A quick investor’s guide to this week’s economic events with portfolio manager TIM HEXT from Pendal’s Income and Fixed Interest team

THE main event for Australian bond markets this week was Wednesday’s release of the Wage Price Index (WPI) for the September quarter.

This number has gained importance with Dr Lowe’s strong view that a sustainable inflation rate at the RBA target (2.5%) is highly unlikely without wage growth comfortably over 3%.

Effectively wages have become a hurdle to cash rate hikes.

So who won this week’s battle between the RBA (no hikes in 2022) and the market (75 basis point of hikes in 2022)?

Well it was a rare recent victory for the RBA.

Inflation prints of late have left the RBA shaky. But the latest wages number fitted the RBA narrative and the market cut expectations from 75 to 60 basis point of hikes.

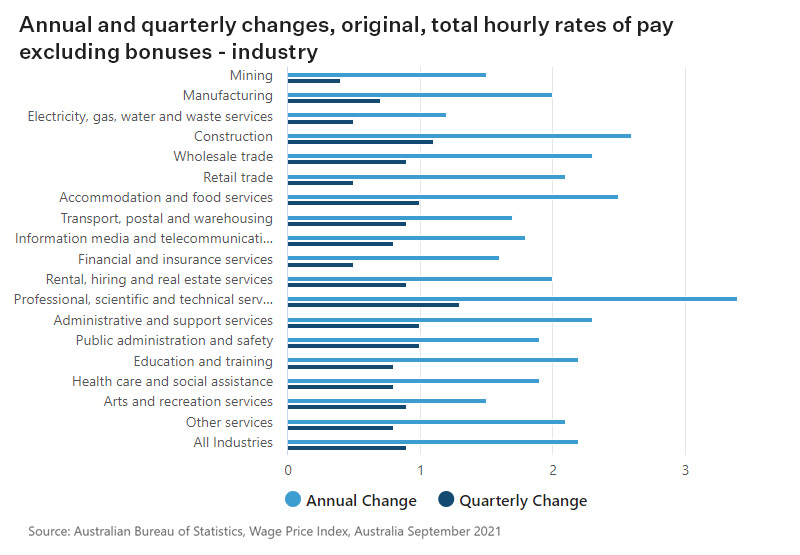

The WPI showed wages growth of 0.6% for the quarter and 2.2% for the year. Reports of labour shortages and accelerating wage growth are yet to show through in a meaningful way.

As you can see below, only one of 18 industries measured was over 3% (Professional, Scientific and Technical Services at 3.4%) and only another two above 2.5% (Construction at 2.6% and Accommodation and Food Services at 2.5%).

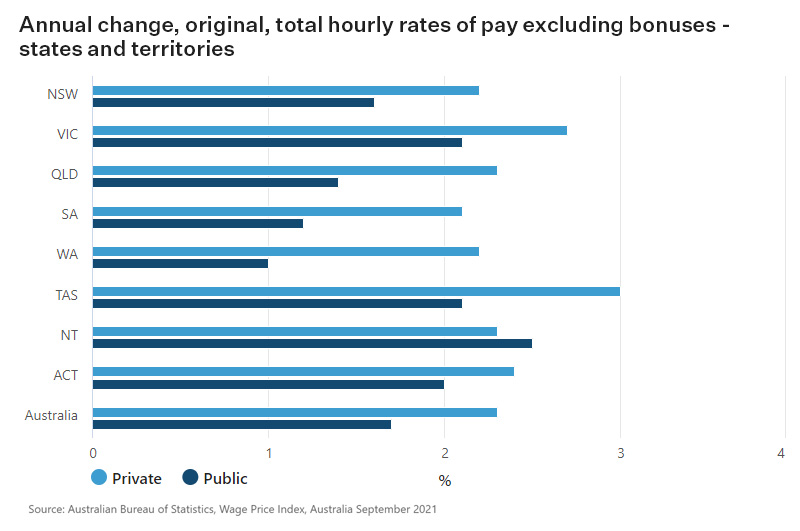

Data by state was also surprising, as you can see below.

You’d think Western Australia — with a booming economy, closed borders and unemployment at 3.9% — would be seeing massive pressure on wages. Apparently not with 2.2% wages growth. Only Tasmania is nearing 3%.

Some of this is due to the inertia of our wage arrangements. Many awards are only negotiated every three years.

Recent awards seem to be targeting 3% and successfully getting it.

Unions know for the first time in a while they hold the better cards. Many are now saying 3% is the minimum they expect. They have the RBA in their camp.

Rather predictably employers are pushing back and asking for quicker border re-openings to give them an increased pool of labour.

Recent reporting seasons suggest most larger companies are able to pass on good times to their workers, even if not willingly.

Public sector wages have been a handbrake, but most states are now back to the 2.5% level of the last decade.

