PENDAL GROUP (ASX: PDL) today announced it has entered into an agreement to acquire 100% of Thompson, Siegel & Walmsley (TSW), a US-based, value-oriented investment manager, for US$320million (A$413 million).

Established in 1969 and headquartered in Richmond, Virginia, TSW operates primarily in long-only equity (US and international) with US$23.6 billion (A$30.5 billion) of funds under management (FUM).

The acquisition price represents 7.6x 1H21 EBITDA (annualised, excluding synergies) and is expected to be double-digit EPS accretive in the first full year after completion.

Pendal Group Chairman Mr James Evans said: “This is a strategic and compelling opportunity to acquire a highly successful complementary business, which will create immediate value and facilitate our growth opportunities in the US market.

“The acquisition will deliver scale and diversification benefits for Pendal across investment capability, asset classes, geographies and distribution channels.

“The Board believes this acquisition will accelerate shareholder returns and strengthen the diversity of earnings.”

Transaction highlights:

- The acquisition is expected to be double-digit EPS accretive in the first full year after completion.

- Pendal’s consolidated FUM will increase 30% to $A132 billion after the acquisition. Its US client FUM will increase 112% to US$44.7 billion (A$57.8 billion).

- TSW has robust business momentum driven by recent large client wins and strong investment performance. Four out of the six funds (where TSW is the sole sub-advisor) hold a 4/5-star Morningstar rating and rank in the top quartile over the last three-year period.

- The acquisition will double Pendal’s addressable market in the US.

- TSW CEO Mr John Reifsnider will be appointed CEO of Pendal’s combined US business.

- The US$320 million purchase consideration will be funded with a combination of equity, debt and existing capital. Equity will be raised through a fully underwritten placement and — to enable retail shareholder participation — a shareholder purchase plan.

Pendal Group CEO Mr Nick Good said: “TSW is a natural strategic and cultural fit with Pendal and expands our successful diversified business model in the largest equity market in the world.

“TSW is highly complementary to Pendal’s US business, with almost no overlap of investment strategies and clients.

“This will deliver the opportunity to generate new FUM through the expansion of our addressable market in the US and our ability to distribute both TSW and JOHCM products through an expanded global distribution network.

“Both businesses have solid flow momentum and high-performing investment strategies. With this growth profile I believe we will be well placed to take advantage of more opportunities inherent in the positive US economic outlook and increasingly strong investor sentiment globally.”

Highly regarded

TSW is a highly regarded value-oriented investment manager. It has a solid base of institutional and sub-advisory relationships and a track record of strong investment performance. Some 86% of TSW FUM outperformed benchmarks over the past year, highlighting the discernable rotation to value strategies over the past six months.

TSW’s investment capability spans international value, US equity and fixed income.

TSW has an experienced, stable team of 74 employees and a long-tenured and talented investment team of 20, with deep bench-strength across all strategies.

Its recent large client wins are testament to the quality of the team and the momentum of the business. The TSW team are fully supportive of the acquisition and are aligned with Pendal’s values, investment independence philosophy, and its growth aspirations.

Alignment of culture and business models

“Cultural fit is all-important in fund management acquisitions,” said Mr Good. “Both parties have put significant effort into considering compatibility, investment, client approach and alignment and mutual commitment to growth.”

TSW’s CEO Mr John Reifsnider will be appointed CEO of Pendal’s combined US business, taking over the role from Mr Good. Mr Reifsnider will also join Pendal’s global executive committee.

“John is an outstanding leader and the right person to head the combined US business,” said Mr Good. “I have every confidence he will continue to drive the positive momentum that is evident in both companies and seize the new growth opportunities we see ahead of us.”

Mr Reifsnider said: “This is a unique opportunity for TSW to join a strategically compatible and highly regarded global investment management company that is a natural fit and has strong alignment to our investment approach and culture.

“All of us at TSW are thrilled to be joining Pendal Group. We see excellent potential for growth and an exciting future.

“I am delighted to take on the role of CEO of the combined businesses. Pendal has been very successful in the US with an extraordinary 10 consecutive years of positive flows and an enviable reputation in the market.

“Investment autonomy is fundamental to both our businesses and to our success. That match has been a very important consideration for the TSW team.”

Mr Good said: “Pendal’s acquisition of JOHCM was a success. We are approaching this acquisition of TSW with the same intent and focus and are confident that we will be able to implement a seamless transition.”

Equity raising

To fund the acquisition Pendal is undertaking a fully underwritten placement to raise A$190 million through the issue of 27.9 million new fully paid shares, representing about 8.6% of current issued capital.

Details of the offer can be found on Pendal’s shareholder webpage here.

The shareholder purchase plan (SPP) will open on May 17, 2021 and close on June 7, 2021.

The SPP is subject to the terms set out in the SPP offer booklet, which is expected to be lodged with the ASX and sent to eligible retail shareholders following the opening of the SPP offer on May 17, 2021.

Pendal expects to complete the transaction in the September quarter, 2021.

Further details are set out in the investor presentation provided to the ASX [PDF download] on Monday, May 10, 2021.

The investor presentation contains important information including key risks and foreign selling restrictions with respect to the Offer.

This presentation can also be accessed on the Pendal website at https://investors.pendalgroup.com/Investor-Centre.

Webcast details

Pendal will present in relation to its 1H21 half year financial results and the acquisition of TSW today, Monday May 10 at 10.30am AEST. The webcast of the results announcement will be available live at https://webcast.openbriefing.com/7243.

If you wish to view the presentation live via the webcast we recommend logging in 10-to-15 minutes prior to start time.

About Thompson, Siegel and Walmsley

TSW is a US-based value-oriented investment management company, operating primarily in the long-only equity (international and US) and fixed income asset classes with US$23.6 billion of FUM at March 31, 2021.

Established in 1969 and headquartered in Richmond, Virginia, TSW is 75.1% owned by the NYSE listed BrightSphere Investment Group (BSIG), but operates as an independent, autonomous, indirect subsidiary. The remaining 24.9% of shares in TSW are held by TSW current and former management.

TSW has a well-known record in attracting and retaining investment talent, with an average tenure of 12 years among the investment team members.

About John Reifsnider

John has been CEO of TSW since January 2021 and has been with the firm for more than 15 years. He was appointed Co-President of TSW in September 2018 overseeing the day-to-day management of the firm and serving as member of the Board of Managers.

Prior to that, he was the Head of Distribution. He remains highly engaged in TSW’s distribution activities. Before joining TSW in 2005, he was Managing Director at Atlantic Capital Management, responsible for business development and client service.

John started his career in the investment industry in 1990.

John earned his BBA from the University of Toledo, is currently registered with FINRA, and is registered as an Investment Adviser Representative. He is an active volunteer for non-profit youth sports organisations.

About Pendal

Pendal Group is an independent global investment manager focused on delivering superior investment returns for clients through active management. Pendal manages A$101.7 billion in FUM (at March 31, 2021) through J O Hambro UK, Europe & Asia; JOHCM USA; Pendal Australia and Regnan.

Pendal operates a multi-boutique style business across a global marketplace through a meritocratic investment-led culture. Its experienced, long-tenured fund managers have the autonomy to offer a broad range of investment strategies with high conviction based on an investment philosophy that fosters success from a diversity of insights and investment approaches.

