nominal GDP.

“Yes, we are likely to have a real GDP recession, but it could easily be in a situation where nominal GDP is still growing by 4 or 5 per cent.

“Real GDP is an artificial construct. It doesn’t exist in the real world. Companies don’t operate in a real GDP world – their revenues and profits are denominated in nominal terms.

“Many analysts are looking at previous recessions and assuming some sort of 20 to 30 per cent earnings fall for the more cyclical parts of the market.

“But in nominal terms, revenues may well be flat or rising.

“Ultimately, equities should give you an inflation hedge.”

Misery ‘slightly overdone’

Beagles says many of the key indicators of Britain’s economic health have also settled down.

Bond yields in the UK are now lower than they were before the political instability. Sterling is trading at a similar price versus the euro to what it was five years ago.

Households have some £230 billion of accumulated savings, which will offset the effect of interest rate rises and cost of living issues.

Shares also look good value, even with the FTSE100 outperforming other developed markets and trading relatively unchanged year to date.

“The dividend yield in our fund for this year is 6 per cent. It’s only ever been higher than that very briefly during the financial crisis,” says Beagles.

“Dividend cover is the highest it’s ever been and many of the stocks in our fund are on free cash flow yields in the mid-teens or above which means there’s quite a buffer against earnings disappointments.

“It feels a bit like the misery is slightly overdone.”

About Clive Beagles

Clive Beagles is a senior fund manager with Pendal Group’s UK-based asset manager, J O Hambro Capital Management. Clive is one of the UK’s most highly respected equity income managers. He has 32 years of industry experience and co-manages the JOHCM UK Equity Income Fund.

About Pendal Group

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Inflationary periods can be a good time to identify mis-priced stocks if you know what to look for, says Pendal’s CLIVE BEAGLES

- Inflation triggers mis-pricing of stocks

- Important to decipher inflation and volume in revenue growth

- Cyclical stocks oversold in UK market

HOW can equity investors identify mis-pricing in an inflationary environment — and therefore identify opportunities?

Pay attention to the difference between real growth and nominal growth rates of a company, says Clive Beagles, senior fund manager at Pendal’s UK-based asset manager J O Hambro.

Real growth measures growth adjusted for inflation. Nominal growth doesn’t adjust for price changes.

“Inflation has meant real growth forecasts have come down somewhat. But companies operate in a nominal growth rate world, and they’re still going to be high,” says Beagles.

“In the UK nominal growth could be 10 per cent — and that hasn’t happened since the 1980s.

“It’s a very different environment and people haven’t been focusing on it. Earnings could prove to be much better than people think because they are in nominal terms.”

Sustainable and

Responsible Investments

Fund Manager of the Year

In all markets it’s important to look at individual companies and decipher the split of revenue growth between inflation and volume, says Beagles.

“Some companies are very helpful at providing it and some aren’t.

“If you can understand the split, you can identify companies that can pass through price rises, and those that might end up with strong revenue growth but no volume growth,” he says.

Rotation away from cyclicals and financials ‘overdone’

In the UK, the rotation away from financials and cyclicals towards defensive stocks is overdone, argues Beagles.

Extreme risk aversion in the market means the valuation between defensives and cyclicals is now at the same low level as after 9/11 and during the Lehman collapse in the global financial crisis.

“That’s pretty staggering. We are in this phony period where everyone is anticipating that life slows down quite dramatically but companies haven’t seen it yet.”

The cost-of-living crisis particularly around energy prices in the UK has gotten a huge amount of attention.

“But the stock of savings is elevated and at an aggregate level that will provide a bit of a cushion.” (Though the savings aren’t distributed evenly across society, he adds.)

“The investment community has been whipped up into very bearish sentiment, but the UK is different to Europe. It hasn’t been hit as hard by higher energy prices. It is much more service, consumer-spending oriented. It hasn’t got a big manufacturing sector.

“Share prices are assuming much worse than what we’ve seen so far.

“As risk tolerance normalises, cyclicals and financials should outperform.”

About Clive Beagles

Clive Beagles is a senior fund manager with Pendal Group’s UK-based asset manager, J O Hambro Capital Management. Clive is one of the UK’s most highly respected equity income managers. He has 32 years of industry experience and co-manages the JOHCM UK Equity Income Fund.

About Pendal Group

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.