We are notifying you of some important changes relating to the Pendal Concentrated Global Share Fund (Fund).

Following a strategic review of our global equity investment capabilities, we have decided to appoint Barrow, Hanley, Mewhinney & Strauss, LLC (Barrow Hanley) as the Fund’s delegated investment manager. As the Fund’s delegated investment manager, Barrow Hanley will have responsibility for the day-to-day investment management of the Fund.

Barrow Hanley’s appointment will take effect from 31 October 2023.

Pendal Institutional Limited (Pendal) will continue to act as the investment manager of the Fund.

Why are we making the change?

As part of the broader Perpetual Group, we want to ensure our clients have exposure to competitive and differentiated strategies which utilise the investment management capabilities that we believe are best placed to meet the investment objectives of the Fund and are likely to deliver the best outcomes for investors, over the medium to long term.

Barrow Hanley, who are also part of the Perpetual Group, has a quality investment process, an experienced well-resourced team of more than 50 investment professionals, scale and depth of research and an aligned investment style to Pendal. As a result, we consider that Barrow Hanley is better placed to meet the Fund’s investment objectives, over the medium to long term.

What is changing?

Fund name

Effective on or around 31 October 2023, the Fund’s name will change (as set out below) to reflect the appointment of Barrow Hanley as the Fund’s delegated investment manager:

| Current Name | New Name |

| Pendal Concentrated Global Share Fund | Barrow Hanley Concentrated Global Share Fund |

Investment related changes

While the Fund will continue to operate in the same way, there will be some changes to the way the Fund is managed.

Effective from 31 October 2023, these changes include:

- Minimum and maximum number of stocks

The Fund will remain a concentrated portfolio of global shares. However, the minimum and maximum number of stocks held by the Fund will reduce from 35 – 55 stocks to 25 – 40 stocks.

- Asset allocation ranges

The Fund’s asset allocation ranges will change as follows:

| Current Asset Allocation Ranges | New Asset Allocation Ranges |

| • Global Shares 80-100% • Cash 0-20% | • Global Shares 90-100% • Cash 0-10% |

- Emerging markets exposure

The Fund will continue to primarily invest in companies domiciled in developed markets and a 20% maximum limit will be introduced for the Fund’s allocation to emerging markets.

- Labour, Environmental, Social and Ethical Considerations

Like Pendal, Barrow Hanley’s investment approach considers labour standards, environmental, social and ethical (ESG) risks to the extent that they are relevant to the current or future valuation of a stock, although Barrow Hanley’s investment approach does not consider ethical or moral judgements.

Effective from 31 October 2023, the Fund will no longer screen for companies involved in the following activities:

- uranium mining for the purpose of nuclear power generation;

- manufacture, ownership or operation of gambling facilities, gaming services or other forms of wagering;

- mining of thermal coal;

- factory animal farming; and

- weapons systems, components and support systems and services.

The Fund, however, will continue to screen for tobacco production and will not invest in companies that are directly involved in tobacco production, where tobacco production accounts for 10% or more of a company’s gross revenue.

- Buy-sell Spread

Effective from 31 October 2023, the Fund’s buy-sell spread will decrease from 0.40% (0.20% buy/0.20% sell) to 0.25% (0.15% buy/0.10% sell), reflecting lower brokerage costs that are expected to be incurred by the Fund following the appointment of Barrow Hanley.

What will stay the same?

Like Pendal, Barrow Hanley’s investment process for global shares strives to achieve the Fund’s investment objectives by adopting a bottom-up investment approach focused on in-depth fundamental company research to identify companies that temporarily trade below their intrinsic value and offer long term capital growth. Like Pendal, Barrow Hanley also applies a benchmark agnostic and high conviction approach to investing.

The Fund’s benchmark will continue to be the MSCI World ex Australia (Standard) Index (Net Dividends) in AUD and the Fund will still aim to provide a return (before fees, costs and taxes) that exceeds its benchmark over the medium to long term.

Fees and costs

The Fund’s management fee will remain at 0.90% p.a.

However, we estimate that the Fund will incur additional, one-off transaction costs of 0.12% (including brokerage, taxes and fees) as a result of Barrow Hanley’s appointment.

About Barrow Hanley

Based in Dallas, Texas (USA), Barrow Hanley is a diversified investment manager offering value-focused strategies spanning global equities and fixed income. With more than AUD$69 billion in assets under management as at 30 June 2023, Barrow Hanley has been providing quality client outcomes for more than 40 years.

Portfolio Manager Brad Kinkelaar will manage the Fund. Brad has more than 27 years’ industry experience and joined Barrow Hanley in 2017.

What do you need to do?

No action is required. You will be able to continue to invest or withdraw from the Fund in the same way.

An updated PDS reflecting the proposed appointment of Barrow Hanley and outlining the above changes, is available on www.pendalgroup.com. If you would like a hard copy of the PDS, please contact Pendal Customer Relations.

If you have any questions about your investment or would like further information regarding the changes, please contact us on 1300 346 821 (for Australian investors) or +612 9220 2499 (for overseas investors) from Monday to Friday, 8.00am to 5:30pm (Sydney time).