Listed on the ASX since 2007 (ASX: PDL), the company has offices in Sydney, Melbourne, London, Prague, Singapore, New York, Boston and Berwyn.

Sustainable investing leader Regnan has analysed the environmental impacts of hydrogen production in a new research report aimed at investors.

Regnan’s H2 beyond CO2 report reviews popular hydrogen production technologies and identifies factors that may lead to competitive advantages and potential constraints.

The report — produced by Regnan’s Abby Frank, Alison George, Maxime Le Floch and Oshadee Siyaguna — can be downloaded here.

-

- Hydrogen production shows strong potential for investors but there are issues to be managed

- Investors can identify key factors that will influence winners and losers

- Listen to an interview with the report’s authors on Decarb Connect podcast

- Find out more about Regnan or contact Jeremy Dean at jeremy.dean@regnan.com

THERE’S a lot of excitement among investors, scientists and politicians about the scope for hydrogen to be a major energy source of the future, based on its potential contribution to decarbonisation goals.

But there is still a long way to go before hydrogen can be considered a practical alternative to traditional energy sources such as gas.

The conundrum for the world economy between now and 2050 is to reach net-zero emissions while providing enough energy to meet demand from an expanding global population.

This energy transition is at the heart of the United Nations’ Sustainable Development Goals (SDGs), the global agenda launched in 2015 to tackle the world’s toughest environmental and social challenges.

In theory, hydrogen could be used as a fuel for transport and power, as heat for industrial processes and buildings, and as a feedstock for chemicals like fertilisers and industrial products like metals.

In practice, hydrogen’s appeal is difficult to judge.

Hydrogen production needs to be assessed across all sustainability dimensions. Investors and companies are wary of locking into a technology only to find problems later on.

This happened with earlier generations of biofuels and liquified natural gas, all of which were initially promoted as impact solutions.

“It’s a relative game between low-carbon technologies,” says Maxime Le Floch, an analyst with sustainable investing leader Regnan.

Mr Le Floch is a contributor to H2 beyond CO2, a new Regnan research report that examines the environmental impact of hydrogen production for investors.

He is part of a London-based team that manages the Regnan Global Equity Impact Solutions Fund, which aims to generate market-beating, long-term returns by investing in solutions to the world’s environmental and societal problems.

Hydrogen’s potential

“Hydrogen is competing against other technologies for decarbonisation in different parts of the economy,” Le Floch says.

“New hydrogen fuel vehicles have been touted, though with the pace of progress of electric vehicles, hydrogen becomes less likely there. But in other applications like heavy industrial and steel-making, hydrogen might be very interesting.

“We need to keep in mind that these are very long investment cycles, so decisions made today have an impact in 10, 20 or 30 years time. There is a whole carbon cost curve that shows where different solutions stack.”

Growing support for investment in hydrogen technology needs a dose of scepticism — not because the enthusiasm is wrong. It’s just too early to say it’s correct.

“The nature of the investment process within the Regnan Global Equity Impact Solutions team is very comprehensive,” says Regnan’s head of research Alison George, a co-author of the report.

“It’s not just looking at SDGs, but all of the environmental and social impacts. Hydrogen might look attractive, but what are all the implications?”

Key economic, environmental and social issues associated with H2 production. Source: Regnan

George says when researching hydrogen, the economics are discussed constantly, and decarbonisation is talked about some of the time. “But there were gaps in the environmental case.”

“We needed some of these questions answered to determine if it was suitable for the fund. It was really a process of trying to fill some pretty surprising gaps,” she says.

The result was H2 beyond CO2, a report that looks beyond carbon emissions analysis alone.

The report can be downloaded here.

“The entire approach of the fund is to find solutions to the grand problems of sustainability and that approach informs investment decisions. There’s a preference for solutions with the greatest contribution to make, and the clearest pathway to making a difference,” George says.

Key hydrogen production technologies

The report concludes that climate change benefits can be achieved through both green hydrogen and blue hydrogen, but with some important caveats.

For green hydrogen, which is made with electricity, the energy source drives the climate outcomes and the majority of other environmental impacts.

An answer, potentially, is to couple electrolysers with intermittent renewables like wind and solar to help manage output peaks and avoid generator curtailment.

That would support growth in renewables and improve the economics of hydrogen production as well as maximising the contribution to climate goals.

“Few of us have been asking the right questions… this report gives essential answers on the sustainability of climatetech” – Alex Cameron, Decarb Connect podcast

Blue hydrogen has the potential to be a sustainable and economic option for hydrogen production — particularly in regions with local natural gas resources, existing pipelines and transport infrastructure.

But it relies on successful carbon capture and reliable carbon storage. They must be maintained for longer periods to be climate effective.

The Regnan report shows there is much more work to be done in the field of hydrogen.

“Some solutions look great on paper but when you scrutinise the environmental impacts things start to get more nuanced,” Le Floch says. “There’s a great need for more research.”

Case study: hydrogen production with offshore wind

Almost 200 years ago, physicist Hans Christian Orsted discovered electromagnetism, and changed the course of history.

Orsted laid the foundation for the modern generation of electricity, and his name is now synonymous with energy in the Scandinavian countries. Orsted, the company, is the biggest offshore wind developer in the world.

Orsted is one of the few global companies able to generate huge amounts of energy through its offshore wind projects across Europe and in Taiwan. It is a critical piece of the renewable energy puzzle, and not just in terms of wind.

“If you want to decarbonise hydrogen production then you need large sources of energy,” says Regnan’s Maxime Le Floch.

“You can take electricity from the grid but that does not always work. So this is why developing hydrogen production with offshore wind makes sense and projects are being announced.

“Offshore wind projects are on a big scale – and scale is a challenge for other sources of renewable energy like onshore wind and solar,” Le Floch says.

“We are talking about gigawatt scale projects in the North Sea, for instance.”

It demonstrates the necessary links between different energy sources, if renewable power is to reach its potential. It also highlights that companies that could benefit from greater use of hydrogen don’t necessary sit in that sector.

“Orsted is getting involved in exploratory projects around hydrogen and much of the work is to demonstrate that the technology can work,” Le Floch says.

About the authors

Alison George is Regnan’s head of research. She has deep experience in ESG, responsible investment and active ownership. Alison oversees Regnan’s research frameworks, processes and outputs, ensuring it remains at the forefront of industry practice and meets evolving clients needs.

Oshadee Siyaguna is a senior ESG analyst with Regnan, responsible for research and engagement and the generation of analysis and insights on ESG themes and issues. Oshadee joined Regnan as an ESG analyst in 2015. Prior to that he was Assistant Vice President at PolitEcon Research.

Abby Frank is an ESG analyst with Regnan, responsible for research and engagement and the generation of analysis and insights on ESG themes and issues. Abby joined Regnan in 2018.

Maxime Le Floch is an investment analyst with Regnan’s Global Equity Impact Solutions team. He has a decade of experience in sustainable investment. Maxime previously worked as an investment analyst at Hermes where he helped manage Hermes Impact Opportunities Equity Fund and led the integration of ESG and stewardship across investment strategies.

