Here are the main factors driving the ASX this week, according to Pendal’s head of equities CRISPIN MURRAY. Reported by portfolio specialist Chris Adams

- Environment may signal equities pushing higher

- Find out about Pendal Focus Australian Share fund

- Watch Crispin’s most recent Beyond the Numbers webinar

WE saw a reversal in recent trends last week.

After rising 47bps in April, US 10-year government bond yields fell 16bp last week, triggering a continued bounce in equities.

The S&P 500 gained 0.56% and the NASDAQ lifted 1.44%.

This followed dovish comments from US Federal Reserve chair Jerome Powell after US interest rates were left unchanged.

Powell clearly indicated rate hikes were not on the agenda and the Fed did not expect a recent jump in inflation to be sustained.

A subsequently softer payroll report and moderating average hourly earnings data lent credibility to his comments.

The fall in bonds yields was reinforced by a 7.3% drop in Brent crude oil on higher weekly inventories.

The key question is whether this is the beginning of a larger reversal in bond yields as inflation momentum begins to wane.

We suspect this will happen, though we anticipate a relatively moderate bonds rally given resilience in economic growth and recognition of structural factors supporting inflation.

Trends also reversed in currency markets (with a potential near-term top in the US dollar/Japanese yen trade) and Chinese equities (where internet stocks have made strong gains this month).

Such an environment may signal the equity market is going to push higher.

US earnings have been supportive. Apple was the latest tech name to surprise on earnings and capital management.

In Australia the S&P/ASX 300 rose 0.74%, supported by tech and banks stocks. National Australia Bank’s half-yearly results were largely as expected and the CEO struck a positive tone.

In contrast, Woolworths delivered another disappointing sales update, indicating they were seeing consumers “trade down”.

US inflation and policy outlook

The Fed left rates on hold, as expected.

The focus was on Powell’s press conference and the potential for rates to rise after recent disappointing inflation data.

The market was pricing a 30 per cent chance of a hike by year’s end.

Find out about

Pendal Focus

Australian Share Fund

Crispin Murray,

Head of Equities

Powell firmly knocked this back.

He acknowledged a set-back on the path to 2 per cent inflation and the need for rates to stay on hold for longer.

But he also noted policy was already restrictive and the question was therefore how long rates should be kept at current settings.

Powell noted the criteria which could allow rates to fall – such as unexpected easing of the labour market – rather than the factors that could lead to a rate rise.

This was likely a deliberate signal on where the Fed is focused.

He also indicated that the Fed expected inflation to move back down this year, noting recent pressure was tied more to lagging factors built into the inflation-measuring process (eg healthcare and rents) as well as confidence in a supply response to support disinflation.

Our conclusion remains that while the Fed retains its current “hold” bias, there is a skew towards looking for reasons to cut rather than reasons to raise rates.

The market’s implied expectations of a rate hike this year have fallen back below 10 per cent.

Liquidity a key factor

Market liquidity has been a key factor driving the equity rally from November 2023.

After the FOMC meeting, the Fed announced a relatively dovish slowdown in Quantitative Tightening (QT) from US$60 billion per month in US Treasury bonds to US$25 billion, effective from June.

This is important as it supports the liquidity environment for markets – and extends that support well into the northern summer.

Elsewhere, the US Treasury announced its projected financing requirements for the September quarter. This is watched carefully since it also affects market liquidity.

Last year more financing was shifted to the short end of the yield curve, which supported liquidity and helped turn markets around.

This time the plan is a moderate reduction in the Treasury General Account (ie their cash on hand) from US$940 billion to US$850 billion. This is not as aggressive as some looked for, but still partly offsets bond issuance.

The mix of issuance remains largely unchanged, retaining the relative skew to the short end of the curve.

The reverse repo market can also serve as a source of further funding for Treasury issuance in coming months.

US economic outlook

The economy continues to hold up well, but there are signs employment growth is slowing.

US employment

April non-farm payrolls rose 175k, well below a three-month average of 269k and 240k consensus expectations. There were also net revisions of -22k for February and March.

The government sector drove the downside surprise, adding just 8k jobs versus a 60k average over the past six months.

The private sector held up at 153k new jobs, with healthcare and social assistance representing half the rise.

The forward signals are mixed. The NFIB small business survey indicates a material slowdown over the next few months, while jobless claims data is more benign.

The average US work week fell marginally to 33.7 hours — another sign the labour market could be weakening.

Average hourly earnings also softened from 4.1% year-on-year in March to 3.9% in April. There was weakness in leisure, hospitality, construction and government.

This reinforces the signal that wage growth is slowing towards a level consistent with low inflation in the low 2 per cent range.

A household survey saw unemployment rise from 3.83% to 3.86% – not quite as large as some were expecting.

We have crossed a threshold for the “Sahm Rule” – which indicates that a 0.5% increase in unemployment signals a recession will follow.

We have some reservations about this rule and do not read too much into it.

The outlook for lower wages was supported by the latest Job Openings and Labor Turnover Survey from the US Bureau of Labor Statistics.

Notably, the favoured “Quits” rate – a decent lead indicator on wages – continued to move lower. Its current level is consistent with 4.5% unemployment based on historic data.

While we note there are still structural factors underpinning inflation, this is all supportive of easing inflationary pressure in the near term.

US service sector activity

There was some focus on the US services sector after an April ISM survey showed a fall of two points to 49.4 – its lowest point since the pandemic.

The data suggested the worst of all combinations: business activity down materially and new orders also lower, while pricing expectations were higher.

We note this is a volatile series, where weather can play a part. But it does provide a warning shot, particularly in the context of a series of consumer facing companies such as McDonalds and Starbucks signalling weaker demand.

