A new kind of bond offers features based on whether an issuer achieves sustainability goals by a deadline. Pendal Credit ESG Analyst Murray Ackman explains the pros and cons

EVERY YEAR we get asked “what are your New Year resolutions?’” Every year I come up with a few, but they tend to fade before the change of season.

When Sydney went into a Covid lockdown at the end of June I decided to try a few new self-improvement goals. As lockdown stretched on (and after some feedback from my mother) I gave up on my “no shaving” goal.

But other goals were more sustainable.

After another day of meeting goals, I got to thinking about why I’d had more success during lockdown compared to my New Year’s resolutions.

A few things came to mind. I told people about them. And I actually wanted to achieve them, rather than it being an arbitrary decision based on the end of the calendar year.

The goals had a deadline and were easily measurable. And I had skin in the game by way of a friendly wager.

How might that apply to a business?

If a business wanted to change, would a New Year’s resolution pledge be enough? Or would it need more incentive to succeed?

Can capital markets encourage businesses to become more sustainable?

This is how I think about a recent change in capital markets: the sustainability-linked bond.

What are sustainability-linked bonds?

Sustainability-linked bonds are a bond instrument where certain features vary based on whether the issuer achieves pre-defined sustainability goals within a timeframe.

Like my lockdown goals, this is an issuer making a statement that they will achieve something by a certain time, such as reducing emissions.

If they fail they have to pay up.

Pendal Sustainable Australian Fixed Interest Fund

An Aussie bond fund that aims to outperform its benchmark while targeting environmental and social outcomes via a portion of its holdings.

This generally takes place though a coupon step-up. An issuer will have to pay investors more if they don’t achieve specific environmental or social goals.

Unlike green, social and sustainability bonds, these are not use-of-proceeds bonds earmarked for specific purposes. They fund general corporate purposes.

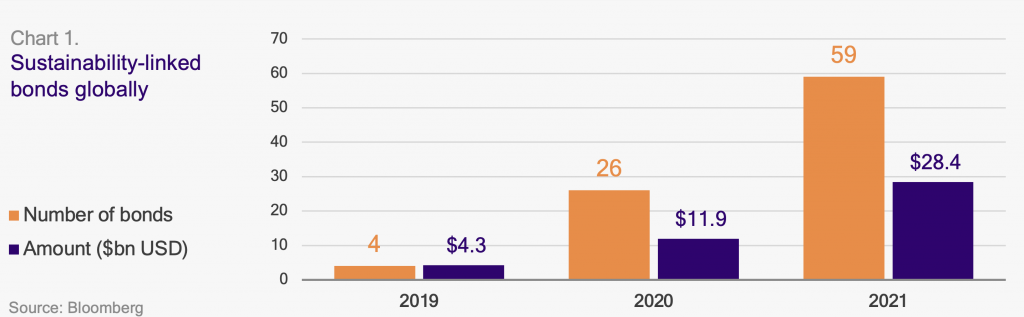

These are relatively new instruments. Globally, there have been a few issuances of sustainability-linked bonds and only one in Australia by Wesfarmers in June.

All sustainability-linked bonds have been oversubscribed and there is growing investor appetite for this type of bond.

Sustainability-linked bonds make public a company’s intention to achieve certain goals by tying financing to sustainability.

For current issuers, they offer a different list of investors and are easier to issue rather than transition or use-of-proceeds bonds.

Only a handful of corporates can do the ring-fencing required for green or social bonds.

Most of these sustainability-linked bonds have featured goals relating to emissions reductions, renewable energy generation, recycling and better waste practices. These are challenges that every business has.

These bonds are a welcome inclusion for capital markets.

They can provide a way for issuers to put something on the line to demonstrate they are serious about targets regardless of the business environment or the energy of specific champions within a business.

Potential concerns

As a new instrument, there are still some outstanding issues, particularly for sustainable investors.

Firstly, these bonds are easier to issue than other sustainable bonds. That means potential uncertainty about whether an issuer cares about sustainability or if they are using the instrument as a way to get cheap debt.

Find out about

Regnan Credit Impact Trust

Secondly, there can be doubts about whether the targets stretch a company beyond what they were planning to do anyway.

There will likely be a “first-mover” benefit whereby company targets become less aggressive compared to peers as more bonds are issued.

Thirdly, there are idiosyncratic concerns for sustainability funds. If an issuer doesn’t hit their step-up, this can potentially hurt an investor. Then it’s no longer a sustainability-linked bond and may need to be sold to comply with the mandate of a fund.

If there is a mass exodus, a step-up of 25bps — the amount generally seen in the international market — won’t necessarily compensate a forced sell-off by a sustainability fund that is not looking to hold more vanilla issuances.

The right direction

This is an evolving market.

Through greater engagement among issuers, arrangers and investors, there is hope that sustainability-linked bonds can improve sustainability offerings in debt markets.

It’s one of many initiatives for helping issuers become more sustainable.

This is about making a public statement with intent, measurable goals and putting something on the line.

It’s working for me.

About Murray Ackman and Regnan

Murray is a Senior ESG and Impact Analyst with sustainable investing leader Regnan.

He also provides fundamental credit analysis on Environmental, Social and Governance factors for Pendal’s Income and Fixed Interest team.

Murray has worked as a consultant measuring ESG for family offices and private equity firms and was a Research Fellow at the Institute for Economics and Peace where he led research on the United Nations Sustainable Development Goals.