For any questions regarding how these changes may impact your own financial situation, we recommend that you speak to your financial advisor and/or tax accountant.

Pendal Institutional Limited has made the decision to appoint Barrow, Hanley, Mewhinney & Strauss, LLC (Barrow Hanley) to manage a portion of the international shares for the Funds as a delegated investment manager. This change will take effect on 31 October 2023.

As a result, effective from 31 October 2023, the international shares of the Funds will now be managed by Barrow Hanley in addition to J O Hambro Capital Management Limited and Pendal Institutional Limited.

Why are we making the change?

We have decided to implement this change because we believe it is in the best interests of investors and we expect the change will deliver improved investment outcomes for the Funds over the medium to long term.

What will stay the same?

The investment objective, benchmark and management fee for each Fund will remain unchanged.

What do you need to do?

No action is required.

If you have any questions about your investment or would like further information regarding the changes, please contact our Investor Services Team on 1300 346 821 (for Australian investors) or +612 9220 2499 (for overseas investors) from Monday to Friday, 8.30am to 5:30pm (Sydney time). For any questions regarding how this change may impact your own financial situation, we recommend that you speak to your financial advisor and/or tax accountant.

Businesses believe the economy remains on a decent footing, which indicates a soft landing looks on track for now, writes Pendal’s head of bond strategies TIM HEXT

- Why bonds, why now? Pendal’s income and fixed interest experts explain

- Browse Pendal’s fixed interest funds

SPRING will well and truly arrive on Australia’s east coast this Saturday.

The forecast here in Sydney is for 31c.

Weather apps are now so accurate that not only am I confident it will be 31c – I also know it will happen at 2pm.

Here in Pendal’s Income & Fixed Interest team we’re always looking for ways to improve our forecasting ability.

We constantly test economic and market indicators that have a track record of predicting bond and credit markets.

We test hundreds of indicators before narrowing them down to a small number help create quantitative models to assist our portfolio positioning.

Even better if the indicators are not widely tracked. Inflation and unemployment numbers are obsessed over but we need to get ahead of those.

While the level of an indicator is important, we’re usually more interested in the direction of travel.

NAB’s Monthly Business Survey is the richest domestic economic information source.

NAB surveys almost 600 firms on a monthly basis, creating numerous indicators of changes in the economy.

Our testing consistently shows many of the outputs have a strong performance in predicting future market moves — so we pay close attention from a qualitative and quantitative perspective.

What does this month’s survey show? Business managers believe the economy remains on a decent footing and has even slightly picked up from July.

The soft landing looks on track, at least for now.

Courtesy of NAB here are the results:

What the data means

The data in the first section is on a net-balance basis. In other words, firms expecting a deterioration are subtracted from those expecting an improvement.

For conditions and confidence, the average has been around six for several decades.

Therefore, businesses are not confident about the future, but still see current conditions as favourable and even improving.

Mining, transport and utilities lead the way. Retail is weaker but holding up, though confidence is very low.

In summary, rate hikes should matter more (and might in the future) – but for now we are holding up well.

Labour costs remain elevated but showed some relief after July’s surge.

Final product and retail prices also eased, though levels remain elevated and consistent with inflation closer to 5% than 2.5%.

Finally, capacity utilisation still shows tight capacity. On average capacity is at around 81%. A reading of 85.1% is near the highs of mid 2022 and is not showing the freeing up of capacity we would have expected.

Overall, when thinking about where the economy is right now, it’s important to separate the nominal economy from the real economy.

Find out about

Pendal’s Income and Fixed Interest funds

In the nominal economy, population growth of almost 450,000 in the past 12 months has seen some expansion in the economy and increasing demand for goods and services provided by business.

Business, concerned about the future, have been reluctant to add to capacity.

However, on the real side inflation and higher rates has meant on an individual basis we are tightening our belts.

Our money quite simply is not going as far as it was, so individually we are buying fewer goods and services.

Business knows this, and when the population growth falls back to around 250,000 next year the nominal economy will also start feeling this.

For now though our models show rate hikes are still more likely than cuts, though the RBA looks happy to sit out the next few months.

About Tim Hext and Pendal’s Income & Fixed Interest boutique

Tim Hext is a Pendal portfolio manager and head of government bond strategies in our Income and Fixed Interest team.

Tim has extensive experience in banking, financial markets and funding including senior positions with NSW Treasury Corporation (TCorp), Westpac Treasury, Commonwealth Bank of Australia, Deutsche Bank, Bain & Co and Swiss Bank Corporation.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia.

Find out more about Pendal’s fixed interest strategies here

About Pendal

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

In 2023, Pendal became part of Perpetual Limited (ASX:PPT), bringing together two of Australia’s most respected active asset management brands to create a global leader in multi-boutique asset management with autonomous, world-class investment capabilities and a growing leadership position in ESG.

Here are the main factors driving the ASX this week according to our head of equities CRISPIN MURRAY. Reported by portfolio specialist Chris Adams

- NEW ON-DEMAND WEBINAR: Watch Crispin Murray’s bi-annual Beyond The Numbers webinar

- Find out about Pendal Focus Australian Share fund

EQUITY markets continue to drift lower and now sit at an interesting juncture.