The April S&P Global US Services PMI remains above 50 – and the ISM had been running above it for some time.

We may be seeing a convergence of these series, rather than a material change in trend.

Markets

US earnings season

First-quarter US earnings have been positive, partly reflecting a low bar of only 3 per cent expected earnings growth.

The response to beats is also much more muted than normal, suggesting the market was positioned for good news.

Apple provided a boost to both the tech sector and overall market, with earnings coming in better than many had feared.

There is also a shift in sentiment towards the potential impact of AI – from concerns that it posed a risk to Apple’s outlook, to speculation it may drive a handset upgrade cycle.

Looking across the tech sector, several trends have been supportive:

- Demand is strengthening and prices are increasing, supporting revenue growth

- Capital returns picking up; Alphabet and Meta both announced their first dividends in 2024, alongside share buy-backs

- Rising profitability; margins are up in 80% of internet companies as a result of greater focus on costs

- The AI cycle; AI use cases are increasing the focus on cutting costs and improving services.

Market signals

There has been some notable price action, likely tied to the reversal in bond yields.

Technology stocks and gold miners represent two ends of the thematic spectrum.

The former’s surge in outperformance from October to February (measured by the Technology Select Sector SPDR Fund versus the VanEck Gold Miners ETFs) reversed entirely in March and April — but now may have turned higher again.

Pendal Focus Australian Share Fund

Now rated at the highest level by Lonsec, Morningstar and Zenith

This may be supportive for equities given tech’s weight in global indices.

There are a couple of other reversals to watch, which are potentially positive signals for the market:

- The USD/JPY currency cross rate, which has seen a material reversal off sentiment extremes.

This may be a catalyst for the US dollar trade-weighted index to start easing. This is positive for markets as it supports liquidity. - A potential shift in sentiment towards Chinese equities. This may be seen in the KraneShares CSI China Internet sector ETF, which has been in extended bear market. There has been a material break higher in recent weeks — on short-term time frames at least. This reflects changing sentiment on the Chinese market combined with very low exposure to it. Allocation to China in active global equity funds is at it record lows — and in the first decile of historical allocation by one measure.

What does this all mean?

We think it means markets are probably supported at current levels and we could see rotation back to higher beta sectors — those stocks with rate exposure such as telcos and REITs, as well as China consumer-related names.

Australian market

National Australia Bank (NAB) delivered the first bank result — which seemed good enough to sustain the sector’s premium valuation rating — with a surprisingly positive message from the new CEO.

Consumer anecdotes were softer, notably from Bapcor (BAP), Ampol (ALD) and Woolworths (WOW).

Gold stocks rolled over reflecting the bond reversal, while lithium names ran higher on a clean-out of IGO’s (IGO) inventory by its Chinese partner.

High-quality growth names began to run again (eg Goodman (GMG), Xero (XRO), Pro Medicus (PME)), reflecting more positive sentiment on rates.

About Crispin Murray and the Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia. Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions.

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

Pendal named in Fund Manager of the Year Awards | ASX small caps back in favour | Two EMs set to benefit from lower rates | 10 investor themes for 2024

Aussie small caps are once again outperforming large caps. Pendal portfolio managers LEWIS EDGLEY and PATRICK TEODOROWSKI explain why

- ASX small caps are back in favour with investors

- Earnings holding up better than expected

- Find out about Pendal Smaller Companies Fund

AUSSIE small caps are once again outperforming their large-cap counterparts after a period of underperformance in recent years.

Conditions have turned in favour of ASX-listed small caps in recent months and Pendal portfolio managers Lewis Edgley and Patrick Teodorowski believe that trend will continue.

Edgley and Teodorowski co-manage Pendal Smaller Companies Fund, which invests in companies outside the top 100 listed on the Australian and New Zealand stock markets.

Together the pair have 25 years of experience with Pendal Smaller Companies Fund. (Teodorowski has been with the fund for 14 years and Edgley for 11.)

In this article, the pair explain why small caps underperformed, how conditions have changed and what they’re doing to take advantage.

Why small caps under-performed in recent years

Small caps underperformed large caps in 2022 and 2023 as higher rates and recession fears pushed investors towards larger, more established companies.

When markets first anticipated a rapid post-pandemic rate-rise cycle, that precipitated a significant underperformance of small caps, relative to large caps, says Edgley.

Many companies in the large cap index — such as banks and insurers — were natural beneficiaries of a rising interest rate environment.

“In the small-cap universe, the composition was quite different,” Edgely says. “For example, we’ve got a large proportion of real estate trusts where rising rates hurt their valuations.”

“We’ve also got a high degree of economically-sensitive businesses.

“When you have a fear of recession these businesses are typically sold off. That happens in advance of any earnings impact as sentiment weighs on those types of businesses.”

At the start of that period small caps had a significant premium compared to large caps, which also exacerbated their relative underperformance.

How conditions changed in favour of smalls

This year, as recession fears dissipated and inflation began moderating, investors regained interest in smaller companies.

“We’ve had the US Fed on hold and the Australian RBA on hold, and in that environment the market starts to anticipate things improving and a shift to the other side of the interest rate cycle, which is rate cuts,” Teodorowski says.

“We’ve also subsequently seen earnings hold up significantly better than investors feared.

“We’ve seen a re-rating of companies that were most likely to feel the pain of higher interest rates.

“More fundamentally, over the past two earnings seasons we’ve seen greater resilience out of the more cyclical companies within our index.

“They’ve been able to manage their earnings far better than the market expected.”

Find out about

Pendal Smaller

Companies Fund

Materially lower valuations and a low Australian dollar has prompted more merger and acquisition activity in the last six months, says Teodorowski.

