There are plenty of so-called ‘climate-aware’ companies to invest in — some 60 per cent of the ASX300 (by market cap) now have net zero commitments. But how do you judge the right ones? EDWINA MATTHEW explains

- Not all net zero commitments are the same

- Strategy and governance, disclosures and analysis of targets are critical, plus transition implications for workers

- Red flags include board sceptics, indirect impact from value chains and lack of progress

Some 60 per cent of the ASX300 (by market cap) now have net-zero commitments.

That’s a reflection of accelerating global progress on climate change.

Almost 90 per cent of global emissions are now covered by net-zero commitments from nations — up from about 75 per cent before the recent COP26 climate change conference.

Financial institutions are also forming initiatives — such as the Glasgow Financial Alliance for Net Zero announced at COP26 — to accelerate the transition away from fossil fuels.

So Australian investors have plenty of opportunity to invest in “climate-aware” companies.

The question is: how do you judge which companies are best placed to deliver on their net-zero commitments?

“Investors and the public are sceptical about the credibility and veracity of many net-zero commitments,” says Edwina Matthew, Head of Responsible Investments at Pendal Group.

“Investors need to ensure the companies they invest in are walking the talk.

“That means having a clear and credible climate strategy in place that is based on delivering actual real-world decarbonisation, and not just ‘virtual’ reductions from carbon offsets and asset divestment.”

Below Edwina lists some key things to look for.

Sustainable and

Responsible Investments

Fund Manager of the Year

Examine a company’s net zero targets

A company needs targets that span the life of its transition plan – including intermediate (typically 2030) and long-term (2050) targets. They need to be science-based and aligned to the Paris Agreement.

Companies should also be clear in their disclosures about whether their targets are across “scope 1, 2 and 3 emissions” — and what percentage of its assets and emissions are covered by those targets.

What are Scope 1, 2 and 3 emissions? They are the three factors an organisation should consider to understand its carbon footprint.

- Scope 1 greenhouse gas emissions come directly from sources controlled by a company

- Scope 2 are indirect emissions associated with the purchase of electricity, steam, heat or cooling

- Scope 3 result from assets not controlled by a company, but indirectly impacted by its value chain

Investors also need to look out for how carbon offsets are used in their net zero plan and also whether there is reasonable consideration of transition implications for their workforce and communities.

To mitigate risks of ‘green-washing’, investors need to not just look at the company’s targets but also look at the governance and incentive structures and disclosure practices.

Is there clear evidence that a company’s climate transition plan is incorporated into its corporate strategy and risk management systems?

Red flags to watch out for

There are also red flags for investors, Matthew says.

“One is having net zero implementation responsibilities sitting solely in a sustainability or ESG role rather than being incorporated into relevant executive and business line responsibilities.

Also look out for climate sceptics on boards or lobbying against change via industry associations.

“Investors should also assess whether scope 3 emissions are sufficiently considered. While it’s an iterative process that should be refined over time, there should be demonstrable evidence of progress.”

Find out about

Pendal Horizon Sustainable Australian Share Fund

Climate transition plan

Companies should have a climate transition plan with detailed analysis of material risks and opportunities.

There should be evidence the analysis is used to inform business decisions (including relevant capital allocation), resourcing and expertise and sometimes links to remuneration.

Investors should ask themselves if the board has sufficient skills. Is there stakeholder engagement? What is the track record of achieving previous transition strategies and targets?

Disclosures

Investors need to also pay close attention to disclosures.

Does a company produce reporting in line with the Task Force on Climate Related Financial Disclosures (TCFD)? How regular and comprehensive are they?

Does a corporate clearly outline the most material climate-related risks and opportunities for its business? How robust is the analysis that sits behind these views?

“We want to make sure their net zero plan is credible. It should be practical but adequately ambitious to align with key stakeholder expectations,” Matthew says.

“Without doubt the private sector on the whole is stepping up to the net zero call to action and this is a very important development.

“As investors, the onus is now on us to pay attention to the detail and progress of individual net zero plans.

“Through company engagements, we are working with companies to address any shortfalls and accelerate real economy decarbonisation.”

About Edwina Matthew

Edwina Matthew is Pendal’s Head of Responsible Investments. Edwina is responsible for maintaining our leadership position in the provision of sustainable and ethical investment products.

Edwina is actively involved in the implementation of the UN-supported Principles for Responsible Investment. She also represents the company in working groups with a number of industry associations and initiatives relating to responsible investment.

About Pendal Group

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

We believe sustainability considerations ultimately drive higher and more stable investment returns over the long term.

Pendal Group has a proud heritage in responsible investing, extending back decades. Our specialist responsible investing business Regnan includes highly experienced ESG research and engagement experts and offers a growing range of investment strategies.

Some of our responsible investing strategies

Here are the main factors driving the ASX this week according to our head of equities Crispin Murray. Reported by portfolio specialist Chris Adams

The market is focused on two issues right now.

- First there is increasing scrutiny on signals from the US Federal Reserve. Expectations are building that rates will need to rise sooner rather than later. The idea that the Fed could be comfortable with higher inflation as a “catch-up” from the previous period of low inflation is in question

- The second issue is the new wave of Covid in Europe, the extent to which this will be replicated in the US and the potential economic impact.

Both issues have the potential to depress bond yields. Confidence that the Fed will take action to control inflation can support the bond market. So too can another Covid wave if it suppresses economic growth.

This is reflected in the equity market with a rotation from cyclicals to growth and defensives.

Equity market returns were muted last week. The S&P/ASX 300 fell 0.47% and the S&P 500 gained 0.36%.

We think sentiment on these two issues presents a risk to markets — but more in the way of driving material rotation rather than a sustained sell-down.