Find out more about Regnan here

Regnan Credit Impact Trust is an investment strategy that puts capital to work for positive change.

Pendal Sustainable Australian Fixed Interest Fund is an Aussie bond fund that aims to outperform its benchmark while targeting environmental and social outcomes via a portion of its holdings.

Self storage is an under-appreciated part of the real estate industry that could be a big winner from Australia’s growing population. JULIA FORREST explains the investment opportunity

- Population and demographics underpin growth

- Built-in inflation protection

- Find out about Pendal Property Securities Fund

SELF-STORAGE is not the first place many investors would think of as a place to stash some cash.

But Aussie equities investors looking for opportunities should take a closer look at the industry, says Pendal PM Julia Forrest.

“The world of self-storage is not something you often hear about, but it’s an asset class we like,” says Forrest, who co-manages property investing in Pendal’s Aussie equities team.

Record high immigration and a downsizing trend towards apartment-living will fuel ongoing strength in the self storage industry, says Pendal’s Julia Forrest.

ASX-listed National Storage REIT (ASX: NSR) — which operates 230 centres across Australia and New Zealand — offers exposure to the sector.

NSR is the biggest active position in Pendal’s property strategy, Forrest says.

The opportunity explained

High inflation and rising interest rates have seen a somewhat muted investor appetite for real estate over the past twelve months.

Office assets are trading as much as 30 per cent below book value and the retail and logistics sectors are both under some pressure.

But self-storage assets are defying that trend, underpinned by strong demographics, low maintenance costs and inbuilt inflation protection, says Forrest.

Find out about

Pendal Property

Securities Fund

“Occupancy was supercharged during COVID — and is now returning to normal — but the underlying metrics remain very strong, linked largely to Australia’s strong population growth.”

Self-storage assets were in strong demand during the COVID lockdowns period as young people returned to the family home, expats were forced to return at short notice, and many households had to clear space for working from home.

Now immigration and an ageing population are underpinning the industry’s growth.

Forrest says 70 per cent of self storage clients are individuals looking for somewhere to store their possessions, often prompted by a life event.

The remaining 30 per cent are businesses needing somewhere to store their inventory, building materials, and tools.

Low costs, strong prices

One of self storage’s key attractions is very low maintenance costs compared to other types of real estate.

“It costs very little to maintain — you’re replacing lighting, there’s a minor amount of depreciation. That means you get strong, resilient cash flows.”

As a result, valuations are holding up well as other real estate sectors come under pressure.

Retail real estate faces structural headwinds from the move to online shopping and infinite supply of virtual alternatives to physical store space, says Forrest.

Office is also facing structural change in the way people work and has risks ahead as the economy slows.

“But self storage is not a discretionary purchase — a lot of it is needs based because of those life events, which makes it a little more resilient than the other sectors.

“Self storage is still transacting at book value. Office is 20 to 30 per cent below book value. Retail and even industrial are beginning to see a bit of pressure on book values, but self storage continues to transact at book values.”

Self-storage sites also have the potential for transformation into high value industrial and logistics space, she says.

“Industrial vacancy is incredibly low. For self storage, one of the higher and better uses is as industrial. You don’t get that with office because of zoning.”

Inflation protection

Forrest says self storage offers a level of inflation protection in a portfolio because of the short duration of leases.

“Because you’re leasing month to month, if there is a big inflationary spike you can just lift your rate. You are not locked into a long-term lease. This provides quite a lot of inflationary resilience.”

She says the Australian market is quite immature relative to other markets.

“Self storage space in Australia represents 2.1 square feet per capita. In the US, it’s closer to 6.1 square feet per capita. So, in terms of available space, Australia is relatively under serviced, although the US is a much more mobile market.”

Real estate sentiment shifts

Sentiment towards real estate has shifted markedly in the last few weeks after a tough year amid signs that inflation is coming under control, Forrest says.

“Until very recently, people were very concerned about interest rates and inflation.

“But with a couple of lower CPI readings here and in the US, the market’s pricing of future rate hikes has come way back and that has led to a real estate rally.”

About Julia Forrest, Pete Davidson and Pendal Property Securities Fund

Julia Forrest has managed Pendal’s property trust portfolios for more than a decade. She has 25 years of experience spanning equities research and advisory, initial public offerings and capital raisings.

Pete Davidson is Pendal’s Head of Listed Property. Over the past 34 years Pete has held financial markets roles spanning portfolio management, advisory and treasury markets. he specialises in the property, retail, insurance and infrastructure sectors.

Pendal Property Securities Fund invests mainly in Australian listed property securities including listed property trusts, developers and infrastructure investments.

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

Recent results from the listed property sector show shopping malls are enjoying robust trading conditions, says Pendal’s JULIA FORREST

- Retail remains robust

- Normalisation of returns ahead

- Find out about Pendal Property Securities Fund

A SURPRISING rebound for shopping malls was the standout feature of this year’s real estate investment trust reporting season, says Pendal’s Julia Forrest.

Rising interest rates and the expiration of interest hedges meant earnings declined for many Australian REITs, surprising investors in a sector where performance is typically well-flagged.

“It was quite a strange reporting season for A-REITs because there were some really outsized moves in response to results which is very unusual,” says Forrest, who co-manages Pendal’s property trust portfolios.

“But the positive surprise was in shopping malls where operating metrics improved.

“Occupancy is pushing towards completely occupied — that’s a long way from where we were two or three years ago.

