Today’s inflation numbers mean the rate-cut window is open in Australia from early next year. Pendal’s head of government bond strategies, TIM HEXT, explains why

- Two easings expected in February and May

- Why bonds, why now? Pendal’s income and fixed interest experts explain

- Browse Pendal’s fixed interest funds

TODAY’S 1% quarterly CPI number would not normally be cause for celebration. After all, that’s 4% annualised – above the RBA target.

But the RBA focuses more on trimmed-mean inflation to avoid high and low swing items like petrol and food.

On this measure, the Q2 CPI number was 0.8% – still not quite in the target band, but comfortably heading that way.

Calls for rate hikes are off, the RBA can again be patient and the inflation picture should improve into year end.

Markets liked it. At the time of writing three-year bonds had fallen from 3.95% to 3.73%.

RBA governor Michele Bullock can avoid the wrath of the government and Anthony Albanese can return to selling his pre-election cost-of-living relief without a rate hike spoiling it.

Key items in the CPI: 1% headline (1% forecast) for Q2

We already had two-thirds of the items from the monthly CPI in April and May, so the headline was no surprise.

There was remarkable consistency across key areas, as food, housing, transport and insurance all went up around 1%.

In the context of these recent moves, housing and insurance were lower than previous outcomes, though there were some seasonal elements for insurance.

Health was up 1.5% as medical and hospital services grew at 2%. This is more structural and recent battles between providers and health insurance show the strains in this sector.

Tobacco was up 3% on tax indexation, which alone added almost 0.1% to CPI. International travel was up 8%, though domestic travel partly offset that – down 5%.

Trimmed (underlying) inflation 0.8% (forecast 1%) – why the forecasting miss?

Given the headline number came in as expected, why did economists miss the trimmed number, which came in at 0.8%?

At the risk of losing readers’ interest, this gets into how “trimmed-mean inflation” works.

Basically, the RBA (or ABS these days) lines up every item from highest to lowest change – weighted for its contribution to the index – and cuts off the top and bottom 15%.

That is, 30% of weighted items are trimmed.

Petrol is nearly always trimmed (it’s 3% of the CPI weight), as are many food and non-alcoholic items (a combined 17% weight).

Volatility in travel prices means they are generally trimmed these days (6% of weight).

This still leaves around 5-10% of weighted items to be trimmed and the extent of their movements feeds back into the trimmed mean.

If I’ve lost you, find your resident mathematician – there’s generally one around in finance.

Rate hikes off, rate cuts on – but not till 2025 despite a potential flat headline CPI in Q3

The RBA releases its forecasts every quarter at its early February, May, August and November meetings.

Given the lack of any guidance from the RBA these days, these forecasts are important.

In May, the RBA expected trimmed mean inflation to be 0.8% in Q2, so it will be pleased with today’s result. The inflation scares from the monthly April and May numbers, which Bullock felt the need to acknowledge at the June RBA meeting, have passed.

When we get the new set of forecasts next week, we think headline CPI will be forecast at 3.2% for year end – down from 3.8% due to electricity subsidies announced in recent Federal and State budgets.

Trimmed mean inflation, however, will likely only be revised down from 3.4% to 3.2%.

That is, trimmed mean inflation will still likely be too high for a rate cut this year, though there should be some probability priced.

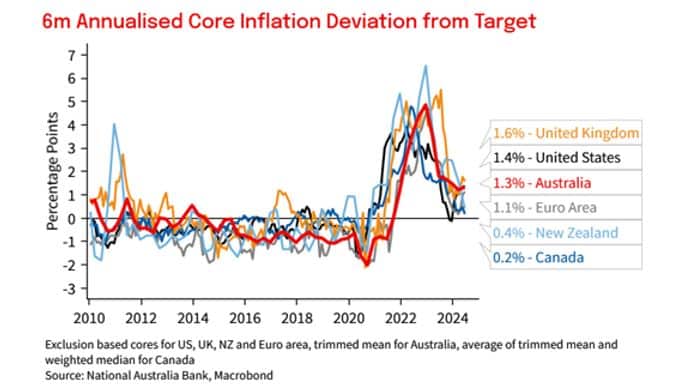

Global factors eventually win over

Here is an interesting chart (courtesy of NAB) on how much higher CPI is than target across key countries.

Inflation is measured on a six-month annualised basis (six months times two) to measure the current pulse more closely. All countries are still over target, but most are either cutting or about to cut.

Australia will be no different.

Looking ahead

Rate cuts globally, better behaved wages, sluggish growth, rising unemployment, and falling oil prices should see the rate cut window open in February 2025.

In Australia, we expect two easings in February and May next year, and six easings in the US by mid-next year.

That’s the RBA at 3.85% and the Fed at 4% by June.

From there, we think the risk is for further cuts, but our confidence is lower.

All this is positive for bonds and real yields. We think Australian ten-year bonds will trade down to 3.75% in the months ahead, before settling down in a 3.5% to 4% range early next year.

About Tim Hext and Pendal’s Income & Fixed Interest boutique

Tim Hext is a Pendal portfolio manager and head of government bond strategies in our Income and Fixed Interest team.

Tim has extensive experience in banking, financial markets and funding including senior positions with NSW Treasury Corporation (TCorp), Westpac Treasury, Commonwealth Bank of Australia, Deutsche Bank, Bain & Co and Swiss Bank Corporation.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia.

Find out more about Pendal’s fixed interest strategies here

About Pendal

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

In 2023, Pendal became part of Perpetual Limited (ASX:PPT), bringing together two of Australia’s most respected active asset management brands to create a global leader in multi-boutique asset management with autonomous, world-class investment capabilities and a growing leadership position in ESG.

Here are the main factors driving the ASX this week according to Pendal investment analyst ANTHONY MORAN. Reported by portfolio specialist Chris Adams

- The small-cap Russell 2000 gained 3.47% while the NASDAQ fell

- Microsoft, Meta, Apple and Amazon all report this week

- We remain constructive on the medium-term market outlook

- Find out about Pendal Focus Australian Share fund

A CONTINING reversal in global asset markets was the main story last week as hedge fund “de-grossing” of equity exposure led to a broader risk reduction among investors.

This prompted underperformance among large caps and ongoing sector rotations.

The S&P 500 fell 0.82% and the S&P/ASX 300 was down 0.65%. The NASDAQ retreated 2.08%, while the small-cap Russell 2000 gained 3.47%.

Limited economic data tended to maintain support for the soft-landing thesis.

It was a busy week for offshore quarterly results, which reinforced the sell-off in Mag7 stocks and reflected an overall challenging top-line environment for many industries.

We remain constructive on the medium-term market outlook given resilient economic growth and easing inflationary pressures.

But the reversal in market momentum may persist given the stretched positioning and the low likelihood of a positive circuit breaker, with a rate cut from the US Federal Reserve not expected until September.

Market reversal and rotation continues into its second week

Market action was dominated by continued de-grossing and the reversal of previously winning crowded trades originally triggered by June’s softer inflation print.

The Mag7 have had an outsized impact on these trends, with Alphabet down 6% and Tesla down 8% for the week.

The rotation into small caps continued in the US but not in Australia, where weakness in commodities has had an influence.

The sell-off appears to be entering a self-fulfilling phase, with investor sentiment becoming much less bullish and VIX (an index of equity market volatility) picking up.

What was initially a rapid resetting of positions by hedge funds has led to a broader number of investors reducing their risk in response to the pullback.

This has also spread beyond equity markets with reversals seen elsewhere, including the JPY/USD cross, metals and commodities, and even gold.

