Cash rates are now close to neutral, but several factors mean recession is still a possibility. ANNA HONG explains

THIS month’s rates decision turned out as expected with 90% of economists predicting the Reserve Bank’s 50-point hike.

The RBA has said the neutral rate is likely to be 2.5% “plus a bit”, so at a cash rate of 2.35% we are getting close.

The question now is whether this cycle of aggressive rate hikes will lead to the desired soft landing or a recession.

The pace of the rate hikes makes recession a clear and present danger when we consider these extra three uncertainties:

1. Impact of fuel excise ending

The December quarter will start with holiday blues.

The fuel excise holiday ends on October 1, meaning we’ll be paying an extra 22c per litre for the drive home after the school holiday break.

This will nudge unleaded petrol towards $2, further increasing cost-of-living pressures.

2. Impact of rate hikes are slow to flow through to mortgages repayments

There is an average three-month lag between an RBA rate hike and the full impact on loan repayments for a variable-rate borrower, says Australia’s biggest mortgage lender, Commonwealth Bank (see graph below).

So borrowers have only experienced the first round of rate hikes from May.

The second 0.5% from June is flowing through about now.

That leaves 1.5% in rate rises from July, August, September to come.

The full impact of locked-in rate increases will come through in December — just as we start our Christmas shopping.

Much has been written about the fixed-rate cliff in 2023, but it appears variable-rate borrowers are also sliding down a steep hill with the pace of rate rises.

Fixed and variable-rate borrowers are in the same boat come 2023.

Without understanding the full force of hikes already passed on, the Reserve Bank is at risk of over-tightening.

Find out about

Pendal’s Income and Fixed Interest funds

3. Supply shocks are hard to forecast

Central banks around the world failed to forecast the inflation impact due to Covid supply shocks.

This task will get harder for central banks as we head into 2023. The desire for countries to lift growth by boosting production will clash with economic nationalism.

This struggle highlights the fragility of the lean manufacturing strategies brought on by globalisation in the last few decades.

If supply shocks ease, the RBA may have already over-tightened. But if the rebuild of supply chains fail, expect more rate pain ahead.

Mixed with the pace of rate hikes, these three factors raise the prospect of a recession.

The Reserve Bank is keenly aware of that. Governor Phil Lowe describes the desired soft landing as a narrow path “clouded in uncertainty, not least because of global developments”.

What does this mean for fixed interest investors?

With 3-year Australian government bonds at 3.3%, the potential for upside gains is higher than the downside risks.

That gives balanced portfolios the opportunity to rotate into defensiveness at good levels.

About Anna Hong and Pendal’s Income and Fixed Interest team

Anna Hong is an assistant portfolio manager with Pendal’s Income and Fixed Interest team.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia. In 2020 the team won the Australian Fixed Interest category in the Zenith awards.

With the goal of building the most defensive line of funds in Australia, the team oversees A$22 billion invested across income, composite, pure alpha, global and Australian government strategies.

Find out more about Pendal’s fixed interest strategies here

About Pendal Group

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Here are the main factors driving the ASX this week according to our head of equities Crispin Murray. Reported by portfolio specialist Chris Adams.

ASSET markets remain weak due to the US Fed’s hawkish tone, renewed concerns about Europe and China’s Covid lockdown in the south-western city of Chengdu.

Ten-year US government bond yields last week rose 15bps to 3.19%. Commodities were also weaker: iron ore was -9.8%, copper -8% and Brent crude -8.5%.

The S&P/ASX 300 fell 3.1% and the S&P 500 lost 3.2%. The latter has unwound quickly and is now 9% off its August 16 high. It now sits on a key support level, just above 3900.

US employment data was somewhat positive for markets. There is emerging evidence that labour force participation is recovering and wage growth slowing. This may be enough to swing the Fed to a 50bp move on September 21. All eyes will be on the Sep 13 CPI data.

Our domestic reporting season was broadly in line with historical averages in terms of revisions.

FY22 delivered 23% EPS growth, driven by 38% EPS growth in resources. Bank EPS rose 15% as bad debt charges fell and Industrial EPS was up 7%.