“There’s genuine demand by tenants for more space and for better space and there’s been no supply for four or five years so you’re seeing competitive tension between tenants.”

Positive leasing spreads

Forrest says the return of positive leasing spreads — where the rent charged for new leases is higher than the rent charged for expiring leases in the same property — has also surprised.

Find out about

Pendal Property

Securities Fund

“Scentre Group, which has all the Westfield malls, has not reported positive leasing spreads since 2011. Nobody expected this change.”

This is a positive sign for property owners as it indicates an increase in demand for their property and allows them to generate higher income from the property.

It is also an indicator of a strong rental market and a competitive environment for tenants.

Forrest says several factors are driving this change.

A rising population and wages growth has sent overall retail sales 15 per cent above 2019 levels.

Alongside that is a lack of supply — for nearly five years there has been virtually no new supply of retail space, says Forrest.

“And the retailers themselves are in a better position because they’ve divested their bottom 5 to 10 per cent of stores, the ones that weren’t profitable.

“So, the ones that they have left are more profitable and many of them are still pursuing a growth strategy and opening new stores.”

Forrest says investors have been waiting for signs that interest rates will reduce retail spending.

“You’re beginning to see some deceleration of growth. If you look at the numbers for Scentre Group for July and August, the rate of growth of spending has come off in apparel and in home wares, but it’s still positive.

“But for food and beverage, we’re all still eating out. That’s still really strong.”

Rent reset

Forrest says the reset of rents lower during the COVID shutdown has set the base for a more sustainable outlook for the sector.

“Even if sales decelerate or go backwards, the starting point with rents does give you a bit of a buffer.”

Elsewhere in A-REITS, Forrest says the single standout performer was Goodman Group, which posted earnings growth of 16 per cent, well ahead of expectations of 9 per cent growth.

“They also announced the fact that a fair amount of their development pipeline is going to be data centres.

“Because data centre opportunities come with much bigger development margins, there’s a huge opportunity — $30 to $60 billion over the next five to 10 years. That was very well received by the market.”.

Industrial leasing spreads continue to be strong: “Spreads are still between 15 and 20 per cent. They are beginning to decelerate, but with a vacancy rate below 1 per cent landlords are still in a very strong bargaining position.”

In residential, pre-sales continue to struggle. “It’s coming off a massive base given the amount of stimulus where interest rates were over the last two years, so it’s only natural that the pre-sales numbers continued to struggle,” says Forrest.

“The likes of Stockland are doing smart things — cutting their land sizes to smaller and smaller blocks to keep them affordable. But even so, the numbers that they’re posting look low.

“First home buyers are a reasonable component of the market, and everything comes back to affordability.”

In office, the picture is mixed, she says.

“We are beginning to see a bit of top line growth for the highest quality offices. Office buildings exposed to tenants where everybody’s back at work and have got amenity and high-quality services, they’re doing well.

“But there a very long tail and in aggregate, it’s going sideways.”

Valuations attractive

Overall, Forrest says that with the volatility of the past year behind us, REIT investors are set for a return to more normal performance.

“If you think about FY24 earnings, we would have cycled through pretty much all of the rate hikes so from FY25 onwards, you’re looking more like your standard A-REIT performance.

“A dividend yield of 4.5-5 per cent plus maybe 3 per cent growth for a total return of 7 to 8 per cent.”

She says A-REIT valuations are compelling.

“The sector is pricing cap rates to move another 100 basis points, which implies the market is expecting asset prices to fall maybe another 15 to 18 per cent.

“They are unlikely to fall that far. So, the entry point is interesting.”

About Julia Forrest, Pete Davidson and Pendal Property Securities Fund

Julia Forrest has managed Pendal’s property trust portfolios for more than a decade. She has 25 years of experience spanning equities research and advisory, initial public offerings and capital raisings.

Pete Davidson is Pendal’s Head of Listed Property. Over the past 34 years Pete has held financial markets roles spanning portfolio management, advisory and treasury markets. he specialises in the property, retail, insurance and infrastructure sectors.

Pendal Property Securities Fund invests mainly in Australian listed property securities including listed property trusts, developers and infrastructure investments.

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

The world of office space provides plenty of challenges, but also opportunities if you know where to look, argues Pendal’s JULIA FORREST

- WFH and rising interest rates challenge office property

- Some winners to emerge from the sector

- Find out about Pendal Property Securities Fund

OFFICE space is on the mind of many businesses as work-from-home tension between workers and bosses plays out.

Commercial property, and specifically office property in Australia, has had a challenging time since the pandemic.

The Covid-driven work-from-home phenomenon, along with rising interest rates, have created a very different environment for the sector.

“It’s been very hard to get people back into the office,” says Julia Forrest, who co-manages Pendal’s property securities funds.

“It seems to be more difficult in Melbourne than anywhere else.”

“The physical occupancy in Melbourne is running at about 47 per cent, though recently there have been some big employers mandating staff to be back in the office 50 per cent of the time,” she says.

“That will help.

“Physical occupancy is still pretty low in government because staff have only been mandated to come back into the office one in every five days. That has an impact on retail services and amenities.”

The doubt over the number of days people are spending in the office has made it difficult for government and the private sector to re-sign leases.

It isn’t clear what the demand for space will be in 12 months or two years, let alone five years.

Find out about

Pendal Property

Securities Fund

“Up until recently, we have just seen tenants sign short term leases because they’re not confident about what their occupancy needs will be.

