- Actively managing credit macro risks is critical

- Inflation and vaccine roll-out are focus areas

- Bulls outweigh the bears – but for how long?

ONE OF THE greatest challenges running any portfolio is when to de-risk. When should a manager decide to change tack and become more defensive?

It’s the same for all asset classes, including credit markets which are often thought of as “low risk”.

In fact, losses in credit markets do occur — and can be very painful for investors — which means the right risk profile is even more critical in fixed income funds trying to achieve target returns.

“If you have a credit portfolio that’s trying to outperform by 2% versus a benchmark over a full year, and you lose 1% in a month, that’s a very bad outcome,” says George Bishay, Pendal’s portfolio manager of Income and Fixed Interest.

Bishay uses the example of March last year when financial markets collapsed. An average credit fund aims to outperform the benchmark by 2% over a year — but many lost 4% in one month.

Risk, and the appetite of a credit fund manager for risk, is reflected in the weighted average maturity (WAM) of their portfolio. A longer WAM is reflective of a bullish credit outlook. A shorter WAM suggests a bearish outlook.

When actively managing a credit fund, it’s important to be more defensive during volatile times, such as March last year.

Right now, credit spreads offer value in a low interest rate environment and Bishay has reflected this in his credit portfolios.

“It comes down to macro factors,” he says. “The huge amount of fiscal stimulus that we’ve had is powerful. That stimulus supports employment and ensures the economy doesn’t fall in a heap.”

“Then there’s an incredible amount of monetary policy stimulus that supports liquidity in the system. The cash rates around the world are near zero and because of that investors are chasing yield, which is supportive for credit markets,” Bishay says.

“You also have global company earnings being revised up.”

US corporate earnings, and what happens on Wall Street, has a big influence on local credit market pricing. The local credit market is correlated with US credit markets. And US credit markets reflect what’s happening in US equity markets.

A rally in US equities tends to prompt a rally in US and AUD credit spreads.

Find out about

Pendal’s Income and Fixed Interest funds

“I’m focused on US equities,” Bishay says.

While the roll-out of vaccinations around the world adds to his argument for accepting greater risk in credit markets, it could quickly become a negative.

“COVID cases are picking up globally, but so are vaccination rates. We know if you get vaccinated you are less likely to transmit coronavirus and less likley to end up in hospital or die. But we don’t know the exact numbers,” Bishay explains. “We don’t really know the accuracy of the trial efficacy rates of vaccines. We don’t yet have the full picture.”

“The vaccination roll-out supports the stronger macro view, but it is also a risk.”

Bishay says the other major risk is a disorderly rise in interest rates. “What if there’s a jump in interest rates because inflation proves not to be transitory and is higher than expected? That’s a risk.”

But for now, the bull case over-rides the bear case. But as Bishay puts is: “I’m constantly focused on when to de-risk the portfolio.”

About George Bishay and Pendal

George Bishay is a portfolio manager with Pendal’s Bond, Income and Defensive Strategies team.

Led by Vimal Gor, Pendal’s BIDS boutique is one of the most experienced and well-regarded fixed income teams in Australia. In 2020 the team won the Australian Fixed Interest category in the Zenith awards.

The team oversees $22 billion invested across income, composite, pure alpha, global and Australian government strategies with the goal of building Australia’s most defensive line of funds.

Find out more about Pendal’s fixed interest strategies here

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

- Tech and education crackdown sends Chinese shares falling

- China government aims to ease cost of living pressures

- Questions over risk-reward balance for investors

CHINESE regulators this week outlined reforms that will ban private firms that teach the school curriculum from generating profits, raising capital or going public.

The move was aimed at reducing cost-of-living expenses for Chinese familes, who are now encouraged to have three children.

The changes caught investors by surprise. Shares in Chinese private education companies inside and outside the country plummeted.

But this policy shift also has potential implications for a number of Australian-listed companies, in areas such as infant formula.

“There’s two interesting aspects here,” says Elise McKay, an analyst in Pendal’s equities team.

“First of all, China needs to address its population problem.”

“New births have fallen off in China to the lowest level since the famine in 1961. Women of child-bearing age are having fewer children and the population is ageing. This causes real issues.”

“COVID has accelerated this because some people are putting off pregnancy while they get vaccinated or to avoid getting COVID while they are pregnant.”

“The new policy is to lower the cost of raising a child and boost birth rates. They also want to reduce inequality amongst those who can afford to pay for after school tutoring and those who cannot,” says McKay.