Consensus now expects market EPS to grow 3% in FY23. This is essentially unchanged over the past month.

Resources EPS is expected to fall 3%. Industrials are expected to grow 9%. This is down from 11% a month ago, but still looks optimistic, in our view.

There are two very different paths forward from here:

- Positive case: The combined effect of diminishing supply chain pressures, slowing labour demand and rising participation allows the Fed to avoid raising rates too far. Falling inflation requires only a moderate economic slowdown. Risk premiums fall, along with the outlook for rates, enabling markets to recover.

- Negative case: Inflation remains embedded too high. Combined with the European power crisis and ongoing lockdowns in China, this forces central banks to raise rates into a global economic slowdown. Such an environment may induce some form of additional financial shock, further exacerbating the downturn and market pessimism.

Economics and policy

US employment data was firm, but dovish on balance for the rate outlook. This was reflected in US 2-year yields dropping 13bps on Friday.

August payrolls rose 315k, but prior months were revised down 107k.

The 3-month moving average has slowed from 437k to 378k as a result. This is positive, but ultimately it needs to get down to sub-100k to meet the Fed’s objectives.

There were three dovish aspects of the data:

- Average hourly earnings growth was stable at 5.2%. This was +0.3% month-on-month (0.1% lower than expected). On a sector-adjusted basis it was also lower than expected.

- Labour force participation rose more than expected, up 0.26% to 62.4%. The unemployment rate increased to 3.7% as a result. Greater labour supply is key to slowing wage growth.

- Weekly hours were down. This meant aggregate hours for the month were slightly lower, demonstrating the labour market is marginally easing off.

All this raises the odds of a 50bp hike in September rather than 75bp. CPI data will be key in this call.

We remain of the view that Fed chair Jay Powell’s tough talk is aimed at holding inflation expectations down, allowing the Fed to avoid raising rates as far as feared.

Job openings data was more negative — there was no sign that the worker shortage was improving in the latest Job Openings and Labor Turnover survey.

However job ads on Indeed.com are falling and the “quits” rate has begun to decline. This suggests employees are a little less confident on the labour market outlook.

On balance, employment data is better. But it’s a long way from the degree of cooling required to solve the inflation problem. Consider these factors:

- The employment gap — measured relative to what is considered sustainable employment —remains near historic peaks. This is consistent with wage growth staying too high.

- This is reinforced by a sector breakdown which shows the service sector is still catching up to pre-Covid levels. We will need to see goods and trade sectors employment free up more to offset this.

- The ratio of job openings to the number of unemployed remains at a record high. This needs to move materially lower to return to levels consistent with a looser labour market.

- Underlying income growth in the economy remains high once you combine employment growth with wages and hours. Nominal income is rising about 7% on three and six-month basis, supporting consumer ability to spend and absorb inflation. This needs to head towards 3-4% to be consistent with the inflation target.

- Wage growth remains too high. Just staying where we are is not enough for policy makers. We need to see significant loosening in the labour market.

We also saw the US ISM Manufacturing Survey index at 52.8 — stronger than an expected 51.9. It implies a 1.4% rate of GDP growth.

This suggests the economy is not slowing as precipitously as some believe.

Europe

Moscow suspended natural gas flows into Germany for three days on the premise of maintenance work. Russia then announced an indefinite suspension due to a technical fault, following the G7’s announcement of a price cap on Russian oil.

Pendal Focus Australian Share Fund

Now rated at the highest level by Lonsec, Morningstar and Zenith

This will further curtail manufacturing. ArcelorMittal, for example, announced it would close two plants.

European policy-makers are in a far more difficult position than the US.

Gas and power issues combined with a weaker currency are exacerbating inflation. German two-year bond yields have moved from 0.5% to 1.1% since the middle of August.

Markets

We continue to note the total financial conditions index feedback loop — where too big a rise in equities starts to work counter to the Fed’s goals and leads to a hawkish shift in their messaging.

This emphasises that the Fed will need to see inflation and the economy much softer before it is comfortable with a sustained rise in equities.