Abundant liquidity, decent economic growth and stimulatory policy all remain supportive of the overall market.

Covid and vaccines

Unfortunately the pandemic has escalated again. A surge in central European cases has culminated in a nationwide lockdown in Austria and the potential for other countries to follow suit.

Only about two-thirds of Austrians are fully vaccinated. But even in The Netherlands, where almost 74% of people are fully vaccinated, there is a surge in new cases.

The acceleration highlights the seasonal element of Covid (as the northern hemisphere heads into winter) and the importance of increasing vaccine penetration.

Pendal Focus Australian Share Fund

Now rated at the highest level by Lonsec, Morningstar and Zenith

In the US, both new cases and hospitalisations have increased.

The market is concerned a new wave will result in a repeat of the economic hit in June and July.

At this point we think two factors can support a less severe outcome:

- Each successive wave has resulted in less economic impact. We think this should continue to hold true. Continued penetration of vaccines since mid-year — coupled with boosters and better treatments — should reduce risk of broad-based lockdowns. There is also a question about the degree to which some communities would tolerate additional blanket lockdowns.

- Economic growth was starting to slow from the second quarter peak when the last wave hit the US. This time the economy is accelerating. So while the latest surge may constrain economic improvement, it would not be reinforcing an already declining trend.

That said, the market will need convincing — and trends are likely to be negative in the next few weeks. This would support continued rotation from cyclicals to growth and defensives.

The key will be whether countries such as Germany and the US follows a UK-like path, where cases are at moderately high levels, but hospital numbers are manageable.

Economics and policy

Japan’s US$500 billion stimulus package and the passage of the Biden US$1.2 trillion infrastructure bill emphasise that fiscal policy will remain supportive.

We’ve also seen agreement at US agricultural equipment maker John Deere and Co, which experienced its first strike for wage growth in 30 years.

Workers agreed to a six-year deal including a 10% rise in the first year, sign-on bonuses and a return of cost-of-living adjustments. Yet another sign of the wage pressure coming through.

Inflation

There is a view building that the Fed is likely to signal a more hawkish shift on rates in its next meeting on December 14-15.

Previously, the Fed’s line has been that it was comfortable with higher inflation because there had been a period of lower-than-target inflation. This could act as a buffer for inflationary pressure.

No matter how transitory you believe current inflation to be, this buffer has now gone.

The Fed can continue to argue it is tolerating higher inflation to support employment goals. But the notion that inflation can run hotter to offset previous muted inflation no longer holds.

The market is also increasingly aware that some of the more structural drivers of inflation are flowing through and will be difficult to hold back. For example, leading indicators of housing rents suggest this will pick up materially over the next 12 months.

At the same time, the outlook for growth remains reasonably strong, despite the potential for another Covid wave, as discussed earlier.

To put some context around the combination of growth and inflation on nominal GDP, we are set to see levels in Q4 not seen since the early 1980s.

Nominal GDP is a reasonable proxy for corporate revenue and should underpin corporate earnings growth into CY22.

The risk comes if it also forces central banks to apply the brakes more aggressively.

This combination of higher growth and the flow-through of property-related inflation saw three members of the Fed signalling last week that the topic of faster tapering will be discussed at the December meeting.

There are two broad schools of thought on inflation at the moment:

- Current inflation is a function of temporary factors relating to the mismatch of supply and demand. Supply chains were unprepared for the rebound in demand as consumers came out of lockdown. There have been episodes of this before, such as in the early 1950s at the start of the Korean War. The lesson then was that inflation quickly fades as it begins to eat into the spending power of consumers and leads to demand destruction.

- The alternative view is that while the initial rise of inflation was induced by these temporary factors, it now becomes entrenched due to issues around labour supply, shortening supply chains, the impact of de-carbonisation (greenflation) and a lack of adequate response from central banks.

In this regard, the two key issues to monitor in upcoming months are US labour market participation and how prepared central banks are to anchor inflation expectations.

On the latter point, a decision to replace Fed Chair Powell or appoint him for a second term with be important. Lael Brainard is seen as an alternative. Powell remains the favourite, but his odds have fallen in recent weeks.

China

There have been signs in recent weeks that Beijing is looking to ease policy in response to slowing growth.

This is not straightforward. The same cocktail of factors dragging on growth also make an effective response difficult. These include:

- Beijing’s zero-Covid approach

- Power constraints

- High raw-material prices

- Weak housing sentiment

- High debt, leading to constraints on local government financing

- A strong currency

Recent statements from Premier Li Keqiang and the People’s Bank of China suggested an emphasis on constraining credit was diminishing and there was a need to safeguard exports.

A shift in policy direction will help limit the slowdown. Concerns around the Evergrande issue have also receded. However we do not see this as the time to be too bullish on China-sensitive stocks.

Beijing faces headwinds in its effort to combat slowing growth. Covid remains a challenge. So, too, do poor consumer sentiment towards property, rising inflation, weakening exports and constraints on local government funding for infrastructure due to falling land sales.

Meanwhile China has imposed environmental-based constraints on growth ahead of the Winter Olympics in March.

Sustainable and

Responsible Investments

Fund Manager of the Year

While we are likely to see cuts in reserve ratio requirements for the banks, increased credit growth and some fiscal measures, these will probably be incremental in nature.

They will also take time to flow through.

We can reasonably expect concerns over China’s growth to remain in place for the first quarter of 2022.

Markets

Rising Covid, combined with a stronger US dollar, has led to a rotation away from cyclicals and back towards growth.

It’s worth noting that within tech, large cap is performing better than small cap in the US. This reflects rising volatility in the macro environment, which favours the more stable names with stronger earnings.

