China faces slowing growth and weak consumer confidence. But there are opportunities for investors willing to take a closer look, argues PAUL WIMBORNE

- Economic stimulus unlikely

- But China equities look good value

- Find out about Pendal Global Emerging Markets Opportunities fund

CHINA’S economic downturn is starting to create attractive opportunities for equity investors, though a mixed performance across the economy means a cautious approach is warranted, says Pendal’s Paul Wimborne.

Beijing’s policymakers are struggling with a mix of slowing growth, weak consumer confidence and rising youth unemployment, as the brief spark of activity after last year’s COVID lockdowns fizzles out.

Markets latched on to a dovish statement from last week’s politburo meeting that said the government planned to step up “countercyclical measures”.

But there are few real signs of significant stimulus, says Wimborne, co-manager of the Pendal Global Emerging Market Opportunities fund.

“There is a lack of confidence in China driving this weakness – so the question is how does the government assess and react to that?

Long-term focus

“We think the key priority for the Chinese government remains building long-term economic and financial system resilience and growth hasn’t yet fallen to the levels that would lead them to aggressively stimulate.

“We think they will continue to push through mini stimulus measures in certain areas where they would like to encourage growth — but we don’t think they’re at a point where we’ll get a big stimulus plan.”

Wimborne says Beijing’s focus on long term resilience means some of the stimulus measures the market is hoping for — like expanding credit availability for the property sector — are unlikely to eventuate.

“The key policy plank that has been in place over the last three years is to shrink the size of the property industry and consolidate around the better run companies with stronger balance sheets.

“We believe that is still a key policy plank for them and it’s very unlikely that they are going to want to shift away from that unless conditions get much worse.”

Find out about

Pendal Global Emerging Markets Opportunities Fund

Direct stimulus for consumers — echoing the West’s policy measures during the pandemic — is also unlikely, says Wimborne.

“The risk of these policies, as we have seen in the West, is inflation. The government has stated that they do not want to move down that path. They don’t think handing out free money is a good way to manage an economy.”

Large-scale stimulus unlikely

The upshot for investors is that any stimulus is likely to be narrowly targeted and aligned with Beijing’s long-term policy outcomes.

“So, for example tax exemptions on electric vehicle sales – that is aligned with the direction they want to take the economy, reducing demand for oil and promoting the size and scale of the domestic electric vehicle manufacturing industry.

“But these are small scale — they help at the margin, but they’re not going to be a big stimulus.”

Value to be found

The implication for investors is not to get fooled by apparently attractive valuations but instead tread a careful path and be selective about investments.

“China’s equity market is very cheap,” says Wimborne.

“While economic growth is slower than people were anticipating at the start of the year, it’s not terrible and there are certain areas where growth is holding up relatively well.

“That means there are parts of the economy we are happy to get exposure to — and parts that we would like to avoid.

“Overall, it leads us to be slightly underweight China but there are key areas which we think show decent growth trends with cheap valuations that are interesting from an investment point of view.”

Wimborne says his preferred investments in China include premium domestic brands Tsingtao Brewery and Proya Cosmetics alongside companies exposed to the energy transition like natural gas distributor ENN Energy and solar panel glass maker Xinyi Solar.

About Paul Wimborne and Pendal Global Emerging Markets Opportunities Fund

Paul Wimborne is a senior portfolio manager and co-manager of Pendal’s Global Emerging Markets Opportunities Fund with James Syme and Ada Chan.

The fund aims to add value through a combination of country allocation and individual stock selection.

The country allocation process is based on analysis of a country’s economic growth, monetary policy, market liquidity, currency, governance/politics and equity market valuation.

The stock selection process focuses on buying quality growth stocks at attractive valuations.

Find out more about Pendal Global Emerging Markets Opportunities Fund

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

A pick-up in cyclical growth in Indonesia is creating opportunities for emerging market investors, argues Pendal’s PAUL WIMBORNE

- Indonesia set for growth

- Retailers, auto dealers and banks well-placed

- Find out about Pendal Global Emerging Markets Opportunities fund

- Join a live webinar with Pendal EM expert James Syme on May 16

INDONESIA has been attracting the attention of investors recently.

What’s driving the interest?

South-east Asia’s biggest economy is a large exporter of commodities like palm oil, coal and nickel — many of which are priced higher since Russia’s invasion of Ukraine.

The rising value of exports follows a period of reduced imports during the pandemic, leaving the Indonesian trade balance strongly in surplus.

“For us, that’s a sign that Indonesia can start to import more on the domestic side of its economy without causing imbalances,” says Wimborne, co-manager of Pendal Global Emerging Market Opportunities Fund.

“So, from a cyclical point of view, Indonesia’s economy looks very well set for above trend growth over the next few years.