Last week the S&P/ASX 300 fell 1.21% and the S&P 500 lost 1.26%.

The bullish perspective is:

- This is a period of consolidation at a seasonally weak time of year

- In the US we are seeing slower inflation and wage growth while the economy holds up — which may mean no recession

- Interest rates have peaked

- This implies earnings are set to grow and valuation ratings rise to drive the market higher

The bearish perspective is:

- Key market leader Apple is falling on concerns over potential Chinese bans, dragging mega caps lower

- The US dollar looks to be breaking back higher

- Bond yields are rising again despite lower inflation data

- Oil is also breaking higher after Saudi Arabia and Russia announced an extension to supply cuts

- Delayed effects of monetary tightening will lead to the economy slowing more materially

- Bond yields, currency and oil are moving in the wrong direction

- In combination with weaker growth, these are warning signs for the market

In Australia we saw the departure of Philip Lowe as Reserve Bank governor, which coincided with abysmal data on productivity and weak GDP data.

This highlights the fundamental challenges facing our economy.

A reliance on immigration and commodities to support growth leaves us vulnerable to an inflation surprise or a growth problem (or both) if the current environment shifts.

US economy

Positive signals continued on the inflation front.

The Atlanta Fed Wage Tracker fell from 5.7% to 5.2% in August, further supporting the “immaculate disinflation” thesis.

The “job switcher” category has now almost fallen into line with the “overall” category.

This supports the case that the main wage-inflation driver was the ramping up of many businesses post-pandemic — and as time goes by this is being resolved.

Combined with slowing growth, companies are becoming wary of chasing too many new hires.

This can be seen in the “job-workers” gap that Goldman Sachs has been estimating. This indicates how job openings have fallen away without unemployment needing to rise materially.

The counter to this view is that wages growth has softened due to a recent drop in inflation which may itself be overstated.

Inflation may start to rise again, given oil price moves and an end to the benefit of supply chain problems unwinding.

This may suggest the declining wage trend is overstated.

On this front the outcome of the United Autoworkers dispute will be an interesting test for persistent wage pressures.

There are 146,000 members seeking a 46% pay increase over four years ($32/hr to $47/hr at the top rate) plus the right to represent workers at electric vehicle battery factories (among other demands).

The union has given the big auto makers until Thursday to come to an agreement.

Economic news continues to support a soft landing. Goldman Sachs, for example, has reduced recession risk to 15%.

One area of contention in the economic debate is how consumers will behave.

Many expect spending to come under pressure with reduced excess saving, a fall in government support in areas such as student loan payments and lower small business rebates, childcare payments and Medicaid coverage.

Goldman Sachs presents a more optimistic view on the consumer which looks at the impact of higher real wages, more hours worked and increased interest income.

They expect this will allow real income growth of 3% in 2024.

This is skewed to higher-income earners due to interest payments, but should translate into consumption growth of 2% without relying on drawing down of savings.

China

Chinese property developer Country Graden got a stay of execution.

It received approval from onshore creditors to extend payments, allowing them to make payments on offshore bonds ahead of a Tuesday deadline. If this went unpaid it would have triggered default clauses on other loans.

Housing remains the key challenge, with sales slowing.

There has been further lifting of homebuyer curbs in tier-two cities. Beijing’s clear message is easing developer liquidity stress and supporting demand for durable goods.

It is worth noting a signal from the Chinese bond market, which reversed last week.

Rising yields suggest the market may be beginning to believe we have seen a peak in growth concerns.

Another issue to watch is Chinese domestic politics. There are stories of unrest over economic performance, while Xi chose not to attend the G20.

Australian economy

Australian GDP grew 0.4% in the June quarter and 2.1% year-on-year.

While in line with expectations, this highlighted some economic challenges. GDP per capita fell 0.3% for the quarter given strong population growth.

When it comes to company earnings, aggregate spending is what counts.

Looking at the breakdown of data:

- Quarterly growth in household consumption was weak at 0.1%. This was partly due to the PCE deflator of 6.1% year-on-year — so nominal consumption is 7.7% year-on-year, but volumes are essentially flat

- Savings rates have fallen to 3.1% — a cycle low.

- Business investment remains strong, with mining up 5.6% year-on-year and non-mining up 9.1%.

- Government spending is strong at 1.8% quarterly, driven by investment at state and federal levels. This highlights how fiscal policy is putting pressure on monetary

- Quarterly exports were strong at 4.3%, again helped by mining

- Nominal GDP fell for the quarter, but is up 3.6% year-on-year

The real shocker in the data is productivity, which fell 1.6% for the quarter, 2.1% year-on-year — and is now back to 2016 level in absolute terms.

This means unit labour costs are rising 7.5%, which is usually tied to services inflation.

Employee compensation growth is strong at 1.6% quarterly and 9.6% yearly. Households continue to find ways to supplement income.

Australia is an economy with slowing growth, reliant on government spending, business investment and commodity exports. All of this is either unsustainable or volatile.

Meanwhile productivity is very weak, which will probably either lead to profits coming under pressure, higher unemployment or more price inflation as companies pass costs on.

