Investing to take account of humans’ impact on the environment has garnered even greater attention over the past several months and its importance for our clients continues to grow.

As Pendal’s Portfolio Specialist, David De Ferranti outlines, there are now opportunities for investors to make a real difference to the lives of everyday people, while also earning a financial return.

Take a two-minute read on the evolving area of impact investing and the positive contributions it can make to the environment and broader society.

View the article here.

The inexorable drift towards lower and lower interest rates is upending many assumptions; from the role of monetary policy in lifting the economy through to where investors look for yield. Australia and the US have positive rates for now. However, as growth slows further, inflation persistently undershoots central banks’ targets and governments prove unwilling to lift spending, rates are being forced closer to zero. This has raised speculation over non-traditional measures like negative rates, as already in place across Europe, as well as quantitative easing in order to move central banks’ key objectives back towards their targets. At Pendal’s recent Lighthouse event, the Bond, Income & Defensive Strategies (BIDS) team shed some light on the conundrum facing policymakers and what the future may look like when monetary policy is no longer effective.

Monetary means at their limits

Central banks around the world have been progressively targeting inflation since 1989, with our friends across the Tasman at the Reserve Bank of New Zealand the pioneers of its modern form. Over this time the policy setting boards have presided over the structural shift to lower interest rates, lower inflation and considerable economic expansion.

Since the 1990s we have seen a few economic cycles, with each changing the nature of policy effectiveness. Our Australian rates manager, Tim Hext, has experienced many over his career and notes every cycle has lower and lower interest rates. In Europe, several countries now have negative interest rates, led by Denmark, Switzerland and Sweden. They have joined Japan, where interest rates hit zero two decades ago, before turning negative.

The issue now is increasing risk aversion resulting from negative rates. Central bank tools are relatively blunt, so to obtain the desired economic response, even deeper negative interest rates will be required for Europe. This is the problem with blanket policy targeting through interest rates. When you’re a hammer, everything looks like a nail.

As such, to address the failures of the current regime there is growing recognition of need for a different policy approach. Enter Modern Monetary Theory (MMT). The thinking around this form of economic management was pioneered by American economist, Professor Bill Mitchell along with a cohort of academics and finance practitioners. MMT directly repudiates the thinking around government budget constraints which form the basis of the ideologically opposed Keynesian school of thought for economic management.

Breaking from tradition

The chorus is growing as central bankers increasingly appeal for help in the unruly task of economic management. In his last meeting at the helm of the ECB, Mario Draghi called again on greater support from the fiscal arm of policy. RBA Governor Lowe has echoed these calls amid the frugality that has characterised government spending at home, driven by a seeming obsession with obtaining a surplus.

Ultimately, if an economic crisis and recession eventuates it will drive radical political change, forcing governments to boost spending, cut taxes and pursue deeper structural reform. This may include elements of MMT, which we can interpret more as a framework, than a set of individual policies.

At the core of MMT is an ideology that upends the traditional view that considers the economy as separate from individuals, who seek to maximise their utility from it. Rather, MMT essentially sees the economy as the people and in turn, works for us as a collective.

Another conventional perspective which is uprooted by MMT is that governments should operate like households. This is an idea perpetuated by our personal experience with budgeting and debt. Simply, if we live beyond our means, there is a deficit which requires debt to finance. We then project this idea onto how governments should operate. As such, we have the notion that governments must raise revenue through taxes in order to spend, otherwise they will run a deficit and accumulate debt.

MMT takes an alternative view under a few assumptions, including that governments have control over their currency. This means a government could create money to finance spending, rather than raise it through taxes or a combination of deficits and debt. Such an approach can be followed when there is excess capacity in the economy and the need for stimulus.

What creates inflation?

The notion of creating money for spending may raise some eyebrows, given concerns over the idea of money printing resulting in inflation running out of control. However, such worries require consideration of the force behind money creation. As has been proven by the recent era of massive central bank stimulus efforts, inflation is not purely supply-driven. It does not matter how cheap money is to borrow or how much is available, ultimately it depends on demand and a borrower’s ability to borrow.

