Despite noise about another inflation surge and higher rates, central banks look to have price rises well under control, argues Pendal’s OLIVER GE

- Fears of 70s inflation rerun unfounded

- Why bonds, why now? Pendal’s income and fixed interest experts explain

- Find out about Pendal fixed interest capabilities

FOR or all the recent headlines about rising costs, oil prices and interest rates, there’s little to suggest inflation is anything other than under central bank control, argues Pendal’s Oliver Ge.

US inflation numbers came in higher than expected for August, marking the first acceleration in price rises since February.

The data sparked a number of news reports extrapolating the monthly figures to warn of a second wave of inflation and a new round of interest rate rises.

But a closer look reveals that the global economy is a long way from the narrative the news media are pushing, says Ge, a portfolio manager with Pendal’s Income and Fixed Interest team.

“This kind of stuff is going to get a lot of clicks.

“Thirteen consecutive months of disinflation in the US and now we’ve had the first tick up, and somehow the media is extrapolating that the Federal Reserve is on the case and it’s all going to end in the crapper.”

Ignoring noise created by business media is an important lesson for investors, says Ge.

“There’s a lot of commentary on a possible ’70s-style, second wave of inflation. And how if that were to happen, central banks would need to react.

“But I don’t believe we’re going down that path. We’re not even close to a rerun of the 70s.”

The dual inflation shocks of the 70s and 80s have gone down in investing folklore as a tumultuous period of skyrocketing prices, spiralling wage rises and damaging unemployment.

“Some people are concluding that we’re on the path to repeat the 70s/80s experience when inflation hit almost 15 per cent in the US.

“But there are a few reasons why we’re not likely to get a re-run of what happened 50 years ago.”

Ge says the 70s crisis was unique and brought about in part because the US economy was running very hot.

“In 1973, the US economy was growing at 7.6 per cent — three times higher than what it is today.

“It also had a highly unionised labour force. And then it got whacked with two major oil shocks.

“The difference is that back then, the US was highly oil dependent, and it also was experiencing a massive devaluation of its currency. Put the two together and it triggered a big wave of inflation.

“At the same time, the US was home to a sizeable manufacturing sector, which was very highly unionised. They had explicit mandates in contracts that matched pay to inflation.”

Find out about

Pendal’s Income and Fixed Interest funds

But he says the environment today is very different.

“The US is no longer energy dependent — in fact it is an exporter of oil. Unionisation is no longer widespread. There are none of the original catalysts that prompted the blowout.”

The central banks also play a different role today, says Ge.

“Central banks today have a very explicit inflation fighting objective — they are not going to suddenly drop rates because inflation is coming down like they did in the 70s.

“They will choose to err on the side of caution. That means we’re going to see an environment where rates are going to be higher for longer.

“The picture I’m painting isn’t sexy — but it’s real. And it should comfort investors.”

About Oliver Ge and Pendal’s Income and Fixed Interest boutique

Oliver Ge is an assistant portfolio manager with Pendal’s Income and Fixed Interest (IFI) team.

Oliver works on developing and running key quantitative investment models, and acting as trading support for the team. Oliver received his Bachelor of Commerce (Finance) from the University of Sydney and is also a CFA Charterholder.

Pendal’s IFI boutique is one of the most experienced and well-regarded fixed income teams in Australia. In 2020 the team won the Australian Fixed Interest category in the Zenith awards.

The invests across income, composite, pure alpha, global and Australian government strategies.

Find out more about Pendal’s fixed interest strategies here

About Pendal Group

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

The risk of recession appears to be sidelined for now, but investors may be overlooking one factor, argues Pendal’s OLIVER GE

- Tightening credit threatens business viability

- Bonds best protection from recession

- Find out about Pendal fixed interest capabilities

A NUMBER of US banks and analysts have walked back their recession predictions in recent weeks.

But there are still worrying signs in the business sector, cautions Pendal’s Oliver Ge.