The federal government has moved from the 2% that Abbott brought in, back to matching the private sector.

Find out about

Pendal’s Income and Fixed Interest funds

Where to from here?

Everyone’s in fierce agreement that wages are going up — but by how much and when?

This is crucial for the interest rate outlook. Given the WPI is an average, to hit 3.5% wage growth you need a lot of 4-to-5% outcomes to counter the many stuck at zero (hello finance) and 2.5%.

There have been isolated cases of 5% or 10% rises in areas such as or Accounting and these could well spread further.

But until we see large-scale awards going through at 4% or 5% — or a similar minimum wage outcome — wages well above 3% seem unlikely.

Maybe it’s a 2023 outcome. I suspect we will get there, but for now Dr Lowe looks to be correct in his patience.

Since wages are the ultimate lagging indicator, markets will not share that patience.

Our portfolios have covered short-duration positions. Depending on levels we will likely wait until early next year before re-establishing.

The two months of upcoming radio silence from the RBA and the lack of domestic inflation data until late January means we will be buffeted by offshore markets.

Steep curves though mean it is costly to sit in cash through the summer.

About Tim Hext and Pendal’s Income & Fixed Interest boutique

Tim Hext is a Pendal portfolio manager and head of government bond strategies in our Income and Fixed Interest team.

Tim has extensive experience in banking, financial markets and funding including senior positions with NSW Treasury Corporation (TCorp), Westpac Treasury, Commonwealth Bank of Australia, Deutsche Bank, Bain & Co and Swiss Bank Corporation.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia.

Find out more about Pendal’s fixed interest strategies here

About Pendal

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

In 2023, Pendal became part of Perpetual Limited (ASX:PPT), bringing together two of Australia’s most respected active asset management brands to create a global leader in multi-boutique asset management with autonomous, world-class investment capabilities and a growing leadership position in ESG.

Two events next week will shed light on whether dovish or hawkish monetary policy settings are likely in the short term. TIM HEXT explains

ON MY desk I keep a list of doves and hawks in the US Federal Open Market Committee — the group that makes monetary policy decisions for the Federal Reserve.

This helps when the 12 voting members — who meet eight times a year on proposed changes to near-term monetary policy — issue comments about their latest decision.

Australia doesn’t have monetary policy “voters” as such.

The RBA bureaucrats present their recommendations to the board. What happens next is top secret — though a source once told me there’s only been one occasion the board has begged to differ.

Which system works best is up for debate. I tend to side with the RBA and the view that too much transparency in decisions can confuse and backfire.

Nevertheless the RBA now provides comprehensive minutes of its meetings — even if they are more RBA staff comments than actual minutes.

Why is this important?

Find out about

Pendal’s Income and Fixed Interest funds

There are two major upcoming events that bear close watching around this.

Firstly, next week Joe Biden will announce the new Fed Reserve Chair.

Jerome Powell is still favourite to be reappointed but if betting agencies are to be believed Lael Brainard — an economist who’s been on the Fed’s board of governors since 2014 — has a decent chance.

Both are considered centrist on the spectrum. But the prospect of Brainard alongside dovish US treasury secretary Janet Yellen is seen as a nod to a more progressive stance in fiscal and monetary policy.

Markets would likely view it as more dovish in the medium to long term even if near term a change of guard might rattle a few.

Australian wages data

The second event to watch for is next week’s release of Australia wages numbers on Thursday.

RBA governor Phil Lowe’s current “dovish” stance on inflation is based on the strong view that you need significantly higher wage growth (at least 3% but likely more) if inflation is to sustain a 2.5% level.

The new reactionary RBA is happy to wait and see.

As Dr Lowe said in a speech this week, Australia’s wage system is always slow to move given the award structure.

Getting back to 2.5% wage growth should be easy since even the public sector — around 20% of workers — has now moved back to 2.5% targets. However he thinks a move above 3% is unlikely till late 2023.

Therefore debate will continue on whether central banks are being too slow to tighten.

Bond markets for now believe they will move quicker than their words suggest but few are predicting a major policy error.

Bonds are settling down after a torrid October.

Markets have already priced decent hikes.

For our upcoming Australian Quarterly report I am writing a piece on what would be needed to push bond rates up significantly from here in the medium term.

Stay tuned.

About Tim Hext and Pendal’s Income & Fixed Interest boutique

Tim Hext is a Pendal portfolio manager and head of government bond strategies in our Income and Fixed Interest team.

Tim has extensive experience in banking, financial markets and funding including senior positions with NSW Treasury Corporation (TCorp), Westpac Treasury, Commonwealth Bank of Australia, Deutsche Bank, Bain & Co and Swiss Bank Corporation.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia.

