With a background in cash and dealing, Steve brings over 20 years’ financial markets experience to our Institutional Managed Cash portfolio. During his time at Pendal Group, Steve has managed numerous New Zealand cash portfolios and has been active in portfolio positioning while executing domestic and international credit and bond funds. Steve previously worked at Tullett and Tokyo as a corporate bond broker, and holds a Bachelor’s degree in Commerce from the Australian National University.

Significant Features: The Pendal Active Long Volatility Fund is managed to generate excess returns from exposure to rising volatility across selected currency, equity and commodity markets. The strategy employs a long volatility approach to achieve this outcome.

Fund Objective: The Fund aims to provide a return (before fees, costs and taxes) that exceeds the RBA Cash Rate by 4-6% per annum over the medium to long term.

Here’s what’s driving Australian equities this week according to Pendal’s head of equities Crispin Murray. Reported by portfolio specialist Chris Adams.

THE FIRST week of reporting season was largely positive, helping Australian equities outperform other markets.

At this point there seems to be surprisingly low levels of concern about the impact of local lockdowns. The S&P/ASX 300 gained 1.33% last week and the S&P 500 was up 0.75%.

Things were quiet on the macro front. US inflation data was strong — but in line with expectations. The focus remains on Delta and the potential implications for economic growth.

Bond yields were stable and there was a small rotation away from growth stocks.

COVID outlook for Australia

The market is grappling with two aspects of the domestic Covid outbreak.

First, the risk that Melbourne also lapses into extended lockdown. This would mean effectively half the nation’s economy was affected by restrictions.

The second issue is speculation on the timing of an easing in restrictions, which is related to vaccine penetration.

Vaccination rates continue to rise — up from 0.74% of the population per day last week to 0.87% now.

NSW is running at more than 1% daily. We could see the rest of the nation reach this point in September as greater supply becomes available. This would be in line with the peak rates of vaccination in other regions.

Simple extrapolation of 1% daily gets us to 70% of the population vaccinated in the first week of October and 80% two weeks later.

The impact of restrictions — combined with the effect vaccinations have on transmission — suggests we could see a reasonable degree of re-opening in October or November.

The question is whether governments will be willing to tolerate a material number of Covid cases, assuming hospital systems are able to handle the pressure.

The link between vaccinations and lower severity of Delta cases — and hence less pressure on medical systems — remains evident in the UK and Israel.

The degree of hospitalisations in these countries equates to 2000 to 2600 hospital patients in Australia, compared to the sub-400 level we see here now. This highlights the policy dilemma we face.

Covid outlook for the US

In the US case numbers and hospitalisations continue to rise.

This reflects a disparity on vaccination rates among the States since fewer than 2% of admissions are fully vaccinated. It also reflects a less systematic approach to protecting vulnerable Americans.

The question is whether the US will follow the Indian and UK path. If so, cases should peak in the next two to three weeks.

This is important given the pressure building on hospital capacity. About a quarter of Americans live in areas where ICU occupancy is running higher than 85%.

Covid outlook for China

The situation in China appears to be stabilising. Seventeen provinces have reported outbreaks — the same as last week — and reported cases are falling.

However the hard measures used to clamp down on the outbreak have come at an economic cost.

Find out about

Pendal Focus

Australian Share Fund

Crispin Murray,

Head of Equities

The Chinese port of Ningbo-Zhoushan — the world’s biggest by bulk commodity volume — has been largely closed since August 11. Containers are now re-routed through Shanghai, creating greater global supply chain delays. (Ningbo-Zhoushan is the world’s third-busiest container port).

Beijing’s policy response will be important to watch.

Short-term measures include permit renewals for coal mines and extra steel capacity. Priority is placed on supporting activity and economic growth even though the tools are at odds with longer-term policy objectives of more balanced and greener growth.

Economic outlook

There are clear signs that Delta is starting to weigh on business and consumer confidence in the US. Surveys on both measures have turned down recently.

The US CPI print showed year-on-year inflation remains above 5%. While high, this is the first time it did not exceed consensus expectations in recent months.

This signals that some drivers of recent inflation — such as used auto prices — are starting to recede.