Oil prices were weaker as the US released some strategic energy reserves. There was talk that Washington was lobbying China to do likewise to help ease energy prices, though this is unlikely to work in the medium term.

In Australia the banks have given up their market leadership for 2021 (year-to-date) on the back of an update from Commonwealth Bank (CBA, -9.54%). Financials have returned 26.09% YTD, versus 33.33% for Communication services and 27.91% for Consumer Discretionary.

Growth names did best last week. Technology (+3.08%) and Health care (+2.82%) led. Financials fell 3.22%, Energy was down 1.57% and Materials lost 1.48%.

About Crispin Murray and Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia. Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Find out more about Crispin Murray’s Pendal Focus Australian Share Fund

Find out about Crispin’s sustainable Pendal Horizon Fund

A quick investor’s guide to this week’s economic events with portfolio manager TIM HEXT from Pendal’s Income and Fixed Interest team

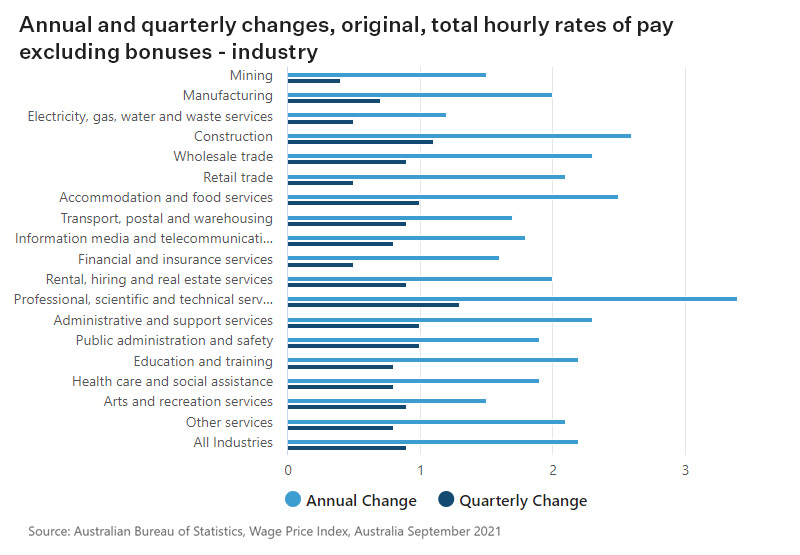

THE main event for Australian bond markets this week was Wednesday’s release of the Wage Price Index (WPI) for the September quarter.

This number has gained importance with Dr Lowe’s strong view that a sustainable inflation rate at the RBA target (2.5%) is highly unlikely without wage growth comfortably over 3%.

Effectively wages have become a hurdle to cash rate hikes.

So who won this week’s battle between the RBA (no hikes in 2022) and the market (75 basis point of hikes in 2022)?

Well it was a rare recent victory for the RBA.

Inflation prints of late have left the RBA shaky. But the latest wages number fitted the RBA narrative and the market cut expectations from 75 to 60 basis point of hikes.

The WPI showed wages growth of 0.6% for the quarter and 2.2% for the year. Reports of labour shortages and accelerating wage growth are yet to show through in a meaningful way.

As you can see below, only one of 18 industries measured was over 3% (Professional, Scientific and Technical Services at 3.4%) and only another two above 2.5% (Construction at 2.6% and Accommodation and Food Services at 2.5%).

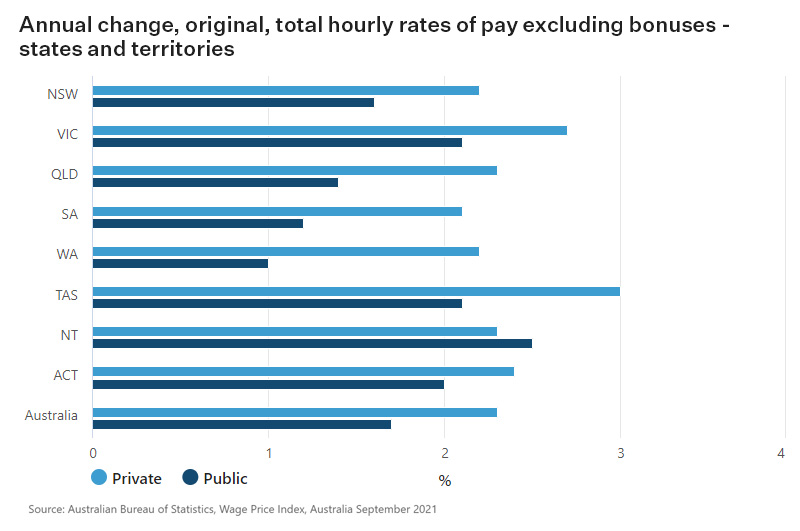

Data by state was also surprising, as you can see below.

You’d think Western Australia — with a booming economy, closed borders and unemployment at 3.9% — would be seeing massive pressure on wages. Apparently not with 2.2% wages growth. Only Tasmania is nearing 3%.

Some of this is due to the inertia of our wage arrangements. Many awards are only negotiated every three years.

Recent awards seem to be targeting 3% and successfully getting it.

Unions know for the first time in a while they hold the better cards. Many are now saying 3% is the minimum they expect. They have the RBA in their camp.

Rather predictably employers are pushing back and asking for quicker border re-openings to give them an increased pool of labour.

Recent reporting seasons suggest most larger companies are able to pass on good times to their workers, even if not willingly.

Public sector wages have been a handbrake, but most states are now back to the 2.5% level of the last decade.

The federal government has moved from the 2% that Abbott brought in, back to matching the private sector.

Find out about

Pendal’s Income and Fixed Interest funds

Where to from here?

Everyone’s in fierce agreement that wages are going up — but by how much and when?