The S&P500 is sitting at a key support level at 3900. A fall through it would likely set up a test of the June lows around 3600.

Germany is already testing these previous lows and may provide a lead on other markets.

The more benign view is that we are forming a trading range of 3600-4300 for the S&P 500. The more bearish path would come with earnings declining and the market forming new lows.

In this context and given greater resilience in Australia, we are retaining a more defensive tilt, skewing to larger stocks and those delivering capital return to shareholders.

We are also mindful that the market retains scope for speculative episodes as seen in the IPO of China’s Addentax Group in the US. The Shenzhen-based garment manufacturer rose more than 20-fold on its first day of trading, only to collapse below issue price the following day. This is another reason to remain wary.

Issues in the bond market have relevance for sector performance in equities. On the positive side US bonds look oversold. The one-month move is now in the 91st decile, indicating we have seen the worst of the decline.

But looking forward there are two negatives to note.

The first is that September marks the step up in quantitative tightening for the Fed to $US90 billion per month, which means more available supply of bonds.

Second is the decline in US banking deposits. These rose substantially through the pandemic. But the cost of holding cash is greater today and corporates are using cash to pay down debt.

Should banks funding become tighter there will be fewer surplus deposits to invest into bonds, also acting as an overhang on yields.

Australia

The S&P/ASX 300 got caught up in last week’s global sell-off.

Resources (-7.2%) led the market lower on the back of the new lockdowns in China.

Energy (-4.6%) also declined as the oil price continues to fall despite lower inventory levels. Technology (-3.9%) fell as bond yields continued to rise and the market rotated to defensive sectors such as staples (+1.5%) and healthcare (-0.7%).

Adviser Sam is invested

in making our world

A better place.

Watch as Sam meets a

mum rebuilding her life

thanks to responsible

investing

About Crispin Murray and Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia. Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Lessons from ASX earnings season; What China’s rate-cutting means for investors; How to invest in sustainable fashion

Despite tough talk from central bankers, cash rates are likely to sit around 3% next year, writes our head of government bond strategies TIM HEXT

CENTRAL banks have largely abandoned forward-looking monetary policy since Covid.

One wonders why they need big teams of economists if they’re merely responding to the latest prints of often-lagging indicators such as inflation.

This was highlighted again last week at the Jackson Hole central bankers conference in Wyoming.

One cannot blame them for hawkish comments on inflation, including talk of bringing on the pain. After all, their lack of forward-looking policy failed to pick up inflation soon enough in 2021.

In the US there is a risk they will get it wrong again — but in the opposite direction, failing to pick up an imminent fall in inflation led by goods inflation, which forward indicators are showing.

Or maybe they are aware of it are and want to take the credit for falling inflation when it’s already baked in as supply chains and business margins normalise.

Market reaction

Markets this week reacted to the rhetoric by selling off bonds and equities.

July’s rally on hopes of a soft landing is a distant memory. But there are signs the rally, although premature, had the right idea.

Find out about

Pendal’s Income and Fixed Interest funds

This comes down to the idea that inflation will fall and then stabilise around 4% in the next year.

That’s still too high, meaning rate cuts would be unlikely. But hikes would then stop around neutral and central banks would feel they had time on their side.

Australia is a bit behind the US. Due to the composition of our CPI the moves both up and down will be less dramatic.

We also face a mortgage fixed-rate cliff next year which US 30-year mortgages don’t have.

If the RBA exhibits any patience it is likely to sit at 3% cash rates in 2023.

Falling global inflation should allow our central bankers more confidence that we are not in some 1970s style spiral.

Wages are key

Wages will be key in the medium term.

Our view is that goods inflation will fall before stabilising at about 2%.

Adviser Sam is invested

in making our world

A better place.

Watch as Sam meets a

mum rebuilding her life

thanks to responsible

investing

Services inflation will remain elevated around 5%, leading to a 4% CPI.

This assumes wage growth of close to 4% next year. Prime Minister Albanese’s jobs summit this week will bring that all into focus.

We will do a deep dive into wages in our upcoming Australian Investor Quarterly. (Contact us if you’re not on the distribution list).