On the other hand areas such as shelter — which may drive more persistent inflation — are starting to pick up.

Market highlights

Concerns over slowing economic growth are reflected in bond yields (which remain well supported) and softness in commodities.

There was an unusual “flash crash” in gold last Monday, when a large seller hit the market during an illiquid Asian time zone. Gold fell 4% before bouncing off the US$1680/ounce support level. This reinforces current scepticism in the metal.

Australian equities outperformed global indices last week after a decent start to reporting season.

Broadly, we are seeing better earnings and higher distributions than expected. Most importantly, a lack of excessive caution among companies regarding the current economic outlook and lockdowns is reassuring the market.

Gold stocks were generally weak following price volatility. Northern Star (NST, -6.5%) was the worst performer in the S&P/ASX 300. Evolution (EVN) was down 4.9%.

REA Group (REA, -6.1%) delivered a reasonable result, though the market focused on management’s note that Sydney listings were down 22% in July due to lockdowns. The fact that lockdowns saw 40-50% falls in Melbourne listings last year shows the industry is getting better at managing this issue.

REAemphasised how quickly the market has consistently bounced back from previous lockdowns. The property website has a number of longer-term growth opportunities, including data and insight services as well offshore ventures in India and the US.

Transurban’s (TCL, -5.8%) revelation of a $3.3 billion cost blow-out on Melbourne’s West Gate project — off an initial cost base of $6.7 billion — disappointed the market. The toll road operator conceded it would have to bear some of the pain in covering these costs to achieve some resolution on the issue. This was despite claiming that the blame lies with the government and contractor.

The market is also wary about the impact of lockdowns on traffic volumes, though this has little impact on longer-term valuation. TCL may need to raise capital if it successfully buys out the remainder of the Westconnex project.

QBE (QBE, +12.1%) was the best performer on the ASX 100 last week. It delivered its first well-received result for some time. Insurance premium growth is driving strong revenue momentum. Costs remain under control, supporting an earnings recovery. QBE is attractively valued in this light — well below historical relative valuations — which helped drive a strong stock price response.

Elsewhere in insurance we saw results from Suncorp (SUN, +8.4%) and IAG (IAG, +8.8%). SUN is enjoying revenue momentum and flagged a constructive outlook for insurance margins. This is allowing strong capital return, with a payout ratio at the top end of expectations, a special dividend and a market buyback.

IAG’s result was less compelling, having pre-announced. It is demonstrating lower revenue growth and less clear cut margin improvement than peers. Nevertheless, the stock reaction reflects more confidence in the insurance sector.

Downer’s (DOW, +12%) result was good. Free cash flow was strong and the company is buying back stock. Markets fears around wage pressure and the impact of lockdowns largely failed to materialise. DOW has successfully shifted from a capital-intensive model with unpredictable earnings and a large exposure to mining service contracts, to a more predictable urban services business with lower capital intensity. We expect this to improve the valuation rating over time.

2021 Money Management of the Year Awards

Pendal Australian Shares Portfolio

Winner – SMA Australian Equities

Pendal Property Investment Fund

Winner – Australian Property Securities

James Hardie’s (JHX, +6.2%) result for 1Q FY22 demonstrated how a strong, well-managed franchise operating with cyclical tailwinds can deliver more operational leverage than the market expects.

The combination of a supportive cycle, higher pricing, more favourable product mix and gains in market share saw JHX grow revenue 21% versus the same quarter in FY19. Management guided to 20% revenue growth for the full financial year.

The longer term outlook is positive. There is an emphasis on gaining share in the home remodelling market in regions such as the north-east US, where JHX has not previously done as well.

Telstra (TLS, +4.2%) was largely in-line with expectations. The Network Applications and Solutions (NAS) division slightly disappointed. But the clear message was the rebasing of earnings as a result of NBN was over and earnings were now growing.

Mobile is key. It grew 18% in the second half, with average revenues per user increasing. This should continue to flow through, as will more cost-out. Further detail is expected in a September Investor Day. The dividend looks underpinned and may grow. TLS is returning some proceeds of their asset sales via buy-back.