Government spending can stimulate this demand and taxes can reduce it. In the MMT world, a key policy that can be used as part of this mechanism is a job guarantee program. If economic activity is weak with low inflation, jobs can be created to absorb idle capacity, and as capacity becomes stretched, inflation will rise. True inflation can only emerge once full capacity is reached. As inflation rises, the government can cut spending and raise taxes to bring the economy back towards balance. In this way the policy acts as an automatic stabiliser.

Such a job guarantee program also supports an idea that anyone who wants to work will work. If the private sector can’t absorb them, then the government will. It will guarantee you a job. There are plenty of public services that are needed – building public facilities, cleaning community spaces or whatever host of other productive activities.

A new New Deal

In the US a similar style policy was implemented in the form of the Civilian Conservation Corps – one of the most successful New Deal reforms introduced by Roosevelt in the 1930s. Looking at the debate in the US now, Tim believes it is not a matter of when a form of MMT arrives, but who will move first – when will they do it, how they do it, and who will then follow.

“For example, you could have a 50-year infrastructure project, which you break down into 5-year, short term projects. This can be slowed as inflation rises. And if inflation rises too far, taxes can be hiked”, he says. “The currency may take a hit, initially, but as growth kicks in, that will flow through to the currency.”

Tim highlights the case of Japan, which has struggled to stimulate growth, but boasts one of the lowest unemployment rates in the world; “everyone’s got jobs, everyone is happy. Why do you need GDP growth if everyone is happy? It begs the whole question of why do you need GDP growth for GDP growth’s sake.”

Looking elsewhere, the UK is likely growing closer to adopting some form of MMT. Their economy is really weak now. And once you see job guarantees coming, then others will follow. Tim notes “You won’t announce we’re doing ‘modern monetary theory’, but you will announce job guarantees. The first implementation will be the UK. The US will follow at some point.”

Investing in an MMT world

With significant experience in rates markets as Head of the boutique, Vimal Gor believes secular stagnation is a problem that is likely to persist for a long time to come. In the medium-term and for the practicalities of investing, the baton of policy stimulus will likely not be passed completely from the current hands of central banks to governments. Arguably, even within an MMT world with more of the heavy lifting done by government spending, we will remain in an environment of structurally lower yields over the long-term. The need for rates to remain low or lower represents further opportunities for bonds as we see the race to the bottom continue. Bonds will also continue to offer investors the important safe-harbour that is critical when risk-assets like equities suffer and as such, will remain a vital part of an investor’s portfolio.

With another cut from the RBA in October and expectations for further easing, in this update we examine the outlook for one of the central bank’s key targets; inflation. Our cash manager, Steve Campbell assesses the direction for the other – the labour market, which received greater emphasis in the latest statement from Governor Lowe. Meanwhile, the path of domestic credit continues to be directed by the global macro backdrop and as such we explain why we maintain flexible positioning.

Finally, humans’ impact on the environment has garnered even greater attention over the past several months and its importance for our clients continues to grow. We explain the evolving area of impact investing and illustrate the positive contributions it makes to the environment and broader society.

Australian Quarterly Update

Regnan has released its annual report on ESG Engagement and Advocacy activity throughout FY19. Climate risk remains an ongoing engagement theme with ASX200 companies and Regnan has increased engagement on climate related issues through the year. Human capital management and ethical conduct has been another key area of focus and Regnan has undertaken increased levels of engagement in this area. Full details are available in the report.

Download Regnan’s Annual Engagement and Impact Report here:

About Regnan

Regnan – Governance Research & Engagement Pty Ltd was established in 2007 to evaluate the relationship between environmental, social and corporate governance (ESG) factors and investment value. Regnan has evolved to become a global leader in long term value, systemic risk analysis and responsible investment advisory.

Regnan provides ESG integration, advisory and stewardship services on behalf of institutional investors including asset owners, fund managers, wealth managers, retail and investment banks to drive improved ESG performance in S&P/ASX200 listed companies. Regnan meets with directors and senior company leaders, in a constructive manner, to influence change on issues with the potential to impact value over the long term.

