With effect from 31 May 2022, the “Pendal Horizon Fund” will be renamed the “Pendal Horizon Sustainable Australian Share Fund”.

The change of name is to further reflect the investment framework and responsible investment priorities of the Fund which extend beyond just ethical screens being applied and also the current name of the Fund does not inform it is an Australian equities and a sustainable fund.

There will be no changes to the investment strategy, objective or distribution frequency of the Fund.

An updated Product Disclosure Statement (PDS) providing information on the Fund will be issued on 31 May 2022 and made available on www.pendalgroup.com.

Impact of the ESG election | A signpost for global equities investors | Simple net zero approach for investors | Why LatAm is looking good

The shift towards progressive politics and climate action that swept Labor to power has important implications for investors. Pendal’s RAJINDER SINGH explains.

- Election 2022 sets tone and atmospherics for investors

- Australia swings to progressive politics and climate action

- Find out about Rajinder’s Pendal Sustainable Australian Share Fund

THE shift towards progressive politics and climate action that swept Labor to power has important implications for investors, says Pendal’s Rajinder Singh.

While uncertainty remains about the final makeup of the next parliament — including whether Labor will govern with a majority in the lower house and what the Senate will look like — it’s clear that the “tone and atmospherics” in Australia have changed, he says.

“It was an ESG election,” says Singh, who manages Pendal Sustainable Australian Share Fund.

“If you break it down, some of the key policy differences in this election were all about E, S and G.

“On the environmental side, it’s about climate change. For social issues, it was about gender and diversity in workplaces, childcare and Indigenous issues. And a federal integrity commission? Well, that’s governance.”

Singh says investors can view the election as a contest of ideas “and the Labor, Green and teals arguments in each of these areas seems to have won the day”.

Incremental change

Still, for all the hope among parts of the community, the new Labor government’s climate ambitions remain modest and it is unlikely that the new government will go further than its stated policy platform in the first term, Singh says.

“They are arguing for incremental change rather than massive change.

“They have a more ambitious target in terms of reducing overall emissions by 2030, and they have a target of 80% of electricity to be renewable by 2030.

Find out about Pendal Sustainable Australian Share Fund

“One thing that’s interesting is the planned investment in transmission capacity. The new government has a fairly large fund that they want to invest to rewire the nation.

“This would better allow renewables to connect to the grid and improve interconnectivity between states so we can actually move electricity around where it’s needed.”

A new climate change conversation

The main impact for investors will be a change in the way climate action is discussed in Australia, says Singh.

“It’s a change in the tone of the conversation about climate change. Even though the stated policy is not that much more ambitious, the underlying tone is going to be a lot more supportive of action.

“I think that may make a difference to companies’ strategic direction, particularly for companies that are looking to make new long-term, climate-related investments.”

While business and industry groups have moved ahead of government in climate action in recent years, a more supportive position from policymakers will reduce “some of the sovereign risk that overseas investors see in Australia.

“The view was Australia was seen as a laggard. This may reduce that risk there.”

Social and governance agenda

On the social front, big policy platforms like expanding access to childcare and investing in aged care will be beneficial to operators and real estate trusts in those areas.

“Healthcare generally should be a more of a beneficiary of a Labor government,” he says.

Sustainable and

Responsible Investments

Fund Manager of the Year

And importantly, a new focus on Indigenous affairs will play out across the stock market.

“The mining industry in recent years has been heavily exposed to these issues and spending time and effort to improve that where it has been mismanaged.

“But this is going to be something for all businesses to be aware and cognisant of — in the same way gender is an issue that companies need to think about, Indigenous affairs is an issue that we also all need to think about.”

Turning to governance, Singh points to the proposed establishment of a federal corruption commission as evidence of these issues becoming more central.

“What we have been seeing is that corporates are being held to a higher level of account from a governance perspective. To some extent, this is the government playing catch up and aligning with what investors have been expecting of the companies they invest in.”

What it means for investors

“This is now a government with policies that are more aligned with the ESG trends that we’re seeing in the market.

“There’s a trend that is already happening and the change in government and some of the new initiatives are supporting that trend.

“Tone and atmospherics are important in markets and companies and investors pick up on that.