Elsewhere Commonwealth Bank (CBA, +0.3%) beat the market’s earnings expectations, largely due to lower provisioning for bad debts. It is performing better than the other big banks in terms of loan growth, particularly in the small business sector.

Overall this did not translate into much growth in revenue or pre-provision profits due to margins and higher costs as the company invested in its digital shift. Whether this is an opportunity to differentiate itself from the other banks, or more a defensive move in response to competition from other payers, is key area of debate.

CBA’s outlook for margins was subdued, which weighed on the stock. On the plus side, it announced a $6 billion buy-back and flagged no significant concerns from current lockdowns. CBA remains on a punchy valuation despite limited growth opportunities. We continue to prefer other names in the financials space.

National Australia Bank (NAB, +3.8%) provided a quarterly update. There was little new information, but cash earnings were running higher than market expected and margins remained stable. Costs and impairments were both a bit lower than expected.

Goodman Group (GMG, -3.1%) grew EPS 14%, but disappointed a market which was looking for an upgrade to FY22’s guidance of 10% earnings growth. It continues to do well operationally and the development pipeline is strong as are assets under management.

A fall in cap rates has revalued their portfolio upwards. This means an upgrade may only be a matter of time. However a valuation over 30x P/E is factoring in a lot of good news.

Finally, AGL (AGL, +0.3%) reminded the market of the challenges it faces, with earnings guidance for FY22 coming in 15% lower than market expectations. The big issue is the company’s path out of trouble, given earnings declines and excess debt.

A demerger remains planned, but it is clear the company is under-capitalised given the pressure on earnings and remediation costs of future plant closures. Ultimately this will need some form of policy from the government to help underwrite the outlook, but we have no certainty this will occur.

About Crispin Murray and Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia. Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Find out more about Pendal Focus Australian Share Fund here.

A monthly insight from James Syme and Paul Wimborne (pictured), managers of Pendal’s Global Emerging Markets Opportunities Fund

- As vaccination rates increase we’re starting to see what a post-Covid world will look like

- Suggestions of a ‘new-normal’ are often wrong, but some recent trends will endure

- Find out about Pendal Global Emerging Markets Opportunities Fund

As US author William Gibson said: “the future is already here — it’s just not very evenly distributed.”

From an investing viewpoint, the big change in developed and emerging economies is the shift in fiscal and monetary policies.

Support to economies and financial systems after the 2008 crisis was at the time shockingly large. But it has been dwarfed by the stimulus response in 2020-21.

JP Morgan estimates the balance sheets of central banks in developed economies will increase by US$11.7 trillion in 2020-21. The aggregate size will be US$28 trillion by the end of this year.

In most of these countries central banks are the biggest single buyer of government bonds due to those economic support programs as well as vastly-expanded healthcare systems.

As economies recover, policy focus is turning to ending quantitative easing and tightening policy. But this is deliberately slow.

The stimulus will sit on government and central bank balance sheets for years to come, but the tapering is carried out with an eye on allowing inflation to run at higher levels.

This tolerance of inflation should be a net positive for nominal GDP growth around the world and also for commodity prices.

This should create a different, more positive, economic environment for more indebted and more commodity-intensive emerging economies.

The enduring ‘new normal’

We have seen signs of shifts in some industries in Emerging Markets.

Suggestions of a “new normal” are often proved wrong, but some recent trends may endure.

The move to an online, digital and e-commerce-based world is a long-term trend, but that trend has accelerated markedly in the last 18 months. Most companies that have benefited expect to keep their new customers.

We have various exposures to this theme in the portfolio, particularly food delivery and online games.

Another shift likely to endure is the shift in travel and tourism patterns.

International travel has collapsed, but so, noticeably, has business travel.

This has been partly replaced — particularly in big countries such as Brazil and China — by very strong growth in internal travel and tourism, including high-end travellers who would previously have gone abroad. Wide-body jets normally used for international long-haul flights are now servicing internal tourist routes.

There has also been a strong rise in dedicated freight flights as cargo capacity in passenger flights declines and e-commerce volumes ramp up.

Also, online bookings continue to replace brick-and-mortar travel agents. We have exposure to all these trends in the portfolio.

Covid drives political change

Covid has driven changes in the stability or direction of politics in several countries.

