While August inflation data shows inflation has eased, more progress is required before we’ll see rate cuts in Australia, writes Pendal’s head of government bond strategies TIM HEXT

- RBA not celebrating just yet

- We still expect four rate cuts next year

- Why bonds, why now? Pendal’s income and fixed interest experts explain

- Browse Pendal’s fixed interest funds

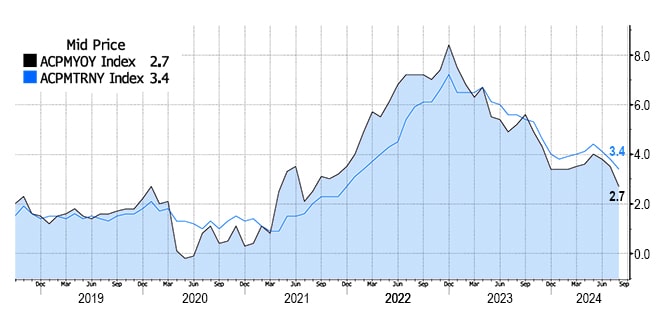

A SHARP fall in headline inflation was reported today, in the latest monthly CPI series for August.

Prices since August last year are only 2.7% higher and are back in the RBA’s target band of 2-3% for the first time since a 3% reading in October 2021.

Market forecasters did a great job in a volatile series, as 2.7% was spot on expectations.

Though encouraged, the RBA will not be celebrating yet.

Massive government subsidies, largely on electricity, are the main reason headline inflation is falling fast.

Electricity prices, accounting for the subsidies, fell 14.5% in August and are now 20% lower in Q3. They make up only 2.4% of the CPI weight, but 20% on 2.4% still impacts CPI by 0.5%.

Trimmed mean (underlying) inflation, which cuts out the highest and lowest-weighted 15% of price moves, is still at 3.4%.

This is the RBA’s main focus, and the central bank would need to be convinced that this will be sustainably at, or very near, 3% to begin cutting rates.

Our initial forecast for underlying inflation for Q3 is 0.7% (headline will be near flat). This annualises at 2.8%.

However, the RBA would likely need to see Q4 at a similar level, though if unemployment were to rise enough in October and/or November, it could tip the balance.

We don’t get Q4 CPI numbers till late January, which makes the current market forecast of an 80% chance of one rate cut by year-end optimistic.

Source: Bloomberg

Another inflation-friendly factor during August was falling fuel prices. These fell 3% in August and are 7.6% lower than a year ago.

Pump prices are lower again in September, though a recent bounce in crude oil prices should see what we pay go up again in early October.

In terms of the higher inflation sectors of recent times, there were no major moves.

Rents were up 0.6% on the month again and still look locked into around 6-7% annual growth.

Insurance prices were up 2.8% for the quarter and remain near double-digit annual growth.

Service inflation (around two-thirds of the CPI) is at 4.2% – still too high – but with wage growth topping out at 4% and likely to ease back, the RBA should be getting a bit more comfortable.

Implications

This data doesn’t change our view.

We still expect four rate cuts next year, likely at a quarterly pace beginning in February.

Market pricing is not too dissimilar, though pricing almost one cut by December.

While the RBA will ignore the subsidy-led lower headline inflation, we feel it is underestimating how this feeds back into wider prices.

A higher inflation loop (inflation leads to wages leads to inflation) of 2022 and 2023 is now a lower inflation loop.

We also expect Federal Government electricity subsidies to become a permanent feature.

The shift by the RBA yesterday to neutral (hikes are no longer being actively discussed) is step one in the move towards an easing.

By year-end, the US Federal Reserve will have its cash rates around Australia’s cash rate and we expect both to move nearer to neutral in 2025.

About Tim Hext and Pendal’s Income & Fixed Interest boutique

Tim Hext is a Pendal portfolio manager and head of government bond strategies in our Income and Fixed Interest team.

Tim has extensive experience in banking, financial markets and funding including senior positions with NSW Treasury Corporation (TCorp), Westpac Treasury, Commonwealth Bank of Australia, Deutsche Bank, Bain & Co and Swiss Bank Corporation.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia.

Find out more about Pendal’s fixed interest strategies here

About Pendal

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

In 2023, Pendal became part of Perpetual Limited (ASX:PPT), bringing together two of Australia’s most respected active asset management brands to create a global leader in multi-boutique asset management with autonomous, world-class investment capabilities and a growing leadership position in ESG.

Here are the main factors driving the ASX this week according to portfolio manager JIM TAYLOR. Reported by investment specialist Chris Adams

- Find out about Pendal Focus Australian Share Fund

- On demand: tune into Crispin Murray’s Beyond the Numbers webinar

THE Big Show finally hit town when the US Federal Reserve began its much-anticipated rate cutting cycle, though at a quicker pace than many judged appropriate.

With a slew of generally positive US economic data (including retail sales, employment, industrial production, housing and the Atlanta Fed GDPNow) conditions were set for new record highs across equity indices during the week.

The S&P 500 gained 1.39% while the NASDAQ rose 1.51%. The S&P/ASX 300 was up 1.38%.

Elsewhere, longer-dated bond yields saw minor gains and commodities had a pretty good week.

So, where to from here?

The immediate reaction on Wednesday was markets giving up gains on the notion that a hawkish cut of 50 basis points (bps) means the Fed knows something (about employment, most likely) that the market doesn’t, so caution is still required.

On Thursday, we saw the classic beta/cyclical rally. And by Friday, it all proved a bit hard for markets to work out, so they dipped a touch as they began a phase of recalibration.

There is a view that the cut should benefit “risk-on” assets such as small caps, cyclicals and commodities, but that a 50bp move also removes some of the Fed’s insurance against a soft landing.

In the US, the August Personal Consumption Expenditures (PCE) release on Friday will be key in setting the market’s mood.

This week in Australia, we have the RBA Board meeting on Tuesday followed by August Consumer Price Index (CPI) on Wednesday.

Find out about

Pendal Focus

Australian Share Fund

Crispin Murray,

Head of Equities

US macro and policy

The Fed

September’s Federal Open Market Committee meeting ended with a 50bp rate reduction to a 4.75-5.00% range – an outcome priced in at a 60% probability leading up to the meeting.

In its statement, the Fed noted indications that economic activity continues to expand at a solid pace, job gains have slowed, and the unemployment rate has moved up but remains low.

It also stated that it had made further progress towards the 2% inflation objective, but that it remains somewhat elevated.

