We have updated and reissued the Product Disclosure Statements (PDSs) for the following classes of units in the Pendal Global Select Fund (the Fund), effective on and from Friday, 28 June 2024:

- Pendal Global Select Fund – Class R

- Pendal Global Select Fund – Class W

- Pendal Global Select Fund – Class Z

The following is a summary of the key changes to the PDSs.

ESG disclosure

We have removed the Responsible Investment Association of Australasia (RIAA) certification symbol, as the Fund is no longer RIAA certified. We have also provided clarification that exclusionary screens are not applied to the Fund’s investments in cash or derivatives and that the use of derivatives may result in the Fund having indirect exposure to the excluded companies from time to time

There has been no change to the Fund’s investment approach, or the exclusionary screens employed by the Fund.

Updates to significant risks disclosure

The Fund’s investment strategy involves specific risks.

We have updated the significant risks disclosure applicable to the Fund to ensure that our disclosure continues to align with the nature and risk profile of the Fund and the current economic and operating environment.

Updates to ongoing annual fees and costs disclosure

The estimated ongoing annual fees and costs for the Fund has been updated to reflect financial year 2023 fees and costs. These include changes to estimated management costs and estimated transaction costs.

We now also disclose the maximum management fee we are entitled to charge under the Fund’s Constitution.

Additional information on how to apply for direct retail investors

We have provided additional information for non-advised retail investors (retail investors without a financial adviser) investing directly in Class R units of the Fund who may also be required to complete a series of questions as part of their online Application, to assist us in understanding whether they are likely to be within the target market for the Fund.

Updates to our complaints handling process

We have provided additional details about our complaints handling process and the Australian Financial Complaints Authority.

We have updated and reissued the Product Disclosure Statements (PDS) for the Pendal Sustainable Share Fund (Fund) on and from Friday, 28 June 2024.

The following is a summary of the key changes reflected in the PDS.

ESG disclosure

We have enhanced our ESG disclosure to describe the Fund’s sustainability objective, the sustainable themes Pendal focuses on when managing the Fund and the sustainability assessment framework employed by the Fund.

There has been no change to the way the Fund is invested.

Updates to significant risks disclosure

Each Fund’s investment strategy involves specific risks.

We have updated the significant risks disclosure applicable to the Fund to ensure that our disclosure continues to align with the nature and risk profile of the Fund and the current economic and operating environment.

Updates to ongoing annual fees and costs disclosure

The estimated ongoing annual fees and costs for the Fund have been updated to reflect financial year 2023 fees and costs. These include changes to estimated management costs and estimated transaction costs.

We now also disclose the maximum management fee we are entitled to charge under the Fund’s Constitution.

Additional information on how to apply for direct investors

We have provided additional information for non-advised investors (investors without a financial adviser) investing directly in the Fund who may also be required to complete a series of questions as part of their online Application, to assist us in understanding whether they are likely to be within the target market for the Fund.

Updates to our complaints handling process

We have provided additional details about our complaints handling process and the Australian Financial Complaints Authority.

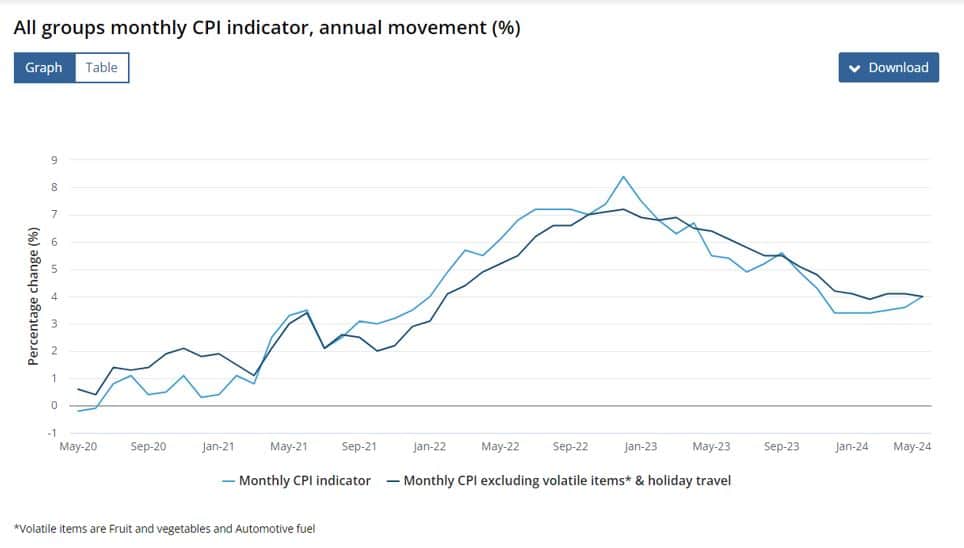

Will May’s monthly inflation data push the RBA to hike again? If it can be patient, says Pendal’s head of government bond strategies TIM HEXT, some relief is at hand

