Pendal has brought a very different global equities strategy to Australia. Here fund managers Chris Lees and Nudgem Richyal explain the Pendal Global Select Fund process

- Something very different in global equities

- “Highly recommended” by Zenith (Sep 27, 2021)*

- Find out about Pendal Global Select Fund

CHRIS LEES and Nudgem Richyal have spent almost 20 years building a highly differentiated global equities investment strategy — and now it’s finally available in Australia.

Originally created in 2004 at Barings Asset Management, the global equities strategy features very different names to those that frequently dominate such funds.

The pair brought their strategy to Pendal’s UK-based asset manager JOHCM in 2008, where they built it into a US$5.3 billion fund.

After recently launching in Australia as Pendal Global Select Fund, Zenith awarded the fund its highest rating of “Highly recommended” (Sep 27, 2021).**

Yin and Yang

“If you asked clients about us, they would say ‘Chris and Nudgem are Yin and Yang’,” says Lees, a Londoner who now lives in a small village called Andermatt in the Swiss Alps.

“We both bring very different things to the process.”

Singapore-based Richyal says: “We feel unique because we are trying to combine this high-conviction, bottom-up stock picking within the context of top-down factors — particularly sectors and countries.

“It sounds glib, but it’s the Warren Buffet bottom-up stuff with the George Soros top-down stuff.”

A four-dimensional, ‘quantamental’ process

Lees uses the word “quantamental” — a merger of quanatitative and fundamental — to describe the the process.

“The first dimension is old-fashioned stock-picking via fundamentals. We are looking for good or improving companies.

“The second dimension is valuation. We want those companies in the right sectors at attractive valuations.”

Analysis of sector, country and other factors is important in this part of the process. “Think of it like real estate. Even the best home in a deteriorating neighbourhood can lose you money,” Lees says.

“Third, we buy shares when they’re going up, not down, because that’s the only way you can make money for your clients.”

Pendal Global

Select Fund

Something very

different in

global equities

A critical part of the third dimension is understanding key drivers of not only different sectors, but different geographies.

“Just look at China right now. It doesn’t really matter what stock you hold, it hasn’t worked out well,” Lees says.

“And the fourth dimension is about tomorrow. The world is always evolving. Nobody could have seen the exact impact of COVID, for example. The fourth dimension is where we are really good,” Lees says.

“We can map out very quickly the good houses in the good neighbourhoods and map out what’s changing over time,” says Lees.

“We quant-screen and that tells us what the best stocks are, what the best sectors are and what the best geographies are. We do that Monday morning — we call that three-two-one.

“Then we spend the rest of the week thinking about the fourth dimension — what’s changing, what’s evolving, which good areas are getting slightly worse. Which bad areas are getting slightly better?”

‘Open-source’ approach to investing

Lees and Richyal adopt what they call an “open-source” attitude to finding opportunities — a reference to the software development paradigm that draws on expertise form many sources.

The pair draws on the expertise of 50-plus investment professionals at Pendal’s UK-based asset manager JOHCM.

“Open source always wins in technology because it’s about taking ideas wherever you find them,” Lees explains.

“All the teams in JO Hambro are coming up with great ideas for us to take a look at.

Richyal says this philosophy is critical to their ability to outperform the benchmark.

“We don’t care about the provenance of the idea. If it’s interesting we will go and do our checks on it,” Richyal says. “That open-mindedness to ideas really helps.”

Rule of thumb

Often, they don’t agree about stocks.

“That’s part of our strength. We come at opportunities from slightly different ways,” Richyal explains.

“We have this rule of thumb about stocks. If it’s one minus one — one of us likes it, and the other doesn’t — it doesn’t get in,” he says.

“If it’s one plus zero, that gets in if one of us can convince the other. Over time that’s where we’ve gotten the best results.

“But if it’s one plus one, those are the stocks that are usually at the end of their life,” Richyal says. “If it’s so obvious that we both really like it, it usually means there’s not much juice left.”

“And then there’s the minus one, minus one. They tend to keep underperforming.”

Lees agrees.

“If we’re both very bullish on something, we make good money on it but not really good money. Historically we’ve made most money where one of us is pounding the table bullish, whether it’s a stock or sector or geography or currency.

“In that case it’s good to have the other person’s scepticism in the room,” he says.

Ability to move fast

Agility is important, Lees says.

“By the time a large investment committee agrees on something, often the opportunity has gone. The real money is made where someone has spotted something early, and the rest of the room waits to gather more evidence.”

And given the breadth of the fund — global equities — there are relatively few stocks.

Hear more from Pendal Global Select Fund portfolio managers Chris Lees and Nudgem Richyal:

- Fast podcast: What makes this cycle different – and which data investors should be watching

- Fast podcast: How to find opportunity in global equities right now

- Webinar: Listen to an in-depth webinar with Chris and Nudgem (registration required)

- Article: A different path to the summit: Chris Lees and Nudgem Richyal launch Pendal Global Select Fund in Australia

- Article: Everyone’s looking for something different in global equities. Here’s how to find it

- Article: Two of us: Pendal global equities fund managers Chris Lees and Nudgem are ‘Yin and Yang’

“If you want to outperform the global index, you’ve had to own a narrow set of companies,” Lees says. “It’s always been that way.”

Over the past decade holding the big technology companies has meant outperformance, he says. The decade prior to that was about holding emerging markets and commodities, and then in the 1990s it was about holding technology, media and telecommunications companies.

Digitisation, decarbonisation and deglobalisation are the new themes.

Not wrong for long

Lees says critical to the fund is knowing when to sell stocks.

“It goes right back to what Einstein said when he was asked what the greatest discovery humankind had ever made. He said the power of compound interest,” Lees says.

“Most people still don’t understand that. If you are holding losers in your portfolio, you’re holding back the compounding effect.

Lees adds that it’s been proven that losing stocks carry on losing with greater persistency, and winning stocks carry on winning.

“Weed out the losers and let the winners run.”

Equal weighting

Just as critical is equal weighting of the portfolio’s 30-to-60 stocks.

“It tilts you away from large-cap growth over time and towards mid-cap value. And it’s systematic rebalancing. It forces you to trim you winners back to equal weight. And review your losers.”

Richyal says its about mitigating the endowment effect on the way down.

“That’s when you ascribe more value to something in your possession than its actually worth in the outside world. And on the upside, we’re trying to mitigate overconfidence bias.”

“We really believe that performance follows flows. And our process has been built to say where is the money going to go to? We aren’t trying to pre-empt that move. We are just fast followers and lock on to the trend.”