“Companies that were on the borderline may now be more likely to be investing in these sort of areas, whether it be something outwardly aligned with ESG such as renewable energy or something like an internal policies on Indigenous affairs, equity and inclusion.

“If anything, it’s going to highlight the laggards across all ESG issues — previously, those that may have had some cover from a government that was not fully supportive. But that’s going to be much harder going forward.”

About Rajinder Singh and Pendal’s responsible investing strategies

Rajinder is a portfolio manager with Pendal’s Australian equities team. He has more than 18 years of experience in Australian equities.

Rajinder manages Pendal sustainable and ethical funds including Pendal Sustainable Australian Share Fund.

Pendal offers a range of responsible investing strategies including:

- Pendal Sustainable Australian Share Fund

- Crispin Murray’s Pendal Horizon Fund

- Pendal Sustainable Australian Fixed Interest Fund

- Pendal Sustainable Balanced Fund

- Regnan Credit Impact Trust

- Regnan Global Equity Impact Solutions Fund

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Responsible investing leader Regnan is part of Pendal Group.

After the evolution of Coalition fiscal spending habits during the pandemic, Australia’s new Labor government won’t be a big change, says Pendal’s Anna Hong

ON THE economic front, Australians will be largely unaffected by the change of federal government — at least in the near term, says Pendal’s Anna Hong.

That’s because key economic policies between Australia’s two major parties are mostly aligned, says Hong, an assistant portfolio manager from Pendal’s Income and Fixed Interest team.

However, there will be an increase in fiscal spending by the Albanese government.

Labor will increase fiscal spending by a net $7.4 billion in areas such as home equity schemes and electric car discounts, as you can see in this table:

Labor’s Fiscal Plan

| Net Budget Impact | -$7.4bn | |

| Revenue + Savings | $11.5bn | |

| Spending | $18.9bn | |

| Key Spends | Childcare subsidies | $5.4bn |

| Aged care | $2.5bn | |

| Medicare | $0.75bn | |

| Electric car discount | $0.47bn | |

| Home equity scheme | $0.31bn |

“This will prop up demand without fixing the supply issues, nudging inflation higher,” says Hong. “It will make the RBA work harder to counter the loose fiscal policy.”

The federal budget will remain in deficit for the rest of the decade — under either party.

“The stumbling block to Labor’s policies may be in generating planned revenue and savings.

“Many items on their list — such as multinational tax revenue — are easy to promise but notoriously difficult to achieve.

“Overall, the change of government is more of the same for the economy and the budget.

“The difference will be in the changes many Australian voters are focused on – climate policy, federal integrity, and gender equity — as Pendal’s Rajinder Singh outlines here.

“Australians want action and will watch this space closely.”

Find out about

Pendal’s Income and Fixed Interest funds

About Anna Hong and Pendal’s Income and Fixed Interest team

Anna Hong is an assistant portfolio manager with Pendal’s Income and Fixed Interest team.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia. In 2020 the team won the Australian Fixed Interest category in the Zenith awards.

With the goal of building the most defensive line of funds in Australia, the team oversees A$22 billion invested across income, composite, pure alpha, global and Australian government strategies.

Find out more about Pendal’s fixed interest strategies here

About Pendal Group

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Has inflation peaked and if so, what’s next for fixed interest investors? Here’s a view from our head of government bond strategies TIM HEXT

AMONG the many adages I’ve heard in my career “sell in May and go away” always sticks in my mind.

The quote apparently originated in London and said in full: “sell in May and go away and come back on St Leger Day” (in September). The “go away” referred to very long summer holidays enjoyed by rich stockbrokers.

In the US equity market November-to-April outperforms May-to-November over time.

Going back more than a century the Dow’s average return is apparently 5.2% for November-to-April, compared to 2.1% for May-to-October.

In Australia the numbers are 5.1% and 2.4%. The term could be recoined as “buy in November and sit back”, but that wouldn’t rhyme.

The calm in the storm

This May has been the calm in the storm. But no one can agree if it’s the eye of the storm or if we’re actually through it.

Markets are clutching at any sign inflation has peaked.

In the US it likely has on both on a monthly and year-on-year basis — but will be slow to come down.

