IT’S almost a year to the day since NSW and Victoria exited lockdowns.

NSW premier Dominic Perrottet declared “freedom day” on October 11 last year as millions of Australians celebrated at pubs and restaurants in Sydney and Melbourne.

Today’s headlines couldn’t be further from that optimism. Recession. Inflation. Strikes. Oil prices. War.

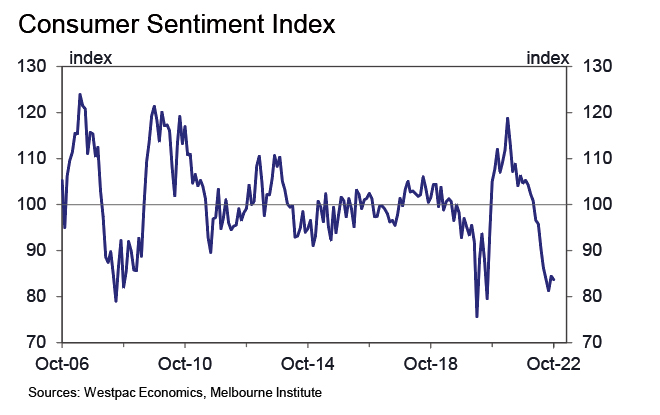

A stream of bad news has led to near-historic lows in consumer confidence.

With central banks unusually coordinated in rapid-fire rate hikes, it’s reasonable to be concerned.

RBA deputy governor Michelle Bullock’s speech yesterday was a timely reminder of the central bank’s objectives: currency stability, full employment and the welfare of the people of Australia.

That differs from the US Federal Reserve’s dual mandate of price stability and maximum sustainable employment.

Welfare of the people. A small but important difference.

This objective influenced the RBA’s discussions, leading to an earlier slowdown in rate hikes this month.

Recessions bring a real human toll that can lead to a prolonged economic slowdown.

Research has shown that people out of work for extended periods become so disconnected from labour markets, that they struggle to find jobs even after the economy has recovered.

The effects of recession on labour force shrinkage is evident in Europe and the US. Participation rates in the US have barely budged despite some of the tightest labour market conditions on record.

In Australia the belt-tightening has started with consumer goods spending growth flat-lining in 2022.

In the RBA’s latest Financial Stability Review, the Reserve Bank stress-tested the impact of a 3.6% cash rate target. About 40% of people would experience a -20% to 0% reduction in cash flows, with almost 15% going into negative cash flows.

The psychological impact of watching savings buffers evaporate would likely increase the pace of decline in consumer spending as rates increased.

The peak rate could very well be lower than the market pricing of 3.6%.

Markets will remain choppy with upcoming CPI releases.

As consumers head into the first fully open Christmas in three years, many will travel to visit families they have not seen in years.

Anyone booking travel will be aware of the high prices of airfares, particularly across the Tasman.

These will feed into CPI – as possibly a last hurrah before belt-tightening in 2023.

Find out about

Pendal’s Income and Fixed Interest funds

About Anna Hong and Pendal’s Income and Fixed Interest team

Anna Hong is an assistant portfolio manager with Pendal’s Income and Fixed Interest team.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia. In 2020 the team won the Australian Fixed Interest category in the Zenith awards.

With the goal of building the most defensive line of funds in Australia, the team oversees A$22 billion invested across income, composite, pure alpha, global and Australian government strategies.

Find out more about Pendal’s fixed interest strategies here

About Pendal Group

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Here are the main factors driving the ASX this week according to portfolio manager Jim Taylor. Reported by portfolio specialist Chris Adams

THE US CPI print, which dominated headlines last week, reminded markets to expect the unexpected.

The highly anticipated data point came in hotter than expected and even the most dovish will now expect 75bps moves in November and December.

The federal funds rate predictions also shifted to just a tick under 5% in Q1 2023, resuming the debate on the likelihood of a recession.

Inexplicably, on the day of the print the market went bottom-left to top-right – which no one foresaw but plenty rationalised.

These theories were swiftly discarded as markets reversed back into the red on Friday.

The situation in the UK highlighted that material policy errors need to be near of mind when forming expectations in this highly unpredictable environment.

Australian markets fared quite well despite a down week for commodities.

The flat performance was mainly attributed to the positive earnings outcomes in the financials sector.

Economics and policy

The Fed’s stance was split in two last week.

At the start, the commentary was somewhat conciliatory and balanced, indicating that past short-and-sharp rate rises will need time to work through the economy.

Current moderation in demand was due to economic tightening being “only partly realised so far”, added Fed vice-chairwoman Lael Brainard.