- Monthly CPI was higher than expected

- The annual inflation rate is around 4%

- Why bonds, why now? Pendal’s income and fixed interest experts explain

- Browse Pendal’s fixed interest funds

THE release of May’s monthly CPI data showed the annual inflation rate flatlining at around 4%. Excluding volatile items, it has – in fact – nudged higher this year.

Source: ABS – Monthly CPI Indicator

The word for inflation that springs to mind is stubborn. Too many items are significantly above the comfort zone.

Rents are 7.4%, insurance is 7.8%, and new housing construction and education are above 5%. Even tradables have picked up above 1%.

The higher monthly result was quite broad-based, though international travel had the biggest upside miss.

Underlying inflation is likely to print around 1%, which annualises at 4%. The RBA itself was expecting 3.8%.

You can see why many in the market are now calling for an August rate hike, though I’m not sure a 0.2% miss warrants another rate hike.

It’s what the RBA thinks that is important.

All eyes will now turn to the Q2 numbers out at the end of July, just before the RBA’s August meeting.

If our central bank can be patient, good news is at hand.

Subsidies will see inflation in Q3 nearer to 0.4% headline and 0.8% underlying. Recent minimum wage outcomes also point to wage relief.

While subsidies are temporary, and therefore dismissed by many, the second-round impacts are important. I also suspect the subsidies will be a more permanent feature in the transition economy.

Is this November all over again?

As the new RBA Governor, Michelle Bullock came in swinging on inflation last year – stating a low tolerance for upside surprises.

However, the Q3 inflation numbers surprised by 0.2%, putting the RBA in a corner and forcing it to hike in November.

Bullock has since avoided that phrase, now referring to vigilance on inflation. This leaves some optionality but will make the discussion at the August meeting very interesting.

It would be a brave call to hike.

The last time the RBA went against the global picture by hiking was in February and March 2008, which turned out to be major errors; there is usually some safety in the pack.

I think, given the international context where other central banks are cutting or leaning towards cuts, the RBA will sit out August and leave rates unchanged. This may be a close call.

Find out about

Pendal’s Income and Fixed Interest funds

The RBA currently expects trimmed mean (underlying) inflation to be 3.4% by year’s end. If we get another 1% in Q2 as we saw in Q1, it means the final two quarters will need to average 0.7%.

The second-round impact of subsidies may help the cause, but it will be a challenge.

What if the RBA does hike?

Politically, the government is hoping to fight the next election on cost-of-living relief and the Stage 3 tax cuts.

A rate hike would wipe out any feel-good impact from the electorate and put Governor Bullock on the front page like her predecessor.

This won’t stop her from hiking if needed, but if the case is not clear, caution may prevail.

A hike would only repeat what has gone on over the last 12 months.

Retirees and wealthy people get richer, younger middle Australia gets whacked again, and everyone sits around scratching their heads as to why rents and insurance – the prices of which move up, not down with rates – aren’t helping.

What about markets?

Markets have moved the odds of an August hike from around 20% to 60%.

Three-year yields are again above 4% (up 15 basis points) and ten-year yields are at 4.3% (up 10 basis points).

We will look for the odds to improve before leaning against these moves.

While we don’t expect a hike, it is not a confident view – meaning, entry levels are important.

For now, our duration remains at – or near – benchmark as we knew Q2 inflation would always be a hurdle markets would need to clear before a more significant rally later in the year.

About Tim Hext and Pendal’s Income & Fixed Interest boutique

Tim Hext is a Pendal portfolio manager and head of government bond strategies in our Income and Fixed Interest team.

Tim has extensive experience in banking, financial markets and funding including senior positions with NSW Treasury Corporation (TCorp), Westpac Treasury, Commonwealth Bank of Australia, Deutsche Bank, Bain & Co and Swiss Bank Corporation.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia.