This is crucial for the interest rate outlook. Given the WPI is an average, to hit 3.5% wage growth you need a lot of 4-to-5% outcomes to counter the many stuck at zero (hello finance) and 2.5%.

There have been isolated cases of 5% or 10% rises in areas such as or Accounting and these could well spread further.

But until we see large-scale awards going through at 4% or 5% — or a similar minimum wage outcome — wages well above 3% seem unlikely.

Maybe it’s a 2023 outcome. I suspect we will get there, but for now Dr Lowe looks to be correct in his patience.

Since wages are the ultimate lagging indicator, markets will not share that patience.

Our portfolios have covered short-duration positions. Depending on levels we will likely wait until early next year before re-establishing.

The two months of upcoming radio silence from the RBA and the lack of domestic inflation data until late January means we will be buffeted by offshore markets.

Steep curves though mean it is costly to sit in cash through the summer.

About Tim Hext and Pendal’s Income & Fixed Interest boutique

Tim Hext is a Pendal portfolio manager and head of government bond strategies in our Income and Fixed Interest team.

Tim has extensive experience in banking, financial markets and funding including senior positions with NSW Treasury Corporation (TCorp), Westpac Treasury, Commonwealth Bank of Australia, Deutsche Bank, Bain & Co and Swiss Bank Corporation.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia.

Find out more about Pendal’s fixed interest strategies here

About Pendal

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

In 2023, Pendal became part of Perpetual Limited (ASX:PPT), bringing together two of Australia’s most respected active asset management brands to create a global leader in multi-boutique asset management with autonomous, world-class investment capabilities and a growing leadership position in ESG.

Two events next week will shed light on whether dovish or hawkish monetary policy settings are likely in the short term. TIM HEXT explains

ON MY desk I keep a list of doves and hawks in the US Federal Open Market Committee — the group that makes monetary policy decisions for the Federal Reserve.

This helps when the 12 voting members — who meet eight times a year on proposed changes to near-term monetary policy — issue comments about their latest decision.

Australia doesn’t have monetary policy “voters” as such.

The RBA bureaucrats present their recommendations to the board. What happens next is top secret — though a source once told me there’s only been one occasion the board has begged to differ.

Which system works best is up for debate. I tend to side with the RBA and the view that too much transparency in decisions can confuse and backfire.

Nevertheless the RBA now provides comprehensive minutes of its meetings — even if they are more RBA staff comments than actual minutes.

Why is this important?

Find out about

Pendal’s Income and Fixed Interest funds

There are two major upcoming events that bear close watching around this.

Firstly, next week Joe Biden will announce the new Fed Reserve Chair.

Jerome Powell is still favourite to be reappointed but if betting agencies are to be believed Lael Brainard — an economist who’s been on the Fed’s board of governors since 2014 — has a decent chance.

Both are considered centrist on the spectrum. But the prospect of Brainard alongside dovish US treasury secretary Janet Yellen is seen as a nod to a more progressive stance in fiscal and monetary policy.

Markets would likely view it as more dovish in the medium to long term even if near term a change of guard might rattle a few.

Australian wages data

The second event to watch for is next week’s release of Australia wages numbers on Thursday.

RBA governor Phil Lowe’s current “dovish” stance on inflation is based on the strong view that you need significantly higher wage growth (at least 3% but likely more) if inflation is to sustain a 2.5% level.

The new reactionary RBA is happy to wait and see.

As Dr Lowe said in a speech this week, Australia’s wage system is always slow to move given the award structure.

Getting back to 2.5% wage growth should be easy since even the public sector — around 20% of workers — has now moved back to 2.5% targets. However he thinks a move above 3% is unlikely till late 2023.

Therefore debate will continue on whether central banks are being too slow to tighten.

Bond markets for now believe they will move quicker than their words suggest but few are predicting a major policy error.

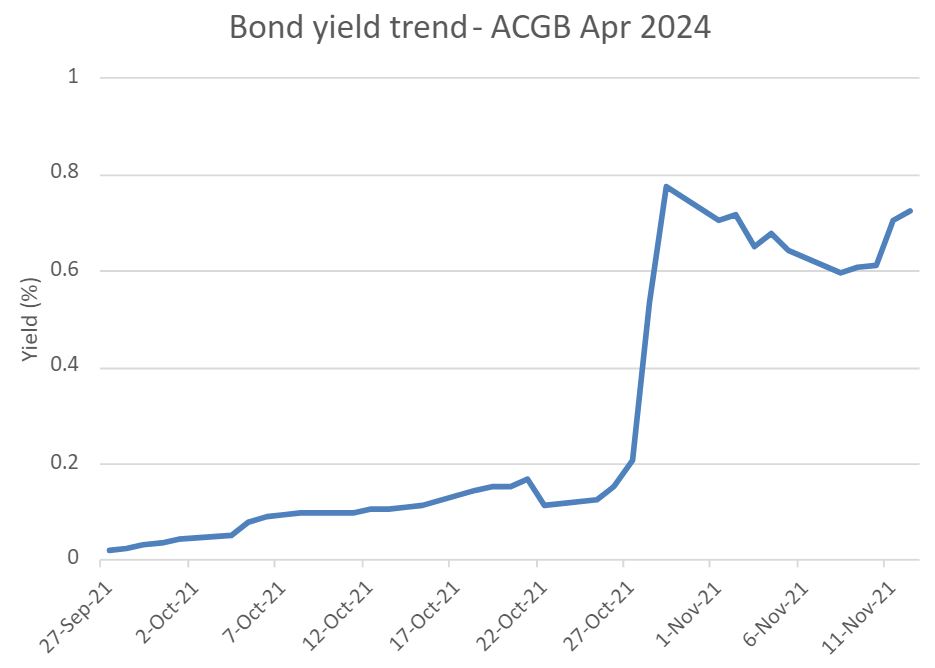

Bonds are settling down after a torrid October.