Chicago’s Fed president Evans warned of the cost of “overshooting” rate rises.

But after the CPI print, the Fed took a more hawkish tone. Key members flagged the prospect of a 5% fed fund rate at the end of 2023.

These latest Fed minute show a greater degree of differing opinions than usual. This is evident in opinions on goods and services, noting relief in key pressure points such as shipping costs, delivery, and rising inventories. This suggests supply bottlenecks have passed their peak.

Find out about

Pendal Focus

Australian Share Fund

Crispin Murray,

Head of Equities

The hawks, however, claim this small improvement does not offset continued elevated rates in core goods prices.

Labour markets appear to be moving towards a better balance, with a lower rate of job turnover, moderation in employment growth and increase in labour force participation rate.

Concerns of a wage-price spiral weighed on sentiment since some expect this may occur sooner rather than later.

Meanwhile it was a tumultuous week in the UK.

The Truss administration backflipped on several key economic policies it defended weeks prior – most notably scrapping plans to freeze UK tax next year.

This was an attempt to settle the markets and allow pension funds to extricate themselves from the recent liquidity crisis.

Attempting to salvage the situation, the PM sacked the treasury chief and back-peddled on her vision for a low-tax environment.

This fanned the political flames, stressing an already nervous market.

US CPI Print

The US CPI rose +0.4% MoM and 8.2% YoY, which was above the consensus of 0.2% and 8.1%.

Core CPI (ex food & energy) surged another 0.6% to 6.6% versus 0.4% and 6.5% consensus.

Shelter and medical care prices also saw big increases.

US inflation is still elevated, though longer-term expectations are fortunately still anchored.

For the first time in two years we saw core services inflation (6.7% YoY) exceed the core goods inflation (6.6%).

This indicates that goods inflation is passing the baton to services. This is alarming for markets, since inflation in services tends to be far more persistent than goods.

Services make up about 75% of the core index, meaning it triples the influence of core goods.

Overall, core goods inflation was relatively flat, with a 1.1% drop in used car prices offsetting a 0.7% increase in new cars. There were smaller gains in tools, tobacco and other recreational goods.

In contrast, core services inflation was up 0.8% MoM – the highest reading of the cycle and the biggest increase in 40 years.

This was largely due to prices (ex-energy) increasing by 0.8%, acceleration in rents and hefty increases in health and vehicle insurance components.

Shelter continued to anchor core inflation, rising 0.75%/6.6% MoM/YoY – accelerating from the July and August run rates.

Owners Equivalent Rent rose 0.8% which was the highest rise since 1990. When looking at current climate however, data suggests rents are beginning to roll over.

Excluding shelter, services still were up 0.9% Additionally, transportation services inflation was up 1.9%, medical care up 1% and airline fares rose 0.84% MoM.

The PPI also rose above consensus (+0.4%), with a 1.2% jump in food prices and 0.7% increase in energy prices.

Similarly with the CPI, the core increase was primarily in services, up 0.6%, while goods remained flat. One positive note is we are not seeing a continued escalation of margins.

Additional non-CPI data was also released last week. Notably, the Michigan consumer sentiment index rose to 59.8 from 58.6 which was slightly above consensus. This suggests the covid-induced savings bubble has continued to support spending, despite it being depressed overall.

Five-to-ten-year inflation expectations rose to 2.9% from 2.7%, reversing the August drop. The one-year expectations rose more materially by 0.4% MoM to 5.1% YoY, the first rise since March.

These increased expectations could pose troublesome for those wanting the Fed to start putting their foot on the breaks, given how closely the policy makers watch this number.

Australia

Similar to the rest of the world, consumer sentiment in Australia remains firmly in a recessionary environment.

Despite this, consumer behaviour continues to contradict with business conditions remaining very robust throughout Q3.

Importantly, low consumer confidence is not driven by labour as Australians remain highly active in the jobs market. Unemployment expectations are reaching all-time lows with no real slowdown in sight for the hiring movement.

Selling price inflation and wage costs dipped slightly but remain strong overall. Measures of price pressures eased somewhat in September but remained elevated in levels terms.

Labour costs eased 30bps to 3.1% QoQ after peaking in July. Purchase costs eased 60bp to 3.8% QoQ while final product prices eased 40bps to +2.1% QoQ.

These data points all point towards robust economic conditions despite inflation remaining elevated.

Markets

Volatility was the name of the game last week. The day of the CPI print was only the fifth time in history the S&P500 has opened down 2% and finished up 2%. It was also the first time the Dow has fallen 5% and risen 8% in a single session.

