The United Kingdom looks as “good as I’ve seen in the 30 years I’ve been working in it”, says Pendal Group’s Clive Beagles.

- Equities in the UK may be significantly undervalued

- Tilt toward value stocks should help the FTSE

- Emergence from COVID could trigger a re-rating

THE United Kingdom market looks “as good as I’ve seen in the 30 years I’ve been working in it,” says Clive Beagles, a senior fund manager with Pendal Group’s London-based subsidiary J O Hambro Capital Management.

“All the stars are aligning for investors.”

Low rates, a tilt towards value stocks, underperformance this year, an undervalued currency and plenty of merger and acquisition (M&A) activity means the UK share market has plenty of opportunities.

“The United Kingdom markets looks as good as I’ve seen in the 30 years I’ve been working in it,” says Beagles. “All the stars are aligning for investors.”

So far international managers have remained reticent about the market — often for reasons that aren’t about equity valuations.

Part of the reason why US companies are now attractive, Beagles says, is low interest rates and a tilt towards value stocks.

“The UK has the highest value bias of any market in the world,” Beagles explains. Value stocks to do better during cyclical upturns, particularly when interest rates are so low.

“Relative to Europe the UK market has fewer industrials companies and many more in services,” he says. “It also has this curious bias to commodities because oil and mining companies have always been in the market.”

2021 Money Management of the Year Awards

Pendal Australian Shares Portfolio

Winner – SMA Australian Equities

Pendal Property Investment Fund

Winner – Australian Property Securities

Over the past three decades, London’s FTSE has underperformed major indices on Wall Street, in Europe and in Australia. So far this year, the underperformance has been accentuated.

While London’s FTSE is up 8 per cent since January, the S&P/ASX is up 12 per cent, Germany’s DAX index is 15 per cent higher, the S&P500 on Wall Street is up 20 per cent, and France’s CAC index is up 21 per cent higher.

There’s plenty of reasons to buy into Britain.

“The currency is cheap and has been ever since Brexit,” Beagles says. “The UK is considered some sort of political hot potato but that’s been overdone.

“The politics around Brexit aren’t perfect, but let’s be honest, the politics in any democracy aren’t perfect. If you look on a purchasing power of parity basis the currency is probably 15 to 20 per cent too cheap.

“And 2021 and into 2022 will be very strong years in terms of GDP. The way the UK measures growth overstated the downturn, but that means it will bounce back further.”

Combined, these factors make the UK bourse attractive, Beagles says.

UK unusually cheap

“The UK is probably 10 to 15 per cent cheaper than Europe, and 30 to 40 per cent cheaper than the United States … and that’s unusual,” Beagles says.

There is another factor playing into the hands of investors in Britain.

“There has been an unprecedented number of companies bid for in the UK because they look cheap relative to international peers. And there is a relatively liberal attitude towards companies being bought, more so than in Europe where politics can sometimes get in the way.”

It means that international corporates are seeing the opportunity in Britain, even if investors aren’t.

“Over the last three years ever lower bond yields mean its all been about growth and momentum and that’s been good for the US and some of Asia,” Beagles says. “The UK and Europe have been viewed as lower growth. That’s changing.”

“On top of the Brexit has been going on since the summer of 2016, and it’s just been dragged out. Both Europe and the UK have suffered from that,” he says.

“But at some point all this has to manifest itself in a re-rating of the UK. If the strategy around re-openings and vaccines for COVID proves the right one, then maybe that will be the trigger point.”

About Pendal Group

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Michael is Head of Multi Asset for Perpetual Asset Management. In this role he is responsible for the suite of Multi Asset Funds and capital markets research.

Michael joined Perpetual in June 2014 and has 18 years finance industry experience. Prior to joining Perpetual Michael worked at JANA for 13 years, and held a number of positions across research, consulting and portfolio management, including Head of Investments, Implemented Consulting.

Earlier in his career Michael held a variety of positions at UBS, Morgan Stanley and Barclays Capital in both Australia and the United Kingdom.

Michael holds a Bachelor of Business (Economics and Finance) from RMIT University and is a Vincent Fairfax fellow.

Here’s what’s driving Australian equities this week according to Pendal’s head of equities Crispin Murray. Reported by portfolio specialist Chris Adams.

Concerns over the Delta variant’s potential to derail economic recovery, both domestically and overseas, dominated headlines.