Find out more about Pendal Global Select Fund

*Source: JO Hambro, Morningstar universe – Global Large-Cap Growth Equity funds, Lipper survey – Sector quartile ranking: IA Global, and Lipper Global Equity Global domiciled in the UK, offshore Ireland, or offshore Luxembourg. Lipper ranking is from A GBP Class. Please note that these performance figures have not been calculated in accordance with the Financial Services Council (FSC) standards

** The Zenith Investment Partners (ABN 27 103 132 672, AFS Licence 226872) (“Zenith”) rating (assigned ) referred to in this document is limited to “General Advice” (s766B Corporations Act 2001) for Wholesale clients only. This advice has been prepared without taking into account the objectives, financial situation or needs of any individual and is subject to change at any time without prior notice. It is not a specific recommendation to purchase, sell or hold the relevant product(s). Investors should seek independent financial advice before making an investment decision and should consider the appropriateness of this advice in light of their own objectives, financial situation and needs. Investors should obtain a copy of and consider the PDS or offer document before making any decision and refer to the full Zenith Product Assessment available on the Zenith website. Past performance is not an indication of future performance. Zenith usually charges the product issuer, fund manager or related party to conduct Product Assessments. Full details regarding Zenith’s methodology, ratings definitions and regulatory compliance are available on our Product Assessments and at http://www.zenithpartners. com.au/RegulatoryGuidelines

About Chris Lees and Nudgem Richyal

Chris Lees and Nudgem Richyal are senior fund managers of Pendal Global Select Fund. The pair have been working together as investment managers for more than 20 years.

Chris has more than 32 years of investment industry experience. He joined Pendal Group’s UK-based asset manager J O Hambro Capital Management (JOHCM) in 2008 after spending 19 years at Baring Asset Management, ultimately as head of its global sector team.

Nudgem has 22 years of industry experience, joining JOHCM with Chris in 2008. He was previously an investment director with the Global Equity Group of Baring Asset Management, where he worked closely with Chris since 2001.

* Source: JO Hambro, Morningstar universe – Global Large-Cap Growth Equity funds, Lipper survey – Sector quartile ranking: IA Global, and Lipper Global Equity Global domiciled in the UK, offshore Ireland, or offshore Luxembourg. Lipper ranking is from A GBP Class. Please note that these performance figures have not been calculated in accordance with the Financial Services Council (FSC) standards.

About Pendal Global Select Fund

Pendal Global Select Fund is a global equities portfolio with a distinctive, yet proven approach and a 17-year track record of outperformance. Since its inception, the underlying strategy (JOHCM Global Select Fund) has delivered top-decile performance in Lipper and 2nd decile in Morningstar.*

About Pendal

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management. Pendal Group includes Pendal Australia, J O Hambro Capital Management, Regnan and Thompson, Siegel and Walmsley (TSW).

Chris Lees and Nudgem Richyal have spent almost 20 years building a differentiated global equities strategy. Here’s their story

- Something very different in global equities

- “Highly recommended” by Zenith (Sep 27, 2021)**

- Find out about Pendal Global Select Fund

“MY KIDS call Nudgem the man with the funny ears because as they grew up, they kept seeing him on my computer screen with his headphones on,” says fund manager Chris Lees of his investing partner of more than 20 years, Nudgem Richyal.

Remote working? The pair have been doing it for years.

Richyal lives in London, while Lees resides in a small village in the Swiss Alps. At the time of this article they hadn’t been in each other’s physical presence since June 2020.

“None of this remote working is new to us,” Richyal explains. “We’ve been doing video calls for a long time.”

For almost 20 years the pair have overseen a highly differentiated, high-conviction global equities fund.

Lees and Richyal created their strategy in 2004 at London-based Barings Asset Management. In 2008 they brought it to Pendal Group’s UK-based asset manager J O Hambro Capital Management, where they built it into a US$5.3 billion fund.

After recently launching the strategy in Australia as Pendal Global Select Fund, research house Zenith awarded the fund its highest rating of “Highly recommended” (Sep 27, 2021).**

Pendal Global

Select Fund

Something very

different in

global equities

The strategy features very different names to those that frequently dominate global equity funds.

Yin and Yang

Lees describes his relationship with Richyal as Yin and Yang — two sides that make up a formidable investment team.

“It’s why we are better together,” Lees explains. “He is definitely not a mini-me. I tend to be big picture first, and then concepts and then drill into the details. I’m good at buying the dips in long-term compounding, great companies.

“Nudgem is details first. And once he’s happy with the details, he steps back and looks at the big picture in a way that many details people can’t.

“I’m very good at holding on to our long-term winners and he is very good at saying ‘actually things might be changing and we need to think about selling’,” Lees says.

“Nudgem has brought to the process a ruthless sell discipline.

“Instinctively I’m very good at buying and Nudgem is very good at selling.”

Path to success

Neither of them started in finance. Lees studied geography and Richyal studied chemistry.

Between Richyal’s second and third year at university, he undertook a work placement. One of his bosses suggested he should try banking rather than science and he soon got a job at British merchant bank Hill Samuel.

On his first day Hill Samuel owner Lloyd Banking Group merged with Scottish Widows — and the investment bank part of the business was going to move to Edinburgh.

“I didn’t want to go … so I got a job at Barings. As part of the traineeship I spent six months in the North American business and that’s where I met Chris.

“He’s a very bubbly personality,” Richyal says of his partner. “He’s an enthusiast and in the US office that wasn’t out of the ordinary. But that type of personality sticks out a little bit more in a UK context.”

While Richyal was still finding his way in the world of finance, Lees had long left geography behind and had nearly decade of experience when he met Richyal.

“When Nudgem was on his graduate program, I was just blown away by his raw intellect,” Lees says. “He’s one of the cleverest people I’ve had the privilege to meet.”

Lees had been asked to move back to London and build a global equities capability. He remembers his boss at the time said build a global equities process not on the way the world should be, but on the way the world is.

“Today those words are still so important. You never make money on should. You make money in an ugly, complicated, evolving, grey world,” Lees explains.

A new global investment process

“I asked Nudgem to help build this new global investment process from scratch based on the way the world actually is.”

Richyal liked the idea.

“I thought that it was a very interesting concept. I thought that was the most entrepreneurial choice to make at the time, and in hindsight I was right,” he says.

The two have been working together ever since.

Hear more from Pendal Global Select Fund portfolio managers Chris Lees and Nudgem Richyal:

- Fast podcast: What makes this cycle different – and which data investors should be watching

- Fast podcast: How to find opportunity in global equities right now

- Webinar: Listen to an in-depth webinar with Chris and Nudgem (registration required)

- Article: A different path to the summit: Chris Lees and Nudgem Richyal launch Pendal Global Select Fund in Australia

- Article: Everyone’s looking for something different in global equities. Here’s how to find it

- Article: Two of us: Pendal global equities fund managers Chris Lees and Nudgem are ‘Yin and Yang’

Sometimes they agree. Sometimes they don’t. In fact, they can be at polar ends of a debate.

“We can disagree about a stock or a sector. But that’s just part of the marriage,” Richyal says.

Lees said it wouldn’t work if they always agreed.

“If I wanted someone to agree with me, I would have employed a mini-me and we wouldn’t be very good.”

After more than 20 years is it still working?

“Nudgem has had job offers for more money,” Lees says. “He’s told me and said we were better working together.

“That’s commitment. I know we’re better together so we’re not splitting up anytime soon. We’re not going anywhere.”