The gains were short lived as a sharp reversal occurred on Friday.

Bond yields were choppy, ending up for the week. Brent oil was up 2.4% alongside copper which bounced down and up 1%. The AUD traded down to 61.7c, was swept in the CPI euphoria and ended back at 63c.

It is predicted that inflation concerns will not be conclusively taken off the Fed agenda until corporate margins/earnings start coming down. As of now, there is not much evidence of broad-based margin/earnings issues yet.

The Australian market was supported last week by the performance of the major banks (Financials +3%) and Consumer Staples (0.4%). Large-cap miners were flat for the week with the brunt of the pain in resources felt in the mid and small-cap space.

The REITs (-2.2%) sector struggled due to big discounts to book value and too much gearing. It is becoming increasingly hard to identify the circuit breaker to this valuation down spiral.

Information Technology (-3%), Health Care (-2.9%) and metals had another tough week.

About Jim Taylor and Pendal Focus Australian Share Fund

Drawing on more than 25 years of experience investing in top-performing Australian companies and a background in accounting, Jim manages our Long/Short Fund and co-manages our Imputation Fund. He is a Chartered Accountant with membership of the Australian Institute of Chartered Accountants.

Pendal Focus Australian Share Fund is managed by Crispin Murray. The fund has beaten its benchmark in 14 years of its 18-year history (after fees), across a range of market conditions. Find out more about Pendal Focus Australian Share Fund here.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

A monthly insight from James Syme, Paul Wimborne and Ada Chan, co-managers of Pendal’s Global Emerging Markets Opportunities Fund

ONE of the main drivers of global financial markets in 2022 has been the strength of the US dollar (and the weakness of other global currencies), driven by tightening US financial conditions.

The dollar is the preferred currency for international trade invoices and cross-border financial claims.

The global financial cycle is essentially a dollar cycle – and an aggressively tightening Federal Reserve has a chilling effect on non-US economies and non-US financial markets.

Emerging markets can generally be divided into two broad groups:

- Net exporters that tend to run current account surpluses (such as China, Korea and Taiwan, but also UAE and Saudi Arabia)

- Net importers that tend to run current account deficits (such as Brazil, Mexico, South Africa and India).

Historically, the first group have broadly tended towards high sensitivity to global growth and the second to global financial liquidity.

So it’s normally been the second group that has the worst currency and equity market performance in strong dollar/tight liquidity environments.

In 2013 the Fed announced an intention to reduce the buying of US treasuries.

The hardest-hit emerging markets were Brazil, India, Indonesia, South Africa and Turkey. They were dubbed the “fragile five” by one market participant.

This time it’s different

This year has decidedly not followed that pattern.

In the first nine months of 2022, the only major EM currencies to strengthen against the dollar were the Brazilian real and the Mexican peso.

The Indian rupee and Indonesian rupiah were also relatively strong, declining 6.8% and 9.4% respectively.

Find out about

Pendal Global Emerging Markets Opportunities Fund

By comparison, the Korean won fell 20.4%, the Taiwanese dollar 14.7% and the Chinese renminbi 12%, despite those economies running big current account surpluses.

This pattern is very interesting and points to a real change in leadership in the asset class.

We have previously commented on the positive effect high commodity prices have on commodity economies such as Brazil – and to a lesser extent Mexico and Indonesia.

This continues to play out in economic data. Recent PMI surveys are 51.1 in Brazil and 47.3 in Korea, for example.

Other drivers at play

The explanation is that there are other drivers at play.

One is the Japanese yen.

With ongoing monetisation of debt and low inflation, Japanese monetary policy remains very loose, leading to about a 25% depreciation of the yen against the dollar year-to-date.

Given the tight trade relationships between the four big East Asian economies (both as partners and as competitors), this has put significant downward pressure on the currencies of China, Korea and Taiwan.

Another driver is energy balances.

The huge moves in oil, gas and coal prices in the last two years have been a boost for energy exporters (or large consumers who also have large domestic production).

The value of Indonesia’s exports of oil and gas in the last three months were $US4.6 billion, compared with $US3 billion for the same period in 2019.

By comparison, the cost of Korea’s crude oil imports in the third quarter of 2022 was $US31 billion, compared to $US17 billion in the third quarter of 2019.

At a broad regional level, North America and the Arab Gulf are in extremely strong positions, while Europe and East Asia face a powerful drag on their external balances and their growth.

Although all four East Asian economies have very substantial ability to use their large foreign exchange reserves to support their currencies, their desire to support exports has meant this has been limited.

