Pendal Sustainable Balanced Fund – Class R (APIR: BTA0122AU, ARSN: 637 429 237)

Pendal Sustainable Balanced Fund – Class G (APIR: PDL4756AU, ARSN: 637 429 237)

Pendal Sustainable Balanced Fund – Class Z (APIR: PDL0478AU, ARSN: 637 429 237)

Pendal Sustainable Conservative Fund (APIR: RFA0811AU, ARSN: 090 651 924)

Investment Manager and Exclusionary Screens

We have decided to replace AQR Capital Management, LLC (AQR) as the investment manager of the international shares portion of the Funds and bring management in house, leveraging the expertise of Pendal Group’s global equities teams. The change will take place on or around 31 May 2022.

Also, the exclusionary screens of the Funds will be enhanced consistent with broad market feedback around the screens for a contemporary sustainable strategy, improving the portfolios’ sustainability footprint. Investment in certain companies and industries which are materially involved in activities we consider contrary to the ethical and ESG goals of the Funds will be excluded, including industries such as:

- Fossil fuels

- Uranium

- Logging

- Gambling

- Pornography

- Weapons

- Alcohol

- Tobacco

- Animal testing

- Predatory lending

These exclusions may be applied differently across the asset classes of the Funds.

Why are we making the change?

We have decided to implement these changes because we believe it is in the best interests of investors to bring the management of the international strategy in-house, following a review of the existing external investment manager, AQR. We expect the changes will deliver improved investment and sustainability outcomes for the Funds, providing investors with better risk-adjusted returns over the medium to long term.

What will stay the same?

The Funds’ investment objective, benchmark, management fee and buy-sell spread will remain unchanged.

What do you need to do?

No action is required. You will be able to continue to invest or withdraw from the Funds.

An updated Product Disclosure Statement (PDS) for each Fund reflecting the change in investment manager and exclusionary screens is available on www.pendalgroup.com. If you would like a hard copy of the PDS, please contact us.

If you have any questions about your investment or would like further information regarding the changes, please contact our Investor Services Team on 1300 346 821 (for Australian investors) or +612 9220 2499 (for overseas investors) from Monday to Friday, 8.30am to 5:30pm (Sydney time). For any questions regarding how this change may impact your own financial situation we recommend that you speak to your financial advisor and/or tax accountant.

How the oil price is affecting sustainable investors, impact of falling Yen on equities, pre-election rate rise on the cards, what’s driving China sentiment

A monthly insight from James Syme and Paul Wimborne, managers of Pendal’s Global Emerging Markets Opportunities Fund

FOLLOWING the initial shock of the Russian invasion of Ukraine, it is becoming possible to focus on the secondary effects around the world.

These substantially result from the disruptions to the supply of many commodities.

Although highly volatile, prices of many basic commodities have moved very sharply since the start of the year.

Compared to the end of 2021, the Brent crude oil price is (at the time of writing) up 30%, wheat futures are up 38%, while and urea prices are up significantly (after doubling in the fourth quarter).

Other major Russian export commodities have also risen, but for the world’s poorest countries the trinity of fuel, food and fertilizer is absolutely key.

Many of these countries are significant importers of these products, subsidise them to their populations or have large weights of these in their inflation baskets.

This means sharp price rises stress the fiscal and current account balances. They also increase inflation and reduce the ability of consumers to purchase other goods and services.

Some of these effects are being seen in major frontier countries, whose equity markets are too small to be in the mainstream emerging market equity asset class.

Find out about

Pendal Global Emerging Markets Opportunities Fund

Pakistan

For example, in Pakistan — which was recently demoted from the MSCI EM Index — a developing political crisis (where the opposition are seeking to bring down the government through a vote of no confidence) coincides with the need to renew a $6 billion debt with the IMF.

Without IMF funding Pakistan will almost certainly face a balance of payments crisis, as foreign exchange reserves have fallen recently to just two months of import cover.

The ramping price of imports has pushed inflation to 12.7% in the year to March, accompanied by a sharp fall in the Pakistani rupee.

Sri Lanka

Meanwhile, Sri Lanka’s poor agricultural policies — combined with the collapse of tourism after Covid — have created a weak starting point from which to deal with soaring prices.

Widespread street protests over severe shortages of food and power, and rampant price inflation led to the resignation of all the ministers in the government cabinet, and of the central bank governor.

In a sign of the depth of the crisis, the new finance minister then resigned after less than 24 hours in post.

Sri Lanka faces soaring inflation (18.7% in the year to March) and a probable sovereign debt default in July.

Mainstream EM markets

Three mainstream emerging markets are potentially exposed to these kinds of risks: Egypt, India and Indonesia.

Egypt is the most exposed of the three. Russia and Ukraine are major wheat exporters. Wheat is a particularly high component of Middle East and North African diets — and Egypt imports over 60% of its wheat.