In keeping with its recent tone, the Fed noted that the risks to achieving its employment and inflation goals are roughly in balance and that the Committee is attentive to the risks to both sides of its dual mandate.

Michelle Bowman became the first Federal Reserve Governor (as opposed to Fed President) to dissent on a rate decision since 2005.

She was alone in calling for a 25bp cut rather than the cut delivered.

A 50bp cut “could be interpreted as a premature declaration of victory” over inflation, she said in a statement on Friday, while a slower pace of cuts would “avoid unnecessarily stoking demand.”

She believes that “moving at a measured pace toward a more neutral policy stance will ensure further progress in bringing inflation down to our 2% target.”

In contrast, Governor Christopher Whaller noted that “50 really was the right number.”

“We’re at a point where the economy is strong, inflation is coming down, and we want to keep it that way,” he said, adding that “inflation is running softer than I thought.”

Looking forward, the Fed’s Summary of Economic Projections (SEP) now shows the FOMC’s median expectation is for a Fed Funds Rate of 4.4% by the end of 2024 and another 100 bps of cuts in 2025.

Presumably, the Fed forecast is now for two further 25bp cuts out to Dec 24. The market is slightly ahead of this, pricing in 75bps of cuts, implying another 50bp move in November or December.

Interestingly, the Fed sees unemployment only increasing to 4.4% in the December 2024 quarter – up from 4.2% in August and 3.7% in January – and sees it also at that point in Q4 2025.

While there may be an intra-point peak above this, it still suggests a very shallow employment recession indeed.

In his press conference, Chairman Jay Powell noted that the economy is in good shape – growing at a solid pace with inflation coming down. He emphasised that the labour market is in a strong place and that the Fed wants to keep it there.

He also said that “nobody should look at today’s 50bp move and say, ‘this is the new pace.’”

This isn’t a “catch-up” rate cut because the FOMC was behind the curve, according to Powell. Instead, it was a signal of the Fed’s “commitment not to get behind.”

Housing

There were some optimistic datapoints on the housing market:

- August new housing starts were 1.356m versus consensus expectations of 1.325m, rising 5.5% from July’s 1.237m. Building permits rose 4.9% month-on-month (m/m), also ahead of expectations, while single-family housing starts in August rose 15.8% from July.

- The NAHB Housing Market Index was in line with consensus at 41.0, up two points from August’s reading of 39.0 after four months of consecutive declines. The report noted lower interest rates mean builders have a positive view for future new home sales for the first time since May 2024.

Existing home sales dropped to 3.86m in August (from 3.96m in July and below consensus expectations of 3.90m). They are at their second-lowest level since 2010.

Mortgage rates have fallen in previous weeks, with the 30-year rate at 6.15% versus 6.80 in the June quarter.

This may prompt increased mortgage activity, which may flow through to strengthen existing home sales in coming months

However, a mortgage rate of 6% is still well above the average rate of about 4% on the stock of existing mortgages. This means moving and taking out a new mortgage would still involve a hit to most household finances.

Fannie Mae noted that lower mortgage rates aren’t likely to finish the current “buyer’s strike” as prices remain too high. They are not seeing an increase in loan applications or improvement in consumer homebuying sentiment.

Instead, they think buyers are sitting on their hands in anticipation of lower rates and improving affordability.

In this vein, the inventory of existing homes for sale hit the equivalent of 3.8 months of sales in August, up from 3.7 in July.

This is the highest since 2020 due, primarily, to slower sales rather than new inventory hitting the market.

The inventory of existing homes for sale remains around one-third below its 2015-to-2019 average, which helps explain – alongside population growth and rational home builder activity this cycle – why median house prices have remained elevated and steady despite higher mortgage rates and subdued sales activity.

Other economic data:

- Industrial production rose 0.8% m/m in August, 60bps higher than consensus and following a 0.9% m/m fall in July. This reflected increases in manufacturing and mining, with utilities activity unchanged.

- Retail sales rose 0.1% in August at a headline level, but a price-driven 1.2% drop in gas station sales weighed upon it. Excluding gas station, autos, food services, and hardware store sales – considered a better guide to the underlying trend – sales rose by 0.3%, following solid increases in the prior few months. The annualised rate of growth in underlying sales in the three months to August rose 5.7%, up from 4.9% in July.

- Weekly initial jobless claims dropped to 219k, from 231k, below consensus expectations of 230k. Continuing claims fell to 1,829k from 1,843k – also below the consensus of 1,850k.

- The Atlanta Fed GDPNow estimate of real GDP climbed from 2.5% to 3% for Q3 2024.

Australia macro and policy

Employment rose by a solid 48k m/m in August, after 49k in July (after revisions) and well ahead of consensus expectations of 26k.

The lift was driven entirely by part-time employment (up 50k). Full-time employment fell a touch, which is perhaps one sign of some softness in the data.

Labour supply continues to grow strongly. This means that even as the participation rate climbs, the upward trend of unemployment probably remains intact.

Population growth is exceeding government expectations by roughly 100k, which is due primarily to lower numbers of residents leaving. Resident departures are running at 35% below pre-Covid levels.

So the contrast with the US, where focus has shifted from inflation to concern over employment, remains. Domestically, employment remains robust, and during reporting season there were few companies talking about job cutting to preserve margins.

The RBA remains more concerned about inflation than jobs.

China

China’s credit impulse remains muted.

Despite some hope, we have not seen the same historical surge in credit that Beijing deployed after the GFC and Covid, as well as in response to domestic slowdowns in 2012 and 2015.

This year, the credit impulse (as measured by the Bloomberg Economics China Credit Impulse) has come down since January.

In August, new home prices in 70 major cities dropped 0.7% from July, falling for the 14th month in a row.

Prices were down 5.3% from a year earlier. This is the fastest rate of decline since May 2015.

There is some dispersion by city size. Prices have fallen 9.4% year-on-year in the four tier-one cities, while second and third-tier cities were down 8.6% and 8.5%, respectively.

House prices in some smaller cities have fallen by more than 40% since peak in 2021.

At the same time, the stock of unsold properties has risen to a new high – demonstrating how far sentiment has weakened despite Beijing’s efforts to underpin the sector.

Europe and Japan macro and policy

As expected, the Bank of England kept rates unchanged, noting that there had been “limited news” in the incoming data and that “a gradual approach to removing policy restraint remains appropriate.”

Some see this as suggesting a 25bp rate cut in November, followed by quarterly steps with scope to adjust in response to material developments.