Some governments have overseen weak or chaotic responses to the pandemic. In places where infection rates and death tolls have been high, it’s been difficult or impossible to govern.

The main incidence of this has been in Latin America, where the human impact of Covid has been worst.

We wrote in June about the challenging political environment in smaller countries of the region. The human and economic impacts of the pandemic have been major drivers of the swing towards populism or socialism in Chile, Peru and Colombia.

A combination of Covid-driven lockdowns and poverty have led to the worst unrest in South Africa in more than 20 years (though it’s yet to coalesce into a coherent political movement).

Where populists are in power, the pandemic has been a major challenge to incumbents’ popularity.

We see this starkly in Brazil, where opinion polling on the Bolsonaro presidency has largely tracked Covid case data.

Find out about

Pendal Global Emerging Markets Opportunities Fund

In Turkey, economic stress is elevated because of policy mistakes as well as the impact of Covid. But the effect is that the governing Justice and Development Party (AKP) and President Erdogan are closer to losing power than at any time since the AKP came into power in 2003.

Governments claiming to operate on a more technocratic basis (sometimes using this as an excuse for holding to weaker democratic values) have not been immune.

In Malaysia the governing Bersatu party lost its coalition partner and was (at the time of writing) using the pandemic-driven suspension of parliament as a tool to cling to power.

So far only the smaller Latin American countries are showing evidence of permanent change as a result of Covid. But there will be many electoral cycles in emerging markets in the next few years.

The pandemic may well prove a decisive factor in next year’s elections in Brazil, Colombia and the Philippines.

Some of these changes may not prove lasting, and doubtless others will appear. But it is definitely the case that the post-Covid world will differ from what came before.

Investors need to factor in those risks and opportunities.

About Pendal Global Emerging Markets Opportunities Fund

James Syme and Paul Wimborne are senior portfolio managers and co-managers of Pendal’s Global Emerging Markets Opportunities Fund.

The fund aims to add value through a combination of country allocation and individual stock selection.

The country allocation process is based on analysis of a country’s economic growth, monetary policy, market liquidity, currency, governance/politics and equity market valuation.

The stock selection process focuses on buying quality growth stocks at attractive valuations.

Find out more about Pendal Global Emerging Markets Opportunities Fund here.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

As State-based Covid strategies diverge we’re looking less and less like a federation. What does this mean for investors? Tim Hext explains in his weekly bond, income and defensive strategies note

IT’S been a rough ride for our federation during Covid.

Closed state borders, sniping among premiers and an us-versus-them mentality have overcome these usually united shores.

In normal times, State of Origin rugby league and the old Melbourne v Sydney debate (which I always think of as an “inside life” versus “outside life” debate) are fodder for mild banter.

But as State-based Covid strategies diverge, we seem less and less likely to be singing together: “I am, you are, we are Australian”.

NSW is going down the international route of learning to live with Covid. Other states are — to put it mildly — quite upset. National Cabinet today should be fiery.

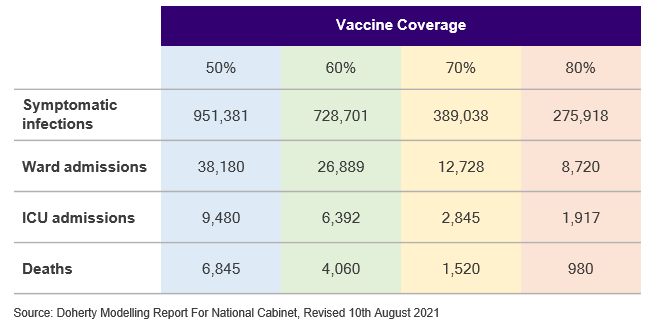

Modelling by the Doherty Institute, updated this week, suggests an “all adults” vaccination allocation strategy (rather than “older first”) looks like this table below.

“All adults” vaccination allocation strategy:

I will leave you to consider what are “acceptable” rates of infection, hospitalisations and deaths over a six-month period.

But it is the uneviable task of a politician to balance these outcomes with the economic and human welfare benefits of reopening.

For now NSW is on its own with incoming fire.