“Indonesia is at that sweet spot in the cycle where the export side of its economy is doing well, the currency has the potential to go stronger and domestic demand — which has been subdued for 10 years — looks like it could pick up.”

Return to growth

A return to growth for Indonesia comes after a decade of below-trend growth — a hangover from a consumption binge fuelled by quantitative easing in the wake of the global financial crisis.

Find out about

Pendal Global Emerging Markets Opportunities Fund

“Money was being pushed from the developed world to the emerging world. Like many other emerging markets, Indonesia started to suck in more and more imports, and it led to big imbalances in the economy,” says Wimborne.

“Trade deficits, current account deficits — this is always where the cyclical parts of emerging markets start to become a problem.”

As US and European regulators began to taper quantitative easing in 2013, money started to reverse out of emerging markets and those imbalances became unsustainable, he says.

“At the same time, commodity prices started to fall so the export side of Indonesia’s economy also fell, which exacerbated these imbalances.”

Now, the cycle is turning in Indonesia’s favour with China’s re-opening set to keep a floor under commodity prices.

“Even if commodities fell a bit from here, Indonesia’s trade surplus is at record levels so they would still be in a very good position.”

Boost from manufacturing and labour reform

Wimborne says Indonesia is also placed to benefit from the government’s push to encourage more manufacturing and reform labour markets.

“Indonesia has made some very interesting policy changes which are helping to drive the value add component of its exports.

“The best example is nickel, where a decade ago they implemented a partial ban on selling raw nickel ore to encourage investment in processing plants.

“This encouraged foreign, direct investment into the country and enabled them to capture more of the value add of what they are exporting.”

The political background means the outcome of next year’s election will be important to the country’s economic prospects.

“At the moment they have a big tent coalition,” says Wimborne. “The losing candidate from the last election is part of the cabinet and is one the leading candidates to win the next election.

“We would expect that big tent coalition to hold together and for politics to be relatively stable despite the election year.”

Wimborne’s preferred exposure to Indonesia is through companies that benefit from rising domestic demand, like banks, retailers and auto dealers.

About Paul Wimborne and Pendal Global Emerging Markets Opportunities Fund

Paul Wimborne is a senior portfolio manager and co-manager of Pendal’s Global Emerging Markets Opportunities Fund with James Syme and Ada Chan.

The fund aims to add value through a combination of country allocation and individual stock selection.

The country allocation process is based on analysis of a country’s economic growth, monetary policy, market liquidity, currency, governance/politics and equity market valuation.

The stock selection process focuses on buying quality growth stocks at attractive valuations.

Find out more about Pendal Global Emerging Markets Opportunities Fund

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

How can investors identify promising Emerging Markets? Watch where the tourists go, says Pendal’s PAUL WIMBORNE

- Tourism data provides a useful EM snapshot

- Mexico a standout, Thailand in a slump

- Find out about Pendal Global Emerging Markets Opportunities fund

WHEN investing in Emerging Markets, consider going where the tourists go.

That’s the message from Paul Wimborne, who co-manages Pendal’s Global Emerging Markets Opportunities Fund.

For Paul and his EM team, investing starts at country-level – which means a lot of time spent sifting through national data before deciding where to invest.

One of the best indicators of the health of a country is its tourism levels, he says.

A strong tourism sector creates jobs, boosts local economies, adds to government revenue and foreign exchange earnings, as well as improving the cultural exchange between countries. It signals opportunities for investors in emerging markets.

This is borne out by comparing the tourism sectors in Mexico, one of the better performing emerging economies, and Thailand, says Wimborne.

Both countries rely on tourism and facing similar challenges – reduced capacity among airlines, airport chaos as operations ramp up again, and rising oil prices.

But there is pent-up demand internally and externally, post-Covid lockdowns.

Find out about

Pendal Global Emerging Markets Opportunities Fund

The outlook for the two countries is very different.

“The best tourism news is coming out of Latin America, and particularly Mexico,” Wimborne says. “Passenger traffic is already back to pre-COVID levels in Mexico. That not really a surprise when you consider that tourism in Mexico depends on the United States consumer.

“In the US, consumer confidence is pretty good along with employment conditions. Extrapolating the tourism sector, Mexico is the bright light within emerging markets.”

In contrast, many Asian economies, reliant on China, are struggling to re-emerge from the COVID pandemic.

“If you take Thailand, there were just over 3 million visitors in June 2019, before the pandemic. Pre-COVD tourism contributed about ten per cent of GDP. In August 2022 there were 1.17 million tourists in Thailand,” Wimborne says.

Sustainable and

Responsible Investments

Fund Manager of the Year

“The missing tourists are mostly from China and other Asian countries. That’s because many Asian countries, including China, are trying to minimise the effects of COVID, and are following zero-COVID strategies. Outbound tourism from China is essentially zero.”