The pullback and rotation may persist, given that a Fed rate cut is unlikely in August (giving us two months until the policy catalyst of a September cut) and quarterly earnings results seem to be reinforcing some of the dynamics – in particular, Mag7 disappointment.

In addition, positioning still has room to unwind and liquidity conditions are tougher. We note:

- commodity trading adviser (CTA) accounts – which are systematic strategies – still have a very long positioning in equities

- equity markets have pulled back but are still a long way from oversold

- the VIX has increased but remains well below the level of recent selloffs. The second half of calendar years have historically had more volatility and greater drawdown risk.

Given the likelihood that current trends persist, we have slightly reduced our exposures to some of our year-to-date winners.

However, this episode is also offering an opportunity to lighten up in companies where stock-specific fundamentals are deteriorating but are benefiting from the macro-driven rotation.

US macro: a soft landing with some downside risk

June’s US Personal Consumption Expenditures (PCE) Deflator was the week’s most important data point, given its role as an input for the Fed’s decision making.

The PCE deflator was up 0.2% month-on-month, which was in line with consensus. This saw the three-month annualised rate at 2.3% and the year-on-year rate at 2.6%. It further de-risks the prospect of a rate cut in September and also triggered a US share market rally on Friday.

The in-line PCE deflator offset a hotter Core PCE release (up 2.9% versus the 2.0% expected) from earlier in the week, which was released along with better-than-expected US Q2 GDP figures (up 2.8% versus the 2.0% expected).

The GDP data supported the view that the US economy remains resilient overall, which is constructive for the market.

Key drivers of the GDP beat were government spending (up 3.6%) and a build in inventories.

Non-residential fixed investment was also a little stronger, driven by an 11.6% rise in spending on equipment. Weakness in durable goods orders and capex intentions surveys suggests this boost is unlikely to be sustained.

Elsewhere, we saw weaker-than-expected new and existing home sales.

The University of Michigan consumer sentiment survey was in line with expectations but also the weakest reading since November 23.

Durable goods orders and the Richmond Fed manufacturing index were also weak, which comes at a time when investment in new factories in the US is at a record high in response to onshoring.

The upshot is that a slowing, but not concerning economic outlook and easing inflation provides support for rate cuts without requiring a material cut to earnings expectations.

When looking beyond the short-term momentum reversal, this should be supportive to equity markets.

Pendal Focus Australian Share Fund

Now rated at the highest level by Lonsec, Morningstar and Zenith

US quarterly reporting: exacerbating negative momentum for market leaders

As we reach one third of the way through US reporting season, earnings have so far beat expectations by 4% in aggregate, driven by margin.

Mag7 share price weakness was boosted by disappointing results.Tesla was down heavily after missing earnings due to price cuts hurting margins.

Alphabetalso sold off despite beating on earnings, as the market decided it was time to start questioning the return on investment on AI spending. Alphabet’s top-line growth in YouTube and Google is slowing sequentially but its capex is up dramatically (up 91% year-over-year).

Microsoft, Meta, Apple and Amazon all report this week.

Staples are showing that the reversal of post-Covid price increases is playing out as hoped, with Unilever and Nestle showing slowing prices but volume growth accelerating in Q224 (after a year of volume declines).

This is supportive of deflationary dynamics globally, taking pressure off the consumer, and is relevant for stocks like Brambles, Amcor, and Orora in our market.

We are also seeing the trade-off of lower prices for higher volume play out in other sectors, including automakers, packaging and homebuilders.

Consumer-exposed stocks are generally seeing softer demand, but in many cases at a slower rate than in Q1. Luxury stocks (e.g. Kering, LVMH) were sold off as a China recovery failed to materialise and the global recovery in luxury spending was pushed out.

Visa also highlighted some weakness in lower income cohorts.

This all suggests that stocks that are more positioned for volume growth, rather than price/revenue, are likely to be relative outperformers.

Any stock that has benefitted quite a lot from higher prices over the past few years probably has margin risk because the slower consumer environment makes it hard to hold price.

Commodities

Slowing macro conditions and no real positive news for China from the Plenum saw another week of declines for commodities, which dragged on the Australian market.

With the Chinese property market continuing to weaken despite policy measures, dragging consumer sentiment and consumption down, the market was hoping for some material policy moves from the Plenum.

These did not eventuate, barring a tiny cut in interest rates, and saw commodity prices continue to slide during the week.

A weak property sector, a soft consumer and declining infrastructure spend means Beijing is increasingly relying on exports and “green” investment to drive economic growth.

This is driving deflation in many global categories, including steel, solar cells, batteries and EVs.

Resources have generally been poor performers this month, but the lack of a catalyst for change in China demand leaves them with poor fundamentals.

The sector may see short-term rallies if the sector/commodity is oversold, but it seems there is a low likelihood of sustained outperformance.

This is arguably a positive for the banks as a “last man standing” among the ASX big-cap sectors.

Commodities

Few sectors were spared declines last week.

Energy (down 5.57%) did the worst after Woodside’s (WDS) poorly received acquisition.

Defensives such as Healthcare (up 0.08%) and Financials (up 0.32%) were the only places to hide.

In contrast to the US, Australian small caps continued to underperform large caps.

At a stock level, the largest underperformers tended to be resources stocks given declining commodity prices and some poor quarterlies, as well as weakness in growth year-to-date winners including Goodman (GMG), Block (SQ2) and NextDC (NXT).

Financials had a good week outside of the big four banks, as did a range of defensives.

About Anthony Moran

Anthony Moran is an analyst with over 15 years of experience covering a range of Australian and international sectors. His sector coverage has included Australian Industrials and Energy, Building Materials, Capital Goods, Engineering & Construction, Transport, Telcos, REITs, Utilities and Infrastructure.

He has previously worked as an equity analyst for AllianceBernstein and Macquarie Group, spending a further two years as a management consultant at Port Jackson Partners and two years as an institutional research sales executive with Deutsche Bank.

Anthony is a CFA Charterholder and holds bachelor’s degrees in Commerce and Law from the University of Sydney.

What a rate hike could mean for bonds and equities | What a Trump presidency might mean for investors | Interpreting emerging markets drivers

Here are the main factors driving the ASX this week, according to Aussie equities analyst and portfolio manager ELISE MCKAY. Reported by portfolio specialist Chris Adams

- Markets are pricing in a 22% chance of an RBA hike in August

- ‘Substantial’ market moves saw small caps (+1.7%) outperform last week

- Copper was down 8% and near-term downside risks remain

- Find out about Pendal Focus Australian Share fund

THE market saw big moves last week, driven by a collision of shifting central bank expectations, an improved growth outlook, overbought technicals, rotational pressures, and increased odds of a second Trump presidency.

While the S&P 500 was down 1.95%, there were some violent rotations within the market that led to leadership completely reversing.

Most stark was the outperformance of small caps, with the Russell 2000 up 1.73% for the week and the mega-cap tech-heavy NASDAQ down 3.65%.

This move was fundamentally driven, with small caps benefiting from economic sensitivity to lower rates and tariff protection. But it was exacerbated by extreme market positioning, as systematic investment strategies moved rapidly to close shorts and go max long.

From here, the near-term risk of a market wobble is more elevated given we face a seasonally weak period of the year, the Fed’s first cut is still two months away, and the US presidential election is not until 5 November.

Earnings expectations are high and there is plenty more data yet to drop, which could threaten the soft-landing thesis near term.