Other states, largely successful in curbing big breakouts of the Delta variant, remain committed to a suppression strategy for now.

Isolated states such as WA and Tasmania seem confident, while Victoria and Queensland are understandably nervous.

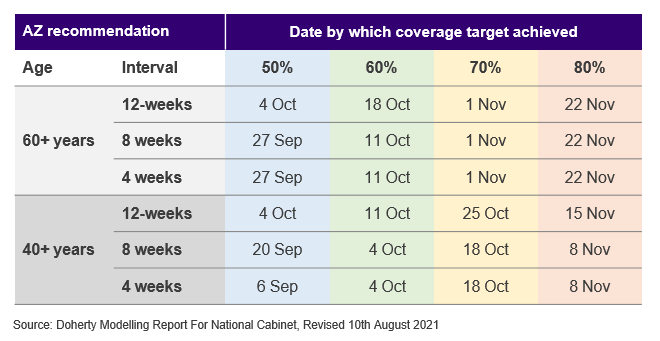

When would we hit these vaccination levels? The Doherty report shows this table below from a month ago. Hopefully recent efforts will see these dates brought forward.

Estimated completion dates for different vaccination rollout strategies (based on progress at July 12):

Welfare as a state responsibility

All this would matter less if welfare was a state responsibility.

Each state could go its own route — with even harder border closures — and reap the associated benefits and costs.

But we are a federation. Canberra controls money printing, social security and interntional borders.

It is likely to get very messy, very soon — further complicated by an upcoming election (latest 2022) where Queensland seats will likely determine the result. Good luck ScoMo!

The outlook

From a market point of view data and outcomes are moving every day, but few expect a full national opening before November or even December.

International border openings are now pushed back well into 2022.

Find out about

Pendal’s Income and Fixed Interest funds

We maintain the view that 2022 will bring a pick-up in wages and services inflation and the RBA will be tightening by 2023.

For risk markets, though, it will be more tailwinds. Inflation is unlikely to reach the kind of levels that tip market psychology into fear.

That level would be persistent inflation above 4%. For risk markets inflation at 2.5% and growth at 3% is almost the perfect mix — and likely to happen medium term.

Whether it’s plain sailing on the way is debatable. Uncertainty remains high but markets for now are alert not alarmed.

About Tim Hext and Pendal’s Bond, Income and Defensive Strategies (BIDS) boutique

Tim Hext is a portfolio manager with Pendal’s Bond, Income and Defensive Strategies (BIDS) team.

Pendal’s BIDS boutique is one of the most experienced and well-regarded fixed income teams in Australia. In 2020 the team won the Australian Fixed Interest category in the Zenith awards.

With the goal of building the most defensive line of funds in Australia, the team oversees A$22 billion invested across income, composite, pure alpha, global and Australian government strategies.

Find out more about Pendal’s fixed interest strategies here

About Pendal Group

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Tim joined Pendal Group in February 2017 with responsibility for managing Australian Bond portfolios. Tim has extensive experience in banking, financial markets and funding.

Tim joined Pendal Group from NSW Treasury Corporation (TCorp), where he was General Manager, Funding and Balance Sheet, with responsibility for defining and executing TCorp’s funding programme and strategy. Tim’s prior experience includes senior positions in Westpac Treasury, Commonwealth Bank of Australia, Deutsche Bank, Bain & Co and Swiss Bank Corporation.

Tim holds a Masters of Economics of Development from the Australian National University and a Bachelor of Commerce from the University of New South Wales.

Companies are increasingly disclosing their exposure to climate risks. But those disclosures often do not give the investors the full picture. Regnan’s ALISON EWINGS explains

- Climate disclosures too narrow

- System-wide effects of climate change often ignored

- Find out about Regnan Global Equity Impact Solutions Fund

- Find out about Regnan Credit Impact Trust

IT’S been five years since the Task Force on Climate-related Financial Disclosures began trialling voluntary, consistent climate-related financial risk disclosures for use by companies.

While take-up has been good, investors still need to see a lot of improvement in ESG-related disclosures, says Alison Ewings, who engages with ASX-listed companies for sustainable leader Regnan.