Regnan is also a regular contributor to the public debate on long term value and sustainability, and is an active commentator in the media and at corporate and financial industry events. Regnan also provides submissions to government and other policy makers to improve both sustainable investment and the identification of systemic risks.

Regnan’s research insights are applied to Pendal’s Sustainable, Ethical and mainstream funds where relevant, as well as enabling us to work with other institutional investors in meeting their sustainability objectives.

DISCLAIMER

This document has been prepared by Regnan Governance Research and Engagement Pty Limited (ABN 93 125 320 041), (“Regnan”) and is republished with Regnan’s permission. It is for general informational purposes only and should not be relied upon in making a decision to invest or a decision in relation to an existing investment. It has been prepared without taking into account any recipient’s personal objectives, financial situation or needs. Because of this, recipients should, before acting on this information, consider its appropriateness having regard to their individual objectives, financial situation and needs. This information is not to be regarded as a securities recommendation.

The information relates only to Regnan’s assessment, based on its research and the information available to it, of the performance of a company in relation to environmental, social and governance issues and should not be regarded as a recommendation or statement of opinion by Regnan on:

i. any other aspect of the company’s performance;

ii. the prospects of the company; or

iii. the company’s suitability or attractiveness from an investment perspective.

The views expressed in this document are exclusively those of Regnan and the information contained within is current as of the date of publication. Pendal Group is the owner of Regnan and commissioned the company to provide research and engagement services for use as inputs into the decision making processes for Pendal’s investment activities. The views of Regnan expressed in this article may differ from those held by Pendal Group.

Ashley Pittard, Head of Global Equities at Pendal recently presented his thoughts on the extent of risk that has developed in global equity markets at the Portfolio Construction Forum’s Strategies Conference 2019 – “20/20 Vision” . This article outlines the insights shared around why investors need to adopt a different mindset when it comes to investing in global equities in the 2020s.

Today global equities investors are facing into markets where the risks go well beyond trade wars and currency tantrums.

I’m proud of the first quartile performance Pendal’s Concentrated Global Share Fund has achieved since we commenced.

But it’s now more important than ever for investment managers in the global equities sector to have the right active strategy for the 2020s.

The extreme risk in global equities right now requires a different mindset as we enter the new decade.

September 15 marks the 11th anniversary of the Lehman bankruptcy and Global Financial Crisis (GFC).

That event sparked one of the greatest credit and equity bull markets in history as central banks adopted extreme and unprecedented monetary policies.

Along with conventional monetary policy actions including 735 interest rate cuts around the world, central banks took unconventional actions such as $US13 trillion worth of quantitative easing which essentially refers to “printing money”, preventing debt default and deflation.

End of the post-GFC era

Over the past ten years broad investment in global equities has been a great investment decision.

Investing in an index fund, exchange traded fund or a growth theme such as tech stocks would have done very well for your retirement savings instead of holding money in the bank.

After the GFC investors benefited from tail winds that drove share prices higher – such as falling interest rates, lower volatility, a declining Australian dollar and quantitative easing.

But that’s now changing.

The 2020s will be very different to the past decade.

In the new environment investors will need to be very selective rather than pursuing broad market exposure for their portfolios.

Macro supports such as cheap money and big government balance sheets won’t provide a blanket for all listed companies.

At Pendal we are contrarian, long-term fundamental stock pickers when it comes to global equities — so this environment plays to our strengths.

Markets in the new phase

Why am I so confident that these 10-year tail winds will become headwinds – even when volatility measures suggest risk is low in global equities?

It’s a hard ask for market valuations to be compelling when the market is trading at all-time highs. Price-to-Earnings ratios are over 17x and the S&P500 Index has grown to nearly four times its value since its GFC lows.

Bifurcation in the market is extreme and distortions are occurring within equity markets. We have a handful of mega cap technology-related stocks that have carried the market higher, while at the other end of the spectrum sectors deemed to be eternally disrupted have languished.

Growth sectors are significantly over-valued on traditional historical measures while value sectors are shunned.