But the longer-term bull market remains intact, and in our view, a market consolidation could present a buying opportunity.

We continue to position the funds for a wide range of potential market scenarios.

Globally, we should see a coordinated central bank cutting cycle, with Australia remaining the exception.

Here, the S&P/ASX 300 gained 0.13% last week.

Domestic employment rose by a solid 50k month-on-month in June, well ahead of expectations for 20k. But despite this increase, the unemployment rate also rose from 4.0% to 4.1%, with the labour force participation rate increasing from 66.8% to 66.9%.

This print suggests that demand for labour is not quite keeping up with labour supply. Conditions are slowly softening but remain tight overall relative to full employment.

This is consistent with the view presented by the RBA in June’s meeting minutes.

The Q2 Consumer Price Index (CPI) data out on 31 July is likely to play a key role in the RBA’s decision on whether to raise or leave rates on hold.

The market is pricing in 22% chance of a hike in August.

Meanwhile, the Chinese Communist Party held a largely anticlimactic Third Plenum of the current Congress, which is traditionally focused on economic reform.

While leadership appears increasingly concerned about near-term economic weakness – with Q2 GDP decelerating from 5.3% to 4.7% versus CY24 targeted growth of 5% – there has been no meaningful step up in stimulus efforts.

This remains a headwind for resource stocks.

Finally, an update from Crowdstrike crash millions of computers globally on Friday. We are not expecting meaningful exposure for portfolio holdings.

US politics

It was a busy week for US politics, with the Trump assassination attempt and pressure heaped on Biden, which culminated in him stepping aside over the weekend.

This has meaningful policy and market implications, with a variety of outcomes still ahead.

The Trump assassination attempt increased odds of him winning the election.

Pollster 538 is forecasting a 51% probability of Trump winning compared to about 40% back in April, while the odds have increased to 63% for a Trump victory based on PredictIT data.

The chances of a Republican sweep also looks more probable, which could result in a meaningful change in policy direction.

Trump’s big three macro ideas of higher tariffs, lower immigration and tax cuts point to lower growth and higher inflation. This is a negative read-through for Aussie resources.

We could also see significant sector-specific policy changes ,including a boost for traditional energy providers, some negative moves for EVs, and financials potentially benefiting from an easing regulatory regime.

The consequences for healthcare and big tech are mixed but may be good for emerging Trump supporters, like Elon Musk.

US macro

Last week saw the release of several macro data points, which further supported the view of a soft landing and the increased expectation of a first rate cut in September, first stoked by lower CPI print the week before.

Retail sales

Retail sales data was well ahead of expectations for June and also saw May revised up.

Headline sales were flat month-on-month in June versus consensus expectations of -0.3% and May was revised up 20 basis points (bps) to +0.3%.

Control-group sales, which excludes autos, gas, building materials and restaurants, were also well ahead of expectations at +0.9% month-on-month versus consensus at +0.2%.

Strength was broad across all categories, with the exception of motor vehicle sales (-2%) due to a cyberattack on auto dealers which prevented the finalisation of some sales.

This data suggests that the US consumer is holding up pretty well – even showing signs of recovering – and is supportive of overall growth.

On the other hand, it was also the second hottest June since 1895, which may have contributed to strength in goods sales like building materials, garden equipment and hardware.

This means we need another month or two of data to show a clear trend, though there was enough to suggest nascent signs of recovery for the US consumer are emerging. This is positive for discretionary retail and payments companies such as Block (SQ2).

Further signs of recovery were seen in the housing starts data, with homebuilders buoyed by the tentative signs of recovery.

Housing starts

Housing starts rose to 1,353k in June which is up 3% month-on-month and 4% ahead of consensus expectations.

Building permits rose to 1,446k, up 3% month-on-month versus flat expectations.

The recovery is coming from multi-family housing. Conversely, single family homes remain under significant pressure – a trend that is expected to continue with the inventory of new single-family homes for sale relative to current sales well above the long-term average.

We saw a decent step up in the AtlantaFed’s GDDNow forecast from 2.0% to 2.7% as at 17 July, reflecting the stronger retail sales and housing starts data from the week.

Unemployment claims

Initial claims rose from 223k to 243k, well ahead of 229k consensus expectations.

The step-up is largely attributed to the combination of auto plant shutdowns being more concentrated than normal, as well as the disruption caused by Hurricane Beryl.

Despite this, claims are gradually trending up and is a leading indicator of the unemployment rate which should rise over the following twelve months. This is supportive for Fed cutting.

Find out about

Pendal Focus

Australian Share Fund

Crispin Murray,

Head of Equities

Europe and the UK

UK CPI inflation came in a touch ahead of expectations at 2% headline (0.1% beat) and 3.5% core for June 2024.

While headline inflation is in line with the Bank of England’s (BoE) target of 2%, services inflation is proving sticky at 5.7% – that’s well ahead of the latest BoE projections, which expect 5.1% in June 24.

The Taylor Swift effect does appear to have weighed, with restaurant and hotels accelerating from 1.7% in June 2023 to 8.8% in June 2024 – a pace that seems unlikely to be sustained through the remainder of 2024.

UK employment data was also released, with three-month average private sector regular pay growth decelerating from 5.8% in April to 5.6% in May.

However, there was a significant step down in monthly data from 5.9% in April to 4.9% in May, which was weaker than expected.

The unemployment rate was unchanged at 4.4%, in line with expectations.

The two offsetting data releases should mean that the BoE’s August meeting remains in play for its first cut, but it is a close call.

As expected, the European Central Bank (ECB) kept rates unchanged at 3.75%.

While not making a commitment on whether it will cut for the second time in September, the statement was more dovish than feared following recent sticky services inflation.

The ECB downgraded its view of the Eurozone’s economic prospects, with risks to growth now “tilted to the downside”.

Australia

Employment rose by 50k month-on-month in June, well ahead of expectations for 20k.

However, despite this increase the unemployment rate also rose from 4.0% to 4.1% (in line with expectations), with the participation rate increasing from 66.8% to 66.9%.

Only 12.5% of people took annual leave in June, versus the pre-Covid average of 14.5% – contributing to a 0.8% lift in hours worked, versus declines in May and in April.

This suggests that labour demand is not quite keeping up with labour supply.

Leading indicators of labour demand (e.g. job ads, employment intentions and vacancies) have continued to show signs of deterioration.

Conditions are slowly softening but remain fairly tight overall relative to full employment, which is consistent with the view presented by the RBA in June’s meeting minutes.

With the August meeting expected to be live, the Q2 CPI data out on 31 July is more likely to play a key role in the RBA’s decision on whether to raise or leave rates on hold.

The market is pricing in 22% chance of a hike in August.

Australia is an outlier compared with the rest of the world (excl. Japan) who have either started cutting rates or expect to do so soon.

While the Aussie dollar bounced earlier in July, reflecting this dynamic, the market is questioning if the RBA has the gumption to raise rates when expectations for a first cut in the US are being brought forward, which has reversed most of the currency’s move.

Should we see the Aussie dollar resume its march higher, this raises an issue for USD earners like Brambles (BXB), ResMed (RMD) and CSL (CSL).

China

The Chinese Communist Party held its third Plenum of the current Congress, concluding with a brief communique and press conference on Friday, and more complete briefings expected over the coming days.

While there were no surprises on the long-term targets, the Plenum discussed near-term issues – an unusual move that signals a sense of urgency on addressing economic weakness and suggests incremental stimulus is on its way.

Economic weakness was on display in the disappointing Q2 GDP growth reported at the start of the week, slowing from 5.3% to 4.7%.

