Significant Features: The Pendal Active Conservative Fund is an actively managed diversified portfolio that invests in Australian and international shares, Australian and international listed property securities, Australian and international fixed interest, cash and alternative investments. The Fund has a significant weighting towards defensive assets.

Fund Objective: The Fund aims to provide a return (before fees, costs and taxes) that exceeds the Fund’s benchmark over the medium term.

Investors expect China may turn its regulatory spotlight on property after tightening industries such as education. Pendal’s Samir Mehta explains the outlook

- China seeking to reduce cost of living pressures on families

- Property industry may be next in Beijing’s sights

- Slowdown would have global ramifications

CHINA’s regulatory tightening of industries such as education, ridesharing, games and food delivery has sent shudders through global investment markets in recent weeks.

The policy changes — which aim to improve quality of life, redistribute income and relieve cost-of-living pressures among China’s most disadvantaged people — may go further with the giant property industry next on the list of investor concerns.

A tightening of property regulation leading to a slow-down in China’s real estate industry would pose a real risk for Australian investors given our commodity exposure to Chinese growth.

How might a China property slowdown play out?

What should investors be looking out for as they weigh these issues?

A real risk

Pendal’s Samir Mehta, who manages Pendal Asian Share Fund, says investors face a real risk that property is next in Beijing’s policy sights.

“There has been chatter around property, because buying a property or renting one remains one of the biggest outlays for an average family,” says Mehta.

“Disparities of income have led to significant real estate price appreciation, particularly in cities like Shanghai, Beijing and Shenzhen.

“There have been a few local articles that have talked about the rising multiples of annual income now required to buy an apartment.”

Find out about

Pendal Asian Share Fund

Regulatory intervention in China’s real estate market could take a number of forms such as:

- Mandating affordable housing as part of new property developments

- Restrictions on investment properties

- New property taxes

- Changing the way capital gains are taxed

Each of these could have serious ramifications for economic growth.

“This is a very tricky part of the economy because of the interactions between construction, property price appreciation and the way provincial and city governments raise revenue through land sales,” Mehta says.

“If China adjusted its policies there would be a noticeable impact down the whole chain.”

Residential property construction is an important component of China’s GDP, “so if property does come under the microscope, you should expect further slowdown.”

“Then there is mounting burden of debt in the system; a fair bit on the balance sheet of property developers and individual mortgages for residence or investment purposes.”

Impact ‘way beyond stocks’

“The impact could be way beyond stocks. Because you’re talking about a system that is built on GDP growth, built on construction, built on debt for that sector and revenues for the government. It’s across the board.”

As a major supplier of building materials including iron ore, Australia could endure the biggest impact of policy changes on China’s real estate.

Iron ore prices fell by a third in recent weeks as China slowed steel production to curb carbon emissions.

Changes to the Chinese property industry would put further pressure on the iron ore price.

What are the signs an investor should look out for?

Investors should watch Chinese retail sales, sales of property and credit growth as leading indicators of a Chinese downturn, Mehta says.

If there is evidence of slowing, investors should watch how China’s central bank responds.

The People’s Bank of China has been winding back stimulus — but they may change tack if Beijing’s policies start to affect property process and weaken the economy too much.

“The ramifications of a slowdown in China are going to be global in nature, and therefore it’s very important for the next three-to-six months to observe how the economy in China fairs,” says Mehta.

About Samir Mehta and Pendal Asian Share Fund

Samir manages Penda’s Asian Share Fund, an actively managed portfolio of Asian shares excluding Japan and Australia. Samir is a senior fund manager at UK-based J O Hambro, which is part of Pendal Group.

Pendal Asian Share Fund aims to provide a return (before fees, costs and taxes) that exceeds the MSCI AC Asia ex Japan (Standard) Index (Net Dividends) in AUD over the medium-to-long term.

Find out about Pendal Asian Share Fund

About Pendal Group

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Significant Features: Barrow Hanley Concentrated Global Share Fund Hedged is an actively managed, concentrated portfolio of global shares and is diversified across a broad range of global sharemarkets.