This year just 6 % of the MSCI World Index stocks have accounted for 53% of the return for the global equity index.

Meanwhile, interest rates are down a long way. We have had 29 cuts from central banks in 2019 and government bond yields for the largest economies are at a 120-year low.

It is hard to say they will be going significantly lower. Consider the US 10-year bond as a proxy. In 2012 when the market believed the euro would break up and European banks would be nationalised, the US 10-year bond touched 1.36%. In 2016 when the ‘Brexit’ vote occurred, it touched 1.36%. In August it has drifted past the 1.75% level.

The Aussie dollar has collapsed from $1.10 over the last decade to hover around the US$0.70 level within a small range. Currency volatility for the major economies is at the lowest level since 1992.

But we have just started to see the US officially label China a currency manipulator.

It is timely to recall the 1995 Plaza Accord, a joint-agreement between France, West Germany, Japan, the United States and the United Kingdom, to depreciate the US dollar in relation to the

Japanese yen and German Deutsche Mark by intervening in currency markets. This event turned currencies upside down at the time and placed Japan into its lost decade. This event turned currencies upside down at the time and placed Japan into its lost decade.

It’s interesting that many economists saw this accord as a direct response from the US to the threat from Japan’s growing status as an economic superpower.

In my view equity risk is the highest in more than 20 years – regardless of what traditional volatility measures suggest.

When you have $US13.7 trillion of negative yielding debt globally investors have been pushed up the risk curve to chase ever decreasing yields.

And when you fundamentally change the value of cash massive distortions occur. We are seeing this on many levels.

Global debt is now 3.2 times the size of global GDP – again at an all-time high.

We have been here before

The tech sector – especially the FAANGs (Facebook, Amazon, Apple, Netflix and Google)- have been the darlings of the bull market for the last 10 years.

Real estate and utilities stocks have also been drivers of market returns, thanks largely to declining interest rates.

But the elephant in the room is the tech sector.

It has tripled its index weight since the GFC and doubled its index weight in the US market over the past five years.

Tech has been at the epicentre of this self-fulfilling circle — declining interest rates, exploding debt and rampant passive investing have helped to triple its representation of the market.

No doubt these are great businesses but it’s amazing how big their market capitalisations are — especially when compared to the GDP of some countries.