Find out more about Pendal’s fixed interest strategies here

About Pendal

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

In 2023, Pendal became part of Perpetual Limited (ASX:PPT), bringing together two of Australia’s most respected active asset management brands to create a global leader in multi-boutique asset management with autonomous, world-class investment capabilities and a growing leadership position in ESG.

Here are the main factors driving the ASX this week according to portfolio manager Jim Taylor. Reported by portfolio specialist Chris Adams

THE market continues to question the notion of “transitory” price pressures.

But it’s remarkable how quickly equity markets have rebounded from recent shocks around inflation.

Stronger-than-anticipated US inflation data last week drove market volatility and a rare down-week for US equities. The S&P/ASX 300 lost 0.04% and the S&P 500 was off 0.27%.

There was also some movement in China. Beijing may be looking to ease pressure on the property sector, which prompted a rebound in the iron ore space.

The market remains focused on the risk of China over-tightening monetary, fiscal and regulatory policy settings, so signals that may mitigate this risk have been well received.

The Chinese Communist Party’s sixth plenum last week appears to have paved the way for indefinite leadership by Xi Jinping.

Covid and vaccines

We are seeing a sharp rise in case numbers in Germany. But as in other similar waves, hospitalisations so far remain under control.

Other European counties are also seeing an increase in cases. Denmark, Austria and the Netherlands are looking at reintroducing some mobility restrictions in response.

Otherwise there was little new to note last week.

Macro and policy

US

However you want to slice and dice the inflation data, the key takeaway is that we are looking at 30-year highs.

US CPI grew 0.9% month-on-month — versus 0.6% consensus expectations — and is running at 6.2% year-on-year.

The core data (ex food and energy) rose 0.6% month-on-month versus 0.4% expected. It is running at 4.6% year-on-year.

A rebound in Covid-affected sectors such as auto and hotel prices helped lift both the headline and core readings, but the breadth of excess inflation pressures continued to increase.

Services inflation will be keenly watched as the US economy re-opens. So far it remains in its 10-year band, but has experienced strong recent momentum.

Core CPI will peak at 6.9% in March 2022 according to consensus expectation at this point. This leaves plenty of scope for the market to continue testing the Fed’s “transitory” line in coming months.

Australia

In Australia, employment declined 46.3k in October while the unemployment rate rose 60bp to 5.2%. This was weaker than expected, but the outcome largely reflected measurement issues related to recent lockdowns.

Elsewhere a strong rebound in company forward orders augers well for growth as we emerge from lockdowns.

China

The slowdown in credit may have bottomed in China. October is showing credit growth, potentially improving confidence for the rest of the year and into 2022.

After recent sharpening of concerns over property there are reports that the People’s Bank of China may introduce several measures to ease pressure on the sector. These include:

- Excluding merger and acquisition loans from the “Three Red Lines” that govern leverage in the property sector, allowing companies to acquire assets from stressed firms such as Evergrande

- Easing restrictions on development loans, which should reduce cash flow pressure on developers

- Extending existing bank loans

Elsewhere, approval of Xi’s doctrine on Chinese Communist Party history — the first in 40 years — at the sixth plenum seems to set the stage for Xi to retain power indefinitely.

Markets

Australian ten-year government bond yields largely held on their 30bp rally from the previous week.

The US equivalent yields rose 11bps to 1.56% on the inflation data, but remain well below recent highs.

Sustainable and

Responsible Investments

Fund Manager of the Year

The inflation print saw the gold price gain 2.8%.

News of potentially looser policy in China prompted good gains among commodity stocks, though the prices of iron ore (-4.9%) and copper (+2.4%) remained more subdued.

It was a disappointing season for the banks in the sense that all missed consensus pre-provision profit expectations.

ANZ (ANZ) slightly missed due to costs and NAB missed by 2% given weak markets. Westpac (WBC) missed by 17% given a sharp hit to net interest margins (NIMs) and higher costs.

Key themes across the results included:

- Mortgage NIMs remain under pressure from competition and changes in product mix, as highlighted by WBC. A focus on price-driven strategies via third-party distribution has led to profitless growth. Business banking NIMs appear to have held up better. The tailwind from lower deposits and funding appears to have largely played out.

- Credit growth is strengthening. All banks (ex ANZ) are enjoying the housing boom, though this should peak in coming months. NAB and CBA are starting to see a recovery in business lending which is a very encouraging sign. Institutional activity is increasing, while NZ credit keeps expanding. Growth is becoming broader based.

- The markets and trading-based divisions have been weaker, outside of Australian and New Zealand.

- All banks recommitted to their cost-out programs, however the market remains very sceptical on success here.

- Asset quality was very benign with every bank reporting negative credit charges.

- All banks beat expectations in terms of capital positions, reporting strong balance sheets.

About Jim Taylor and Pendal Focus Australian Share Fund

Drawing on more than 25 years of experience investing in top-performing Australian companies and a background in accounting, Jim manages our Long/Short Fund and co-manages our Imputation Fund. He is a Chartered Accountant with membership of the Australian Institute of Chartered Accountants.