Lifting China’s birth rate is potentially good news for businesses that sell to Chinese families, including Australia’s high-profile suppliers of infant formula.

However there is a second aspect to this shift.

“There’s also this increasing uncertainty around regulation, particularly in public companies,” says McKay.

“We need to watch for signals of regulation around pricing for infant formula – this also affects the cost of rearing children.”

Pendal Focus Australian Share Fund

A high-conviction equity fund with 16 years of strong performance in a range of market conditions

“We may also see China look to prioritise domestic brands.”

There are several recent examples of greater intervention in markets. The move in education comes after similar crackdowns in technology, payments and ride-hailing.

A high-profile investigation into ride-hailing firm Didi’s handling of customer data that halved the newly-listed company’s share price.

And it follows a regulatory inquiry into tech giant Alibaba earlier this year that scuppered the float of its payments arm Ant.

A higher birth rate could be an opportunity for Australian companies. But the prospect of more regulation and the prioritisation of domestic brands may shift the balance of risk against investors.

“It’s very nuanced,” says McKay. “And it’s a case for actively managing risk. It is a development that we will be watching very closely.”

About Elise McKay and Pendal

Elise is an investment analyst with Pendal’s Australian equities team. Elise previously worked as an investment analyst for US fund manager Cartica where she covered a variety of emerging market companies.

She has also worked in investment banking and corporate finance at JP Morgan and Ernst & Young.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Find out about Pendal Focus Australian Share Fund here.

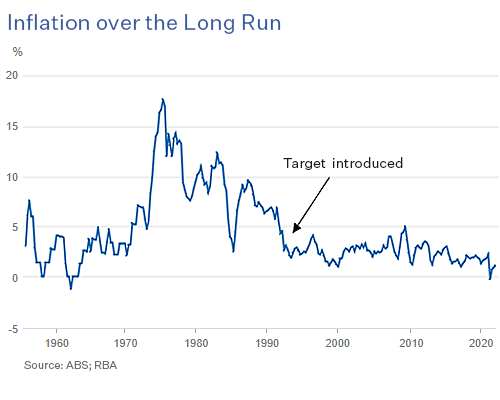

The biggest question in local and global financial markets is no longer about the COVID pandemic. It’s about inflation and whether it will stick around.

- The current bout of inflation is more than transitory.

- RBA models have a bias toward low price rises.

- Mortgage rates likely to start drifting higher

CENTRAL BANKS around the world acknowledge that the global economy is in the midst of a bout of inflation. Most argue it’s transitory, driven by supply-side effects that will dissipate later in 2021.

But has the Reserve Bank of Australia, and its peers, got it wrong?

Quite possibly, says Tim Hext, portfolio manager in Pendal’s Bond, Income and Defensive Strategies team.

“We think that inflation and wages will come back to the RBA target range a lot quicker than the Reserve Bank thinks.”

One of the reasons for the central bank’s potential misreading of the economy is because it forecasts inflation using a model developed about five years ago, which picks up on inflation expectations, Hext says. And expectations over recent years have been low.

“So the model says … the best guide to future inflation is past inflation, because of people’s expectations. It says businesses will be slow to increase prices and consumers won’t be expecting inflation to be a problem. It has a bias in it.”

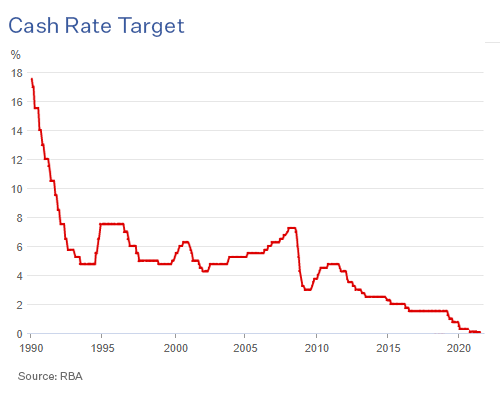

Another reason for the likelihood of the official cash rate rising sooner than the RBA’s current forecast of 2024 is because it came out so publicly about rates remaining low in an effort to stem the downturn in the economy.

“The Reserve Bank is like a big oil tanker. It takes time to turn around,” Hext says. “After providing strong guidance last year, everything in the economy started improving.

“It’s gotten to the point where they’re now using inflation to fit their narrative, as opposed to building their narrative around inflation.”