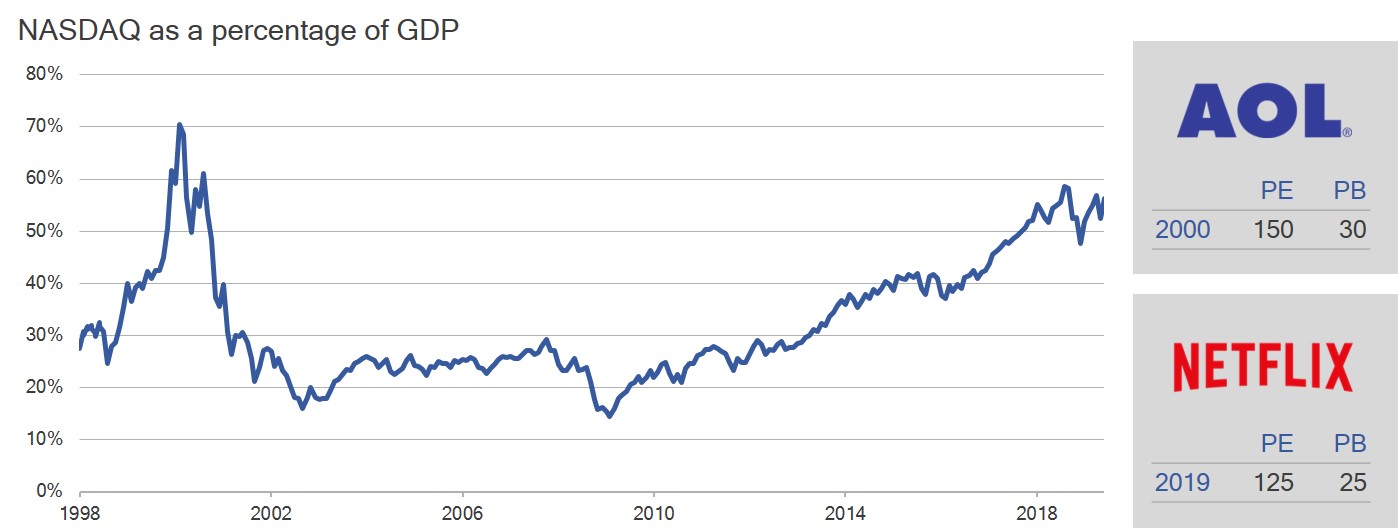

If we use the 2000 technology bubble as another proof point, the valuations again are stark.

It’s uncanny how AOL at its peak traded at similar levels to Netflix today.

Look at the metrics on the right hand side of this graph:

* Source: Bloomberg, Pendal. PE refers to price-earnings ratio, PB refers to price-book ratio.

You could argue about the relevance of using a price-book ratio for these tech names but as a long term valuation tool across different sectors, price-book is still a clean gauge of value.

And Nasdaq as a percentage of GDP is near historical bubble levels.

The extreme size of valuation premiums is a key risk driver.

Passively fulfilling a virtuous cycle

Here’s another aspect of the self-fulfilling circle. Passive and index-hugging strategies are reinforcing these valuation trends.

Over the past 10 years $US4.1 trillion has gone into passive investment funds versus outflows of $US1.5 trillion out of active.

In the year-to-date we have seen 65% of stocks in the MSCI World proceed into bear markets as passive inflows top $US7.4 billion and outflows from active strategies top $US22.4 billion.

The issue here is index and traditional strategies — by their inherent design — see more and more investors bet on higher growth for what has already risen.

This creates distortions in the market as passive ETFs focus on the largest companies in a sector, not the best companies.

Why we’re different

At Pendal, we are clearly very different.

We don’t look at the largest companies — just the best companies.

We focus on leading number one or number two franchises in their space when they are out of favour — regardless of size.

That is the lowest cost producer if it’s a commodity or largest market share if it’s a bank. We like monopoly assets.

We look at industries horizontally — not vertically as do many traditional index strategies.

We focus on fewer higher quality businesses and build a deep understanding of them like a business owner would.

We launched our Concentrated Global Share Fund three years ago and we have been very happy with the 1st quartile performance over the three-year period which reflects this very different approach compared to passive index following strategies.

Our philosophy and process has been the same since I started at BT Australia (the former entity name of Pendal) more than 20 years ago.

We have a universe of about 500 leading businesses that we follow.

We spend a lot of time focusing on disruption in industries. Usually we are buying businesses when we think they are cyclically depressed — while the market may think they are structurally impaired.

In our experience, only 15-20% of the market is attractive at any point in time.

You need to be very selective to grow wealth over the long term. Our top 10 holdings (see table) are very different to the index. We have a very large active positions.

We hold specific industry leaders such as Anheisser Busch Inbev – a leader in the beverage market.

We hold Colgate – makers of toothpaste around the world. We hold Total – Europe’s leader in oil and gas production.

We don’t hold these companies because they’re included in the Index or have driven returns. We hold them for very different reasons.

Consider the recent Amazon Wholefoods acquisition as an example.

The consumer staples sector shows how we like to research, stay patient and use disruption to our advantage.

We focus on the best businesses, understand fundamentally how they work, then stay patient and wait until they are out of favour.

There is no doubt the Amazon Wholefoods deal will change food distribution globally.

As a result of this disruption the market discounted the sector as they questioned the brand value longer term post the deal.

We looked at the industry differently and focused on market share and their return on investment (ROI).

It was clear you only wanted to focus on P&G and Colgate with greater than 60% market share and 100% ROI.

We never wanted to own Kraft Heinz, Campbell soup or Kellogg’s due to their lower market shares — even though they were larger in the index.

Think differently to drive different results

Overall I believe you need to think differently, have a concentrated highly active and very selective stock picking approach,

Think like an owner in a group of #1 unique premium assets, be patient on valuation and get paid a dividend to wait while the business normalises.