Japan did intervene last month, but the ongoing economic weakness in China and Japan mean major intervention was unlikely.

By comparison, both India and Indonesia have intervened, supporting their currencies, reducing imported inflation and facilitating economic growth.

Sign of change

We think 2022 is a sign of a change in market leadership in emerging markets.

The markets that might be expected to underperform instead may be the best performers.

We believe that can continue with either a stronger or weaker US dollar.

About Pendal Global Emerging Markets Opportunities Fund

James Syme, Paul Wimborne and Ada Chan are co-managers of Pendal’s Global Emerging Markets Opportunities Fund.

The fund aims to add value through a combination of country allocation and individual stock selection.

The country allocation process is based on analysis of a country’s economic growth, monetary policy, market liquidity, currency, governance/politics and equity market valuation.

The stock selection process focuses on buying quality growth stocks at attractive valuations.

Find out more about Pendal Global Emerging Markets Opportunities Fund here

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

An asset class snapshot | bond-buying in a hiking cycle | Signs to watch for a turning point | US earnings outlook

In the current environment tightening must come from a big reduction in government spending to support private sector growth, says assistant portfolio manager Anna Hong

THE RBA’s Financial Stability Review sheds light on last week’s decision to limit the cash rate rise to 25bps.

It shows the Reserve Bank is keeping a close eye on the ability of households to absorb the impact of rate rises instead of blindly following other central banks.

In this world of instant gratification the effect of monetary policy is no different. If inflation has not reversed since the last hike, let’s go again, more this time.

Our collective impatience meant the Reserve Bank’s decision to hike 25bps stuck out like a sore thumb in a sea of 50bps and 75bps rate hikes from other central banks.

These consecutive rate hikes ignore the fact that the cash rate target is a blunt instrument that requires time to trickle into the economy.

Its ability to control demand in a supply-shocked environment is made even harder by large-scale Covid stimulus programs we’ve seen in most of developed economies.

In Australia, the fiscal stimulus – JobKeeper, JobSeeker – was effective because it skipped part one of the song and went straight to part two – the household balance sheet.

Interest rates alone will not be sufficient to unwind demand supported by the lingering effects of the stimulus.

The federal government will need to deliver a sensible budget to help the RBA keep the Australian economy on track.

Despite signs of a roaring economy – real GDP growth, low unemployment, strong business conditions – household nerves about the future have led to near-historic lows in consumer confidence.

A never-ending increase to interest debt-servicing costs will only make consumers more pessimistic, eventually hurting business profitability in the form of lower consumer demand and higher cost of credit.

Fiscal policy is the circuit breaker required to stop that trajectory.

Productivity drives real growth. That comes from private sector growth.

In the current environment, tightening must also come from a large reduction in government spending so the private sector can take over.

A productivity-driven expansion will ensure the economy stays on the right track with a lift in real wages, ultimately creating sustainable growth.

Are we still the lucky country? The upcoming federal budget will paint a better picture of what’s ahead.

Find out about

Pendal’s Income and Fixed Interest funds

About Anna Hong and Pendal’s Income and Fixed Interest team

Anna Hong is an assistant portfolio manager with Pendal’s Income and Fixed Interest team.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia. In 2020 the team won the Australian Fixed Interest category in the Zenith awards.

With the goal of building the most defensive line of funds in Australia, the team oversees A$22 billion invested across income, composite, pure alpha, global and Australian government strategies.

Find out more about Pendal’s fixed interest strategies here

About Pendal Group

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Here are the main factors driving the ASX this week according to our head of equities Crispin Murray. Reported by portfolio specialist Chris Adams.

THE sharp equity market rally last week was fuelled by very bearish positioning and ignited by weak job opening and manufacturing data. There were also hopes that emerging financial strain would prompt a Fed pivot.

But the “good is bad” phase proved short-lived. Solid US employment data emphasised a tight labour market, while OPEC+ quota cuts sent the price of oil higher.

The S&P 500 ended the week up 1.56% and sitting at a key technical support level of 3500-3600.

There is scope for the bear market bounce to continue back to the next technical level of 3900-4000, but data trends are not supportive.

The US economy remains resilient with insufficient signs of weakness. Meanwhile inflation remains stubbornly high – with the additional risk that fuel prices are rising again.

The S&P/ASX 300 was up 4.5% last week and continues to outperform. It’s down 6% for 2022, while the S&P 500 has lost 22.7%.

This is due to currency moves, the index sector mix and a defiant RBA.

Our central bank raised rates only 25bps. It’s crossing fingers and toes that the rest of the world fixes the inflation problem and it won’t have to induce a recession here.