“Landlords have been willingly accepting two-year leases, which they haven’t done in the past, and in some cases one-year leases,” Forrest says.

These short-term leases affect long term returns, but also the amount of finance a landlord can get against a property asset. It’s also triggered creativity between landlords and tenants.

“We’ve seen large tenants commit to new buildings and large amounts of space, and they’ve negotiated contraction rights – the ability to hand back floors,” Forrest says.

“That’s not new in itself. What is different is that they have the ability to reduce the amount of space, even before they occupy the building. Until now, there’s never been contraction rights before commencement.”

Opportunities remain

Forrest says there are still opportunities to find good returns in commercial property, citing 555 Collins Street in Melbourne which has just been developed.

It has a good range on tenants, including Amazon, will open close to fully tenanted, and the construction contract was well negotiated, she says.

Midcaps on

the move

Hear from lithium industry pioneer

Ken Brinsden and Pendal’s

Brenton Saunders

On-demand webinar

“Obviously it’s a tenants market, but office landlords are being a bit more creative. I don’t think things are getting worse, but I do think things will stay tough for quite a while,” Forrest says.

Proeprty investors shold also keep an eye on the unemployment rate.

“Normally you see elevated vacancy rates when unemployment is high,” Forrest says.

“The problem is you have vacancy rates high when unemployment is at 50-year lows, so there’s not a whole lot of employment growth coming through that’s going to fill the space.”

About Julia Forrest, Pete Davidson and Pendal Property Securities Fund

Julia Forrest has managed Pendal’s property trust portfolios for more than a decade. She has 25 years of experience spanning equities research and advisory, initial public offerings and capital raisings.

Pete Davidson is Pendal’s Head of Listed Property. Over the past 34 years Pete has held financial markets roles spanning portfolio management, advisory and treasury markets. he specialises in the property, retail, insurance and infrastructure sectors.

Pendal Property Securities Fund invests mainly in Australian listed property securities including listed property trusts, developers and infrastructure investments.

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

Investing in listed property can look tricky when bond yields are higher and recession fears abound. But it’s a good time to be an active stock-picker, argues JULIA FORREST

- Assets need pricing power and inflation protection

- Supermarket based retail, self storage and logistics the best

- Find out about Pendal Property Securities Fund

INVESTING in listed property when bond yields are higher – and amid talk of a recession — is tailor-made for active stock pickers, says Pendal’s Julia Forrest.

As bond yields increase, the yield on Real Estate Investment Trusts may appear less attractive by comparison. Higher bond yields also indicate higher rates, which can mean higher finance costs for real-estate developers.

But there are opportunities out there for REITs investors who know where to look.

“You want a portfolio with inflation protection, and you want to own assets that have pricing power,” says Forrest, who has co-managed Pendal’s property trust portfolios for more than a decade.

“We’ve positioned our portfolio so we are over-weight in supermarket-based, shopping centre REITS, because the big supermarkets have reasonable pricing power and demand is fairly resilient.

“We also like mall REITS.

“We have self-storage property in the portfolio which works quite well in this environment.

“They have pricing power. About 40 per cent of tenants are business tenants and they get to sign leases on a monthly basis as opposed to locking themselves in for three to five years.

“That means there is protection against inflation.

“We are also overweight logistics and industrial REITS.

“The landlords have pricing power because the vacancy rate is so incredibly low. They’re ability to charge market rents means you have reasonable earnings growth and protection against inflation.”

Forrest says inflation isn’t going away anytime soon.

Find out about

Pendal Property

Securities Fund

“We’re of the mindset that inflation will probably be stickier. We are not going back to this incredibly low inflationary environment,” she says.

Keep an eye on leasing spreads

A metric commonly used by REIT investors is “leasing spreads”. It’s the difference between what a landlord charges on an expiring lease, and what they get on a new lease for the same asset.

During the recent ASX reporting season, industrial REITs were commonly getting leasing spreads of between 15 per cent and 20 per cent.

“The industrial REITs have the widest positive leasing spreads,” Forrest says.

“Over the past five years, retail REITS have had negative leasing spreads as a result of depressed sales. Supermarket based REITS did not go negative, though they were close to flat.

“Mall REIT leasing spreads are no longer negative and as such no longer an earnings headwind.”

The retail REITS have changed tack in recent years, focusing more on services, which are harder to replicate online, and encouraging food and beverage outlets to encourage people to stay longer.

It’s a very positive active leasing strategy for those assets, Forest says.

“We are looking for asset classes that continue to have direct property tailwinds, like industrial, and have pricing power and inflation protection.”

Midcaps on

the move

Hear from lithium industry pioneer

Ken Brinsden and Pendal’s

Brenton Saunders

On-demand webinar

About Julia Forrest, Pete Davidson and Pendal Property Securities Fund

Julia Forrest has managed Pendal’s property trust portfolios for more than a decade. She has 25 years of experience spanning equities research and advisory, initial public offerings and capital raisings.

Pete Davidson is Pendal’s Head of Listed Property. Over the past 34 years Pete has held financial markets roles spanning portfolio management, advisory and treasury markets. he specialises in the property, retail, insurance and infrastructure sectors.

Pendal Property Securities Fund invests mainly in Australian listed property securities including listed property trusts, developers and infrastructure investments.