Inflation has been pushing higher in recent months (to 8.8% in the year to February). Policymakers have begun to react, devaluing the Egyptian pound by 15%, hiking interest rates and imposing price controls on bread.

While these steps are likely to help — and Egypt is a net oil exporter — the non-oil component of the economy is already showing stress, with PMIs declining sharply.

The risk is a repeat of the political unrest that led to the overthrow of the Mubarak government during the Arab Spring in 2011.

There are, so far, no signs of unrest, but Egypt must be carefully monitored in the months ahead.

Sustainable and

Responsible Investments

Fund Manager of the Year

India

India has historically had vulnerabilities, both as a major importer, but also as a major subsidiser of these commodities.

India’s current account deficit will weaken with oil prices above $100/barrel — and inflationary pressures are showing. But India is in a much better position than in previous periods of commodity price inflation.

Firstly, the reforms to the subsidy regime have essentially removed the risk to the fiscal balance.

Diesel subsidies were removed in 2014, while direct LPG subsidies were replaced with cash transfers to poorer citizens, and fertilizer subsidies have been substantially reduced in recent years.

Secondly, India has in recent years become a major producer of wheat, even becoming a small exporter, while a series of rich harvests have allowed the government’s wheat reserves to reach 21 million tons against a targeted level of 7.5 million tons.

The economic reforms the government has driven have absolutely moved India onto a safer and more sustainable footing, and the country should feel the benefit of this in coming months.

Indonesia

The other major emerging market to have had historical problems with fuel subsidies is Indonesia. Indonesia also had problems in the mid-2000s from the fiscal effects of fuel price subsidies.

In 2004-5, newly elected president Yudhoyono faced a budget crisis, as spending on fossil fuel subsidies for gasoline, diesel and kerosene had reached $8bn.

The government was forced to trim fuel subsidies to alleviate the budget deficit, but this both lifted inflation and hit growth.

Subsequently, though, fuel subsidies have been first reformed and then, under current president Widodo, removed.

Additionally, inflation in Indonesia is very benign, reaching just 2.6% to March, so commodity price pressures are far more manageable.

Emerging markets are generally countries with macro-economic vulnerabilities, but the examples of India and Indonesia show that good planning and effective economic reform can limit these vulnerabilities.

While frontier equity markets and some of the major emerging market sovereign debt issuers may face a difficult 2022, emerging equity markets look to have lower secondary risks from the conflict in Ukraine.

About Pendal Global Emerging Markets Opportunities Fund

James Syme and Paul Wimborne are senior portfolio managers and co-managers of Pendal’s Global Emerging Markets Opportunities Fund.

The fund aims to add value through a combination of country allocation and individual stock selection.

The country allocation process is based on analysis of a country’s economic growth, monetary policy, market liquidity, currency, governance/politics and equity market valuation.

The stock selection process focuses on buying quality growth stocks at attractive valuations.

Find out more about Pendal Global Emerging Markets Opportunities Fund here

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Here are the main factors driving the ASX this week according to our head of equities Crispin Murray. Reported by portfolio specialist Chris Adams.

Find out about Crispin’s Pendal Focus Australian Share Fund

Find out about Crispin’s sustainable Pendal Horizon Fund

FIVE factors combined to drag down equity and bond markets last week, while commodity prices also fell:

- Further signals of aggressive Fed tightening, which saw US two-year government bond yields rise 21bps

- Concerns over Chinese economic growth with the Shanghai stock market and yuan both falling sharply

- Fears that supply chain problems will re-emerge as a result of Chinese lockdowns

- Some fear of a slowing US economy

- Selective US earnings disappointments – primarily from Netflix and Alcoa.

The combination of factors meant technology and cyclical sectors were both affected.

The S&P 500 fell 2.7% last week and is now down 10% year to date. The NASDAQ lost 3.8% last week and is down 17.8% for the year.

The S&P/ASX 300 (-0.7%) held up better, but the futures market suggests that effect will be lagged into this week. It is up 1.8% for the year.

Market paradoxes

Several paradoxes are facing the market, complicating portfolio positioning:

- US growth is strong and earnings revisions positive — but the market is pricing in a slowdown as the mechanism for the Fed to reduce inflation

- Measures of investor sentiment are negative — but flows into equity markets remain strong

- There are signs inflation may be peaking — but bond yields continue to rise

- Lockdowns are seeing sentiment towards Chinese growth sour — but commodities and resources have been strong.

We remain wary of the near-term outlook in this environment.

As mentioned in previous weeks, the tighter financial conditions needed to tame inflation require equity markets to remain flat at best.

Meanwhile we are seeing the twin headwinds of uncertainty over Chinese growth and the market’s need to deal with what is likely to be back-to-back 50bp rate hikes in the US.