Find out about Pendal Global Select Fund

*Source: JO Hambro, Morningstar universe – Global Large-Cap Growth Equity funds, Lipper survey – Sector quartile ranking: IA Global, and Lipper Global Equity Global domiciled in the UK, offshore Ireland, or offshore Luxembourg. Lipper ranking is from A GBP Class. Please note that these performance figures have not been calculated in accordance with the Financial Services Council (FSC) standards

** The Zenith Investment Partners (ABN 27 103 132 672, AFS Licence 226872) (“Zenith”) rating (assigned ) referred to in this document is limited to “General Advice” (s766B Corporations Act 2001) for Wholesale clients only. This advice has been prepared without taking into account the objectives, financial situation or needs of any individual and is subject to change at any time without prior notice. It is not a specific recommendation to purchase, sell or hold the relevant product(s). Investors should seek independent financial advice before making an investment decision and should consider the appropriateness of this advice in light of their own objectives, financial situation and needs. Investors should obtain a copy of and consider the PDS or offer document before making any decision and refer to the full Zenith Product Assessment available on the Zenith website. Past performance is not an indication of future performance. Zenith usually charges the product issuer, fund manager or related party to conduct Product Assessments. Full details regarding Zenith’s methodology, ratings definitions and regulatory compliance are available on our Product Assessments and at http://www.zenithpartners. com.au/RegulatoryGuidelines

About Chris Lees and Nudgem Richyal

Chris Lees and Nudgem Richyal are senior fund managers of Pendal Global Select Fund. The pair have been working together as investment managers for more than 20 years.

Chris has more than 32 years of investment industry experience. He joined Pendal Group’s UK-based asset manager J O Hambro Capital Management (JOHCM) in 2008 after spending 19 years at Baring Asset Management, ultimately as head of its global sector team.

Nudgem has 22 years of industry experience, joining JOHCM with Chris in 2008. He was previously an investment director with the Global Equity Group of Baring Asset Management, where he worked closely with Chris since 2001.

* Source: JO Hambro, Morningstar universe – Global Large-Cap Growth Equity funds, Lipper survey – Sector quartile ranking: IA Global, and Lipper Global Equity Global domiciled in the UK, offshore Ireland, or offshore Luxembourg. Lipper ranking is from A GBP Class. Please note that these performance figures have not been calculated in accordance with the Financial Services Council (FSC) standards.

About Pendal Global Select Fund

Pendal Global Select Fund is a global equities portfolio with a distinctive, yet proven approach.

About Pendal

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management. Pendal Group includes Pendal Australia, J O Hambro Capital Management, Regnan and Thompson, Siegel and Walmsley (TSW).

Net zero is a megatrend that will define the business landscape for decades. Pendal analyst and co-portfolio manager Oliver Renton explains what it means for investors

- Net zero carbon emissions required to halt global warming

- Hydrogen and carbon capture the key technologies

- Find out about Pendal Focus Australian Share fund

NET ZERO has become a mantra for many businesses in recent months as governments and corporations outdo each other in their commitments to reducing carbon emissions and fighting climate change.

The noise will reach a peak at November’s United Nations climate change summit in Glasgow but arguably the real work to achieve net zero has yet to begin.

Every nation and every company will need to a play a role reducing carbon emissions to avoid the worst effects of global warming. That defines net zero as a megatrend that will define the planet for decades.

“There aren’t that many certainties in investing but the move towards Net Zero is one of them,” says Oliver Renton, an energy analyst at Pendal Group. “It’s a helpful framework in which to invest.”

But what exactly is net zero?

How does the world get there?

And what does it really mean for investors?

What is net zero?

Scientists agree it is unequivocal that human influence has warmed the planet and this can be attributed to increasing greenhouse gases in the atmosphere including carbon dioxide, methane and nitrous oxide.

These emissions are combined into a measure known as “carbon dioxide equivalents” and referred to simply as “carbon” for simplicity.

A wide range of human activities generate greenhouse gases including construction and manufacturing, generating electricity, agriculture, transport and heating and cooling.

To limit warming to 1.5 degrees Celsius above pre-industrial levels – a level scientists estimate to be safe – governments agreed in Paris in 2015 that carbon neutrality by the mid-21st century was essential.

Find out about

Pendal Horizon Sustainable Australian Share Fund

Net zero by 2050 refers to this goal of a mid-century point of neutrality where humans add no more greenhouse gases to the atmosphere than is removed.

Of course, net zero does not mean zero.

Greenhouse gases have always been emitted but historically emissions were absorbed into forests, oceans and soil and the cycle was roughly balanced.

Getting to net zero means carbon emitted by humans is balanced by carbon removed from the atmosphere.

How to get to net zero

There are essentially two ways the world can get to net zero carbon emissions, says Renton:

- Reducing demand for carbon producing activities, and

- Changing the way these activities are undertaken to eliminate emissions

But energy usage and economic growth are inextricably linked. Taking a demand-reduction approach to emissions generally means reducing living standards in prosperous countries and condemning much of the developing world to poverty. (There is of course energy efficiency available to aid in the move to net zero.)

“Developing countries want and deserve to live a more energy-intensive lifestyle,” says Renton.

“Energy poverty is an ESG [Environmental, Social and Governance] issue as much as the environmental impacts of carbon. So, it’s important to take a broad perspective.”

That means solving net zero predominantly falls to the supply side.

The role of energy

Almost all aspects of human society use energy. Right now 80 per cent of the world’s energy supply comes from carbon-emitting fossil fuels, chiefly oil, coal and gas, says Renton.

The remaining 20 per cent comes from non-carbon emitting sources like nuclear, hydroelectricity and renewables.

Importantly, for all the focus on electric vehicles, only about quarter of energy use is transport and only half of that is passenger vehicles.

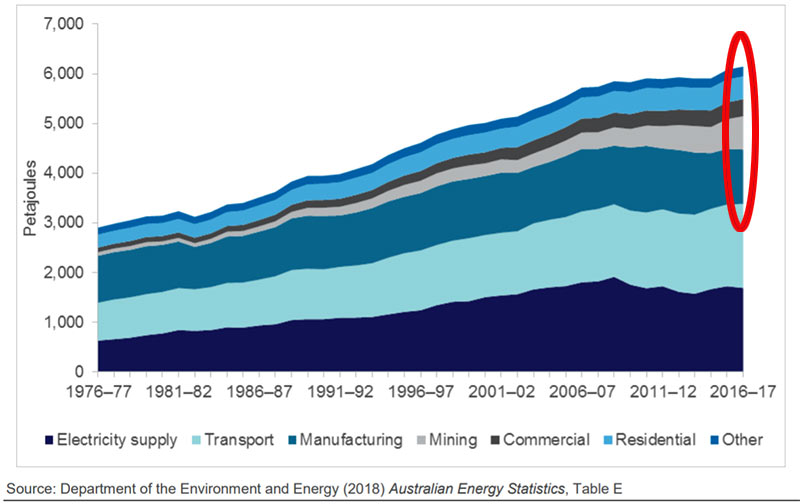

In Australia, the bulk of energy consumption is electricity generation. Other big energy users are manufacturing and mining, the retail and services industries and households.

Australian energy consumption by sector (2018):

So where does that leave net zero?

“We have pretty good solutions for electricity supply and transport in the form of renewables and batteries,” says Renton.