The average is in line with 5.0% target for CY24, but the quarter-on-quarter pace of deceleration is concerning.

Weak domestic demand and no signs of property improving puts the 5% target for 2H24 at risk.

As a result, it is likely more policy easing could be announced at the Politburo meeting at the end of this month.

Combined with the fear that a Trump presidency could increase tariffs on China (noting prior comments from Trump floating a 60% tax on products from China), commodities did not have a great week.

While seemingly unlikely, an across-the-board 60% tariff from US could be a cumulative 2% GDP drag over several quarters, according to Goldman Sachs estimates.

Copper legged down 8% on the week and the miners followed.

Though the copper bulls argue that the set up for supply deficits is a sure thing post-2025, the market is currently in surplus, inventories are building at the London Metal Exchange, and China demand remains a headwind – suggesting there is further risk to the downside over the near term.

Find out about

Pendal Smaller

Companies Fund

IT outages

Computers across the globe started displaying the “Blue Screen of Death” on Friday, with an update from Crowdstrike causing outages for millions of Microsoft Windows device users.

The outages touched almost every industry, from financial institutions through to airlines – with about 1,400 flights disrupted globally on Friday. Qantas (QAN) appeared to be back online relatively quickly.

The disruption was caused by a software update (not a hacking issue) pushed via Falcon, a cybersecurity monitoring service, to client computers.

While the change has now been undone, clients are required to perform a manual workaround to download a fix to affected computers.

We don’t expect this to have meaningful insurance implications.

Most cyber policies are designed to cover cyberattacks/security breaches and are therefore unlikely to cover this incident. On the Business Interruption side, most policies typically have a 45-day clause before they start paying out.

Markets

Last week saw substantial moves within the S&P 500, catalysed by a shift in Fed expectations, earnings hits and misses, overbought technicals, rotational pressures, and increased odds of a second Trump presidency and Republican sweep.

This completely upended the CY24 year-to-date patterns of very strong headline returns, very low realised volatility, and steady factor and thematic trends.

Small caps were, by far, the strongest performer – up 1.7% for the week and 7.6% month-to-date.

There is a strong fundamental case for strength in small caps continuing:

- Decelerating inflation and expectations for a first Fed cut brought forward to September. Approximately 49% of Russell 2000 debt is floating, compared to ~9% for S&P500.

- Steady/improving economic growth.

- Increased likelihood of a Republican election sweep, though a lot can change between now and 5 November. Small caps are typically more domestic facing, less vulnerable to tariffs and very levered to US economic growth. They performed strongly following Trump’s 2016 election.

- Compressing earnings growth premium for the largest tech companies versus the rest of the index. Collectively, Microsoft, Nvidia, Amazon, Aphabet and Meta are expected to grow 37% in CY24 versus 5% for the S&P 500 median – a 32% spread. But this is expected to compress to a 9% spread in CY25 and 5% spread in CY26, with the largest companies growing EPS at slowing rates while the rest of the index accelerates.

The rotation was exacerbated by extreme positioning versus history and the need to close out shorts related to a slowing economy.

This resulted in a period of de-grossing, with hedge funds aggressively unwinding risk across both the long and short sides of books and at the fastest pace since January 2021. Tech, Financials, Consumer Discretionary and Healthcare saw the most notional de-grossing activity.

The combination of strengthening fundamentals and extreme positioning led to some violent rotations within the market.

Small caps, homebuilders, financials and REITs rose quickly – as key beneficiaries of lower rates – funded by previous winners in AI, GLP and copper.

Market breadth increased, but not as much as might have been expected, which raises some questions as to the strength of this rally.

Market dispersion is picking up, albeit still below the 30-year average – suggesting a more selective, stock-pickers market heading into reporting season.

Factor rotation has been sudden and meaningful, with most of the year’s underperformers rallying hard. Therefore, we are being presented with an opportunity to take risk off the table for any names with near-term downgrade risk.

We are heading into a seasonally weak period, with August and September usually the softest two months of the year.

Systematic strategy positioning remains elevated, with commodity trading adviser (CTA) equity positioning remaining near highs. CTAs have moved from net short to now max long the Russell 2000, with the signal to trim at about 6% lower than current levels.

While the structural AI thesis remains intact, the likes of Microsoft (30 July) and Nvidia (28 August) can’t afford to miss earnings expectations.

Historically, a pull-back in momentum stocks (i.e. AI basket) is usually recovered within the following six-to-twelve months as the longer-term structural thesis plays out. But near-term historical returns could support the argument for taking some profits here.

Though it is still early days, US Q2 2024 results so far have been relatively good, with 14% of the market cap having reported and – on average – surprising on sales (up 1.8%) and earnings (up 5%).

There is a big week ahead, with 29% of the S&P market cap reporting, including Tesla and Alphabet kicking off the Magnificent 7. The bar for Q2 earnings is pretty high.

So, while much of the move over the past week has been technical (e.g. forced hedge fund de-grossing and CTA buying in the Russell 2000) and arguably overextended, the risk is elevated for a broader market wobble as we enter the seasonally weakest period of the year, as the Fed’s first cut is still two months away, and as the US election is not until 5November.

Earnings expectations are high and there is plenty more data to drop ,which could threaten the soft-landing thesis near term.

But – as discussed earlier – the longer-term bull market remains intact and a market wobble should present a buying opportunity. We continue to position the funds for a wide range of potential market scenarios.

About Elise McKay and Pendal Australian share funds

Elise is an investment analyst and portfolio manager with Pendal’s Australian equities team. Elise previously worked as an investment analyst for US fund manager Cartica where she covered a variety of emerging market companies.

She has also worked in investment banking and corporate finance at JP Morgan and Ernst & Young.

Pendal Horizon Sustainable Australian Share Fund is a concentrated portfolio aligned with the transition to a more sustainable, future economy.

Pendal Focus Australian Share Fund is a high-conviction equity fund with a 16-year track record of strong performance in a range of market conditions. The Fund is rated at the highest level by Lonsec, Morningstar and Zenith.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Here are the main factors driving the ASX this week according to portfolio manager JIM TAYLOR. Reported by investment specialist Chris Adams

- Find out about Pendal Focus Australian Share Fund

- On-demand: tune into Crispin Murray’s bi-annual Beyond the Numbers webinar

TESTIMONY on Capitol Hill from Federal Reserve Chairman Jerome Powell emphasised that he is cognisant of the risk of keeping policy too restrictive for too long.

“Elevated inflation is not the only risk we face,” he said on Tuesday.

“We’ve seen that the labour market has cooled really significantly across so many measures.

“It’s not a source of broad inflationary pressures for the economy now.”

The market took this acknowledgement of both the up and downside risks of current policy settings positively, with the S&P 500 gaining 0.89%. The S&P/ASX 300 was up 1.75%.

A dovish Consumer Price Index (CPI) print in the US, following a string of weaker economic data over the last few weeks, increased expectations of a first rate cut in September.

This led to a sharp rotation in equities away from the mega-cap tech stocks, which have dominated year to date, to small and mid caps, cyclicals, value stocks and rate sensitives.

While the headline returns in the equity indices were modest, a broadening of market leadership is very healthy.

Bonds rallied, with US ten-year government yields dropping 10 basis points (bps) to 4.28%. Commodities were weaker across the board.

Aside from the market-moving US CPI data, there was very little news flow from an economic or company-specific perspective.

US reporting season has just kicked off, with about 5% of S&P 500 companies having reported, while Australian reporting season is still a few weeks away.