A little more than 20% of workers are now covered by awards — the main one being the minimum wage set by the Fair Work Commission.

Another 40% of us have individual agreements.

The jobs summit will focus on the remaining 40% covered by collective agreements or enterprise bargaining.

This is where the major battleground over wages will be fought, especially if agreements try to keep pace with the recent 4.6-5.2% minimum wage increase.

Bonds outlook

For now, bonds have once again entered the buy zone.

I will avoid predictions on equities.

But I make the observation the landing in the US may not be as hard as many are predicting.

About Tim Hext and Pendal’s Income & Fixed Interest boutique

Tim Hext is a Pendal portfolio manager and head of government bond strategies in our Income and Fixed Interest team.

Tim has extensive experience in banking, financial markets and funding including senior positions with NSW Treasury Corporation (TCorp), Westpac Treasury, Commonwealth Bank of Australia, Deutsche Bank, Bain & Co and Swiss Bank Corporation.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia.

Find out more about Pendal’s fixed interest strategies here

About Pendal

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

In 2023, Pendal became part of Perpetual Limited (ASX:PPT), bringing together two of Australia’s most respected active asset management brands to create a global leader in multi-boutique asset management with autonomous, world-class investment capabilities and a growing leadership position in ESG.

Here are the main factors driving the ASX this week according to our head of equities Crispin Murray. Reported by portfolio specialist Chris Adams.

THE late northern summer repose and the domestic focus on earnings season was dramatically disrupted by Jerome Powell’s short-but-direct speech at the Jackson Hole central bank conference last week.

Powell reminded the market of his singular focus on bringing down inflation, even if it brought “some pain to households and businesses”.

The S&P 500 slumped in response, ending down 4% for the week.

We’ve previously flagged that the market rally was running up against technical resistance and losing steam as the position covering played out.

The S&P is now down 5.5% and the NASDAQ off 7.5% from their Aug 16 highs.

Powell’s message was not so much the need for rates to go higher than markets expect. Rather, rates would need to be sustained at restrictive levels for some time to bring inflation under control.

This is at odds with recent optimism that rates would fall in 2023. This saw US two-year yields rise 17bps and 10-year yields up 7bps to 3.04%.

The Fed’s stance emphasises the importance of the total financial conditions index as a signal. It will not allow this to rise too far.

This means bond yields are underpinned and equities are capped while inflation remains an issue.

Three other developments also weighed on sentiment:

- Oil back above US$100

A week ago the Iran deal looked likely and the market expected oil to drop sub-US$90 on the incremental supply. But on Tuesday we got the “Saudi put” under the oil price. Riyadh’s minister of energy effectively indicated that OPEC+ supply agreements would continue in 2023 and flagged the prospect of supply cuts in response to higher volumes from Iran. He also highlighted a view that there was a disconnection between the physical and paper oil markets. This can be interpreted as a belief that the US is manipulating the oil price down and OPEC will act in response. - European power prices surge higher

We are now at levels where huge swathes of German industry is unviable. This is driven by the inexorable rise of gas prices. Storage levels in Germany are approaching 80% — but this level is required in winter even when flows from Russia are normal. Moscow is now allowing only 20-40% of normal flows. If this continues, no amount of storage will suffice. - US dollar index (DXY) breaks back to 20-year highs

This creates liquidity pressures in many other countries. A return to the trifecta of higher bond yields, oil and US dollar is typically bad for equities. That said, the outlook for oil is still challenged by the potential for weaker demand as the global economy slows.

The petrol price remains a key signal for US inflation expectations — and therefore yields and hawkishness from the Fed.

So there is potential for inflation to resolve itself faster — requiring less policy pain if it comes down.

But for the moment the market is back in a nervous holding pattern with 4000 on the S&P 500 viewed as a key support level.

Australia

Australia enjoyed a short respite from global macro factors. On balance, the busiest week of reporting season delivered a neutral outcome.

Consensus expects FY23 earnings to rise 4%, up from +18% in FY22.

Revisions to earnings expectations are flat for FY22 and -2% for FY23 compared to four weeks ago.