Markets

There is a lot of attention on the US dollar, which appears to be breaking higher.

This is usually associated with liquidity tightness and weaker markets.

Oil continues to push higher, supported by Saudi and Russian plans to extend production cuts.

However it is unlikely to be allowed to go much higher, given the impact that can have on global economy and substitution.

Apple had a poor week, falling about 6 per cent on China’s threat of an iPhone ban. This is possibly a warning about shifting too much of its supply chain out of the country.

This week’s annual Apple product day will be an important test of sentiment, given its lead status for tech and the market overall.

It may help inform whether bull or bear thesis plays out.

About Crispin Murray and Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia. Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions.

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

Stocks suited to a high-cost environment | Can commodities be sustainable | Why we’re in a per-capita recession | Assessing company management

ASX-listed accounting software provider Xero recently held its major Xerocon conference in Sydney. Pendal equities analyst ELISE McKAY attended.

- LIVE WEBINAR SEP 7: Register for Crispin Murray’s bi-annual Beyond The Numbers webinar

- Find out about Pendal Focus Australian Share fund

XERO’S annual Xerocon event is known as ‘Coachella for accountants’ – a reference to a Californian rock concert with a cult-like following.

The ASX-listed cloud-accounting platform has a pretty strong following itself now, with more than 3.7 million subscribers in 180 countries.

And that’s led to a pretty good understanding of the state of small-to-medium businesses (SMBs).

Pendal equities analyst Elise McKay has been following Xero closely for years and attended the recent Xerocon event in Sydney.

Here are some take-aways relevant to Xero investors and anyone interested in the state of small business in Australia.

Sales growth under pressure

Small businesses are seeing slower sales growth in Australia, Canada, NZ, the UK and the US, Xero reports.

While all five countries averaged double-digit sales growth in the first half of 2022, this has since slowed to single-digit growth everywhere except the US (where sales were 5% lower).

After adjusting for inflation, Australia was the only country where small businesses typically reported volume growth (an increase in the number of units sold).

“On the positive side, Xero reports that wage pressures are starting to ease in Australia, NZ and the UK,” says McKay.

“Xero now sees wages growing in-line with the long-term average of its data — and materially lower than record highs in 2022.

“While they’re holding up, it’s a difficult time to be running a small business,” says McKay.

One of the ways Xero is responding is by integrating third-party payments systems (such as Stripe or Paypal or Square) which can speed up customer payments.

“There’s been an increase in the number of days before SMBs are paid, putting more pressure on cash flows,” McKay says.

“An integrated payment solution such as a Pay Now button offers customers more ways to pay. As a result, the small business can get paid faster,” she says.

The impact of artificial intelligence

Not surprisingly, SMBs are reporting mixed views on the extent to which artificial intelligence will disrupt their industries.

Like a number of other software developers, Xero expects AI will mostly benefit businesses where the technology is used to boost human expertise rather than replace it.

Xero is adding AI where it can speed up repetitive tasks or provide better insights that help humans focus on higher-value strategic activities.

“For example, helping to better enable reconciliations or provide better forecasting tools around things like cash flow,” says McKay.

“And potentially using generative AI to improve customer support.”

The value of brand

Anyone watching the recent FIFA Women’s World Cup would know Xero made a significant investment in branding at the event.

“The success of the world cup event was not only great for women’s sport, but also Xero’s brand equity,” says McKay.

“Brand equity is a leading indicator of market share.”

The Xerocon event also highlighted the importance of the SMB “eco-sphere”, Mckay says.

Xero now has more than 1000 partners in its ecosystem — relationships which help improve the ‘stickiness’ of the group’s products.

Xero’s app store is also a revenue stream.

“As small businesses adopt more apps, and have more linkages to Xero, they become more integrated and that provides a greater lifetime value.”

That also helps Xero develop cross-selling opportunities and build awareness of its products in new audiences.

About Elise McKay and Pendal Australian share funds

Elise is an investment analyst and portfolio manager with Pendal’s Australian equities team. Elise previously worked as an investment analyst for US fund manager Cartica where she covered a variety of emerging market companies.

She has also worked in investment banking and corporate finance at JP Morgan and Ernst & Young.

Pendal Horizon Sustainable Australian Share Fund is a concentrated portfolio aligned with the transition to a more sustainable, future economy.

Pendal Focus Australian Share Fund is a high-conviction equity fund with a 16-year track record of strong performance in a range of market conditions. The Fund is rated at the highest level by Lonsec, Morningstar and Zenith.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Australia is in a ‘per-capita recession’, which means economic growth is not keeping pace with population growth. TIM HEXT explains the problem and what’s likely to happen next

- Why bonds, why now? Pendal’s income and fixed interest experts explain

- Browse Pendal’s fixed interest funds

AUSTRALIA’S national accounts — quarterly estimates of economic flows such as GDP, consumption, investment, income and saving — land two months after the end of a quarter.

Many therefore ignore them as old news.

But they are the most comprehensive picture of the Australian economy from a macro and micro lens.

So what does the latest data — released today — reveal about Australia at the end of June?