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

Shopping centre owners and fund managers were the stand-out sectors in a strong reporting season for listed property, says Pendal’s JULIA FORREST

- Listed property performed well during ASX reporting season

- Shopping centres and fund managers stood out

- Find out about Pendal Property Securities Fund

IT WAS a strong reporting season for ASX-listed property largely due to a post-pandemic bounce-back, says Pendal’s Julia Forrest.

Owners of shopping centres, and property fund managers were the stand-out sectors, while office trusts were still struggling.

Higher interest rates will have negative effects on the sector, but locally many Australian Real Estate Investment Trusts (REITs) have hedged against higher debt costs and offer reasonable value.

The pandemic — and government regulations instituted in response — hurt revenue and profits in the property sector. But that’s now ended earnings across the sector were up 19 per cent last financial year — or 14 per cent if you exclude fund managers, Forrest says.

For the owners of big shopping centres, it was a very good earnings season.

“The malls had the biggest rental abatements during Covid, but they are now not too far off where they were pre-COVID. It is quite extraordinary that they’ve been able to come back to where they were FY19,” Forrest says.

While things are improving, they aren’t back to ‘normal’. Vicinity Centres, which owns shopping centres across the country, reported 10 to 12 per cent lower foot traffic.

Find out about

Pendal Property

Securities Fund

“Foot traffic is returning on the weekends but not during the week. Having said that, sales have surpassed FY19 because we’re spending 30 per cent more when we do go to shopping centres,” Forrest says.

“We don’t quite know how much of that is permanent but we are seeing food and beverage coming back in malls. Even cinemas are coming back.”

The other stand-out sector within property was the fund managers, Forrest says, nominating Goodman Group, which focuses on industrial property, and Charter Hall. Both expect to maintain earnings growth this financial year.

“It’s a function of assets under management. They have both been acquisitive the last year or two and they have big development pipelines, and they have the tail wind of asset values going up.”

Industrial property was a particularly strong performer during COVID, as businesses scrambled for space to fulfil e-commerce sales. But unlike many other parts pandemic favourites, industrial remains strong.

“Rental growth in the US is well over 20 per cent. In Europe its ten to 12 per cent. Australia has the lowest industrial vacancy rate in the world … and growth is around 20 per cent. Supply hasn’t been able to keep up with demand,” Forrest says.

While fund managers and shopping centres are performing much better than during the pandemic, the outlook for the office sector is less certain.

“In FY22 it was impacted by lockdowns again,” Forrest says. “It’s just a function of people not returning to work, though there’s a sense that it has started to improve in the past couple of weeks.

“We got through COVID and the flu season … and maybe people want to be in the office because things are getting more difficult.”

There has been a preference for better space, but vacancy rates remain high and more supply will hit the market in coming years.

For investors looking at buying or selling property in a rising interest rate environment, Forrest says there’s three ways to think about interest rates.

The first is ring interest rates make fixed income alternatives more attractive.

The second is that as rates rise, discount rates increase, and asset values fall. An exception she says is industrial space because demand is so high. And finally, the cost of debt rises.

Fortunately, many companies in the REITs sector have hedged their debt exposure, so rising rates won’t hit interest costs too hard.

“And the sector looks reasonable value,” Forrest says. “It’s trading at around 15 times which is a discount to the all-industrials… and excluding the fund managers, it’s at a 16 per cent discount to NTA (net tangible assets).”

“We’re looking at EPS growth of a bit over three per cent … and an initial yield, excluding fund managers, of around five per cent, so eight per cent isn’t bad.”

About Julia Forrest, Pete Davidson and Pendal Property Securities Fund

Julia Forrest has managed Pendal’s property trust portfolios for more than a decade. She has 25 years of experience spanning equities research and advisory, initial public offerings and capital raisings.

Pete Davidson is Pendal’s Head of Listed Property. Over the past 34 years Pete has held financial markets roles spanning portfolio management, advisory and treasury markets. he specialises in the property, retail, insurance and infrastructure sectors.

Pendal Property Securities Fund invests mainly in Australian listed property securities including listed property trusts, developers and infrastructure investments.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Climate change investing tends to focus on removing carbon from portfolios or helping companies decarbonise. But a third opportunity — investing in adaptation — is often overlooked. Regnan’s Alison George explains

- Climate-aware portfolios focused on divestment, decarbonisation

- Adaptation is a third opportunity often overlooked

- Irreversible climate change means adaptation is essential

CLIMATE CHANGE caused by past emissions is likely to be irreversible for thousands of years — even if emissions stopped today.

That was a finding in the latest major report from the United Nations Intergovernmental Panel on Climate Change released in August.

Despite this, climate-aware portfolio construction often focuses on decarbonisation by removing investments with high emissions; tilting to low-carbon stocks and investing in offsets; or by investing in solutions that help companies reduce emissions — such as green hydrogen or low-carbon transportation.

But there is another approach that is largely overlooked — investing in companies that are successfully adapting to climate change.

“Adaptation is always the poor cousin to decarbonisation,” says Alison George, head of research at global responsible investing leader Regnan.

Find out about

Regnan Global Equity Impact Solutions Fund

“But it’s a critical component of climate-aware investing given the amount of climate change already baked into the system from historical emissions.

Huge driver of investment

“Adaptation will be a huge driver of investment going forward, alongside transition.

“Climate-resilient infrastructure and water-efficiency solutions that respond to reduced water availability under climate change are two key opportunity areas.”

Adaptation has been discounted as a legitimate investment option due to two investment views that have dominated in recent years, says George.