Meanwhile, the Bank of Japan left rates unchanged.

About Jim Taylor and Pendal Focus Australian Share Fund

Drawing on more than 25 years of experience investing in top-performing Australian companies and a background in accounting, Jim manages our Long/Short Fund and co-manages our Imputation Fund. He is a Chartered Accountant with membership of the Australian Institute of Chartered Accountants.

Pendal Focus Australian Share Fund is managed by Crispin Murray. The fund has beaten its benchmark in 14 years of its 18-year history (after fees), across a range of market conditions. Find out more about Pendal Focus Australian Share Fund here.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

What US rate cuts mean for investors | Lessons from ASX reporting season | Where to find opportunities in Asia

Now that the US rate-cut cycle has begun, the Fed’s focus turns from inflation to employment. Head of government bond strategies TIM HEXT explains what this means

- Rate-cutting cycle has begun

- Near term, the market is still ahead of the Fed itself

- Why bonds, why now? Pendal’s income and fixed interest experts explain

- Browse Pendal’s fixed interest funds

THE US Federal Reserve cut 50 basis points overnight to 5 per cent, ending the 25bp-or-50bp debate of the past month.

You might have expected the bigger cut to help bond and equity markets, but both moved slightly the other way.

Yields were around 5 bps higher and equity markets around 0.5 per cent weaker.

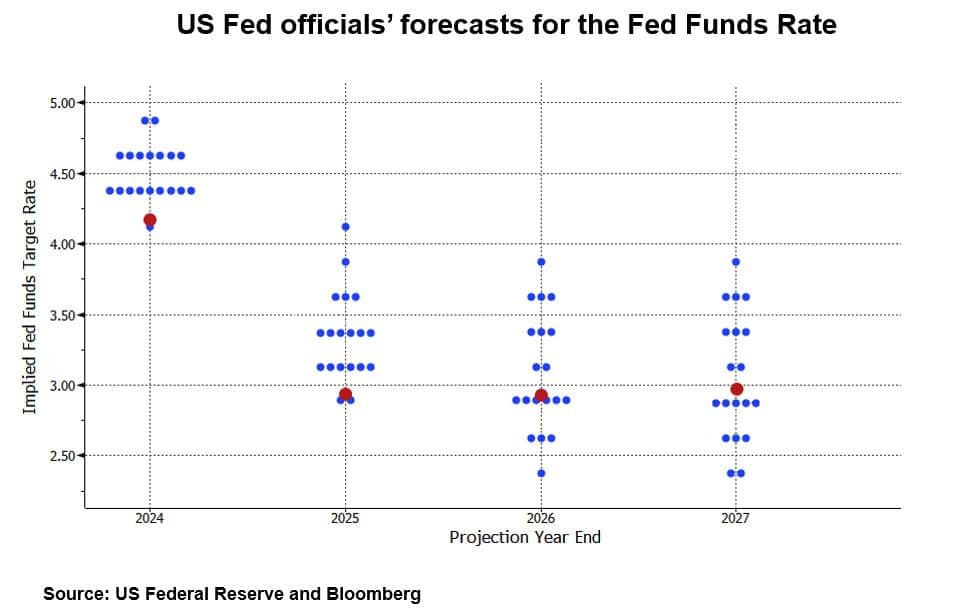

This response is more to do with the optimism already priced in versus the Fed estimates for future rates – known as the “dots”.

The Fed’s closely followed “dot plot” visually represents the rate expectations of individual Federal Reserve officials.

Every quarter these 18 officials publish their economic projections across a number of economic indicators.

Each September they extend out to three years – so we now have our first look at these projections for 2027.

They also provide an estimate of the long-term neutral rate of interest.

Here are the 18 dots for each year as per the latest information from the Fed (PDF). I have added the market estimate based off current pricing (in red).

As you can see, near term the market is still ahead of the Fed itself.

So, while the actions overnight could be seen as bullish for markets, the dots were also a reminder that speed and final destination matters.

The impact of hosing down expectations outweighed the larger actual cut.

Now, Fed officials are always at pains to say these are just estimates and not some preset path.

As always, it will react to incoming data.

With two meetings between now and the end of the year, the Fed estimate of only 50bp in further cuts may prove too low. Time will tell.

In the big picture though, a rate-cut cycle has begun.

The Fed is now more focused on employment than inflation, so payroll data will be front and centre.

We expect a day or two of slightly higher yields as some positions are cleaned out.

But any move back to 4 per cent or higher on Australian 10-year yields should be seen as an opportunity to add duration.

About Tim Hext and Pendal’s Income & Fixed Interest boutique

Tim Hext is a Pendal portfolio manager and head of government bond strategies in our Income and Fixed Interest team.

Tim has extensive experience in banking, financial markets and funding including senior positions with NSW Treasury Corporation (TCorp), Westpac Treasury, Commonwealth Bank of Australia, Deutsche Bank, Bain & Co and Swiss Bank Corporation.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia.

Find out more about Pendal’s fixed interest strategies here

About Pendal

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

In 2023, Pendal became part of Perpetual Limited (ASX:PPT), bringing together two of Australia’s most respected active asset management brands to create a global leader in multi-boutique asset management with autonomous, world-class investment capabilities and a growing leadership position in ESG.

There have been a few false starts in the turning point for the current economic cycle, but now it’s the real deal, says Pendal’s head of government bonds, TIM HEXT

- Focus is shifting from inflation to the labour market.

- Bond yields likely to keep falling

- Why bonds, why now? Pendal’s income and fixed interest experts explain

- Browse Pendal’s fixed interest funds

CENTRAL banks never use language unintentionally and Federal Reserve chair Jerome Powell has made it very clear that rate cuts are coming, Hext says.

Powell recently used phrases like “the inflation battle is over”, Hext says, and while inflation is always important, it is less important than it was.

“The market will now be more forgiving. A slightly higher number on inflation, or a slightly lower number, won’t move the market as much,” he says.

“The focus now is squarely on employment and unemployment and Powell’s line that the Fed does not ‘seek or welcome further cooling in labour market conditions’ is particularly interesting. He is basically saying the US is at full employment, at a point where it is not inflationary.”

That is a key difference between the US and Australia, and a reason why the Reserve Bank has not indicated a bias towards easing monetary policy.

“It’s hard to put a number on it but the RBA believes full employment in Australia is probably around 4.4 per cent and currently the unemployment rate is 4.1 per cent.”

What does that mean for investors in government bonds?