In short, it is a very mixed picture. More than ever how you are feeling depends on where you sit.

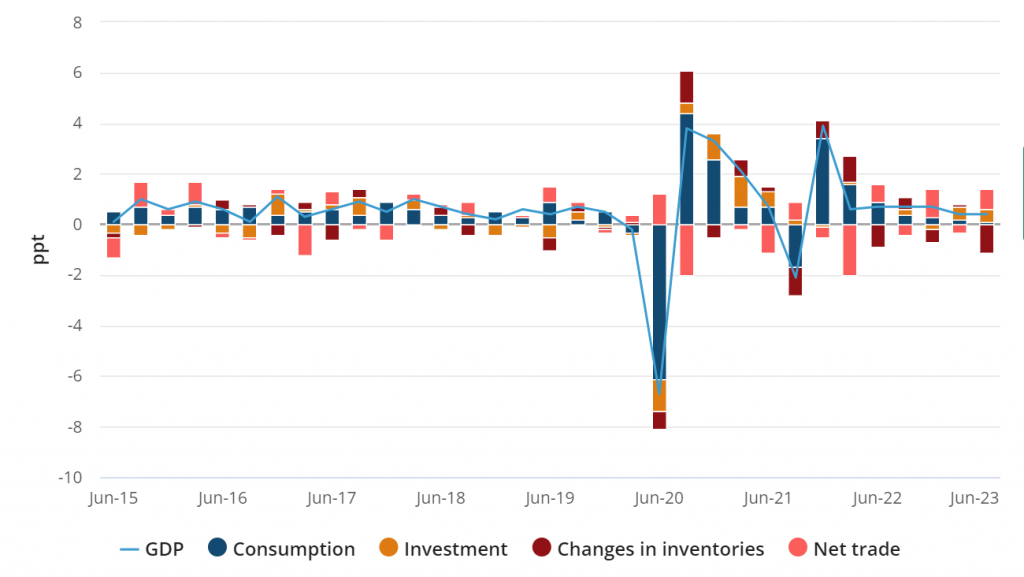

This ABS graph below shows the various contributions:

First, the good news. We are avoiding a recession.

GDP is 2.1% higher than a year ago, though slowing.

It’s been 0.4% for two quarters now and will likely end the year near 1.2% — slightly higher than the RBA forecast of 0.9%.

Inventories are unlikely to be a drag next quarter, but net trade should also stabilise.

Now the bad news. We are clearly in a per-capita recession.

In other words, this level of economic growth is not enough to keep pace with population growth.

Which means the average person is going backwards in their standard of living.

Our population grew by 0.7% in Q2, the economy only 0.4%. GDP per capita is now 0.3% lower than a year ago and 0.6% lower than six months ago.

We are importing growth, not growing from within.

Per-capita recession

Why are we in a per-capita recession?

We are seeing more hours worked as employment rises along with our population. But we are going backwards in GDP per hour worked — down a staggering 2% in the quarter.

This is one of the worst results since deregulation in the 1980s.

Remember this is a volume measure — not price or value.

Productivity is going backwards. It has now gone nowhere since 2016.

Put simply, the RBA is facing labour costs rising at 4% — with stagnant or even negative productivity.

Unless businesses wear the squeeze, inflation is not coming back too far below 4% for some time.

Consumers tighten belts

How is the consumer holding up in the face of rate rises?

Household consumption barely grew in the June quarter at 0.1%. Services were up 0.2% but goods were flat.

Find out about

Pendal’s Income and Fixed Interest funds

We are tightening our belts in discretionary spending, which fell 0.5%.

This is consistent with a soft landing and is not disastrous, at least for now.

Motor vehicle sales are still strong, so maybe cashed-up baby boomers are buying four-wheel drives for their lap of Australia.

Pandemic stimulus savings are a thing of the past — the savings rate has fallen to a cycle low of 3.2%.

In the national accounts savings is a residual (income less consumption) and not directly measured — so it is not always an accurate indicator.

But it shows buffers are falling, albeit very differently across age groups.

The growth we did have came through a rebound in export volumes and ongoing government investment.

This continues a pre-pandemic theme and shows as a country our ongoing reliance on these two sectors, which is concerning.

Likely we will commission another productivity report — having ignored previous recommendations — and kick the can down the road.

The immigration lever

In the near term, the RBA would be a little less comfortable about this national accounts picture.

But we think labour supply via immigration will push unemployment back up to 4% and ease some wage pressures.

This should buy the RBA more time while the full impact of 4% in rate rises in little over a year feeds through. (We are still only 80% of the way there).

If Australia was a company these accounts would be causing analysts to downgrade their outlook. Workers are less productive and costs are rising.

But some of this may still be the lingering impact of the pandemic. Cue discussions on working from home.

The RBA will be hoping this can turn around in the year ahead.

Immigration will slow in the next 12 months to around 1%, because the sharp increase in foreign student numbers was a one-off return from the pandemic.

An outright recession (not just a per capita one) is not a base case — but the chances of it will rise.

Dr Bullock will be facing the dilemma of a slowing economy under full employment and high wages as she takes over as RBA governor in a fortnight.

We wish her luck trying to work out what all this means for rates.