About Regnan

Regnan is a responsible investment leader with a long and proud history of providing insight and advice to investors with an interest in long-term, broad-based or values-aligned performance.

Building on that expertise, in 2019 Regnan expanded into responsible investment funds management, backed by the considerable resources of Pendal Group.

Regnan Global Equity Impact Solutions Fund invests in mission-driven companies we believe are well placed to solve the world’s biggest problems, while the Regnan Credit Impact Trust (available in Australia only) invests in cash, fixed and floating rate securities where the proceeds create positive environmental and social change.

Both funds are distributed by Pendal in Australia.

Find out about Regnan Global Equity Impact Solutions Fund

Find out about Regnan Credit Impact Trust

For more information on these and other responsible investing strategies, contact Head of Regnan and Responsible Investment Distribution Jeremy Dean at jeremy.dean@regnan.com.

One year after the market low, here’s how head of equities Crispin Murray (pictured) drove outperformance for Pendal Focus Australian Share Fund during the pandemic. Chris Adams reports.

THIS week marks one year since the market’s low point during the pandemic.

Since the pre-Covid peak on February 21, 2020, Pendal Focus Australian Share Fund has returned 2.9% after fees (to Mar 19, 2021).

The benchmark ASX 300 lost 2.2% over the same time according to Morningstar.

A key factor in the fund’s 5.11% outperformance against the benchmark has been its ability to perform through each phase of the market last year. This is driven by our approach to portfolio construction.

Pendal Focus Australian Share Fund does not rely on a certain set of macro variables to be in place to perform. This has enabled the fund to deliver outperformance while other more thematic approaches have not performed as well.

A market of rapid rotations

The world has run out of clichés to describe the past 12 months.

We had the impact of lockdown policies, supply chain disruption, fiscal stimulus, monetary policy, China-Australia trade tension, the shift of consumers to online, increased focus on ESG and US Presidential elections.

It’s fair to say we have never seen such a material change to so many structural factors in such a short space of time.

Swift changes in key macro factors prompted often-sudden rotations in market leadership.

Defensives did well in the initial market slump. Though the nature of the crisis meant some sectors previously considered defensive – such as A-REITS – were anything but.

The policy response of slashed interest rates helped growth companies renew their pre-Covid surge.

In November, news of successful vaccines drove a swift rotation to cyclicals and value.

Meanwhile entire industries and business models were structurally disrupted in a matter of weeks. Other companies encountered a once-in-a-generation opportunity.

As a result it’s been an incredibly challenging period for investors.

It has also been a period in which the Pendal Focus Fund showed its mettle.

How our portfolio construction drove outperformance

Relying on one “style” of investing can lead to prolonged periods of underperfomance — as value investors have seen for many years.

Trying to “time” swings in style involves anticipating changes in macro variables and investor sentiment — something that’s incredibly hard to get consistently right.

We address this issue by building portfolios based on company insight. We want a portfolio that can perform regardless of the environment, driven by stock selection.

Our aim is a portfolio that is not hostage to one style or a theme playing out in a certain way. In environments of heightened uncertainty, we want to avoid heroic calls on binary outcomes.

Under our approach we created different segments in the portfolio that worked together, allowing it to perform in different scenarios. Key segments last year included defensives, growth stocks, policy beneficiaries, quality franchises and recovery plays.

The key is to find companies with attractive fundamental features that can help limit the downside if the macro factors are not supportive, while delivering the potential for large upside gains in the right environment.

This requires an understanding of companies and industries drawn from access to management that comes with our 18-strong, highly experienced Australian equity team.

2020 provides a strong case study of why we do it this way:

- We were able to move quickly to identify and avoid companies facing existential threats.

- We were able to take opportunities in companies where we anticipated a better outcome than share prices implied – such as Nine Entertainment and Qantas.

- Pendal Focus Australian Share Fund’s outperformance in periods of negative sentiment was driven by defensive holdings such as Metcash (MTS) and by the portfolio insurance provided by gold miners such as Evolution (EVN).

- Falling bond yields helped our growth exposure via Xero (XRO) – which has then held up well due to company-specific fundamentals as other growth stocks sold off.

- Recent outperformance has been driven by recovery-linked exposures such as Qantas (QAN), Santos (STO) and Westpac (WBC).

- Throughout the period there has been a strong tailwind from policy beneficiaries such as Fortescue Mining (FMG) and JB Hi-Fi (JBH).

- We have also done well as the market recognised the value offered in long-term winners such as Aristocrat (ALL), James Hardie (JHX) and Nine Entertainment (NEC).

The outcome is a portfolio that has outperformed through each phase of the market in 2020.

Outlook

The world is now in a better place than many expected a year ago.

The economic rebound has been strong, helped by a surge in monetary and fiscal policy support. Vaccines are arriving. The world is getting better at living with the virus and mitigating its economic damage.

Nevertheless, risks remain.

The risk of premature policy-tightening cannot be ruled out. Vaccinations are working, but efficacy against new strains must be monitored. Geopolitical risk – particularly around the relationship between China and Australia – is higher than usual.

There has been a rotation from growth to value and cyclicals, but the reality is far more complex than broad style labels.

Within value there are plenty of companies that are structurally challenged and are cheap for very good reason.

Growth stocks may have lost the tailwind of falling real rates, but plenty of growth companies remain attractive long-term investments. It’s interesting to note the market seems to be starting to differentiate between profitable growth companies with cash flow and more speculative, long-duration stocks.

Given heightened macro risk, we believe a strategy that is not reliant on a certain macro outcome offers the best chance for consistent performance.

If value, recovery-related stocks continue to outperform, that part of our portfolio will benefit.

If inflation starts to creep up we have exposures with pricing power that will do well.

If we see a hit to sentiment – either from tighter policy or a deterioration in Covid – then the defensives should step up.

We continue to have exposure to carefully selected growth stocks, where we see fundamental valuation support on the basis of earnings visibility and realistic expansion opportunities.

The upshot is that we believe our balanced approach remains as valid now as it did a year ago. It has served our investors well in the sell-off and has worked in the rebound.

No-one knows what will come next. But we believe our portfolio construction, underpinned by our company knowledge, should give investors confidence that their portfolio is well positioned regardless of the next phase of the Covid saga.

Here’s an overview of Pendal Focus Australian Share Fund performance at February 28, 2021:

Source: Pendal. *Benchmark: S&P/ASX300. Past performance is not a reliable indicator of future performance

About Crispin Murray and Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia.

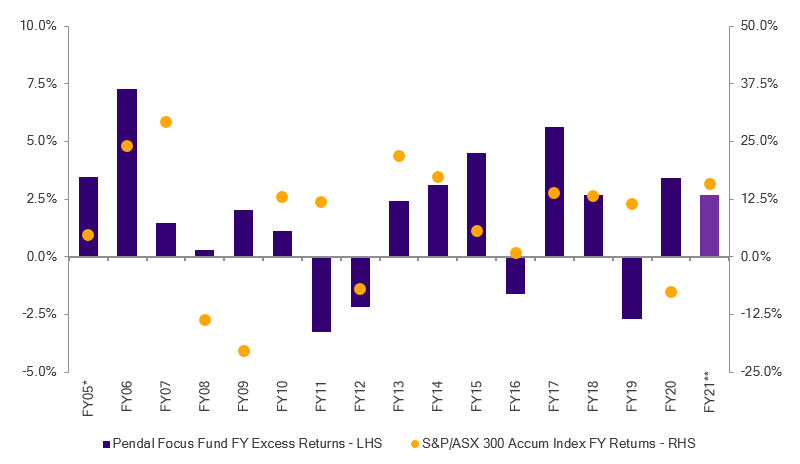

Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions , as this graph shows:

Source: Pendal. Performance is after fees and before taxes. *From 01 Apr 05; **as at 28 Feb 21. Past performance is not a reliable indicator of future performance.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Find out more about Pendal Focus Australian Share Fund here.