Find out more about Pendal’s fixed interest strategies here

About Pendal

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

In 2023, Pendal became part of Perpetual Limited (ASX:PPT), bringing together two of Australia’s most respected active asset management brands to create a global leader in multi-boutique asset management with autonomous, world-class investment capabilities and a growing leadership position in ESG.

Pendal’s head of income strategies AMY XIE PATRICK joined Livewire Markets to answer some of the market’s quick-fire questions

- Why bonds, why now? Pendal’s income and fixed interest experts explain

- Browse Pendal’s fixed interest funds

PENDAL’S Amy Xie Patrick featured on Livewire’s Signal or Noise to discuss some of the burning topics impacting the Australian fixed income market.

Tune in to hear from Amy and fellow panelists Shane Oliver (AMP) and Michael Price (Ausbil) about the implications of a changing interest rate cycle, the future for term deposit returns, and why now may be the time for intelligent investors to consider some “out-of-consensus” income-paying opportunities.

See more on Livewire Markets

About Amy Xie Patrick and Pendal’s Income and Fixed Interest team

Amy is Pendal’s Head of Income Strategies. She has extensive expertise and experience in emerging markets, global high yield and investment grade credit and holds an honours degree in economics from Cambridge University.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia. The team oversees some $20 billion invested across income, composite, pure alpha, global and Australian government strategies.

Find out more about Pendal’s fixed interest strategies here

About Pendal Group

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

Here are the main factors driving the ASX this week, according to Pendal’s head of equities CRISPIN MURRAY. Reported by portfolio specialist Chris Adams

- Markets experience a moderate rally, led by growth

- Political fears in Europe weigh on bond markets

- Find out about Pendal Focus Australian Share fund

- Watch Crispin’s most recent Beyond the Numbers webinar

THE most constructive US inflation data this calendar year drove bond yields lower and helped the US equity market reach new highs last week, led by tech names.

The US Federal Reserve left rates on hold and was quite hawkish, signalling only one rate cut this year in its dot plots. However, the market wasn’t buying that given the better CPI print.

Apple’s developer day also helped tech sentiment; AI and all that it touches seems to be the only narrative that matters.

The S&P 500 gained 1.62%, but equity markets fell elsewhere.

The Euro STOXX 50 fell 4.17% on political concerns triggered by France’s snap election, while Japan’s TOPIX 500 was off 0.47% as the Bank of Japan struck a hawkish tone, possibly mindful of a weaker yen.

The S&P/ASX 300 fell 1.71% – led by Resources, with battery metals weaker and iron ore down again.

We also saw some FY25 downgrades feeding through the market, reflecting a softer economy.

Domestic employment data was better; underlying trends indicating a softening economy but nothing too severe and certainly no window for rate cuts. As with the US, the growth part of the market continues to outperform.

US: the Fed issues a hawkish statement that the market sees as backward-looking

Inflation

The headline Consumer Price Index (CPI) returned 0% month-on-month, versus the 0.1% expected.

The Core CPI measure was up 0.16%, which was well under the 0.3% expected and the lowest reding since August 2021.

This was well received by the market and supports the case that higher inflation data in recent months was tied to backward-looking factors, such as annual price hikes and insurance.

For example, half of the difference between the expected and actual Core numbers was related to insurance – which had been running at 15%-20% annual increases and turned negative in May – as well as lower airfares.

Some of these factors may partially unwind, but the signal is positive.

The preferred “super core” number – which excludes rent and owner’s-equivalent rent – fell 0.04% month-on-month, helped by Core services falling to 0.22%. Rent inflation does remain more persistent than expected.

The measures of “sticky” inflation, as measured by the Atlanta Fed Sticky Core CPI, are also falling materially.

This good news was compounded by lower Producer Price Index (PPI) data, with Headline falling 0.2% in May, versus expected growth of 0.1%. Core PPI was flat month-on-month, versus the 0.3% forecast.

This data can be used to project May’s Personal Consumption Expenditure Index (PCE) – the Fed’s preferred measure – coming in at 0.11% to 0.13% month-on-month, which is well below the 0.32% average in the first four months of the year.

Year-end expectations for annual PCE are being shaved down by 0.1% to 2.7%.

Inflation bulls believe the economy has slowed enough to reduce corporate pricing power and return to more traditional promotional activity which supports this lower year-end forecast.