There are emerging economies between Mexico and Thailand whose tourism markets fall in the middle.

“In Turkey, visitor numbers are just below the record level set in 2019. In Dubai, numbers are at 85 per cent of pre-COVID levels,” Wimborne says. There is a geographic trend in the health of emerging economies’ tourism markets.

“As you move east from Latin America through the middle east, and then into Asia, tourism markets worsen. In essence, Chinese tourists are the key lagging factor in international tourism recovery.

“Countries like the Philippines, Malaysia and particularly Thailand because of its reliance on tourism, are going to lag emerging markets in other regions. It’s going to take longer for some countries in Asia to recover, than in other parts of the world.”

About Paul Wimborne and Pendal Global Emerging Markets Opportunities Fund

Paul Wimborne is a senior portfolio manager and co-manager of Pendal’s Global Emerging Markets Opportunities Fund with James Syme and Ada Chan.

The fund aims to add value through a combination of country allocation and individual stock selection.

The country allocation process is based on analysis of a country’s economic growth, monetary policy, market liquidity, currency, governance/politics and equity market valuation.

The stock selection process focuses on buying quality growth stocks at attractive valuations.

Find out more about Pendal Global Emerging Markets Opportunities Fund

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

The global commodity cycle could be beneficial for Brazil investors despite concerns over a national election, says Pendal’s PAUL WIMBORNE

- Markets nervous about Brazilian election

- But global commodity cycle looks helpful

- Find out about Pendal Global Emerging Markets Opportunities fund

A NATIONAL election is occupying the minds of Brazil investors but the real key to the country’s prosperity is the global commodity cycle, says Pendal’s Paul Wimborne.

Brazil’s powerful agriculture, energy and mining sectors have been among the world’s big economic winners from the supply squeeze in 2022. Consensus estimates for GDP and earnings growth have been revised upwards in the first half.

But with an election underway between candidates from opposite ends of the political spectrum, markets are starting to get nervous about the ramifications of a change of government.

An October 30 run-off vote is loomig between the incumbent, populist right-wing president Jair Bolsonaro, and former president and head of the left-wing Workers Party, Luiz Inácio Lula da Silva, who is leading in the polls.

Lula is leading Bolsonaro, with 49% of voter support against the incumbent’s 44% ahead, according to a poll last week.

“There’s two main risks the market is worried about,” says Wimborne, co-manager of Pendal Global Emerging Market Opportunities Fund.

Find out about

Pendal Global Emerging Markets Opportunities Fund

“The first — which we are less worried about — is that Bolsonaro is already questioning the electoral system and setting the groundwork for a potential challenge.

“He is from a military background and his government has the support of the military. But we think Brazil’s institutions are strong enough to withstand any challenge.

“The second big risk that markets are pricing in is that Lula wins the election.”

When da Silva was last elected president in 2002, markets sold off sharply, fearing a big spending, left-wing agenda.

“Lula was seen as a hard-left candidate, but moved centre-left when actually took office,” says Wimborne.

“A large part of that was the timing of his presidency. His two terms in office, from 2003 to 2011, coincided with a commodity super-cycle that boosted export conditions for Brazil and provided him with a sound base to increase welfare spending and increase spending on social projects.

“It was an incredibly successful period for Brazil where they dramatically improved the lives of tens of millions of ordinary Brazilians.”

Sustainable and

Responsible Investments

Fund Manager of the Year

The next commodity super-cycle

Ironically, a similar story may play out again in 2022.

“We think that if Lula is elected, the commodity cycle could once again determine how much spending power he has and how successful his government will be.

“He will want to spend more on improving the lives of the lower classes in Brazil and whether he has that spending power will be determined by the export conditions and the commodity cycle.”

Right now, things look helpful.

High prices for energy, agricultural commodities and iron ore are boosting Brazil’s export earnings and lifting government tax revenue.

“It’s too early to say, but it may well be that if Lula is elected he could once again be very fortunate in the timing of the commodity cycle.”

About Paul Wimborne and Pendal Global Emerging Markets Opportunities Fund

Paul Wimborne is a senior portfolio manager and co-manager of Pendal’s Global Emerging Markets Opportunities Fund with James Syme and Ada Chan.

The fund aims to add value through a combination of country allocation and individual stock selection.

The country allocation process is based on analysis of a country’s economic growth, monetary policy, market liquidity, currency, governance/politics and equity market valuation.

The stock selection process focuses on buying quality growth stocks at attractive valuations.

Find out more about Pendal Global Emerging Markets Opportunities Fund

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Micro-economic reforms have driven success in India, but other factors will determine if this is a long-term success story for investors. PAUL WIMBORNE explains

- India’s micro-reforms are powering growth

- “The kind of reforms” emerging markets investors should look for

- But several risks must be considered

A SERIES of important micro-economic reforms in recent years explains the success of the Indian economy, says mmerging markets fund manager Paul Wimborne.