“But half of energy consumption is considered hard to abate and thousands of different solutions will be required.”

One way to analyse how these solutions could play out is to follow how energy is delivered to end users.

Electricity is only one way energy is delivered – and represents about 20 per cent of global energy demand. The 80 per cent remainder is still dominated by oil, coal and gas.

“Even under the best scenarios, electricity only gets to 30 or 40 per cent share – it’s just not feasible to electrify everything,” says Renton.

“So, we still need a solution for transportable liquid or gas forms of energy.

“This is a very interesting insight – because at the moment, the net zero commodity that can be used to transport energy does not exist in a commercial way.”

Technology solutions

The answer to this puzzle lies with technology.

“We’re going to need technological breakthroughs throughout the whole system. But historically, we underestimate the effect of technological change and miss the big picture,” says Renton.

Solar is a case in point. Innovation is driving prices down so rapidly that the solar industry achieved cost milestones some two decades ahead of forecasts.

“It’s pretty unbelievable – and that trajectory can probably be applied to various other aspects of the energy transition.”

The two big hopes for net zero transportable energy are two relatively immature technologies: hydrogen and carbon capture and storage (CCS).

And their prospects are interlinked.

Hydrogen theoretically solves the problem of a transportable, net zero emissions energy source.

Hydrogen is the most abundant and simplest element in the universe and is safer than conventional fuels. It can be manufactured and when burned emits nothing but energy and water. It can be delivered though gas pipelines and used to fuel vehicles.

But, for the foreseeable future, it is too expensive to compete as a fuel.

And worse, depending on how it is made, the hydrogen manufacturing process itself creates carbon.

There are two ways to make hydrogen. The more expensive way is using electricity to split water – a net zero activity only if the electricity itself is carbon free. The cheaper way is to split it from natural gas using steam, but this process produces carbon dioxide as a by-product.

2021 Money Management of the Year Awards

Pendal Australian Shares Portfolio

Winner – SMA Australian Equities

Pendal Property Investment Fund

Winner – Australian Property Securities

The solution? Capturing the carbon emissions and storing them so they cannot add to greenhouse gases in the atmosphere.

This carbon capture and storage (CCS) is the second leg in the net-zero technology race. It quite literally involves a process that captures carbon dioxide from the air — it is in use in fossil fuel power generation and industry.

But its track record is patchy, and the current economics are not promising at mass scale.

“There’s scepticism about carbon capture and storage but it is in everyone’s forecasts to get to net zero,” says Renton.

What does this mean for investors?

Capital markets have already moved in line with net zero.

The cost of capital for fossil fuel energy companies is rising and net zero shareholder resolutions are on the rise.

All evidence shows the energy transition and the drive towards net zero has enormous momentum.

“But energy and fossil fuels have been inextricably linked to GDP and the decoupling will be difficult,” says Renton.

Renton says the challenges facing hydrogen and carbon capture and storage are only resolved in a world where the carbon price is high enough that projects become economic in a timeframe that allows the world to meet its 2050 goals.

“That’s one of the main conclusions for investors — the implicit or explicit price of carbon is going up and it’s really the only solution.”

This means projects that can efficiently reduce carbon emissions are going to be highly valuable.

Ironically, one of the best avenues for investors could be the natural gas industry, which can produce energy at half the emissions intensity of coal.

“We have confidence than the market for gas is there for the medium term, but the focus should be on top-tier projects or projects that complement CCS” says Renton.

Keep an eye on the energy transition

Renton also cautions investors about taking an all-or-nothing approach to assessing investments, saying some fossil fuel companies have the skills, assets and customer base that will allow them to play an important role in the energy transition.

“Look at the fuel companies that distribute fuel on behalf of society — even if we switch to hydrogen these are still difficult substances to deal with. Who are going to be the natural companies to deal with this? They have the skills and existing assets like pipelines and ports that all become very important.

“It’s too narrow a view to label this a dead asset class.”

He says investors should seek out companies with strong management, governance, capital positions, assets that have value in a renewable world and favourable industry structures that will allow them to best hold margins in times of change.

“And look for carbon capture opportunities that can take advantage of a higher carbon price,” he says.

The conclusion? Investors cannot afford to be ideological about net zero.

“The oil and gas companies are the ones that are genuinely going to be the drivers of change – they are the ones developing and distributing hydrogen and the ones capturing and storing carbon.

“Don’t give up on the energy sector – that could be a very poor outcome for the world.”

About Oliver Renton

Oliver is an analyst and co-portfolio manager with Pendal’s Australian equities team. He has more than 15 years of industry experience and focuses on utilities and health care.

About Pendal Group

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

We believe sustainability considerations ultimately drive higher and more stable investment returns over the long term.

Pendal Group has a proud heritage in responsible investing, extending back decades. Our specialist responsible investing business Regnan includes highly experienced ESG research and engagement experts and offers a growing range of investment strategies.

Find out about some of our responsible investing strategies:

Chris Lees and long-time investing partner Nudgem Richyal have spent 17 years building a highly differentiated — yet highly successful — global equities investment strategy. Here they explain their process

- Many global equity strategies look the same

- Differentiation comes from focusing on “neighbourhoods”

- Find out about Pendal Global Select Fund

- ‘Highly recommended’ by Zenith (Sep 27, 2021)*

THESE days a lot of global equities strategies have started to look very similar — particularly after the outperformance of big tech stocks in recent years.

But as investors eye high stock prices and volatility among the popular picks, the question becomes — how do you find differentiation? How do you assess sectors and geographies to find attractive opportunities?

Chris Lees and long-time investing partner Nudgem Richyal have been thinking about this for many years.

Over the past 17 years they have built their JOHCM Global Select Fund into a highly differentiated — yet highly successful global equities strategy.

The pair recently brought their strategy to Australian investors, launching Pendal Global Select Fund. Research house Zenith awarded the fund its highest “Highly Recommended” rating on September 27, 2021.**

Lees and Richyal use a distinct four-dimensional investment process (stocks, sectors, countries, time/change), which focuses on the behaviour of a company’s share price to determine whether the most important driver of each prospective investment is stock-specific or based on sector, country or another factor.

Pendal Global

Select Fund

Something very

different in

global equities

“When you look at the way the world is — not the way consultants say it should be — the average western large cap stock has surprisingly low alpha and surprisingly high correlation to the sector it’s in,” says Lees.

“Take the Aussie mining companies. There isn’t that much money to be made deciding between Rio Tinto or BHP. It’s about deciding when commodities are going up or commodities are going down.

“What we’ve mathematically discovered is that most people’s ladders are up against the wrong wall,” he says.

“When you look at large caps in the west, it’s the sector effect that drives most stocks, and the move to passive investing and ETFs (exchange traded funds) has just made that greater.

“In the east, in places like Japan and emerging markets in Asia, it’s the country effect. For example, Toyota doesn’t behave like a global automobile company. Chinese banks don’t behave like financials.” Those share prices are highly correlated to the country.

“An average stock in a great sector or country usually makes you more money than a great stock in a terrible sector or neighbourhood,” says Lees.

Understanding global trends

To outperform, investors need to identify and understand global trends.