“It is very difficult to pick the very top or very bottom in yields. What is easier is to look at the trend. Are rates going up or are they going down?” Hext asks.

“When the central bank starts hiking or cutting benchmark rates, the bond market has already moved. But that doesn’t mean the moves in bond yields have gone as far as they are going to go. The changes in benchmark rates continue the trend. They don’t end it.”

“When the Reserve Bank hiked rates in May 2022 the market had been selling off quite aggressively for six months and it continued to sell of afterwards. Right now, there’s been a decent rally for six months and that will continue,” Hext says.

“The point is the trend will keep going and there’s still time to benefit from that.”

In equities trading, price-to-earnings multiples and forward earnings expectations are widely used to determine the “fair value” of a stock. Is there an equivalent in bonds?

“There’s two key anchor points for bonds,” Hext explains.

“One is inflation, and that other is real interest rates. It is a bit definitional because inflation plus a real rate equals a nominal rate, but it tells investors if interest rates are protecting them against inflation.”

Hext says if the Reserve Bank is doing its job, inflation over the long term will be about 2.5 per cent, which provides a starting to point for risk-free government bonds.

To get a real return in excess of the risk-free rate, over the long term, an economy must become more productive, meaning more output per unit of input.

The Productivity Commission estimates that productivity should be around 1.2 per cent long term, meaning a risk-free bond yield of 3.7 per cent is about par.

Hext emphasises these are long run concepts and provide a guide only.

The yield on a ten-year government bond currently is around four per cent, suggesting bonds are fetching more than the long-term average, Hext says.

“If anyone asks what fair value is for a ten-year bond, then that’s as good a guess as any. It looked ridiculous when ten-year bonds were at one per cent and optimistic when they were at five per cent, but it is a long-term concept,” he says.

“It is the sort of analysis people need to undertake if they are, for example, considering a term deposit. Within 12 months you are not going to get a term deposit for a four in front of it, whereas in bond markets, which are liquid, you can buy a semi-government bond at closer to five per cent.”

About Tim Hext and Pendal’s Income & Fixed Interest boutique

Tim Hext is a Pendal portfolio manager and head of government bond strategies in our Income and Fixed Interest team.

Tim has extensive experience in banking, financial markets and funding including senior positions with NSW Treasury Corporation (TCorp), Westpac Treasury, Commonwealth Bank of Australia, Deutsche Bank, Bain & Co and Swiss Bank Corporation.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia.

Find out more about Pendal’s fixed interest strategies here

About Pendal

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

In 2023, Pendal became part of Perpetual Limited (ASX:PPT), bringing together two of Australia’s most respected active asset management brands to create a global leader in multi-boutique asset management with autonomous, world-class investment capabilities and a growing leadership position in ESG.

The Pendal Enhanced Credit Fund (Fund) will terminate on Monday, 2 December 2024.

Why is the Fund terminating?

The Fund’s small size means that it has high running costs and cannot be managed in a cost efficient way.

We also consider that the Fund has little prospect of significant growth in funds under management in the foreseeable future. If the Fund were to continue, the Fund’s size would result in higher management costs for investors, which would reduce their investment returns.

How this affects you?

We will terminate the Fund on Monday, 2 December 2024.

Any applications received after 11:00am (Sydney time) on Tuesday, 17 September 2024 will not be accepted. There will be no reinvestment of distributions from 11:00am (Sydney time) on Tuesday, 17 September 2024.

Withdrawals and transfers will continue to be processed until 2:00pm (Sydney time) on Friday, 29 November 2024.

As soon as practicable after the Fund is terminated on Monday, 2 December 2024, we will begin winding up the Fund. The assets remaining in the Fund will be realised and the proceeds distributed to all investors in proportion to their unit holding.

What does this mean for you?

Cash proceeds from this termination will be paid directly to your nominated bank account on file on or around the week commencing Monday, 9 December 2024 or shortly thereafter.

Any distributions paid from 11:00am (Sydney time) on Tuesday, 17 September 2024 will be paid as cash into your nominated bank account on file.

Details of any distributions paid to you during the current financial year will be included in your final AMIT Member Annual (AMMA) statement. This statement will set out the components of the income that have been attributed to you following the end of the financial year ending 30 June 2025.

Questions?

If you have any questions, please contact our Investor Relations Team during business hours on 1300 346 821.

Here are the main factors driving the ASX this week according to investment analyst SONDAL BENSAN. Reported by investment specialist CHRIS ADAMS

- On demand: watch Crispin Murray’s Beyond the Numbers webinar

- Find out more about the Pendal Focus Australian Share Fund

A SOFT LANDING is increasingly accepted as the most likely outcome in the US, with inflation-related data in check and the labour market not showing any material incremental deterioration.

Last week, we went from the market pricing next-to-no chance of a 50-basis-point (bp) cut by the Fed following Wednesday’s CPI data, back to an almost 50% chance of a 50bp cut by week’s end.

This drove equities higher and gold to new highs. The S&P 500 rose 4.06%, the NASDAQ was up 5.98%, and Australia’s S&P/ASX 300 was up 1.48%.

The change seemed to come from what was viewed as a leading article in the Wall Street Journal: “The Fed’s Rate Cut Dilemma: Start Big or Small”.

It quoted Jon Faust, who served as senior adviser to Fed Chairman Jay Powell until earlier this year, who said it was a “close call” between whether the first move is 25bps or 50bps but that the number of cuts over the next few months is going to be more important.

Markets also got a boost from the AI thematic as NVIDIA CEO Jensen Huang made positive comments about trends toward densification and acceleration in data centres at the Goldman Sachs Communacopia and Technology Conference. NVIDIA was up about 16% for the week.

Oracle also had an investor presentation that provided bullish future guidance well above market expectations. Its stock was up 14% for the week.

US macro and policy

August Consumer Price Index (CPI) and Producer Price Index (PPI)

There was not a great deal of new information, or anything to derail the path of inflation falling back to 2%, in the August CPI or PPI released last week.

Core CPI rose 0.3%, slightly above consensus but driven by segments that will moderate:

- A 0.33% increase in the core services ex-rents index was primarily driven by a 3.9% rise in airline fares, reversing a five-month decline. The impact of pandemic-related travel restrictions and the surge in travel demand in summer 2021 and 2022 has distorted seasonal patterns.

- A 1.8% jump in accommodation prices contributed an additional 0.10 percentage points to the core services index increase. However, accommodation price growth is expected to average just 0.2% in the coming months, as households cut back on discretionary spending due to a worsening labour market.