Much of the discussion about higher interest rates has focused on the impact of bigger mortgage repayments for homeowners.

But tightener credit conditions and stricter collateral requirements for business are likely to have a more significant impact on the economy, argues Ge, an assistant portfolio manager with Pendal’s income and fixed interest team.

“There’s a growing narrative that the economy can navigate through this tightening cycle without derailing growth and causing havoc to the jobs market.

“It can be hard to argue against this. Despite 400 basis points in hikes from the RBA, economic activity remains reasonably robust and domestic employment is incredibly strong.

“But the economic brakes applied via interest rates is very gradual.

“What often gets overlooked is that there is another transmission mechanism — the tightening of lending standards — that carries perhaps more importance to the business cycle.”

As interest rates lift, banks will increase the perceived credit risk of all borrowers. To mitigate these risks they will impose stricter income and collateral requirements on their borrowers.

Small businesses are generally more reliant on bank loans given that they have fewer alternative sources of funding.

“It’s not the cost but access to credit that matters,” says Ge.

“Small business owners rely on a flow of working capital to pay their suppliers and employees. At the moment, the banks are happy to supply that. But should lenders’ outlook on the economy turn, they may have to cut off those lines of credit”.

“That’s when businesses will be forced to pare back on labour and supplies. That spills over into the rest of the ecosystem — that’s when you get that pain.

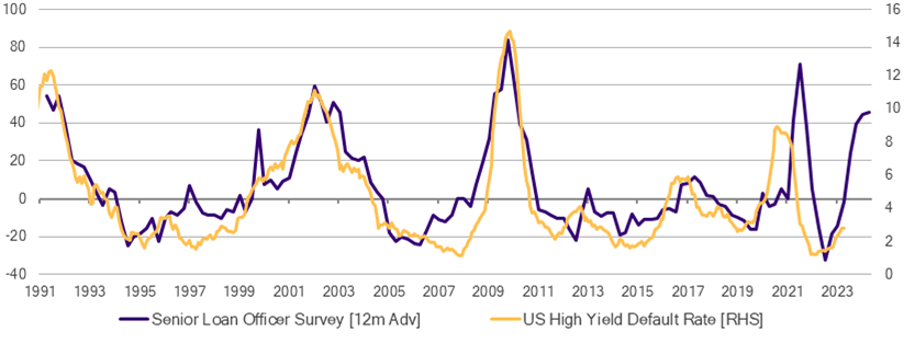

Tighter lending in the US

As you can see below, there’s evidence that banks are already tightening lending in the US, where the Federal Reserve conducts a quarterly survey of the biggest banks to assess lending terms.

“Lending standards have tightened significantly, comparable to historic highs,” says Ge.

“Business cash buffers are running out and you’ll likely see a wave of defaults over the course of the next six-to-nine months.

“Ultimately, that is where we’re headed. But it’s not something people are factoring into their forecasts.”

A tightening of lending standards has real potential to push the global economy into recession, says Ge.

“Whatever happens in the US will filter through to the rest of the world. There’s no way that Australians can somehow insulate themselves.

“At the start of the year, people were tossing up between a soft and hard landing. The hard landing scenario has faded from people’s memories.

“But the prospect of recession is still very much out there.”

Find out about

Pendal’s Income and Fixed Interest funds

About Oliver Ge and Pendal’s Income and Fixed Interest boutique

Oliver Ge is an assistant portfolio manager with Pendal’s Income and Fixed Interest (IFI) team.

Oliver works on developing and running key quantitative investment models, and acting as trading support for the team. Oliver received his Bachelor of Commerce (Finance) from the University of Sydney and is also a CFA Charterholder.

Pendal’s IFI boutique is one of the most experienced and well-regarded fixed income teams in Australia. In 2020 the team won the Australian Fixed Interest category in the Zenith awards.

The invests across income, composite, pure alpha, global and Australian government strategies.