Nevertheless, equity markets remain resilient. The S&P/ASX 300 gained 1.96% and S&P 500 0.96% for the week.

We don’t see this as an unsustainable disconnection between growth concerns and market returns. There are a number of factors providing support, including a strong US earnings season and ample liquidity which is fuelling M&A activity. Concerns over growth have also seen bond yields fall, bolstering returns for growth stocks.

US employment data at the end of the week was a reminder that economic growth may prove more resilient than the market thinks.

COVID – US

The US is bracing for an inevitable rise in cases as Delta takes hold. The main issue is that, unlike in the UK, the rise in new cases is leading to a material increase in headline hospitalisation rates.

The link between vaccination and a less severe infection is holding. However, there are states with low rates of vaccination, leading to a pick up at the headline levels of hospitalisations as new cases surge. We are also mindful that new case numbers are clearly being understated, as people are less likely to get tested.

The impact on mobility is yet to be seen. Mask mandates are being reinstated and are now recommended indoors by the Centre for Disease Control and Prevention (CDC). There is a high degree of resistance to this – from both vaccinated and unvaccinated people. At this point there appears to be no appetite for returning to lockdowns and there has only been limited signs of more subdued economic activity form this wave.

Find out about

Pendal Focus

Australian Share Fund

Crispin Murray,

Head of Equities

We are watching Missouri and Florida closely as some of the first states to experience the Delta wave. Based on the Indian and UK experience cases here could peak around 60-70 days into the wave, which would be by the end of August. There is some risk to this, given it would coincide with the return to school. Nevertheless, signals of a peaking wave in these states could be the trigger for a rotation back to cyclicals.

COVID – China

There are reports that China is facing Delta outbreaks in 17 of its 32 provinces. Beijing faces a similar challenge to Australia in that the political strategy has been elimination of Covid and there are not sufficient people vaccinated. Only 16% of the population is fully vaccinated and 60% have had one dose. Data suggests that the Chinese vaccines are also less effective than the mRNA-based approaches.

China is implementing lockdowns as a result, which of course affects growth. This is dragging on commodities and resources. However, it also means Beijing is more likely to pull the lever of traditional stimulus – property and infrastructure – given consumer demand growth remains muted.

Covid – Australia

The domestic emphasis is on the run rate of vaccinations. This has been accelerated by the shift in recommendation for AstraZeneca.

We are now running at 0.7% of the population being vaccinated each day. Peak rates in places such as Israel and the UK ranged from 0.8% to 1.0% per day. Australia could reach that rate on the current trajectory by the end of this month if people continue to take up AZ, where supply is available.

Nevertheless we go into reporting season with some wariness around domestic cyclicals, given uncertainty over the economic consequences, policy response and likely cautious tone from a number of these companies.

Economics

The narrative of concern around a slow-down seems to be nearing a crescendo – just as we get a reminder that the real US economy is still going well – in the form of jobs data.

- US July payrolls rose 943,000 on the previous month versus expectations of 870,000. The previous months’ result was also revised up by 199,000. Government jobs were an important contributor, but the private sector was also strong driven by leisure and hospitality.

- The Unemployment rate dropped from 5.9% to 5.4% which is real progress to the Fed’s goal of full employment.

- Hourly earnings were also up 0.4% month-on-month and 4.0% year-on-year. Wage growth in leisure and hospitality is now running >12%.

2021 Money Management of the Year Awards

Pendal Australian Shares Portfolio

Winner – SMA Australian Equities

Pendal Property Investment Fund

Winner – Australian Property Securities

This demonstrates ongoing resilience in the US economy, despite the narrative of “peak growth “ and surge in Delta.

There is also capacity for more upside surprise with >5m jobs still not returned. This will become apparent once the holiday season ends, although the Delta strain has likely reduced the pace of this job recovery.

This strength is reflected in shifting expectations around policy. The strong jobs data means consensus now expects the Fed to announce tapering of QE in November and implement it immediately, or in December, rather than waiting until 2022. The market is also now assuming that the pace of tapering will be swifter than was the case a few months ago.

Inflation

Inflationary expectations are also playing a role in this view. There are some indications that the supply bottlenecks which caused the spike in short-term inflation may prove more persistent than first thought. For example, the number of ports seeing capacity issues has actually increased.