Pendal Focus Australian Share Fund

Now rated at the highest level by Lonsec, Morningstar and Zenith

US inflation and rates

A number of signs suggest US inflation has peaked:

- Statistically we will see the biggest months of inflation growth in 2021 – April, May and June – rolling off the annual figures

- Commodity prices are rolling over off recent peaks

- The US dollar continues to rise

- There are signs of supply chain pressures easing in the US. Shipping rates for freight and containers have begun to fall. There is also evidence of less pressure in US trucking systems.

- Employment participation rates are creeping higher. There’s an argument the impact of inflation and running down of savings is slowly encouraging people back into the job market.

- Company wage surveys have begun to ease. This reflects less pressure to raise wages, which have already been materially re-based.

- Company pricing power surveys are stalling, albeit at historically high levels

We can conclude that at this point inflation is unlikely to get worse. But before declaring victory on inflation it’s important to note three things:

- The labour market remains very tight, so some wage pressure is likely to remain

- Supply chain issues could be about to flare up as a result of lockdowns in China

- The US economy remains strong, though there is a shift in demand to services. Coincident indicators are robust. Continuing unemployment claims are at 50-year lows, bank lending is rising 7% year-on-year and house prices remain strong.

Key question

The key question is: if inflation rates have peaked, where do they fall back to? This comes down to two unpredictable factors:

- At what point will the Fed tolerate inflation in order to avoid a recession?

- The Fed’s ability to control the economy

The Fed maintains a hawkish message.

Federal Open Market Committee member James Bullard mentioned the potential need for a 75bp hike in some remarks last week. Again, there was talk of an “expeditious” need to get back to neutral.

At this point we think back-to-back 50bp hikes are more likely — with the potential for a third — as well as a start of quantitative tightening.

The market continues to price in further acceleration of rate hikes. The consensus is now 2.75% by the end of 2022, versus 2.5% previously.

It’s been a long time since markets have had to face such a rapid tightening cycle. There is still a question over the degree to which this is priced in. This underpins our near-term caution.

There is also a view that Fed tightening cycles will continue until something “breaks” — such as the 2016 collapse in oil prices, the 2012 Eurozone Crisis or the Russia/Long Term capital management crisis in 1998.

This is also making some in the market cautious.

Sustainable and

Responsible Investments

Fund Manager of the Year

China

There has been a rapid deterioration in sentiment towards the Chinese economic outlook due to a combination of:

- Lockdowns choking demand and supply chains

- Currency appreciation relative to competitors

- Global slowdown

- Weak consumer confidence

- Property market remaining fragile

It is estimated that 44 Chinese cities are under some form of lockdown. This equates to 25% of the population and 38% of GDP — of which around 16% is in strict lockdown.

Estimates indicate Chinese growth could slow from 4.8% in Q1 to less than 2% in Q2.

This risk is emphasised by a sharp fall in road freight volumes (a reasonable indicator of Chinese economic health) and a backlog of ships off Shanghai.

There were hopes that policy easing would see a moderate pick-up in the housing market. This is not yet showing any sign of coming through.

The rise of the US dollar — against which the Chinese yuan is managed — has left China in a difficult competitive position given the relative depreciation in the Japanese yen and Korean won.

This exacerbates the existing pressure on China’s export engine from slowing global growth and a shift in consumer demand from goods to services.

Under pressure

This pressure seems to have forced a crack last week, with the currency breaking down relative to historical ranges.

It moved about 3% against the US dollar. While that may not be large in absolute terms, it is a four-standard-deviation event in historical terms.

The equity market was also pummelled. The rebound after the government’s comments in support of the market following concerns earlier in the year has proved short-lived, with some signs of outflows in foreign capital.

The policy response so far is regarded as too limited. The People’s Bank of China announced a 25bp cut in the bank reserve requirement ratio from April 25.

The immediate impact is concern around commodity demand, which risks being crimped by slower growth and a weaker currency.

We think the structural story in commodities remains attractive. But there is a sense it is a very long position among investors at the moment.

Aggressive Fed tightening — plus slowing Chinese growth and a devalued yuan — may see a sharp near-term unwind in the sector.

This is also materialising in some recent Australian dollar weakness.

Markets

Most asset classes weakened in response to all this.

Some are pointing to negative sentiment measures as a possible support. We are not so convinced by this — we are still seeing positive inflows into equity markets.

This is the key week for US earnings.

Last week saw two high-profile disappointments which dragged on sentiment:

- Netflix: The US$100bn cap stock fell 38% in a week. Several issues (such as switching off the Russian subscriber base) were specific to the company, but they exacerbated market concerns regarding consumer demand. Combined with other issues outlined above, this seemed to be a negative catalyst for mega cap growth names which have previously supported the market overall.

- Alcoa: The alumina and aluminium producer fell 23% on concerns regarding costs – particularly around energy which is a large input into the refining and smelting process. This was compounded by the broader growth outlook.