In FY23 resources earnings expectations are now 4% lower and 1% higher for banks, with the rest of the market revised down 2%.

In terms of results, consumer staples disappointed as supermarkets proved less defensive than hoped. Companies delivering capital management — such as Qantas (QAN) and Nine (NEC) — performed better.

Economics and policy

Fed Chair Powell kept his Jackson Hole speech short and narrowly focused for deliberate effect, sending a strong message on inflation.

The odds of a 75bp move higher in September have jumped to about 60 per cent.

The curve of implied hikes is moving back towards its June highs and is a long way above the end of July lows.

The market is divided into two broad camps:

- The Fed will drive the economy into recession as it looks too literally at current data and over-tightens. This triggers a recession and earnings downdraft that takes the market back to the lows.

- The Fed is bluffing. It wants to send a hawkish message to restore credibility, but knows the economy is already slowing rapidly and inflation data will improve. This gives it scope not to push rates too hard. This scenario leads to bond yields falling and is more positive for equities.

The next Federal Open Market Committee meeting concludes on September 21 — so with more employment and inflation data to come the outcome is yet to be determined.

Pendal Focus Australian Share Fund

Now rated at the highest level by Lonsec, Morningstar and Zenith

In terms of inflation, the Core PCE price index rose 0.1% month-on-month — less than expected — and continues a run of incrementally more-positive data.

This may be an unwind following the June spike in core PCE.

Averaging across the two brings it back in line with the run-rate from January to May.

The Core Services PCE price index came in at 4.2% year-on-year. This was also lower than expected and is the lowest print since December 2021.

The Cleveland Fed’s ‘nowcast’ measure of inflation also continues to track lower, as do the Evercore surveys of wage pressure and retail pricing power.

Australian equities

The S&P/ASX 300 finished down 0.6% last week, not capturing Friday night’s slump in US equities.

It held up on the back of reasonable results and better performance from the resource and energy sectors.

Consumer staples underperformed on the back of disappointing results from Coles (COL) and Woolworths (WOW).

Small caps also underperformed, which is a sign that the rally driven by defensive positioning has run out of steam.

Key observations on ASX results so far:

- Pricing power is a key point of differentiation. Disappointing results mostly reflect insufficient moves to offset cost pressure, particularly in the building-related sector and companies with European exposure (eg Dominos Pizza, DMP). Meanwhile companies such as Wisetech (WTC) and Qantas (QAN) showed the value of pricing power.

- Costs are a headwind to some of the defensive stocks, leading to less defensiveness than expected. We saw this in Endeavour (EDC), Coles (COL), Woolworths (WOW) and Ramsay Health Care (RHC).

- Some cyclicals are not experiencing the weakness many feared, eg Nine Entertainment (NEC) and some advertising-related names.

- Companies with cyclical tail winds are performing well. For example the lithium sector remains strong, as does oil refining.

- The market is liking capital return. New buy-backs from NEC and QAN were well received

Adviser Sam is invested

in making our world

A better place.

Watch as Sam meets a

mum rebuilding her life

thanks to responsible

investing

About Crispin Murray and Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia. Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Pendal’s head of equities Crispin Murray explains why he is fully supportive of Perpetual’s acquisition of Pendal

Find out about Crispin’s Pendal Focus Australian Share Fund

Find out about Crispin’s sustainable Pendal Horizon Fund

BY NOW you’ll be aware that Pendal has formally joined with Perpetual.

I remain fully supportive of Perpetual’s acquisition of Pendal — completed on January 23, 2023.

It’s the right deal for clients, the business and the team.

It maintains the independence of the Australian equities boutique and strengthens our industry position in the long run — since all senior people of the team are committed to being here for the long term.

The industry is fundamentally changing.

Consolidation is occurring at all levels — super funds, platforms and fund managers. This is an inevitable trend to which we must respond in the most effective way.

When Pendal Group originally floated on the ASX, the goal was to build a diverse multi-boutique business which combined scale for the provision of best services and systems with independence, autonomy and focus for investment teams.

This model has stood the test of time — and has been replicated by others.