Find out more about Pendal’s fixed interest strategies here

About Pendal Group

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

Pendal Government Bond Fund (APIR: BTA0111AU ARSN: 098011048)

Change in investment return objective from 16 May 2022.

With effect from 16 May 2022, the Fund’s investment objective will change from

“The Fund aims to provide a return (before fees and expenses) that exceeds the Bloomberg AusBond Govt 0+ Yr Index by 1.0% pa over a rolling 3 year period.”

to “The Fund aims to provide a return (before fees and expenses) that exceeds the Bloomberg AusBond Govt 0+ Yr Index over a rolling 3 year period.”

The change to the investment objective is to make the Fund consistent with the majority of our asset class strategies where we reference the outperformance of a benchmark and not a target return. There is no change to the investment strategy or process.

The current yield curve inversion — where short-dated bonds yield more than long-dated bonds — may not mean a recession is imminent, argues Pendal’s OLIVER GE

- Yield curve inversion traditionally predicts recession

- But transitory inflation could be an alternative explanation

- Find out about Pendal fixed interest capabilities

THE prospect of stagflation has been the talk of markets in recent weeks as rising short-term interest rates push the bond yield curve into inversion, flagging a sign of impending recession.

An inverted yield curve — where shorter-dated bonds yield more than longer-dated bonds — is an important indicator for investors.

Longer-dated bonds usually pay higher interest rates to compensate for their increased risk over time. But right now short-term interest rates are moving closer to — and even higher than — long term rates.

That’s important because it’s traditionally a harbinger of recession.

But with a strong global economy, low unemployment and benign equity market conditions, analysts have been looking for an alternative explanation for the inversion other than a surprise descent into stagflation and recession.

Oliver Ge, a portfolio manager with Pendal’s Income and Fixed Interest team, says the yield curve inversion may also be explained by expectations that current inflationary pressures are only short term.

“There are two ways this can be interpreted,” says Ge.

“In one sense you can see it as a sign of recession. But I don’t think that’s the case”.

“Instead, what we’re seeing in the market is that short-dated bond yields are higher because they carry a premium to their longer-dated counterparts to compensate investors for bearing higher near-term inflation risk. That’s what’s driving the inversion”

Stagflation is a worry for markets because it means a toxic combination of rising prices and lower economic growth.

Find out about

Pendal’s Income and Fixed Interest funds

But Ge says the conditions for stagflation are not present in the global economy.

“There’s 1.8 jobs available for every person who wants a job in the US,” he says.

“That’s more jobs per person than there has ever been.

“In Australia, the workforce is in a stronger position than it was pre-pandemic. We’ve recovered all the job losses we had in the pandemic and created more and there are still labour shortages.

“Some say it’s about borders and immigration — but this is a global phenomenon. The overriding theme across the world is employment is fantastic. There are jobs for everyone.”

Ge says in such a strong economic environment, it’s difficult to believe that a few interest rate hikes will stop businesses hiring.

Returning to recession so soon after the global pandemic downturn would also be surprising from an historical view, he says.

“Looking back, you see a recession every eight to 10 years or so. The yield curve is telling us there is a recession around the corner but that’s almost never the case historically.

“Maybe you get a bit of a slowdown, but you don’t get the end of days that some people are calling for.”

About Oliver Ge and Pendal’s Income and Fixed Interest boutique

Oliver Ge is an Assistant Portfolio Manager with Pendal’s Income and Fixed Interest (IFI) team.

Oliver works on developing and running key quantitative investment models, and acting as trading support for the Income & Fixed Interest team. Oliver received his Bachelor of Commerce (Finance) from the University of Sydney and is also a CFA Charterholder.

Pendal’s IFI boutique is one of the most experienced and well-regarded fixed income teams in Australia. In 2020 the team won the Australian Fixed Interest category in the Zenith awards.

The invests across income, composite, pure alpha, global and Australian government strategies.