The introduction of a national biometric identification system — the largest of its kind in the world — and the reformation of state-based taxation systems into a single national goods and services tax are paying dividends for both businesses and households.

“These are the kind of reforms you want to look for as an emerging markets investor,” says Wimborne, who co-manages Pendal Global Emerging Markets Opportunities Fund with James Syme.

“These are positive reforms that generate stronger structural growth. India has a very positive story going forward.”

Biometric benefits

India’s biometric national identity system has allowed hundreds of millions of people to access services like banking that they were previously locked out of due to a lack of documentation.

“In the past, if you were from a rural poor area it was very difficult to prove you existed because you typically did not have identification,” Wimborne says. “Once you can prove you exist you can enter the formal side of the economy like banking and taxation.”

This not only lifts economic activity, but it also cuts down on fraud in government payments.

Find out about

Pendal Global Emerging Markets Opportunities Fund

Tax reform

Alongside providing documentation to its citizen, India also reformed its taxation system, moving from a series of state-based duties to a single national goods and services tax.

“Until about three years ago, moving goods from one state to another was like crossing an international border with taxes to be paid and customs checks. The national goods and services tax has removed all those inefficiencies,” says Wimborne.

“Rather than having a warehouse in each of the different states, a business can now have a nationwide distribution.”

The combination of a simpler national taxation system and the conversion of undocumented workers into tax-paying citizens has put a rocket under government revenue.

“In the period April to September this year, personal income taxes grew 28.7 per cent compared to the pre-COVID base two years before.

“Corporate tax collections increased by 23.8 per cent over the same period.”

This is allowing the Indian government to spend and top of its shopping list is big ticket capital expenditure aimed at further improving economic growth and quality of life.

“They’re spending on things improving drinking water and sanitation, building roads and railways, and development of rural areas.

“This is all very positive for future growth of India.”

The benefit of the reforms is also protecting the Indian economy against the economic risks facing much of the rest of the world. As strong oil prices and a high US dollar start to drive inflationary pressures in many economies, India is holding up well.

“The growth story is driving strong foreign direct investment which is holding up the currency. That means the imported inflationary pressures are much lower in India.”

Sustainable and

Responsible Investments

Fund Manager of the Year

This lowers the likelihood of future interest rate rises, further bolstering the economy.

Investors have been reaping the rewards. While the emerging markets index has been flat in US dollar terms in the year to date, Indian stocks are up 25.7 per cent.

The question for emerging markets investors is what risks are on the horizon.

Risks to long-term success

The biggest risk in India is that valuations have risen, says Wimborne.

“Valuations in India have always traded at a premium to emerging markets and that premium has grown larger over the last year.

“We shouldn’t be surprised in the current global environment where the market has been paying up for growth stories that India is benefiting from that, but valuations are something that needs to be watched.”

Still, right now earnings growth looks to justify the valuations. Indian stocks are trading at 24.1 times the next twelve months’ earnings, while earnings growth is forecast at 25.9 per cent. Over the last few months, earnings forecasts have been revised upwards.

The other risk factor is the oil price. India imports oil and rising energy prices tend to have a negative effect on its economy.

So, what could turn a few years of growth in India into the kind of multi-decade success story the world has long been waiting for?

Wimborne says the key is exports.

“Why don’t emerging markets always carry on and fulfil their potential? The answer is that as you grow, your consumers tend to want to buy more goods which sucks in more imports. You need to be able to pay for those imports.

“The question is whether India’s export side — both goods and services — can generate enough foreign exchange to be able to cover what will be increasing demand for imported goods.”

“If we looked in five or ten years time, that will be a key determinate of how sustainable India’s improvements will be.”

About Paul Wimborne and Pendal Global Emerging Markets Opportunities Fund

Paul Wimborne is a senior portfolio managers and co-manager of Pendal’s Global Emerging Markets Opportunities Fund with James Syme.

The fund aims to add value through a combination of country allocation and individual stock selection.

The country allocation process is based on analysis of a country’s economic growth, monetary policy, market liquidity, currency, governance/politics and equity market valuation.

The stock selection process focuses on buying quality growth stocks at attractive valuations.

Find out more about Pendal Global Emerging Markets Opportunities Fund

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

BUSINESSES often promote workplace diversity to investors as a key performance driver. But a new report from responsible investing leader Regnan finds diversity strategies mean little without equity and inclusion.

- New research report analyses diversity, equity and inclusion as indicators of company performance

- Diversity programs won’t improve business performance without equity and inclusion

- The report offers a blueprint for Diversity, Equity and Inclusion (DEI) programs that deliver both social equity and business performance.

- Download: Beyond Diversity: Equity and inclusion as an overlooked opportunity for investors

NEW RESEARCH from responsible investing leader Regnan suggests investors should be asking tougher questions about diversity practices among listed companies.