US macro and policy

The Fed

The doveish tilt seen in Powell’s semi-annual Monetary Policy Testimony reassured the market, laying the foundation for the move in response to softer CPI data on Thursday night.

His commentary was very much in line with the June FOMC statement and repeated some phrases from it.

He noted that the labour market is “strong” with the caveat that it was “not overheated.”

The economy was continuing to expand “at a solid pace” and recent monthly inflation readings have shown “modest further progress”.

He kept well away from using language that would allow him to be pinned down in terms of any indication of when easing may commence – repeatedly observing that “more good data” would boost the Committee’s confidence that inflation is moving sustainably toward 2%.

Interestingly, he observed that “elevated inflation is not the only risk we face”.

Reducing policy restraint too little or too late could unduly weaken economic activity and employment, and Powell said the Fed has “seen considerable softening.”

This indicates that the central bank is fretting a bit more about the potential costs of waiting too long to ease, though he did warn that reducing rates too soon could “stall or even reverse the progress we have seen on inflation”.

Eyes now turn to the Jackson Hole symposium, held between 22-24 August.

This could be an ideal opportunity for Powell to give customary notice of an impending policy change. He will have one more employment report and two CPI reports in hand by then.

The market-implied chance of a rate cut in September now sits at 92%.

June CPI

Headline CPI was down 0.06% month-on-month in June, versus consensus expectations of a 0.1% lift and the 0.01% increase in May. It now sits up 2.97% year-on-year, versus the 3.10% expected and the 3.25% seen in May.

The Core CI rose 0.06%, versus a 0.16% lift in May and the 0.2% increase expected. It is up 3.27% year-on-year, versus the 3.40% expected and seen in the previous month.

The Core-core Services Index – which excludes airline fares, auto repairs and insurance, health insurance, hospital services, and accommodation services components from the core services ex-rents measure – rose by just 0.2%.

Core Goods prices fell by 0.1%, driven by a hefty 1.5% drop in used car prices and a 0.2% decline in new motor vehicle prices, making it the fifth straight drop.

Core Goods ex-Auto prices rose by just 0.1%, driven by a 0.5% jump in prices for household furnishings, but the trend still looks flat.

Primary rent increased by only 0.26%, while Owners’ Equivalent Rent rose by 0.27%, both the smallest increases since April 2021.

These components have averaged 0.40% and 0.46%, respectively, for the first five months of 2024.

Zillow data for new rents have been signalling for some time that the run-rate of the whole-market CPI primary rent would slow – and it is finally starting to show up in the data.

Producer Price Index (PPI)

The 0.2% month-on-month increase in the headline PPI took a little shine off the earlier CPI data, given consensus expectations of 0.1%, though the market’s reaction was muted. Net revisions were 0.2%.

The Core PPI rose 0.4%, versus consensus at 0.2%. Net revisions also were 0.2%.

The miss was driven, in part, by the notoriously volatile airfare and vehicle margins components of trade services, so the market was content to take this in its stride.

The Core ex-Trade Services measure was unchanged at 0.2%, below consensus expectations.

Core Goods prices also were unchanged despite the recent increase in the cost of shipping for imports.

Last week’s CPI and PPI data suggests that the core PCE deflator – the Fed’s preferred inflation measure – rose by just 0.15% in June, helping to reduce the quarter-on-quarter annualised growth rate to 2.7% in Q2 from 3.7% in Q1.

Other data

- There were 222k initial jobless claims for the week ended 6 July, down from 239k the previous week.

- Continuing claims came in at 1,852k for the week ended 19 June, versus a forecast of 1,855k.

- The New York Fed Survey of Consumer Expectations showed one-year inflation expectations down 0.2% month-on-month to 3.0%, though three-year expectations rose 0.1% to 2.9%. Five-year inflation expectations fell 0.2% month-on-month to 2.8%.

- Finally, the NFIB survey suggests we are seeing increased pushback from consumers to higher prices, with 27% of small business raising prices, down from a peak of over 60%. However, the ability to raise prices still remains elevated versus pre-pandemic levels, where this measure was running at about 10%.

Find out about

Pendal Focus

Australian Share Fund

Crispin Murray,

Head of Equities

Macro and policy in Australia and NZ

Westpac consumer sentiment suggests the prospect of further rate rises increasing mortgage rates has permeated the Australian populace.

The survey fell 1.1% month-on-month to 82.7% in July – driven by weaker perceptions of personal finances. The decline occurred alongside a sharp rise in expectations around the level of mortgage rates.

The RBNZ kept rates unchanged at 5.50% in July, in line with consensus expectations.

The meeting minutes noted the decision was “consensus” across the Committee and removed prior language around considered hiking rates.

The forward guidance was more dovish, noting “monetary policy will need to remain restrictive” but moving “…for a sustained period” and remarking that the “extent of this restraint will be tempered over time, consistent with the expected decline in inflation pressures”.

Markets

US Q2 earnings season

The market is currently looking for S&P 500 Q2 earnings growth of 8.8%, which would be strongest since the 9.4% print for Q1 2022.

The bottom-up EPS estimate declined by just 0.5% over the course of the quarter, much lower than the five, ten, fifteen and twenty-year average declines of 3.4%, 3.3%, 3.2% and 4.0%, respectively.

Eight of eleven S&P 500 sectors are expected to report year-over-year earnings growth for Q2.

However, big tech remains the key tailwind – with the six largest stocks in the index (Amazon, Apple, Google, Meta, Microsoft and Nvidia) expected to grow EPS by 30% year-on-year, with the other 494 stocks to grow by 5% on average.

It is interesting to note some comments from those companies that have reported so far:

- Pepsi: “There is a cohort of consumers that have become more price conscious. They’re looking for more deals to get more for their money.”

- Delta Airlines: “We see the industry already taking pretty significant corrective action by pulling capacity down. And we expect by the end of August, we’ll have that back in balance.”

- Finally, snack-maker Conagra reported lower sales for its latest quarter and issued a disappointing profit outlook for its current fiscal year.

US equities

There was interesting price action post Thursday’s CPI print, with a big rally in bonds and a huge rotation in equities.

At a headline level the S&P 500 fell 0.8%, the NASDAQ lost 2%, while the small-cap Russell 2000 Index gained 3.6%.

Breadth was extremely positive, with almost 80% of S&P 500 companies rallying. The Russell 2000 saw 95% of members up.

The Magnificent Seven fell 4.2% as a group, and the divergence in performance between the S&P 500 and Russell was the most extreme in over four years.

At a sector level within the S&P 500, the yield-sensitive sectors performed strongest – with REITs up 2.7% and Utilities up 1.8%, while Tech fell 2.7% and Communication Services was down 2.6%.

About Jim Taylor and Pendal Focus Australian Share Fund

Drawing on more than 25 years of experience investing in top-performing Australian companies and a background in accounting, Jim manages our Long/Short Fund and co-manages our Imputation Fund. He is a Chartered Accountant with membership of the Australian Institute of Chartered Accountants.

Pendal Focus Australian Share Fund is managed by Crispin Murray. The fund has beaten its benchmark in 14 years of its 18-year history (after fees), across a range of market conditions. Find out more about Pendal Focus Australian Share Fund here.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Demand looks strong in key EMs and our Pendal Global Emerging Markets Opportunities investment team believes US dollar softness – when it comes – will create conditions for strong returns

EMERGING equity markets are driven by two broad global drivers:

- Global end demand and trade

- US dollar interest rates and liquidity

Individual markets have their own business and credit cycles – as well as political environments – but these are always interacting with the main global drivers.