Bonds rallied and the market has shifted back to two rate cuts in 2024 on this data.

Fed meeting and interest rates

The Fed left rates unchanged and issued a hawkish statement which saw the median dot plot of rate forecasts shift to imply only one rate cut in 2024.

Chairman Powell reinforced the notion that the Fed would need to see a series of better inflation data.

He also noted that the Fed had increased the non-accelerating inflation rate of unemployment (NAIRU) by 0.1% to 4.2% and that the unemployment rate would only impact its decision if it went above its expectations.

On face value this was negative, implying a higher bar for cutting rates.

However, while this happened after the CPI release, it was clear from the press conference that the latter had not been factored into the dot plot.

Given that eight members of the FOMC still expect two cuts – with Powell widely perceived as one of them – the inflation data trumped the Fed’s statement and the market moved to price in more cuts.

The implied probability of zero or one cut in 2024 has shifted from 55% on 7 June to 30%, with the chance of two or more cuts rising to 70%.

This has been good for bonds, which are now seeing positive signals in terms of technical price action.

It has also been important for equity sector rotation.

Finally, we note that the hit that Trump’s betting odds took following his conviction has unwound and the RCP Betting Average now has his chance of election back above 50%.

Pendal Focus Australian Share Fund

Now rated at the highest level by Lonsec, Morningstar and Zenith

Europe: political concerns weigh on bond markets

French President Macron’s snap election – which came after the right-wing National Rally (RN) trounced his own centrist grouping party’s in the European elections – triggered a mini bond crisis in Europe.

French bond spreads widened 25 basis points (bps), which cascaded through to EU periphery nations and raised concerns of a more general flight to safety.

The key concern is that RN have historically had policies which are market unfriendly, such as nationalising private roads, as well as looser fiscal settings as a result of tax cuts.

The reaction looks overdone at this stage, given the degree of unknowns.

We note that national parliamentary elections follow a very different structure, with two rounds of voting (occurring on 30 June and 7 July), and that it is also effectively 577 small elections – that is, local candidates running in a “winner beats all” approach.

Voter turnout will likely be a lot higher; there is apathy toward European elections as they have less bearing on day-to-day life. However, some potential outcomes include:

- Status quo, with a coalition of centre-right parties securing sufficient seats to run government.

- A hung parliament, which could end with either a minority far right, a centre left/right coalition, or a minority left-wing government.

- A right-wing majority, which concerns the market, but appears a lower risk at this point.

Fear is driving markets in the short term, as this was a risk that few were expecting. But on a probability basis, pricing looks to have gone too far.

It is a salient reminder of the unpredictability of politics and relevant given the upcoming US election.

Australia: stronger-than-expected jobs data underpins expectations of no rate cuts

Employment rose 40,000 in May versus the 25,000 expected – with full time employment up 42,000. Unemployment fell from 4.1% to 4.0%.

The underlying trends are slowing, with three-month annualised job gains at 25,000 versus 51,000 in April.

Hours worked also fell from the previous month, indicating slowing domestic activity.

All this paints a picture of an economy slowing, but not falling into a hole, and on track to delivered subdued growth.

This means rates look set to remain on hold for the balance of the year.

Markets: conditions suggest continued moderate rally led by growth stocks

The combination of lower inflation driving lower bond yields as well as subdued economic growth and falling pricing power limiting earnings growth, is supporting companies with their own earnings growth dynamic.

This is primarily US tech names and utilities on the AI power demand story.

Looking at year-to-date in the US, there are some interesting observations.

The divergence between the outperforming tech sector and the broad-based Russell 2000 has widened in the last seven weeks and accelerated further last week.

Japanese equities, which had been a leader this year as they reflected a more positive outlook for global growth, have begun to stall.

This highlights how the market is getting more wary of industrial earnings relative to tech – a view reinforced by the fact that the financial and industrial sector did not participate in the S&P 500’s breakout to new highs last week.

There is a lot of debate about the lack of breadth in the US market as a sign of building weakness in the rally. This is a fair concern as historically, breadth is a lead indicator of markets though the lag can take a lot of time.

The data on concentration is clear.

In 2019, one company moved to more than 6% of the S&P 500 – the first time this had happened in a data set running back to 1990. There are now three companies weighing more than 6%.