In Australia we are unlikely to see a repeat of the Q1 2.1% quarterly CPI number. But base effects mean annual inflation will peak closer to 6% (currently 5.1%) in Q3 (released in late October).

Find out about

Pendal’s Income and Fixed Interest funds

We have just finished a deep dive into inflation which we will release shortly as part of our Australian Investor Quarterly newsletter.

As the inflation narrative settles down, all eyes will turn to the impact of inflation and interest rates on growth.

Share markets remain vulnerable to earnings downgrades and weakening growth numbers.

This becomes reflexive, though, as equity weakness in turn causes confidence to fall which may eventually take some pressure off rising interest rates thereby supporting equities.

We may well spend the northern summer rolling around in this cycle of volatility, heading eventually nowhere as the dynamics try to work themselves out.

What it means for investors

As a fixed interest portfolio manager it means we must look to harvest more tactical trades than big-picture moves for the next few months.

We continue to think short-dated inflation bonds are cheap in outright real yields but also in break-evens (inflation expectations).

The picture for duration and credit is less clear though we do have some positions based on cash rates “only” getting to 2% this year as opposed to markets pricing closer to 2.75%.

With both bond markets and equity markets trashed in the last four months I will ignore the “sell in May and go away” advice as coming way too late — wishing someone had instead advised me this year to “Sell on New Years Day and go away.”

About Tim Hext and Pendal’s Income & Fixed Interest boutique

Tim Hext is a Pendal portfolio manager and head of government bond strategies in our Income and Fixed Interest team.

Tim has extensive experience in banking, financial markets and funding including senior positions with NSW Treasury Corporation (TCorp), Westpac Treasury, Commonwealth Bank of Australia, Deutsche Bank, Bain & Co and Swiss Bank Corporation.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia.

Find out more about Pendal’s fixed interest strategies here

About Pendal

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

In 2023, Pendal became part of Perpetual Limited (ASX:PPT), bringing together two of Australia’s most respected active asset management brands to create a global leader in multi-boutique asset management with autonomous, world-class investment capabilities and a growing leadership position in ESG.

Here are the main factors driving the ASX this week according to our head of equities Crispin Murray. Reported by portfolio specialist Chris Adams.

Find out about Crispin’s Pendal Focus Australian Share Fund

Find out about Crispin’s sustainable Pendal Horizon Fund

THE MARKET is at an interesting near-term juncture.

The S&P 500 has lost ground seven weeks in a row and is now off about 20% from its peak. It has re-tested and held recent lows.

Expiring options may reduce volatility and we may see some month-end rebalancing towards equities in a low-liquidity environment due to next Monday’s US Memorial Day holiday.

A near-term bounce may be possible and counter-trend moves can be material.

However we don’t think we’ve seen the low point for this cycle. The market is yet to work through the effect of a slowing economy on corporate earnings.

The S&P 500 fell 3% last week as the market continued to worry about the potential for recession.

This was compounded by some poor earnings results out of US retailers. The issue here was not weaker consumption, but the mix shift from goods to services and a rising cost impost.

This emphasises the market’s vulnerability should a slowdown occur and begin to affect earnings.

US 10-year government bond yields fell 14bp. The positive correlation between bonds and equities appears to have broken down as the focus moves to risk aversion and a flight to safety.

We also saw a fall in the US dollar. This was probably a consolidation after a big run. It helped commodities and resource stocks, as did more signs of Chinese easing.

Australia again remains the market for these times.

The S&P/ASX 300 was up 1.2% for the week. It’s down only 2.5% for the calendar year to date, versus -17.7% for the S&P 500 and -27.2% for the NASDAQ.

Two key issues driving the market

We see two primary issues driving the outlook for markets.

The first issue is whether the US economy slows down or slips into recession.

Looking at recent bear markets, a recession has tended to lead to bigger drawdowns – such as in 2000-2002 and 2007-2009.

Pendal Focus Australian Share Fund

Now rated at the highest level by Lonsec, Morningstar and Zenith

Current investor surveys indicate a 50-55% probability of recession.