Right now, one of the challenges for emerging markets investors is interpreting differing signals from these drivers.

Global demand

Indicators of global demand look supportive for emerging markets.

In June, manufacturing data (measured by Purchasing Managers Index surveys) continued to look strong in many emerging countries, while Asian exporters Korea, Taiwan and Vietnam saw strength in new export orders.

June manufacturing PMIs were 52 in Korea, 53.2 in Taiwan and 51.1 in Mexico, with exports growing in all three countries.

A PMI above 50 suggests expansion, below 50 indicates contraction, and 50 means no change.

Recent PMIs also indicate growth in domestically driven emerging economies such as India (57.5 for May), Brazil (52.5 for June) and Indonesia (50.7 for April).

Consumer confidence also looks robust in these three markets.

Find out about

Pendal Global Emerging Markets Opportunities Fund

China has two PMI data series with some conflicting messages, but both measures show weaker export and domestic orders.

In the Gulf PMIs look very strong. UAE, Saudi Arabia and Qatar were all above 54 for June.

US dollar

So far so good. But the other half of the story is the US dollar’s continuing strength and caution about the future direction of US monetary policy.

Against the US Dollar Index (DXY) basket of developed market currencies, the USD has strengthened by 3.5% year to date. Medium-and-longer-dated US government bonds have seen yields rise by about 0.4% over the same period.

No other major emerging market central bank has yet felt the need to follow Bank Indonesia’s surprise 0.25% policy interest rate hike in June.

But, following the US, yield curves across EM remain higher year-to-date, and the expected timing of policy interest rate cuts in markets like Brazil and Mexico keeps getting pushed out.

Meanwhile the stronger US dollar has seen corresponding weakness in emerging market currencies such as the Brazilian Real (-11.6% against the US dollar in the second quarter), Mexican Peso (-10.6%) and Indonesian Rupiah (-3.3%).

This reduces returns to international investors.

Although Mexico saw a surprisingly strong election win for the left-wing Morena party in the quarter, the Mexican Peso weakened alongside other similar emerging market currencies.

The strong US economy is good for emerging market exports (and remittances) but less good for US dollar liquidity.

In this environment we continue to find opportunity in some emerging markets where growth (particularly, corporate earnings growth) remains attractive, even if the current US liquidity environment is a headwind.

These particularly include Mexico, Brazil and Indonesia. Each has seen strong upward revisions to corporate earnings expectations this year.

Local currency weakness has been a drag on returns in each of these countries, but we remain confident US dollar softness, when it comes, will create the conditions for strong returns from these markets.

About Pendal Global Emerging Markets Opportunities Fund

James Syme, Paul Wimborne and Ada Chan are co-managers of Pendal’s Global Emerging Markets Opportunities Fund.

The fund aims to add value through a combination of country allocation and individual stock selection.

The country allocation process is based on analysis of a country’s economic growth, monetary policy, market liquidity, currency, governance/politics and equity market valuation.

The stock selection process focuses on buying quality growth stocks at attractive valuations.

Find out more about Pendal Global Emerging Markets Opportunities Fund here

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

Here are the main factors driving the ASX this week, according to portfolio manager RAJINDER SINGH. Reported by portfolio specialist Chris Adams

- Markets trying to identify beneficiaries of the US election, unmoved by UK election

- RBA could diverge from global central bank rate cuts

- Find out about Crispin Murray’s Pendal Focus Australian Share Fund

GLOBAL equity markets made a solid start to the second half of 2024, supported by easing rate pressures in the US.

A short week in the US due to the Independence Day holiday didn’t stop both the S&P 500 and NASDAQ finishing the week at all-time highs – breaking through the 5,500 and 18,000 levels, respectively, for the first time.

US Treasuries rallied on weaker macroeconomic data prints, with the release of softer numbers for jobs, unemployment and purchasing managers’ indices (PMI).

Overall, these indicators incrementally point to a US economy that is slowing and so reducing any ongoing inflationary pressures.

While the Federal Reserve continues wanting to accumulate more evidence, further softer data in line with the data released this week could allow the committee to consider interest rate cuts as soon as the September meeting.

There was plenty to interest followers of international politics, with ongoing developments in the US presidential election, French National Assembly voting, and the UK general election, though the implications for markets are not entirely clear and straightforward.

In Australia, we saw further evidence of economic resilience following last week’s strong CPI print, with May retail sales and building approvals data surprising on the upside – accompanied by continued strong price growth across capital city housing markets.

Some commentators continue to push the view that – unlike other central banks – the RBA’s next interest rate move will be up.

Overall views are mixed, as reflected in the latest RBA minutes.

Australian bonds fell in response, with ten-year yields up 9 basis points (bps). This contrasts with the 9bps fall in US ten-year yields, indicating different positions in the interest rate cycle for the two economies.

The S&P/ASX 300 gained 0.71%, lagging the 1.98% gain in the S&P 500 and 3.51% rise in the NASDAQ.

Commodity prices supported resource sector returns for the week. However, most ASX companies are now in black-out until August’s reporting season, so there was little news on the stock front.

US macroeconomics

On Tuesday, we saw the release of the Institute for Supply Management’s Manufacturing PMI, which showed the latest reading declining to 48.5 from 48.7.

This indicator has now been in contraction (i.e. less than 50) for 19 out of the last 20 months going back to October 2022.

Various components of the index such as Production, New Orders and Employment indicate broad contraction, so the briefly positive March 24 reading now looks the outlier compared to recent trends.

Jerome Powell, Chairman for the Fed, spoke at a European Central Bank (ECB) conference in Portugal.

He argued that the latest data shows evidence of continued disinflation and said he expects inflation to fall to the “low to mid-twos” a year from now.

He also argued that progress has been made in balancing the labour market and suggested that the Fed would respond to an unexpected weakening of the labour market.

Initial jobless claims continued their grind higher, printing 238k (up from 234k).

Importantly, the four-week trend is now at the highest level since August 2023, showing the degree of softening the labour market has experienced during the calendar year to date.

The JOLTS Quit Rate further supported the case that wages growth is easing towards historically average levels.

On Thursday, we saw the release of the other key ISM measure – the June Services PMI – which, at 48.8, significantly surprised to the downside.

This was well below the consensus of 52.7 and May’s reading of 53.8, and is the lowest level since May 2020 in the depths of Covid shutdowns.

While this series has been volatile, similarly to the Manufacturing PMI, numerous components showed broad weakness.

Interestingly, the prices component of the ISM Services survey continues to remain subdued.

This is important because it has been a pretty good lead indicator of one the Fed’s preferred inflation indicators, core Personal Consumption Expenditure (PCE) services ex-housing, in the past few years.

It is now also back pre-Covid levels.

The last key economic release of the week was the June payrolls, which came in at 206k versus consensus of 190k. However, net revisions to previous months were a large 111k decline.

The unemployment rate edged up to 4.1% from 4.0%.

Interestingly, these numbers are getting close to triggering the Sahm rule – a measure to identify the start of a recession developed by former Fed economist Claudia Sahm.

It looks at the changes in the three-month average unemployment rate relative to recent lows and is triggered once it hits 0.5%. The latest unemployment figures reading takes this measure to 0.4%.

The Fed minutes also came out, highlighting that it is in no rush to ease but that it is open to changing quickly if inflation and employment moderates.

The minutes mentioned that modest progress towards reducing inflation in recent months though labour markets are normalising, with a watch on unemployment in response to weakening demand.

