Russell Turner is a Portfolio Manager in the Multi-Asset team for Perpetual Asset Management Australia. In this role, he assists the ongoing development of macro-economic modelling, the evolution of dynamic asset allocation process and undertakes manager research.

Russell joined Perpetual Asset Management Australia in July 2015, having previously worked as the Business Manager to Geoff Lloyd, Perpetual’s CEO. Prior to this, he was a Graduate in Perpetual Private.

Russell has a Bachelor of Laws, Bachelor of Science, majoring in Applied Mathematics and a Master of Commerce, majoring in Applied Finance and is a Chartered Financial Analyst.

BUSINESSES often promote workplace diversity to investors as a key performance driver. But a new report from responsible investing leader Regnan finds diversity strategies mean little without equity and inclusion.

- New research report analyses diversity, equity and inclusion as indicators of company performance

- Diversity programs won’t improve business performance without equity and inclusion

- The report offers a blueprint for Diversity, Equity and Inclusion (DEI) programs that deliver both social equity and business performance.

- Download: Beyond Diversity: Equity and inclusion as an overlooked opportunity for investors

NEW RESEARCH from responsible investing leader Regnan suggests investors should be asking tougher questions about diversity practices among listed companies.

Diversity has long been promoted by responsible investors as a way to contribute to creating just societies as well as improving business performance.

But the Beyond Diversity report from Regnan’s Insight and Advisory Centre suggests diversity programs can fail to deliver unless companies place equal importance on equity and inclusion.

The work suggests investors should reconsider the indicators they use to evaluate company performance when it comes to Diversity, Equity and Inclusion (DEI) practices.

What are Diversity, Equity and Inclusion?

Diversity: the representation of different kinds of people

Equity: fair arrangements that enable all people to access opportunities

Inclusion: workplace conditions that enable all individuals to make their fullest contributions at work

It’s more likely that equity and inclusion are the factors driving business outperformance, concludes Regnan.

“This finding suggests that investors need to reconsider how they evaluate and engage with companies, increasing their focus on equity and inclusion,” says Regnan co-author and Head of Engagement, Alison Ewings.

The report, Beyond diversity: equity and inclusion as an overlooked opportunity for investors, is based on wide-ranging analysis of the academic literature on diversity, equity and inclusion, as well as interviews with practioners and a review of leading organisations.

The work has identified organisational conditions critical to boosting both diversity and business performance and provides a framework by which they may be considered.

For example a study by Deloitte found that “inclusive” companies were 3.6 times better at dealing with performance issues.

Inclusion framework

The conventional wisdom in responsible investing is that diversity is a driver of performance and, as a result, investors can focus purely on measures of an organisation’s diversity when evaluating investments.

Regnan offers a new framework for judging equity and inclusion, drawing on research by Cornell University’s Lisa Nishii.

The framework highlights three essential pre-requisites for effective DEI:

- Equitable employment practices: eliminating bias at all stages of the employee lifecycle through recruitment, retention and progression.

- Supportive culture: ensuring that employees can make their fullest contributions at work, without fear of negative consequences.

- De-biased decision-making: focusing on the ability of the organisation to elicit, understand and adapt itself to feedback from its people.

The report then offers a blueprint for how this approach can be best implemented.

“Organisations can self-assess against these pre-requisite conditions to identify potential areas of strength or weakness in their current approach,” says Ewings.

“Further, there is an opportunity for investors to consider the presence of these factors as an indicator of the likely contribution of the DEI efforts to the improved performance of investee companies.”

Download Regnan’s Beyond Diversity: Equity and inclusion as an overlooked opportunity for investors

About Regnan

Regnan is a responsible investment leader with a long and proud history of providing insight and advice to investors with an interest in long-term, broad-based or values-aligned performance.

Building on that expertise, in 2019 Regnan expanded into responsible investment funds management, backed by the considerable resources of Pendal Group.

Regnan Global Equity Impact Solutions Fund invests in mission-driven companies we believe are well placed to solve the world’s biggest problems.

Regnan Credit Impact Trust (available in Australia only) invests in cash, fixed and floating rate securities where the proceeds create positive environmental and social change.

Both funds are distributed by Pendal in Australia.