Markets have already priced decent hikes.

For our upcoming Australian Quarterly report I am writing a piece on what would be needed to push bond rates up significantly from here in the medium term.

Stay tuned.

About Tim Hext and Pendal’s Income & Fixed Interest boutique

Tim Hext is a Pendal portfolio manager and head of government bond strategies in our Income and Fixed Interest team.

Tim has extensive experience in banking, financial markets and funding including senior positions with NSW Treasury Corporation (TCorp), Westpac Treasury, Commonwealth Bank of Australia, Deutsche Bank, Bain & Co and Swiss Bank Corporation.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia.

Find out more about Pendal’s fixed interest strategies here

About Pendal

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

In 2023, Pendal became part of Perpetual Limited (ASX:PPT), bringing together two of Australia’s most respected active asset management brands to create a global leader in multi-boutique asset management with autonomous, world-class investment capabilities and a growing leadership position in ESG.

Here are the main factors driving the ASX this week according to portfolio manager Jim Taylor. Reported by portfolio specialist Chris Adams

THE market continues to question the notion of “transitory” price pressures.

But it’s remarkable how quickly equity markets have rebounded from recent shocks around inflation.

Stronger-than-anticipated US inflation data last week drove market volatility and a rare down-week for US equities. The S&P/ASX 300 lost 0.04% and the S&P 500 was off 0.27%.

There was also some movement in China. Beijing may be looking to ease pressure on the property sector, which prompted a rebound in the iron ore space.

The market remains focused on the risk of China over-tightening monetary, fiscal and regulatory policy settings, so signals that may mitigate this risk have been well received.

The Chinese Communist Party’s sixth plenum last week appears to have paved the way for indefinite leadership by Xi Jinping.

Covid and vaccines

We are seeing a sharp rise in case numbers in Germany. But as in other similar waves, hospitalisations so far remain under control.

Other European counties are also seeing an increase in cases. Denmark, Austria and the Netherlands are looking at reintroducing some mobility restrictions in response.

Otherwise there was little new to note last week.

Macro and policy

US

However you want to slice and dice the inflation data, the key takeaway is that we are looking at 30-year highs.

US CPI grew 0.9% month-on-month — versus 0.6% consensus expectations — and is running at 6.2% year-on-year.

The core data (ex food and energy) rose 0.6% month-on-month versus 0.4% expected. It is running at 4.6% year-on-year.

A rebound in Covid-affected sectors such as auto and hotel prices helped lift both the headline and core readings, but the breadth of excess inflation pressures continued to increase.

Services inflation will be keenly watched as the US economy re-opens. So far it remains in its 10-year band, but has experienced strong recent momentum.

Core CPI will peak at 6.9% in March 2022 according to consensus expectation at this point. This leaves plenty of scope for the market to continue testing the Fed’s “transitory” line in coming months.

Australia

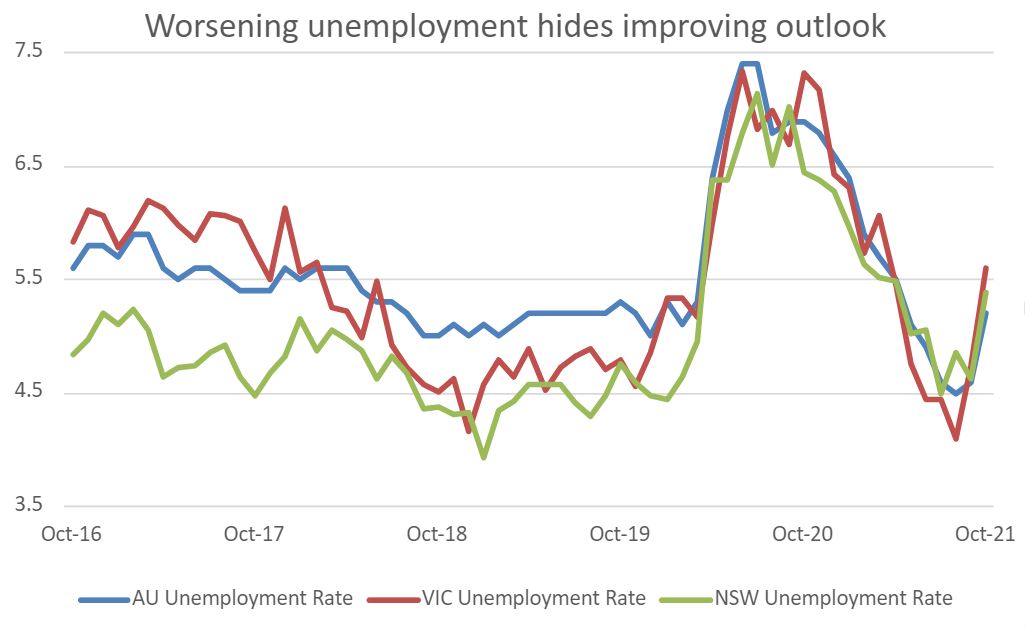

In Australia, employment declined 46.3k in October while the unemployment rate rose 60bp to 5.2%. This was weaker than expected, but the outcome largely reflected measurement issues related to recent lockdowns.

Elsewhere a strong rebound in company forward orders augers well for growth as we emerge from lockdowns.

China

The slowdown in credit may have bottomed in China. October is showing credit growth, potentially improving confidence for the rest of the year and into 2022.