An expected flurry of “new and bigger Initial Public Offerings” should also see increased demand and investment opportunities.

What sets Pendal’s small caps team apart

“We believe a few things set us apart as quality small-cap investors,” says Edgley.

“The key driver is the breadth and depth of the team.

“We’re a team of five. That would be one of the largest, dedicated small cap teams in the market.

“We’re also supported by the broader Pendal Aussie equities team. So in total there’s 19 of us.“

A larger team allows Pendal to cover a lot of ground — which is very important in small-cap investing, Edgley says.

“The small-cap universe is very diverse by sector. There are always new moving parts. The refresh within the universe is significant.

“With sectoral responsibility across all areas we’re able to make active decisions in certain sectors, and we think we’re able to make the best investment decisions.”

Active management important

“The process has always revolved around going out and wearing out boot leather,” says Teodorowki.

“We do a lot of direct meetings with the management of companies. We meet with other industry participants, whether customers or competitors.

“That’s always been a big part of the process in coming up with a view on a business.

“Another big part of our process is peer review. Lewis and I are not only portfolio managers, we’re analysts.

“When any idea gets brought to the team, we all sit around as a group and debate the merits of that investment as a team.

“The five people in the team are very experienced. This brings a different lens into analysing the business. It normally raises additional questions and drives deeper research into the investment idea.”

Says Edgley: “It’s very much style-agnostic, bottom-up idea generation. “We take a pragmatic view of the opportunities in front of us and converting those opportunities.

About Lewis Edgley and Patrick Teodorowski

Lewis and Patrick are co-managers of Pendal Smaller Companies Fund.

Portfolio manager Lewis Edgley co-manages Pendal’s Australian smaller companies and micro-cap funds and conducts analysis on a range of smaller companies. He joined the Pendal Smaller Companies team in 2013 as an analyst, before being promoted to the role of portfolio manager in 2018. Lewis brings 20 years of industry experience with previous roles spanning equities research, as well as commercial and investment banking roles at Westpac and Commonwealth Bank.

Portfolio manager Patrick Teodorowski co-manages Pendal’s smaller companies and micro-cap funds and conducts analysis on a range of smaller companies. He joined Pendal in 2005 and developed his career as a highly regarded small cap analyst. Patrick holds a Bachelor of Commerce (1st class Honours) from the University of Queensland and is a CFA Charterholder.

About Pendal Smaller Companies Fund

Pendal Smaller Companies Fund is an actively managed portfolio investing in ASX and NZX-listed companies outside the top 100. Co-managers Lewis Edgley and Patrick Teodorowski look for companies they believe are trading below their assessed valuation and are expected to grow profit quickly. Lewis and Patrick together have more than 40 years of investment experience.

Find out about Pendal Smaller Companies Fund

Find out about Pendal MicroCap Opportunities Fund

Find out about Pendal MidCap Fund

About Pendal Group

Pendal is a global investment management business focused on delivering superior investment returns through active management.

In 2023, Pendal became part of Perpetual Limited (ASX:PPT), bringing together two of Australia’s most respected active asset management brands.

Here are the main factors driving the ASX this week according to Pendal portfolio manager JULIA FORREST. Reported by portfolio specialist Chris Adams.

- Underlying inflation in Australia remained well above the RBA’s target in Q1

- The GDP print in the US suggested ongoing economic strength

- Find out about Pendal Focus Australian Share fund

LAST week was a big one for macro data.

In the US, headline Q1 2024 Gross Domestic Product (GDP) growth came in relatively soft at 1.6%, versus 3.4% in the prior quarter and the 2.5% expected.

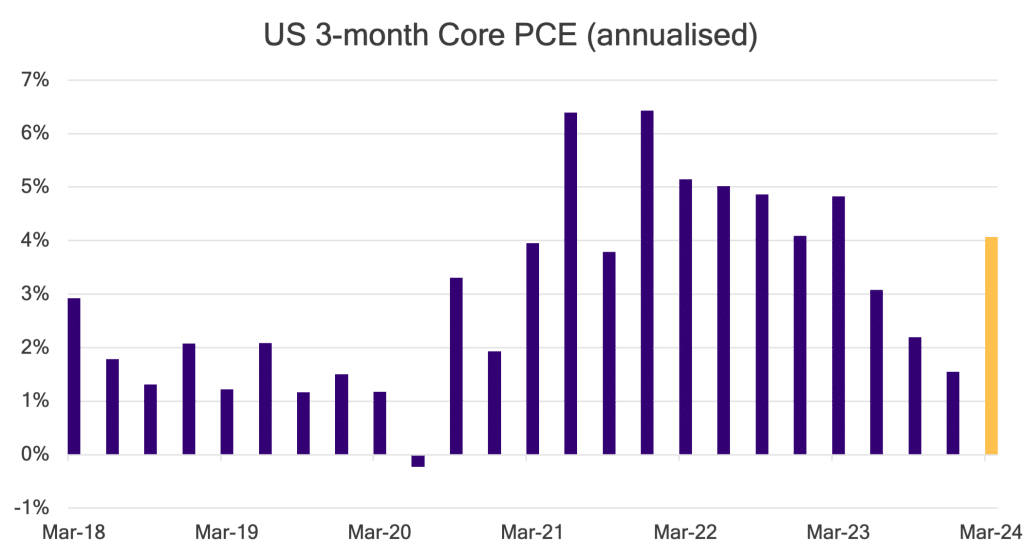

At the same time, the Q1 Core Personal Consumption Expenditure (PCE) deflator – a measure of inflation – accelerated to 3.7% annualised, versus 2% in Q4 2023 and the 3.4% expected.