In the 1980s winning portfolios needed to include Japan, Lees says. In the 1990s its was technology, media and telecommunications companies.

In the 2000s investors needed emerging markets and commodities to consistently outperform. Over the past decade it’s been the big tech FAANG stocks (Facebook, Amazon, Apple, Netflix, Google) — which is why most global portfolios include them today.

Today, high stock prices among the FAANGs and recent volatility have some investors looking for “a different path to the summit”, says Lees. (It’s a familiar analogy since he lives in a small town in the Swiss Alps.)

“There will be a regime change and we have a proven process that locks in on new regime shifts,” he says.

(The pair say digitisation, decarbonisation and deglobalisation are the new themes or “neighbourhoods” to consider.)

Zigging when others zag

Lees and Richyal have outperformed most global equity funds without owning all the FAANG stocks. They refer to it as not being a one-trick pony.

Lees and Richyal created their strategy in 2004 at Barings Asset Management. It was later launched at Pendal Group’s UK-based asset manager JOHCM in 2008 and since then has delivered 3.13%* annualised alpha (before fees) compared to the MSCI All Country World NR Index benchmark.

Since its inception, the underlying JOHCM Global Select Fund strategy has delivered top-decile performance in Lipper and 2nd decile in Morningstar.*

Hear more from Pendal Global Select Fund portfolio managers Chris Lees and Nudgem Richyal:

- Fast podcast: What makes this cycle different – and which data investors should be watching

- Fast podcast: How to find opportunity in global equities right now

- Webinar: Listen to an in-depth webinar with Chris and Nudgem (registration required)

- Article: A different path to the summit: Chris Lees and Nudgem Richyal launch Pendal Global Select Fund in Australia

- Article: Everyone’s looking for something different in global equities. Here’s how to find it

- Article: Two of us: Pendal global equities fund managers Chris Lees and Nudgem are ‘Yin and Yang’

“The fact that we’ve proven we can outperform over a long period and many cycles with different portfolio tilts and geographies — and a different set of stocks — gives our clients confidence that we aren’t a one-trick pony.”

The obvious question is what’s the next decade about?

“It’s going to be healthcare,” Lees says. “That’s where we are getting positive signals.

“Great and improving fundamentals, improving valuations and the beginning of a new price trend. And not many of the winning global equities portfolio have much healthcare in them.”

Find out more about Pendal Global Select Fund

* Source: JO Hambro, Morningstar universe – Global Large-Cap Growth Equity funds, Lipper survey – Sector quartile ranking: IA Global, and Lipper Global Equity Global domiciled in the UK, offshore Ireland, or offshore Luxembourg. Lipper ranking is from A GBP Class. Please note that these performance figures have not been calculated in accordance with the Financial Services Council (FSC) standards.

** The Zenith Investment Partners (ABN 27 103 132 672, AFS Licence 226872) (“Zenith”) rating (assigned ) referred to in this document is limited to “General Advice” (s766B Corporations Act 2001) for Wholesale clients only. This advice has been prepared without taking into account the objectives, financial situation or needs of any individual and is subject to change at any time without prior notice. It is not a specific recommendation to purchase, sell or hold the relevant product(s). Investors should seek independent financial advice before making an investment decision and should consider the appropriateness of this advice in light of their own objectives, financial situation and needs. Investors should obtain a copy of and consider the PDS or offer document before making any decision and refer to the full Zenith Product Assessment available on the Zenith website. Past performance is not an indication of future performance. Zenith usually charges the product issuer, fund manager or related party to conduct Product Assessments. Full details regarding Zenith’s methodology, ratings definitions and regulatory compliance are available on our Product Assessments and at http://www.zenithpartners. com.au/RegulatoryGuidelines

About Chris Lees and Nudgem Richyal

Chris Lees and Nudgem Richyal are senior fund managers of Pendal Global Select Fund. The pair have been working together as investment managers for more than 20 years.

Chris has more than 32 years of investment industry experience. He joined Pendal Group’s UK-based asset manager J O Hambro Capital Management (JOHCM) in 2008 after spending 19 years at Baring Asset Management, ultimately as head of its global sector team.

Nudgem has 22 years of industry experience, joining JOHCM with Chris in 2008. He was previously an investment director with the Global Equity Group of Baring Asset Management, where he worked closely with Chris since 2001.

About Pendal Global Select Fund

Pendal Global Select Fund is a global equities portfolio with a distinctive, yet proven approach and a 17-year track record of outperformance. Since its inception, the underlying strategy (JOHCM Global Select Fund) has delivered top-decile performance in Lipper and 2nd decile in Morningstar.*

* Source: JO Hambro, Morningstar universe – Global Large-Cap Growth Equity funds, Lipper survey – Sector quartile ranking: IA Global, and Lipper Global Equity Global domiciled in the UK, offshore Ireland, or offshore Luxembourg. Lipper ranking is from A GBP Class. Please note that these performance figures have not been calculated in accordance with the Financial Services Council (FSC) standards.

About Pendal

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management. Pendal Group includes Pendal Australia, J O Hambro Capital Management, Regnan and Thompson, Siegel and Walmsley (TSW).

Recent billion-dollar sporting team deals demonstrate why it’s important to be selective when choosing global equities. Pendal’s ASHLEY PITTARD explains

- Choose the top one or two stocks in a sector

- Find out about Ashley Pittard’s Pendal Concentrated Global Share Fund

In 2023, following a strategic review of Pendal’s global equity investment capabilities, we appointed Barrow, Hanley, Mewhinney & Strauss (Barrow Hanley) as the delegated investment manager for Pendal Concentrated Global Share Fund. The fund has been renamed Barrow Hanley Concentrated Global Share Fund.

This article is more than 12 months old. Find our latest insights here

THE record-breaking $US6 billion sale of the Washington Commanders NFL team last month is the latest in a rush of billion-dollar transactions involving trophy sporting teams.

If you can choose the right sporting “franchise” to buy, the returns are eye-watering.

The last time there was a rush of sporting team sales was around 20 years ago – and their value has soared around ten times since then.

What’s that got to do with stocks? A lot, says our head of global equities, Ashley Pittard

Ashley and his investing team haven’t bought any sporting teams lately.

But like the most successful sporting team transactions, Ashley focuses on what he calls “franchise assets”.

It’s all about being selective, he says.

Look for franchise assets

“Franchise assets – companies that are number one or two in their space or are monopoly or duopoly business – are also highly valued among investors at the moment,” Ashley says, pointing to the tech leaders dominating Wall Street.

Pittard’s Pendal Concentrated Global Share Fund focuses on franchise assets such as airports, Boeing and Airbus, stock exchanges, brewers, major banks and select technology companies.

Find out about

Pendal Concentrated Global Share Fund

Being selective — choosing the top one or two players in a market — is key, just as it is when buying a sporting team.

“Last month, the Washington Commanders NFL team in the US was sold for just over $US6 billion,” Pittard notes. “In February this year, the Phoenix Suns basketball team was sold for $US4 billion.

“Michael Jordan recently sold the Charlotte Hornets for $US3 billion. And English Premier League giant Manchester United is, reportedly, close to being sold for £6 billion.”