Find out more about Pendal’s fixed interest strategies here

About Pendal Group

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Bonds have the potential to provide a positive investment return even during central bank rate-hiking cycles. Pendal’s OLIVER GE explains how

RATES go up, bonds go down. It’s an investing truism that has become ingrained in our thinking.

But what if, in fact, bonds had the potential to provide an investment return during central interest rate hiking cycles?

That’s the finding from research by Oliver Ge, a portfolio manager with Pendal’s Income and Fixed Interest team.

Monetary policy tightening cycles are actually kinder on bonds than people believe, Ge says.

“The key is that it depends on how much is priced into the bond market at the point central banks start lifting rates.

“Looking at history, an investor who buys bonds at the moment of the first rate hike in a cycle and sells at the last rate hike actually gets quite a substantial return.”

The finding demonstrates that there is a lot more nuance to the classic doctrine of “rates go up, bonds go down”, says Ge.

Since the 1990s there have four rate hiking cycles in Australia, each averaging an increase of 2.25 per cent to the RBA’s policy rate, he says. The annualised bond return over the same period was more than 4 per cent.

“The compelling story is don’t ignore bonds when rates are rising — they can still give you mid-single digit returns.

“That’s quite significant in a market where equities are negative.”

Find out about

Pendal’s Income and Fixed Interest funds

The explanation for why bonds had positive returns over those times is based on two factors, he says.

First, rate hikes do not materialise unannounced. The RBA broadcasts its decisions in advance and a considerable portion of future hikes are already in the price of the bonds before the first hike.

This means a 25 basis points move higher rarely translates into a direct one-for-one change in the yield of a bond, says Ge.

“During the 2009-2010 cycle, the RBA moved the policy rate up by 175 basis point from 3 per cent to 4.75 per cent. Over the same horizon, a five-year Commonwealth government bond moved up by around only 35 basis points,” he says.

The second thing is the pace of rate hikes. In principle, the more gradual a central bank tightens, the more income a bond can accrue to offset would-be losses, says Ge.

By magnitude, the largest tightening cycle over the last 30 years was 300 basis points, but it occurred over a six-year window, allowing bonds to maintain mid-single digit returns per annum despite the absolute quantum of moves.

“Right now, the market expects the RBA to kick off their hiking cycle in June, ending in mid-2024 at a peak rate north of 3 per cent.

“This puts the expected bond experience somewhere between the last two hiking cycles, both of which resulted in a positive outcome for fixed income investors.

“While a negative shock can’t be ruled out, the likelihood of further inflation surprise is diminishing.

“There’s already a lot priced into bonds. And it’s reasonable to say that we’re closer to the end of this higher rates move than we are at the start.”

About Oliver Ge and Pendal’s Income and Fixed Interest boutique

Oliver Ge is an Assistant Portfolio Manager with Pendal’s Income and Fixed Interest (IFI) team.

Oliver works on developing and running key quantitative investment models, and acting as trading support for the Income & Fixed Interest team. Oliver received his Bachelor of Commerce (Finance) from the University of Sydney and is also a CFA Charterholder.

Pendal’s IFI boutique is one of the most experienced and well-regarded fixed income teams in Australia. In 2020 the team won the Australian Fixed Interest category in the Zenith awards.

The invests across income, composite, pure alpha, global and Australian government strategies.

Find out more about Pendal’s fixed interest strategies here

About Pendal Group

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Ultra-loose monetary policy is creating exceptions to risk and reward – and bringing opportunities for investors seeking better returns for their cash. OLIVER GE explains

- Bonds paying better returns than bank deposits

- 4x returns when held to maturity

- Find out more about Pendal fixed interest funds

THE link between risk and reward is a staple of investment theory.

But ultra-loose monetary policy as the Reserve Bank of Australia seeks to support the economy’s pandemic recovery is creating some exceptions to that age-old rule.

Investors who choose the safety of a government bond (held to maturity) are now offered better returns than a nominally higher-risk bank term deposit, says Oliver Ge, a portfolio manager with Pendal’s Income and Fixed Interest team.