Sustainable and

Responsible Investments

Fund Manager of the Year

Economics and policy

US job openings were a lot weaker than expected, which is good for markets. The ratio of openings to unemployed remains very high, but the quarterly downward trend is encouraging.

There was also a fall in job “quits” which is a signal people see less opportunity to move.

Job layoffs remain low, which is also constructive. The best scenario is one where the job market loosens via less hiring (ie less labour demand) but layoffs remain limited (ie more supply). A big increase in layoffs is more likely to trigger a recession.

The US is now 50% of the way to reducing the gap between jobs and workers to a level where wages should slow sufficiently, according to a Goldman Sachs indicator.

Wage growth appears to be running over 5% annualised on most measures and needs to drop below 4%.

However the relief on this data was short-lived. Payroll and employment data reinforced the tight labour market.

This is the Fed’s key policy problem, since they risk recession in bringing this down.

There is much focus on the lessons of the 1970s, where the Fed heeded political pressure and loosened too soon. This meant it had to go through three phases of tightening to finally solve the problem.

US payroll data was in line with expectations (+263k jobs). The household survey was a bit stronger than consensus, with the unemployment rate falling to 3.5% due to a 0.1% drop in the participation rate.

The market did not like this because:

- Other data points had been weaker – and the market was hoping for more of that

- A tight labour market supports wage growth, reinforcing the Fed’s need to tighten rates further and potentially risk recession

- The participation rate looked to be increasing, but it fell this month as hopes of greater labour supply faded. The gap in participation compared to pre-Covid levels is mainly in older people and this is unlikely to return

Payrolls need to get down to 50-75k per month to be at a level where wages may slow to the target level.

The household survey of wage growth among production and non-supervisory workers is seen as a better proxy of underlying wage growth. It was stable month-on-month, landing at 5.8% year-on-year. This is consistent with inflation running between 4 and 4.5%.

Pendal Focus Australian Share Fund

Now rated at the highest level by Lonsec, Morningstar and Zenith

Mixed signs on the state of the economy are another challenge for markets.

The bears can point to measures such as housing and trucking as signs the economy is slowing sharply. But consumers continue to hold up – as do hiring intentions.

One of the signals from the employment report is that nominal incomes continue to grow – and in fact are picking up in real terms as inflation slows. This makes the Fed’s job harder.

Underlying resilience in the US economy is also evident in a pick-up in the Atlanta Fed GDP Now tracker. It’s re-accelerated in the last couple of weeks, driven by net exports and the consumer.

The Cleveland Fed inflation tracker is another real-time indicator not helping the case for a pivot. It continues to indicate inflation running at 0.4-0.5% month-on-month.

We will see the CPI print released on Wednesday. This will be a key determinate of market direction.

Oil

OPEC+ surprised the market with a bigger-than-expected quota cut of 2 million barrels per day.

It is worth bearing in mind that many members are already producing below their quotas. By a rough estimate the real production impact would be about half of that announced. The market is expect 0.8 to 1.2m barrels to be taken out of the market.

There will be another meeting in early December to review the impact, so this will be in place for at least two more months.

This was not designed as a direct attack on the US, despite the latter’s reaction.

Instead, OPEC is concerned about the impact of recession on demand – and also that the oil price appears to have disconnected from fundamentals.

When you compare the oil price to inventory levels there is probably a US$20 gap.

OPEC also believes the inability to reach production quotas shows a lot of countries are not investing in capacity – which will make the oil supply-and-demand balance more precarious in the future.

This requires higher prices to incentivise investment. In response to rhetoric from the US, OPEC is also pointing to factors such as levies, carbon taxes and fuel standards as reasons why petrol prices are so high in the west. These, they say, are in the hands of western governments to resolve – if they want to.

Adviser Sam is invested

in making our world

A better place.

Watch as Sam meets a

mum rebuilding her life

thanks to responsible

investing

There is now upside risk to the oil price because:

1. Chinese refinery production is ramping up (counter to OPEC’s concern over recession)

2. Another round of sanctions on Russian oil will start in the next few months, creating more friction in oil markets

3. SPR releases will slow from 1m barrels per day to about 500k through to the year’s end.

In combination, these could have an impact of 1.5m to 2m barrels a day on oil supply-and-demand balance, more than offsetting any slowdown.

Australia

The Reserve Bank got global attention last week as people thought the lower-than-expected 25bp hike might signal the beginning of a small pivot from central banks.

We find it hard to draw any broader global conclusions from the RBA’s move.