It continues to be the right way to run a fund management business.

But we now need greater scale and diversity to build a stronger organisation through which to deliver the best possible services.

This deal enshrines and codifies the independence and autonomy of Pendal’s Australian equities boutique in a way that covers strategy, remuneration, personnel decisions, proxy voting, dealing and service provision.

The Pendal Australian equities team remains unchanged and separately located.

The team is fully supportive of the deal.

We are a separate, independent boutique focused on the job of investing for our clients.

We are protected by strong governance rules and will benefit from being part of a more diverse, larger and stronger group.

Our large and experienced team, our strong performance culture — and a business structure that enables us to focus on investing — provides the critical factors we believe will enable the continuation of the consistent performance we have delivered to our clients for the past 20 years.

Crispin Murray

Head of Equities, Pendal Australia

About Crispin Murray and Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 29 years of investment experience and leads one of the largest equities teams in Australia. Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 17-year history (after fees), across a range of market conditions.

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

In 2023, Pendal became part of Perpetual Limited (ASX:PPT), bringing together two of Australia’s oldest and most respected active asset management brands to create a global leader in multi-boutique asset management with autonomous, world-class investment capabilities and a growing leadership position in ESG.

Perpetual is a diversified, ASX-listed financial services company providing asset management, private wealth and trustee services to local and international clients in Australia, Asia, Europe, United Kingdom and US.

Lessons from ASX earnings season; Importance of ESG in asset allocation; How inclusion impacts product design; A reminder from central banks

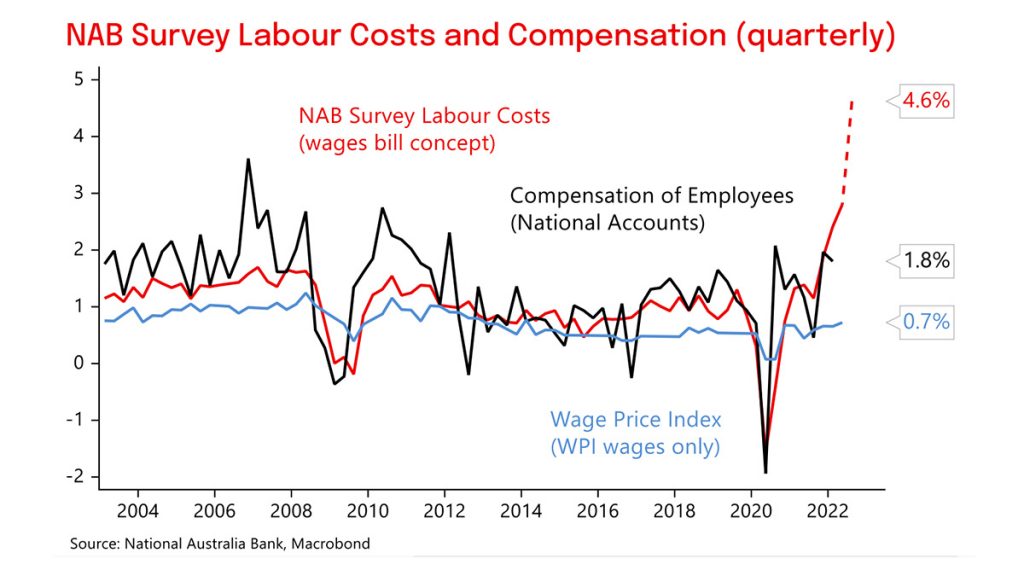

There’s little to suggest Australia’s tight labour market is easing, which means more pressure on the RBA to continue hiking rates, writes ANNA HONG

IT’S reasonable to expect wages to rise as unemployment in Australia trends down to 3.4%.

So when the most recent Wage Price Index printed below the 0.9% market consensus at 0.7%, newspaper headlines unsurprisingly bemoaned wage outcomes for Australians.

But the headlines don’t show the true picture.

Look closer and you’ll see signs that wages are lifting more than we realise.

Businesses have learned from past mistakes that issues caused by entrenched wage bills are hard to correct.