Pendal has today launched our first Responsible Investment and Stewardship Annual Report for Australia. Here Pendal Australia’s chief executive Richard Brandweiner (pictured) explains what it means

I AM pleased to introduce our inaugural Responsible Investment and Stewardship Annual Report for 2020.

This is a new initiative to summarise the responsible investment practices — including environmental, social and governance (ESG) integration and stewardship activities — we undertake on behalf of our clients.

As an active investment manager, we are truly stewards of our clients’ capital. We believe we have a role and responsibility to deliver sustainable returns for them, as well as influence sustainability practices more broadly.

We do this as part of our fiduciary duty to clients, but also in recognition of our position as one of the largest allocators of capital in the Australian ecosystem.

This means we need to influence positive change by taking a constructive and forward-looking approach to supporting companies improve their ESG credentials.

Long-term value creation

As society evolves and consumers and regulators increasingly look towards organisations to be mindful of their social licence to operate, we believe attention to ESG factors leads to better informed investment decisions and can improve the quality and consistency of long-term value creation.

We are proud to work with many clients who have additional ethical and sustainability-related objectives, in addition to generating returns. For these reasons, we integrate financially material ESG factors across all Pendal funds, as well as offer dedicated investment solutions to meet our clients’ additional priorities.

At Pendal we have a multi-boutique structure, with four distinct investment teams: Australian Equities, Global Equities, Multi-Asset Strategies and Bond, Income & Defensive Strategies.

Each boutique integrates ESG and undertakes stewardship in a way that makes sense for their respective strategies and asset classes.

In other words, we don’t have a single way of investing responsibly at Pendal, although our dedicated Responsible Investments team does bring a common thread across the firm by supporting all boutiques and helping to define quality.

Regnan: Sustainable and impact investing

As many of you will be aware, in early 2019 we assumed full ownership of Regnan, bringing the team in-house to be Pendal Group’s specialist sustainable and impact investing business unit.

Regnan’s experienced team of experts have been a great addition, supporting our engagement and research activities and the continued development of our investment products.

Excitingly, 2020 saw Regnan’s capabilities expand to investment management.

Pendal Group secured a specialist global impact investment team to join the Regnan ecosystem and we launched two products under the Regnan brand.

We look forward to the expansion of the Regnan business, further enabling the purposeful allocation of capital.

Learning and growth

While 2020 in many ways went down as a year most would rather forget, for Pendal it was also a year of learning and growth.

It was a year of paradoxes: a reminder that not every situation is an “either/or”, and not every decision can be bound by the immediate environment or issues at hand.

The year saw, for example, corporate management held to account for more than just the maximisation of short-term shareholder profit in ways we have not seen before.

As we turn our attention to the future and “building back better”, we expect the topics of climate change and inequality will gain importance in the year ahead — and beyond.

The COVID-19 pandemic laid bare many underlying inequalities in societies around the world. Women, elderly and vulnerable communities were disproportionately represented in the hardest hit sectors of the economy.

Encouragingly we are seeing investor action already and we share in this report some of the ways we are working with our clients and investee companies to address this rising inequality.

Tranformation through collective action

The pandemic has also shown us that collective action can drive transformative policies and deliver break-through technologies that seemed unthinkable before the crisis.

Through our engagements and advocacy efforts we will seek to ensure the advances witnessed in 2020 continue.

How else can we ensure that our health, political and economic systems can be resilient in the face of a pandemic, or other form of crisis in the future?

We are thrilled with some of the things we achieved in responsible investment and stewardship in 2020.

These efforts are detailed in this report which I hope you enjoy reading.

We look forward to reporting annually on the ways in which we continue to enhance our approach, responding not only to the ever-changing investment environment but to the evolving needs of our clients.

— Richard Brandweiner

Pendal Chief Executive Officer, Australia

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Download Pendal’s Responsible Investment and Stewardship Annual Report 2020 (PDF)

Contact a Pendal key account manager here.

As part of its approach, Pendal Horizon Fund invests in companies that enable and lead in the transition to a more sustainable and future-ready Australian economy, while avoiding those that cause significant harm.

An example is business software innovator Xero, a leader in the trend to digitalisation which is changing the way we work.

Pendal equities analyst Elise McKay explains in a short video above.

ASX-listed technology stocks — particularly so the so-called WAAAX stocks Wisetech (WTC), Afterpay (APT), Altium (ALU), Appen (APX) and Xero (XRO) — have been favourites among many investors in recent years.

A key part of this has been the benefit of low-bond yields, which have lifted valuations for growth companies — including many tech names — worldwide.

This tailwind has receded in recent months as yields have begun to rise. Meanwhile vaccines have provided a pathway to re-opening, boosting sentiment around more cyclical stocks. As a result market leadership has shifted from growth stocks to cyclical and value.

In our view this does not mean a shift to a stance of “sell growth, buy value”.

There are plenty of value stocks that are structurally impaired. At the same time, we think there are compelling opportunities in tech stocks. Stock selection is as critical as ever.

In the tech sector we think the market will start to discern between companies with less tangible prospects that are not delivering cashflow — and those that are profitable with good earnings visibility.

We see accounting software provider Xero as one of the latter. It is our top pick in the ASX tech sector.

In this video above Pendal Research Analyst Elise McKay shares insights into XERO, the ASX tech sector and the five-factor framework by which we assess companies.

XERO is included in Pendal Horizon Fund (formerly Pendal Ethical Share Fund) and Pendal Focus Fund.

“We use this framework to find those companies like Xero that are generating strong, sustainable returns on the capital that they’re investing today in unlocking a large global addressable market and creating significant value in the future,” says McKay.

In Xero’s case:

- The industry structure and competitive landscape is favourable and there is a large global addressable market

- Xero is well placed in the cycle as secular trends drive the adoption of cloud accounting products

- It’s investing heavily in innovating the next generation of products.

- The culture of the company is strong, and it’s able to internally create the products it needs.

- And finally, the capital return and unit economics of the business are attractive.

“One of the great things about Xero is that it has accelerated digitalisation of the economy, particularly for small businesses.”

Digitalisation refers to the use of digital technologies “to change a business model and provide new revenue and value-producing opportunities” according to research house Garnter. (It’s distinct from digitisation, which simply means converting things such as bank accounts or books from analog to digital.)

“This platform opportunity allows Xero to be the plumbing into so many more solutions being offered to this community.”

Digital tools are rapidly becoming essential for small business in Australia, according to McKay, who says businesses adopting digital are on average able to save 10 hours a week and generate 27 per cent more revenue.