After recent sharpening of concerns over property there are reports that the People’s Bank of China may introduce several measures to ease pressure on the sector. These include:

- Excluding merger and acquisition loans from the “Three Red Lines” that govern leverage in the property sector, allowing companies to acquire assets from stressed firms such as Evergrande

- Easing restrictions on development loans, which should reduce cash flow pressure on developers

- Extending existing bank loans

Elsewhere, approval of Xi’s doctrine on Chinese Communist Party history — the first in 40 years — at the sixth plenum seems to set the stage for Xi to retain power indefinitely.

Markets

Australian ten-year government bond yields largely held on their 30bp rally from the previous week.

The US equivalent yields rose 11bps to 1.56% on the inflation data, but remain well below recent highs.

Sustainable and

Responsible Investments

Fund Manager of the Year

The inflation print saw the gold price gain 2.8%.

News of potentially looser policy in China prompted good gains among commodity stocks, though the prices of iron ore (-4.9%) and copper (+2.4%) remained more subdued.

It was a disappointing season for the banks in the sense that all missed consensus pre-provision profit expectations.

ANZ (ANZ) slightly missed due to costs and NAB missed by 2% given weak markets. Westpac (WBC) missed by 17% given a sharp hit to net interest margins (NIMs) and higher costs.

Key themes across the results included:

- Mortgage NIMs remain under pressure from competition and changes in product mix, as highlighted by WBC. A focus on price-driven strategies via third-party distribution has led to profitless growth. Business banking NIMs appear to have held up better. The tailwind from lower deposits and funding appears to have largely played out.

- Credit growth is strengthening. All banks (ex ANZ) are enjoying the housing boom, though this should peak in coming months. NAB and CBA are starting to see a recovery in business lending which is a very encouraging sign. Institutional activity is increasing, while NZ credit keeps expanding. Growth is becoming broader based.

- The markets and trading-based divisions have been weaker, outside of Australian and New Zealand.

- All banks recommitted to their cost-out programs, however the market remains very sceptical on success here.

- Asset quality was very benign with every bank reporting negative credit charges.

- All banks beat expectations in terms of capital positions, reporting strong balance sheets.

About Jim Taylor and Pendal Focus Australian Share Fund

Drawing on more than 25 years of experience investing in top-performing Australian companies and a background in accounting, Jim manages our Long/Short Fund and co-manages our Imputation Fund. He is a Chartered Accountant with membership of the Australian Institute of Chartered Accountants.

Pendal Focus Australian Share Fund is managed by Crispin Murray. The fund has beaten its benchmark in 12 years of its 16-year history (after fees), across a range of market conditions. Find out more about Pendal Focus Australian Share Fund here.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

A weekly income and fixed interest snapshot from Pendal assistant portfolio manager ANNA HONG

FOR ALMOST two years economic data points have been accompanied with lockdown disclaimers — pre-lockdown, post-lockdown, back into lockdown.

Hopefully 2022 brings more incisive data as high vaccination rates put the lockdowns behind us.

The headline unemployment numbers released yesterday briefly shocked the market.

Positivity from the end of lockdowns was briefly snuffed out as the Australian unemployment rate jumped from 4.6% to 5.2% — much higher than the market consensus.

That was until we got to the fine print at the end.

The release was backward looking and reflected job numbers from Sep 26 to Oct 9.

Find out about

Pendal’s Income and Fixed Interest funds

That’s before NSW came out of lockdown — much less Victoria — which meant unemployment numbers in VIC and NSW dragged the national number higher.

Moreover, most borders were still shut as state policies outweigh federal.

That meant tourism-related industries in Queensland were affected, while states less reliant on tourism such as WA and NT saw an improvement in unemployment.

So the glass is half full, given those were essentially lockdown unemployment numbers.

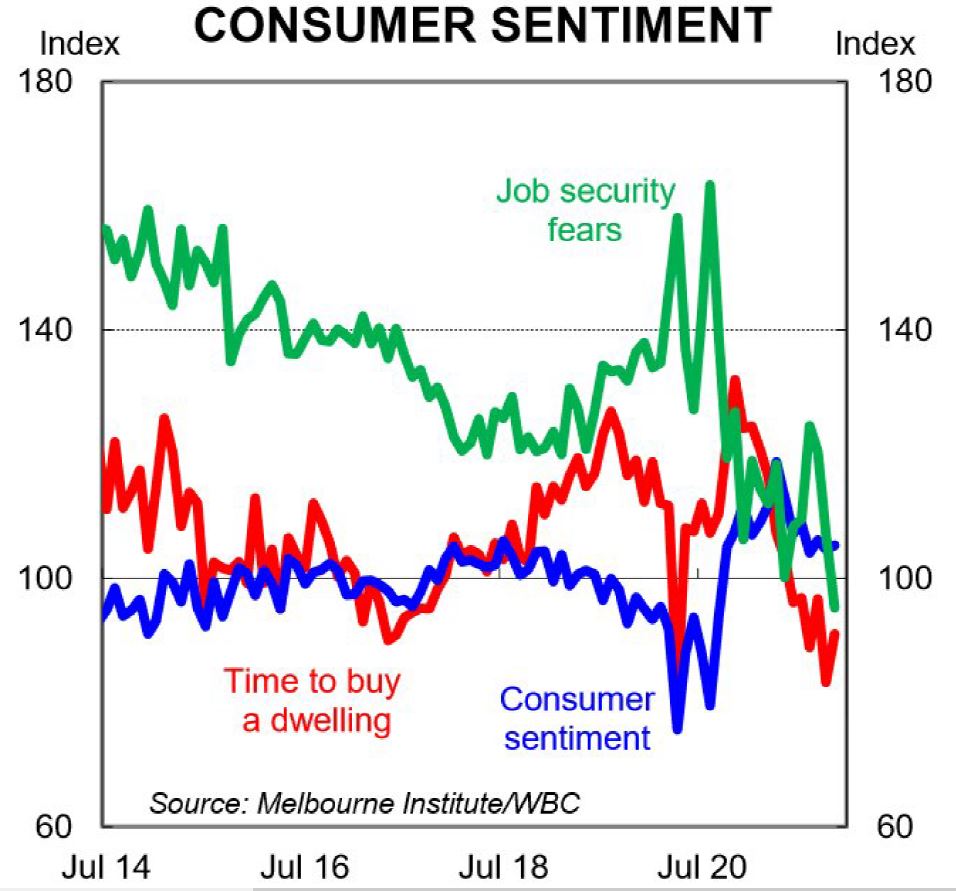

Furthermore, the consumer sentiment numbers around job security fears are at their lowest in more than seven years.