Employers are now using bonus payments as a stop-gap solution to maintain labour levels required to sustain production. The public sector is also joining the bonus party: NSW Health is handing out a $3000 bonus to workers.

The hope is migration will kick in, keeping these increases as a temporary measure — at least while businesses have the power to pass on price rises to consumers.

Will overseas workers arrive in time to help businesses?

July migration shows little sign of temporary or skilled workers returning — a trend that may continue for a while yet.

Why? Visa bottlenecks.

Before 2022 there was already a visa processing problem — the Department of Home Affairs was struggling to keep pace with a large volume of applications.

Fast-forward to the last federal government’s $875 million budget cut for the Department of Home Affairs and now we have an even bigger problem.

Find out about

Pendal’s Income and Fixed Interest funds

That cut was equivalent to a third of the department’s migration expenses.

So regardless of the new Labor government’s desire for a Jobs Summit solution, there is little to suggest the current labour supply pain will be alleviated.

While companies continue to pay up in wages (albeit in variable rather than fixed payments), the Australian consumer will be able to sustain healthy levels of spending.

CBA’s household spending data last week showed a 1.1% month-on-month rise for July. That means the RBA will have to continue hiking on its path to a 2% to 3% inflation outcome.

About Anna Hong and Pendal’s Income and Fixed Interest team

Anna Hong is an assistant portfolio manager with Pendal’s Income and Fixed Interest team.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia. In 2020 the team won the Australian Fixed Interest category in the Zenith awards.

With the goal of building the most defensive line of funds in Australia, the team oversees A$22 billion invested across income, composite, pure alpha, global and Australian government strategies.

Find out more about Pendal’s fixed interest strategies here

About Pendal Group

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Earnings are ahead of expectations halfway through ASX reporting season. But there are signs companies are bunkering down amid uncertainty on rates and wages, says Pendal’s JIM TAYLOR

- Earnings and free cash flow impress in ASX earnings season

- Buy-backs and dividends disappoint

- Find out about Pendal Focus Australian Share Fund

AUSTRALIAN corporate earnings are ahead of expectations halfway through the reporting season.

But there are early signs that companies are starting to bunker down amid uncertainty about interest rates and wages growth, says Pendal portfolio manager Jim Taylor.

About a third of companies exceeded market consensus for their June 30 numbers — while 18 per cent missed the consensus number, he says.

Bottom-line earnings and free cash flow have been pleasing. But dividends and buy-backs have disappointed — indicating managers are taking a conservative view on the economic outlook.

Earnings forecast downgrades are also accelerating as interest rates rise and commodity prices ease.

“The bottom line is the results for these six months have come in there or thereabouts,” says Taylor.

“But the outlook commentary from the companies indicates some very significant uncertainty about the economic environment and what interest rates are doing,”

“Boards are taking quite a conservative view on what the next year sort of looks like and have taken the opportunity to temper some expectations in the out years and preserve some balance sheet capacity and cash.”

Find out about

Pendal Focus

Australian Share Fund

Crispin Murray,

Head of Equities

ASX shares have lifted about 10 per cent from their June lows through earnings season as some of the more dire concerns that sent markets lower in the first six months of 2022 failed to materialise.

“The reporting season is always a concertinaed period of intense information overload, but the market is getting quicker and quicker at sifting through the information,” says Taylor.

Three key themes

Three themes are weighing on the outlook, says Taylor:

- Consumer confidence

- Interest rates

- Wages

“One of the key questions we’re trying to get answers for is how the consumer demand environment will fare heading into Christmas,” he says.

“That’s going to be vital. There are a few questions marks over the amount of inventory the retailers are taking into that environment.

“If you get a rapid slow-down in consumer demand, we’re going to see inventory problems, but there’s nothing that’s really come from this reporting season which would suggest that that’s highly likely.”

Impact of rates

The trajectory for interest rates is also a key factor for markets, particularly how much benefit from higher rates accrues to the financial sector.

“We’ve had a few companies that have tried to temper expectations, stressing that the benefit of rate rises is nuanced. There are competitive forces. There’s the way their hedges are structured. And there’s a desire to spend some of the windfall from higher rates on maintaining market share.