About Tim Hext and Pendal’s Income & Fixed Interest boutique

Tim Hext is a Pendal portfolio manager and head of government bond strategies in our Income and Fixed Interest team.

Tim has extensive experience in banking, financial markets and funding including senior positions with NSW Treasury Corporation (TCorp), Westpac Treasury, Commonwealth Bank of Australia, Deutsche Bank, Bain & Co and Swiss Bank Corporation.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia.

Find out more about Pendal’s fixed interest strategies here

About Pendal

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

In 2023, Pendal became part of Perpetual Limited (ASX:PPT), bringing together two of Australia’s most respected active asset management brands to create a global leader in multi-boutique asset management with autonomous, world-class investment capabilities and a growing leadership position in ESG.

Here are the main factors driving the ASX this week according to Aussie equities analyst ELISE MCKAY. Reported by portfolio specialist Chris Adams

- LIVE WEBINAR SEP 7: Register for Crispin Murray’s bi-annual Beyond The Numbers webinar

- Find out about Pendal Focus Australian Share fund

GLOBAL equity markets remained relatively quiet last week as northern-hemisphere investors made the most of the last days of summer.

Economic data was largely thought to be supportive of a soft landing and markets responded accordingly.

The Nasdaq gained 3.27% and the S&P 500 lifted 2.55%.

A softer-than-expected US employment report on Friday supported the view that the Fed did not need to hike rates again.

The market is now pricing in a 94% chance that Fed holds rates steady in September and 65% chance of a hold in November.

The consensus view is firmly a soft landing, goldilocks scenario.

Data suggests the US is on track to deliver a very solid quarter of GDP growth, with the Atlanta Fed’s GDPNow measure at 5.6% growth.

The market takes a more nuanced view, however, believing consumer strength won’t be sustained with a wave of headwinds closing in.

Real personal spending growth has continued to run hotter than expected. But headwinds associated with a lower savings rate, resumption of student loan repayments and run-down of pandemic excess savings suggest strong personal consumption growth won’t be sustained into Q4.

This raises concerns that a stronger-than-expected economy may over-ride improving trends in inflation and wages, leading to further uncertainty in rates and the Fed.

This runs counter to the soft-landing scenario now priced into the market (and which recent data supports).

Despite dovish data on Friday, US 10-year bond yields counter-intuitively moved 10bps higher. Some pointed to stronger ISM manufacturing data (and particularly a move up in the price index) as less contractionary.

Though lower market liquidity in a quiet week may have exacerbated the move.

In Australia, July inflation data came in well below expectations at 4.9%, down from 5.4% in June.

Softness was largely driven by more volatile items. Excluding these, inflation picked up in July, mainly driven by higher electricity prices and housing purchase-price inflation.

Meanwhile we wrapped up a volatile reporting season with one in eight stocks moving more than 10 per cent up or down – nearly double the average.

This was despite results that were largely in line with expectations and earnings revisions no bigger than normal.

The S&P/ASX 300 gained 2.6% for the week.

The Reserve Bank is expected to keep rates on hold this Tuesday.

The latest Chinese manufacturing data was mixed. Beijing announced a number of easing measures to support the property sector, consumption and currency. This is a step in the right direction, though more is needed.

The global disinflation story continues.

This is supportive for markets as we come close to the end of the tightening cycle and growth in the world’s largest economies remains largely intact.

US economics and policy

At 5.6%, the Atlanta Fed GDPNow – a measure of the growth of the US economy – continues to run well ahead of consensus estimates (which are in the mid-2% range for Q3 GDP).

Who is right? And why the difference?

The Atlanta Fed methodology is model-based and extrapolates the latest economic data for the remainder of a quarter. This compares with human forecasting, which is more likely to mean revert.

The biggest area of differences are:

- Real consumption: GDPNow has extrapolated strong July data while forecasters are expecting weakness in August and September

- Inventory: GDPNow has levels rebounding, which is not yet seen in actual levels across the economy

While GDPNow is a pretty accurate predictive tool, it only has one month of data for the quarter so far.

Find out about

Pendal Horizon Sustainable Australian Share Fund

This raises a concern that a stronger-than-expected economy may swamp improving trends in inflation and wages.

This could create a dilemma for the Fed, leading to further uncertainty which runs counter to the soft-landing scenario now being priced into the market.

US employment data

August’s employment report had non-farm payroll ahead of expectations at 187k new jobs versus 170k expected, but significant downward revisions (-110k) to the prior two months.

The three-month average is now 150k. This is still above the equilibrium needed to keep pace with labour force growth, but it’s moving in the right direction (and is the lowest since 2021).

The unemployment rate surprised to the upside, rising 30bps to 3.8%. This is now the highest unemployment rate since February 2022.

This reflects higher labour force participation which is now at 62.8% – the highest since February 2020 – as well as a higher number of unemployed.

Average hourly earnings also came in below expectations with the private sector rising 0.2% month-on-month, versus 0.3% expected.

In combination with Tuesday’s JOLTS data, which showed lower job vacancies in June (revised lower) and July, this suggests labour market conditions are continuing to loosen.