- Primary rents increased by 0.37% in August, down from July’s 0.49% rise. However, it was still higher than expectations given that Zillow’s new rents index has averaged a 0.29% increase over the past two years. It is anticipated that primary rent increases will converge to 0.30% over the next six months.

- Auto insurance prices rose by 0.6%, an improvement compared to the previous six months’ average increase of 1.2%. The downward trend in vehicle prices suggests that auto insurance inflation could continue to decline.

- CPI for hospital services increased by 0.4%, which was better than anticipated following a sharp 1.0% decrease in July.

The market’s reaction was an increase in the implied probability of an initial 25bp rate cut from 66% to 83%.

Core PPI increased 0.3%, a modest overshoot of 0.2% consensus expectations.

Importantly, most of the components of the PPI that feed into the personal consumption expenditures (PCE) deflator – the Fed’s key measure of inflation – were lower than expected.

In particular, the unadjusted PPI for domestic air passenger transportation fell by 1.8%, which means that the seasonally adjusted PCE deflator for airline fares likely dropped by about 2%.

There is a debate that airline fares will fall further over the next few months, given the drop in oil prices. But US airlines have been making no money and have cut capacity into the fourth quarter, so oil prices will likely drop to the bottom line and fares could actually go up.

PPI for portfolio management charges, health insurance, and hospital services also rose less than expected. Auto insurance prices were unchanged, in contrast to the CPI equivalent, which has continued to rise rapidly.

Growth in wages – the key input cost for services firms – is continuing to slow in response to the recent fall in the openings-to-unemployment ratio, the drop in the quits rate, and the decline in inflation expectations.

Mortgage applications

US 30-year fixed mortgage rates came back a long way last week.

While still high in an absolute sense, lower rates are already having an impact on the appetite for households to borrow again and breathe some life into the housing market.

Applications for home purchase rose by 1.8% last week. The year-over-year growth rate has improved to -3.5% from -7.9% four weeks previously, and a low this year of -22.8% in early April.

Weekly jobless claims

There was nothing alarming here. Initial jobless claims increased to 230k from 228k, a bit above the consensus of 227k.

Let’s not forget the market panic when this number shot up to 240k in July. Since that aberration, it has been relatively steady at these current levels.

Forward indicators for jobless claims point to the number falling further based on layoff announcement data.

US election

The second US Presidential debate was largely a non-event. While the candidates remain neck-and-neck, post the debate the odds swung marginally toward Harris.

A Harris win is generally seen as a pro-market outcome given spending continues and we don’t have the negative growth and inflation impacts of tariffs from Trump. The election is 5 November, two days before the FOMC meeting.

Australia macro and policy

August CBA retail data confirmed some of the partial-month retail updates from corporates through reporting season.

Some of these numbers may have got a slight bump from the timing of Father’s Day this year and there is likely still some upside from tax cuts.

The conclusion remains that the consumer is holding up quite well in Australia. There still seems no real chance of the rate-cutting cycle beginning in Australia this year.

That said, the NAB Business Survey Index deteriorated for August, with retail conditions one of the big areas of weakness.

The Consumer Sentiment Survey for August was also soft. Compositionally, weaker perceptions of the economic outlook offset a marginal improvement in perceptions of personal finances. Perceptions around the labour market and house prices continued to soften.

The Melbourne Institute inflation gauge, which is a timelier measure of where inflation is headed, points to further easing in Australian inflation back to within the RBA target band.

China

As the S&P 500 retests its highs, Chinese equity markets are retesting their lows as both the property market and domestic demand remain problematic and as policymakers sit on their hands – most likely until after the outcome of the US election.

This underperformance is also being reflected in Australian companies that are leveraged to growth from China.

There are three broad issues in China:

- High savings rates are leading to lower domestic demand, domestic deflation and a growing trade surplus in goods.

- The housing problem remains after years of overbuilding. Housing starts and sales are tumbling.

- Birth rates are low as people lack confidence to have babies, creating a demographic problem.

There is no easy solution, other than perhaps handing out cash and free homes to those willing to have a few children.

On Friday, Beijing approved a plan for the first hike in retirement ages since 1978, raising the age to 63 for men and 58 for women.

China’s export growth for August was stronger than expected at 8.7% year-on-year (YoY), versus 7.0% YoY in July.

Imports lagged and slowed from 7.2% YoY in July to 0.5% YoY in August.

For most of the post-pandemic period, exports and imports have been tightly correlated.

However, from the start of this year imports have consistently fallen short of export growth, supporting a prognosis of weak domestic demand.

Europe macro and policy

The European Central Bank (ECB) cut its deposit rate for a second time this year, by 25 bps to 3.5% as expected.

It also lowered its growth forecasts through 2026, with President Christine Lagarde saying the recovery is “facing some headwinds” and reiterating that the path for rates is not pre-determined.

Find out about

Pendal Focus

Australian Share Fund

Crispin Murray,

Head of Equities

Lithium

Lithium equities rebounded over the week following news that CATL (Contemporary Amperex Technology Co. Limited), a Chinese battery manufacturer and technology company, has suspended production of a lepidolite mine in China.

Lepidolite is a mineral from which lithium is extracted.

The announcement drove a short squeeze across the sector, with the suspension expected to take roughly 10% of China’s existing supply, or 3% of global 2025 supply, of lithium carbonate equivalent out of the market.

The suspension is driven by the sharp drop in pricing – with the CATL mine cash cost estimated at US$11k/t, or RMB89k, below where spot was trading.

The news also follows recent moves by Arcadium Lithium and Mineral Resources to defer growth projects and near-term supply.

Pricing has dropped below marginal cost, providing more support to pricing from here.

However, the market remains in surplus and new projects that were approved and/or funded over the past two years will continue to drive material supply growth near term, limiting expected price gains.

Markets

US equity sector performance was led by a rebound in materials (with gold stocks up about 9%), continued performance in tech and interest rate-sensitive sectors like homebuilders.

Energy stocks were the key laggards, even with a small reprieve in oil prices, as the oil price move was more from traders short covering as Hurricane Francine ripped through key oil-producing zones in the US Gulf of Mexico.

In Australia, Materials gained 5.69% and Real Estate 5.65%. Financials were weakest, down 0.76%.

About Sondal Bensan and Pendal

Sondal is an investment analyst with more than 20 years’ experience covering the Retail, Telecom, Media and Transport sectors. He joined Westpac Investment Management in 1999 and has previously held roles with Commonwealth Bank and Bell Commodities.