As a result, US bond yields continued their climb, with ten-year Treasury yields ending up five basis points (bps) for the week at 4.67% and the market increasingly implying a first rate cut by the Fed in December.

Chicago Federal Reserve President Austan Goolsbee said that the Federal Open Market Committee needs to “recalibrate” its stance – noting that “progress on inflation has stalled” in 2024 and that after three months, this signal “cannot be dismissed”.

While it was a bumpy week for data, there was an underlying tone of resilience, with the market finding comfort in US Q1 earnings.

The Nasdaq and SP500 ended up by having their best week since November, returning 4.23% and 2.68%, respectively.

AI optimism lifted Alphabet (+10%) across the US$2 trillion market cap threshold, while Nvidia (+6%) and Microsoft (+2%) also gained.

The S&P/ASX 300 was up 0.12%.

The Australian Q1 2024 consumer price index (CPI) came in at 3.6% year-on-year versus the 3.5% expected, slowing from 4.1% in the previous quarter.

The “trimmed mean” measure preferred by the RBA rose 1.0%, again above forecasts of a 0.8% gain.

Following the data release, the Aussie Dollar jumped 0.7% to $0.6530 versus the US Dollar before settling at $0.6517, while yields on the 2-year (up 31bps) and 10-year government bonds (up 27bps) moved higher to trade at 4.18% and 4.52%, respectively.

The two things that the RBA focusses on – employment and inflation – are both above target, with the recent unemployment rate 20bp below the RBA’s forecast (3.9% vs 4.1%) and the trimmed mean inflation now 20bp above (1.01% vs 0.8%).

US macro

Headline GDP growth of 1.6% for the first quarter was softer than the 2.5% expected and the 2.7% forecast by the Atlanta GDPNow measure.

However, the breakdown was quite constructive, as final domestic demand remained solid (up 2.8%) for the quarter – with robust contributions from consumer spending, business fixed investment and residential investment.

The drag came from net exports (down 0.86%), driven by strong import growth apparently related to technology (computers, parts, semiconductors and telecommunications equipment).

In sum, the GDP print suggested ongoing economic strength in the US.

The Atlanta Fed GDPNow estimate for Q2 GDP growth is near 4%, which further fortifies upside risks to the inflation outlook.

The annualised Q1 Core CPI growth of 3.7% was the strongest quarter since the early 1990s, excluding the immediate post-pandemic period.

Core services ex-housing is the key driver, growing at a three-month-on-three-month annualised rate of 5.2%.

This is largely driven in turn by wage growth, where there are some possible early signs of cooling in measures of labour market hiring plans, the quits rate, and the Atlanta Fed wage growth tracker.

However, the US macro backdrop remains strong, with the ISM Manufacturing index showing a big uptick in 2024 and – importantly for markets – earnings fears as reflected in 12-month forward earnings-per-share estimates seeming to have passed.

The combination of sticky inflation and economic resilience raises the question of whether the neutral rate is as low as the Fed and market previously thought and, by extension, whether policy settings are as restrictive as assumed.

Financial conditions are now looser by the Chicago Fed’s own metric than at the beginning of 2022, when rates were effectively at zero and the Fed was still officially saying that inflation was transitory.

The Fed significantly eased financial conditions late last year via its “dovish pivot”, which reduced the global cost of both equity and debt capital.

Fiscal policy is working against the Fed’s rate settings.

The economy is resilient, unemployment is at 3.8% (too low to reduce inflation), and wage growth is strong (albeit slowing).

However, the US fiscal deficit is -6.2% and it is unusual for large deficits in boom times – normally it is the result of recession.

We are a little over six months out from the US Presidential Election and a balanced budget is probably the farthest thing from the mind of either candidate.

As such, the Fed is likely to continue to lean against the continued fiscal dominance.

The problem for the stock market is that rates seem too high to allow equities to push through to higher levels, but not high enough to create the kind of economic slowdown that forces the Fed to ease.

Australia macro

The Q1 3.6% twelve-month growth in Australian CPI slowed from 4.1% in Q4 2023, but by less than the 3.5% expected.

Nearly half of Australia’s CPI basket rose at an annualised rate of more than 3% in the March quarter.

The trimmed mean measure rose 1.0% in Q1, versus the 0.8% seen in Q4 2023 and expected again. The twelve-month rate dropped from 4.2% to 4.0%.

Several components appear to be sticky, notably in domestic market services lifted by rents, insurance and education costs.

Rental prices rose 2.1% for the quarter, in line with low vacancy rates across the capital cities. Rents continue to increase at the fastest rate in 15 years.

On any measure, underlying inflation in Australia remained well above the RBA’s target in Q1.

Adviser Sam is invested

in making our world

A better place.

Watch as Sam meets a

mum rebuilding her life

thanks to responsible

investing

There are some signs that the labour market is beginning to soften, but wage rates remain too high to be consistent with the RBA’s targets.

Monetary policy is working its way through the system, lifting debt service costs and reducing household disposable income.

However, the Stage 3 tax cuts are likely to see an uptick in retail spending from July, with a possible additional $23 billion in spending capacity in FY24/25.

If 75% of this is spent, this could see a 4.1% lift in retail sales.

Europe/UK macro

The Euro area Composite Purchasing Managers’ Index (PMI) came in at 51.4 versus the 50.7 expected, while the Services PMI was at 52.9 versus the 51.8 expected.

The UK Composite PMI was at 54.0 versus the 52.6 expected. Recent data has been solid and picking up, suggesting that economic activity – having initially been shocked by a shift from zero rates – is now adjusting.

