Mainstream Online Web Portal

LoginInvestors can view their accounts online via a secure web portal. After registering, you can access your account balances, periodical statements, tax statements, transaction histories and distribution statements / details.

Advisers will also have access to view their clients’ accounts online via the secure web portal.

Tim Hext: Finally a good year for labour

This article is more than 12 months old. Find our latest insights here

Wages are the next battleground for policy. Pendal’s TIM HEXT explains how it will play out and what it means for investors

THE upcoming federal election will determine if it’s a good year for the Australian Labor Party, which for some reason adopted the US spelling more than a century ago.

No matter the election result, it will finally be a good year for labour at least.

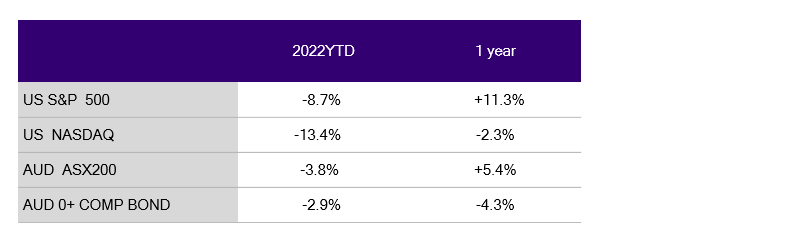

This year has not started well for asset owners, though a late 2021 surge means the one-year picture is better.

Here are the returns in AUD:

Of course these are nominal returns. If we look at it in real returns (including inflation) the picture is 3.5% worse. Spending power is going backwards.

This week we are seeing further evidence of the next battleground for policy — wages.

Wages will be under pressure on two fronts.

Firstly, workers who are feeling cost-of-living pressures are more likely to push for higher increases.

Secondly, there is a window in Australia we have not seen for a very long time where limited migration means worker shortages. Unions are not going to miss their chance.

Teachers and nurses have already begun their bargaining dance and transport workers have now joined them.

Expect a lot more of this as the NSW government (and others) 2.5% wage policy comes under attack. First introduced by Mike Baird a decade ago they got away with it given private sector wages were 2.5% or even lower.

The next year or even two will not be that kind. Collective agreements and awards underpin the majority of wages.

Watching with keen interest will be the RBA.

Wages are the ultimate lagging indicator but the clock is now ticking.

We think the market will be right about rate rises this year, likely beginning in August — though five hikes is probably one too far.

It is important to keep some perspective though. If by December we have a strong economy, wages at 3.5%, unemployment at 3.5% and inflation at 3% then it should be smiles all round.

Capital has had a much better decade — even during Covid — than labour. So a reversal for several years should be applauded.

Ultimately a strong economy, spurred on by pent-up savings and re-openings, should mean risk markets take rate hikes in their stride.

Mistakes happen late cycle and that will be a number of years away.

Investors should take advantage of higher bond yields in the next few years to start building up some defensive positions.

At 2.5% (zero real yields plus 2.5% inflation) I will stop calling bonds expensive.

History suggests, though, it is too early to call them cheap.

Find out about

Pendal’s Income and Fixed Interest funds

About Tim Hext and Pendal’s Income & Fixed Interest boutique

Tim Hext is a Pendal portfolio manager and head of government bond strategies in our Income and Fixed Interest team.

Tim has extensive experience in banking, financial markets and funding including senior positions with NSW Treasury Corporation (TCorp), Westpac Treasury, Commonwealth Bank of Australia, Deutsche Bank, Bain & Co and Swiss Bank Corporation.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia.

Find out more about Pendal’s fixed interest strategies here

About Pendal

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

In 2023, Pendal became part of Perpetual Limited (ASX:PPT), bringing together two of Australia’s most respected active asset management brands to create a global leader in multi-boutique asset management with autonomous, world-class investment capabilities and a growing leadership position in ESG.

This information has been prepared by Pendal Fund Services Limited (PFSL) ABN 13 161 249 332, AFSL No 431426 and is current as at February 21, 2022.

PFSL is the responsible entity and issuer of units in the Pendal Monthly Income Plus Fund (ARSN: 137 707 996) and Pendal Dynamic Income Fund (ARSN: 622 750 734) (Funds). A product disclosure statement (PDS) is available for the Fund and can be obtained by calling 1300 346 821 or visiting www.pendalgroup.com. The Target Market Determination (TMD) for the Fund is available at www.pendalgroup.com/ddo. You should obtain and consider the PDS and the TMD before deciding whether to acquire, continue to hold or dispose of units in the Fund.

An investment in the Fund or any of the funds referred to in this web page is subject to investment risk, including possible delays in repayment of withdrawal proceeds and loss of income and principal invested.

This information is for general purposes only, should not be considered as a comprehensive statement on any matter and should not be relied upon as such. It has been prepared without taking into account any recipient’s personal objectives, financial situation or needs. Because of this, recipients should, before acting on this information, consider its appropriateness having regard to their individual objectives, financial situation and needs. This information is not to be regarded as a securities recommendation.

The information may contain material provided by third parties, is given in good faith and has been derived from sources believed to be accurate as at its issue date. While such material is published with necessary permission, and while all reasonable care has been taken to ensure that the information is complete and correct, to the maximum extent permitted by law neither PFSL nor any company in the Pendal group accepts any responsibility or liability for the accuracy or completeness of this information.

Performance figures are calculated in accordance with the Financial Services Council (FSC) standards. Performance data (post-fee) assumes reinvestment of distributions and is calculated using exit prices, net of management costs. Performance data (pre-fee) is calculated by adding back management costs to the post-fee performance. Past performance is not a reliable indicator of future performance.

Any projections are predictive only and should not be relied upon when making an investment decision or recommendation. Whilst we have used every effort to ensure that the assumptions on which the projections are based are reasonable, the projections may be based on incorrect assumptions or may not take into account known or unknown risks and uncertainties. The actual results may differ materially from these projections.

For more information, please call Customer Relations on 1300 346 821 8am to 6pm (Sydney time) or visit our website www.pendalgroup.com