That’s evidenced by the labour turnover in NSW, which showed signs of better health as many workers switched jobs for better opportunities and better pay.

The economic outlook gets better as we add improving consumer spending intentions to the mix.

Higher spending in good, services and dwellings will help the states’ bottom line with stamp duty receipts and GST handouts from the federal government.

Market moves

Globally, most CPI numbers printed higher than consensus.

Yields rose due to global sentiment around inflation.

Australia’s unemployment number miss did not shift the yields significantly.

Market Implications

Short-end cash maintains its slight curve with six months BBSW still holding its ground above the RBA cash rate of 10bps.

Semi-government spreads have widened with issuances now coming through at close to its historical spread of +50bps to commonwealth government bonds.

The recently tendered TCV 2034 is now trading at +48bps to CGL. As semi spreads normalise the accruals can once again provide a healthy income to investors.

Additionally, the improving Australian economy will result in higher tax receipts.

Potentially that will improve the states’ finances and be supportive of semis on reduced supply.

About Anna Hong and Pendal’s Income and Fixed Interest team

Anna Hong is an assistant portfolio manager with Pendal’s Income and Fixed Interest team.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia. In 2020 the team won the Australian Fixed Interest category in the Zenith awards.

With the goal of building the most defensive line of funds in Australia, the team oversees A$22 billion invested across income, composite, pure alpha, global and Australian government strategies.

Find out more about Pendal’s fixed interest strategies here

About Pendal Group

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Renewable energy and battery-powered cars grab attention in the climate change debate. But tougher, “hard-to-abate” sectors may be more important for sustainable investors. Pendal’s RAJINDER SINGH explains

- Challenging or “hard-to-abate” sectors offer opportunity for sustainable investors

- These include agriculture, airlines, steel and cement

- Climate change “not just about fossil fuels”

YOU’VE probaby heard sustainable investment experts describe some industries as “hard to abate”.

Abatement means reducing the intensity of something unpleasant.

Climate-change experts refer to sectors such as cement, steel, air travel and agriculture as “hard to abate” because they lack obvious, cost-effective carbon-reduction solutions.

That’s a problem since these sectors make up more than a third of the world’s carbon emissions. Finding solutions in “hard-to-abate” sectors is critical to meeting net zero commitments — which makes them interesting to investors.

The fact they are largely overlooked in government policy and public debate may indicate there are opportunities for investors seeking to help create a better planet.

“Tackling climate change is not just about fossil fuels,” says Rajinder Singh, who manages several Pendal sustainable funds.

“There are some really difficult things we need to solve — things like airlines, cement, steel, agriculture and a wide range of industrial processes are significant carbon emitters.

“They are going to exist in 2050 and beyond and they are going to take time to solve.”

Singh says solutions for some of the trickiest questions about greenhouse gas emissions in these sectors are only beginning to emerge and sustainable investment success requires working with companies to solve these hard-to-abate sectors.

Find out about Pendal Sustainable Australian Share Fund

“It demonstrates the value of active ownership,” says Singh. Unlike most ETF or passive fund managers, active investment managers such as Pendal are run by managers who engage with companies to influence positive change.

“As a sustainable investor, you can’t just buy an ETF that owns all the good stocks and excludes the bad stocks. You have to work with companies and help with the transition.”

Solving the air travel problem

Airlines are one of the industries at the early stages of solving for net zero.

Batteries are unlikely to provide a solution for long-haul travel because of their weight, though short-haul electric airplane trips are feasible.

As a result, airlines are experimenting with biofuels — jet fuel made from renewable sources like plants or waste.

“But it has to be done sustainably,” says Singh. “You can’t divert agricultural products that would ordinarily be used for food,” says Singh.

In the meantime, the opportunity for airlines is in improving fuel efficiency by optimising routes and investing in more efficient planes.

Green cement

Another hard-to-abate sector that investors are seeking answers for is the cement used to make concrete.

“It’s in the basic chemistry — heating the raw materials releases CO2. That’s how concrete has been made for thousands of years,” says Singh.

Investments in technology solutions are showing promise. Trials are underway to capture carbon emissions in the concrete itself, trapping it and preventing it entering the atmosphere.

Fly ash — ironically a waste product from burning coal — is used to replace cement in concrete, dramatically reducing carbon emissions.

Other hard-to-abate areas include industrial processes that require high heat such as steel production or making bricks in a kiln.

Hydrogen offers a potential solution here although there is a long road of capital investment and trials ahead.

Sustainable and

Responsible Investments

Fund Manager of the Year

Risks and opportunities

These are important issues for investors to understand, says Singh.

“There is a cost in terms of capital that needs to be invested — over and above the regular business-as-usual investment.

“Steel companies need to spend tens or hundreds of millions of dollars investigating technologies and implementing in existing operations.

“If they’re going to spend shareholders money, we want to have a return based on that.

“Some of that return may be a green premium — but it may also simply be that you need to spend the money just to stay in business.”