Diversity has long been promoted by responsible investors as a way to contribute to creating just societies as well as improving business performance.

But the Beyond Diversity report from Regnan’s Insight and Advisory Centre suggests diversity programs can fail to deliver unless companies place equal importance on equity and inclusion.

The work suggests investors should reconsider the indicators they use to evaluate company performance when it comes to Diversity, Equity and Inclusion (DEI) practices.

What are Diversity, Equity and Inclusion?

Diversity: the representation of different kinds of people

Equity: fair arrangements that enable all people to access opportunities

Inclusion: workplace conditions that enable all individuals to make their fullest contributions at work

It’s more likely that equity and inclusion are the factors driving business outperformance, concludes Regnan.

“This finding suggests that investors need to reconsider how they evaluate and engage with companies, increasing their focus on equity and inclusion,” says Regnan co-author and Head of Engagement, Alison Ewings.

The report, Beyond diversity: equity and inclusion as an overlooked opportunity for investors, is based on wide-ranging analysis of the academic literature on diversity, equity and inclusion, as well as interviews with practioners and a review of leading organisations.

The work has identified organisational conditions critical to boosting both diversity and business performance and provides a framework by which they may be considered.

For example a study by Deloitte found that “inclusive” companies were 3.6 times better at dealing with performance issues.

Inclusion framework

The conventional wisdom in responsible investing is that diversity is a driver of performance and, as a result, investors can focus purely on measures of an organisation’s diversity when evaluating investments.

Regnan offers a new framework for judging equity and inclusion, drawing on research by Cornell University’s Lisa Nishii.

The framework highlights three essential pre-requisites for effective DEI:

- Equitable employment practices: eliminating bias at all stages of the employee lifecycle through recruitment, retention and progression.

- Supportive culture: ensuring that employees can make their fullest contributions at work, without fear of negative consequences.

- De-biased decision-making: focusing on the ability of the organisation to elicit, understand and adapt itself to feedback from its people.

The report then offers a blueprint for how this approach can be best implemented.

“Organisations can self-assess against these pre-requisite conditions to identify potential areas of strength or weakness in their current approach,” says Ewings.

“Further, there is an opportunity for investors to consider the presence of these factors as an indicator of the likely contribution of the DEI efforts to the improved performance of investee companies.”

Download Regnan’s Beyond Diversity: Equity and inclusion as an overlooked opportunity for investors

About Regnan

Regnan is a responsible investment leader with a long and proud history of providing insight and advice to investors with an interest in long-term, broad-based or values-aligned performance.

Building on that expertise, in 2019 Regnan expanded into responsible investment funds management, backed by the considerable resources of Pendal Group.

Regnan Global Equity Impact Solutions Fund invests in mission-driven companies we believe are well placed to solve the world’s biggest problems.

Regnan Credit Impact Trust (available in Australia only) invests in cash, fixed and floating rate securities where the proceeds create positive environmental and social change.

Both funds are distributed by Pendal in Australia.

Find out about Regnan Global Equity Impact Solutions Fund

Find out about Regnan Credit Impact Trust

For more information on these and other responsible investing strategies, contact Head of Regnan and Responsible Investment Distribution Jeremy Dean at jeremy.dean@regnan.com.

Pendal Group (ASX:PDL) has announced the completion of its acquisition of US-based value-oriented investment management company, Thompson, Siegel & Walmsley LLC (TSW).

Highlights:

- 96% of TSW client consent to the acquisition secured and expect to achieve 100% consent shortly after close.

- Early completion achieved – reflecting the cultural and commercial alignment of both teams and the strong mutual commitment to realise the growth opportunities ahead.

- John Reifsnider, TSW CEO, to lead Pendal’s consolidated US business and joins the Pendal Group Global Executive Committee.

- Step change in Pendal’s FUM: more than doubling US FUM to A$62.5 billion (US$47.0 billion)* and increasing total Group FUM by 31% to A$139.3 billion.

- Expected to be double digit EPS accretive in the first full year, post completion.

PENDAL Group CEO, Nick Good (pictured), said: “We are thrilled to welcome the TSW team and its clients to Pendal Group.

“Client support has been incredibly strong, with 96% TSW client consent received in just 11 weeks. It is testament to the compatibility and drive of the two organisations and their teams that we have completed the acquisition well ahead of original expectations.

“As a result of the acquisition, we will double our addressable market in the US and extend our ability to generate new FUM through the distribution of both TSW and JOHCM products across an expanded global network.

“Today, John Reifsnider becomes the new leader of the combined US business. John and I have worked closely together to complete the transaction expeditiously, cognisant of the importance of client and team support for the go-forward proposition. I am very pleased that John will be taking on this key role.”