Delta’s rise in Asia is also raising concerns for global supply chains if lockdowns remain in place. Anecdotally, US auto dealers are sitting on several million fewer cars in inventory than would normally be the case at this time of year.

In addition to this, survey data indicates US companies currently have more pricing power than we have seen in decades.

The upshot is that inflation concerns are still real, despite what the decrease in bond yields in recent months might suggest.

Markets

The confluence of surging US cases and outbreaks in China exacerbated concerns over global growth and weighed on commodities last week. Brent crude fell -7.4%, iron ore -6.0% and copper -3.0%.

Commodity prices remains largely hostage to Covid sentiment in the near term. This will be tied to the rate of new US cases and hospitalisations, which are likely to deteriorate for at least 2-3 weeks.

Bonds yields may be hitting their lows for the balance of the year. Concerns over growth feel like they are reaching a peak, while several technical supports also look to be near their maximums. The potential for more persistent inflation is also likely to play a role.

While we could not expect yields to fall much lower, we would not be surprised to see bonds holding in near these levels for the rest of the quarter. We don’t expect anywhere near the degree of sell-off seen in Q1 2021.

US earnings season continues to be very strong. The S&P 500 is beating quarterly earnings forecasts by 25%. Re-opening stocks have fared best, beating expectations by 45% on average. However, the stocks have not reacted given concerns over Delta.

Upgraded CY21 earnings expectations means the S&P 500 is now on 21x earnings. This isn’t cheap, but is reasonable given rates. At this point the consensus is only for 5% earnings growth in CY22.

There was significant rotation on the ASX. Concerns over the growth outlook saw Technology (+12.7%), Staples (+2.8%) and Health Care (+2.6%) outperform the benchmark. Technology also got a kicker from Square’s bid for Afterpay (APT, +36.7%).

One key risk heading into reporting season is that the valuation multiple for a lot of growth and quality defensive companies remains elevated, reflecting high expectations. Any disappointment – or impact from lockdowns – leaves them vulnerable.

Stocks

Resource stocks fared worst on the ASX 100 reflecting lower prices. Fortescue Metals (FMG, -7.5%) and Mineral Resources (MIN, -6.4%), both leveraged to iron ore, were the worst performers. Oz Minerals (OZL, -3.3%), Northern Star (NST, -2.7%), BHP (BHP, -2.6%) and Rio Tinto (RIO, -2.5%) were all close behind.

REA Group’s (REA, -1.4%) result was broadly in line. Management’s observation that Sydney listing volumes were down 22% in July should not have surprised anyone. However, it does emphasise the potential impact of near-term operating momentum on the more highly-valued parts of the index, as both it and Domain (DHG, -4.9%) came off.

Santos (STO, 0.0%) and Oil Search (OSH, +3.9%) agreed terms on their proposed merger. We still have limited insight on synergies. However, the combined entity will be better positioned to navigate the on-going energy transition.

APT jumped on the bid and – given that it is now effectively trading as a proxy for Square – continued to benefit from rotation to the latter in the US market. It was the best performer on the ASX 100.

The bid highlights the escalation of the land grab in buy-now-pay-later (BNPL) and in payments more broadly. Square, Paypal, Shopify, Apple and Affirm are all jostling for positions within this system, alongside more traditional banks. The battle-lines are being drawn and competitive intensity is likely to increase. APT’s decision to sell seems a good one in this context.

Other growth stocks performed well mainly driven by thematics. Wisetech (WTC, +7.6%) and Xero (XRO, +6.0%) also did well, the latter announcing measures to drive revenue growth through its app store.

ResMed’s (RMD, +3.2%) result was a good one. The flowgen machine recall by Philips leaves RMD is a strong competitive space and is driving large increases in revenue, although they are running into some supply constraints. There is also some pressure on margins last quarter as a result of rising prices on polymers and components. The stock has been strong and is in a sweet spot. However, we are wary over the degree to which people are capitalising the share gains from Philips.

Finally, it is worth noting that the Federal Court ruled in favour of Chubb Insurance in a dispute over business interruption cover with Star Entertainment (SGR, -2.3%) based on the lack of physical damage. This may help set a precedent for other similar cases.

Find out about Crispin Murray’s Pendal Focus Australian Share Fund

About Crispin Murray and Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia. Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Find out more about Pendal Focus Australian Share Fund here.

Contact a Pendal key account manager here.