Sondal holds a Bachelor of Commerce (Finance) and a Bachelor of Science (Maths and Statistics).

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

Where next for Asia? As companies and countries across the continent adapt to China’s slowdown, opportunities are emerging. Portfolio managers ADA CHAN and SAMIR MEHTA explain

- Asia’s companies rapidly adapting

- If liquidity improves, Asia could be “well set for a decent run”

- Find out more about the Global Emerging Markets Opportunities Fund

- Find out more about the Asian Share Fund

ASIAN economies are shaking off China’s slowdown and showing signs of renewed vigour, sparked by a wave of tech innovation and a global trend to supply-chain diversification.

Renewed optimism for Asia is a reminder to avoid the trap of assuming temporary challenges are here to stay, says Pendal portfolio manager Samir Mehta. Companies tend to actively adapt and evolve during difficult times, he says.

Mehta and emerging markets portfolio manager Ada Chan were speaking in an Asia Reborn webinar which examined the drivers of the improving outlook for Asian equities.

“When a country goes through significant challenges, you don’t expect companies to remain static,” says Mehta.

“Headlines about tariffs and geopolitics are all we hear of. But each and every company we meet with is reacting in a very different manner, adjusting and getting more competitive to deal with these challenges.

“All the company meetings we do and the managers we meet make us reasonably confident that if liquidity conditions do get better — which is the potential in the next 12 to 18 months — Asia could be well set for a decent run in terms of economic activity and potentially even stock market performance.”

Mehta manages Pendal Asian Share Fund, an actively-managed portfolio of Asian shares.

Find out about

Pendal Global Emerging Markets Opportunities Fund

Chan co-manages Pendal Global Emerging Markets Opportunities Fund which takes a top-down, country-driven approach to stock selection in emerging markets.

China: pockets of strength

Beijing’s crackdown on excesses in the real-estate sector sent Chinese credit growth tumbling to multi-year lows, says Chan.

“The property sector, which is a pillar of growth in China, has slowed down because the Chinese government was concerned about the balance sheet of property developers. Hence, we’ve seen this credit deterioration,” says Chan.

However, the overall decline masks a more nuanced story. As real-estate credit growth plummets, credit in China’s industrial sector is rising sharply.

“The government needs to take care of over-leverage — so spending is going into other industries.”

This reflects a deliberate policy choice.

Ada Chan, far right, a co-manager of Pendal Global Emerging Market Opportunities fund

“China is very government driven,” says Chan. “Even though the overall economy might be weak, there are pockets of strength, and we want to try to align with what Beijing wants.

“To sum it up in a simplistic way, the Chinese government wants people to spend domestically, and that’s one of the themes we have in our portfolio: domestic consumption and domestic travel.”

Taiwan and Korea: strong tech outlook

Taiwan and Korea are pivotal players in global technology and the big tech exporters are benefiting from the rapid adoption of artificial intelligence, says Chan.

“Within technology we want to position in the leading-edge technology.

“We think AI will be an important growth driver for many years. The timing might be uncertain, but if you own the leading-edge technology companies, we think you can play it through the cycle.”

Chan says her portfolio is underweight Taiwan and Korea overall, but with investment in those leading-edge technology firms.

Mehta says investors could also look beyond the leading firms to capture growth from a potential AI-inspired upgrade cycle for both corporate and personal technology devices over the next few years.

“That replacement cycle will require a lot of the expertise that Taiwanese manufacturing companies have, even below the leading-edge technologies.

“That’s where we have some of the stocks in our portfolio, reflecting that potential for growth.”

But he says in his view the potential for gains in Korea is somewhat clouded by an inheritance tax regime that discourages the big family-owned chaebol conglomerates from realising the full value of their businesses as they seek to hand down control to the next generations.

India: valuation concerns

In contrast to China, the Indian economy has performed very well in recent years, driving equity markets strongly higher.

Mehta says the outperformance is driven in a large part by a dramatic improvement in the country’s Incremental Capital Output Ratio — a measure of the efficiency of capital use in an economy.

“One of things investors are trying to understand is if there are any fundamental drivers that could justify some of the elevated valuations in India,” he says.

“ICOR is how much incremental capital investment is required in an economy to generate additional marginal $1 of GDP growth.

“For the period between 2005 to 2014, China and India were relatively similar. But since 2015, so much of the investment in the mainland Chinese economy went into unproductive assets, which has led to a stark deterioration in the ICOR in China.

“Whereas in India, which is a country that has perennially been starved of capital, when you had this growth come through, returns on capital employed for the economy as a whole, and therefore for companies that are listed on the stock exchange, have done exceedingly well.

“That partly, we think, explains the elevated valuations.”

Chan says the high valuations have led her to tilt towards businesses exposed to infrastructure spending and away from export-related businesses and those exposed to domestic consumption.

“We think the valuation is too rich. The economy is growing and economically strong, however with that kind of valuation, we are a bit concerned — it’s basically pricing for perfection.”

‘China plus one’ strategy

Indonesia’s decade-long ban on raw nickel exports has helped position its economy to capture a larger share of battery manufacturing for electric vehicles, says Chan.

This is driving a rapid improvement in the country’s trade balance and attracting attention from foreign investors.

But Mehta says what is less known is that a similar story is playing out throughout South-East Asia.

“Overall, I’d say ASEAN is in a much, much better position and all these countries are very well-suited to take advantage of the ‘China plus one’ strategy that is at the heart of geopolitics.”

Adopting a ‘China plus one’ business strategy means keeping a Chinese supply chain but adding parallel suppliers elsewhere to build redundancy.

“And it’s not just the multinationals,” says Mehta.

“In fact, some of the largest Chinese manufacturing enterprises also want to de-risk the tariffs that might come through — and so they’ve set up operations, not just in ASEAN, but in Mexico and other countries.”

Mehta highlights Thailand’s expertise in auto-manufacturing.

“Some of the leading companies out of China have taken one of the biggest parcels of land ever bought in an industrial estate in Thailand.

“A number of Chinese workers and management are moving into Thailand to run these operations. That requires a lot of services to be provided for them and their families and so there are opportunities that Thai businesses are taking advantage of.”

About Ada Chan and Samir Mehta

Ada Chan is a co-manager of Pendal’s Global Emerging Markets Opportunities Fund.

The fund’s top-down allocation process is based on analysis of a country’s economic growth, monetary policy, market liquidity, currency, governance/politics and equity market valuation.