This comes down to views on what the Fed sees as acceptable inflation and what they will need to do to achieve it. There are two scenarios here:

- The positive scenario: Financial conditions have tightened enough, the economy is already slowing, inflation pressures are beginning to ease and therefore bonds have peaked and aggressive monetary tightening (and therefore recession) will not occur. A variant of this view is that the Fed will live with inflation in the mid to high 2s — rather than go for 2% — to avoid pushing the economy into recession

- The negative scenario: The economy will prove more resilient to rising rates, with consumers bolstered by excess savings and the labour market remaining tight. This will force the Fed to do more tightening and ultimately “break” the economy to control inflation. Proponents point to unemployment of 3.5% needing to rise to around 4.25% to create sufficient slack to ensure wages don’t reinforce inflationary pressures. The US has never been able to engineer such a rise in unemployment without it being associated with a recession.

The second major issue is whether the Chinese economy deteriorates or sees a policy-driven rebound.

Again, there are two scenarios:

- The positive view: China is close to peak Covid lockdown and the combination of re-opening and additional infrastructure stimulus will trigger a recovery, generate good commodity demand, and underpin resource stocks.

- The negative scenario: The economy is in far worse shape than the market realises. Lower rates reflect the financial vulnerability of property developers, stimulus will be ineffective due to low confidence, high input costs and inability to execute due to Covid restrictions.

Economics and policy

There is a lot of debate about whether we have seen peak inflation and peak bond yields.

Official data such as retail sales is signalling that the consumer remains strong, though there are signs the economy is slowing. For example, the Economic Surprise index – which shows the degree to which economic data is beating or missing estimates – is deteriorating in most countries. Consumer confidence is also weak and is at 40-year lows in the UK.

Sustainable and

Responsible Investments

Fund Manager of the Year

The combined effects of higher mortgage rates and fuel prices have reached levels consistent with previous consumer slowdowns. This indicator tends to lead by around 12 months.

Total financial conditions – which includes rates, equities and credit spreads – have tightened to a reasonable degree and should lead to a headwind of 1.3% of US GDP growth by Q3 2022.

We are also seeing signs that corporate pricing power – while still at high levels – may be easing.

There are signs that consumers are under some stress – particularly at the lower income end – with credit outstanding rising rapidly. This may support current consumption but is unsustainable.

Freight shipping rates are beginning to drop and there are early signs of a fall in US trucking rates.

That said, the freight rate may be a misleading signal due to a drop-off in Chinese exports. It’s unclear how much of this is a genuine de-bottlenecking of supply chains.

All this indicates the economy is responding to tighter financial conditions. It is slowing down and this is beginning to reduce inflation pressures.

This belief can be seen in forward pricing of inflation, where both break even yields and the 5-year inflation swap have rolled over since late April.

This could be positive for the equity market since it’s in line with the first scenario outlined above.

However there are still two key unknowns:

- This slowing could be the prequel to a recession. A slow-down and a recession will look the same initially. It will also probably result in negative earnings revisions, which the market will not like as we saw last week in the US.

- The second unknown is whether this will equate to inflation falling enough to allow the Fed to declare victory.

Fed Chair Powell has stressed that the labour market is resilient enough to weather tightening policy.

While this sounds reassuring, the question is whether a resilient labour market is consistent with inflation falling to target levels. If it is not, policy needs to tighten even more.

The labour force is very tight and this is driving wage growth. Some measures suggest we need to see employment decline by at least 1% to reduce wage pressure.

China

Economic surveys indicate the Chinese economy is weak. Q2 GDP is expected to decline 1.5% to 2%, with growth for the year coming in between 3% and 4%.

Beijing has responded with a larger-than-expected cut in its 5-year loan prime rate.

China bears see this as a move to prop up private developers who are facing a funding squeeze, thereby preventing deterioration rather than providing stimulus.

The more bullish view is that while this may not be a sizeable move, it is a very strong signal that the government will support property, similar to November 2014. Then it was the precursor to a big bounce in Chinese growth sentiment in 2015.

We remain cautious on a China recovery.

The property market appears to be deflating, but prices remain very high and developers are still too leveraged. At best the market stays flat, but the risk is to the downside, so any infrastructure related stimulus will only be offsetting this.

The other challenge is the lack of transparency over the extent of Covid and the real level of restrictions.