“If you’re willing to hold government bonds for a year — just like you would with a bank term deposit — you’ll get four-to-six times more money than you’ll get from a bank,” says Ge.

Cash is an important asset for many investors. It provides security and flexibility, and importantly it offers protection from being forced to sell assets in a downturn.

But for investors seeking income, it can offer very poor returns.

Find out about

Pendal’s Income and Fixed Interest funds

“You go to one of the big banks and they’re offering about 0.25 per cent interest rates on a one-year term deposit — $25 on a $10,000 investment. That’s not a lot.

“But if you’re happy to lock your money away for a year, why not try a government bond? A one-year Australian government bond is paying 1 per cent, so you’re getting four times as much money.

“Unless you think the Australian government is going to default — and as long as you hold to maturity — you’re better off giving them your money.”

Ge points out that state government bonds can offer even better returns, with the Western Australian semi-government bonds offering returns as high as 1.6 per cent.

Protection against downturn

Bonds provide a further advantage over term deposits because alongside guaranteed income and capital protection, they offer protection against an economic downturn.

“If there was a catastrophic event like a Covid version two and the RBA decides not to lift rates, these bonds could return a lot more as they will rise in value,” says Ge.

“Bonds are just insurance policies that always pay you — and when things blow up, they pay you even more.”

Ge says the anomaly exists because the RBA is providing very cheap funding to the banks, meaning they do need to compete for deposits in the market and can keep deposit rates artificially low without affecting the financing of their lending businesses.

“They have so much money they can afford to do this,” he says.

By contrast, government bonds are issued into a competitive global market and rates are set by investor demand.

Ge says the anomaly is likely to stay in place as long as the banks have access to cheap funding.

“This is a genuine opportunity to get a lot more juice with the same or better safety – assuming you hold to maturity,” says Ge.

About Oliver Ge and Pendal’s Income and Fixed Interest boutique

Oliver Ge is an Assistant Portfolio Manager with Pendal’s Income and Fixed Interest (IFI) team.

Oliver works on developing and running key quantitative investment models, and acting as trading support for the Income & Fixed Interest team. Oliver received his Bachelor of Commerce (Finance) from the University of Sydney and is also a CFA Charterholder.

Pendal’s IFI boutique is one of the most experienced and well-regarded fixed income teams in Australia. In 2020 the team won the Australian Fixed Interest category in the Zenith awards.

The invests across income, composite, pure alpha, global and Australian government strategies.

Find out more about Pendal’s fixed interest strategies here

About Pendal Group

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Could Russia’s invasion of Ukraine prompt Chinese action in Taiwan? That’s not likely in the medium term argues Pendal’s OLIVER GE

ALARM bells are ringing in the East.

As fighting intensifies in Ukraine’s urban core, Chinese jets have entered Taiwan’s air defence zone, leading some to speculate that it’s only a matter of time before we see People’s Liberation Army boots on the ground.

At times like this it’s understandable that investors pondering their exposure to Russia’s invasion of Ukraine might also think harder about the China-Taiwan stand-off.

Pre-election positioning among Australian politicians pulls the China-Taiwan situation into even sharper focus for local investors.

However a Chinese invasion of Taiwan is a very low probability event in the short and medium term.

Near term, the Chinese Communist Party has other priorities at stake.

President Xi has promised to rectify growing domestic discontent over diminished living standards. Housing affordability and employment opportunities are key focal points for the CCP leadership.

They do not have time for major external distractions.

In the medium term, Taiwan’s support from the US remains crucial. Remember that Taiwan (but unfortunately not Ukraine) is of great strategic importance to Washington.

Its proximity over major shipping lanes and dominance in semiconductor manufacturing has seen consecutive US administrations pledge Taiwan military support in the event of a war.

China has no appetite for a direct confrontation with the US.

In the longer term these reasons above do not negate the possibility of a future conflict.