US earnings season

With the US market near its most concentrated in history, earnings for the “Magnificent 7” were crucial to markets.

Three of the four that reported were well received (Tesla, Microsoft, Alphabet), with only Meta disappointing – here’s more:

- Alphabet beat expectations for revenue, operating income and EPS. It also announced its first ever dividend and an additional US$70 billion buyback.

- Microsoft beat consensus EPS expectations and highlighted the growth of its cloud computing business and its efforts to bring AI technology to clients.

- Tesla missed on revenue ($21.3 billion versus expectations for $22.3 billion) and earnings estimates for Q1, noting that “vehicle volume growth rate may be notably lower” in 2024 than in 2023. However, investors were upbeat on the company’s strategy going forward, with a focus on “accelerating” the rollout of new, cheaper models. There are some interesting potential parallels between EVs and today’s enthusiasm for AI. Three years ago, EVs – and Tesla in particular – were expected to take over the world. However, competition has been intense in the sector (especially from China) and demand disappointing in some regions.

- Meta saw lighter revenues and higher expenses and capex as it looks to spend more on AI. 2Q24 revenue guidance was below consensus. There is a concern being that advertising revenue is slowing due to geopolitical events.

About Julia Forrest and Pendal Property Securities Fund

Julia Forrest is a portfolio manager with Pendal’s Australian Equities team. Julia has managed Pendal’s property trust portfolios for more than a decade and has 25 years of experience in equities research and advisory, initial public offerings and capital raisings.

Pendal Property Securities Fund invests mainly in Australian listed property securities including listed property trusts, developers and infrastructure investments.

About Pendal Group

Pendal is an Australian investment management business focused on delivering superior investment returns for our clients through active management.

Pendal’s investment teams are often recognised by the Australian investment industry’s most-respected research houses and publishers. Here are our latest awards and nominations

2026 Lonsec/Money Management Fund Manager of the Year awards

(Winners to be announced Jun 26, 2026)

- Multi-Asset Diversified Fund of the Year – Pendal Monthly Income Plus Fund

2026 Morningstar Awards

- Fund Manager of the Year – Listed Property (finalist)

2025 Zenith Fund Awards

- Australian Equities (Large Cap) (finalist)

- International Equities (Emerging Markets & Regional) (finalist)

- Sustainable and Responsible Investments (Growth) (finalist)

2025 Financial Newswire / SQM Fund Manager of the Year

- A-REITs — Pendal Wholesale Plus Property Securities Fund (finalist)

2024 Lonsec / Money Management Fund Manager of the Year awards

- Australian Property Securities Fund of the Year – Pendal Property Securities Fund (finalist)

- Global Emerging Market Equity Fund of the Year – Pendal Global Emerging Markets Opportunities Fund (finalist)

- Australian Fixed Income Fund of the Year – Pendal Short Term Income Securities Fund (finalist)

2024 Zenith Fund Awards

- Sustainable and Responsible Investments — Income (winner)

- Multi-Asset – Diversified (finalist)

Find out about

Pendal Property

Securities Fund

Find out about

Pendal’s

cash funds

Find out about

Pendal Global Emerging Markets Opportunities Fund

Here are the main factors driving the ASX this week according to portfolio manager JIM TAYLOR. Reported by investment specialist Jonathan Choong

- Find out about Pendal Focus Australian Share Fund

- On-demand: tune into Crispin Murray’s bi-annual Beyond the Numbers webinar

THE stock market fell for the third week in a row last week, as investors grappled with rising geopolitical tensions in the Middle East.

This overshadowed positive economic data that previously fuelled expectations of an interest rate cut by the US Federal Reserve.

Fed officials commented frequently throughout the week, but their remarks had little impact on those expectations, which are now firmly entrenched.

Bond yields rose across the board and the US dollar strengthened.

Gold prices continued to climb, along with copper and iron ore.

Oil prices, however, have retraced back to pre-strike levels following the Israeli attack in Syria.

The S&P 500 Index suffered its first six-day losing streak in 18 months, and the NASDAQ took a major hit on Friday night – closing down more than 2 per cent.

The Dow Jones Industrial Average, however, managed a small gain as investors shifted their focus from technology stocks to industrial and financial sectors.

Over the course of the week, the Magnificent Seven lost a collective $950 billion.

Fedspeak

Fed officials hinted at potential interest rate cuts this year, but ongoing inflation concerns are causing some hesitation.

John Williams, president of the Federal Reserve Bank of New York, expressed confidence in the economy and said: “we will likely start bringing rates back to normal levels this year.”

However, Chairman Jerome Powell indicated inflation remains a hurdle.

“The recent data suggests it may take longer than expected” to achieve its goals, he said, adding that the Fed believed its policies were “well-positioned to handle the risks”.

Powell emphasised the Fed’s flexibility, saying it can maintain current restrictions “as long as needed” or ease them if the labour market weakens.

Ultimately, Powell concluded, the central bank would “let the data guide our decisions”.

In other Fed commentary, Fed Vice Chair Jefferson said the economy remains strong and he raised possibility of holding if inflation remains more persistent than expected.

Goolsbee noted that “progress on inflation has stalled”.

Richmond’s Barkin repeated the hawkish messaging, saying CPI data has not been supportive of a soft landing and that the Fed should be patient.

Elsewhere, Mester and Bowman also highlighted there is no rush to cut, with Bowman saying only time will tell if rates are “sufficiently restrictive.”

Find out about

Pendal Focus

Australian Share Fund

Crispin Murray,

Head of Equities

And Kashkari said rate cuts may need to be delayed until after 2024. Ultimately, notwithstanding the volume of the rhetoric, this week’s Fedspeak did little to move the needle on the market expectations for just two 2024 cuts, likely beginning in September.