Mr Reifsnider said: “The team and I are more convinced than ever of the merits of bringing together these two culturally aligned and forward-looking businesses.

“We believed from the outset that both organisations are a natural fit with compatibility in investment philosophy, client service and our entrepreneurial approach.

“The teamwork in delivering early completion and client consent is validation of this view and bodes well for future success.”

Broader range of product solutions

Mr Good commented: “This acquisition significantly broadens the range of product solutions we can offer clients via an expanded distribution network, and we are focused on providing our combined investment strategies to our enlarged client base as soon as possible.

“Both organisations share a core belief in investment team autonomy, and TSW’s investment autonomy will be preserved, an important consideration for our clients.

“As complementary businesses, with almost no overlap of investment strategies, together, we will be better placed to take advantage of the growth opportunities we see in the US market.”

There was strong support for the acquisition from Pendal’s institutional and retail shareholders and as a result, the successful Placement and Share Purchase Plan raised A$380 million in total.

This equity raising reduced the debt and balance sheet funding which was required to complete the transaction to A$57 million (US$44 million). This outcome provides additional balance sheet strength and capacity for Pendal to accelerate its growth opportunities.

Mr Good concluded: “The acquisition has delivered immediate value for our shareholders and a step change in Pendal Group’s diversification, scale and client offering.

This creates enhanced opportunities for growth, particularly with increasingly positive investor sentiment, a flourishing US economy and the global economic rebound.”

* Includes TSW FUM of US$24.6 billion (A$32.6 billion). Based on exchange rate of AUD:USD of 0.7518 at 30 June 2021.

Visit Pendal’s shareholder website for more information.

About Pendal

Pendal Group (“Pendal”) is an independent global investment manager focused on delivering superior investment returns for clients through active management. Pendal manages A$106.7 billion in FUM (as at 30 June 2021) in client assets through J O Hambro UK, Europe & Asia; JOHCM USA; Pendal Australia and Regnan.

Pendal operates a multi-boutique style business delivering superior results across a global marketplace through a meritocratic investment-led culture. Its experienced, long-tenured fund managers have the autonomy to offer a broad range of investment strategies with high conviction based on an investment philosophy that fosters success from a diversity of insights and investment approaches.

Listed on the Australian Securities Exchange since 2007 (ASX: PDL), the company has offices in offices in Sydney, Melbourne, London, Prague, Singapore, New York, Boston and Berwyn, Pennsylvania in the US.

About Thompson, Siegel and Walmsley (TSW)

TSW is a US-based value-oriented investment management and advisory company, operating primarily in the long-only equity (International and US) and fixed income asset classes with US$24.6 billion (A$32.6 billion) of FUM as at 30 June 2021.

Established in 1969 and headquartered in Richmond, Virginia, the company has a well-known record in attracting and retaining investment talent, with an average tenure of 12 years among the investment team members.

Investors who want to make a difference in the world have far more potent weapons at their disposal than merely selling their shares.

- Screening strategies not enough to drive change

- Investors need a new approach – hold and vote

- Exxon Mobil defeat a clarion call for shareholder power

THIS YEAR’s stunning defeat of Exxon Mobil by Engine No.1, a tiny activist fund that resulted in three new directors on the board of one of the world’s largest fossil fuel companies, is the most public example of the rise of a new type of shareholder engagement.

It is expected to accelerate a dawning realisation among investors that when it comes to public equity markets, there are stronger avenues for change than traditional methods of screening and divesting companies.

If every climate-minded investor sold their coal shares, that would leave control of those companies in the hands of the least climate-minded owners.

Susheela Peres da Costa

“But while there are good reasons for an investor to not want to be exposed to fossil fuel assets, it’s another thing altogether to assume a company cares who owns its shares.

“It’s worse than having no impact because it makes for a false sense of security.

“Even if every climate-minded investor sold their coal shares, that would leave control of those companies in the hands of the least climate-minded owners.”

Regnan’s work suggests investors who want to make a difference in the world have far more potent weapons at their disposal than merely selling their shares.

Stewardship initiatives, in which institutions use their investor influence for change, are proving to be a powerful lever.

Investor stewardship can also be successful putting resolutions to boards and reigning in unhelpful corporate influence on government policy.

Advocacy is an area where coalitions of smaller investors can have a real effect, directly asking regulators, industry bodies and governments for change.

And investing in disruption to drive change is also an effective strategy.

But what about small investors without access to these avenues?

“Figure out where your power really is,” says Peres da Costa. “Unless you are an enormous institution, big enough to move market prices, you have much more power as a consumer – what products and services you buy, who from, and whether you are vocal about why.

“So, you say ‘I don’t want my shares ever to be voted in favour of a director who is trying to entrench fossil fuels in the economy’. And you check which financial service providers commit to that before you entrust them with your money.