“It suits them to use the inflation figures [which are very low], but you have to remember that inflation lags the economy by 12 to 18 months. The economy started to pick up in the middle of last year, so I expect to see inflation at the end of this year,” Hext says.

He doesn’t support the view that the supply-induced price rises, currently apparent in the economy, are transitory.

“You’re going to see goods prices squeezed and businesses are in a pretty good position to pass on the cost increases. The data is already showing that in the US.

“And services inflation, which is more important than goods inflation, is exposed to labour markets. Labour is the primary input into services. And the labour market is going to get a lot stronger. It’s likely to be near four per cent this time next year.”

The oil tanker, as Hext puts it, will have to start turning.

Find out about

Pendal’s Income and Fixed Interest funds

The first thing the Reserve Bank did was switch off the term funding facility for banks at the end of June, thereby denying lenders a cheap source of funds, Hext says.

They have also announced a taper of quantitative easing by reducing purchases of government bonds from $5 billion a week to $4 billion a week in September, although recent lockdowns may see that timing pushed back.

And finally the central bank will have to lift the official cash rate, which is used to price other lending rates.

Hext says the term funding facility played as big a role on interest rates for mortgages on the way down and is likely to do so on the way back up.

“The money the banks borrow [to lend to customers] will be at a higher rate once the funding facility ends. It will take time to work through the system, but the overall cost of funding for banks will go up. And mortgage rates will start drifting higher.”

The spectre of inflation is back, and as Hext puts it, the Reserve Bank oil tanker might need to turn just a bit faster.

About Tim Hext and Pendal’s Income and Fixed Interest boutique

Tim Hext is a portfolio manager with Pendal’s Income and Fixed Interest team.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia. In 2020 the team won the Australian Fixed Interest category in the Zenith awards.

With the goal of building the most defensive line of funds in Australia, the team oversees A$22 billion invested across income, composite, pure alpha, global and Australian government strategies.

Find out more about Pendal’s Income and Fixed Interest strategies here

About Pendal Group

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Here’s what’s driving Australian equities this week according to Pendal’s head of equities Crispin Murray. Reported by portfolio specialist Chris Adams.

ALTHOUGH the ASX is touching new highs, equity markets continue to grapple with a slowdown in economic growth and potential implications of the Delta variant.

The sell-off on July 19 reversed late last week as US earnings continued to show strength and M&A activity supported the local market. The S&P/ASX 300 rose 0.6% last week and the S&P 500 was up 2%.

Despite growing uncertainty, the underlying foundations of fiscal stimulus and abundant liquidity continue to win out.

COVID and vaccines

British data continues to show a disconnection between the rise in new Delta-strain Covid cases and the resulting rate of hospitalisations.

Initial signs of a decline in new UK cases provide grounds for optimism, though new cases are expected to pick up as restrictions are removed.

There are also signs of stabilisation in new cases elsewhere — including Spain, Malta and Indonesia which have all experienced a surge in Delta infections.

On the negative side, it is becoming apparent that even well-vaccinated countries will experience a Delta-driven wave.

In the US we are not seeing a disconnection to the same extent as the UK. New cases are up 56% week-on-week and hospitalisations have risen 36%. This may reflect lower testing rates and a higher proportion of unvaccinated people. Data shows that fewer than 3% of hospital admissions are vaccinated.

The big issues are Delta’s effect on government policy, the potential for on-going restrictions and the need for booster doses. The reality is that we don’t have answers at the moment.

Find out about

Pendal Focus

Australian Share Fund

Crispin Murray,

Head of Equities

We are seeing increased hospitalisations in Israel – albeit off a low base and well below the previous wave.

The sample size is small and there are complexities related to age, but this may suggest vaccines become less effective in terms of infection and hospitalisation over time. This could mean some restrictions will remain in place even after countries move to re-open.

The issue of “breakthrough” infections in people who have been vaccinated poses a difficult issue for Australia, given low political tolerance for any degree of community infection.

The concept of herd immunity is getting difficult to pursue and may require some pivot in approach. There remains potential for policy confusion and further delays in re-opening of borders.

In Australia the news has been mixed. There are signs that Victoria will be able to re-open to a degree, while Sydney is facing an extended lockdown.

The market is focused on economic implications. We may see the RBA signal an extension of tapering given the change in economic momentum. There will be a lot of focus on potential for government stimulus.

Economics

Some indicators suggest the second derivative of growth – the rate at which it is growing – has ticked over. This is unsurprising: the speed of economic recovery could not be maintained.

