Close

Leave Feedback

Welcome to the new btim.com.auTake a two minute tour to see what we've changed

Hi there! Welcome to the new look Pendal website... Take a two minute tour to see what we’ve changed.

Mainstream Online Web Portal

LoginInvestors can view their accounts online via a secure web portal. After registering, you can access your account balances, periodical statements, tax statements, transaction histories and distribution statements / details.

Advisers will also have access to view their clients’ accounts online via the secure web portal.

The Point

Quick, actionable insights for investors

Australian Equities

Crispin Murray: Two factors underpinning ASX company earnings

Most people would be aware from last week’s per-capita recession headlines that Australia’s population growth is outstripping economic growth.

But population growth – especially immigration and temporary visas – is also supporting corporate earnings, says Pendal’s head of equities Crispin Murray.

“All up, we’re probably looking at about a 3 per cent rise in the population today versus a year ago.

“People are coming to Australia with money in their pockets, setting themselves up and getting accommodation – which is driving up rents.

“Part of the reason we’re seeing resilience in the top line of companies is because they’re basically driven by nominal GDP, not per capita GDP.”

Population growth is also offsetting the effects of the ‘mortgage cliff’ which forces households into higher, variable mortgage payments as low-rate fixed loans expire, Crispin says.

“With each company we met over reporting season, we talked about the issues facing them and if they were seeing consequences from this mortgage cliff. So far, the consequences are very limited.”

Small businesses are doing it tough. Cloud accounting platform Xero has some answers

Quick view

Small businesses are doing it tough. Cloud accounting platform Xero has some answers

Xero’s annual Xerocon event is known as ‘Coachella for accountants’ – a reference to a Californian rock concert with a cult-like following.

The ASX-listed cloud-accounting platform has a pretty strong following itself now, with more than 3.7 million subscribers in 180 countries.

That’s led to a pretty good understanding of the state of small-to-medium businesses (SMBs), says Pendal equities analyst Elise McKay.

Xero is seeing SMBs report slower sales growth in Australia, Canada, NZ, the UK and the US, though wage pressures are starting to ease in Australia, NZ and the UK, says Elise.

While SMBs are still unsure about the impact of AI, Xero is adding the technology to speed up repetitive tasks or provide better insights that help humans focus on high-value strategic activities.

“For example, helping to better enable reconciliations or provide better forecasting tools around things like cash flow. And potentially using generative AI to improve customer support.”

What’s driving ASX stocks this week

Quick view

What’s driving ASX stocks this week

Three things stood out among the best industrials this ASX earnings season

Quick view

Three things stood out among the best industrials this ASX earnings season

What did the best-received results have in common this ASX earnings season?

Among industrials – which includes industries such as transportation and machinery – it was all about pricing power, cost of debt and where a company sits in its business cycle, says Pendal analyst Anthony Moran.

“Some companies with pricing power have not only kept up with prices, but have also been able to achieve some margin expansion,” says Anthony. He points to James Hardie and Boral as examples.

This season marked a return to more typical themes after cost control, staffing and inflation dominated post-Covid reporting, Anthony says.

And don’t forget the weather.

“It’s not just resilient demand in Australia. It’s also the good weather. That’s quite significant for Australian construction companies.”

What about the rest of the ASX? Find out next Thursday when Pendal’s head of equities Crispin Murray delivers his bi-annual Beyond The Numbers report.

Crispin Murray: What’s driving Aussie equities this week

Quick view

Crispin Murray: What’s driving Aussie equities this week

Confidence in China continues to weaken.

High youth unemployment is deterring consumer spending. Fears about the solvency of private developers are discouraging new home purchases.

Investment trust defaults such as Zhongrong risk triggering redemption requests, leading to a potential liquidity squeeze.

A number of incremental policy initiatives have been unable to reverse deteriorating sentiment.

Despite the bearish portrait, our head of equities Crispin Murray notes that some China-related stocks and ASX sectors have held up – notably the miners.

The bulls are taking the view that things are so bad, they’re good – which increases the chance of a more convincing policy response such as the one we saw in 2015, says Crispin.

“They are drawing a comparison with the period prior to the reversal of the Zero-covid policy, where there were incremental signals before a major policy change,” says Crispin.

If a major policy response doesn’t materialise, Crispin sees some risk around bulk commodity producers at these levels.

Elise McKay: The questions to ask this ASX earnings season

Quick view

Elise McKay: The questions to ask this ASX earnings season

ASX earnings season kicks off next week. What should Aussie equities investors be looking for?

Much more than revenue and profit margins, says Pendal investment analyst Elise McKay.

The macro-economic environment will play a big part, predicts Elise.

“In the US, even though companies are delivering better earnings, their share prices aren’t going up on the news.

“The recent market outperformance has been driven by the macro environment, not the earnings.”

Elise says investors should be asking: “Have companies maintained the ability to pass through higher prices? What’s happening to wages? Are further cost reduction programs announced?”

Look out also for how companies are managing opportunities and threats related to artificial intelligence, she says.

Crispin Murray: What’s driving Aussie equities this week

Crispin Murray: What’s driving Aussie equities this week

Quick view

Crispin Murray: What’s driving Aussie equities this week

EQUITIES continue to rally even as bond yields rise on the back of the Fed’s “hawkish pause” which held rates steady but added in a second rate rise by the year’s end to the “dot plot”.

The market is not convinced of the need for that hike, with CPI data indicating inflation is coming down.

There has been some good news recently.

Jim Taylor: What’s driving ASX stocks this week

Quick view

Jim Taylor: What’s driving ASX stocks this week

Each week our Aussie equities team runs through the factors driving the Aussie stock market.