Europe

The ECB struck a more hawkish tone in response to poor inflation data. The market is now being primed for a first rate rise in July, with a possible 50bp move straight up. This is unlikely, but helped the Euro bounce off its lows against the US dollar.

Australia

There is little to read into the election outcome at this point. A majority government provides more clarity than a minority.

We are also likely to see more emphasis on reducing carbon emissions in coming years, which will have an impact on corporate disclosures and investment.

US earnings

Overall quarterly earnings were good. Full-year earnings lifted from about 5% to 11% growth.

However the outlook looks overly optimistic, with 9% eps growth expected in CY23 despite a slowdown.

Last week demonstrated the impact earnings headwinds can have. Broadline retailers missed earnings expectations as a result of freight costs and the mix shift in consumption.

Walmart and Target have joined Amazon in highlighting material gross margin pressure.

Underlying sales have not been particularly disappointing. But the impact of the unexpected mix shift caused problems as spending moved away from home, consumer electronics and sporting goods to travel, toys and luxury goods.

Inventories are also building in areas such as home furnishings and consumer electronics, while unit demand growth is dropping. This crimps a company’s ability to push through price rises.

The share of “private label” sales are rising. This is partly due to improved product availability as labour issues improve. It may also indicate consumers are “trading down” as real income falls – potentially a signal of softer consumption.

The overall impact were large hits to stocks in the previously defensive consumer staples sector.

This highlights the difficulty in identifying defensive pockets in this environment

Markets

We may be seeing a near-term low in the US equity market.

Historically, bear market bounces average a 15% gain over 30-40 days.

This does not signal the market has hit its lows for the cycle. Most technical signals have not indicated a degree of panic or capitulation. For example put/call ratio data has not yet moved into 99th percentile level – a usual indicator of capitulation. Nor have we seen high volumes in stocks being sold down.

Retail investors are yet to give up on the bull market.

The triple-leveraged NASDAQ ETF is still seeing large net inflows – despite being down over 60% year-to-date. Interestingly energy-related ETFs – among the best performing year to date – are seeing negligible inflows by comparison.

The high proportion of “buy” ratings on the market leaders of the past few years is another sign that we are yet to see capitulation.

We see scope for short, sharp bear-market rallies, but remain defensively positioned overall. We don’t believe it is yet the time to reload on high beta, illiquid names.

The Australian market last week saw a good bounce in the resource sector (+3.8%) on China optimism. The Technology (+5%) sector bounced as Xero’s management clarified a post-result message and emphasised confidence in improved margins and cash flow over time. Consumer staples (-3.3%) lagged, following the US lead.

About Crispin Murray and Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia. Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Three rules for turbulent times, Where wages go next, Renewables look set to win in Europe, Opportunities amid inflation

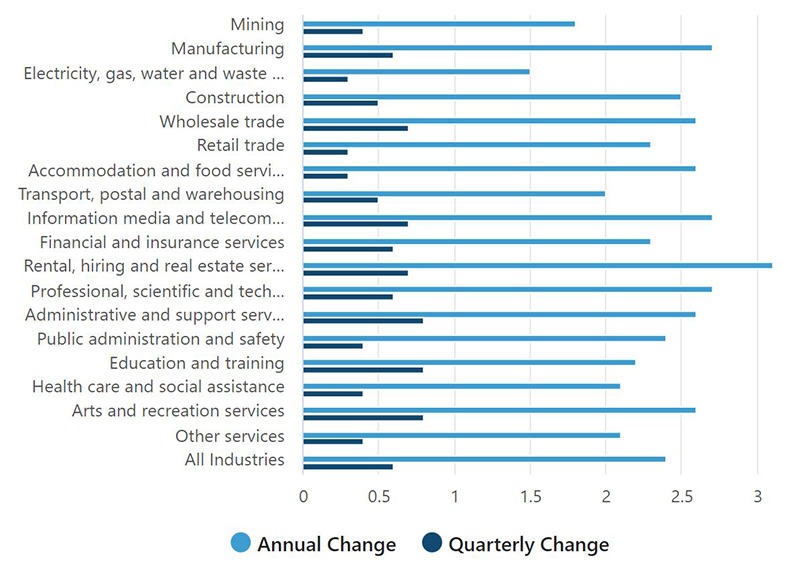

The latest wages data shows surprisingly modest growth in some sectors. But wages are the ultimate lagging indicator and that will soon change, says our head of government bond strategies TIM HEXT

DESPITE increasing anecdotal evidence of rising wages, the latest data shows the price of labour grew a modest 0.7% in the March quarter.