Pendal Focus Australian Share Fund is managed by Crispin Murray. The fund has beaten its benchmark in 12 years of its 16-year history (after fees), across a range of market conditions. Find out more about Pendal Focus Australian Share Fund here.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

A weekly income and fixed interest snapshot from Pendal assistant portfolio manager ANNA HONG

FOR ALMOST two years economic data points have been accompanied with lockdown disclaimers — pre-lockdown, post-lockdown, back into lockdown.

Hopefully 2022 brings more incisive data as high vaccination rates put the lockdowns behind us.

The headline unemployment numbers released yesterday briefly shocked the market.

Positivity from the end of lockdowns was briefly snuffed out as the Australian unemployment rate jumped from 4.6% to 5.2% — much higher than the market consensus.

That was until we got to the fine print at the end.

The release was backward looking and reflected job numbers from Sep 26 to Oct 9.

Find out about

Pendal’s Income and Fixed Interest funds

That’s before NSW came out of lockdown — much less Victoria — which meant unemployment numbers in VIC and NSW dragged the national number higher.

Moreover, most borders were still shut as state policies outweigh federal.

That meant tourism-related industries in Queensland were affected, while states less reliant on tourism such as WA and NT saw an improvement in unemployment.

So the glass is half full, given those were essentially lockdown unemployment numbers.

Furthermore, the consumer sentiment numbers around job security fears are at their lowest in more than seven years.

That’s evidenced by the labour turnover in NSW, which showed signs of better health as many workers switched jobs for better opportunities and better pay.

The economic outlook gets better as we add improving consumer spending intentions to the mix.

Higher spending in good, services and dwellings will help the states’ bottom line with stamp duty receipts and GST handouts from the federal government.

Market moves

Globally, most CPI numbers printed higher than consensus.

Yields rose due to global sentiment around inflation.

Australia’s unemployment number miss did not shift the yields significantly.

Market Implications

Short-end cash maintains its slight curve with six months BBSW still holding its ground above the RBA cash rate of 10bps.

Semi-government spreads have widened with issuances now coming through at close to its historical spread of +50bps to commonwealth government bonds.

The recently tendered TCV 2034 is now trading at +48bps to CGL. As semi spreads normalise the accruals can once again provide a healthy income to investors.

Additionally, the improving Australian economy will result in higher tax receipts.

Potentially that will improve the states’ finances and be supportive of semis on reduced supply.

About Anna Hong and Pendal’s Income and Fixed Interest team

Anna Hong is an assistant portfolio manager with Pendal’s Income and Fixed Interest team.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia. In 2020 the team won the Australian Fixed Interest category in the Zenith awards.

With the goal of building the most defensive line of funds in Australia, the team oversees A$22 billion invested across income, composite, pure alpha, global and Australian government strategies.

Find out more about Pendal’s fixed interest strategies here

About Pendal Group

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Renewable energy and battery-powered cars grab attention in the climate change debate. But tougher, “hard-to-abate” sectors may be more important for sustainable investors. Pendal’s RAJINDER SINGH explains

- Challenging or “hard-to-abate” sectors offer opportunity for sustainable investors

- These include agriculture, airlines, steel and cement

- Climate change “not just about fossil fuels”

YOU’VE probaby heard sustainable investment experts describe some industries as “hard to abate”.

Abatement means reducing the intensity of something unpleasant.

Climate-change experts refer to sectors such as cement, steel, air travel and agriculture as “hard to abate” because they lack obvious, cost-effective carbon-reduction solutions.

That’s a problem since these sectors make up more than a third of the world’s carbon emissions. Finding solutions in “hard-to-abate” sectors is critical to meeting net zero commitments — which makes them interesting to investors.

The fact they are largely overlooked in government policy and public debate may indicate there are opportunities for investors seeking to help create a better planet.

“Tackling climate change is not just about fossil fuels,” says Rajinder Singh, who manages several Pendal sustainable funds.

“There are some really difficult things we need to solve — things like airlines, cement, steel, agriculture and a wide range of industrial processes are significant carbon emitters.

“They are going to exist in 2050 and beyond and they are going to take time to solve.”

Singh says solutions for some of the trickiest questions about greenhouse gas emissions in these sectors are only beginning to emerge and sustainable investment success requires working with companies to solve these hard-to-abate sectors.

Find out about Pendal Sustainable Australian Share Fund

“It demonstrates the value of active ownership,” says Singh. Unlike most ETF or passive fund managers, active investment managers such as Pendal are run by managers who engage with companies to influence positive change.

“As a sustainable investor, you can’t just buy an ETF that owns all the good stocks and excludes the bad stocks. You have to work with companies and help with the transition.”