The first factor is the group of people who did not believe in climate change in the first place. “For anyone who doesn’t think climate change is real, why would you spend money on adapting?”

The second, more important factor is a belief that focusing on adaptation is like giving up the fight against climate change.

In truth, transition and adaptation are both needed — and both offer investible solutions.

Find out about

Pendal Horizon Sustainable Australian Share Fund

Pendal Group’s responsible investing specialists note in a recent two-part climate-change investing report that the physical impacts of climate change will continue to materialise even in the best-case, low-carbon transition scenario.

The report discusses how permanent changes in rainfall patterns and increased temperatures have significant impacts on agricultural productivity. This means businesses that do not adapt — for example through geographic or product diversification — may see a permanent decline in profits.

“A changing climate also impacts consumer demand,” the report points outs.

“Businesses that don’t pay attention to emerging trends from changing seasons and weather patterns may risk being caught out.

“For example, shorter winters can leave retail businesses with surplus winter stock, while wetter summers may reduce demand for outdoor entertainment.”

The report provides the example of a salmon farming business investing in cooler water offshore pens and ways to lift water oxygen levels.

Download: Pendal’s two-part guide explaining the impact of climate change on business and investing.

About Alison George

Alison George is Regnan’s head of research. She has deep experience in ESG, responsible investment and active ownership. Alison oversees Regnan’s research frameworks, processes and outputs, ensuring it remains at the forefront of industry practice and meets evolving clients needs.

About Regnan

Regnan is a responsible investment leader with a long and proud history of providing insight and advice to investors with an interest in long-term, broad-based or values-aligned performance.

Building on that expertise, in 2019 Regnan expanded into responsible investment funds management, backed by the considerable resources of Perpetual Group.

The Regnan Global Equity Impact Solutions Fund invests in mission-driven companies we believe are well placed to solve the world’s biggest problems.

The Regnan Credit Impact Trust (available in Australia only) invests in cash, fixed and floating rate securities where the proceeds create positive environmental and social change. Both funds are distributed by Perpetual Group in Australia.

Find out about Regnan Global Equity Impact Solutions Fund

Find out about Regnan Credit Impact Trust

For more information on these and other responsible investing strategies, contact Head of Regnan and Responsible Investment Distribution Jeremy Dean at jeremy.dean@regnan.com.

When investing with a sustainable tilt, bonds as an asset class needs to be thought of very differently to equities, property and infrastructure. Pendal’s Michael Blayney explains

- Bond investors have several options to get a sustainable tilt

- Sustainable, green and impact bonds have different attributes

- A multi-asset approach provides greatest flexibility

A MULTI-ASSET approach to building a sustainable portfolio provides many more options than a single asset class.

But it also means investors have to understand how to go green within each asset class — and the implications that decisions in one asset class impacts other asset classes.

In Australian equities, where the market is more concentrated, fundamental active management is the optimal approach.

In international equities, the main implication of a sustainable fund is lower energy exposure. To achieve that it might be necessary to invest in correlated assets in other asset classes.

Sustainable investing in property and infrastructure involves fewer exclusions than the broader equities category, but it can be harder to find dedicated sustainable products.

What about fixed income?

“When investing with a sustainable tilt, bonds as an asset class needs to be thought of very differently to equities, property and infrastructure,” says Michael Blayney, head of Pendal’s Head of Multi-Asset.

“It is less about increasing in value, and more about avoiding defaults and impairments.”

In other words, investing in bonds is about much more than returns, as the world learned during the Covid downturn.

Pendal Sustainable Australian Fixed Interest Fund

An Aussie bond fund that aims to outperform its benchmark while targeting environmental and social outcomes via a portion of its holdings.

Bond markets are not simple, partly because derivatives are often needed across products to achieve interest rate and credit exposure outcomes. That makes bonds far more complicated than buying stocks.

But understanding the complexity allows greater flexibility in creating a sustainable portfolio across asset classes.

Blayney explains that credit spreads — the difference between what a government bond and a corporate bond of the same maturity is yielding — are tighter on sustainable indices.

“That’s because by their nature, they tend to be underweight in the riskier industry sectors, particularly energy,” he says. “ESG [environmental, social and governance] characteristics tend to correlate with higher quality businesses.”

There are also green bonds, where proceeds are earmarked for projects that have a positive impact on the environment. Increasingly there are also impact bonds that target social outcomes.

Comparing the different types of bonds – aggregate, sustainable and green – shows that yield to maturity is lower for the latter two. This is partly due to the country composition, with green bond issuance dominated by Europe.

| Global Aggregate | Global Aggregate Sustainability | Global Green Bond | |

|---|---|---|---|

| Rating | AA- | AA- | A+ |

| Yield to maturity (%) | 1.05 | 0.79 | 0.53 |

| Weighted average spread (basis points) | 34 | 30 | 58 |

| Duration (years) | 7.5 | 7.6 | 8.5 |

Source: Bloomberg. Bloomberg composite rating shown. Data as at 19 July 2021. Global Green Bond Select Index proxied with an index tracking ETF.

“There are tools — futures or interest rate swaps — that allow investors to get access to the desired yield curve without the exposure to the market where the physical capital is allocated,” Blayney says.

The weighted average spread of the securities in the Sustainability Index is lower than the standard index, partly because of the individual securities and partly because of sector differences. While the credit ratings are broadly the same, when one index is rated higher it is always the Sustainability index. All indexes are investment grade.