Find out about Regnan Global Equity Impact Solutions Fund

Find out about Regnan Credit Impact Trust

For more information on these and other responsible investing strategies, contact Head of Regnan and Responsible Investment Distribution Jeremy Dean at jeremy.dean@regnan.com.

Rema Elias is an Investment Analyst in the Multi-Asset team for Perpetual Asset Management Australia. In this role, she will assist with the portfolio management of smart beta portfolios and the implementation of tactical asset allocation positions.

Rema joined Perpetual Asset Management Australia in July 2014, having previously managed the Performance and Analytics team at BNP Paribas. Prior to this, she was a Senior Performance Analyst at RBC Investor and Treasury Services.

Rema has a Bachelor in Mathematics and Finance.

- Actively managing credit macro risks is critical

- Inflation and vaccine roll-out are focus areas

- Bulls outweigh the bears – but for how long?

ONE OF THE greatest challenges running any portfolio is when to de-risk. When should a manager decide to change tack and become more defensive?

It’s the same for all asset classes, including credit markets which are often thought of as “low risk”.

In fact, losses in credit markets do occur — and can be very painful for investors — which means the right risk profile is even more critical in fixed income funds trying to achieve target returns.

“If you have a credit portfolio that’s trying to outperform by 2% versus a benchmark over a full year, and you lose 1% in a month, that’s a very bad outcome,” says George Bishay, Pendal’s portfolio manager of Income and Fixed Interest.

Bishay uses the example of March last year when financial markets collapsed. An average credit fund aims to outperform the benchmark by 2% over a year — but many lost 4% in one month.

Risk, and the appetite of a credit fund manager for risk, is reflected in the weighted average maturity (WAM) of their portfolio. A longer WAM is reflective of a bullish credit outlook. A shorter WAM suggests a bearish outlook.

When actively managing a credit fund, it’s important to be more defensive during volatile times, such as March last year.

Right now, credit spreads offer value in a low interest rate environment and Bishay has reflected this in his credit portfolios.

“It comes down to macro factors,” he says. “The huge amount of fiscal stimulus that we’ve had is powerful. That stimulus supports employment and ensures the economy doesn’t fall in a heap.”

“Then there’s an incredible amount of monetary policy stimulus that supports liquidity in the system. The cash rates around the world are near zero and because of that investors are chasing yield, which is supportive for credit markets,” Bishay says.

“You also have global company earnings being revised up.”

US corporate earnings, and what happens on Wall Street, has a big influence on local credit market pricing. The local credit market is correlated with US credit markets. And US credit markets reflect what’s happening in US equity markets.

A rally in US equities tends to prompt a rally in US and AUD credit spreads.

Find out about

Pendal’s Income and Fixed Interest funds

“I’m focused on US equities,” Bishay says.

While the roll-out of vaccinations around the world adds to his argument for accepting greater risk in credit markets, it could quickly become a negative.

“COVID cases are picking up globally, but so are vaccination rates. We know if you get vaccinated you are less likely to transmit coronavirus and less likley to end up in hospital or die. But we don’t know the exact numbers,” Bishay explains. “We don’t really know the accuracy of the trial efficacy rates of vaccines. We don’t yet have the full picture.”

“The vaccination roll-out supports the stronger macro view, but it is also a risk.”

Bishay says the other major risk is a disorderly rise in interest rates. “What if there’s a jump in interest rates because inflation proves not to be transitory and is higher than expected? That’s a risk.”

But for now, the bull case over-rides the bear case. But as Bishay puts is: “I’m constantly focused on when to de-risk the portfolio.”

About George Bishay and Pendal

George Bishay is a portfolio manager with Pendal’s Bond, Income and Defensive Strategies team.

Led by Vimal Gor, Pendal’s BIDS boutique is one of the most experienced and well-regarded fixed income teams in Australia. In 2020 the team won the Australian Fixed Interest category in the Zenith awards.

The team oversees $22 billion invested across income, composite, pure alpha, global and Australian government strategies with the goal of building Australia’s most defensive line of funds.

Find out more about Pendal’s fixed interest strategies here

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

- Tech and education crackdown sends Chinese shares falling

- China government aims to ease cost of living pressures

- Questions over risk-reward balance for investors

CHINESE regulators this week outlined reforms that will ban private firms that teach the school curriculum from generating profits, raising capital or going public.