After this week’s macro data, the market is now pricing an 80% chance of a Fed rate cute by the September 2024 meeting, up from approximately 70% before this week.

A total of two rate cuts are expected by the end of 2024, and almost five full cuts for the next year to June 2025.

Find out about Pendal Sustainable Australian Share Fund

Global macroeconomics

Europe

Eurostat published June inflation for the Euro area of 2.5% headline and 2.9% core (year-on-year).

This, along with comments from speakers including ECB President Lagarde at the Sintra conference, indicate that it currently remains on track for a September rate cut.

China

We saw the release of various PMIs.

The Caixin Composite and Services PMI were 52.8 and 51.2, respectively, indicating modest expansion.

However, the widely watched Manufacturing PMI component surprised at 51.8 (versus 51.5 consensus). This is the highest level since May 2021 and the eighth consecutive month of expansion.

This helped support the 6.1% gain in iron ore prices last week.

New Zealand

New Zealand’s central bank meets on 10 July, with rates forecast to stay on hold. Expectations are for a first cut in August, given ongoing softness in recent data.

Australia

May’s retail sales surprised to the upside, up 0.6% month-on-month versus consensus at 0.3%.

Building approvals rose 5.5% in May versus expectations of 3.0%.

While both series can be quite volatile, these data points are notable as recent trends in both have been on the softer side.

House prices continued their recent strength, with the latest CoreLogic data showing the rate of growth of 0.6% month-on-month country-wide and 0.5% month-on-month among state capitals.

Brisbane and Perth remain strong while Melbourne looks lacklustre, which is in line with our anecdotal feedback on their respective economies.

The RBA released minutes from the June meeting and there were no major surprises, with forward guidance consistent with Governor Bullock’s post-meeting press conference i.e. “not ruling anything in or out”.

In particular, the discussion focused on the case for hiking rates or keeping them steady, rather than any reduction.

This reinforced the view of some forecasters that next direction or rate moves is up rather than the downward trajectory forecast for most other central banks around the world.

Markets

There are a few observations to make at the halfway point of the calendar year:

- Historically (since 1928), when the S&P 500 is positive in the first half of the year, it follows with a positive second half 74% of the time, with an average 5.70% return. After a first half with gains of 10-20% (remembering that it delivered 14.5% in 1H 2024), the second half has had positive returns 88% of the time with an even stronger 8.58% average return.

- The second half in presidential election years has delivered a positive return in 83% of years.

- In data going back to 1950, July has seasonally been a strong month, followed by weakness in August and September.

- Strong EPS growth estimates continue to support US equities and the 9% consensus EPS growth for 2Q 2024 is the highest since Q4 2021.

- There are no signs of any stress in credit markets, with US corporate BB spreads remaining subdued and at recent low levels.

On the political side, President Biden’s re-election odds have plummeted.

Markets are trying to identify beneficiaries of a Trump victory, and if history is a guide, the Financials sector was a clear winner in 2016/17.

There were no surprises in the result or market reaction to the UK election, with moves in equities, bonds and the currency all muted on Friday.

Australian equities

Australian equities gained last week but lagged global markets.

All the positive returns were driven by Resources, with Industrials generally flat to down.

Tech and Utilities were weakest, but this follows very strong 1H returns for both sectors.

Within Resources, Anglo American suspended production of its Grosvenor metallurgical coal mine in Queensland following an underground fire.

The mine was due to produce 3.5 million tonnes this year, which is 1% of the seaborne market but 20% of Anglo’s volumes – throwing a spanner into its plans to divest the business following the failed approach from BHP a few months ago.

The suspension, along with a fire at Allegheny in the US and against a backdrop of multiple production downgrades by BHP this year, had the effect of tightening the met coal market and pushing prices higher.

About Rajinder Singh and Pendal’s responsible investing strategies

Rajinder is a portfolio manager with Pendal’s Australian equities team and has more than 18 years of experience in Australian equities. Rajinder manages Pendal sustainable and ethical funds, including Pendal Sustainable Australian Share Fund.

Pendal offers a range of other responsible investing strategies, including:

- Pendal Sustainable Australian Share Fund

- Crispin Murray’s Pendal Horizon Fund

- Pendal Sustainable Australian Fixed Interest Fund

- Pendal Sustainable Balanced Fund

- Regnan Credit Impact Trust

- Regnan Global Equity Impact Solutions Fund

Part of Perpetual Group, Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management. Responsible investing leader Regnan is now also part of Perpetual Group.

Here are the main factors driving the ASX this week, according to portfolio manager OLIVER RENTON. Reported by portfolio specialist Chris Adams

- Find out about Pendal Focus Australian Share Fund

- Tune into our latest on-demand webinar: Beyond the Numbers

THE final week of the financial year featured a bit of everything.

On the macro front, US data continued to point to a slowing – but still growing – economy, while inflation data also remained encouraging.

We also saw the first US presidential debate.

Australia was focused on the May Consumer Price Index (CPI), which came in hotter than expected.

Company-specific news drove individual stock volatility globally and domestically. Nvidia, for example, had a large drawdown on Monday, got it all back on Tuesday, but began losing steam again through the rest of the week.

However, equities in aggregate were flattish on the week. The S&P 500 returned -0.06% while the S&P/ASX 300 -0.25%.

The Aussie bond market saw some action, with yields up materially.

US macro

May’s Core Personal Consumption Expenditure (PCE) report showed that inflation rose 2.6% year-on-year – marking the lowest annual rate since March 2021, when inflation topped the Federal Reserve’s 2% target for the first time in this economic cycle.

The June flash S&P Global US composite Purchasing Managers’ Index (PMI) rose a touch to 54.6, ahead of the 53.5 consensus expectations.

This is viewed as bullish, suggesting solid growth alongside cooling inflation.

Sales of existing homes in the US fell for a third straight month in May, underscoring persistent affordability challenges that hobbled the important spring selling season.

Existing housing inventory is well below historical averages, as people are reluctant to refinance mortgages at a higher rate. This has helped drive existing home prices higher, up 5.7% year-on-year – a trend which may complicate the Fed’s thinking.

Personal spending for Q1 2024 was revised down from 2% growth to 1.55%, while separate releases showed a decline in business equipment orders and shipments – a widening trade deficit and job market weakness.

The Atlanta Fed’s GDPNow forecast shifted expectations of Q2 GDP growth down from 3.0% to 2.7%.

US consumer confidence eased in June on a more muted outlook for business conditions, jobs and incomes. The Conference Board’s sentiment gauge also slipped to 100.4 from May’s downwardly revised 101.3.

Notably, consumer expectations of better business conditions dropped to the lowest levels since 2011, yet expectations of higher equity prices remained close to all-time highs – a good reminder that the stock market is in fact not the economy.

The big banks aced the Fed’s annual stress test, pointing to a financial system that remains generally strong and well-capitalised.

There was little to come out of the first presidential debate in terms of policy that affects markets. The NFIB Small Business Uncertainty Index is surging, but that is normal for election years.

It is interesting to note that 2024 is the first election in 30 years where Baby Boomers will not form the majority voting bloc – now being outnumbered by the combination of Millennials and Gen Zs.

Fedspeak

James Bullard, former President of the St Louis Fed, said that he expects the pace of easing to be slow because there is no sense of urgency provided by the economy.

Fed Governor Lisa Cook noted that she expects inflation to improve gradually this year, then more quickly in 2025.

Elsewhere, Fed Governor Michelle Bowman sounded a cautionary note on potential upside risks to inflation, with Covid-era supply chain dislocations largely resolved and limited labour force participation growth recently.