About 80 per cent of big global companies now disclosed in line with at least one of the taskforce’s 11 recommendations.

But most companies are still taking too narrow a view of climate risks and failing to consider the underlying, system-wide interdependencies and economics risks of climate change that will impact their operations, says Ewings.

A Regnan assessment of disclosures shows they are often narrow in scope and place climate transition risks ahead of considering system-wide interdependencies and different potential economic scenarios.

Regnan is a leader in sustainable investing and an affiliate of Pendal.

“Look at what’s happened in Australia lately — fire, fire, flood, flood, flood — everyone who’s dependent on the Australian economy has been affected by those things,” says Ewings.

“But when you look at an individual company you see ‘well we’re fine’. But you’re not fine. You’re not an island. You’re part of the broader economy.

“We think about this as an additional risk that climate change is going to add for every business.

“Some businesses are more leveraged to economic activity than others, so they’re more exposed, but they’re all exposed to some extent.

“So instead of saying there’s no climate risk, internally we talk about it as there being a background level of risk that is not nil.

“This is something that’s not being explicitly considered by companies in their TCFD disclosures and we’re not sure that it’s really being explicitly considered by investors, insurers and banks.”

Five underlying climate risks for investors

Ewings says underlying climate risk can take five main forms.

Pendal Sustainable Australian Fixed Interest Fund

An Aussie bond fund that aims to outperform its benchmark while targeting environmental and social outcomes via a portion of its holdings.

First, general consumer behaviour will likely change as temperatures rise and extreme weather events become more common.

This could include changing preferences for food, clothing and holiday destinations, to the need to rebuild after natural disasters or even relocate for more favourable climatic conditions.

Second, businesses are all reliant in some way on the underlying infrastructure around them, from roads, telecommunications and power to access to water. Changes to the availability of infrastructure can have profound implications for a business’s operations.

Third, disruptions in supply chains due to extreme weather, shifting demand or interrupted transportation.

Fourth, businesses rely on the resilience of the communities they operate in to maintain their workforce and customer base.

Assessing the health of the community should form part of a business’s risk assessment.

Find out about

Regnan Global Equity Impact Solutions Fund

And finally, with extreme weather no longer an infrequent, temporary phenomenon, overall economic growth is likely to be lower.

Businesses should reflect this base level reduction in demand in their planning.

“The key thing is the interdependency,” says Ewings.

“Once you get outside of your organisational boundary, that’s where things start to fall apart.

“For instance, companies do a good job of site-by-site analysis of the impacts of climate change to physical locations.

“But it is very rare to see consideration of the infrastructure on which they also rely on like the transport networks that move things to and from those sites.

“It’s rare to see anything about the resilience of the communities in which their employees work — it might well be that your factory is fine, but nobody can get there or nobody’s feeling like coming to work.

“All of these factors should be considered.”

Find out about

Pendal Horizon Sustainable Australian Share Fund

About Regnan

Regnan is a responsible investment leader with a long and proud history of providing insight and advice to investors with an interest in long-term, broad-based or values-aligned performance.

Building on that expertise, in 2019 Regnan expanded into responsible investment funds management, backed by the considerable resources of Pendal Group.

The Regnan Global Equity Impact Solutions Fund invests in mission-driven companies we believe are well placed to solve the world’s biggest problems.

The Regnan Credit Impact Trust (available in Australia only) invests in cash, fixed and floating rate securities where the proceeds create positive environmental and social change. Both funds are distributed by Pendal in Australia.

Find out about Regnan Global Equity Impact Solutions Fund

Find out about Regnan Credit Impact Trust

For more information on these and other responsible investing strategies, contact Head of Regnan and Responsible Investment Distribution Jeremy Dean at jeremy.dean@regnan.com.

Sustainable investing leader Regnan is exploring new approaches to ESG engagement. Regnan’s ALISON EWINGS explains

- Systems-wide engagement is needed to drive change

- Download Regnan’s 2022 Australian engagement report, From stock to system (PDF)

- Find out about Regnan Global Equity Impact Solutions Fund

- Find out about Regnan Credit Impact Trust

THESE days it’s a basic expectation that active managers will meet regularly with investee companies and issuers to drive behaviour that benefits shareholders and the community.