Matt Sherwood is Perpetual’s Head of Investment Strategy, Multi Asset. In this role, Matt is responsible for monitoring, analysing and forecasting earnings growth, interest rates, currencies, economic growth and policy implications across major regions.

Matt joined Perpetual Asset Management Australia in 2005 and his viewpoints and analysis of international developments are frequently sought by policymakers, opinion leaders and investors in Australia and Asia. These include television news networks such as Reuters, CNN and Bloomberg in Asia and Sky News, SBS and the ABC in Australia. His opinions have appeared in many newspapers including the Wall Street Journal, Washington Post, the New York Times and Australian Financial Review.

Matt has previously been a panel member which discussed macro issues with the US Federal Reserve on a quarterly basis and has briefed the BIS on several occasions on balance sheet issues facing the global economy. His current research focus is on the global trade war and whether monetary policy can prevent a serious downdraft in growth and regional sharemarkets.

Matt is a published author of the book titled ‘Intelligent Investing’ and began his career as a Senior Economist at the Reserve Bank of Australia, where he gained significant experience in monetary policy formulation and undertook detailed research into the equity risk premium, currency markets and business investment.

Matt has a Bachelor of Business from the University of Newcastle and a Masters Degree in Economics (Finance and Econometrics) from the University of Sydney. Matthew has also held a lecturing position with Kaplan Education (formally FINSIA) between 1997 and 2010 and has also lectured MBA classes from Case Western Reserve University in the United States.

Here’s our weekly Bond, Income and Defensive Strategies note from Pendal portfolio manager Tim Hext.

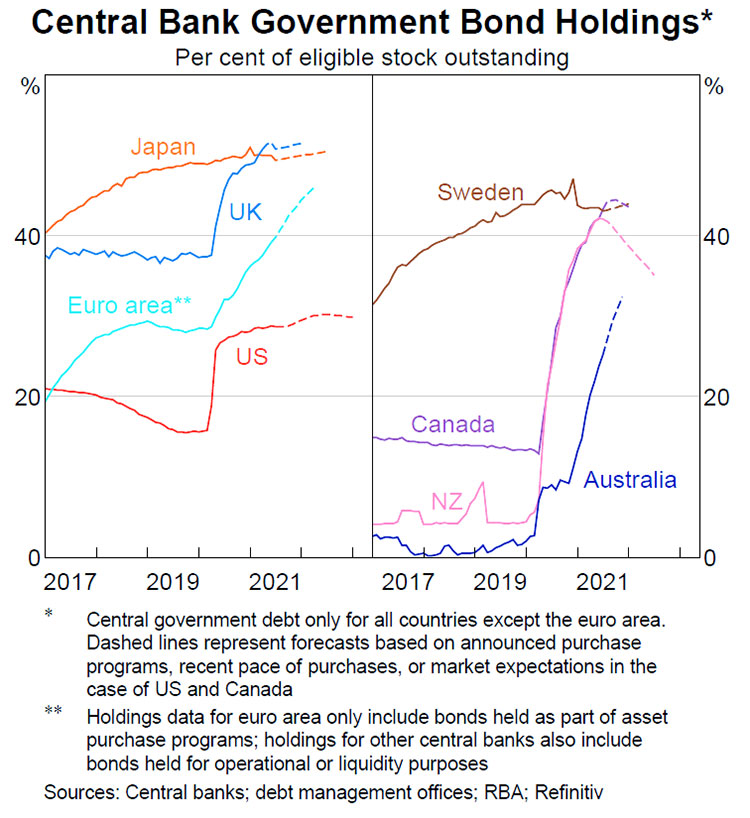

THE latest RBA statement on monetary policy is a great read, not just for thoughts on the economy but for the graphs.

The RBA’s vast team of economists always find new and interesting ways to look at the state of play.

There were several that caught our eye this time.

We are truly in a world of money printing

The first graph below shows how much government bond markets are owned by central banks.

This is the government printing money to finance the government. And still no inflation. Modern Monetary Theory is onto something here.

The message from the RBA seems to be: relax, we’re not even in the medals.

These purchases and super-low cash rates are all part of a slow and subtle financial repression.

Rather than having people go backwards nominally, just keep rates below inflation and have savers go backwards in purchasing power.

At first this is not noticed too much. Since growth assets re-rate higher with negative real yields, asset owners sit back happily. This is the period we are still in.

But eventually this will eat away at our standard of living — especially as inflation picks up.