Compare those values to sports sales 20 years ago — around the time of the last tech boom.

“The Washington football team was sold in 1999 for $US600 million. In 2004 the Phoenix Suns was sold for $US400 million.

“The Charlotte Hornets went for $US300 million in 2003 and Manchester United was sold for £300 million,” he says.

“These assets are trading for around ten times what they sold for back then.”

The tech franchises

In the world of investing, it’s also interesting to observe when trophy assets change hands, says Pittard.

Last time the there was a rush of sales of sporting teams, the technology sector in the US was dominated by the ‘Four Horseman’ – Microsoft, Intel, Cisco and Dell.

They comprised about 17 per cent of the weighting of the S&P500.

“If you look today, the magnificent seven, which are Apple, Microsoft, Alphabet, Amazon, Meta, Tesla and Nvidia, comprise about 20 per cent of the market,” Pittard says.

“The Four Horsemen had unquestioned market dominance and the magnificent seven today have unquestioned market dominance in their fields.”

The similarities between the last tech boom and trophy asset sales back then, and what’s happening today are worth considering, Pittard says.

“The sales of sports franchises don’t come up that often. They are high in demand. Usually sales happens when there is a crisis or valuations get extreme. It’s interesting to watch what’s happening with these franchise assets.”

“The lesson for investors is that you want to be selective, and you want to be concentrated when investing.

“You also want to be defensive because there are uncertainties in the world around the macro-outlook and credit.”

About Ashley Pittard and Pendal Concentrated Global Share Fund

Ashley Pittard leads Pendal’s Global Equities investment boutique. He is responsible for setting the strategy, processes and risk management for the boutique and its funds including Pendal Concentrated Global Share (COGS) Fund.

Ashley has more than 24 years of finance experience, including roles in petroleum economics, global energy investment analysis and 20 years as a global equities fund manager.

Pendal COGS Fund is an actively managed, concentrated portfolio of global shares diversified across a broad range of global sharemarkets.

Find out more about Pendal Concentrated Global Share Fund

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

One way to get exposure to the post-Covid tourism growth story is via plane manufacturers. Pendal global equities PM ASHLEY PITTARD explains

- Paris Air Show demonstrates strong demand

- Major manufacturers act as duopoly

- Find out about Ashley Pittard’s Pendal Concentrated Global Share Fund

AUSTRALIANS who experienced shoulder-to-shoulder tourist crowds during overseas holidays this year might be wondering how to get exposure to the fast-recovering travel industry.

Even before the northern Summer travel season, international tourism was returning strongly towards pre-pandemic levels, notes the UN’s World Tourism Organisation.

Commercial flight bookings have also recovered, catching up with leisure bookings late last year, notes Mastercard in its latest travel industry trends report.

One way to get exposure to this story is via plane manufacturers says Pendal global equities PM Ashley Pittard.

Pittard recently attended the 2023 Paris Air Show during two months of travel, meeting company executives across Europe.

The Paris Air Show is the world’s premier aerospace trade show. This year, post-Covid, more than 1000 new plane orders were announced, demonstrating the rude health of the two big manufacturers, says Pittard.

“Demand for planes is very, very strong,” says Ashley Pittard, who manages Pendal Concentrated Global Share Fund.

“The backlog for the industry is about 8000 units which is about the next ten years of production.”

There are four key reasons, Pittard says.

- “There are new markets like India which are opening up dramatically as demonstrated by the orders at the Paris Air Show.

- “China is slowly opening up again, albeit slower than Europe.

- “There is a sustainability trend – airlines are getting rid of older planes and buying new, more efficient options.

- “And there is also higher airline yields – more people are flying.”

The two major airline manufacturers comprise about 7 per cent of Pittard’s concentrated share fund, while airport monopolies account for another 4.5 per cent.

When valuing aircraft manufacturers, investors need to look five years out because of the long-life cycle in manufacturing an aircraft, Pittard says.

That cycle, alongside capital expenditure and other factors, means Airbus and Boeing act as a duopoly with little chance of a competitor in the medium term.

Post-Covid tourism growth

While demand has jumped, there’s still some way to go with Asian tourists yet to return to pre-Covid levels, and international travel still below 2019 numbers.

That augurs well for the manufacturers.

Find out about

Pendal Concentrated Global Share Fund

Also, both large manufacturers have been able to maintain pricing power.

Airbus, which has about a 60 per cent share of the narrow-bodied planes, benefitted from the grounding of Boeing 737 MAX aircraft in 2019.

“There is plenty of demand for Airbus, it has a beautiful back-book and it has pricing power,” Pittard says.

Boeing has less pricing power, but it is trading on a low multiple. Boeing continued to build planes during 2019, notwithstanding its challenges around its Boeing 737 aircraft.

As a result it has planes ready to deliver, and be paid for, resulting in very strong cash flow.

“Boeing is really cheap. It has $78 billion dollars of inventory on its balance sheet. The majority is finished, or near-finished planes.

“Its total market capitalisation is only $US150 billion. So half its market cap are planes that are sitting there, and they just have to deliver them.”

Keep an eye on supply chain

The potential downside for the aircraft manufacturers is supply chain issues.

“It’s skilled labour – building a plane needs high skills and many left the industry during Covid.

“And there’s a shortage of engine parts. Suppliers are able to produce engines, but because demand for planes is so strong, some of them have been diverting resources into manufacturing spare parts for existing planes. They are getting a higher return on servicing parts.”

Main image: A Boeing 777X flies over the Paris Air Show (June, 2023). Photo credit: Anthony Guerra

About Ashley Pittard and Pendal Concentrated Global Share Fund

Ashley Pittard leads Pendal’s Global Equities investment boutique. He is responsible for setting the strategy, processes and risk management for the boutique and its funds including Pendal Concentrated Global Share (COGS) Fund.

Ashley has more than 24 years of finance experience, including roles in petroleum economics, global energy investment analysis and 20 years as a global equities fund manager.

Pendal COGS Fund is an actively managed, concentrated portfolio of global shares diversified across a broad range of global sharemarkets.

Find out more about Pendal Concentrated Global Share Fund

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

The long-forecast US recession has been delayed once again, says ASHLEY PITTARD, who heads up Pendal’s Global Equities investment team

- Capex spending to boost economy

- Tech stocks selection critical

- Find out about Ashley Pittard’s Pendal Concentrated Global Share Fund

In 2023, following a strategic review of Pendal’s global equity investment capabilities, we appointed Barrow, Hanley, Mewhinney & Strauss, LLC (Barrow Hanley) as the delegated investment manager for Pendal Concentrated Global Share Fund. The fund has been renamed Barrow Hanley Concentrated Global Share Fund.

This article is more than 12 months old. Find our latest insights here

BANK of America last week became the first big Wall Street bank to reverse its recession call.

Are they right?

“Given the strong capital expenditure numbers we are seeing in the US June quarter earnings season, it’s going to be very hard for the US to have a recession this year,” says Ashley Pittard, who heads up Pendal’s global equities investment team.

“Over the last ten years, US companies under-invested. Since the global financial crisis, only 38c in every dollar that was generated from operations or borrowed, was invested.