She believes the fast-growing cloud accounting provider is at the start of a multi-year journey to unlock an enormous global market and become a platform for transforming small business.

XERO is included in Pendal Horizon Fund (formerly Pendal Ethical Share Fund) and Pendal Focus Fund.

About Elise McKay

Elise is an investment analyst with Pendal’s Australian equities team. Elise previously worked as an investment analyst for US fund manager Cartica where she covered a variety of emerging market companies. She has also worked in investment banking and corporate finance at JP Morgan and Ernst & Young.

About Pendal Horizon Fund and Pendal Focus Australian Share Fund

Pendal Horizon Fund (formerly Pendal Ethical Share Fund) is a concentrated, high-conviction portfolio aligned with the transition to a more sustainable, future-ready economy.

Pendal Focus Australian Share Fund is an actively managed, concentrated portfolio of 15 to 30 of our best investment ideas across the Australian share market.

Both funds are led by one of Australia’s most experienced portfolio managers, Crispin Murray. Crispin is backed by one of the largest, most experienced Australian equity teams.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Find out more about Pendal Focus Australian Share Fund here.

Contact a Pendal key account manager here.

Major shifts in policy-making — driven by the Covid crisis and a desire to correct GFC-era mistakes — can drive equities higher despite pockets of excess, says Pendal’s head of equities Crispin Murray (pictured).

Here are some insights from reporting season, drawn from Crispin’s bi-annual Beyond The Numbers presentation.

Watch the presentation here (registration required).

Key points

- Equities to benefit from major shifts in policy goals

- A number of factors are driving rotation from growth to value

- Performance is not simply “buy value, sell growth”

- Find out about Pendal Focus Australian Share Fund

INVESTORS may see pockets of excess in markets at the moment — but that’s not necessarily a sign that we’ve reached a top in equities, says Pendal’s Head of Australian Equities Crispin Murray.

These are symptoms of a policy agenda designed to avoid the mistakes of the Global Financial Crisis era.

That era resulted in fiscal austerity, pre-emptive monetary tightening and a focus on economic goals to the exclusion of other factors.

Today policy makers are thinking more about reducing inequality, building economic resilience and a greater role for clean energy.

This means bigger fiscal spending and very accommodative monetary policy.

Coupled with the impact of pent-up demand amid a re-opening economy and the return of fund inflows, this should combine to drive the stock market higher, Murray believes.

But he cautions investors to watch for additional complexity in markets.

For example Covid has accelerated structural trends such as the transformation of work via digitalisation and the impact of Environmental, Social and Governance factors when scrutinising companies.

Growing concern about inflation can also trigger bond market sell-offs which can have varying impacts across equity market sectors.

“We think equity markets will be resilient in the face of rising bond yields,” he says. “[But] they do have a big effect on what’s going to actually perform in the market.”

Higher inflation expectations and bond yields are seeing market leadership shift away from growth to cyclicals with pricing power. This suits the Australian markets, he says.

But future outperformance is not a simple matter of buying value stocks and avoiding growth stocks.

“There are still going to be companies in the value sector that are structurally disadvantaged.

“And you’re going to find companies in the growth sector that still have incredibly strong franchises. So, you need to be nuanced about your stock selection.”

The environment is ripe for an active, style-neutral approach focused on company specifics.

Four components of a well-constructed equities portfolio

Murray says a well-constructed portfolio should have four components:

- First, defensive stocks are needed to protect against risk and the chance of policymakers changing their minds.

- Second, a portfolio should have exposure to stocks that are leveraged to the potential inflationary pressures coming through.

- Third, investors should hold companies that used the crisis to improve their position and are ready to benefit from the release of pent-up demand.

- And finally, investors should consider the companies hit hardest by the pandemic who will see a material shift in fortune once the vaccines roll out.

“When we think about our portfolio, we think about the different roles stocks play. Like a football team, you need the defence, you need the midfield, and you need the attack.”

About Crispin Murray and Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia.

Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions, as this graph shows:

Source: Pendal. Performance is after fees and before taxes. *From 01 Apr 05; **as at 28 Feb 21.

Past performance is not a reliable indicator of future performance.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Find out more about Pendal Focus Australian Share Fund here.

Pendal Group Limited (ASX: PDL or Pendal) today announced the appointment of Mr Bertrand Lecourt and Mr Saurabh Sharma to establish a global equities sustainable water and waste investment strategy within the Regnan business.

Based in London, Mr Lecourt will join Regnan as Senior Fund Manager and Mr Sharma as Fund Manager.

It is expected the investment specialists will commence in April 2021, with the investment strategy to be launched in the UK and Europe in the second half of calendar 2021.

The team joins from Fidelity International where they manage the Luxembourg-domiciled US$2.4 billion Fidelity Funds Sustainable Water & Waste Fund.

The investment strategy will invest in companies involved in the design, manufacture or sale of products and services used in the water and waste management sectors.

Emilio Gonzalez, Group Chief Executive Officer of Pendal Group, said: “The appointment of Bertrand Lecourt and Saurabh Sharma demonstrates our ability to attract superior talent and progresses Regnan’s plans to become a global leader in providing environmental, social, and governance (ESG) investment strategies and solutions to clients.

“Regnan’s focus is on delivering innovative and specialist sustainable and impact investment solutions, drawing on over 20 years of experience at the frontier of responsible investment.

“The team’s appointment is the second investment team hire since Regnan expanded into investment management and follows the appointment of the Regnan Equity Impact Solutions team in December 2019, led by Tim Crockford, who joined from Federated Hermes.

“Clients are increasingly seeking out investment strategies that address environmental concerns in a sustainable way.

“The development of new technologies and proper water and waste management will be critical to manage the increasing demand for clean water and waste management as populations grow and become more urbanised.

“This will drive investment opportunities that Bertrand Lecourt and Saurabh Sharma will be able to capture through the unique combination of a diversified water and waste global equities portfolio with strong ESG credentials.”

Team biographies

Bertrand Lecourt, Senior Fund Manager

Bertrand Lecourt joined Fidelity International as a Portfolio Manager in 2018, where he launched and managed the Fidelity Funds Sustainable Water & Waste Fund.

Previously he was a Portfolio Manager at Polar Capital and the founder and CIO of Aquilys Investment Management. Prior to moving to the buy-side, Bertrand was Head of Equity Research, France at Deutsche Bank and a utilities analyst at Dresdner Kleinwort Benson and Goldman Sachs.

He holds an MSc in International Finance from HEC School of Management, France; an MSc in Money, Banking and Finance from Birmingham University, UK; and a DEA in Monetary Economics from Orleans University, France.

Saurabh Sharma, Fund Manager

Saurabh Sharma joined Fidelity in 2014 as a Product Specialist before becoming an Assistant Portfolio Manager in February 2020.

Previously, he held equity research analyst roles at Moody’s Analytics and GlobalData.

Saurabh has an MBA in Finance from IBS Hyderabad School in India and is a CAIA and ICFAI Charterholder.

Who is Regnan?

Regnan is a responsible investment business within Pendal Group with a vision to grow its funds under management and become a global leader in providing environmental, social, and governance (ESG) investment strategies and solutions to clients.