It could be slowing rate rises to gather more information and gauge the effect of tightening to avoid a policy mistake and recession. The likely rationale includes the notions that:

1. Australian wages have not risen as quickly as other nations, so the RBA has less to do at the moment in loosening the labour market

2. Australia has more short-rate sensitivity due to floating-rate mortgages

3. The RBA has more meetings than the Fed, so they will get the opportunity to re-appraise in early November with more data.

4. They are probably anticipating a reasonably tight federal budget, ie no fiscal stimulus, unlike the UK

5. They will be expecting the tightening in the ROW to help contain inflationary pressures

Also, the RBA has already tightened more than other regions in Europe and Canada, though not as much as the US.

There is some risk to the RBA stance.

While wages growth is slower than the US, surveys indicate it is still rising, unlike the US.

Should this continue – and the Australian dollar weakens – we could see inflationary pressures build, forcing the RBA to go harder again.

For now the ASX can take comfort from the more benign approach from the RBA, with strength across all sectors and resources and domestic cyclicals running. Consumer staples was the laggard.

Markets

The trifecta of higher bond yields, oil prices and the USD is a challenge for equities.

Friday’s sell-off leaves the US market in a finely balanced position in the near term.

The bounce earlier in the week had all the hallmarks of the start of at least a bear market rally, with some extremes in terms of buying / selling ratios.

On average, these rallies are 15% over 32 days, so the 6% in 4 days looked like it should have had legs.

Wednesday’s CPI print is likely to have a large bearing on whether the S&P 500 gets back to 3900 in the near term.

About Crispin Murray and Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia. Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Pendal’s Tim Hext, head of government bond strategies and Steve Campbell, head of cash strategies explain why.

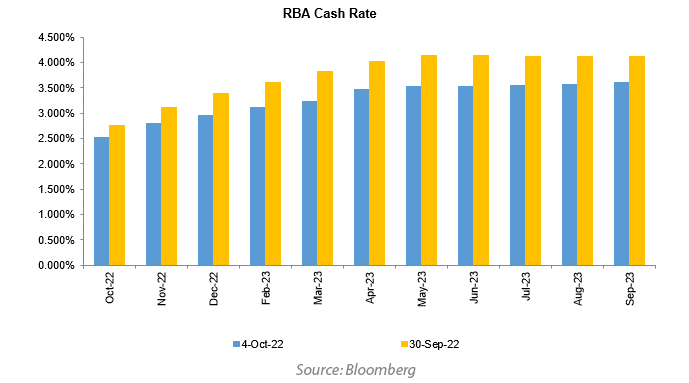

The Reserve Bank of Australia (RBA) surprised the market yesterday when raising the cash rate by 25 basis points to 2.60%.

The market had assigned an 85% probability of the RBA hiking by 50 basis points.

Governor Lowe dropped a hint last month that the pace of tightening would slow when he commented that “the case for a slower pace of increase in interest rates becomes stronger as the level of the cash rate rises”.

The market rallied following this comment which indicated 25 rather than 50 was more likely to happen in the nearer term.

Yesterday’s 25bp hike means the RBA has now raised rates from 0.1% to 2.6% in 5 months. This is now seen as the bottom end of neutral territory.

Markets were looking for a 50bp hike given the hawkish party happening globally, led by Jerome Powell and his recent 75bp hike.

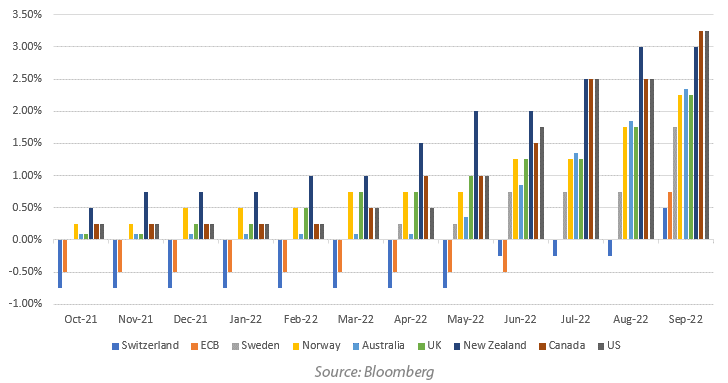

It was a case of a rising tide lifts all boats. As the following graph shows, central banks globally continued to tighten monetary policy aggressively in September.

In Sweden the Riksbank tightened by a more than expected 100 basis points.

The Federal Reserve, Bank of Canada, European Central Bank and Swiss National Bank (the last remaining member of the negative interest rate policy club) all raised their rates by 75 basis points.