Over the year wage growth was 2.4%, according to the Wage Price Index (WPI) released yesterday.

Only one sector nudged over 3% annually and none grew at or near 1% for the quarter.

In some areas this was not surprising. But in industries such as construction and retail trade this flies in the face of worker shortages.

This will change, since we’ve really only fully opened up this year.

Wages are the ultimate lagging indicator — and patience is required.

Annual and quarterly changes, WPI Mar 2022 (total hourly rates of pay excluding bonuses, per industry):

Earlier this year the Reserve Bank had WPI front and centre when trying to ignore rising inflation and pressure to raise rates.

Unless we got strong wage growth, inflation would eventually come back, the RBA said.

But in May — as they threw in the towel and hiked rates — the RBA referenced broader measures of wages:

“The outlook for broader measures of labour costs had also been revised up; average earnings were expected to increase at a faster pace than the WPI, as firms turned to bonuses, allowances and other measures to attract and retain workers,” the RBA said in its May board minutes.

They also highlighted the great inertia of wage growth:

“While the inertia arising from multi-year enterprise agreements and current public sector wages policies would continue to weigh on aggregate wages growth in the near term, a period of faster growth in labour costs overall was in prospect.”

The main battleground this year will be public sector agreements across the big employment areas of health, education and transport.

Find out about

Pendal’s Income and Fixed Interest funds

The public sector employs around 20% of the workforce. These are state government responsibilities and for now at least the governments largely have a 2.5% wage cap.

However unions quite rightly point out that a 5% inflation rate is seeing real wages fall. With staff shortages in key areas they are in a good position to extract wage rises closer to 5% than 2.5%.

Maybe for teachers and nurses they can offer 2.5% and a “thank you” bonus of 2% for their efforts through Covid, keeping their policy “intact”.

The RBA expect the WPI to hit 3% by year end and 3.5% by the end of 2023.

Chances are we hit these levels sooner.

Let’s remember this is a good thing overall. It does however add to the narrative that inflation will struggle to fall back to target anytime in the next few years.

What it means for fixed interest investors

Investors should still be looking to inflation bonds ahead of nominal bonds.

In our portfolios we have been adding inflation risk, which has cheapened up in May.

Inflation will moderate next year but levels above 3% look like being more entrenched over the next two to three years, helped by wages eventually nearing 4% growth.

About Tim Hext and Pendal’s Income & Fixed Interest boutique

Tim Hext is a Pendal portfolio manager and head of government bond strategies in our Income and Fixed Interest team.

Tim has extensive experience in banking, financial markets and funding including senior positions with NSW Treasury Corporation (TCorp), Westpac Treasury, Commonwealth Bank of Australia, Deutsche Bank, Bain & Co and Swiss Bank Corporation.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia.

Find out more about Pendal’s fixed interest strategies here

About Pendal

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

In 2023, Pendal became part of Perpetual Limited (ASX:PPT), bringing together two of Australia’s most respected active asset management brands to create a global leader in multi-boutique asset management with autonomous, world-class investment capabilities and a growing leadership position in ESG.

Where are the opportunities emerging in fixed interest? Here are the latest insights from Pendal’s head of government bond strategies TIM HEXT

SO FAR 2022 has been an extraordinary year for markets.

This past week was perhaps the first where you could draw breath.

I am normally hesitant to forecast too far ahead given elevated uncertainties. “Conviction” is generally a positive word, but at times like this the negative simile of “entrenched” can be dangerous.

So let’s summarise where we are up to (at end of Monday, May 16):

| Data point | Market Pricing |

| Cash rates — Dec 2022 | 2.7% |

| Cash rates — Dec 2023 | 3.6% |

| 3-year govt bond | 2.83% |

| 10-year govt bond | 3.38% |

| 5-year inflation break-even (implied inflation) | 2.55% |

| 10-year inflation break-even | 2.35% |

Several things stand out in the above numbers.