A unified China is arguably the biggest political objective of the CCP. China’s dominance in the region and military capacity continues to build.

But for now the carrot of economic cooperation remains the preferred policy over brute force.

About Oliver Ge and Pendal’s Income and Fixed Interest boutique

Oliver Ge is an Assistant Portfolio Manager with Pendal’s Income and Fixed Interest (IFI) team.

Oliver works on developing and running key quantitative investment models, and acting as trading support for the Income & Fixed Interest team. Oliver received his Bachelor of Commerce (Finance) from the University of Sydney and is also a CFA Charterholder.

Pendal’s IFI boutique is one of the most experienced and well-regarded fixed income teams in Australia. In 2020 the team won the Australian Fixed Interest category in the Zenith awards.

The invests across income, composite, pure alpha, global and Australian government strategies.

Find out more about Pendal’s fixed interest strategies here

About Pendal Group

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Even with the promise of meeting bond interest payments, the risk of contagion from Evergrande has increased as investors rotate away from equities and high yield credit. Pendal’s Oliver Ge explains what’s next

CHINESE property giant Evergrande has staved off default on the first of many payments covering some $US300 billion in debt.

But investors are still holding their breath to see whether Beijing will step in and what happens next.

Pendal’s Oliver Ge says the fallout on the domestic Chinese market would be minimal in the event of a controlled default.

Evergrande — which owns 1300 projects in 280 cities according to Bloomberg — represents a small 0.2% portion of China’s loan system, says Ge, an assistant portfolio manager with Pendal’s Income and Fixed Interest team.

“Right now Beijing has not been materially vocal on a rescue package, preferring instead that the company quietly sells down its assets and makes investors, suppliers and homeowners whole before quietly exiting the industry.

“But the issue is that Evergrande is unable to deliver on the ‘quietly’ part since they have no credibility in the financial system.

“No one will lend them any money. The only way they can quickly raise cash is to mark down their existing inventory of apartments.”

Find out about

Pendal’s Income and Fixed Interest funds

Markdowns as a high as 25% have been quoted, says Ge.

But going down this path means the rest of Evergrande’s peer group would have its asset book revalued too –prompting the sell-off we’ve seen so far.

Broader impact for investors

Until recently the contagion was limited to Asia and resource names such as BHP and Rio Tinto, which supply the iron ore for Chinese property projects.

Today, even with the promise of meeting bond interest payments, the risk of contagion has increased as people rotate away from equities and high-yield credit altogether, Ge says.

And the market implication for offshore USD bonds is significant.

“Right now Evergrande USD bonds are trading around 20-25c to the dollar (yuan).

“Default is almost guaranteed at those levels and other domestic peers will invariably get dragged into the sell-off.

“The current Asian high-yield default rate is around 3%. This could rise to 9% if Evergrande and its subsidiaries officially miss their debt obligations going forward.

“In lieu of a policy u-turn from the Federal Reserve, government bonds will likely thrive in this regime.”

Evergrande is just the tip of a large iceberg in China right now, says Ge.

“There is an ongoing vicious cycle that won’t stop until Beijing decides to scale back their social inequality reforms.

“Loose monetary and fiscal can help but it won’t be enough to offset existing headwinds.”

About Oliver Ge and Pendal’s Income and Fixed Interest boutique

Oliver Ge is an Assistant Portfolio Manager with Pendal’s Income and Fixed Interest (IFI) team.

Oliver works on developing and running key quantitative investment models, and acting as trading support for the Income & Fixed Interest team. Oliver received his Bachelor of Commerce (Finance) from the University of Sydney and is also a CFA Charterholder.

Pendal’s IFI boutique is one of the most experienced and well-regarded fixed income teams in Australia. In 2020 the team won the Australian Fixed Interest category in the Zenith awards.

The invests across income, composite, pure alpha, global and Australian government strategies.