“Before the global financial crisis it was 53c.”

Instead, corporate America has spent more on share buybacks, notwithstanding the very low interest rates during the period and a pretty good economy, Pittard says.

But this US earnings season, corporate America looks to be taking a different view.

“What you are seeing in the earnings numbers, and what you have seen the entire year, is that capital expenditure is accelerating – 15 per cent in the current quarter, year-on-year, and 14 per cent in the first quarter.

“It’s very hard to have a recession when you capital expenditure is so high,” Pittard says.

The key reason for the boost in capex is re-shoring of operations, post-Covid in a more fraught geo-political environment.

“A couple of years ago, no-one mentioned re-shoring. This earnings season, mentions have gone exponential,” he says.

That’s the headline outcome of Wall Street’s earnings season.

US earnings are beating estimates

In terms of numbers, earnings have beaten estimates by about four per cent, and by one per cent on sales, Pittard says.

Find out about

Pendal Concentrated Global Share Fund

“We are seeing better margins.

“The ‘beats’ are about the historical average, so it’s been a nice earnings season.

“Where you’ve seen most headwinds is in energy, year-on-year, and that’s because prices are lower.

“Materials have come back due to softness in China. And the low-end semi-conductor sector has been weak, cutting their guidance and outlining high inventory levels.”

The outlook for tech

In terms of the Wall Street technology companies, which have outperformed for much of this calendar year, Pittard says investors need to be selective.

“One of the core themes in our concentrated share fund since the beginning of the year was keep the COVID losers but be selective on 2022 losers. And 2022 losers were mostly tech stocks,” he says.

Ashley’s Pendal Concentrated Global Share fund has substantial positions in Amazon, Google, Netflix, Meta and Warner Bros. Discovery.

“We have been selective. We don’t own Apple, Microsoft, Nvidia and Tesla.

“With Apple, Microsoft and Nvidia, it comes down to valuation.

In the case of Apple and Microsoft, they are trading on a price-to-earnings multiple of 33 times. If they can’t get sustainable growth, then that PE is coming down.

“In Apple’s case, the only thing that grew last quarter was their service business.”

Some of the other tech stocks, such as Meta, Amazon and Google, also have the ability to lower costs, Pittard says.

“They are the businesses which have a better skew towards where the growth is, particularly Artificial Intelligence.”

About Ashley Pittard and Pendal Concentrated Global Share Fund

Ashley Pittard leads Pendal’s Global Equities investment boutique. He is responsible for setting the strategy, processes and risk management for the boutique and its funds including Pendal Concentrated Global Share (COGS) Fund.

Ashley has more than 24 years of finance experience, including roles in petroleum economics, global energy investment analysis and 20 years as a global equities fund manager.

Pendal COGS Fund is an actively managed, concentrated portfolio of global shares diversified across a broad range of global sharemarkets.

Find out more about Pendal Concentrated Global Share Fund

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Here, Pendal’s head of global equities ASHLEY PITTARD makes the case for quality banks ahead of a likely US recession

- UBS, JP Morgan, Wells Fargo top picks

- US recession likely; should trigger a steepening of the yield curve

- Find out about Ashley Pittard’s Pendal Concentrated Global Share Fund

THE turmoil among global banks over the past six weeks has created opportunities for investors, with Swiss based UBS and Wall Street giants JP Morgan and Wells Fargo the top picks, says Ashley Pittard, our head of global equities.

“I think UBS is a standout for the next ten years as an investment,” he says.

“You want to invest in a bank that’s one or two in its market, and has high quality management.

“Bank stocks can go down in a crisis environment, but the quality banks don’t go broke and that’s a key point.”

Banks should do well in coming quarters as they reprice credit and achieve higher margins.

“Near term, interest rates have stopped rising and the yield curve is flattish or even inverted.

“But if we fast-forward through the year, we believe there’s going to be a recession in the US. That would likely mean the Federal Reserve will have to cut rates into next year.

“The yield curve will steepen and that’s good for banks because they borrow short and lend long and they are going to get a wider spread. That will feed back in a couple of years’ time into higher earnings.”

The current turmoil could push out weaker lenders who aren’t pricing loans rationally — which would help the top banks.

Short-term risks

Pittard warns there are risks in the short term.

“What are the write-downs going to be, particularly if the recession is hard? That’s the big near-term risk.

“That’s why you want to be with the highest quality banks – number one or two in their market.”

On UBS, Pittard says its metrics are strong. It has just absorbed its second largest competitor, has a 30 per cent plus share in retail banking in Switzerland, and is the number one global bank for ultra-high net worth individuals.

Importantly, UBS has strong management, he says.

Find out about

Pendal Concentrated Global Share Fund

“The new CEO, Sergio Ermotti, is the Tom Brady of European banking,” Pittard says, referring to most successful quarterback in US football.

Ermotti left the bank in 2020 after a successful stint, and then took the top job again on April 5.

“He first came to UBS after the global financial crisis and got them out of high-risk investment banking, increased market share in their ultra net worth business, and boosted dividends and the stock price.

“He just grinds away. He gets costs out of the business, right sizes the riskier parts and gives money back to shareholders.”

Pittard says two US bank stocks worth looking at are JP Morgan, run by the very experienced Jamie Dimon, and Wells Fargo, run by Charles Scharf.

“Dimon is the last remaining US bank CEO who actually went through the GFC,” Pittard says. “Scharf got the CEO job at Wells Fargo in late 2019 and has cleaned it up and ticked all the boxes.”

In terms of why the global banking sector found itself in its current situation, there are several factors, Pittard says.

“There were poor management practices. There’s also been mishandling of the repricing of the rapid interest rate changes over the last year. You’ve also had volatility around what the US Federal Reserve is going to do.”

Pittard says there’s also a regulatory overlay.

“When Donald Trump was in power, he rolled back some of the banking regulations that were put in place directly after the global financial crisis which meant the regulation of smaller banks, like Silicon Valley Bank, was lighter than regulation of the big banks,” Pittard says.

“Also stress testing of the bank last year didn’t consider large jumps in interest rates, which is what actually happened.”

About Ashley Pittard and Pendal Concentrated Global Share Fund

Ashley Pittard leads Pendal’s Global Equities investment boutique. He is responsible for setting the strategy, processes and risk management for the boutique and its funds including Pendal Concentrated Global Share (COGS) Fund.

Ashley has more than 24 years of finance experience, including roles in petroleum economics, global energy investment analysis and 20 years as a global equities fund manager.

Pendal COGS Fund is an actively managed, concentrated portfolio of global shares diversified across a broad range of global sharemarkets.

Find out more about Pendal Concentrated Global Share Fund

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

A US recession is highly likely, but it will be shallow and provide compelling valuations for global equities investors, says Pendal’s ASHLEY PITTARD

- Capex to underpin US growth

- CHIPS and Science Act drives US138bn in spending

- Find out about Ashley Pittard’s Pendal Concentrated Global Share Fund

THE great re-shoring of American industrial production will help the US avoid a deep recession this year and could underpin strong economic growth for the next decade, says Pendal’s Ashley Pittard.