The move was aimed at reducing cost-of-living expenses for Chinese familes, who are now encouraged to have three children.

The changes caught investors by surprise. Shares in Chinese private education companies inside and outside the country plummeted.

But this policy shift also has potential implications for a number of Australian-listed companies, in areas such as infant formula.

“There’s two interesting aspects here,” says Elise McKay, an analyst in Pendal’s equities team.

“First of all, China needs to address its population problem.”

“New births have fallen off in China to the lowest level since the famine in 1961. Women of child-bearing age are having fewer children and the population is ageing. This causes real issues.”

“COVID has accelerated this because some people are putting off pregnancy while they get vaccinated or to avoid getting COVID while they are pregnant.”

“The new policy is to lower the cost of raising a child and boost birth rates. They also want to reduce inequality amongst those who can afford to pay for after school tutoring and those who cannot,” says McKay.

Lifting China’s birth rate is potentially good news for businesses that sell to Chinese families, including Australia’s high-profile suppliers of infant formula.

However there is a second aspect to this shift.

“There’s also this increasing uncertainty around regulation, particularly in public companies,” says McKay.

“We need to watch for signals of regulation around pricing for infant formula – this also affects the cost of rearing children.”

Pendal Focus Australian Share Fund

A high-conviction equity fund with 16 years of strong performance in a range of market conditions

“We may also see China look to prioritise domestic brands.”

There are several recent examples of greater intervention in markets. The move in education comes after similar crackdowns in technology, payments and ride-hailing.

A high-profile investigation into ride-hailing firm Didi’s handling of customer data that halved the newly-listed company’s share price.

And it follows a regulatory inquiry into tech giant Alibaba earlier this year that scuppered the float of its payments arm Ant.

A higher birth rate could be an opportunity for Australian companies. But the prospect of more regulation and the prioritisation of domestic brands may shift the balance of risk against investors.

“It’s very nuanced,” says McKay. “And it’s a case for actively managing risk. It is a development that we will be watching very closely.”

About Elise McKay and Pendal

Elise is an investment analyst with Pendal’s Australian equities team. Elise previously worked as an investment analyst for US fund manager Cartica where she covered a variety of emerging market companies.

She has also worked in investment banking and corporate finance at JP Morgan and Ernst & Young.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Find out about Pendal Focus Australian Share Fund here.

Alan joined Pendal Group in February 2017, with extensive investment management and consulting experience. Prior to joining the company, Alan was Senior Manager, Model Portfolios and Risk Research at TCorp, with responsibility for portfolio management of over $40 billion in defined benefit and insurance multi-asset portfolios, developing TCorp’s strategic and dynamic asset allocation processes covering $80 billion in assets, and liquid alternative manager research.

Alan’s prior experience includes six years at AMP Capital in portfolio management and quantitative analysis roles. His most recent role at AMP Capital was a Portfolio Manager/Analyst within the quantitative equites team running and developing the quantitative process across Australian and Asian equities in long only and long/short form. Alan joined AMP Capital as a Quantitative Risk Analyst within the Investment Risk Team that worked to tailor and develop bespoke risk models and analytics for the various internal investment teams, as well as whole of business investment risk analysis. Alan started his career at Mercer Investment Consulting, where he was an investment consultant to some of the largest institutional clients in Australia providing investment advice as well as being actively involved in strategic and manager research functions.

Alan has a Masters of Quantitative Finance, Bachelor of Business (Finance) and Bachelor of Science (Applied Physics) from the University of Technology, Sydney, a Graduate Diploma in Applied Finance and Investment from FINSIA, and is a CFA Charterholder.

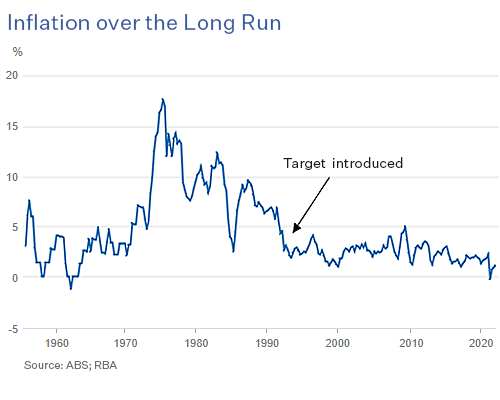

The biggest question in local and global financial markets is no longer about the COVID pandemic. It’s about inflation and whether it will stick around.