Regnan exists to drive positive impact and investment for a sustainable future and works towards this by developing and promoting more principled, rigorous and outcome-oriented approaches in responsible investment. It has a long and proud heritage in engagement and advice on ESG issues.

Regnan has produced pioneering research that has changed the way investors think about their wider responsibilities to society including advising influential organisations, such as the Principles for Responsible Investment (PRI).

Regnan can trace its roots back to a collaboration with Monash University, Melbourne in 1996, with an investigation into overlooked ESG-sources of risk and value for long-term shareholders in Australian publicly listed companies.

Regnan has since taken its ESG expertise globally. Its diverse experience in advocacy, regulation, academia and advising investment managers has enabled Regnan to offer ESG-related advisory, engagement and research services.

Visit Regnan.com

Find out about Regnan Global Equity Impact Solutions Fund

Find out about Regnan Credit Impact Trust

For more information on these and other responsible investing strategies, please contact Head of Regnan and Responsible Investment Distribution Jeremy Dean at jeremy.dean@regnan.com.

A global shift towards sustainable agriculture and food production is opening attractive opportunities for investors as new technologies and business models start to gain traction.

RESEARCHERS at Regnan, a global leader in sustainable investing, have named four areas of investment that will drive the transformation of food production while minimising waste and developing new sustainable and affordable food products.

The findings are featured in a new Regnan report, Catalysing Sustainable Agriculture and Food Production, by Regnan senior adviser Doug Holmes and Regnan fund manager Mohsin Ahmad.

Reforming agriculture is essential to meeting the challenge of climate change because agriculture and food production accounts for nearly a quarter of the world’s greenhouse gas emissions. Without change, emissions are forecast to grow more than 30 per cent by 2050.

“Industrial farming was the right solution for increasing global production of food back in the 50s and 60s,” says Holmes, who has worked in the sustainability sector for nearly three decades.

Source: WRI analysis based on FAO (2017a); UNDESA (2017); and Alexandratos and Bruinsma (2012).

“But there’s so much evidence out there around the negative impacts from industrial farming as practised now that it’s quite clear we need to change course.”

Climate change aside, large-scale food production is doing astonishing damage to the environment.

Run-off from fertilisers, pesticides and herbicides is polluting waterways and marine habitats, soil is being degraded by reliance on chemicals and irrigation is depleting aquifers.

A third of the planet’s soil has already been degraded. Without significant change, 90 per cent of soil on earth will be degraded by 2050.

But despite the toll, crop land and pasture land will increase by 600 million hectares over the next three decades, destroying forests and natural ecosystems.

The challenge is how to feed a global population that will hit 10 billion by 2050 — requiring 50 per cent more food than we produce today — without inflicting further damage on struggling ecosystems.

In the new report, Regnan’s team identifies four areas of investment that are crucial to the key stress points in global food production, ideal to catalyse change and – perhaps most importantly – largely unsung by the global investment industry.

1. Soil health

The first is regenerative and organic farming aimed at improving soil health.

Organic matter – essentially dead and decomposing plant and animal debris alongside billions of living creatures like bacteria, fungi, insects and worms – plays a vital role in soil health.

A 1 per cent increase in soil organic matter helps soil hold 20,000 more gallons of water per acre. Organic matter is also a powerful store for carbon dioxide that helps mitigate climate change.

The investment opportunity lies in the carbon credits that can be generated by better soil management.

“There are business models being developed monitoring and measuring and tracking soil carbon using various technologies and then creating markets for soil carbon that can be brought into the public space,” says Holmes.

2. Controlled farming

The second opportunity is controlled farming which can be conducted in cities as indoor or vertical farms, or larger-scale state-of-the-art greenhouse farming close to urban areas.

“Within developed economies, this is a real growth area,” says Holmes.

“There are some quite large controlled-farming start-ups and businesses in places like the United States and in Europe developing models that are very focused on feeding a rapidly growing urban population. They typically employ AI and advanced technologies.”

Controlled farming is essential to support the rapid growth of cities and the increasing urbanisation of the world.

The growing risk of extreme weather is another driver, as controlled farming can be better protected, lowering the risk of crop loss.

3. Waste management

Third on the ledger is the growing industry aimed at reducing the enormous waste in food supply chains.

Close to a third of all food produced is lost to waste.

This not only means that fewer meals are available for those in need, but it also lifts the land area and resources required to make up lost food, putting additional stress on the food system and lifting greenhouse emissions.

“By reducing food waste, there’s more food available that eventually reaches the dinner plate, so that means less load on systems upstream.

“Less land is cleared for agriculture and there is less load from the agricultural processes themselves and all the inputs that go into producing food.

“You’re reducing greenhouse impact and the also providing more food at the other end of the cycle.”

Food is lost across the food supply chain, from growing to storage, processing and distribution right through to the food thrown out by retailers and households.

Source: FAO 2011, Regnan 2020

ReFED, a non-profit aiming to end food waste, says a 20 per cent reduction in US food waste over the next decade would be equivalent to removing about 4 million cars from the road.

“It’s a key area for attention,” says Holmes, who says some of the more promising innovations are platforms connecting farmers with pre-determined buyers for food that might otherwise go to waste.

“For example, in developed countries, farmers who have produced crops that might be less presentable from a marketing perspective have pre-determined buyers to take that product and turn it into other value-added food products like juices or similar products.

“The systems are developed to pre-identify buyers for food that may be less visually appealing or perceived to be of lesser quality.”

The Regnan team singles out Tomra, which has its origins as a reverse vending machine company that collects bottles and cans for recycling. Tomra has now expanded into providing sorting technology for the food industry, inspecting produce and helping divert low-quality food to alternative uses.

You can read more about Tomra here.

Regnan funds also hold shares in NYSE-listed Ecolab, which makes antimicrobial water additive products that reduce foodborne pathogens and help control spoilage of processed fruit and vegetables.

4. Plant-based meat

Finally, Holmes points to the growth of a new plant-based meat industry as an example of a move to sustainable food products that replace resource intensive agriculture.

“Livestock production is enormously greenhouse intensive. The opportunities afforded by the plant-based products is a very big one from a sustainability perspective, and particularly as those products are get better and better.

“It seems to be to me there’s a there’s a very big business opportunity there.”

Download Regnan’s Catalysing Sustainable Agriculture and Food Production report here.

Who is Regnan?

Regnan is a responsible investment leader with a long and proud history of providing insight and advice to investors with an interest in long-term, broad-based or values-aligned performance.

Building on that expertise, in 2019 Regnan expanded into responsible investment funds management, backed by the considerable resources of Pendal Group.

The Regnan Global Equity Impact Solutions Fund invests in mission-driven companies we believe are well placed to solve the world’s biggest problems.

The Regnan Credit Impact Trust (available in Australia only) invests in cash, fixed and floating rate securities where the proceeds create positive environmental and social change.

Both funds are distributed by Pendal in Australia.

Visit Regnan.com

Find out about Regnan Global Equity Impact Solutions Fund

Find out about Regnan Credit Impact Trust

For more information on these and other responsible investing strategies, contact Head of Regnan and Responsible Investment Distribution Jeremy Dean at jeremy.dean@regnan.com.