“Engagement”, as it’s known in the investment industry, is usually undertaken on a one-to-one basis between an investor and an investee.

For example, sustainable leader Regnan last year engaged with 40 ASX-listed companies – some on multiple occasions – as part of its Australian program. Engagements aimed to reduce economic, social and environmental risk to client portfolios.

Regnan’s 2022 engagement report From Stock to System (PDF) shows demonstrated progress in 98 per cent of engagements.

But as interest in ESG snowballs — and the complexity of issues increases — engagement must evolve to ensure continued effectiveness, says Regnan’s head of engagement Alison Ewings.

Engagement can be more successful — particularly on portfolio-wide risks — if it shifts away from a company-by-company approach and evolves into collaborative, systems-wide activity, says Ewings.

Evolution of engagement

Regnan’s latest report sets out the changing nature of engagement amid worsening greenhouse gas emissions, rising inequality and repeated examples of poor corporate practice.

It’s becoming clear that we need to look beyond closed-door, direct engagement with directors and company leaders to truly tackle these systemic risks, says Ewings.

Sustainable and

Responsible Investments

Fund Manager of the Year

“Historically, we’ve engaged in a very bottom-up fashion, looking at the ESG risks to an individual company.

“While there is still a role for this kind of engagement, we must acknowledge that individual companies are limited in the actions they can take on some ESG issues.

“For these multifaceted, system-wide issues, one-to-one engagement will not be enough to reduce the risks to portfolios.

“Climate change is a classic example.

“You can divest your way out of the risks to a certain point. But if climate change is left unchecked, it will still create risk in portfolios and the potential for associated economic shocks.”

New models for engagement

As a result, Regnan is making changes to its activities and investigating new models for engagement.

“We are approaching engagement in two ways.

“One is to engage right along the value chain to achieve system change and reduce portfolio risks from major ESG trends.

“The other is to look at opportunities to bring companies together to address these issues.”

Adviser Natalee is invested

in making our world

A better place.

Natalee shows us how

investment in affordable

housing changed a

woman’s life

Ewings points to Regnan’s establishment of a roundtable on sustainable agriculture , which brings together senior executives and directors to identify barriers to shifting to more sustainable agricultural and food production practices.

“The full impact is still unknown but it’s proving an effective way of raising awareness and developing a deeper understanding of these issues among market participants,” she says.

Progress on diversity, equity and inclusion

Regnan also had success during the year with its work on diversity, equity and inclusion, including a research paper that explored why companies struggle to make meaningful progress on diversity.

“We looked at how organisations can achieve their diversity goals in a meaningful way — both for individuals and for organisational value creation,” says Ewings.

Regnan’s research found that diversity strategies must include a conscious focus on inclusion and equity to reap the upside of a diverse workforce.

Other engagements during the year focused on issues ranging from the financial service sector’s exposure to carbon emissions, the physical risks of climate change and how companies can reduce the risk of exposure to modern slavery.

“These are significant changes to the way that we undertake our engagement activities,” says Ewings.

“Our ability to make positive change by engaging with single actors is becoming limited as the issues become more complex.

“We have to be actively exploring new models for engagement to address these system-wide challenges.”

A more intentionally inclusive approach to problem solving also enhances the pool of ideas for how to tackle major societal challenges, she says.

About Regnan

Regnan is a responsible investment leader with a long and proud history of providing insight and advice to investors with an interest in long-term, broad-based or values-aligned performance.

Building on that expertise, in 2019 Regnan expanded into responsible investment funds management, backed by the considerable resources of Pendal Group.

The Regnan Global Equity Impact Solutions Fund invests in mission-driven companies we believe are well placed to solve the world’s biggest problems.

The Regnan Credit Impact Trust (available in Australia only) invests in cash, fixed and floating rate securities where the proceeds create positive environmental and social change. Both funds are distributed by Pendal in Australia.

Find out about Regnan Global Equity Impact Solutions Fund

Find out about Regnan Credit Impact Trust

For more information on these and other responsible investing strategies, contact Head of Regnan and Responsible Investment Distribution Jeremy Dean at jeremy.dean@regnan.com.