Macro and policy

Australia and NZ

Australia’s March labour data was generally in line with expectations – not much of a retreat after the exceptionally strong February print of 118,000 and notwithstanding job ads showing some loosening.

The data remains indicative of a labour market that probably remains tighter than would have been expected a few months ago.

Total employment was down 6,600, with the decline in part-time employment more than offsetting the rise in full-time employment.

Unemployment ticked up to 3.84% but was below expectations of 3.9%, and the participation rate was down more or less in line with consensus.

Hours worked rebounded strongly over the month, up 0.9% month on month.

New Zealand’s headline CPU increased 0.6% quarter-on-quarter in Q1 2024, with the year-end rate easing down to +4.0% year on year.

The outcome was broadly in line with consensus expectations, albeit somewhat above the RBNZ’s standing forecasts from February’s Modern Policy Statement.

Compositionally, tradables inflation was somewhat softer than expected, while non-tradables inflation was somewhat firmer than expected.

Likewise, goods inflation was a bit softer than expected, while services inflation was firmer than expected.

US

US consumer spending surprised to the upside, rising 0.7% in March.

This strength outpaced forecasts and comes with upward revisions to prior months.

Even excluding volatile items, consumer spending remained robust, climbing 1.1% vs consensus expectations of 0.4%.

Over the last few quarters, consumption has been a consistent contributor to GDP growth and there does not appear to be any sign of weakening in the near future.

This resilience can be attributed to a couple of factors, including a strong rise in real incomes and stock market strength in the first quarter of 2024.

There are some underlying signs of increasing levels of stress on the consumer, with accounts relying on minimum payments increasing past pre-pandemic levels.

Initial jobless claims met expectations and held steady at 212,000, while continuing claims remained relatively flat – suggesting the environment is still stable.

The EVRISI survey of companies in corporate America shows that the aggregate is still in “solid” business conditions.

EU

UK inflation surprised the market, with core CPI dipping slightly to 4.2% but remaining above forecasts.

Headline inflation also came in higher than expected at 3.2%, while Services inflation displayed some resilience – falling only to 6.0%.

While inflation showed some deceleration, it is still front of mind for the Bank of England.

China

There were some signs of stabilisation in China, as Q1 GDP growth beat expectations at 5.3%.

In contrast, retail sales and industrial production missed forecasts.

Despite this, fixed asset investment exceeded estimates, with strong growth in manufacturing and infrastructure.

This suggests targeted policy support is having an effect, however, continued weakness in the real estate market presents a risk.

The EU is expected to announce an investigation into Chinese medical device procurement, raising concerns over future trade relations as it could result in the bloc curtailing Chinese access to its public contracts.

In response to trade practices, President Biden proposed new 25% tariffs on certain Chinese steel and aluminium products.

He also announced an investigation into China’s shipbuilding industry and is considering reinstating tariffs on solar panels.

China’s auto industry has also undergone a dramatic shift, transforming from a net importer to a net exporter in 2023. This rapid rise has sparked anxieties in Western economies.

By facing domestic weakness, China is offloading excess car production through exports at competitive prices.

This aggressive strategy has fuelled trade tensions, with the emergence of the aforementioned tariffs as a potential response.

Australian and US housing

Australia is facing signs of a growing housing crisis.

Record migration is boosting demand, but completions are falling short.

This underbuilding, estimated at a 120,000 annual gap, has been driven by affordability issues.

We are reaching a point where developers cannot make money at current prices and buyers cannot afford more.

This lack of profitability, combined with a shortage of creditworthy contracts, is squeezing supply.

Anecdotally, companies like Mirvac have been keeping sub-contractors on credit support to ensure completions.

In the US, the housing market presents a mixed picture.

March housing starts dropped unexpectedly by 14.7%, while building permits also fell significantly below consensus.

Despite the decline, single family construction continues to trend upwards.

Conversely, apartment starts have plunged 50% from their highs, dragging down overall construction activity which is still at peak levels.

Markets

US earnings season brought some disappointment as positive surprises were below historical trends.

The S&P 500 reported weaker-than-expected earnings for Q1 2024.

The blended earnings growth rate came in at just 0.5%, far below the 3.4% anticipated at the end of the quarter.

While 74% of companies beat earnings estimates, this falls short of historical averages.

Revenue growth also missed expectations.

Some analysts pointed to the strong performance of the Magnificent Seven early in the quarter potentially inflating initial forecasts, but as more companies report, this early boost may start to fade.

In Australian markets it was a sea of red, with losses consistently seen across the market cap spectrum.

Plenty of sectors lost ground by 2% to 3%, with REITs and healthcare suffering the most.

About Jim Taylor and Pendal Focus Australian Share Fund

Drawing on more than 25 years of experience investing in top-performing Australian companies and a background in accounting, Jim manages our Long/Short Fund and co-manages our Imputation Fund. He is a Chartered Accountant with membership of the Australian Institute of Chartered Accountants.

Pendal Focus Australian Share Fund is managed by Crispin Murray. The fund has beaten its benchmark in 14 years of its 18-year history (after fees), across a range of market conditions. Find out more about Pendal Focus Australian Share Fund here.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

It will be a bumpy last mile for inflation, but volatility provides fertile ground for opportunistic trades, argues Pendal deputy portfolio manager, insurance and rates, ANNA HONG

- Jobs data indicates a continued bumpy last mile for inflation

- Volatility provides fertile ground for opportunistic trades

- Why bonds, why now? Find out more from Pendal’s income and fixed interest team

THE jobless rate rose only slightly from 3.7% to 3.8% for March – still well below the Reserve Bank’s expectation of 4.2% by June.