Find out about

Regnan Global Equity Impact Solutions Fund

Peres da Costa points out that this simplifies many of the challenges associated with trying to invest responsibly, by focussing the discussion on what kind of impact investors want to have.

“It’s too easy to get caught up in details when you focus on divestment, or ‘screening’,” Peres da Costa says.

“For instance, should divestment focus on companies that produce fossil fuels? Or firms that burn them, releasing global warming gases into the atmosphere? Are firms that support the fossil fuel supply chain in or out? Coal ports? Gas pipelines? Roadside retailers of petrol?

“Burning fossil fuels is a major part of industries as diverse as energy generation, steelmaking and aviation. Many of the largest organisations involved in fossil fuels are governments; are we divesting airlines and countries too?

“Are all carbon emissions equal? Is coal burnt to make steel for wind turbines worse than lower-carbon oil to air-freight fresh tropical fruit to temperate markets?

“These are often interesting debate topics, but dodge the deeper question most clients are interested in addressing: What does my money do?”

Read more about what investors can do to drive change at The Divestment Dilemma.

About Susheela Peres da Costa

Susheela is Regnan’s head of advisory. She has more than 15 years of domestic and international experience advising institutional investors on responsible investment.

As Head of Advisory, she has assisted small foundations through to the world’s largest institutions, including a successful 18-month project in Switzerland responsible investment leadership for a global full-service bank and strategic advice to the UN-backed Principles for Responsible Investment on upgrading stewardship.

Susheela chairs the Responsible Investment Association of Australasia and is special adviser to the co-chair of the Australian Sustainable Finance Initiative.

About Regnan

Regnan is a responsible investment leader with a long and proud history of providing insight and advice to investors with an interest in long-term, broad-based or values-aligned performance.

Building on that expertise, in 2019 Regnan expanded into responsible investment funds management, backed by the considerable resources of Pendal Group.

Regnan Global Equity Impact Solutions Fund invests in mission-driven companies we believe are well placed to solve the world’s biggest problems, while the Regnan Credit Impact Trust (available in Australia only) invests in cash, fixed and floating rate securities where the proceeds create positive environmental and social change.

Find out about Regnan Global Equity Impact Solutions Fund

Find out about Regnan Credit Impact Trust

For more information on these and other responsible investing strategies, contact Head of Regnan and Responsible Investment Distribution Jeremy Dean at jeremy.dean@regnan.com.

Find out about

Regnan Global Equity Impact Solutions Fund

Here’s our weekly Bond, Income and Defensive Strategies wrap from Pendal portfolio manager Tim Hext (pictured).

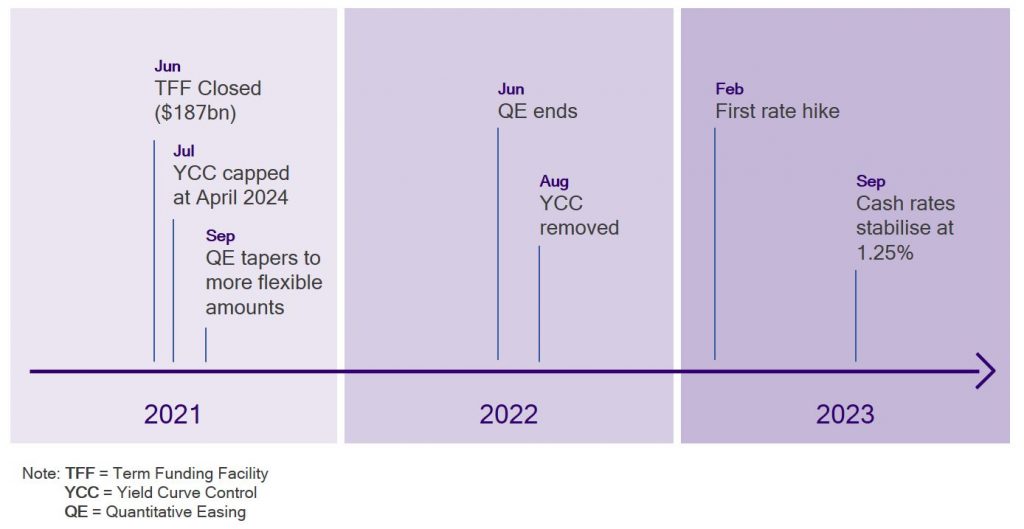

THE RESERVE BANK last week started the slow unwind of extraordinary monetary policy.

In recognition of the overall stronger economy, Yield Curve Control will not extend beyond the current April 2024 bond.

When the current $100 billion of Quantitative Easing (QE) ends in September, the pace will fall from $5 billion a week to $4 billion a week. It will be reviewed again in November.

Together with the closing of new borrowing from the Term Funding Facility (in total $187 billion lent) this represents the first steps back toward conventional monetary policy.