- The current bout of inflation is more than transitory.

- RBA models have a bias toward low price rises.

- Mortgage rates likely to start drifting higher

CENTRAL BANKS around the world acknowledge that the global economy is in the midst of a bout of inflation. Most argue it’s transitory, driven by supply-side effects that will dissipate later in 2021.

But has the Reserve Bank of Australia, and its peers, got it wrong?

Quite possibly, says Tim Hext, portfolio manager in Pendal’s Bond, Income and Defensive Strategies team.

“We think that inflation and wages will come back to the RBA target range a lot quicker than the Reserve Bank thinks.”

One of the reasons for the central bank’s potential misreading of the economy is because it forecasts inflation using a model developed about five years ago, which picks up on inflation expectations, Hext says. And expectations over recent years have been low.

“So the model says … the best guide to future inflation is past inflation, because of people’s expectations. It says businesses will be slow to increase prices and consumers won’t be expecting inflation to be a problem. It has a bias in it.”

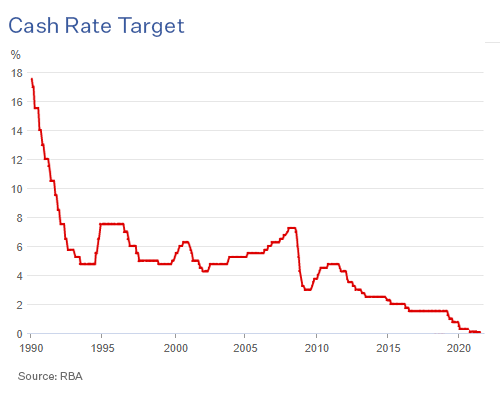

Another reason for the likelihood of the official cash rate rising sooner than the RBA’s current forecast of 2024 is because it came out so publicly about rates remaining low in an effort to stem the downturn in the economy.

“The Reserve Bank is like a big oil tanker. It takes time to turn around,” Hext says. “After providing strong guidance last year, everything in the economy started improving.

“It’s gotten to the point where they’re now using inflation to fit their narrative, as opposed to building their narrative around inflation.”

“It suits them to use the inflation figures [which are very low], but you have to remember that inflation lags the economy by 12 to 18 months. The economy started to pick up in the middle of last year, so I expect to see inflation at the end of this year,” Hext says.

He doesn’t support the view that the supply-induced price rises, currently apparent in the economy, are transitory.

“You’re going to see goods prices squeezed and businesses are in a pretty good position to pass on the cost increases. The data is already showing that in the US.

“And services inflation, which is more important than goods inflation, is exposed to labour markets. Labour is the primary input into services. And the labour market is going to get a lot stronger. It’s likely to be near four per cent this time next year.”

The oil tanker, as Hext puts it, will have to start turning.

Find out about

Pendal’s Income and Fixed Interest funds

The first thing the Reserve Bank did was switch off the term funding facility for banks at the end of June, thereby denying lenders a cheap source of funds, Hext says.

They have also announced a taper of quantitative easing by reducing purchases of government bonds from $5 billion a week to $4 billion a week in September, although recent lockdowns may see that timing pushed back.

And finally the central bank will have to lift the official cash rate, which is used to price other lending rates.

Hext says the term funding facility played as big a role on interest rates for mortgages on the way down and is likely to do so on the way back up.

“The money the banks borrow [to lend to customers] will be at a higher rate once the funding facility ends. It will take time to work through the system, but the overall cost of funding for banks will go up. And mortgage rates will start drifting higher.”

The spectre of inflation is back, and as Hext puts it, the Reserve Bank oil tanker might need to turn just a bit faster.

About Tim Hext and Pendal’s Income and Fixed Interest boutique

Tim Hext is a portfolio manager with Pendal’s Income and Fixed Interest team.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia. In 2020 the team won the Australian Fixed Interest category in the Zenith awards.

With the goal of building the most defensive line of funds in Australia, the team oversees A$22 billion invested across income, composite, pure alpha, global and Australian government strategies.

Find out more about Pendal’s Income and Fixed Interest strategies here

About Pendal Group

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.