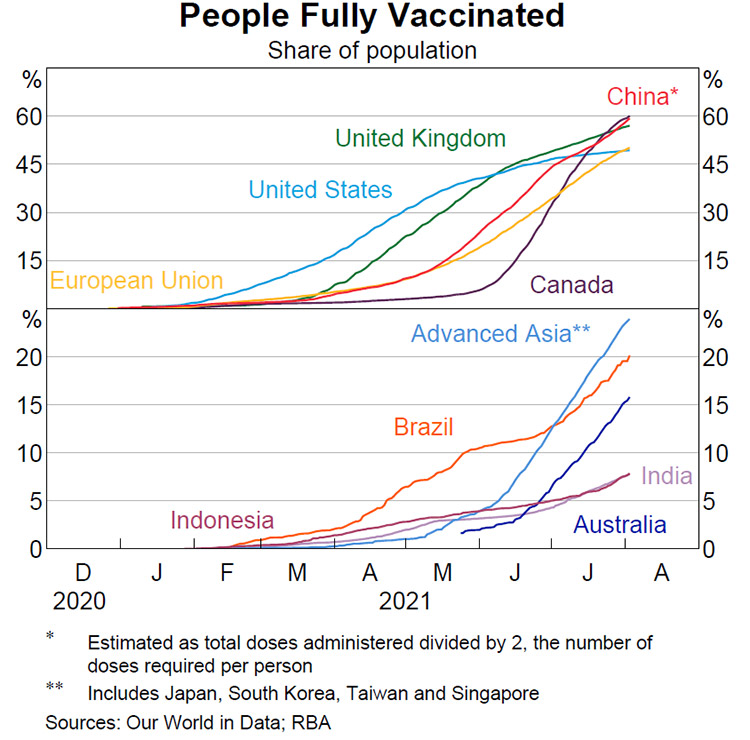

Most of the world’s GDP is opening up and living with 50-60% vaccination rates

This second graph will come as no surprise to locked-down readers.

Australia’s developing country status in vaccines versus our developed peers is shown here. I guess our success and eventual complacency in 2020 came back to bite us in 2021.

This graph shows that the majority of the world’s GDP is now opening up and living with the virus at around 50-60% vaccination rates.

By 2022 we should be opening and hopefully seeing the end of lockdowns.

Pent-up savings and demand should see a strong rebound in the economy and some wage and price pressures.

Other than that, rates markets have spent the past few weeks treading water — sitting back and once again watching with envy the never-ending riches of equities.

Find out about

Pendal’s Income and Fixed Interest funds

About Tim Hext and Pendal’s Income and Fixed Interest boutique

Tim Hext is a portfolio manager with Pendal’s Income and Fixed Interest team.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia. In 2020 the team won the Australian Fixed Interest category in the Zenith awards.

With the goal of building the most defensive line of funds in Australia, the team oversees A$22 billion invested across income, composite, pure alpha, global and Australian government strategies.

Find out more about Pendal’s Income and Fixed Interest strategies here

About Pendal Group

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

David Hudson is the Head of Asset Allocation within the Multi Asset team for Perpetual Asset Management Australia. In this role, David is part of the portfolio management team managing all multi asset funds. He is responsible for generating and implementing active asset allocation ideas and the strategic asset allocation of multi asset funds.

David is a proven portfolio manager with almost two decades experience in multi asset portfolio management including 14 years as the lead portfolio manager of diversified funds at BlackRock Investment Management. David has a strong fundamental background in macroeconomics and all asset classes.

David has also held positions as an equity strategist at Bankers Trust Investment Management; fixed income strategist and senior economist at Bankers Trust Investment Bank; and as a senior adviser to the Prime Minister. He started his career as an economist with the Commonwealth Department of Treasury in the early 1980s.

David has an Honours degree in Economics from Adelaide University.

The cement industry accounts for about 8 per cent of global greenhouse gas emissions. French-based Hoffmann Green Cement has a potentially lucrative solution

- Innovative solution to one of the biggest emissions conundrums

- Potential long-term upside for investors

- Find out more about Regnan Global Equity Impact Solutions

THE cement industry is one of the world’s biggest carbon polluters.

It is the most widely used human-made material across the globe with about 4.6 billion tonnes produced each year. And it’s remained largely the same for centuries.