Solving the air travel problem

Airlines are one of the industries at the early stages of solving for net zero.

Batteries are unlikely to provide a solution for long-haul travel because of their weight, though short-haul electric airplane trips are feasible.

As a result, airlines are experimenting with biofuels — jet fuel made from renewable sources like plants or waste.

“But it has to be done sustainably,” says Singh. “You can’t divert agricultural products that would ordinarily be used for food,” says Singh.

In the meantime, the opportunity for airlines is in improving fuel efficiency by optimising routes and investing in more efficient planes.

Green cement

Another hard-to-abate sector that investors are seeking answers for is the cement used to make concrete.

“It’s in the basic chemistry — heating the raw materials releases CO2. That’s how concrete has been made for thousands of years,” says Singh.

Investments in technology solutions are showing promise. Trials are underway to capture carbon emissions in the concrete itself, trapping it and preventing it entering the atmosphere.

Fly ash — ironically a waste product from burning coal — is used to replace cement in concrete, dramatically reducing carbon emissions.

Other hard-to-abate areas include industrial processes that require high heat such as steel production or making bricks in a kiln.

Hydrogen offers a potential solution here although there is a long road of capital investment and trials ahead.

Sustainable and

Responsible Investments

Fund Manager of the Year

Risks and opportunities

These are important issues for investors to understand, says Singh.

“There is a cost in terms of capital that needs to be invested — over and above the regular business-as-usual investment.

“Steel companies need to spend tens or hundreds of millions of dollars investigating technologies and implementing in existing operations.

“If they’re going to spend shareholders money, we want to have a return based on that.

“Some of that return may be a green premium — but it may also simply be that you need to spend the money just to stay in business.”

Singh says investors seeking to create a sustainable investment portfolio — and genuinely impact the future — need to stay close to companies at the cutting edge of change in these hard-to-abate areas and resist the temptation to just divest.

“How can you own a mining company in a sustainable fund? Well, if you think about what a sustainable company fund is trying to do, it is investing in a society that is better.

“If you want to have electric vehicles, solar panels and a green electricity grid, you’re going to need metals like steel, copper and lithium.

“So, you want to invest in those companies that are providing those materials in the most sustainable way — what are the emissions, but also, what does workplace health and safety look like and how are they treating indigenous land holders?

“Mining is not bad. We just want sustainable mining.”

About Rajinder Singh and Pendal’s responsible investing strategies

Rajinder is a portfolio manager with Pendal’s Australian equities team. He has more than 18 years of experience in Australian equities.

Rajinder manages Pendal sustainable and ethical funds including Pendal Sustainable Australian Share Fund.

Pendal offers a range of responsible investing strategies including:

- Pendal Sustainable Australian Share Fund

- Crispin Murray’s Pendal Horizon Fund

- Pendal Sustainable Australian Fixed Interest Fund

- Pendal Sustainable Balanced Fund

- Regnan Credit Impact Trust

- Regnan Global Equity Impact Solutions Fund

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Responsible investing leader Regnan is part of Pendal Group.

The federal government estimates $20 billion of funding is needed to hit net zero emissions by 2050. But it could be triple. TIM HEXT explains what that means for investors

You probably don’t spend much time pondering our federal and state government arrangements.

But after running the NSW debt program for ten years as a general manager of TCorp (NSW Treasury Corporation) — which involved regularly explaining the arrangements to offshore investors — I know state governments are more important than federal governments.

The only reason people gathered on the sheep paddocks of southern NSW in the first place was to discuss defence and foreign affairs.

Covid has demonstrated the importance of the states to the population. In day-to-day life, Australians now should well understand that premiers are more important than prime ministers.

Therefore it’s interesting to watch Prime Minister Morrison trying to reclaim ascendency in recent times, as we move towards a federal election due by May.

Whether it be vaccine rollouts, new infrastructure and now climate policy, the prime minister’s main job seems to be repackaging state initiatives as his own.

That’s nothing new. But it appears people are now onto it — and the spin doctors are having to work harder.

Why does this matter for investors?

Well, the states are like you and me. They have to either earn or borrow money to spend it. They must live within their means.

On the other hand, the federal government — via the Reserve bank — has the ability to create money. They don’t need to borrow or earn it. The only constraint on federal spending is inflation.

Pendal Sustainable Australian Fixed Interest Fund

An Aussie bond fund that aims to outperform its benchmark while targeting environmental and social outcomes via a portion of its holdings.

Central bankers and economists used to push back on this. But after the past two years the cat is out of the bag.

Now the challenge is how to finance all the required climate initiatives.

Federal/state fiscal arrangements are complex — and in the relatively new area of climate policy thay are largely untested.

The federal government’s “Technology Investment Roadmap” estimates $20 billion of funding is needed to hit net zero emissions by 2050.