Samir Mehta manages Pendal Asian Share Fund, an actively managed portfolio of Asian shares excluding Japan and Australia.

Ada and Samir are senior fund managers at UK-based J O Hambro, which is part of Perpetual Group.

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

Earnings season results indicate a positive outlook for the Australian economy. That’s good news for stocks, says Pendal’s head of equities CRISPIN MURRAY

- Earnings season indicates economy is resilient

- US rate cuts bolster outlook

- Find out about Pendal Focus Australian Share fund

- Register to watch Crispin’s Beyond the Numbers webinar

A DIMINISHING threat of recession in Australia and US rate cuts should support Australian stocks over the next 12 months, says Pendal’s head of equities, Crispin Murray.

Australian equities have performed strongly since March, driven by ratings increases and growing confidence in the economic outlook.

Strong spending from older Australians and a growing population should see Australia avoid recession, even as younger generations come under increasing cost of living pressures, says Murray.

“We think the economy is OK. Doesn’t mean it’s strong — there’s still going to be plenty of challenges — but we don’t believe we will see recession.

“That’s important, because that helps ensure that earnings in the equity market hold up and are supported,” he says.

Murray was speaking at the bi-annual Beyond The Numbers webinar after the August ASX earnings season.

US outlook positive

The outlook for the US economy is an important influence on markets, with concerns growing about the effect of cumulative interest rate rises, ongoing high fiscal deficits, and the uncertainty of the impending elections.

“But I think it is important to keep in mind that the US economy has held up better than pretty much everyone was expecting,” says Murray.

“We have a US Fed that feels they have done the job on inflation, and they have a clear easing bias.”

Murray says financial conditions in the US are easing — as measured by an index of credit spreads, mortgage rates, equity market moves, and currency — indicating the US has already entered a moderate easing cycle.

“The key message here is that even if the US economy turns out to be somewhat weaker, we will see more rate cuts. That will be supportive for equity markets, knowing there is this safety net in terms of much more aggressive easing, if required.”

China structural issues

China, another big influence on Australia’s fortunes, looks more problematic, says Murray.

“The issues in China are structural” as the economy deals with the unwinding of a multi-year property bubble, he says.

“The government has decided that they need to address that, and they continue to avoid stimulating the economy.

“But the trade-off is to what extent those structural issues begin to gather steam and China goes into even lower growth trajectory — or will government policy continue to be able to ensure that we get moderate growth.”

Murray says China has traditionally relied more on investment than consumption and the longer-term hope is that domestic demand becomes a more important driver of growth.

Pendal Focus Australian Share Fund

Now rated at the highest level by Lonsec, Morningstar and Zenith

“We believe that this sort of sluggish growth will continue, but we do also believe that the government [wants] to underpin growth — that they will continue to come through with a series of policy measures that will help prop up growth.

“So, while we remain wary and cautious on China, we do not believe that it’s going to spiral further down.”

That would indicate upside for markets, where investors are pricing in further negative outcomes in China.

Positive market outlook

What does this mean for potential market outcomes?

Murray says the profit season reports showed earnings revisions remain resilient, particularly in industrials, offsetting declines in resource sectors.

Unlike in previous periods of economic weakness, such as the Global Financial Crisis and the pandemic, the monthly rate of earnings revisions for the next twelve months indicates no sign of material economic deterioration.

As a result, Murray says he anticipates positive returns for the ASX over the next 12 months.

About Crispin Murray and the Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia. Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions.

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

Here are the main factors driving the ASX this week according to portfolio manager JIM TAYLOR. Reported by investment specialist Chris Adams

- The call on how big the Fed’s September cut will be is “finely balanced”

- Need to look elsewhere for data, which will shift markets and guide the Fed

- Find out about Pendal Focus Australian Share Fund

- On demand: Crispin Murray’s Beyond the Numbers webinar

SOME elements of the current investment landscape are finely balanced right now.

For example, the US election is anyone’s call at this juncture.

That’s pretty handy, because the market can ignore policies from both sides at the moment – it’s a bridge too far to price anything in.

The call on whether the Fed cuts by 25 or 50 basis point (bps) in September is also finely balanced.

Pricing has been seesawing between a 30% and 60% chance of a 50bps cut. The much-anticipated employment data out of the US last week wasn’t non-consensus enough to move the dial materially outside of these bands.

Comments from the Fed late in the week saw the market finish at the lower end of the 50bps cut probability band.

On the other hand, the toe-to-toe in Australia last week between RBA Governor Michele Bullock and Federal Treasurer Jim Chalmers wasn’t “finely balanced”.

The treasurer pointed fingers at the RBA, which retorted with comments that may not sit very well with the government this close to a federal election.

The S&P/ASX 300 fell 0.66%, while the S&P 500 was off 4.2%.

Resources were trounced (down 6.27%), with red ink across the commodity and equity screens. The outperformance of banks versus resources nearly added another 10% to an already incredibly lop-sided ~50% for the year to date.

Australian reporting season wrapped, with overall downgrades to FY24 earnings-per-share (EPS) of about 3%. Reporting season market volatility was in line with what we have experienced since Covid.

Margin pressure was probably the key call-out from reporting season. A more subdued sales environment means that continued cost pressures are manifesting in negative operating leverage, which is flowing through to pressure on earnings and dividends.

There is some CPI and PPI due this week but the infatuation with inflation has largely run its course, and without any real data on growth, the market may be a bit skittish as we head toward Fed decision time.

US macro and policy

The Fed

Emphasis on the focus shift from inflation to the labour market was evident in several comments from the Fed – probably the last as it moves into black-out mode before the next meeting:

San Francisco Fed President Mary Daly noted the need to cut rates to keep the labour market healthy, highlighting the risk from “a real rate of interest that’s rising into a slowing economy”.

FOMC Board member Christopher Waller said that Friday’s job report showed that the labour market has cooled, but that evidence doesn’t suggest that the economy is in recession or “necessarily headed for one”. He noted that front-loading rate cuts, or cutting in 0.50% increments, could be appropriate if determined “by new data”, suggesting he would need to see subsequent evidence of significant deterioration.

New York Fed President John Williams noted that balance in the labour market and good data on inflation “are telling us it’s time to dial down that restrictiveness” of monetary policy.

Atlanta Fed President Raphael Bostic sounded more cautious, saying that the Fed’s goals of stable prices and full employment are in balance but that he is “not quite prepared” to claim victory on inflation.