“The story goes that if the Roman emperors were in the world today, one thing that would still be familiar to them is cement production,” says Maxime Le Floch, an investment analyst focused on equity impact solutions at Regnan.

It’s an industry that hasn’t innovated very much. Until now.

French-based Hoffmann Green Cement Technologies is changing the way cement is manufactured, drastically reducing the amount of greenhouse gases emitted in the process of creating concrete.

“The reason we got interested in the company is because we need to decarbonise the economy,” Le Floch says candidly.

“The cement industry accounts for about 8 per cent of global greenhouse gas emissions. That’s a big share of industrial emissions, which is going to stand out even more as other sectors decarbonise.”

Find out about

Regnan Global Equity Impact Solutions Fund

Hoffmann Green’s breakthrough was to eliminate the use of clinker in the creation of cement.

Clinker is a mix of limestone and minerals that are heated in a kiln as part of the cement making process. This releases enormous amounts of carbon dioxide.

Eliminating clinker substantially reduces the amount of CO2 released into the atmosphere during the production of cement.

“Hoffmann Green reduces the carbon footprint of cement by a factor of five,” Le Floch explains so was an obvious option for Regnan to consider.

Regnan thinks about stocks in terms of impact, value creation, value distribution and value gap. The impact Hoffmann Green can have in terms of reducing carbon emission is clear.

“Most of the innovation happening in the cement industry is incremental, around existing technology. But Hoffmann Green has removed the clinker chemical reaction in making cement and that’s quite dramatic.”

Hoffmann Green also ticks the value creation box, in part because its competitors aren’t innovating fast enough, burdened by existing infrastructure that risks becoming stranded. Cement is generally a relatively localised industry because of costs associated with transporting the product long distances.

“Hoffmann Green can come in, have a product that’s much more radical and better for the environment, and there’s demand for that. They are able to charge about twice the price of normal cement because of the green credentials.”

[Hoffmann] are able to charge about twice the price of normal cement because of the green credentials.

Maxime Le Floch, Regnan investment analyst

Hoffmann Green’s process also means the energy bill to produce cement is lower, reducing the group’s cost base.

“The cost base is quite low. The capital requirements on new sites are much lower than other cement companies. There’s a lot more operating leverage as they scale up,” Le Floch says.

“In terms of value distribution, this is a relatively small company that’s scaling up,” he says. “They’re very committed to sustainability. It’s quite an automated process that doesn’t involve large amounts of industrial heat for instance … so it’s also a much safer process for employees compared to other types of cement making.”

A company like Hoffmann Green should benefit in the future because as they grow, their value proposition will become more evident to customers, who are being pushed to de-carbonise.

“Hoffmann Green is relatively small – a half a billion Euro market cap. It’s the smallest company we have. But as they scale up, we will have the opportunity to scale up,” Le Floch says. “They are in an investment phase. They are building new sites.”

He argues there’s plenty of opportunity for the company. There’s a potential for more sites. There’s also a benefit when carbon prices increase, because customers will be look for low CO2 emission options. And there’s an option for an international licensing model.

Of course, every investment carries risk.

“The key risk is in execution,” Le Floch says. “It’s in delays to building out their manufacturing and production capacity. There is always a technology risk with new processes, though I think that’s reducing over time as they get more confirmation from customers using their cement. And there will be other competitors emerging in the pathway to decarbonisation.”

“But Hoffmann Green has been able to hit its key milestones in terms of its product being validated. There’s a new innovation cycle in the economy around decarbonisation and sustainability more generally … and Hoffmann Green is at the cutting edge.”

About Regnan

Regnan is a responsible investment leader with a long and proud history of providing insight and advice to investors with an interest in long-term, broad-based or values-aligned performance.

Building on that expertise, in 2019 Regnan expanded into responsible investment funds management, backed by the considerable resources of Perpetual Group.

The Regnan Global Equity Impact Solutions Fund invests in mission-driven companies we believe are well placed to solve the world’s biggest problems.

The Regnan Credit Impact Trust (available in Australia only) invests in cash, fixed and floating rate securities where the proceeds create positive environmental and social change. Both funds are distributed by Perpetual Group in Australia.

Find out about Regnan Global Equity Impact Solutions Fund

Find out about Regnan Credit Impact Trust

For more information on these and other responsible investing strategies, contact Head of Regnan and Responsible Investment Distribution Jeremy Dean at jeremy.dean@regnan.com.