Find out about

Pendal’s Income and Fixed Interest funds

First and most importantly the RBA is tightening because inflation is now well above its target band — and likely to stay there until mid-2024.

Below are our best guesses for the headline inflation rates going forward. They are conservative and risks are probably to the upside.

| Period | Estimate Quarterly Headline CPI | Estimated Annual Headline CPI |

| Current (Q1 2022) | 2.1% (actual) | 5.1% (actual) |

| Q2 2022 | 1.2% | 5.6% |

| Q3 2022 | 1.1% | 5.7% |

| Q4 2022 | 1.3% | 5.7% |

| Q1 2023 | 0.9% | 4.5% |

| Q2 2023 | 0.8% | 4.1% |

| Q3 2023 | 0.8% | 3.8% |

| Q4 2023 | 0.7% | 3.2% |

The fuel excise relief pushes Q2 2022 down 0.4%. But Q4 2022 gains back 0.4% when the full-rate duty returns (if indeed it ever does).

Clearly forecasting inflation over a year out involves some guesswork.

We assume goods prices moderate with some supply chain easing but service prices continue to rise above target with wages and strong employment.

When we look at the two tables above, the most glaring mispricing or opportunity is in 5-year inflation bonds.

Current breakeven pricing — ie the inflation rate that would make you neutral about owning them versus nominal bonds — is near the RBA target of 2.5%.

However for at least the next two years CPI is averaging close to 4.5%.

Unless you think inflation in the following three years will be around 1%, this is just wrong. And we haven’t even included the extra carry from owning these bonds.

A brief lull in inflation concerns has seen these 5-year inflation bonds cheapen and we have been adding them to our nominal portfolios.

Market expectations

As for market expectations on cash rates, like most observers I think they are a bit too high.

I think they will get to 2% this year, not 2.7%.

By mid next year inflation should be moderating, so it’s unlikely they will need to push above 3%.

Needless to say the mortgage fixed-rate cliff and variable rates 3% higher should be enough to drop the economy down a few gears. We get wage and employment data in the days ahead which will again recalibrate expectations.

About Tim Hext and Pendal’s Income & Fixed Interest boutique

Tim Hext is a Pendal portfolio manager and head of government bond strategies in our Income and Fixed Interest team.

Tim has extensive experience in banking, financial markets and funding including senior positions with NSW Treasury Corporation (TCorp), Westpac Treasury, Commonwealth Bank of Australia, Deutsche Bank, Bain & Co and Swiss Bank Corporation.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia.

Find out more about Pendal’s fixed interest strategies here

About Pendal

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

In 2023, Pendal became part of Perpetual Limited (ASX:PPT), bringing together two of Australia’s most respected active asset management brands to create a global leader in multi-boutique asset management with autonomous, world-class investment capabilities and a growing leadership position in ESG.

Here are the main factors driving the ASX this week according to portfolio manager Jim Taylor. Reported by portfolio specialist Chris Adams

WE SAW more of the same last week in terms of the market’s thematic drivers.

Inflation persists, the Ukraine conflict grinds on, Chinese lockdowns remain in place, parts of the crypto space are unwinding and global growth is slowing.

Market participants remain on edge as a result. The US inflation print didn’t serve as a circuit breaker. The headline number declined, but less than expected.

The S&P 500 fell 2.35% and the NASDAQ lost 2.77%. The S&P/ASX 300 was off 1.73%. The week’s falls were softened by a strong rebound on Friday.

Commodity prices have given up recent gains. Mega cap growth names in the US have also rolled over, now adding to index weakness now rather than holding things up.

The withdrawal of liquidity is making itself felt in speculative, profitless business models. Last week this manifested in the crypto market.

While details, exposures and implications are likely to be revealed in coming weeks, the issue is the potential for any second-order impact on the broader system.

US Treasury Secretary Janet Yellen said it did not count as “a real threat to financial stability”, but this needs to be watched.

The quarterly reporting season in the US shows consensus annual earnings for the S&P 500 remain intact for FY22 and FY23.

That said, the market has become a bit narrower in this regard, with energy doing a lot of the heavy lifting.