Fund Objective: The Fund aims to provide a return (before fees, costs and taxes) that exceeds the MSCI World ex Australia (Standard) Index (Net Dividends) hedged to AUD over the medium to long term.

Here are the main factors driving Australian equities this week according to Pendal’s head of equities Crispin Murray. Reported by portfolio specialist Chris Adams.

WE HAVE seen positive developments on two fronts in the past week.

Firstly, Fed Chair Jerome Powell was relatively dovish in his Jackson Hole speech, calming fears of aggressive tightening.

Secondly, there are signs that Covid cases may be peaking in the US.

In response, we saw bond yields rise slightly in a controlled manner, commodities rally and equity market gains. The S&P/ASX 300 rose 0.57% and the S&P 500 1.54% for the week.

The domestic reporting season remains a small positive.

Last week’s theme was the return of the unloved. Some of the re-opening stocks rallied as investors got a better gauge on near-term risks and were prepared to look through them.

We see four key issues facing markets:

- Economic growth: Having reached peak momentum do we see material downside surprises as a result of fiscal cliffs and the re-emergence of structural issues?

- Covid: Does a combination of the Delta variant and waning immunity lead to an environment of perpetual new waves that require on-going restrictions, limit the service sector recovery, hit confidence and lead to weaker growth?

- Inflation: Will it be higher than expected if recent drivers prove to be more than “transitory” and a tight labour market drives wage growth?

- Policy: Is there a risk of policy mistakes as central banks exit quantitative easing (QE) and attempt to reconcile the need to anchor inflation expectations and support growth?

Good news on Covid and policy should help support markets into the quarter’s end.

Fed policy outlook

At this point, the Fed is managing its message well.

The minutes of the last FOMC meeting indicated that QE tapering would occur sooner than previously indicated.

Cautious statements from some committee members raised concerns that Powell may have struck a more hawkish tone.

While Powell did clearly suggest tapering is coming this year — probably announced in November and started in December — he also signalled:

- There is almost no chance of tapering in September

- The Delta strain is a clear risk to growth, which may offset the impact of positive employment data on policy decisions

- The decision to taper is distanced from the decision on rates. Rate rises may not follow on the heels of QE tapering as quickly as many expect

- He still sees recent inflation as transitory

The analogy is that, in taking the foot off the accelerator of QE, the Fed is not yet ready to start pumping the brakes of rate rises.

At this point the risk of a 2013-style taper tantrum is low as long as unemployment or inflation data does not materially surprise.

This time around the Fed has been very careful to seed the market and manage expectations.

Tapering looks set to align with a reduction in the issuance of treasuries as stimulus measures fall away. There will be less of an issue with over-supply as a result.

Economic outlook

US savings rates have fallen from close to 35% at the peak of early 2020 to a more normalised rate of just under 10%. But this is still well above post-GFC levels.

Although the rate has fallen, the high levels of the past 18 months have left a significant amount of pent-up household savings which can be deployed.

Spending on goods appears to be rolling over from very high levels in the US.

It will important to see how far this falls in individual sectors. But we are also mindful that spending on services has only just returned to pre-Covid levels and is still well below trend growth.

Pendal Focus Australian Share Fund

A high-conviction equity fund with 16 years of strong performance in a range of market conditions

Delta may see some near-term pressure on this, but longer-term this is an additional source of spending growth in the US.

In Australia, retail sales have fallen quickly. Annualised growth was -15% in July, down from -1% in June.

Much of this is driven by NSW where sales fell 35% in July. By comparison, sales were up 11% in Western Australia.

This highlights risk in areas such as household goods, which are still well above trend growth levels.

Some 36% of Australians were under lockdown in July — and likely around 50% in August.

At this point Q3 GDP is expected to be down 3-4%. CY21 is now likely to step down to just over 1% GDP growth.

These near-term issues will affect growth and earnings, but it is clear there is still a lot of confidence in corporate Australia.

This is evident in capex intentions outside the mining sector, which continue to rise.

It has also been reinforced in our company meetings. A lot of management teams are pointing to how quickly demand snapped back once restrictions were lifted previously.