Singh says investors seeking to create a sustainable investment portfolio — and genuinely impact the future — need to stay close to companies at the cutting edge of change in these hard-to-abate areas and resist the temptation to just divest.

“How can you own a mining company in a sustainable fund? Well, if you think about what a sustainable company fund is trying to do, it is investing in a society that is better.

“If you want to have electric vehicles, solar panels and a green electricity grid, you’re going to need metals like steel, copper and lithium.

“So, you want to invest in those companies that are providing those materials in the most sustainable way — what are the emissions, but also, what does workplace health and safety look like and how are they treating indigenous land holders?

“Mining is not bad. We just want sustainable mining.”

About Rajinder Singh and Pendal’s responsible investing strategies

Rajinder is a portfolio manager with Pendal’s Australian equities team. He has more than 18 years of experience in Australian equities.

Rajinder manages Pendal sustainable and ethical funds including Pendal Sustainable Australian Share Fund.

Pendal offers a range of responsible investing strategies including:

- Pendal Sustainable Australian Share Fund

- Crispin Murray’s Pendal Horizon Fund

- Pendal Sustainable Australian Fixed Interest Fund

- Pendal Sustainable Balanced Fund

- Regnan Credit Impact Trust

- Regnan Global Equity Impact Solutions Fund

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Responsible investing leader Regnan is part of Pendal Group.

The federal government estimates $20 billion of funding is needed to hit net zero emissions by 2050. But it could be triple. TIM HEXT explains what that means for investors

You probably don’t spend much time pondering our federal and state government arrangements.

But after running the NSW debt program for ten years as a general manager of TCorp (NSW Treasury Corporation) — which involved regularly explaining the arrangements to offshore investors — I know state governments are more important than federal governments.

The only reason people gathered on the sheep paddocks of southern NSW in the first place was to discuss defence and foreign affairs.

Covid has demonstrated the importance of the states to the population. In day-to-day life, Australians now should well understand that premiers are more important than prime ministers.

Therefore it’s interesting to watch Prime Minister Morrison trying to reclaim ascendency in recent times, as we move towards a federal election due by May.

Whether it be vaccine rollouts, new infrastructure and now climate policy, the prime minister’s main job seems to be repackaging state initiatives as his own.

That’s nothing new. But it appears people are now onto it — and the spin doctors are having to work harder.

Why does this matter for investors?

Well, the states are like you and me. They have to either earn or borrow money to spend it. They must live within their means.

On the other hand, the federal government — via the Reserve bank — has the ability to create money. They don’t need to borrow or earn it. The only constraint on federal spending is inflation.

Pendal Sustainable Australian Fixed Interest Fund

An Aussie bond fund that aims to outperform its benchmark while targeting environmental and social outcomes via a portion of its holdings.

Central bankers and economists used to push back on this. But after the past two years the cat is out of the bag.

Now the challenge is how to finance all the required climate initiatives.

Federal/state fiscal arrangements are complex — and in the relatively new area of climate policy thay are largely untested.

The federal government’s “Technology Investment Roadmap” estimates $20 billion of funding is needed to hit net zero emissions by 2050.

The cost may be closer to $60 billion based on estimates from countries that are less optimistic on the whole technology vibe.

I suspect much of this will come via guarantees of private projects rather than direct funding.

This is the European model and leads the world. Projects would need backing from the federal government, though, since state funding is already stretched.

Let’s hope federal and state governments can get back on the same page and work out a joint approach to climate policy.

States are already leading the execution, but the federal government will need to step up and do the heavy lifting on financing. (They already have the Australian Renewable Energy Agency and the Clean Energy Finance Corporation in place.)

Otherwise state credit ratings will deteriorate and the federal government will end up footing the bill anyway.

This is an increasing focus for us when assessing the credit ratings of semi governments and the positioning in our government bond portfolios.

We have also recently finished our wider ESG assessment of the states and will publish a piece on this in our upcoming Australian Quarterly.

About Tim Hext and Pendal’s Income & Fixed Interest boutique

Tim Hext is a Pendal portfolio manager and head of government bond strategies in our Income and Fixed Interest team.

Tim has extensive experience in banking, financial markets and funding including senior positions with NSW Treasury Corporation (TCorp), Westpac Treasury, Commonwealth Bank of Australia, Deutsche Bank, Bain & Co and Swiss Bank Corporation.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia.

Find out more about Pendal’s fixed interest strategies here

About Pendal

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

In 2023, Pendal became part of Perpetual Limited (ASX:PPT), bringing together two of Australia’s most respected active asset management brands to create a global leader in multi-boutique asset management with autonomous, world-class investment capabilities and a growing leadership position in ESG.

Regnan Global Equity Impact Solutions Fund – Class R (APIR: PDL4608AU, ARSN: 645 981 853)

On 9 August 2021, the designation of this class of units was changed from ‘Class A’ to ‘Class R’. The name of the Fund did not change and there were no changes to the terms of the class or your rights as an investor in the class.

What do you need to do?

No action is required. You will be able to continue to invest or withdraw from the Fund.

An updated Product Disclosure Statement (PDS) was issued on 9 August 2021 and made available on www.pendalgroup.com.

Pendal Concentrated Global Share Fund Hedged – Class R (APIR: RFA0031AU, ARSN: 098 376 151)

On 23 September 2021, the existing units of the Pendal Concentrated Global Share Fund Hedged (Fund) were reclassified as ‘Pendal Concentrated Global Share Fund Hedged – Class R’. The name of the Fund did not change and there were no changes to the terms of the class or your rights as an investor.

What do you need to do?

No action is required. You will be able to continue to invest or withdraw from the Fund.

An updated Product Disclosure Statement (PDS) was issued on 23 September 2021 and made available on www.pendalgroup.com.