Interestingly, despite a few major disappointments aggregate revisions to Q1 FY23 have been positive, reflecting what remains a strong economy.

For example, US airlines are seeing strong upgrades. At this point, earnings remain supportive of markets.

The ASX missed the big US fall on Friday, which is likely to emerge this week.

The local market was helped by the private equity bid for Ramsay Health Care (RHC, +30.6%). This supported the health care sector. Other than this, defensive sectors out-performed.

Mining was weak on a series of disappointing quarterly production report. Costs and production both disappointed, mainly due to the disruption associated with Omicron.

About Crispin Murray and Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia. Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Generational shift drives ESG opportunity, which fixed interest funds are well placed for rising yields, what’s next for China and beware the ‘brownium’

Here are the main factors driving the ASX this week according to our head of equities Crispin Murray. Reported by portfolio specialist Chris Adams.

Find out about Crispin’s Pendal Focus Australian Share Fund

Find out about Crispin’s sustainable Pendal Horizon Fund

The recent recovery in equity markets looks to be ending as the S&P 500 fell -1.2% and the NASDAQ -3.9% last week.

Australia remains more defensive in this environment, falling just 0.3% for the week. More hawkish comments from the Fed prompted the fall.

It signalled a 50bps hike in rates for May, absent any major new shock. It also reinforced the message that quantitative tightening is on its way. While this was known, it triggered a further sell off in long-dated bonds.

US 10-year Treasury yields rose 32bps for the week. It also took the yield curve back into positive territory.

This reinforces the key message that the Fed needs overall financial conditions to tighten sufficiently to cool wage inflation.

Surging equity markets loosen overall conditions, and the Fed is likely to try and prevent this.

China is also weighing on market sentiment. The situation in Shanghai appears to be deteriorating, with lockdowns potentially remaining in place into May.

This puts growth at risk but, unlike the US, Beijing’s desire to achieve its growth target is likely to see policy stimulus to mitigate the effect of lockdowns. This would be supportive of commodities.

Fed policy

The Fed remains focused on tightening financial conditions, as it tries to slow the economy enough to choke off wage inflation. The trick will be to do this without triggering a recession.

To this end, both Fed minutes and comments from Board member, Lael Brainard, last week suggested that quantitative tightening may proceed at a faster pace than expected. As well as implying greater risk to the upside for inflation.

Federal Open Market Committee (FOMC) minutes flagged a plan to shrink the balance sheet at a run rate of ~US$95bn per month, from May. This would comprise US$60bn in Treasuries and US$35bn in mortgage-backed securities.

This would enable them to reduce the balance sheet from US$9tr to US$6tr over 3 years. The technical aspect of how they would accomplish this was slightly more hawkish than the market expected.

The Fed also reiterated talk of moving ‘expeditiously’ towards neutral. This raised expectations of back-to-back 50bp hikes in rates.

These factors triggered the sell-off in bonds and led to slight steepening in the yield curve.

US 10-year Treasury yields are very close to a multi-decade trend line. This is being seen by some as the potential catalyst for a rally on bonds, as we saw for equities in May. Others see the potential for bonds to break the trend line, which could trigger a sell-off in equities and underperformance from growth stocks.

Any sustained rally in bonds would be contrary to the Fed’s goal of tighter monetary conditions.

We have also seen credit spreads tighten as fears around the US economy have eased. Hence the Fed remains hawkish on inflation and the need to tighten.

Former Fed official, Bill Dudley, noted in a Washington Post article that the Fed will only be able to achieve its inflation goals without increasing rates past 2.5% if;

- supply chains ease sufficiently

- the shift from goods to services ease inflationary pressures, and

- more people return to the labour market as wages move higher.

His key point is that the Fed needs tighter financial conditions if their plan is to work. This requires bond yields to move higher or equities to be flat to lower.

US economy

We are at an interesting juncture. Lagging indicators such as labour remains very strong, and wages are also continuing to slowly climb, with the latest Atlanta Fed wage tracker data coming in at 6.0 vs 5.8% quarterly wage growth.

Q1 GDP growth will slow down dramatically, with estimates down 1%.

Much of this reflects a reversal in the inventory build that drove Q4 growth, however some lead indicators of growth are signalling slowing momentum.

Consumer spending remains critical to the growth outlook. Anecdotally, consumption remains resilient, despite the increase in mortgage rates and inflation.

The US consumer is helped by having record net worth and a strong balance sheet, with US$3.9tr in savings and wages growing strongly in nominal terms.

In addition, the rotation from goods to services is becoming more evident.

Trucking appears to be showing signs of slowing, which is typically a good lead on consumption, however airline sales are strong.

There are some signs of easing inflationary pressures. For example, the backlog of container ships is falling rapidly. So too are the pricing rates for freight.