Covid outlook — international

Most regions are seeing a stabilisation in case trends.

Europe has so far avoided a Delta wave similar to that seen in the US and UK, reflecting ongoing caution in re-opening rules.

Israel continues to experience a surge in cases. But the number of hospital patients has stabilised at just over half the January peak.

Markets are focused on the US wave because of its potential to affect the global growth outlook.

Here, we have seen case growth and hospitalisations begin to decelerate.

Risks remain with the return to school and the fact that 38% of Americans live in areas where ICU occupancy is over 85%.

But there is evidence that the peak is close.

The effective reproduction (R eff) number — which measures the average amount of people an infected person goes on to infect — has fallen below one in some of the first-hit states such as Florida.

Testing positivity numbers have also started to fall.

It is becoming apparent China is continuing to get on top of its Delta outbreak. The number of districts categorised as “mid-risk” have halved from the peak. This is also helping sentiment on global growth.

Covid outlook — Australia

Australia is now reaching vaccination levels equivalent to the peak levels in other countries.

Some models suggest that at the current R eff of 1.34, NSW cases will peak in late September at about 2500 per day.

If restrictions lead to an R eff 0.06 lower, the peak could be below 2000 per day.

As vaccination starts taking effect, case numbers could then drop quickly, back to 300 per day by the start of November, and negligible by December.

2021 Money Management of the Year Awards

Pendal Australian Shares Portfolio

Winner – SMA Australian Equities

Pendal Property Investment Fund

Winner – Australian Property Securities

The same analysis for Victoria implies a peak of 400 cases per day in early October at the current R eff of 1.36.

While modelling of Covid has often proven wrong, this highlights that we may be facing a significant bow wave of new cases in September.

Markets

Powell’s speech helped push all markets higher and increased breadth. Growth and value sectors both rallied last week.

Key commodities bounced from oversold levels. Copper rose 4.4% and iron ore 10.1%. Brent crude was up 11.5% as Kuwait flagged a potential pause on output increases.

The AUD gained 2.5% against the USD.

We saw a recovery among lockdown-affected stocks.

This was partly better macro sentiment, but also resulted from greater context around the near-term risk.

In several instances the market was been reassured by management’s reminders about how quickly demand bounced back after restrictions were lifted.

About Crispin Murray and Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia. Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Find out more about Pendal Focus Australian Share Fund here.

As Portfolio Manager, Lewis co-manages our Australian smaller companies and micro-cap funds and conducts fundamental analysis on a range of smaller companies. Lewis joined the Pendal Smaller Companies team in 2013 as a small cap analyst, before being promoted to the role of Portfolio Manager in 2018. Lewis brings 20 years of industry experience with previous roles spanning equities research at boutique stockbroking firm, Taylor Collison, as well as commercial and investment banking roles at Westpac Bank and Commonwealth Bank. Lewis holds a Bachelor of Commerce (Corporate Finance) from the University of Adelaide.

Significant Feature: The Pendal Active Growth Fund is an actively managed diversified portfolio that invests in Australian and international shares, Australian and international listed property securities, Australian and international fixed interest, cash and alternative investments. The Fund has a significant weighting towards growth assets.

Fund Objective: The Fund aims to provide a return (before fees, costs and taxes) that exceeds the Fund’s benchmark over the medium to long term.

We’re getting ready to live with Covid — and we’re getting ready to spend again, writes Tim Hext in his weekly bond, income and defensive strategies outlook

THIS WEEK New South Wales embarked on a journey to re-opening. The state government announced plans to ease lockdowns as key vaccination hurdles are met.

Australia has started down a path of living with Covid.

Many countries are already in the living-with-Covid phase.

The transition will be bumpy. But three pillars will ensure a sustained recovery: increasing levels of vaccination, strong fiscal support and continued monetary stimulus.