In our view the timeline looks something like this:

QE will likely taper further once the US Fed starts its own taper later this year.

The end of QE is probably brought forward by recent AUD weakness, relieving RBA concerns that higher rates here would push the AUD above 80c.

Of course there are a number of clear criteria laid out by the RBA to actually hike cash rates.

Inflation must be sustainably within the 2-3% band. For that to happen they believe wages need to be at least 3%, which in turn requires full employment.

The view is full employment is nearer 4% than 5%. We wrote extensively about employment and wages in our last newsletter. (Contact a Pendal key account manager for a PDF copy).

Given our views on inflation and wages we expect rates to lift-off in the first half of 2023. We expect them to stop around 1.25% to 1.5% before staying there for some time.

Of course this is a view into the future. In a week dominated by lockdowns and US bond rallies, bond markets here saw lower yields.

There is a lot more to play out in US employment markets in the months ahead.

Unlike Australia where jobs are now higher than before Covid, the US still has 8.5 million jobs “missing”.

The bulls blame higher welfare payments discouraging people from returning to low-paying jobs. The bears suggest COVID has shown the way for businesses to permanently operate with fewer staff.

The truth is likely a bit of both.

How this plays out in the months ahead will set the tone for bonds markets and eventually equity markets.

We will dive deeper into this topic in the weeks ahead.

About Tim Hext

Tim Hext is a portfolio manager with Pendal’s Bond, Income and Defensive Strategies (BIDS) team.

Led by Vimal Gor, Pendal’s BIDS boutique is one of the most experienced and well-regarded fixed income teams in Australia. In 2020 the team won the Australian Fixed Interest category in the Zenith awards.

The team oversees $22 billion invested across income, composite, pure alpha, global and Australian government strategies with the goal of building Australia’s most defensive line of funds.

Find out more about Pendal’s fixed interest strategies here

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

The next five years will see inflation significantly higher than the past decade. We should be alert to this but not alarmed says Pendal portfolio manager Tim Hext in our weekly Bond, Income and Defensive Strategies note.

Find out more about Pendal’s fixed interest strategies

THE two big highlights of the week were the federal budget and US inflation numbers — and they are more closely linked than it might seem.

Federal Budget

The RBA and Treasury now forecast GDP and employment at full capacity for next year.

That means no slack left in the economy. Normally this would signal a tightening of monetary and fiscal policy. But times have changed.

Invoking the continuing transition from the crisis, the RBA and government are both firmly foot-to-the-floor.

For the government a looming federal election translates to “why not keep handing money out?” After all no one seems too troubled.

Even the usual crowd of economists who warn of impending doom from too much debt have gone quiet. The only ones who can hold their heads high are proponents of Modern Monetary Theory. They understand better just how government debt works.

The RBA seems to have gotten itself in a corner. Like the rest of us they expected the health crisis to be far worse. Unlike us they made commitments (or guidance in some cases) out to 2024 based on that expectation.

The RBA is more oil tanker than speedboat when it comes to turning around. For now they remain committed to Quantitative Easing, Yield Curve Control and no rate hikes.

This is now based solely on benign inflation and wage forecasts — not growth and employment, which are strong.

Future RBA statements will be watched closely for watering down of rhetoric.

US inflation

That leads us to this week’s US CPI numbers. CPI was 0.8% for April and 4.2% year-on-year.

Extraordinary numbers.

Economists and no doubt the Federal Reserve will be quick to reassure us this is transitory.

Supply bottlenecks in the auto industry have prompted a spike in used car and rental car prices. Hotel rooms, airfares, sporting events — most things have spiked as the economy reopens.

These spikes won’t repeat but other spikes are coming. Rents are creeping up and wages are already rising. Commodity prices are taking off.

If there is excess capacity in labour markets perhaps the Fed can get away with the idea of ignoring these transitory factors and we can return to business-as-usual low inflation.

I suspect though with ongoing massive fiscal and monetary stimulus the inflation genie is out of the bottle.

Low inflation expectations may become, if not unhinged, at least challenged in the years ahead. Wages could well follow. Inflation in Australia will also follow.

Eventually technology and demographics will keep a lid on inflation becoming a massive problem.

But the next five years will see inflation significantly higher than the last 10 — something we should all be alert but not alarmed at.

Tim Hext is a portfolio manager with Pendal’s Bond, Income and Defensive Strategies (BIDS) team.

Led by Vimal Gor, Pendal’s BIDS boutique is one of the most experienced and well-regarded fixed income teams in Australia. In 2020 the team won the Australian Fixed Interest category in the Zenith awards.

The team oversees $22 billion invested across income, composite, pure alpha, global and Australian government strategies with the goal of building Australia’s most defensive line of funds.

Find out more about Pendal’s fixed interest strategies here