Pendal Focus Australian Share Fund

Now rated at the highest level by Lonsec, Morningstar and Zenith

China

Shanghai’s streets are deserted, while attendance at the Melbourne Grand Prix was 420,000 over the four days.

This demonstrates how quickly things can change in the space of just a few months in the Covid era.

Official statistics suggest that the number of districts classed at “high risk” of Covid started declining last week. The share of nationwide GDP at risk also dropped from over 30% to under 20%.

However, there is more anecdotal evidence that the trends are not improving.

The situation in Shanghai has deteriorated. There are reports of food shortages as lockdowns and a reluctance to deliver to Shanghai is constraining supplies and leading to unrest.

This situation has the potential to affect supply chains. It is also relevant for specific industries. For example, Shanghai and Jilin, another city affected by Covid, provide 20% of China’s auto production.

The State Council noted the ‘especially difficult’ conditions facing a number of service industries and the desire to underpin growth this year. This is likely to lead to more stimulus which, given the limits on consumer spending, may have to come in the form of infrastructure spending. This would be supportive of commodities.

Australian Federal election and rates

From a market perspective there appears to be little at stake in this election. Given Labor’s ‘small target’ approach and the likely focus on issues such national security.

However, once the election is over it is likely that the RBA will be looking to move rates. The April meeting release removed the reference to ‘patience’ in terms of the RBA’s stance.

Recent comments have noted wages rising outside of fixed agreements and building wage pressure.

The effect of floods on construction costs, further supply chain disruption from China and the stimulatory effect of the budget have also been flagged.

All this signals the need to raise rates.

June is set to be the ‘live’ meeting, with a debate as to whether they move 15 or 40bp.

The market is implying a cash rate of 3% by June 2023, which at this point we think is a bit high.

The financial stability review released last week showed that the loan-to-value distribution in mortgages has improved significantly in the last two years due to lower rates and higher house prices.

While that signals a more resilient housing market, it should be noted that the proportion of people with more than 6x debt to income levels has risen significantly, which raises the sensitivity to rate increase.

Part of this sensitivity to rates is initially mitigated by a high proportion of people maintaining higher than required repayments in recent years.

Data suggests that 40% of households would not be affected by a 200bp rise in mortgage rates as their current repayments are already high enough.

That said, by the same measure 20% will see their repayments rise by more than 40%.

The added complexity this cycle is the higher proportion of fixed rate mortgages. This will defer the initial impact of rate increases but may cause issues 18-24 months down the line.

Overall, a 150bp move in mortgage rates would reduce capacity to pay by around 10%. It would also render consumer discretionary exposure, particularly in goods, vulnerable to a slow down.

Sustainable and

Responsible Investments

Fund Manager of the Year

Markets

Renewed concerns over Fed tightening and uncertainty in China saw bond yields rise while equity and commodity markets fell.

Heading into US earnings season, headline revisions still look good. However, once the energy sector is stripped out, the effect of input costs, labour, supply disruptions and a slowing consumer is beginning to tell, with the rest of the market seeing revisions back to flat for the calendar year to date.

The other thing to watch is the US dollar, which continues to grind higher and close to testing its highest levels in five years.

The Australian market saw more defensive sectors such as utilities, energy, and staples outperforming, while tech and discretionaries lagged.

About Crispin Murray and Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia. Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

How the federal budget will affect rates and bonds, why ASX stocks and Australian bonds look good, how to find competitive advantage among international shares

Where will interest rates be at the end of 2022 and 2023? Here’s a view from Pendal’s head of government bond strategies TIM HEXT

THE Reserve Bank is keen to make its recent dramatic about-turn on rates look like an evolution — and not the revolution it is.

This week’s statement edged us a little closer to a June hike. The RBA dropped its usual reference to being “patient” — and its commitment to highly accommodative monetary policy.

The statement finished with:

“Over coming months, important additional evidence will be available to the Board on both inflation and the evolution of labour costs.

“The Board will assess this and other incoming information as its sets policy to support full employment in Australia and inflation outcomes consistent with the target.”

We get Q1 CPI on April 27, which will likely be around 1.7% and 1.2% underlying.

We also get Q1 Wages Price Index on May 18. This will be less spectacular but will not stop a June tightening.

Meanwhile there is a good chance one of the next few unemployment numbers will be sub 4%.

The RBA will therefore be able to say in May that inflation is sustainably within its band in the medium term and can tighten in June.

A May hike is not impossible. But with a federal election and the desire to evolve the narrative June is odds on.

News to some

Many (including us) expected all this. But judging by yet another sell-off of around 0.15% it was news to some.

Three-year physical bonds (as measured by the April 2025 Commonwealth Bond) are now nudging 2.5%.

Ten-years are nearly at 3% and with a large new syndication of a 2033 Commonwealth Bond next week will likely break 3%.

Find out about

Pendal’s Income and Fixed Interest funds

The short end is now predicting cash rates to peak around 3.5% in early 2024.