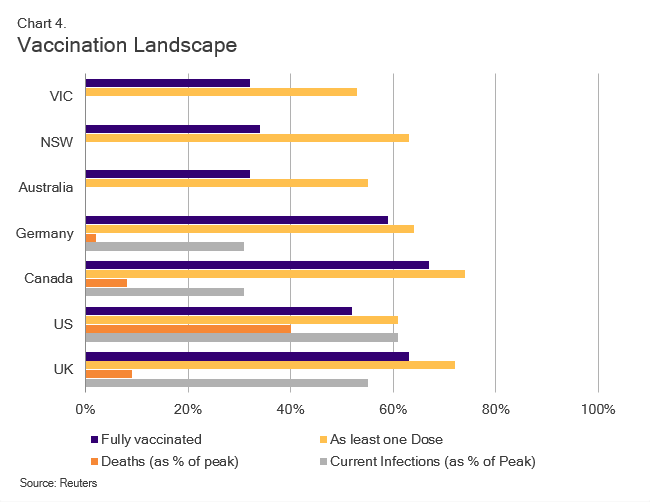

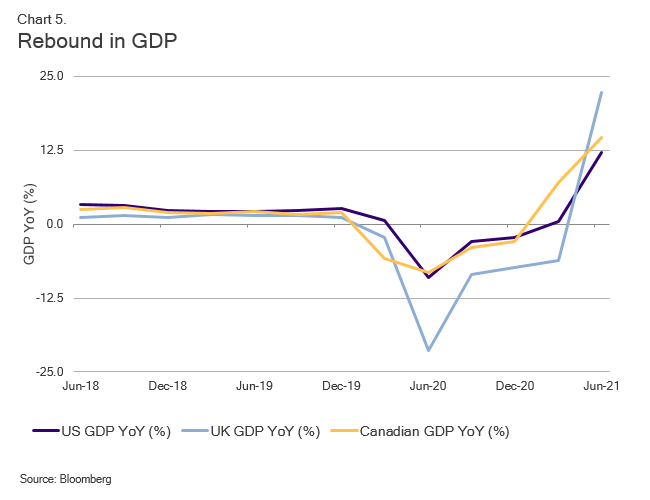

Sharp rebounds in economic activity in the US, UK and Canada paint a picture of what Australia could be like in the near future.

Better health outcomes from higher vaccination rates are allowing greater freedom of movement in those countries.

That gives us hope of returning soon to a level of normality.

Recovery: replaying an old tune

Australia had a strong start to 2021 as the recovery from March 2020 gathered steam.

The economy appears to have done a U-turn after the spread of the Delta strain in June.

Find out about

Pendal’s Income and Fixed Interest funds

Still, the change in circumstances won’t impact the economy as much as it did in March 2020, because measures to support the economy remain in place.

This is a hibernation for many businesses. With savings once again building, lost activity will rebound quickly.

Most of the direct costs of the current lockdowns across the nation are cushioned by state and federal government assistance. That will assist the recovery once lockdown ends, as was observed in the first half of 2021.

Pent-up demand for retail services, travel and recreation, as well as construction activity will rebound sharply once this hibernation ends.

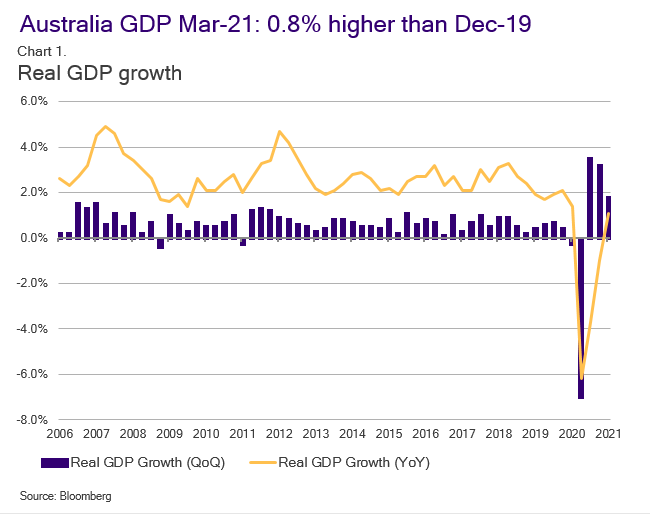

Expect to see similar strong economic data as we did in Q1 2021, a year after the March 2020 Covid impact:

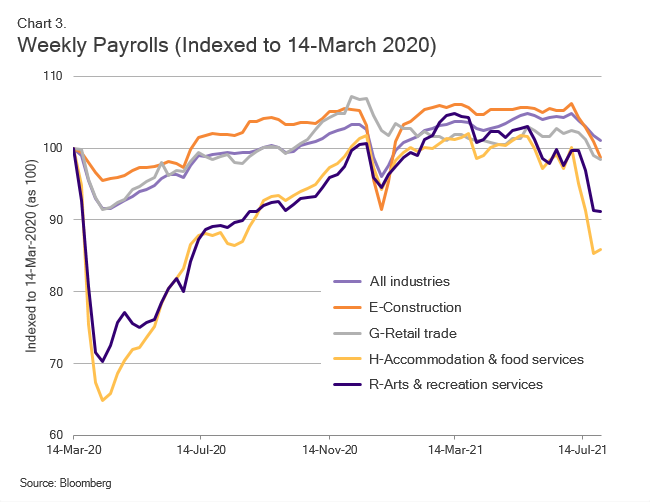

It’s also important to note that current lockdown measures have not had the same level of negative impact on payrolls as they did in March 2020:

Australian consumers are ready to spend for summer. They’re just waiting for the opportunity.

A word of caution

Even as countries such as the US and UK rebound from lockdowns, it is not a complete rosy picture. Infections can still occur, especially among the unvaccinated.

Stark improvements in hospitalisation and death rates for the vaccinated have prompted many industries to mandate jabs for staff:

- The US Pentagon is making vaccination mandatory for all defence troops

- New York’s school board requires all public school employees to be vaccinated

- Delta Airlines has implemented policies with very severe penalties for unvaccinated staff

Concerted efforts to increase vaccination rates and keep the economy open have resulted in strong GDP rebounds in those countries.

This shows high vaccination rates will pave the way forward:

What this means for investors

Our view is the Reserve Bank of Australia will delay any further tapering talk, at least for the rest of 2021.

The RBA has already stopped the Term Funding Facility, capped Yield Curve Control at April 2024 and reduced Quantitative Easing from $5 billion to $4 billion per week from September.

Given current uncertainties they will think they have done enough for now. But they are in glass half-full mode, so they will talk up the rebound.

We think in medium term they will be right — so expect yields higher into 2022.

We continue to expect higher inflation in 2022, so we prefer inflation bonds to nominal bonds for now.

About Tim Hext and Pendal’s Bond, Income and Defensive Strategies (BIDS) boutique

Tim Hext is a portfolio manager with Pendal’s Bond, Income and Defensive Strategies (BIDS) team.

Pendal’s BIDS boutique is one of the most experienced and well-regarded fixed income teams in Australia. In 2020 the team won the Australian Fixed Interest category in the Zenith awards.

With the goal of building the most defensive line of funds in Australia, the team oversees A$22 billion invested across income, composite, pure alpha, global and Australian government strategies.

Find out more about Pendal’s fixed interest strategies here

About Pendal Group

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Significant Features: The Barrow Hanley Concentrated Global Share Fund No. 3 is an actively managed, concentrated portfolio of global shares and is diversified across a broad range of global sharemarkets.

Fund Objectives: The Fund aims to provide a return (before fees, costs and taxes) that exceeds the MSCI World ex Australia (Standard) Index (Net Dividends) in AUD over the medium to long term.