Find out about

Pendal Focus

Australian Share Fund

Crispin Murray,

Head of Equities

It is also notable that on the back of this reporting season, corporate activity in buybacks and capex spending is up strongly for the US.

Fed policy

The Fed continued to reinforce the expectations of a series of 50 bp hikes.

Fed Governor Powell said tackling inflation would “include some pain” as the impact of higher interest rates was felt — but that was preferable to prices continuing to rise.

The Fed was “prepared to do more” if data turned the wrong way, he added.

That said, Altanta Fed President Bostic noted that a 75bp hike was still a low probability outcome. There were signs of improvement in a number of supply chain issues, he said.

For example, trucking companies are no longer turning down business and shipping bottlenecks are easing. He sees as yet unrealised downside risks to demand from the squeeze on finances.

US Inflation

The inflation rate fell, but not as far as some hoped.

The April CPI measure rose 0.3% month-on-month, ahead of the 0.2% consensus. Core CPI (excluding food and energy) rose 0.6% month-on-month versus 0.4% expected.

Headline inflation fell from 8.5% to 8.3% and core from 6.5% to 6.2%, helped by base effects.

While we have passed the peak, price growth remains very elevated and consumer expectations conflating “peak inflation” with falling prices may cause some consternation.

Overall, it was a disappointing set of numbers, with core elements of inflation proving to be sticky.

Some details worth considering:

Used vehicle prices fell only 0.4% and new car prices rose by 1.1%.

Rents rose 0.5% and are proving very resilient.

Plane tickets rose 19%, reflecting booming demand and airlines successfully passing through fuel price increases.

Overall the number of CPI components seeing price growth remains very broad by historical standards. While inflation is starting to decline in some goods, it is just starting to pick up in services.

This is feeding through to measures of consumer sentiment, which have ticked down.

The petrol price, which is important to consumer hip pockets and inflation prints, continues to remain very high.

There are some signs of pressure in the labour market easing, with the initial unemployment claims 4-week average climbing 22,000 to 193,000 over the last month.

The EVRISI Trucking survey, historically a good measure of economic pulse, also continues to track down, which suggests softer economic growth.

Australia

At this point the implied path of rate rises in Australia is similar to the US — despite our goods and wages inflation being nowhere near the US experience.

Sustainable and

Responsible Investments

Fund Manager of the Year

We are seeing private sector wage growth come through in Australia, but it is well below the US and is expected to peak at 3.7% in 2024.

We are keeping an eye on the New Zealand economy, where rate increases have led to falls in house prices. The question is whether this causes an air pocket in consumer spending at some stage in the remainder of 2022.

Markets

We saw significant dislocation in crypto markets as stable coin TerraUSD, with US$18 billion of value, lost its peg to the dollar. The events that precipitated the crash appear to be analogous to a traditional bank run in the non-digital world, coupled with a good old-fashioned short squeeze.

Sentiment wasn’t helped when crypto exchange Coinbase quarterly reported a loss of US$430 million, citing 20% fall in monthly transacting users.

Elsewhere, commodity price falls on the back of further China lockdowns and increased prospects for a European recession saw resource stocks giving back a lot of the recent gains.

Value continues to win out over growth. The mega cap tech names in the US are at last reflecting the pain felt elsewhere across the market.

The bond market stabilised and is no longer going down in lockstep with equities. US 10-year government bond yields fell 21bps. The Australian equivalent fell 7 bps.

The Australian equity market held up better, but less so than in past weeks as the resource sector saw some pressure.

Weakness across the technology, lithium, gold, base metals and REITs sectors contrasted to financial strength on the back of some recent results.

About Jim Taylor and Pendal Focus Australian Share Fund

Drawing on more than 25 years of experience investing in top-performing Australian companies and a background in accounting, Jim manages our Long/Short Fund and co-manages our Imputation Fund. He is a Chartered Accountant with membership of the Australian Institute of Chartered Accountants.

Pendal Focus Australian Share Fund is managed by Crispin Murray. The fund has beaten its benchmark in 14 years of its 18-year history (after fees), across a range of market conditions. Find out more about Pendal Focus Australian Share Fund here.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.