If mortgage holders were aware of this impending doom house prices would be off 10% tomorrow.

Mortgage brokers I’ve spoken with are telling clients rates shouldn’t go up by more than 1% to 1.5%.

The average size of a new mortgage is now well over $600,000 – so an extra $20,000 a year in interest is coming borrowers’ way if markets are correct.

We still think a 2.5% cash rate is neutral.

Inflation is currently peaking. Although it will remain elevated into 2023 we think by late next year the RBA won’t likely need to push cash rates higher than 2.5%.

Rates should finish 2022 around 1.25% and 2023 around 2.5%.

Therefore markets are now cheap in the medium term.

However with the US Federal Reserve determined to keep pushing its rates higher – and ramping up the hawkish rhetoric – all markets globally will likely remain under pressure.

For those of us concerned with the short term as well as the medium term, the challenge will be to balance these two in the months ahead.

About Tim Hext and Pendal’s Income & Fixed Interest boutique

Tim Hext is a Pendal portfolio manager and head of government bond strategies in our Income and Fixed Interest team.

Tim has extensive experience in banking, financial markets and funding including senior positions with NSW Treasury Corporation (TCorp), Westpac Treasury, Commonwealth Bank of Australia, Deutsche Bank, Bain & Co and Swiss Bank Corporation.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia.

Find out more about Pendal’s fixed interest strategies here

About Pendal

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

In 2023, Pendal became part of Perpetual Limited (ASX:PPT), bringing together two of Australia’s most respected active asset management brands to create a global leader in multi-boutique asset management with autonomous, world-class investment capabilities and a growing leadership position in ESG.

What’s next for rates now the Reserve Bank has lost its patience? Assistant portfolio manager ANNA HONG explains

THE Reserve Bank this week took a small step towards a June rate hike.

In February and March, Governor Phil Lowe’s monthly statements referred to the board’s willingness to be “patient” as it “monitors how the various factors affecting inflation in Australia evolve”.

This month the word “patient” was conspicuously absent — though the omission was anticipated by the market.

“Over coming months, important additional evidence will be available to the board on both inflation and the evolution of labour costs,” Dr Lowe said.

“The board will assess this and other incoming information as its sets policy to support full employment in Australia and inflation outcomes consistent with the target.”

Some are expecting a hike in May. But the reference in this month’s statement to upcoming inflation data on April 27 and wages data on May 18 suggests a pre-election rate rise in May is unlikely.

It’s more likely next month’s statement will feature a further change of language that paves the way for a rate hike in June.

Only twice in Australian history has the RBA changed interest rates during an election — the first was a rate hike, the second a rate cut.

Find out about

Pendal’s Income and Fixed Interest funds

Both times there was a change in government.

Dr Lowe declined to cut rates in May 2019 — just 11 days before the last federal election — even though unemployment was drifting higher.

We expect this time will be no different.

The first election rate change occurred in November 2007.

Back then RBA Governor Glenn Stevens decided to raise interest rates 17 days out from the election to manage rising inflation.

This action — and two more rate hikes in early 2008 — helped Australian inflation peak in September 2008. Though the global financial crisis may have played a bigger role.

There are similarities between our current state and November 2007.

But inflation is now more supply-side led. And the RBA has this time chosen to remain dovish for longer, continuing to leave cash rates at 0.1%.

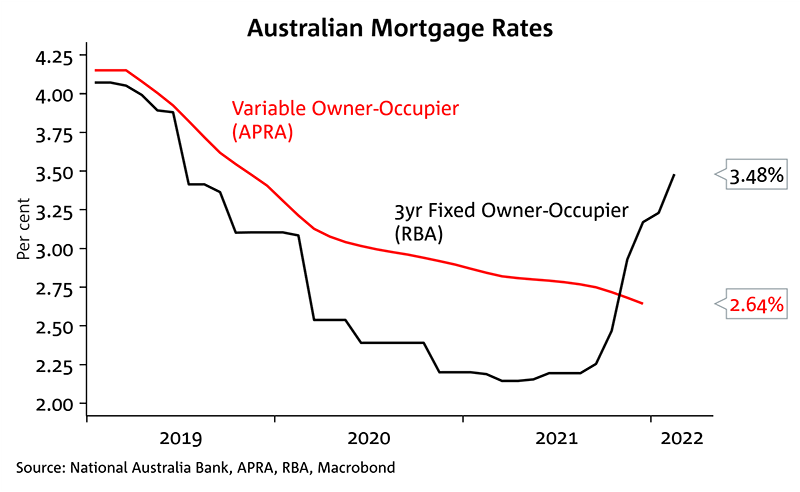

Despite that, the banks are already repricing for the future.

Advertised fixed rates have risen more than 60% from an average of 2.14% to 3.48%, according to APRA and RBA data.