Observations on two major forces stood out in the latest report from PM Jim Taylor – one in the virtual world and one in the physical world.

On the AI mania gripping US markets, Jim noted that last week was the biggest ever weekly inflow into US listed tech companies at close to $US9 billion, according to researcher EPFR.

“That’s about 40% more than the next biggest inflow in 2021.”

Those more invested in the physical world would have noted the Bureau of Meteorology updating its El Niño-Southern Oscillation outlook from “watch” to “alert”.

“This means about a 70 per cent chance of El Niño forming in 2023 – roughly three times the normal chance,” said Jim.

“After three years of high rainfall, the ‘weather ate my homework’ excuse may be taken off the table for many ASX-listed companies.”

What’s driving ASX stocks this week

Quick view

What’s driving ASX stocks this week

Do spikes among US chipmakers such as NVIDIA and Marvell mark the start of a multi-year, AI-driven bull cycle?

What might it mean for ASX stocks?

NVIDIA and its rivals are churning out Graphics Processing Units which are in-demand for AI services such as OpenAI’s ChatGPT.

Pendal equities analyst Elise McKay notes that just seven US tech mega caps (Apple, Microsoft, Alphabet, Amazon, NVIDIA, Meta and Tesla) have driven most of the 25% NASDAQ rally this year.

“But valuation metrics for this group do not seem stretched,” she says. “They are growing, making efficiency gains, have strong balance sheets, are buying back stock and may be moving into a more favourable macro and interest rate backdrop.

“While timing and take-up of accelerated computer infrastructure is uncertain, we expect this to be a net positive for ASX-listed data centre player NEXTDC.

“There could also be a positive impact for Macquarie Technology’s data centre business and Megaport on the network-as-a-service side.”

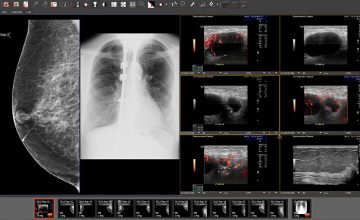

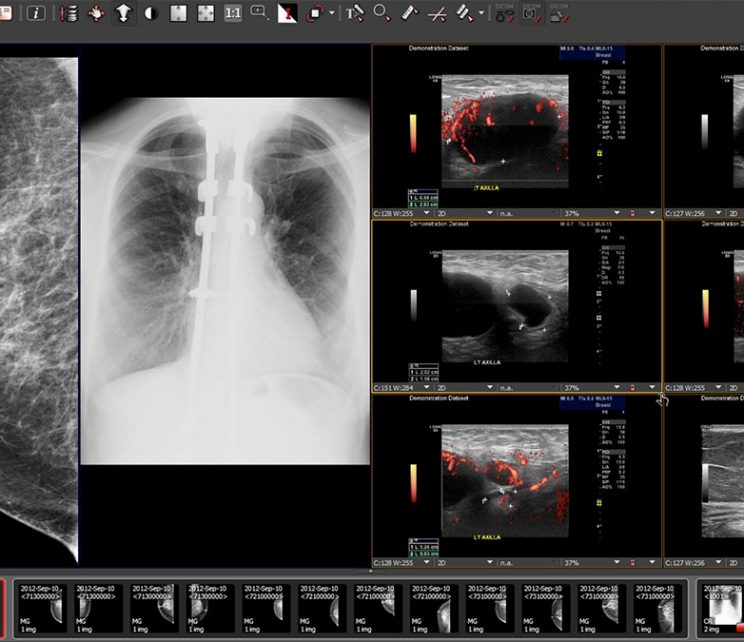

ASX midcaps: Why medical imager Pro Medicus has captured our attention

Quick view

ASX midcaps: Why medical imager Pro Medicus has captured our attention

Sam Hupert started as a GP in 1980 and within a couple of years realised the then-nascent world of computing would have a big impact on medicine.

Within three years he’d started Pro Medicus, an imaging software provider working with hospitals, imaging centres and health care groups.

Today the ASX-listed group – held in Pendal Midcaps Fund – is worth more than $6 billion.

The global diagnostic imaging market is worth some $US28 billion globally – and growing at 4.9%, according to Grand View Research.

Growth drivers include an increasing prevalence of lifestyle-related diseases, rising demand for early detection tools, speedier diagnosis, government investment and expansion into developing nations, Grand View reports.

Pro Medicus is mainly in radiology now, but its technology could be used in cardiology, ophthalmology and pathology and all areas of reflected light, says Pendal equities analyst Oliver Renton.

Crispin Murray: Pollution law shows investors need to keep a close eye on government

Quick view

Crispin Murray: Pollution law shows investors need to keep a close eye on government

Government policy is a significant risk to investors, particularly in the resources and energy sectors, says our head of equities, Crispin Murray.

Sovereign risk can be more unpredictable than competitor risk, Crispin told a recent AFR conference.

“Competitors are largely focused on returns, so you can anticipate what they’re likely to do. But governments overlaying policy agendas can create quite unpredictable risks.

As an example, Crispin points to the federal government’s “safeguard mechanism” law which will regulate Australia’s 215 biggest polluters from July.

“They are still negotiating on details, but it means we’re asking mining companies, as an example, to quickly cut their scope-one emissions.

“That means cutting diesel emissions over the next seven years – and there’s no solution to that.

“I think we will see carbon price go up more than people realise. And it’s not beyond the realms of possibility we’ll see a carbon price by the end of the decade.”

Loading posts...

Loading posts...