The RBA, Bank of England and Norges Bank were all in the 50 basis point hike camp last month.

However, unlike other central banks, the RBA has shown some patience with this move. Rate hikes normally take 2 to 3 months to show up in any data given lags between the RBA hikes and the higher rates hitting mortgages.

One of the key lines out of the statement yesterday was “One source of uncertainty is the outlook for the global economy, which has deteriorated recently”.

The UK Government’s mini budget released last month was the source of much financial turmoil last month, the moves (and lack of liquidity) were astonishing late in the month.

Find out about

Pendal’s Income and Fixed Interest funds

The RBA is also acutely aware of the large amount of fixed rate mortgages that roll off over 2023.

The national accounts also reflected a drop in the household savings rate, indicating that the large savings buffers that households have built over the past 2 years may start to be called upon as cost of living pressures rise.

The decision to raise by a less than expected 25 basis points yesterday resulted in the market pricing in a terminal cash rate of 3.6% in 1 years time. At the end of September this was around 4.1%.

Back around neutral the RBA now thinks it has time on its side.

Their hope will be for better behaved CPI numbers in the quarters ahead.

The Sep Quarter CPI, due out later this month, should show elevated yet slowing CPI.

Our initial forecast is for a 1.4% increase, although electricity subsidies in WA and Victoria, and a lesser extent Queensland, could mean a lower number.

1.4% would be no cause for celebration but after a 2.1% and a 1.8% in recent quarters it is in the right direction.

Governor Lowe will likely take his next round of speeches reiterating their preparedness to tackle inflation with above neutral rates if needed.

“The Board remains resolute in its determination to return inflation to target and will do what is necessary to achieve that” was the final line of yesterday’s decision.

For now though, reopening of supply chains, anchored inflation expectations and falling commodity prices are working in their favour.

The key domestically will be how tight labour markets feed into wage outcomes over the next year.

The RBA is prepared for 3.5% to 4% increases to wages, as many agreements are now showing, but will be alert for any trend higher.

Immigration is making a welcome comeback and may well impact enough in the next 12 months for the RBA to get their way.

However, the jobs market is unlikely to be back at pre COVID conditions until 2024 so the RBA patience, although welcome, may be tested again.

About Tim Hext and Pendal’s Income & Fixed Interest boutique

Tim Hext is a Pendal portfolio manager and head of government bond strategies in our Income and Fixed Interest team.

Tim has extensive experience in banking, financial markets and funding including senior positions with NSW Treasury Corporation (TCorp), Westpac Treasury, Commonwealth Bank of Australia, Deutsche Bank, Bain & Co and Swiss Bank Corporation.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia.

Find out more about Pendal’s fixed interest strategies here

About Pendal

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

In 2023, Pendal became part of Perpetual Limited (ASX:PPT), bringing together two of Australia’s most respected active asset management brands to create a global leader in multi-boutique asset management with autonomous, world-class investment capabilities and a growing leadership position in ESG.

Significant Features: The Pendal Global Emerging Markets Opportunities Fund is an actively managed portfolio of global emerging market shares. The portfolio is managed by J O Hambro Capital Management Limited.

Fund Objective: The Fund aims to provide a return (before fees, costs and taxes) that exceeds the MSCI Emerging Markets (Standard) Index (Net Dividends) in AUD over the long term.

Here are the main factors driving the ASX this week according to Pendal’s Head of Equities, Crispin Murray. Reported by portfolio specialist Chris Adams

Higher bond yields, a stronger US dollar and the expectation of a US recession before the end of 2023 continued to weigh on markets last week.

A bout of panic in the UK bond market added some spice. A government ‘mini’ budget triggered the rout and demonstrated the currently fragile state of the financial system. The Bank of England was forced to buy long-dated bonds to maintain solvency in the pension fund system.

Finally, geopolitical risk remains elevated. Sabotage of the Nordstream pipelines and Putin’s speech signalled the potential for the conflict with Russia to escalate.

The S&P 500 shed -2.9% for the week. The S&P/ASX 300 continues to outperform. It was down -1.6% for the week, helped by a weaker AUD, which broke down versus other currencies.

Find out about

Pendal Focus

Australian Share Fund

Crispin Murray,

Head of Equities

US economy and policy.

The Core Personal Consumption Expenditure (PCE) index – which is the Fed’s preferred measure of inflation – came in a little higher than expected for August.

A headline of 0.6% growth versus 0.4% expected caused some alarm, although the actual number of 0.56% versus 0.44% made for better reading. July was also revised down from 0.1% to 0.0%.