In addition, the serviceability buffer was raised from 2.5% to 3% in the new home loan assessments.

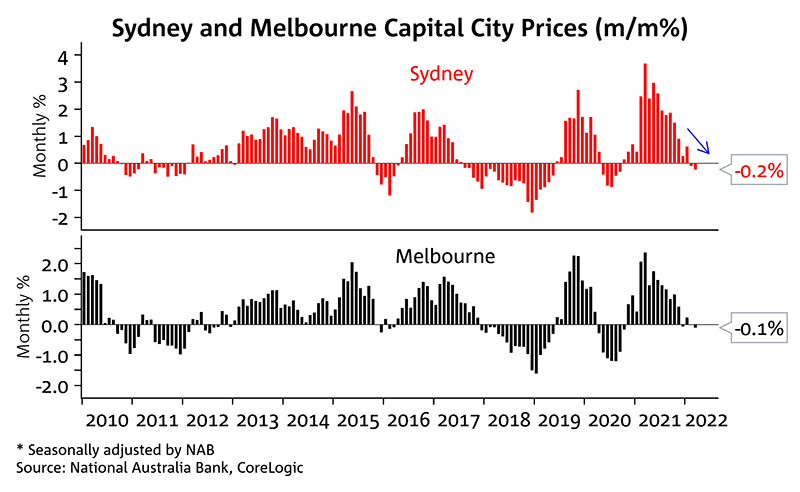

This has led to Sydney and Melbourne house prices cooling off, signalling that a phase of high capital gains may be behind us.

With a surge in fixed-rate borrowing well and truly behind us, variable rate rises are not far away.

The market is predicting more than 3% of rate hikes in the next few years. If that’s correct it will be interesting to see how mortgage holders cope.

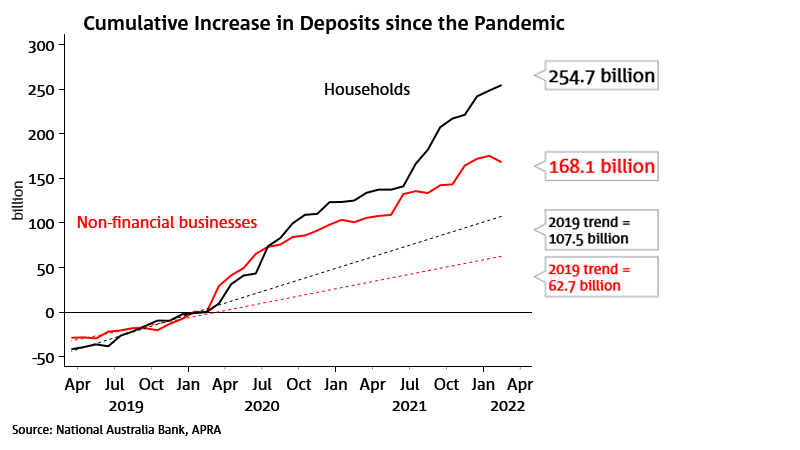

Household deposits continue to rise — up $255 billion since the pandemic — indicating Australian households have a war chest to cushion the blow.

But that’s not necessarily good news.

Delayed action in tackling inflation may result in a long, drawn-out battle to curb price rises fuelled by supply chain issues.

Will the supply chain issues ease sufficiently to prevent a protracted rate hike cycle?

The RBA will be cautiously watching this dynamic.

Looking ahead, we have the RBA Financial Stability Review coming up, in addition to the NAB Business Conditions and CBA Household Spending Intentions.

We are keen to understand the RBA’s assessment of the impending mortgage stress and its concerns around the ability of the wider economy to withstand rate rises.

NAB Business Conditions and CBA Household Spending Intentions will provide a good gauge on forward-looking business and consumer confidence.

If those indicators remain elevated we may see costs of living get another leg up.

Portfolio implications

For many investors, the current dilemma in portfolio decisions relates to the relative importance of the geopolitical instability in Europe versus the inflation trajectory.

With Australian Government 10-year bonds appearing to have found support in the 2.8% to 3% range, a balanced portfolio can increase its defensiveness knowing that most of the inflation concerns are already priced in.

Furthermore, 10-year real yields are now positive (more than 0.3%).

That carry can provide good protection for investors.

About Anna Hong and Pendal’s Income and Fixed Interest team

Anna Hong is an assistant portfolio manager with Pendal’s Income and Fixed Interest team.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia. In 2020 the team won the Australian Fixed Interest category in the Zenith awards.

With the goal of building the most defensive line of funds in Australia, the team oversees A$22 billion invested across income, composite, pure alpha, global and Australian government strategies.

Find out more about Pendal’s fixed interest strategies here

About Pendal Group

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Here are the main factors driving the ASX this week according to portfolio manager Jim Taylor. Reported by portfolio specialist Chris Adams.