“In the case of impact bonds, many are issued by banks. So they can have high creditworthiness while allowing capital to be directed to meaningful projects,” Blayney says.

“There’s also a relatively newer, and quite innovative range of credit securities where the coupon paid by the borrower is linked to achievement of various non-financial objectives.”

“Ultimately investors have a range of ways to express ESG preferences or insights within the bonds component of portfolios. We believe a blend of green bonds — sovereign and non-sovereign, other impact bonds, and sustainable corporates — can represent a solid core to a portfolio,” Blayney says.

Is it worth thinking green across your portfolio?

Yes, says Blayney.

“A broad universe of securities allows investors to give effect to a variety of ESG tilts within their portfolios,” Blayney says. “Generally, we expect less tail risk and a quality bias in moving to a more sustainable portfolio.”

About Michael Blayney and Pendal’s Multi-Asset capabilities

Michael Blayney leads Pendal’s multi-asset team.

Michael has more than 20 years of investment management and consulting experience. He was previously Head of Investment Strategy at First State Super and head of Diversified Strategies at Perpetual.

Pendal’s diversified funds provide investors with a variety of traditional and alternative asset classes and strategies.

The team manages our multi-asset portfolios with a focus on strategic asset allocation, active management and tactical asset allocation.

Browse Pendal’s multi asset funds here

Find out about Pendal Sustainable Australian Fixed Interest Fund here

The net-zero movement is driving a ‘circular economy’ which presents opportunities for investors to make money and make the world better, argues Regnan’s MOHSIN AHMAD

- Circular economy crucial to net zero

- Companies with a technology edge are favoured

- Reverse-vending machine maker TOMRA aims to convert trash to cash

- Find out about Regnan Global Equity Impact Solutions fund

BY NOW most people know they need to understand the impact of the “net zero” movement on their investments.

Countries including Australia are pressuring companies to help reduce emissions to zero by 2050 – in order to limit a global temperature rise to 1.5 degrees Celsius above pre-industrial levels.

Science shows that’s the level needed to avert the worst impacts of climate change.

But “impact investors” also believe many activities needed to achieve net zero are an investing opportunity.

“In terms of getting to net zero, energy efficiency and switching to renewables is only going to solve half the problem,” says Mohsin Ahmad, a fund manager with sustainable investing leader Regnan.

“To get the rest of the way, we need to look closely at how we make and use products, and that’s where the circular economy comes in.”

What is the circular economy?

The circular economy is all about moving away from a linear model that we have known since the dawn of the industrial revolution, whereby we extract, we produce and we discard.

“It’s about producing more efficiently, repurposing waste, using more renewable inputs and ultimately that leads to less greenhouse gas emissions” Ahmad says.

It is also an investable trend.

From a portfolio perspective, there are three different angles, says Ahmad:

- “One is to invest in companies that facilitate a more efficient production of goods and services

- “Then there are companies that are enabling recycled inputs, renewables and biodegradable type solutions.

- “And then there are companies that leave the ecosystem in better shape.”

Ahmad says one of the lessons from recent years is that companies that can help reduce natural resource intensity will be winners in the short term.

Find out about

Regnan Global Equity Impact Solutions Fund

“These are companies that help others to minimise their input requirements and deal with some of the inflationary pressures currently prevalent.

“They will also be winners longer term because of their contribution to lowering greenhouse gas emissions.

“If we are going to speed up the transition to net zero, these companies play an important role in addressing the systemic challenge of climate change we face,” he says.

Stock story: Dürr

An example of one such company is German engineering firm Dürr, argues Ahmad.

Dürr is held in Regnan Global Equity Impact Solutions fund.

“They provide solutions to automotive and other industrial customers to improve their resource efficiency of production,” Ahmad says.

“One of the main areas they are focused on is paint application in the automotive space which is very energy and water intensive.

“About 70 per cent of the total energy consumption at an automotive assembly facility takes place in the paint shop. What Dürr has done is to significantly reduce the environmental impact of paint shops.

“They’ve been able to achieve a 67 per cent reduction in energy input in paint shops, a 71 per cent reduction in water, a 73 per cent reduction in volatile organic compounds and a 36 per cent reduction in the amount of paint being used,” he says.

Watch this video to find out more:

Where to start

Investing in circular economy companies starts with understanding the United Nations Sustainable Development Goals, and then finding a company that addresses at least one of the underlying targets in a meaningful way, says Ahmad.

“Then we look for additionality.

“Is the company doing something that’s differentiated? Have they got a technology edge? Are they doing something innovative?

“We also like companies that are in the relatively early stages of adoption of the new technology with large addressable markets.

“Companies where penetration rates are just starting to kick off and there’s a long path of growth ahead.”

Find out more about Regnan Global Equity Impact Solutions fund.

About Mohsin Ahmad

Mohsin is a fund manager with Regnan’s impact investment team. He focuses on Regnan Global Equity Impact Solutions Fund. Before joining Regnan, Mohsin was a senior analyst working on the Hermes Impact Opportunities Equity Fund. He has worked on thematic equity funds such as water, clean energy and agriculture.

About Regnan

Regnan is a responsible investment leader with a long and proud history of providing insight and advice to investors with an interest in long-term, broad-based or values-aligned performance.

Building on that expertise, in 2019 Regnan expanded into responsible investment funds management, backed by the considerable resources of Perpetual Group.