This should translate into weaker wage pressure, where we are looking for growth in a range of 3.0-3.5% growth, which is more consistent with inflation at 2%.

US inflation

The Fed’s preferred read on inflation – Personal Consumption Expenditures – is a measure of the total amount of goods and services purchased by Americans.

The latest data released on Thursday showed core PCE prices rising 0.22% in June, slightly ahead of consensus (0.20%). The annualised three-month rate is 3.3% and is up 4.2% year-on-year.

Core goods inflation declined further (-0.45% month-on-month) – the second negative read in a row.

This should provide some comfort to the Fed, since Chair Jay Powell said sustained progress was “needed” at Jackson Hole.

Disappointingly, core services (excluding rent) rose 0.5%, breaking the downward trend evident since January. More than half of the increase was due to a volatile financial services component.

US consumer spending

Personal income grew 0.2% in July, slightly weaker than expected. There was a deceleration from +0.6% to +0.4% in wages and salaries.

Consumer spending rose 0.8% in July with all categories stronger, driven by strong retail sales (assisted by Amazon’s Prime Day sale) and discretionary services.

The “Barbenheimer” effect of the popular Barbie and Oppenheimer films showed in the data. Recreational services spending (such as movie tickets) were particularly strong at +10.7% for the month.

Stronger spending and higher taxes contributed to a decline in the savings rate to 3.5%.

Restarting student loan payments should cause a significant headwind to consumption in Q4.

Find out about

Pendal Focus

Australian Share Fund

Crispin Murray,

Head of Equities

Meanwhile, about 75% of pandemic excess savings have now been spent. The remaining 25% are held by higher income households, which are less likely to spend it.

US manufacturing

August US manufacturing data sent a mixed message to the market on Friday.

While remaining in contractionary territory at 47.6 (marginally above consensus at 47) there was a focus on the Institute for Supply Management “prices paid” data.

A surprise jump from 42.6 to 48.4 (versus consensus at 44) raised some concern about how this might roll into core goods inflation, which is now in deflationary territory.

Australia

Inflation data for July came in well below expectations, moderating to 4.9% (consensus at 5.2%) from 5.4% in June.

Softness was largely driven volatile items such as fuel, fruit and veg, as well as travel.

Excluding volatile items and travel, inflation picked up in July, mainly driven by higher electricity prices and housing purchase price inflation.

China

Manufacturing PMI increased to 49.7 in August, the highest reading since March. This was broadly consistent with anecdotal information that the pace of inventory destocking was slowing.

However, non-manufacturing PMI declined to 51, the lowest reading of 2023, as the “reopening boost” from covid faded and construction activity weakened.

We are seeing a drip-feed of policies and support for markets, with concerns around housing, leverage, shadow-banking and capital flight still in focus.

Last week, Beijing delivered a number of easing measures to support the property sector, consumption and currency. It is a positive step in the right direction but more is needed.

Summarising the key announcements:

- China Banks: Cuts to mortgage down-payment ratios and mortgage rates for new and existing mortgages. Looking to stimulate the property sector and address concerns about the risk of a collapse given the increased number of credit risk events among major developers and financial institutions in the past couple of weeks.

- As part of the overall easing package, the PBoC also announced it would cut the reserve requirement ratio for foreign exchange deposits by 200bp to 4% from 6%, effective from September 15. On the same day a year ago, the PBoC cut the FX RRR to 6% from 8%. A cut to 8% from 9% was made on May 15, 2022.

- Ministry of Finance: Cut stamp duty rates by 50% to 5bps. This marks the sixth stamp duty cut in history and the first since 2008.

- China Securities Regulator: Announced it will lower minimum margin requirements for margin finance effective September 8.

- China Securities Regulator: Will tighten IPO activities and major shareholder divestments. This includes major shareholder divestment restrictions if stocks trade below IPO price.

- US Commerce Secretary Raimondo and China counterpart Wang Wentao established a “commercial issues” working group, to find trade/investment solutions, and to meet twice annually. They agreed to set up an “export control enforcement information exchange” to serve as a platform to reduce misunderstandings on export restrictions

- China’s Finance Minister Liu Kun and the National Development and Reform Commission pledged to strengthen policy support and speed-up Govt spending to support the economy

In an example of how China could restimulate the birth rate, South Korea plans to cut mortgage rates for new parents to 1-3% below loans offered by commercial banks.

Markets

August was one of the most volatile Australian earnings seasons in the past 15 years with one in eight stocks moving more than 10% up or down.

This is nearly double the average move and comes despite results being largely in-line with expectations and earnings revisions no larger than normal.

For stocks up more than 10%, 85% of the move was explained by valuation re-rating. For those that moved down more than 10%, 65% of the move was from earnings downgrades.

This possibly implies an overly-bearish outlook going into reporting season.

Cyclical sectors were better than expected, whilst defensives were more likely to disappoint.

Operating margins contracted slightly, resulting in a 2% average hit to EPS.

The bigger impact was increased financing costs, with average interest expense up ~50% year-on-year, which dragged EPS down 6% on average.