“That’s something the market is very focused on.”

Labour market and wages

The third issue investors should watch out for is the state of the labour market and wages. Recent data shows wage growth at a 10 year high in Australia, but Taylor says availability of workers is a more pressing issue for local companies.

“It’s not so much the cost of labour but the access to labour and the rate at which sick leave is occurring.

“We’ve seen a couple of the building material companies come out and flag weather and access to labour as a key issue that they’re very focused on towards the back end of this year.”

What does it mean for investors?

Australian stocks still look well placed despite some rising concerns from boards and earnings downgrades, Taylor says.

With high exposure to resource companies and financials, the ASX is less sensitive to higher interest rates than other developed markets.

“The absolute level of commodity prices is still very healthy.

“There’s still going to be excellent margins generated and excellent levels of free cash flow and resulting dividends.

“And Australia just doesn’t have this significant weighting to high growth and tech that some of the other markets do.

“As a result of that, we’ve got a much lower level of sensitivity to what interest rates are doing.”

About Jim Taylor and Pendal Focus Australian Share Fund

Drawing on more than 25 years of experience investing in top-performing Australian companies and a background in accounting, Jim manages our Long/Short Fund and co-manages our Imputation Fund. He is a Chartered Accountant with membership of the Australian Institute of Chartered Accountants.

Pendal Focus Australian Share Fund is managed by Crispin Murray. The fund has beaten its benchmark in 14 years of its 18-year history (after fees), across a range of market conditions. Find out more about Pendal Focus Australian Share Fund here.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Central banks are reminding us they’re still hawkish — but they won’t risk sending people broke with a 4% rate, argues Pendal’s head of government bond strategies TIM HEXT

FOR some reason markets spent July ignoring central bank hawkishness.

Recession talk was all the rage, which meant rate hikes were largely discounted.

This was despite central banks keeping their messages hawkish, and seeing little relief on inflation.

Financial conditions — measured by bond rates, credit spreads and equities — eased back to May levels.

Clearly central banks were not impressed. This week they came out swinging, singing from the hymn book of restrictive rates needed to rein in inflation.

Find out about

Pendal’s Income and Fixed Interest funds

St Louis Fed president Bullard talked of rates needing to go into “higher and restrictive territory”.

Minneapolis Fed’s Neel Kashkari wasn’t sure if inflation could be tamed without a recession.

Reserve Bank of New Zealand governor Adrian Orr wants to see his country’s official cash rate “unambiguously” above neutral.

All of this was lit up by UK inflation pushing through 10% and heading higher.

The playbook from earlier this year is back.

Bonds sell off, credit and equities get hit and cash rates go up.

What does it mean for investors?

In Australia we’re likely to get another 50bp hike in September.

Rates should finish the year around 3%.

Given our high levels of household debt (and in particular the stress on 2020 and 2021 homebuyers) consumers will be hit hard at 3% — let alone higher rates in significantly stricter territory.

While the RBA will remains hawkish I doubt they will risk sending households broke by raising rates to 4% — even if markets are now playing with the idea.

Bonds are now getting more fairly priced in balancing the risks to inflation and growth.

I still prefer inflation bonds for now — but 10-year bonds north of 3.5% are interesting again.

Adviser Sam is invested

in making our world

A better place.

Watch as Sam meets a

mum rebuilding her life

thanks to responsible

investing

About Tim Hext and Pendal’s Income & Fixed Interest boutique

Tim Hext is a Pendal portfolio manager and head of government bond strategies in our Income and Fixed Interest team.

Tim has extensive experience in banking, financial markets and funding including senior positions with NSW Treasury Corporation (TCorp), Westpac Treasury, Commonwealth Bank of Australia, Deutsche Bank, Bain & Co and Swiss Bank Corporation.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia.

Find out more about Pendal’s fixed interest strategies here

About Pendal

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

In 2023, Pendal became part of Perpetual Limited (ASX:PPT), bringing together two of Australia’s most respected active asset management brands to create a global leader in multi-boutique asset management with autonomous, world-class investment capabilities and a growing leadership position in ESG.