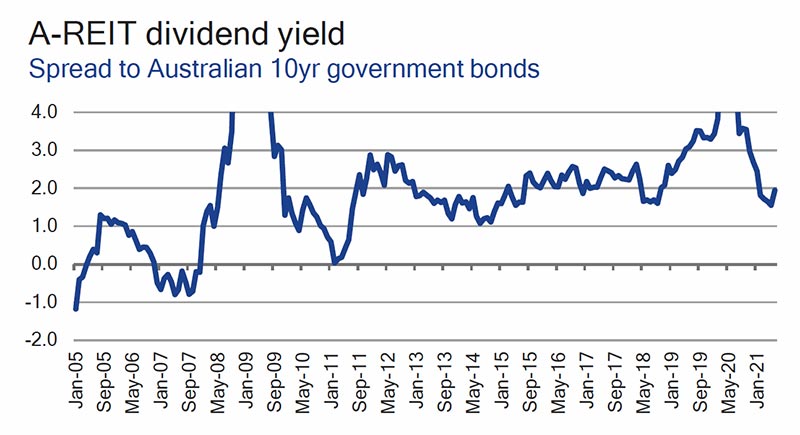

Sustainable investing options aren’t as obvious in property and infrastructure as they are in equities and fixed income. Michael Blayney explains what to look for

INVESTING in property and infrastructure in a sustainable way isn’t always as easy or obvious as buying into equities and fixed income.

Add in structural challenges amplified by the pandemic and it’s clear investors need to do their homework to find opportunities in the world of real assets.

But there are opportunities.

“Long term, inflation-linked cash flows are attractive, albeit with some downside risk due to REITs [Real Estate Investment Trusts] interest rate sensitivity,” says Michael Blayney, head of Pendal’s multi-asset investment team.

“They are also relatively high-yielding assets.”

Similarly, there are opportunities in infrastructure, with long-term, stable returns, particularly from assets that will benefit from the transition to a low-carbon economy.

But sorting through the options can be hard going.

In the property world it’s a challenge finding a benchmark to compare one asset with another.

“In respect of the overall opportunity set of negative exclusions for REITs, any impact is relatively less than general equities,” Blayney says.

“The most obvious exclusions are landlords of hotels or casinos. In Australia, that impacts less than 1 per cent of the A-REIT universe. Globally it can be up to 5 per cent of the universe, depending on how strictly screening criteria are applied.”

Few major portfolio construction issues are caused by explicitly excluding these sub-sectors.

“The bigger issue is the lack of dedicated sustainable product in the AREIT category,” Blayney says.

In the infrastructure world, investors can get access to some of the biggest polluters — such as utilities and assets trying to find climate solutions — and promote the transition to a low-carbon economy.

Find out about

Pendal Multi-Asset Funds

“Typical listed infrastructure portfolios are often exposed to carbon risk, because many assets are inherently linked to the use and distribution of fossil fuels — such as electric and gas utilities, some seaports, pipelines, and also airports,” Blayney says.

“Toll roads are less of an issue than airports, since decarbonising cars is already happening. But large-scale decarbonised air travel is not yet a reality.

“Digital infrastructure, such as data centres, are somewhat of a conundrum.

“On one hand greater uptake of technology can act to reduce emissions via less commuting and less business travel. On the other hand datacentres can have a significant carbon footprint due to high levels of energy consumption.

“Other assets in the digital infrastructure category — such as fibre and towers — can also make a positive contribution to decarbonisation via reduced commuting and business travel, and enabling a portfolio to leverage itself for growth in the digital economy,” Blayney says.

“Finally, within infrastructure allocations, investors have an opportunity to support clean-energy technologies while earning a strong risk-adjusted return.

“Examples include investing in renewable energy generation, in large-scale battery storage technology, and in better waste management,” he says.

How much portfolio construction in property and alternatives is influenced by ESG factors or sustainability considerations depends much more on implementation — and the subjective views of the portfolio manager making the investment decisions — rather than the hard screening of the assets themselves, says Blayney.

About Pendal’s multi-asset capabilities

Pendal’s diversified funds provide investors with a variety of traditional and alternative asset classes and strategies.

These include Australian and international shares, property securities, fixed interest, cash investments and alternatives.

In March 2024, Perpetual Group brought together the Pendal and Perpetual multi-asset teams under the leadership of Michael O’Dea.

The newly expanded nine-strong team will manage more than $6 billion in AUM and create a platform with the scale and resources to deliver leading multi-asset solutions for clients.

Michael is a highly experienced investor with more than 23 years industry experience, including almost a decade leading the team at Perpetual.