The Regnan Global Equity Impact Solutions Fund invests in mission-driven companies we believe are well placed to solve the world’s biggest problems.

The Regnan Credit Impact Trust (available in Australia only) invests in cash, fixed and floating rate securities where the proceeds create positive environmental and social change. Both funds are distributed by Perpetual Group in Australia.

Find out about Regnan Global Equity Impact Solutions Fund

Find out about Regnan Credit Impact Trust

For more information on these and other responsible investing strategies, contact Head of Regnan and Responsible Investment Distribution Jeremy Dean at jeremy.dean@regnan.com.

Half of all Australian advisers are expected to offer sustainable investing products by next year as interest in green and social bonds grows. Pendal’s Murray Ackman explains why

- 50% of advisers will offer responsible products next year; two-thirds by mid-2020s

- Green, social and sustainability bonds issues growing rapidly

- Not all bonds are alike — investors should watch ‘bang for buck’

A LITTLE over a decade ago, a group of Swedish pension funds phoned the World Bank looking for a way to lend money to projects fighting climate change. The result was the first ever Green Bond.

Today, it’s a market that is growing rapidly.

The number of green, social and sustainability bonds issued in Australia in the first half of 2021 almost equalled the total for 2020.

The variety of issuers is growing too, with more than 30 different institutions issuing bonds across a wide range of sectors.

“This is a market that is becoming more sophisticated and we’re pleased to be able to participate in this fast-growing market,” says Murray Ackman, a credit ESG analyst at Pendal Group. (ESG stands for Environmental, Social and Governance).

Pendal Sustainable Australian Fixed Interest Fund

An Aussie bond fund that aims to outperform its benchmark while targeting environmental and social outcomes via a portion of its holdings.

“We believe the future of investing will continue to be directly funding impact to benefit our environment and the less fortunate.”

So what is a green bond? And how can they play a part in a well-constructed portfolio?

Fundamentally, the term green bond refers to a bond issued to raise finance for a climate-related solution such as clean energy or energy efficiency.

Similarly, a social bond raises finance for an initiative that aims to improve social outcomes in the community like affordable housing or support for indigenous people. You can read here about a social bond that helped put a roof over the head of Sam and his family.

Green bonds can form an important part of a responsible investing portfolio. Financial advisers are rapidly turning towards responsible investing, according to industry researcher Wealth Insights.

About 40 per cent of Australian advisers now offer responsible or sustainable investing products to their clients. This is expected to rise to 50 per cent by next year — and two-thirds by the middle of the decade.

Pendal participated in a few different types of bonds this year, including a bond issued by the Asian Development Bank which funds projects that improve gender equality and women’s empowerment, known as a gender bond.

The funds raised will be used in projects including training and financing women entrepreneurs in Sri Lanka and providing vocational training to women in Laos.

Other types of green bonds include the Climate Awareness Bond from the European Investment Bank, the lending arm of the European Union.

This bond funds renewable energy and energy efficiency projects across Europe, including an offshore wind farm near Portugal, a battery factory in Poland and an energy efficient shopping centre and railway station in Finland.

Find out about

Regnan Credit Impact Trust

Closer to home, the NSW Treasury Corporation Green Bond funds green projects including low carbon transport and buildings, renewable energy and land conservation.

Elsewhere in Australia, the National Housing Finance and Investment Corporation provides cheaper and longer financing to community housing providers to increase the amount of affordable and social housing in Australia.

How can green, social and impact bonds play a part in a portfolio?

Ackman says the performance of green bonds shows they can take the place of traditional bond allocation in a portfolio – and that many investors are taking a broader look at the market.

“We’re finding more and more clients incorporating funds that invest in green, social and sustainable bonds as part of their normal bond allocation,” he says.

When choosing which bonds to invest in, Ackman cautions against simply investing in any bond that says it will bring about an impact.

“We have a rigorous process where all criteria must be met before we can invest. Our impact goals are to find investments that seek to achieve targeted environmental and social outcomes in addition to financial returns,” he says.

Sometimes, the other activities of an issuer can be a warning sign.

“We won’t even look at an impact bond if we’re not happy with the issuer. A tobacco company with a green bond to recycle packaging would not pass our screens or our sniff-test of a sustainable issuer.

“With use of proceeds bonds, we must be happy with the underlying projects.”

Ackman says he has seen a number of impact bonds that ostensibly would support people who impacted by COVID.

“However, after looking a bit closer, we determined these weren’t the types of bonds we wanted to invest in as there were really just repackaged vanilla bonds.”

The other important thing to consider is how much impact the bond will have, what Ackman calls the ‘bang-for-buck’.

“We have an impact database so we calculate and compare how much impact we are helping to achieve by each bond.”

Read the green, social and sustainability bond full report here

About Murray Ackman and Regnan

Murray is a Senior ESG and Impact Analyst with sustainable investing leader Regnan.

He also provides fundamental credit analysis on Environmental, Social and Governance factors for Pendal’s Income and Fixed Interest team.

Murray has worked as a consultant measuring ESG for family offices and private equity firms and was a Research Fellow at the Institute for Economics and Peace where he led research on the United Nations Sustainable Development Goals.

Find out more about Regnan here

Regnan Credit Impact Trust is an investment strategy that puts capital to work for positive change.

Pendal Sustainable Australian Fixed Interest Fund is an Aussie bond fund that aims to outperform its benchmark while targeting environmental and social outcomes via a portion of its holdings.