The pandemic accelerated responsible investing as an investment theme, magnifying issues such as resilience and engagement. Pendal’s head of equities Crispin Murray outlined the big lessons at the Responsible Investment Association Australasia’s RI Australia 2020 conference.

View an edited video of the presentation above or read the transcript below.

Key points:

- How 2020 emphasised the importance of responsible investing

- How Crispin Murray thinks and acts on Environmental, Social and Governance (ESG) matters as an active fund manager and steward of capital

- Crispin’s observations on engaging with companies about ESG matters

TRANSCRIPT

Simon O’Connor, Chief Executive of the Responsible Investment Association Australasia:

Crispin you have a long history looking at ASX-based equities. I’m fascinated to hear your view on the year.

Crispin Murray, Head of Equities, Pendal:

Thanks for the opportunity. I’ll focus on three things. One is to give you my thoughts on what’s changed this year — and it’s been an enormous amount.

The second thing is to give you a snapshot of how an active fund manager thinks and acts on Environmental, Social and Governance (ESG) matters. And then some observations on what we’re seeing when we deal with the companies that we invest in.

What changed in 2020

First in terms of what’s changed, the pandemic has really brought attention to how existential risks are real. When they happen they have a dramatic effect. That’s across a number of areas, but from an equity market point of view you’ve seen huge divergence.

You’ve had clear losers and you had clear winners. I think that’s brought home how you need to not just understand where these risks are, but what are the consequences of these risks.

One of the lessons to come out of this is that when we think about investing and sustainability, we need to think about it from a risk management point of view.

We don’t actually have to prove that responsible investing is always going to beat more generalised investing. What you need to show is that in certain scenarios, that is the thing that could be protecting your portfolio.

That was a very interesting outcome from the pandemic.

Lack of resilience

Another feature of the year is that it’s really demonstrated a lack of resilience within economies, societies and within companies.

This tag that I think [former US treasury secretary] Larry Summers came up with is that we were moving from a just-in-time world to a just-in-case world.

I think that requirement to understand building in resilience to your business models is a really big imperative.

The final thing I’d say is it’s been an acceleration of some of the big themes that we’ve seen over the last few years.

Digitisation, the move online and ESG are are themes that have been supercharged by the lessons from the pandemic. So that’s one set of issues.

Geopolitical issues

I also think globally, geopolitically, we’ve seen some very important developments.

First of all we’ve seen China commit to a net zero target. While it may be a long way out, you can already see some of their policies that have been put into their latest five-year plan, which are very much linked to that long-term target. So I think that’s a strong signal.

On top of that clear, clearly we’re seeing in the US a shift towards the Biden administration, which I think will put in a renewed effort.

So I think there’s a very strong signal globally that a lot of companies are seeing and receiving.

Then the final thing I’d point to is this year’s local events.

There’s [the events of Rio and] Juukan Gorge, we’ve had the situation at AMP. There have been situations that have really demonstrated that if you’re not managing ESG risks well, it has significant impact on companies in terms of how they’re managed and the way investors perceive them.

How we think about ESG today

In terms of how we as investors think about ESG, Pendal’s very fortunate.

We’re a large fund manager. We have $17 billion invested in the Australia market.

That gives us a very important responsibility, which is to engage on behalf of our clients and to use that influence in a positive way.

We’re also fortunate we have a lot of resources. We have 19 people in our Australian equity team. We can also draw upon our colleagues at Regnan who have a team of eight dedicated to doing a lot of research in these matters. And then we have a responsible investing team.

So the resources dedicated to ESG matters has really multiplied in the last few years.

I think what’s shifted is, we’ve always been aware of ESG risks. Our job is about risk management contingency planning.

But the awareness is that these issues and these risks are far more material now and far more significant in terms of the consequence for our portfolios.

In addition, I do also believe that one of the big trends that we’ve seen over the last 25 years is the shift to passive [investing].

Part of that has led to a significant reallocation of resources towards more momentum, more growth-orientated stocks.

I think the next 20 years is going to be about people investing in sustainability-orientated portfolios. Even the managers who are not in those dedicated funds [will] have a greater and greater overlay of that in their investment decisions. In terms of a cost of capital outcome, there’s going to be a very material consequence.

So companies that do not deliver and are not seen to be managing these risks, are going to see their cost of capital rise. They’re going to see their ratings on their stocks fall. And they will not be allocated capital.

Markets are very efficient in terms of determining where they want capital to be allocated. We’ve seen that with growth stocks more recently. I think we’re going to see that increasingly with people’s allocation towards people who are not managing those risks properly.

So when we think about our investments, we think about it both from the perspective of the industry —what are the risks to that industry? what are the longer term trends? — and then how within the company, they are thinking about and managing those risks.

And we rate those companies. So we have a formal process of rating those companies on our own metrics, and we use the Sustainability Accounting Standards Board (SASB) framework to help guide us in what are the key things to focus on.

The importance of engaging with companies

The other element of what we do — and probably the most interesting and the most challenging — is we’re very much at the front line.

Our job — having done the analysis and having listened to perspectives from our investors — is to actually go in and meet these companies and raise these issues.

These are often quite uncomfortable discussions. That’s the nature of our job and that’s what we do.

I’m not expecting much sympathy on that front, but it’s worth highlighting.

You can often go into a meeting and the first part of the conversation with the chairman is ‘we don’t think the executives’ pay is aligned with shareholders, there’s a disconnect here, we need you to reassess that’.

Then we need to talk about how you’re managing your ESG risks and why you’re not thinking strongly enough about your targets on scope two and how you think about scope three and what what actions that you’re taking.

Then you may move on to a discussion about diversity within the organisation and what’s going on.

Keep in mind you’re dealing with people who, for most of their lives, are having people responding to them — they’re the ones directing everyone else.

In the last few years there has been a shift from ‘I’m not really used to people telling me what I need to change’ to an awareness that ‘okay, now I need to embrace this a little bit more’.

But there’s clearly still some resistance to that. That’s part of this process.

On one end of the spectrum there’s an understanding of where society needs to go [and] how economies need to transition to a more sustainable future. But then there’s still a traditional mindset that ‘well, we’re companies, we’ve got to focus on our returns and we’ve got to think about the real issues in front of us now’.

I’m not saying either end of that spectrum is wrong. What we need to do is meld those together so people can see they are actually intertwined.

So a lot of what we do is informing and discussing and trying to share perspectives with companies over these matters.

What we’re seeing when we meet with companies

That takes me to some of the observations we’ve made over the last couple of years within companies.

The first point is that everyone actually understands risks. I don’t think there’s a debate about whether there are issues that we need to be thinking about and taking care with.

The discussion is about the degree to which those risks are real and tangible in any reasonable timeframe.

That’s the push-back that we get. But I do think Rio with Juukan Gorge is a very seminal moment. Understanding community relations and working with the traditional landowners was something a company probably never thought would lead to the CEO and two senior executives being removed if they got it wrong.

That clearly was a risk that was underestimated by that company. That is a very stark lesson for all companies.

That’s one of the areas that’s being reassessed and needs to be continually discussed and highlighted with these companies.

The second thing is the interesting debate about the reporting versus the outcomes on ESG matters.

Both are very important but my observation is there’s an element now where companies feel that by delivering on the reporting side — giving the past — that’s showing that they’ve done their job.