Looser financial conditions and geopolitical issues could also add to inflation, she said.

She also sees the need to keep borrowing costs elevated for some time and that – while there are a number of potential outcomes for 2024 – she does not expect rate cuts before the year end.

Finally, Atlanta Fed President Raphael Bostic continues to expect one rate before the end of the year, with recent inflation prints signalling some evidence of movement towards the Fed’s goal, and risks between the labour market and inflation becoming more balanced.

He is anticipating four rate cuts in 2025.

Australia macro

The number of job vacancies in Australia fell 2.7% quarter-on-quarter in May, equal to roughly 9,800 vacancies.

Job openings (as a proportion of job opening plus employment) remains well above pre-Covid levels, unlike in the US.

The Melbourne Institute’s “nowcast” for quarterly GDP growth remains muted at 0.2%.

Insolvencies continue to rise in Australia and business payment defaults at a record high suggests there is further to go, though new business formation remains on an uptrend.

Some economists have shifted to a base case of a rate hike in August following the May CPI print, which came in at 4.0% year-on-year versus 3.6% in April.

This was the fastest monthly print since November 2023 and the concern was an acceleration in underlying inflation, with the trimmed-mean measure rising 4.4% year-on-year (from 4.1% in April).

Service rose 4.8% year-on-year, while disinflation in goods has halted.

Housing and transportation were firmer, while growth in food prices eased, and insurance and health costs remained persistently strong.

CPI and energy

Several of the strongest categories for CPI growth in May – such as electricity, transport and automotive fuel – are linked to the price of energy.

A recent research trip to Asia, which looked at energy and the energy transition, highlights the importance of energy and the CPI and some of the longer-term risks we need to be thinking about.

Net Zero and the energy transition may have inflationary consequences – for example:

- Replacing coal with ammonia in power generation is inherently more expensive.

- Building out transmission and other infrastructure puts additional pressure on commodity prices.

- Transition targets, intervention in markets and regulatory uncertainty create dislocations and ultimately higher commodity prices through under-investment e.g. East Coast gas prices.

- The Safeguard mechanism imposes an additional cost on large emitters, which will be passed on where possible.

In Japan, the government is now incentivising coal-fired generators to run on up to 20% ammonia and gas plants to run on hydrogen. The higher input prices for power generation are likely to be passed on to the consumer.

There is also a debate around mandates for sustainable aviation fuel (SAF), which are already in place in Europe. Again, SAF is much more expensive that tradition aviation fuel, which is likely to be inflationary for airfares.

Energy is the cornerstone of all economies, and the energy transition appears to support higher inflation – and not the kind of inflation that central banks can control with monetary policy.

In fact, we probably need rates as low as possible given the capital-intensive nature of the investment required.

Find out about

Pendal Focus

Australian Share Fund

Crispin Murray,

Head of Equities

Markets

Most of the action was in the bond markets, with Australian two-year government bond yields rising 15 basis points (bps) to 4.17% as a result of the CPI print.

Equity markets, in aggregate, did not move that much into the end of the financial year.

On the global side, there were some updates which provided a snapshot on consumer demand:

- Carnival Corporation upgraded guidance off the back of record levels of demand for cruises, helped by the value of sailing versus land-based travel.

- Pool Corp, which distributes swimming pool supplies, cut its earnings forecast, citing cautious discretionary consumer spending on big ticket items such as swimming pools – with new pool construction activity estimated to be down 15-20% for the year.

- Fuel and convenience retailer Alimentation Couche-Tard missed Q4 estimates as same-store sales declined in the US, Europe and Canada, with management pointing to challenging economic conditions constraining discretionary spending. Levi Strauss and Nike also reported quarterly sales that fell short of expectations.

- General Mills disappointed the market with its sales outlook, noting that shoppers continue to reduce spending as prices rise.

- Walgreen Boots plunged after it cut guidance on a worsening retail environment and announced store closures.

About Crispin Murray and Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia. Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Find out more about Pendal Focus Australian Share Fund here.

Contact a Pendal key account manager here.

Drawing on more than 25 years of experience investing in top-performing Australian companies and a background in accounting, Jim manages our Long/Short Fund and co-manages our Imputation Fund. He is a Chartered Accountant with membership of the Australian Institute of Chartered Accountants.

Pendal Focus Australian Share Fund is managed by Crispin Murray. The fund has beaten its benchmark in 14 years of its 18-year history (after fees), across a range of market conditions. Find out more about Pendal Focus Australian Share Fund here.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

We have updated and reissued the Product Disclosure Statements (PDSs) for the following classes of units in the Pendal Global Select Fund (the Fund), effective on and from Friday, 28 June 2024:

- Pendal Global Select Fund – Class R

- Pendal Global Select Fund – Class W

- Pendal Global Select Fund – Class Z

The following is a summary of the key changes to the PDSs.

ESG disclosure

We have removed the Responsible Investment Association of Australasia (RIAA) certification symbol, as the Fund is no longer RIAA certified. We have also provided clarification that exclusionary screens are not applied to the Fund’s investments in cash or derivatives and that the use of derivatives may result in the Fund having indirect exposure to the excluded companies from time to time

There has been no change to the Fund’s investment approach, or the exclusionary screens employed by the Fund.

Updates to significant risks disclosure

The Fund’s investment strategy involves specific risks.

We have updated the significant risks disclosure applicable to the Fund to ensure that our disclosure continues to align with the nature and risk profile of the Fund and the current economic and operating environment.

Updates to ongoing annual fees and costs disclosure

The estimated ongoing annual fees and costs for the Fund has been updated to reflect financial year 2023 fees and costs. These include changes to estimated management costs and estimated transaction costs.

We now also disclose the maximum management fee we are entitled to charge under the Fund’s Constitution.

Additional information on how to apply for direct retail investors

We have provided additional information for non-advised retail investors (retail investors without a financial adviser) investing directly in Class R units of the Fund who may also be required to complete a series of questions as part of their online Application, to assist us in understanding whether they are likely to be within the target market for the Fund.

Updates to our complaints handling process

We have provided additional details about our complaints handling process and the Australian Financial Complaints Authority.

We have updated and reissued the Product Disclosure Statements (PDS) for the Pendal Sustainable Share Fund (Fund) on and from Friday, 28 June 2024.

The following is a summary of the key changes reflected in the PDS.

ESG disclosure

We have enhanced our ESG disclosure to describe the Fund’s sustainability objective, the sustainable themes Pendal focuses on when managing the Fund and the sustainability assessment framework employed by the Fund.

There has been no change to the way the Fund is invested.

Updates to significant risks disclosure

Each Fund’s investment strategy involves specific risks.

We have updated the significant risks disclosure applicable to the Fund to ensure that our disclosure continues to align with the nature and risk profile of the Fund and the current economic and operating environment.

Updates to ongoing annual fees and costs disclosure

The estimated ongoing annual fees and costs for the Fund have been updated to reflect financial year 2023 fees and costs. These include changes to estimated management costs and estimated transaction costs.

We now also disclose the maximum management fee we are entitled to charge under the Fund’s Constitution.

Additional information on how to apply for direct investors

We have provided additional information for non-advised investors (investors without a financial adviser) investing directly in the Fund who may also be required to complete a series of questions as part of their online Application, to assist us in understanding whether they are likely to be within the target market for the Fund.

Updates to our complaints handling process

We have provided additional details about our complaints handling process and the Australian Financial Complaints Authority.