Find out about Pendal Focus Australian Share Fund

Find out about Pendal’s sustainable Pendal Horizon Fund

THERE’S been increased chatter about yield curve inversion and potential recession, on top of speculation around inflation, commodity prices and the conflict in Ukraine.

Fed Chair Powell is showing signs of frustration with the view linking curve inversion to an inevitable recession — particularly since recent data indicates the US economy remains very strong.

The minutes from March’s Federal Open Market Committee meeting — due this week — are expected to contain details on the Fed’s thoughts about quantitative tightening.

Australian data also suggests ongoing economic strength, but the signs are more worrying in Europe. German data in particular shows an increased risk of recession.

Policy decision and timing in Europe are complicated by a strong inflationary pulse. This is underpinned by continued capacity constraints, second-order effects of the Ukraine war and China’s Covid response.

Despite all this US equity markets remained largely unchanged. The S&P 500 gained 0.1% last week.

The Australian market continued its bounce. The S&P/ASX 300 lifted 1.2% last week on the back of a 3.62% increase in resources.

Australian economy

A strong economic recovery has prompted a $150 billion expected improvement in public finances for 2025-26. This is underpinned by lower unemployment benefits and higher income from commodities.

Last week’s Federal budget set aside about 75% for fiscal repair and deployed 25% into new spending initiatives. This comes on top of an already strong economy.

Measures addressing the cost of living were probably the most significant feature, totalling around $10 billion.

This equates to 1% of household income for the next six months and includes:

- Expanded tax offsets worth $420 for about 10 million low or middle income taxpayers, payable in the second half of 2022.

- One-off $250 payment for about 6 million welfare recipients to be paid in April

- 50% reduction in fuel excise for the next six months

Australian retail sales increased 1.8% month-on-month in February — better than expectations of 0.9%.

Sales now are only 0.7% below the pre-Omicron peak in November. NSW did best with 3.6% growth and WA was the laggard at -2.9%. Fashion and eating out dominated with about 15% growth.

Statistics released during the week indicate housing credit growth continues to accelerate to a post-GFC high, while residential approvals have rebounded strongly from a Covid-induced delay.

It is also worth noting that the Budget expanded the First Home Loan scheme. Property prices have rolled over modestly.

Business credit growth is also strong, running at 10% year-on-year. This is also a post-GFC high.

Other data showed household wealth was growing as quickly as ever.

Pendal Focus Australian Share Fund

Now rated at the highest level by Lonsec, Morningstar and Zenith

On the jobs front, vacancies are up 47% year-on-year to a record high of 424,000.

The ratio of job vacancies to unemployed persons has also spiked to a record high 75%.

Normally for every job vacancy there are three-to-four unemployed people available. Now there are only about 1.25.

The transmission of this feature of the current cycle into wage growth continues to be very muted. But we are keeping an eye on negotiations surrounding minimum wages.

Australian businesses are still reporting that the tight labour market is a key constraining factor in their operations.

US economy

In the US 431,000 new jobs were added in March based on payroll data.

This was below expectations, though the January and February figures were revised up 95,000.

This marks the 11th consecutive month of job gains above 400k — the longest stretch since data was first recorded.

The participation rate also climbed 0.2% to 62.4% — compared to a pandemic trough of 60.2% in April 2020. There is evidence that women and retirees continue to return to the workforce.

The unemployment rate fell to 3.6%, one of the lowest on record.

Average hourly earnings rose 0.4%, after rising only 0.1% in February. The annual growth rate remains high at 5.6%, but all eyes will be on April to see if the trend of moderation continues.

Core PCE inflation rose 0.35% month-on-month in February and is running at 5.4% year-on-year versus 5.2% year-on-year in January. This was in line with consensus and is the lowest monthly gain since September 2021.

The breadth measures moderated substantially in contrast to the CPI data, due to different index constructs. Specifically the PCE has a higher weighting to healthcare and a lower weighting to petrol and housing which results in lower overall readings of PCE versus the CPI.

Indicators of manufacturer and retailer pricing power remain at extremely high levels. It is unlikely that inflation can be slowed materially until this recedes. At this point there is little evidence of demand destruction caused by rising prices.

The Dallas Fed’s Exuberance indicator is providing a different perspective on the state of the US housing market.

While materially lower than pre-GFC levels, it still shows just how strong the environment has been compared to any other era going back to 1981.

The move in the mortgage rate is rapidly impacting equity values in the space, though current activity levels remain very robust.

Europe and China economies

Surveys of economic activity in the Eurozone and China point to significantly slower activity.

The Ukraine war and higher commodity prices are dragging on Europe, while Beijing’s zero-Covid policy is seeing further shutdowns in China.

We expect the economies of the EU and the US to begin to diverge materially from here, given the much lower exposure of the US economy to these headwinds.

Sustainable and

Responsible Investments

Fund Manager of the Year

About Crispin Murray and Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia. Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.