Find out about

Pendal Focus

Australian Share Fund

Crispin Murray,

Head of Equities

Economic data

The Institute for Supply Management (ISM) US manufacturing index shrank in August for the fifth consecutive month. At 47.2, it was higher than July’s 46.8 but lower than the 47.5 expected.

New orders – which are watched as an indicator for growth – fell from 47.4 to 44.6, which is an 18-month low. Production, at 44.8, is at a four-year low.

The bottom line is that the manufacturing sector is just not large enough to weigh too heavily on overall GDP, and so remains a small headwind to production and employment as it has been for a few years now.

We need to look elsewhere for economic data, which will shift markets and guide the Fed.

The ISM Services index rose from 57.0 in July to 57.3 in August and continues to suggest moderating inflation in underlying services over the next few months.

Employment

There was a raft of datapoints which generally underpinned the notion of a softer labour market:

- Friday’s August non-farm payrolls were keenly anticipated and rose 142k versus a consensus expectation of 165k. Net revisions to previous readings were down 86k.

- The unemployment rate fell from 4.3% in July to 4.2% in August, which was in line with expectations. The three-month average is now 0.54% above the trailing 12-month average, rising from 0.49% in July and leaving the Sahm Rule of recession still triggered.

- Average hourly earnings rose 0.4%, the biggest gain in seven months and ahead of 0.3% expectations, driven by the service sector. It is now running at 3.8% year-on-year, up from 3.6% in July, and while the Fed focuses more on the employment cost index (ECI) than average hourly earnings, this bears watching.

- Earlier in the week we saw the ADP Employment Report, which rose 99k in August versus 141k expected. July was revised down from 122k to 111k. Private job creation slowed for the fifth consecutive month and was the lowest since January 2021.

- The bulk of new jobs were in construction, education and health services, and financial activities. There were declines in manufacturing, information and professional/business services.

• July job openings, measured by JOLTS, came in at 7.67m versus 8.10m expected, falling to the lowest level since January 2021. The number of vacancies per unemployed worker is now at 1.1x, the lowest level in three years and almost half the peak of 2.0x in early 2022. - Finally, initial jobless claims came in at 227k versus the 230k expected and the previous week was revised up from 231k to 232k. Continuing claims were 1,838k versus the 1,868k expected and the previous week was revised down from 1,868k to 1,860k.

Australia macro and policy

Federal Treasurer Chalmers noted that while he and the RBA Governor have different responsibilities, they are both focused on getting “on top of this inflation challenge in our economy without making life harder for people or smashing an economy, which is already weak enough”.

In contrast, Governor Bullock observed that “if the economy evolves broadly as anticipated, the Board does not expect that it will be in a position to cut rates in the near term” and that “full employment is not served by letting inflation stay above target indefinitely”.

She noted that younger and lower-income households have been particularly affected by cost-of-living pressures given tighter budgets.

On the data front, GDP increased by 0.22% in Q2 2024, which was largely as expected, and decelerated by 0.30% to 0.97% year-on-year, which was the weakest in 32 years barring the pandemic. Furthermore:

- Domestic demand rose 0.20% for the quarter and 1.5% for the year. Private demand remained constant at 0.8% year-on-year while public demand rose 0.8% for the quarter to 3.5% for the year. Public demand as a proportion of the economy is now 28%, which is the highest ever level (again, barring the pandemic).

- Net exports (up 0.20%) and inventories (down 0.30%) largely offset each other.

- Household consumption fell 0.20% in the quarter and rose 0.50% for the year. This was the largest quarterly decline (ex-Covid) since the GFC, with the Australian Bureau of Statistics suggesting that the “Taylor Swift” effect of the March quarter may have contributed to the decline. The RBA was expecting 1.1% year-on-year growth. Transport fell 4.4% for the quarter, while hospitality (down 1.5%) and clothing (down 2.6%) were also weak. Gains came in household goods (4.0%), utilities (2.4%) and education (1.2%).

Elsewhere, CoreLogic noted that its rent index was unchanged in August for the second straight month.

- The national annual growth trend was 7.2%, the lowest rate since May 2021.

- Rent values in Sydney declined for a second consecutive month.

Australian reporting season wrap-up

Earnings misses (38% of the market) outnumbered beats (32%), with the ratio of 0.8x ratio of beats to misses well below the long-term average of 1.4x.

Disappointments were driven more by margin, as revenues were largely in line with expectations.

At an aggregate level, ASX 200 FY24 EPS Growth was down 4.6%, which was in line with consensus and a second straight year of falling profits for the index.

Sales growth for the average firm slowed to 6.4% from 8.9% in the prior comparable period, but stickier costs (particularly wages) continued to put pressure on profitability – with margins now back in line with long-run averages.

Dividends fell 1.9% but, at 3.6%, were notably higher than forecast thanks to rising payout ratios and a number of special dividends from retailers such as Woolworths, JB Hi-Fi and Super Retail Group.

At an index level, small caps fared worse – 45% of small caps missed expectations versus 31% of large caps, and earnings revision trends have been twice as negative.

- Outlook commentary was generally cautious, with earnings revision trends weaker than normal:

- ASX 200 FY25 EPS growth has been cut from 3.7% to 0.4%, putting in play a third-straight year of negative growth for the index.

- Across Industrial firms, FY25 EPS was cut by 3%, nearly twice the long-run average and now standing at 4.4% (7.0% ex-banks). While revenue forecasts were trimmed, the bigger driver of downgrades was margins given companies are continuing to struggle to pass on higher costs.

- Downgrades were broad-based, but larger in cyclical sectors such as steel, gold, media, energy and mining. Of the more defensive sectors, healthcare continued its recent run of negative earnings momentum.

- Banks was the only sector to see net upgrades, driven by better net interest margins, albeit to only flat earnings for FY25 and despite highlighting some concerns around deteriorating asset quality.

Stock volatility in response to earnings was lower than the past two reporting seasons but remained elevated versus the pre-Covid era.

About Jim Taylor and Pendal Focus Australian Share Fund

Drawing on more than 25 years of experience investing in top-performing Australian companies and a background in accounting, Jim manages our Long/Short Fund and co-manages our Imputation Fund. He is a Chartered Accountant with membership of the Australian Institute of Chartered Accountants.

Pendal Focus Australian Share Fund is managed by Crispin Murray. The fund has beaten its benchmark in 14 years of its 18-year history (after fees), across a range of market conditions. Find out more about Pendal Focus Australian Share Fund here.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.