The cost may be closer to $60 billion based on estimates from countries that are less optimistic on the whole technology vibe.

I suspect much of this will come via guarantees of private projects rather than direct funding.

This is the European model and leads the world. Projects would need backing from the federal government, though, since state funding is already stretched.

Let’s hope federal and state governments can get back on the same page and work out a joint approach to climate policy.

States are already leading the execution, but the federal government will need to step up and do the heavy lifting on financing. (They already have the Australian Renewable Energy Agency and the Clean Energy Finance Corporation in place.)

Otherwise state credit ratings will deteriorate and the federal government will end up footing the bill anyway.

This is an increasing focus for us when assessing the credit ratings of semi governments and the positioning in our government bond portfolios.

We have also recently finished our wider ESG assessment of the states and will publish a piece on this in our upcoming Australian Quarterly.

About Tim Hext and Pendal’s Income & Fixed Interest boutique

Tim Hext is a Pendal portfolio manager and head of government bond strategies in our Income and Fixed Interest team.

Tim has extensive experience in banking, financial markets and funding including senior positions with NSW Treasury Corporation (TCorp), Westpac Treasury, Commonwealth Bank of Australia, Deutsche Bank, Bain & Co and Swiss Bank Corporation.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia.

Find out more about Pendal’s fixed interest strategies here

About Pendal

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

In 2023, Pendal became part of Perpetual Limited (ASX:PPT), bringing together two of Australia’s most respected active asset management brands to create a global leader in multi-boutique asset management with autonomous, world-class investment capabilities and a growing leadership position in ESG.

Regnan Global Equity Impact Solutions Fund – Class R (APIR: PDL4608AU, ARSN: 645 981 853)

On 9 August 2021, the designation of this class of units was changed from ‘Class A’ to ‘Class R’. The name of the Fund did not change and there were no changes to the terms of the class or your rights as an investor in the class.

What do you need to do?

No action is required. You will be able to continue to invest or withdraw from the Fund.

An updated Product Disclosure Statement (PDS) was issued on 9 August 2021 and made available on www.pendalgroup.com.

Pendal Concentrated Global Share Fund Hedged – Class R (APIR: RFA0031AU, ARSN: 098 376 151)

On 23 September 2021, the existing units of the Pendal Concentrated Global Share Fund Hedged (Fund) were reclassified as ‘Pendal Concentrated Global Share Fund Hedged – Class R’. The name of the Fund did not change and there were no changes to the terms of the class or your rights as an investor.

What do you need to do?

No action is required. You will be able to continue to invest or withdraw from the Fund.

An updated Product Disclosure Statement (PDS) was issued on 23 September 2021 and made available on www.pendalgroup.com.

Here are the main factors driving the ASX this week according to our head of equities Crispin Murray. Reported by portfolio specialist Chris Adams

INFLATION concerns eased last week and there were implications for central bank messaging.

There had been concern that higher inflation would prompt central banks to shift messaging more aggressively towards potential rate hikes.

That seems to be allayed for now.

This came via statements from central banks, a US labour report that indicated a return of supply, and the firming chances of Jay Powell being appointed for a second term at the Fed.

Bond yields fell in response. In combination with a decent US earnings season and good news on Pfizer’s antiviral pill, the S&P 500 rose 2.03% and the S&P/ASX 300 gained 1.91%.

US equities have had a strong run, up 9.17% for the quarter to date.

Australian equities have lagged, up only 2.02%. This reflects our skew to resources and the need to digest new capital issuance.

While they might pause for breath in the near term, equity markets should remain sell-supported into the year’s end.

Central banks outlook

Various statements from central banks went a long way to calming the market’s concerns about how quickly rates will need to rise.

The Fed announced it would begin tapering asset purchases by US$15 billion per month, implying that Quantitative easing would end in mid-June 2022.

This is in-line with expectations and was a dovish statement given speculation that the rate might have been accelerated.

Chair Powell was at pains to talk down inflationary fears. He noted that “transitory” did not necessarily mean “short-lived” — rather they were not expecting “permanently higher inflation”, ie a wage-price spiral. They did give themselves room to adjust their plans.

Pendal Focus Australian Share Fund

Now rated at the highest level by Lonsec, Morningstar and Zenith

A strong showing for the Republicans in gubernatorial elections in Virginia and New Jersey is seen as beneficial for Powell’s chances of securing a second term as Fed Chair.

The view is that the Biden Administration will not want to appoint a potentially less-predictable candidate to the Fed at this point.

The Bank of England caught the market on the hop when it kept rates stable. A 15bp rise had been signalled and widely expected. The BoE pushed back against the market projection for rate increases — citing signs of slowing economic momentum — and made the case for transitory inflation.

The market is still pricing in a 15bp move for December and is split as to whether the following one will be February or May.

So at this point major central banks are signalling a lagged response to rising inflationary pressure.