The Biden government this month opened applications for some US$53 billion in manufacturing subsidies under the CHIPS and Science Act, which seeks to boost domestic semiconductor and high-tech manufacturing.

Already, US$138 billion of capital spending has been committed from companies including Intel, Samsung, Texas Instruments, Micron Technology and GlobalFoundries. The first new facilities are expected to be operating as soon as this year.

“It’s just like Warren Buffett says: never bet against America,” says Pittard, who manages the Pendal Concentrated Global Share Fund.

“The US always was and still remains a powerhouse in manufacturing.”

The tailwind of bringing manufacturing capacity back onshore will drive capital expenditure back to its pre-2000 levels, believes Pittard.

Find out about

Pendal Concentrated Global Share Fund

“It is going back to pre-peak-globalisation — and should compound 5 to 6 per cent a year which would give you a nice buffer. That’s why we don’t think the recession will be that deep in the US.”

Capital expenditure a critical driver

Capital expenditure is a critical driver of economic growth, says Pittard.

“You’re not just putting a digger in the ground. You need to hire people to help with permits, you need builders, you have to buy the equipment, you have to have the equipment installed, you need to find a high skilled workforce. It’s pure Reagan trickle-down economics,” says Pittard.

It’s a big turnaround for the US, which has long seen companies move production offshore to take advantage of cheaper labour in China and south-east Asia.

The trend to outsourcing means capital expenditure has grown at an annual rate of just 3 per cent since 2000 compared to the 5 per cent plus clip in the prior two decades.

The decline in capex growth was largely due to falling spending on technology, consumer electronics and apparel.

The average American company now outsources between 25 and 50 per cent of production, compared to a 10 per cent outsourcing rate in comparable firms in the UK and Europe, Pittard says.

“They do it because they get a higher return on capital. They’ve got supply chains and just in time inventory and all that stuff.

“But what they learned from COVID and China’s lockdowns and war is that the sales that you lose by outsourcing that production just isn’t worth it now.

“America is saying ‘for the sake of national security, for the sake of jobs, let’s bring it all back so that instead of giving jobs to the rest of the world, we’re bringing them back to the US’.”

Pittard says onshoring is estimated to create an additional 200,000 jobs a year which is a 1.4 per cent boost to the total US manufacturing labour force.

US ‘highly attractive’

The upshot for investors? The US remains a highly attractive market, says Pittard.

“The caveat of course is if the Fed hits us over the head with a hammer by raising rates too aggressively, but there’s a tailwind from this higher capital expenditure which will help buffer the economy.

“The CHIPS and Science Act is an awesome act.

“It was passed in November last year and this week was the first implementation and already you’ve had the $140 billion in investment that will all kick in over the next two years.

“Peak globalisation went too far.”

Pittard says investors should ensure they have a good industrial base in their portfolios and be selective on the big technology companies that benefit from the re-shoring.

About Ashley Pittard and Pendal Concentrated Global Share Fund

Ashley Pittard leads Pendal’s Global Equities investment boutique. He is responsible for setting the strategy, processes and risk management for the boutique and its funds including Pendal Concentrated Global Share (COGS) Fund.

Ashley has more than 24 years of finance experience, including roles in petroleum economics, global energy investment analysis and 20 years as a global equities fund manager.

Pendal COGS Fund is an actively managed, concentrated portfolio of global shares diversified across a broad range of global sharemarkets.

Find out more about Pendal Concentrated Global Share Fund

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

It could be time for US equities investors to take a bit of money off the table in some sectors, says Pendal’s ASHLEY PITTARD

- Wall St earnings season stronger than expected

- Macro-economy remains the wildcard

- Find out about Pendal Concentrated Global Share Fund

THE macro-economy – inflation, growth, employment – drives top-line sentiment among investors.

But earnings in sectors and companies drive the valuation of specific stocks, notes Pendal’s head of global equities Ashley Pittard.

This was demonstrated recently by a better-than-expected result for Facebook-owner Meta which pushed its share price up 25 per cent.

As the graph below shows, it then fell back sharply, albeit briefly, when stronger-than-expected labour force figures in the US hinted at further interest rate rises, taking the steam out of Wall Street.

Still, earnings season allows investors to look beyond the big picture.

“We’re about halfway through US earnings season and we’ve seen earnings growth fall by about 3 per cent, which is marginally better than what was forecast,” says Pittard, who manages Pendal Concentrated Global Share Fund.

Sectors to watch

While the energy sector has been the out-performer, thanks to very high prices, consumer discretionary stocks have been the surprise packet so far this season.

“The worst-case scenarios for the US consumer have been averted and they’re looking okay. It reinforces the view that if there is a recession, it should be mild.”

The laggards, as expected, have been the technology stocks.

“Across the economy, you are now seeing a normalisation of spending on technology and a slowing of cloud build outs,” Pittard says.

Find out about

Pendal Concentrated Global Share Fund

“As a result, you are seeing cost savings announcements and capital expenditure cuts in the big tech companies.”

Across the earnings season there have been plenty of signs of easing inflationary and supply chain pressures.

At Amazon, for example, shipping costs as a percentage of gross merchandise value is back to 2019 levels and is trending lower.

Pittard notes one exception is Apple, where the company has been hit hard by production lockdowns in China.

Time to take money off the table

Pittard believes it’s time to “take a little bit of money off the table” when it comes to energy stocks.

“I’m only talking about a couple of percentage points, and I’d use that to invest in the 2022 losers — that’s companies like Netflix, Warner Bros, Meta, Alphabet and Amazon,” he says.

Pittard uses Meta, which owns Facebook, Instagram and WhatsApp, to illustrate his point.

“After Meta’s earnings result its share price jumped 25 per cent. That’s because it was beaten down so much in 2022 – it fell nearly 65 per last year.

“When Meta said advertising revenue wasn’t as bad as people had thought, and they’re taking cost cutting measures and reducing capital expenditure, the share price surged.

“In summary, you want to be fully invested,” Pittard says.

“Earnings are coming through better-than-expected. There’s a lot of hurt in the market already from what happened last year.”

But investors need to be selective.

“You want to keep your financials because the recession will be mild. You want to keep your industrials because of the re-shoring that’s going on.

And you can be selective in technology and consumer discretionary.

“Investors should use the strength of their energy investments to rotate into some of those assets. “

About Ashley Pittard and Pendal Concentrated Global Share Fund

Ashley Pittard leads Pendal’s Global Equities investment boutique. He is responsible for setting the strategy, processes and risk management for the boutique and its funds including Pendal Concentrated Global Share (COGS) Fund.

Ashley has more than 24 years of finance experience, including roles in petroleum economics, global energy investment analysis and 20 years as a global equities fund manager.

Pendal COGS Fund is an actively managed, concentrated portfolio of global shares diversified across a broad range of global sharemarkets.

Find out more about Pendal Concentrated Global Share Fund

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

In 2023, Pendal became part of Perpetual Limited (ASX:PPT), bringing together two of Australia’s most respected active asset management brands to create a global leader in multi-boutique asset management with autonomous, world-class investment capabilities and a growing leadership position in ESG.