Then I actually think about the point of the reporting and what we’re actually trying to achieve here and what are the outcomes.

We certainly want to emphasise — what is it that a company can do specifically? How can they make a dedicated change rather than just signing off on a series of targets that are not necessarily going to achieve a lot in a good timeframe.

If you take the mining sector, it’s going to be very difficult for the iron ore companies, for example, to push a lot of their customers such as the Chinese steel companies to embrace some of the measures that perhaps they should be embracing.

But what they can do is sit down with their suppliers of trucks and diggers and so forth and put a lot of pressure on them to transition away from diesel towards alternatives such as hydrogen or electric vehicles.

So we’ve been encouraging our companies to think about not just the reporting (you’ve still got to do that) but also the tangible things where we have a point of leverage to deliver a material outcome in a good timeframe.

Amcor as an engagement case study

Another company we’ve had a lot of discussions with is Amcor.

Amcor is an interesting company because it’s in a very controversial area — single-use plastics.

But it also has the potential to drive technology improvements and infrastructure that can lead to recyclable, reusable, combustible packaging becoming pervasive in our consumption habits.

We believe it’s really important to encourage them to realise that by doing something — and I believe they are doing something about it — that will help the rating of the company and their cost of capital.

And if they don’t do enough about it, it’ll actually go the other way.

So there’s a much more binary outcome in terms of their decision-making.

The carrot or the stick

That also leads me to this issue of the carrot and the stick.

I do believe that generally to motivate people and motivate companies, you need to not only tell them the consequences of not doing something and the penalties that will come. You also need to provide them with an incentive.

I think that’s where the market’s price action, the way that markets are rating companies is actually a very valuable tool in sending that signal and providing an incentive for companies.

In addition I think there’s enormous amount of opportunities. We’ve spent a lot more time recently thinking about the opportunities that are presenting themselves with this transition in the economy.

Going back to the pendemic, the companies that were able to help facilitate remote work and online shopping have had huge returns for investors.

So if you’re talking to a company you can say, ‘think about the opportunity, where can you tap into these trends and how can you actually take advantage of them and deliver a positive outcome?’

Intertwinment of E, S and G

The final observation I’ll make is to really reinforce this point about the intertwinement of the E, the S and the G [Environmental, Social and Governance issues].

When I speak to companies I see a parallel to what we’re seeing in broader society. There’s a group of people who are very much on board with the need to transition the economy. But there’s also still people who realise that they’re probably near-term losers from that transition.

That’s why the ‘S’ is so important.

We need an economy that is able to create industries that create new jobs, create wealth and enables us to transition quicker.

In terms of our portfolios the message we’re giving to companies is we’re really looking for those companies that help deliver on those other aspects of ESG, and are able to help facilitate the transitions that we’re seeking to achieve.

Simon O’Connor (RIAA): Crispin, you have quite unique access to very senior levels of Australian companies. We’ve seen something of a revolution on the investor side around ESG issues which you talked about. Are you saying the response at the leadership level in boards and among executives you speak to is responding and upskilling and building capability and knowledge quickly enough in your view — as a broad observation across the ASX?

Crispin Murray (Pendal): Yes the first thing I’ll say is, there’s an enormous emphasis across the board on these matters. Certainly we are through the stage of people dismissing this as an issue.

The challenge now is the output. I will sit down in some situations and we’ll literally have a 40-page deck, and it will just go through a whole bunch of things that companies are doing. But you get the sense sometimes that this is a case of ‘let’s just create lots of examples of all the things we’re thinking about’. But there’s no common theme or purpose as to what they’re trying to achieve.

The targets have created a mindset which is: ‘as long as we’re answering and delivering on these sorts of KPIs, we’re doing what we’re supposed to be doing’.

Getting people to actually think about the ‘whys’ is really important.

The other observation is it’s a lot easier for large companies to do this than small companies.

One of the things I worry about is that when you look at some of these third-party rating services, they’re penalising smaller companies because they haven’t got the reporting levels that larger companies have.

[Smaller companies] need to raise their game, and that’s a message that we give to them. But in many cases we think there’s a disconnect between the perception and the reality of these companies.

We want to try and find the right balance between, having companies feeling that they have to dedicate resources just to apply reporting standards that work for a global perspective versus if there’s one area of your business that you can really facilitate a change. We’d certainly encourage them to focus on that and work more on that front.

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and a strong track record leading Australian and European equities funds.

He manages a number of our flagship funds along with one of the largest equities teams in Australia.

Click here for more information about Pendal’s newly enhanced Ethical Share fund.

For more information, please contact Pendal’s Head of Responsible Investment Distribution Jeremy Dean at Jeremy.Dean@pendalgroup.com.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Find out more about our investment capabilities: https://www.pendalgroup.com/about/investment-capabilities

Contact a Pendal key account manager: https://www.pendalgroup.com/about/our-people/sales-team/

PENDAL is proud today to introduce Regnan Global Equity Impact Solutions Fund in Australia.

The new fund is one of the first to provide Australian investors with access to global public market impact assets. The announcement follows the successful launch of Regnan Credit Impact Trust in January 2020.

Regnan, a specialist ESG research, engagement and advisory business that is fully owned by Pendal Group, expanded into global investment management in 2020 with the appointment of a four-person Global Equity Impact investment team.

The fund is offered as part of Regnan’s Global Equities Impact strategy which is available in the UK and now in Australia. The strategy is managed by Regnan’s London-based investment team and marketed by Pendal’s distribution team locally.

“The Regnan Global Equity Impact Solutions Fund is an important step in our vision to develop Regnan as one of the world’s foremost responsible investment managers,” said Pendal Australia Chief Executive Officer Richard Brandweiner.

“It’s an innovative investment strategy developed by a dynamic and passionate team with proven credentials as impact investors.”

Positive impact, active returns

Impact investment products are in high demand. The value of Australian impact investments is forecast to grow to $100 billion in five years — five times the current market size of $20 billion, the Responsible Investment Association Australasia reports.

Regnan Global Equity Impact Solutions invests in mission-driven companies that provide solutions for the growing, unmet sustainability needs of society and the environment while seeking to generate strong financial returns.

Using a proprietary taxonomy system, Regnan has identified more than 50 areas of potential investment based on the United Nations Sustainable Development Goals — and some 2200 innovative companies well-placed to become leaders in these new markets.

“We are excited to launch the fund in Australia,” said Tim Crockford, Head of the Regnan Equity Impact Solutions team.

“Impact investing is a nascent and fast evolving space. Our ethos is about investing in companies that are trying to solve environmental and social challenges like water and food security and embedding circular economy in their business principles. For us, the impact case is the investment case.”

Hear more from Tim Crockford in this video.

Click for detail about Regnan Global Equity Impact Solutions fund

Regnan’s new look

Reflecting its new, expanded mission, Regnan has introduced a new look and a new website.

The new Regnan logo evokes shifting tectonic plates, signifying the permanent change that sustainability brings to the investment landscape.

Australian investors: For more information, please contact Head of Regnan and Responsible Investment Distribution Jeremy Dean at jeremy.dean@regnan.com.

Information for UK, European and other international investors: www.regnan-johcm.com