This also flowed through into a lower trajectory for projected ECB rate rises.

The RBA also adjusted its messaging.

The three-year yield target was removed as expected. The possibility of a rate rise in 2023 was also mentioned for the first time.

The Reserve noted that the labour market was stronger than expected, but border re-opening should provide additional supply.

This remains to be seen.

The market is still wary of inflationary pressures, particularly in housing. Nevertheless, there was relief that the RBA didn’t take a dogmatic stance towards the target for a first hike in 2024.

Economic outlook

The dominant narrative at this point is that global growth is accelerating following a hit from the Delta strain and disrupted supply chains.

Bottlenecks persist but there are signs the situation is improving.

This was reinforced by US payroll data, which showed 531,000 jobs were added in October, versus 450,000 expected.

The previous month was also revised upwards by 235,000 new jobs. The private sector added 604,000 new jobs, which was good, while the government sector shed 73,000 jobs.

Sustainable and

Responsible Investments

Fund Manager of the Year

The underemployment rate fell from 4.8% to 4.6%. Wages grow rose 0.4% to 4.9% year-on-year.

The household survey showed the labour force rose 104,000 after falling 183,000 in September.

However the participation rate remain a key variable in the outlook for wage inflation. It was 63% pre-pandemic, fell to 60% during the economic downturn and is now steady at 61.6%.

The St Louis Federal Reserve estimates there have been more than 3 million retirements in excess of what would normally be expected. This represents more than half the 5 million people who left the workforce since the beginning of the pandemic.

The resulting tight labour market can be seen in the ratio of employed workers to each new job opening, which is at its lowest point since measurement began in 2001.

So the outlook for inflation and bond yields — and the effect on growth stock premiums in the equity market — will be very tied to wage growth in the US.

This continues to move higher and is probably the key macro factor to watch in the coming year.

That said, it is worth noting that given the high rates of inflation, current real wage growth is negative.

This helps explain a backlash against the Democrats last week and a rising incidence of industrial action in the US.

Covid and vaccines

New daily cases in the US continue to flatten.

One factor to watch here will be the combination of waning immunity from vaccines and the onset of colder weather. We are seeing the number of people getting a third jab picking up quickly.

We are also watching the situation in China, which is going it alone in pursuit of zero-Covid. This could see an impact on economic growth — and potential demand for commodities.

The more important news was that Pfizer published data on its anti-viral pill, which so far in trials is indicating an 85% reduction in severe cases.

Markets

The US equity market may be a touch over-bought in the near term. But there are positive signals for the outlook into the year’s end:

- Bond yields look to have peaked near term as supply chain issues improve

- Market breadth is improving in the US, with the small cap Russell 2000 breaking higher after an eight-month consolidation and outperforming the broader market

- We are seeing US consumer discretionary stocks break out versus consumer staples. This is a signal of consumer confidence, though we are yet to see this in Australia.

In the US, 89% of companies have reported quarterly earnings.

Market eps is up 38% year-on-year. While a deceleration from previous quarters, this is well ahead of the +27% consensus expectation.

About 60% of companies have beaten expectations by a standard deviation or more, versus a long-term average of 49%.

Given the headwinds of supply chain and Delta this is a very good outcome.

The S&P/ASX 300 did well last week despite a drag from resources, which is the now the worst-performing area for the year to date.

About Crispin Murray and Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia. Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Find out more about Pendal Focus Australian Share Fund here.

A weekly income and fixed interest snapshot from Pendal assistant portfolio manager ANNA HONG