Taken in isolation, the number could suggest the economy has not slowed down significantly.

But that’s not the case. The Australian economy grew at a misery 0.2% in the fourth quarter of 2023.

Employment fell by 6,600.

That’s a small reversal to February’s employment gains, but it’s significant against a backdrop of 60,000 working-age adults joining the labour market every month. More on that below.

Reading the unemployment tea leaves

With three months to go, it is unlikely unemployment will reach the RBA’s 4.2% June forecast.

Will that worry the RBA, potentially delaying local rate cuts? Not necessarily.

Firstly, the RBA is not opposed to low unemployment. High unemployment is not a stated objective.

The Reserve Bank will only be troubled by low unemployment if it feeds through to inflation via strong household consumption.

Right now real household consumption is in negative territory and card-spending data shows little sign of a bounce.

Find out about

Pendal’s Income and Fixed Interest funds

It’s unlikely inflation will catch a second wind from the demand side.

The unemployment number does not need to reach 4.2% before the RBA achieves sufficient disinflation to cut rates.

Furthermore, the headline number does not tell the full story.

Net arrivals into Australia picked up pace again in 2024, adding more labour supply.

Some 60,000 working-age adults are joining the labour market every month and hiring intentions have reduced significantly.

The labour market is loosening and will continue to moderate from here.

What does this mean for investors?

It will be a bumpy last mile for inflation as notoriously laggy indicators like unemployment generate noise.

That volatility provides fertile ground for opportunistic trades, however.

At current valuations, we believe fixed-income investors should be positioning now for lower rates later this year.

About Anna Hong and Pendal’s Income and Fixed Interest team

Anna Hong is Deputy Portfolio Manager, Insurance and Rates, with Pendal’s Income and Fixed Interest team.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia.

With the goal of building the most defensive line of funds in Australia, the team oversees some $20 billion invested across income, composite, pure alpha, global and Australian government strategies.

Find out more about Pendal’s fixed interest strategies here

About Pendal Group

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Pendal’s emerging markets team expects significant interest rate cuts in Mexico and Brazil, increasing their attractiveness. Pendal Global Emerging Markets Opportunities fund co-manager JAMES SYME explains

- Our EM team remains overweight in Mexico and Brazil

- Significant rate cuts expected in both countries

- Find out about Pendal Global Emerging Markets Opportunities fund

ONE of the reasons we maintained overweight positions in Mexico and Brazil was the expectation of big interest rate cuts when disinflation was achieved.

When disinflation did arrive after a strict monetary orthodoxy from their respective central banks in 2021 and 2022, rate cuts were initially slow to follow.

(Though this didn’t prevent MSCI Mexico and MSCI Brazil comfortably outperforming the MSCI EM Index over the last three years.)

With Mexico’s central bank Banxico finally cutting policy rates this month, this piece aims to review the current prospects for policies, economies and equities in the two big Latin American markets.

A broad rate-cutting cycle

Although many developed and emerging market central banks have been cautious on lowering policy interest rates, Latin America has seen a broad rate-cutting cycle that expanded this month to include Mexico.

It’s true that some Latin American central banks that were quick to cut are now turning more cautious – notably Chile and Peru.

But we believe Mexico and Brazil should both be able to deliver hundreds of basis points of cuts in policy interest rates over the next 24 months.

Mexico’s outlook

After inflation rose to 7.6%, Banxico hiked Mexico’s official overnight rate to 11.25% in March 2023. Rates remained at that level until February, pushing inflation down to 4.4%.

Find out about

Pendal Global Emerging Markets Opportunities Fund

In March, Banxico confirmed the beginning of an easing cycle with a broadly anticipated 25-point cut to 11%.

A supporting statement suggested easing would continue through the bank’s next few meetings, which was a positive surprise for markets.

At the time of writing, the consensus holds that Mexican policy rates will decline to 9.5% this year and 7.5% by the end of 2025.

Mexican economic data has softened in recent months, due to a slow in service activity and expectations of reduce agricultural production due to drought.

But overall the Mexican economy continues to do well, supported by a strong US economy.

Mexico’s Purchasing Managers Index (PMI) – a measure of business activity – is well above 50, which indicates manufacturing is expanding.

Fourth-quarter (2023) GDP growth of 2.5% was above expectations and unemployment has declined to near record-low levels.

In addition, we can expect some stimulus ahead of Mexico’s general election, scheduled for June 2.

This economic success comes despite a very high level of real interest rates. A rate-cutting cycle should prove supportive of domestic demand growth and corporate earnings growth.

Brazil outlook

Meanwhile, the rate-setting committee of Brazil’s Banco Central do Brasil unanimously voted for a sixth cut of 50 basis points, bringing rates to 10.75%. (CPI inflation is at 4.5%). A BCB statement shortened the horizon of guidance to only a 50-point cut in May. After this, policy decisions would be data dependent.

Consensus foresees policy rates at 9% this year and 8.5% by the end of next year.

The central bank’s more cautious guidance reflects strong economic growth in the first part of this year.

PMIs look very strong, retail sales and services output have surprised to the upside, and January’s economic activity index rose 0.6%, following an increase of 0.82% in December.

As in Mexico, drought may reduce agricultural output, but not enough to drag down the broader economy.

Lower-than-expected rates

So both countries are experiencing significant rate cuts amid growing economies.

But the Pendal Global Emerging Markets Opportunities team expects a significant positive surprise in the quantum of cuts.

Our model for the interaction between emerging economics and financial markets emphasises reflexivity, where each feeds the other.