Rent increases, which comprise 17% of the index, drove the increase. There is some debate about whether the lagged effect is giving the Fed a false signal as lead indicators of PCE rents – such as the Zillow Home Price index – may have rolled over. However these lead indicators also suggest that inflation in rents is much stronger than is being reflected in the PCE measure. So it probably is not right to discount this component.

Core Services PCE remains resilient, up 0.6% month on month and 4.7% year on year.

All told, this data likely cements in the 75bp November rate increase.

Consumer spending on autos and services continues to hold up and is expected to support 1% growth in real consumption in Q3 2022, helped by a fall in the savings rate. This demonstrates the current resilience in the US economy, given the headwinds from energy and other prices rises.

With real incomes on the rise again, savings rates are likely to rebound higher in Q4. Current estimates have US households running down US$63bn of their excess saving so far, around 30% of the total. This leaves US$1.5tr remaining – around 5.5% of GDP. This helps explains the Fed’s challenge in slowing the economy.

Finally, it is worth noting the downgrade from Nike, which pointed to substantial excess inventories in North America. This will lead to discounting; another sign of easing prices for goods.

Australia

The ASX fell 1.6% and is now -10% in 2022.

The more rate-sensitive sectors led the market lower last week, reflecting concerns over financial stability and rising credit spreads. Financials were down -3.1% and Real Estate -2.9%.

Resources (-1.0%) held up better, helped by a weaker currency and also gold beginning to rally.

Traditional defensives did best, with Health care (1.6%) and Communication Services (0.7%) up on the week.

UK bond market chaos

The fiscal largesse of the UK mini-budget shook confidence and triggered a selling loop in UK bonds, sending the market into tailspin.

The issue is many UK pension funds hold their long-dated exposure via synthetic 30-yr government bonds. This theoretically matches their long-dated liabilities. The problem is that there is a liquidity mismatch. When the bonds start falling, the funds are forced sellers of bonds to raise the liquidity to meet the margin call. This was reinforced by broader positioning in the market.

At one point the UK 30 year bond had fallen almost 50% in value since August, with the yield rising from 2.5% to north of 5.0%.

The Bank of England (BOE) intervened, promising to buy bonds to ensure the market was functioning. Their quantitative easing (QE) did the job, with UK 30-yr yields rallying back to 3.8% by the end of week.

It also saw the British pound bounce back from 1.05 to 1.11 versus the US dollar. This coincided with a broader fall in the latter.

The BOE has said they will continue to buy bonds through to mid-October, which buys time for the pension funds to raise liquidity.

This highlights the current risk of forced liquidations from some market players – another headwind for equities.

The challenge is that the interest rate the BOE should target, given fiscal policy, is likely to be too high for many households to service their mortgages. This could trigger a housing bust.

So the expectation is that they will tolerate higher inflation to hold rates lower and probably sacrifice the GBP.

The BOE’s intervention and Whitehall’s decision to reverse tax cuts may help calm the bond market.

Extreme risk aversion saw money parked in US dollars. With this crisis seemingly averted, this may reverse and we may have seen a near-term top in the US dollar and bond yields.

These signs of financial strain may have a perverse silver lining for markets, in that it may prompt a less severe tone from the Fed.

We may have seen this on Friday where Fed Vice Chair Brainard noted the need to consider time lags with monetary policy. She also noted how the spill-over impact of rate hikes can amplify the tightening of conditions, which appears to be a nod to the risk of some form of financial contagion.

We see three scenarios which could lead to a Fed Pivot:

- Inflation looks to be under control,

- The economy falls into a major downturn, or

- A major financial shock.

At this point the latter two appear more likely but would result in further equity market falls before bouncing back once the Fed pivots.

Sustainable and

Responsible Investments

Fund Manager of the Year

Australia

We continue to see the Australian market as more defensive. It trades on a P/E of 12x, versus the S&P 500 at 17x, while the economy is supported by higher savings, a less aggressive central bank, supportive terms of trade and immigration.

The issue for Australia is as much as the RBA may want to limit rate rise, there may be a limit to the gap between our short-term rates and those in the US, before it creates issues with the currency which would exacerbate inflationary pressures.

About Crispin Murray and Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 30 years of investment experience (including 28 years at Pendal) and leads one of the country’s biggest equities teams.

Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Effective 3 October 2022 we are changing the Fund’s custodian from the Hong Kong and Shanghai Banking Corporation Limited, Sydney Branch (HSBC) to the Northern Trust Company.

Also effective 3 October 2022 we are changing the Fund’s administrator from Westpac Financial Services Group Limited to The Northern Trust Company.