This will serve you well as we enter the next decade.

Convulsion: a sudden, violent, irregular movement of the body, caused by involuntary contraction of muscles and associated especially with brain disorders such as epilepsy; a violent social or political upheaval

Our long-planned trip to visit companies in China could not have been better timed. A breakdown of negotiations between the US and China prompted President Trump to impose higher tariffs on a wider range of product imports from China. Combined with the imposition of sanctions on Chinese telecom and technology giant Huawei, this has convinced almost all seasoned observers of geopolitics that the ‘genie is out of the bottle’. The posturing and counter-moves by the two global economic giants is just the start of what could be a long lasting ‘economic war’ for ideological dominance in the decades to come. It is beyond my remit to posit on this development, yet suffice to say all countries will need to rethink and adjust as we undergo a massive change to the current global political and economic order.

“Overall the mood in China was combative and downbeat”

Most of the companies we met were cautious to downbeat. To generalise, as industrial profit growth in China slows sharply and export orders come under a cloud, almost every firm is understandably affected. There was a common thread running through most companies’ future expectations: government policies will save the day. I met a few companies which rank very high on the quality and growth score (in the health care and consumer space) but valuations reflect a lot of positivity. Those are on my radar to buy in case markets face further challenges, but overall the mood in China was combative and downbeat.

Our working assumptions are that growth rates (in China and globally) will moderate while volatility of growth will increase. In what is not just a case for China, governments and central banks across the world will increasingly try to cushion negative outcomes for growth in almost every country. Hence, risk of policy mistakes – knowable only in hindsight – will exacerbate asset price moves. Corporate capital expenditure and consumer spending might reflect a high degree of caution as confidence and clarity is diminished.

Pumping life through the economy

In other news, election results in Indonesia and India have given an increased mandate to incumbents. Both leaders face similar challenges: revitalising growth, job creation, growing income levels and infrastructure investment are the priorities. These challenges have no immediate solutions. In a challenged external environment bordering on protectionism, government subsidies will play an increasing role to help the lower strata of society. The constraint will be the fiscal deficit of both countries, but, from what I have read, the initial thrust of both governments will be on devising strategies towards this end. By way of example, Indonesia’s actions of the past few years may be indicative of policy direction for its peers.

Indonesia: Purse wide open

Source: CLSA Securities

Despite these efforts, growth has been difficult to come by. In Indonesia’s case in particular, there is an urgent need to address relatively inflexible labour laws. This has been the most cited reason for the lack of significant relocation of manufacturing at a time when firms are looking for alternatives to China.

Cautious, yet confident

From a portfolio standpoint, there is a fair bit of defensiveness through most of our holdings. I have tried to focus on companies that have managed the disruptive forces of online commerce and stand a better chance of success. With uncertainty emanating from restrictive trade policies, vigilance on monitoring second order effects (like moderation of consumer demand) will be important. There is genuine concern over the economy in China, yet even in these times there are pockets of growth. With this in mind I am keen to add to a couple of names in the ‘A’ share market if there is a further sell-off.

Fund Manager commentary for the month ended 31 May 2019 covering market reviews, Pendal fund performance and our outlook for the period ahead.

Access the monthly commentary here.

In this Australian Quarterly Update, we analyse the hot-button issue of negative gearing and the potential effects of proposed Labor policies on the domestic housing market. We also look at why some of the broader global concerns appear to be easing for local credit investors, as well as developments in the local cash market. Finally, we examine ESG trends in Australia and distinguish between the range of different classifications in the area.

I hope you find the piece useful and we welcome feedback from readers.

View our Australian Quarterly Update here.

Fund Manager commentary for the month and quarter ended 30 September 2018 covering market reviews, Pendal fund performance and our outlook for the period ahead.

Access the monthly commentary here.

Access the quarterly commentary here.

Fund Manager commentary for the month ended 31 August 2018 covering market reviews, Pendal fund performance and our outlook for the period ahead.

Access the monthly commentary here.