We believe the history of booms and busts in individual emerging markets is driven by a process where, generally, everything goes right at the same time, or everything goes wrong at the same time.

In Latin America that tends to mean interest rates overshoot expectations (up or down) through the cycle.

We do not expect this cycle to be any different.

We think interest rates in both Mexico and Brazil will come in much lower than consensus expectations in coming quarters.

This should bring an even more-positive boost to economies, corporate earnings and equity market returns.

About Pendal Global Emerging Markets Opportunities Fund

James Syme, Paul Wimborne and Ada Chan are co-managers of Pendal’s Global Emerging Markets Opportunities Fund.

The fund aims to add value through a combination of country allocation and individual stock selection.

The country allocation process is based on analysis of a country’s economic growth, monetary policy, market liquidity, currency, governance/politics and equity market valuation.

The stock selection process focuses on buying quality growth stocks at attractive valuations.

Find out more about Pendal Global Emerging Markets Opportunities Fund here

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

Effective 9 February 2024, the auditor for the Pendal Australian Long/Short Fund changed from PricewaterhouseCoopers to KPMG. As a result, KPMG will now act as the independent auditor of the Fund’s financial statements.

Effective 16 April 2024, KPMG will also act as the auditor of the Fund’s Compliance Plan.

Consumer inflation accelerated faster expected in the US this week, while wholesale price rises were more moderate. Pendal’s head of government bonds TIM HEXT explains what it means for investors

- US inflation looks sticky at around 3%

- Bonds are nearing the buy zone

- Why bonds, why now? Pendal’s income and fixed interest experts explain

- Browse Pendal’s fixed interest funds

THIS week’s hotter-than-expected US inflation numbers would be disappointing — but not alarming — for the US Federal Reserve.

Late last year the Fed glimpsed core annualised quarterly inflation nearing its 2% target. That’s now given way to a pulse above 4%.

In other words, 0.2% monthly results have been replaced by 0.4% results.

Jumps in rent, car insurance and health

What’s driving this jump in US consumer inflation?

Firstly, rents have remained stubbornly high, ignoring lead indicators that suggest some relief.

Rents and “owners-equivalent rents” (an estimation of what homeowners would pay if they were renting their own home) are both growing at 0.4% a month, rather than the 0.2% suggested by the Zillow rent index.

The direction of these numbers is important, since they represent almost a third of US CPI.

We still expect moderation ahead.

Secondly, a number of services have shown unexpected price spikes.

Car insurance and hospital services jumped sharply in March. The former looks strange, but the latter reflects a surge in medical wages over the past year. Either way service prices are drifting up not down.

Finally, oil prices have shown a slow-but-steady rise since the start of the year, now up 20%.

Although this is excluded directly from core inflation, second-round impacts do matter.

Wholesale prices look better

This week we also saw data from the US producer price index, a measure of inflation at the wholesale level.

The PPI numbers showed a more positive story, reflecting ongoing moderation of price pressures in goods markets.

This is partly a commodity price story (oil aside) and also a falling margin story.

But after almost flat-lining late last year, the data is now showing a steady 0.2% pulse, again showing that disinflation is no longer the main story.

On ANZAC Day we will see new data from the Fed’s preferred inflation reading — the broader core Personal Consumption Expenditures Price Index (excluding food and energy).

(This will arrive two days after Australia’s first-quarter CPI numbers.)

We expect a number around 0.3%, the same as last month.

This means 1% for Q1, or 4% annualised — a meaningful pick up from last year.

This all suggests US inflation will be sticky around 3% for a while.

The Fed needs to see 0.2% outcomes on average before starting any meaningful easing.

US Inflation medium-term outlook

Where does all this leave the medium-term picture?

We are not drifting back into high-inflation territory. For that we would need to see new supply shocks.

Supply chains are normal, wage growth is moderating and margins are still falling.

Even the US fiscal pulse, which remains very strong, is showing some small moderation. So patience is required — and the US Fed has plenty of that.

Economic commentators can choose from a variety of recent Fed speaker quotes to fit their own outlook.

But the one I like best is from New York Federal Reserve governor John Williams.

Find out about

Pendal’s Income and Fixed Interest funds

There was no need to adjust rates in the “very near term” Williams said on Thursday.

“I expect inflation to continue its gradual return to 2%, although there will likely be bumps along the way, as we’ve seen in some recent inflation readings.”

This would allow rate cuts later this year.

Bonds nearing the buy zone

A move higher in yields is seeing opportunities to look at duration once again.

In Australia, the US sell-off has seen our 10-year government bonds near the cash rate and semi governments once again above 5%.

While the US won’t be easing near term, the European Central Bank still looks disposed towards a June rate cut.

Inflation will be sticky above targets for some time. Our core view is inflation over the next five years will average 2.5% in the US and 3% in Australia.

However, this is not consistent with 5.5% and 4.35% cash rates medium term.

In our view, investors should position now for lower rates later this year.

About Tim Hext and Pendal’s Income & Fixed Interest boutique

Tim Hext is a Pendal portfolio manager and head of government bond strategies in our Income and Fixed Interest team.

Tim has extensive experience in banking, financial markets and funding including senior positions with NSW Treasury Corporation (TCorp), Westpac Treasury, Commonwealth Bank of Australia, Deutsche Bank, Bain & Co and Swiss Bank Corporation.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia.

Find out more about Pendal’s fixed interest strategies here

About Pendal

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

In 2023, Pendal became part of Perpetual Limited (ASX:PPT), bringing together two of Australia’s most respected active asset management brands to create a global leader in multi-boutique asset management with autonomous, world-class investment capabilities and a growing leadership position in ESG.