Nevertheless, this is some causing some concern in markets, particularly in combination with the Delta strain.

History suggests that when the second derivative of growth turns, this marks the beginning of a phase where disappointments are more likely and earnings revisions are negative.

But the unique nature of this cycle may offer a counter-argument.

Normally slowing economic momentum is a function of some form of policy action. For example in 2018 Fed tightening clearly prompted the slowdown. This time slowing momentum is a function of the unprecedented growth rate triggered by the Q1 US stimulus.

The bullish case for cyclical stocks says there is currently no policy tightening; no prospect of rates rising; and tapering is increasingly likely to be pushed into 2022.

2021 Money Management of the Year Awards

Pendal Australian Shares Portfolio

Winner – SMA Australian Equities

Pendal Property Investment Fund

Winner – Australian Property Securities

The bear case says the Fed will face a quandary with slowing economic momentum yet high inflation — and may end up tapering into a weaker economy.

We tend towards the bull case at this point. Slowing economic momentum would likely ease inflationary pressures as well. All the evidence of the past 18 months suggests governments are pro-growth and will react with more policy stimulus.

Clarity on this issue is unlikely before Q4 2021. By then we’ll have seen the end of the US summer break and unemployment insurance payments trailing off. At this point we’ll potentially see job growth reaccelerating.

Until then, we could see the current rotation to more defensive, quality, bond-sensitive stocks persist.

Markets

Equity markets continue to rise despite concerns over Delta and the slowing pace of growth, although breadth has narrowed.

Liquidity and low rates continue to act as backstops. The combined balance sheet of the Fed and European Central Bank continues to expand at more than US$100 billion a week.

US earnings season is good so far. Earnings revisions have the potential to shift the S&P 500 price/earnings ratio from 22x to 20x. The next two weeks will be important to watch in this regard.

Australia’s upcoming earnings reason will not be as buoyant as the US and guidance will be subdued. But the prospect of a weaker Australian dollar, delayed monetary tightening and potential for fiscal stimulus should continue to support the market.

Last week rotation continued into defensives and quality. Health care (+4.6%) led alongside Consumer Staples (+2.1%). Energy (-1.8%) and Materials (-1.1%) underperformed.

Altium (ALU, -9.4%) was the weakest on the ASX 100. Management rejected a takeover offer from US company Autodesk, which then withdrew the bid.

Gold miners underperformed despite the market’s more defensive bent, as the gold price came off 0.7%. There was some news flow in the sector. Evolution (EVN, -9.4%) was weaker on a quarterly update that signalled lower production and higher capex in the near term as they accelerate longer-term project development.

The stock fell, but rebounded as management raised capital to buy an asset from Northern Star (NST, -6.0%) which will help increase utilisation and extend the life of its Mungari mill in Western Australia. The deal makes sound strategic sense, though the timing of the capital raise could have been better.

Crown (CWN, -8.4%) continued to wallow in the wake of the Victorian Royal Commission. Last week Star (-1.4%) withdrew its offer for CWN. There is still logic to a merger, but the three-month wait until the Commission’s outcome makes it hard to value the company.

Santos (STO, -6.1%) proposed a merger with Oil Search (OSH, +3.1%) which also makes strategic sense, given the impact that ESG is having on capital available in the sector. A merger would address a number of issues depressing OSH’s valuation rating and would offer cost synergies. The implied 10% premium proposed by STO may not be enough for OSH shareholders at this point.

BHP (BHP, -1.2%) delivered a decent quarterly production update, in contrast to Rio Tinto (RIO, -2.7%) where operating issues remain. There was speculation that BHP would combine some or all of its Australian oil and gas business with Woodside (WPL, -1.9%) in some form. This is complex given the difficulty of estimating reserves and arriving at a valuation in areas such as Bass Strait.

Health care stocks benefited from the rotation to quality and defensives. Fisher and Paykel Healthcare (FPH, +7.6%) did best.

CSL (CSL, +5.7%) was among the strongest ASX 100 stocks last week. It has lagged for some time over concerns around plasma collection in the US. The outlook here is improving.

Retailers were strong with Wesfarmers (WES) up 4.8% and JB Hi-Fi (JBH, +4.6%). JBH provided positive guidance, but we are cautious. Unlike previous lockdowns there is not the same support for retail spending.

Find out about Crispin Murray’s Pendal Focus Australian Share Fund

About Crispin Murray and Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia. Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Find out more about Pendal Focus Australian Share Fund here.

Contact a Pendal key account manager here.