Should interest rates stay at current levels, this implies a further 7-14% headwind to EPS in the next couple of years as fixed-rate debt rolls off. The other recurrent theme was upwards revisions to capex budgets, with a median +17% increase in capex for the half and +6% increase in consensus forecast for capex spending over FY24 / 25, largely driven by resources sector. This is driven by cost overruns and inflation rather than growth.

About Elise McKay and Pendal Australian share funds

Elise is an investment analyst and portfolio manager with Pendal’s Australian equities team. Elise previously worked as an investment analyst for US fund manager Cartica where she covered a variety of emerging market companies.

She has also worked in investment banking and corporate finance at JP Morgan and Ernst & Young.

Pendal Horizon Sustainable Australian Share Fund is a concentrated portfolio aligned with the transition to a more sustainable, future economy.

Pendal Focus Australian Share Fund is a high-conviction equity fund with a 16-year track record of strong performance in a range of market conditions. The Fund is rated at the highest level by Lonsec, Morningstar and Zenith.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Identifying the best ASX industrials | Where to next for inflation | Solving AI’s big problem

The best-received earnings results in the ASX industrials sector had a few things in common. Pendal equities analyst ANTHONY MORAN explains

- Pricing power, interest expense, business cycles matter

- The weather makes a big difference to earnings too

- LIVE WEBINAR SEP 7: Register for Crispin Murray’s bi-annual Beyond The Numbers webinar

WHAT did the best-received results have in common this ASX earnings season?

Among industrials — which includes industries such as transportation and machinery — it was all about pricing power, cost of debt and where a company sits in its business cycle, says Pendal analyst Anthony Moran.

This marked a return to more typical themes after cost control, staffing and inflation dominated post-Covid reporting, Moran says.

The power of pricing

“Calendar 22 was a story of strong inflation … and companies were then all about doing what they could to keep up with inflation.

“What we’ve seen in the past six months is that input costs have eased in some cases,” Moran says, citing freight and energy costs.

“Some companies with pricing power have not only kept up with prices, but also been able to achieve some margin expansion. James Hardie is a really good example of that.”

In James Hardies’ case, volumes declined as the construction sector in the United States struggled, but margins increased.

“They’ve shown a lot of pricing power because they’ve got a very strong value proposition and a very strong market position. And we’ve seen some of their input costs come off,” Moran says, adding that it was a similar story for Boral in Australia.

“The contrasting example is [plumbing manufacturing company] Reliance Worldwide. By the nature of their products, they only have limited pricing power, particularly in the US.”

Cost of debt

Interest expense — the cost of debt — was a second theme emerging in the industrials sector.

“I’ve had a numebr of companies surprise to the upside, materially, on interest expense for financial year 2024,” says Moran.

“Because interest rates have gone up so much, it’s meant a few stocks have had 5 per cent downgrades just on interest expense.

“Amcor surprised on the extent of their interest expense step up in fiscal year 2024.”

Fellow packaging group Orora had a similar interest headwind, which took the edge off a positive 2024 outlook.

With interest rates higher and interest expenses normalising, an imbalance in price-to-earnings and Enterprise Value / EBITDA metrics in some stocks over recent years is coming back into alignment, Moran says.

“One of the reasons the PE ratio looked so cheap was the low interest expense, even when a company had a lot of debt on its balance sheet.”

Business cycles matter

A third theme of the earnings season was where companies are in their business cycles, Moran says.

“Not all sectors and countries economies are moving on one track.

“There are a variety of industry cycles running at different stages.

“So companies are seeing a range of end-demand experiences — and that could be driven by the country in which they operate”.

Moran refers to James Hardie and Reliance as cases in point.

Pendal Focus Australian Share Fund

Now rated at the highest level by Lonsec, Morningstar and Zenith

Due to the vagaries of the US housing cycle, strategies of home builders and the preponderance of fixed rate mortgages, there has an unexpected uptick in new housing starts, but the renovation sector remains in the doldrums.

“While James Hardie’s volumes were quite weak last half, it has exposure to this upside in new homes and that’s benefited their outlook.

By contrast, Reliance is exposed to the repair and remodel market … and hasn’t benefited from upside in new homes.”

And don’t forget the weather

As always, the weather matters, Moran says — particularly for building materials companies such as BlueScope and Boral.

“BlueScope has a diversified exposure to the Australian construction industry. Its volumes surprised to the upside in the last half year, and they will be flat in the current six months. It’s not seeing any great weakness,” Moran says.

“It’s not just resilient demand though — it’s also the good weather, which has moved from La Nina in FY22 to more benign conditions recently.

“That’s quite significant for Australian construction companies.”

About Anthony Moran

Anthony Moran is an analyst with over 15 years of experience covering a range of Australian and international sectors. His sector coverage has included Australian Industrials and Energy, Building Materials, Capital Goods, Engineering & Construction, Transport, Telcos, REITs, Utilities and Infrastructure.

He has previously worked as an equity analyst for AllianceBernstein and Macquarie Group, spending a further two years as a management consultant at Port Jackson Partners and two years as an institutional research sales executive with Deutsche Bank.

Anthony is a CFA Charterholder and holds bachelor’s degrees in Commerce and Law from the University of Sydney.