Mainstream Online Web Portal

LoginInvestors can view their accounts online via a secure web portal. After registering, you can access your account balances, periodical statements, tax statements, transaction histories and distribution statements / details.

Advisers will also have access to view their clients’ accounts online via the secure web portal.

Tim Hext: Australian inflation is heading back to 4pc

This article is more than 12 months old. Find our latest insights here

Despite higher-than-expected monthly data, the outlook for inflation should be mildly friendly over the next few months, says Pendal’s TIM HEXT

- Why bonds, why now? Pendal’s income and fixed interest experts explain

- Browse Pendal’s fixed interest funds

THE RBA will be encouraged things are moving in the right direction on the inflation front.

The June quarter inflation numbers came in this week at 0.8% for the quarter, or 6% annual.

Underlying inflation (the trimmed mean where they remove the highest and lowest 15%) came in at 0.9%, or 5.9%.

These outcomes were both 0.2% lower than expected.

The RBA is now forecasting 4.5% by year end. Given we are at 2.2% for the first six months of 2023 this seems a little high if anything.

We forecast 4.2% by year end, unchanged from before.

We last saw a 0.8% result in Q3 2021, just before the very large numbers kicked in.

However this may prove to be a low point for the quarterly number this year as utility prices kick in again in Q3 and Q4.

We expect 1.1% in Q3 and 0.9% in Q4 as goods prices moderate but services remain elevated.

The high and lows of these numbers

Let’s start with the items that are accelerating.

Rents are finally kicking in, up 2.5% for the quarter and 7.3% for the year. They are finally catching up with other rental indicators and should remain at 2.5% a quarter for a while yet.

Find out about

Pendal’s Income and Fixed Interest funds

Insurance was up 5.3% for the quarter – no surprise for anyone who has received a payment notice recently.

International travel was up 6.5% in the quarter, again of little surprise.

On the high, but moderating side was new home dwellings.

They rose by 1% in the quarter, though that’s a long way down from the peak. The supply side issues in building seem to be finally working their way through.

On the low side, five of the 11 categories actually saw prices slightly fall.

Most of these were due to government subsidies, highlighting the impact both federal and state governments are having on dampening inflation.

Health, education, electricity and gas were impacted by government subsidies, highlighting the impact governments are having on dampening inflation. Q3 and Q4 will see utilities rebound sharply.

More genuine were falls in motor vehicles, telecommunications and domestic holiday travel as supply constraints ease.

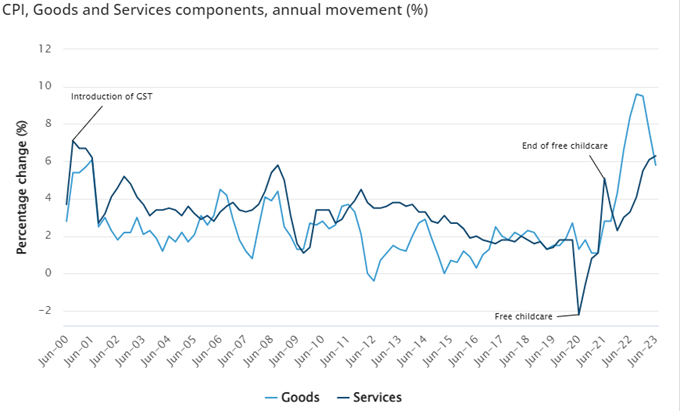

Goods versus Services

Services inflation is finally higher than goods.

The ABS provided us with this graph below, which highlights services inflation above 6% — not seen since GST started in 2000.

Given the strong link to wages this highlights the RBA point that wage growth above 4% with no productivity is not consistent with target inflation.

The RBA

Despite strong employment data this number should continue to provide the RBA headroom to stay on hold.

August will be Dr Lowe’s second last meeting in charge and having moved 4% in a little over 12 months there is room for further patience.

It will be interesting to see if the inflation forecasts are lowered again, although they lowered them in May and hiked anyway so perhaps it doesn’t matter too much.

Three-year swap is now around 4.25%, and the market has one more hike priced in.

I suspect the RBA will keep one more hike up its sleeve and if unemployment has not risen by October they may execute.

This would be Michele Bullock’s first meeting in charge where she may choose to stamp her mark as an inflation-fighting governor.

About Tim Hext and Pendal’s Income & Fixed Interest boutique

Tim Hext is a Pendal portfolio manager and head of government bond strategies in our Income and Fixed Interest team.

Tim has extensive experience in banking, financial markets and funding including senior positions with NSW Treasury Corporation (TCorp), Westpac Treasury, Commonwealth Bank of Australia, Deutsche Bank, Bain & Co and Swiss Bank Corporation.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia.

Find out more about Pendal’s fixed interest strategies here

About Pendal

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

In 2023, Pendal became part of Perpetual Limited (ASX:PPT), bringing together two of Australia’s most respected active asset management brands to create a global leader in multi-boutique asset management with autonomous, world-class investment capabilities and a growing leadership position in ESG.

This information has been prepared by Pendal Fund Services Limited (PFSL) ABN 13 161 249 332, AFSL No 431426 and is current at July 27, 2023. PFSL is the responsible entity and issuer of units in the Pendal Monthly Income Plus Fund (ARSN: 137 707 996) and Pendal Dynamic Income Fund (ARSN: 622 750 734) (Funds). A product disclosure statement (PDS) is available for the Fund and can be obtained by calling 1300 346 821 or visiting www.pendalgroup.com. The Target Market Determination (TMD) for the Fund is available at www.pendalgroup.com/ddo. You should obtain and consider the PDS and the TMD before deciding whether to acquire, continue to hold or dispose of units in the Fund. An investment in the Fund or any of the funds referred to in this web page is subject to investment risk, including possible delays in repayment of withdrawal proceeds and loss of income and principal invested. This information is for general purposes only, should not be considered as a comprehensive statement on any matter and should not be relied upon as such. It has been prepared without taking into account any recipient’s personal objectives, financial situation or needs. Because of this, recipients should, before acting on this information, consider its appropriateness having regard to their individual objectives, financial situation and needs. This information is not to be regarded as a securities recommendation. The information may contain material provided by third parties, is given in good faith and has been derived from sources believed to be accurate as at its issue date. While such material is published with necessary permission, and while all reasonable care has been taken to ensure that the information is complete and correct, to the maximum extent permitted by law neither PFSL nor any company in the Pendal group accepts any responsibility or liability for the accuracy or completeness of this information. Performance figures are calculated in accordance with the Financial Services Council (FSC) standards. Performance data (post-fee) assumes reinvestment of distributions and is calculated using exit prices, net of management costs. Performance data (pre-fee) is calculated by adding back management costs to the post-fee performance. Past performance is not a reliable indicator of future performance. Any projections are predictive only and should not be relied upon when making an investment decision or recommendation. Whilst we have used every effort to ensure that the assumptions on which the projections are based are reasonable, the projections may be based on incorrect assumptions or may not take into account known or unknown risks and uncertainties. The actual results may differ materially from these projections. For more information, please call Customer Relations on 1300 346 821 8am to 6pm (Sydney time) or visit our website www.pendalgroup.com