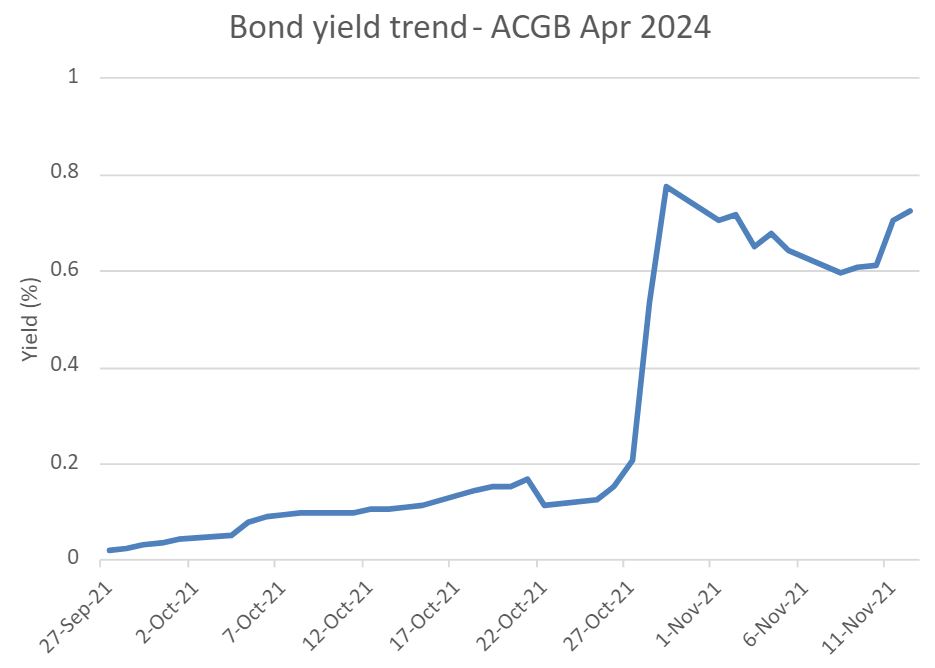

It’s been a topsy-turvy week.

Monday started with the after-shocks of the latest Australian CPI print which featured core inflation numbers that convincingly beat forecasts.

The lead-up to Tuesday’s Melbourne Cup race at 3pm was unusually nerve-wracking as many in the markets waited for Governor Lowe’s statement at 2.30pm.

It marked the continuing removal of extraordinary monetary policy in Australia. As expected, the RBA announced the termination of Yield Curve Control.

Finally we had Friday’s release of the Statement of Monetary Policy (SoMP).

The RBA pushed back against market sentiment, which is pricing in a 2022 rate hike.

Find out about

Pendal’s Income and Fixed Interest funds

The RBA maintains its central scenario of a 2024 rate hike, though it will no longer defend the 0.10% YCC target for April 2024.

The key drivers of the scenario are unemployment and inflation. Unemployment was only marginally revised lower since the forecast scenario expects a gradual tightening of the labour market.

Inflation was revised upwards. But the inflation forecast has largely discounted surges experienced in other countries. The RBA says the impact of supply chain disruptions is less evident in Australian CPI.

But there is strong evidence to suggest otherwise.

Unemployment — one of the key lynchpins — has rebounded remarkably.

Businesses regained confidence and started hiring in late September, readying themselves for the end of lockdown.

In the foreseeable future, laggard industries such as accommodation, air & transport services and construction will very likely pick up as the economy continues to re-open.

Australian consumers, flushed with cash, are on the same page as businesses.

The major banks are reporting that internal high-frequency consumer spending data demonstrates a strong recovery in consumer spending.

This may continue as disposable income grows and savings are unwound.

Market Implications

Even before the SoMP was released, the impact on housing credit could already be felt.

Westpac led the charge, raising fixed rate home loans by between 10 basis points (0.10%) and 21 basis points (0.21%). CBA followed with rate hikes to its home loan products, shortly after SoMP.

Before the SoMP, financial markets fully priced in a hike by July 2022 — with almost four increases priced by the end of 2022.

Markets eased off post-SoMP — but remained sceptical. Markets held firm to their pricing in of 2022 rate hikes.

Time will tell which side is right.

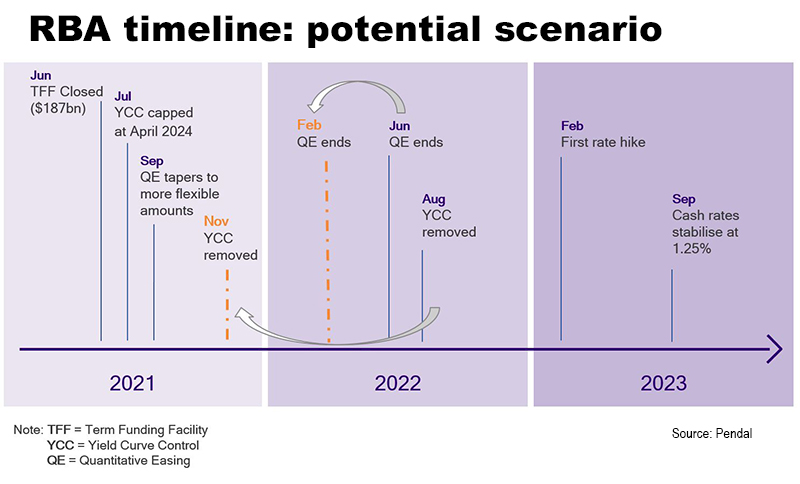

Here is Pendal’s time-line of potential RBA moves.

This timeline was first created in May. The arrows represent changes after recent RBA actions.

About Anna Hong and Pendal’s Income and Fixed Interest team

Anna Hong is an assistant portfolio manager with Pendal’s Income and Fixed Interest team.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia. In 2020 the team won the Australian Fixed Interest category in the Zenith awards.

With the goal of building the most defensive line of funds in Australia, the team oversees A$22 billion invested across income, composite, pure alpha, global and Australian government strategies.

Find out more about Pendal’s fixed interest strategies here

About Pendal Group

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.