Find out more about Pendal’s fixed interest strategies here

About Pendal Group

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Market uncertainty means equity investors should consider positioning themselves across defensive and cyclical stocks. Pendal’s ANTHONY MORAN explains why

- Consider both defensives and cyclical stocks

- Building materials, steel and gaming less attractive

- Find out about Pendal Focus Australian Shares Fund

STOCKMARKET investors are experiencing how quickly inflation and policy responses can hit share prices.

So how should an ASX investor approach the stockmarket right now? Which sectors look promising and which should be reconsidered?

“The challenge is that all the sector outlooks are being challenged by the macro outlook at the moment — and whether central banks can engineer a soft landing, or maybe a mild recession as they get inflation under control,” says Anthony Moran, an investment analyst in Pendal’s Australian equities team.

“The uncertainty means investors need to be positioned across defensive and cyclical stocks right now.

“If we get a soft landing then cyclicals will do well and the defensives will underperform, and vice versa.”

Building materials

Some sectors may be better to avoid, says Moran. For example, the building materials sector is difficult to support given the macro outlook.

“We’ve been enjoying boom conditions globally for residential construction.

“Now we are seeing rates rise at different paces in different markets and Australia is behind the curve.

Pendal Focus Australian Share Fund

A high-conviction equity fund with 16 years of strong performance in a range of market conditions

“We are going to see faster rate rises here, and we are still a long way from the bottom of the cycle, so building materials is an easy avoid.”

Still, every sector — including building materials — will feature stocks that are more likely to outperform.

James Hardie, which earns a large chunk of its revenue in the United States, is an example. It has more exposure to renovations than new buildings, and demand in that part of the sector is more resilient.

“It’s kind of perverse. You can’t afford a new home so you renovate instead,” Moran says. James Hardie also operates in the US economy which is further through its housing cycle than Australia.

Steel is probably a sector to broadly avoid, Moran says.

The sector did well last year, but now it is normalising down. Moran said the industrial warehouse market has now peaked, and that has been a material driver of steel demand.

Gaming

Another sector to reconsider given the macro-economic climate is gaming, Moran says.

Adviser Sam is invested

in making our world

A better place.

Watch as Sam meets a

mum rebuilding her life

thanks to responsible

investing

“There was tremendous industry growth through the COVID years due to stimulus packages and a lack of alternative forms of entertainment.

“People were basically stuck at home playing mobile games or betting on the races and other sports.”

As those tailwinds subside, along with the drop in discretionary income thanks to higher cost-of-living expenses, gaming could be a sector to stay away from.

Though the newly demerged Lottery Corporation – which is the lotteries business of Tabcorp – may go against the trend.

“Essentially, it’s an infrastructure business with long dated concessions, very strong free cash flows, extremely resilient demand and some specific growth opportunities from increased digital penetration.

“It’s as much an infrastructure stock as a gaming stock and due to corporate activity there aren’t many of them left.”

What looks promising

What about sectors to invest in, given the macro-economic outlook?

“Paper and packaging is really interesting right now,” Moran says. “Some of the stocks in the sector have shown a tremendous ability to pass through inflationary cost pressures.

“In the case of Orora, it’s actually a tailwind because they’ve been able to pass on more than the price increases.

“Demand for their products is inelastic and it’s quite a defensive sector. There are also stock-specific factors that will help them.”

About Anthony Moran and Pendal Focus Australian Share Fund

Anthony Moran is an Australian equities investment analyst with more than 15 years of experience in a range of local and international sectors. His sector coverage includes Australian Industrials and Energy, including Building Materials, Capital Goods, Engineering & Construction, Transport, Telcos, REITs, Utilities and Infrastructure. Anthony is a CFA Charterholder and holds bachelor degrees in Commerce and Law from the University of Sydney.

Pendal Focus Australian Share Fund is Crispin Murray’s flagship Aussie equities strategy. It is a high-conviction equity fund with a 16-year track record of strong performance in a range of market conditions. The Fund features our highest conviction ideas and drives alpha from stock insight over style or thematic exposures.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.