On a calendar-year basis, 2024 is second only to 2007 in terms of top ten index weight concentration in years with positive performance (76.5% concentration versus 78.7% in 2007). The year 1999 was another example of high concentration (54.5%) driving performance.

Both years led into bear markets.

However, looking at the ten historical instances in which 40% or more of S&P 500 calendar year returns are attributable to the top five contributors, only 1999 and 2007 preceded falls the following year.

Markets continued to rise in remaining eight instances.

So, in our view, breadth is not a clear signal for the following year.

The alternate perspective is that we are seeing a unique market event with a small number of stocks demonstrating significant sustainable earnings power and real cash flow being generated, as opposed to just speculation, and that this is a platform for material continued earnings growth.

We note that the basket including Microsoft, Nvidia, Amazon, Alphabet and Meta has seen 38% growth in consensus 2024 EPS since June 2023, versus 0% for the S&P 500.

Apple’s developer day was the latest example of how companies with a coherent AI strategy are being rewarded.

It has described its strategy as “AI for the rest of us”, mirroring the successful 1980s Mac campaign of a “computer for the rest of us”.

Apple proposed embedding AI in productivity features, proofreading, mail prioritisation, text to image (including “genmojis”) and so on.

While some of these features are already available on Android, Apple’s appeal lies in consumer privacy, as the company plans on using an Apple data centre with Apple chips – or the phone itself – rather than relying on the public cloud.

The expectation is that this will drive a faster upgrade cycle as it requires the chipsets from the most recent models, which led to a 3-6% EPS upgrades. The stock broke to new highs, helping the broader market reach new highs.

This narrative, plus the earnings appeal, is reinforced by ETF flows into the sector.

This dynamic appears unlikely to break in the next few months, as liquidity remains supportive and valuations are not yet at historical relative extremes.

The key risk is inflation forcing rates to stay higher for longer and hurting the economy or the AI theme to run out of steam. Neither appears to be occurring.

Australian equities

The ASX was soft relative to other global markets, with Resources off 4.17% and Industrials also weaker (down 0.9%) as the market began to factor in lower 2025 earnings.

Previous expectations of close to 10% FY25 earnings-per-share growth in Industrials are looking stale given the softer economy.

Battery metals was the weakest part of Resources as lithium prices look to be rolling over again – with supply returning from China and Africa and demand a little lighter as the popularity of hybrids grows relative to battery electric vehicles.

Growth stocks continue to outperform, reflecting the appeal of companies generating growth in a more subdued economy.

About Crispin Murray and the Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia. Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions.

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

Canberra’s green bond explained | Quarterly fixed-income deep dive | Three charts that show the advantage of an active approach to fixed income

In their latest quarterly report, Tim Hext, Amy Xie Patrick, Terry Yuan and Murray Ackman explain the trends affecting Australian fixed income investors right now

- Download Pendal’s June quarter income and fixed interest report (PDF)

- Why bonds, why now? Pendal’s income and fixed interest experts explain

- Browse Pendal’s fixed interest funds

Pendal’s income and fixed interest team has just published its quarterly deep dive into the themes driving Australian markets (PDF).

In the latest edition, head of government bond strategies Tim Hext explains how the RBA’s liquidity system affects investments – and why Australians need to honestly appraise the liquidity of their funds.

Head of income strategies Amy Xie Patrick explores which kind of income funds are best suited to the likely economic landing scenarios. (Hint: not one-dimensional funds)

Senior credit analyst Terry Yuan writes about a recent transformation in the credit bond issuance market which has led to a number of deals becoming heavily over subscribed.

An unprecedented shift from a buyer’s market to a seller’s market has led to significant changes in pricing dynamics, Terry says.

Lastly, senior ESG and impact analyst Murray Ackman has a quick guide to the key questions investors should ask about sustainable investing opportunities

Find out about

Pendal’s Income and Fixed Interest funds

About Pendal

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia.

The team won Lonsec’s Active Fixed Income Fund of the Year award in 2021 and Zenith’s Australian Fixed Interest award in 2020.

Here are the main factors driving the ASX this week according to portfolio manager JIM TAYLOR. Reported by investment specialist Chris Adams

- Find out about Pendal Focus Australian Share Fund

- On-demand: tune into Crispin Murray’s bi-annual Beyond the Numbers webinar

EQUITY and bond returns were strong last week, with the local market leading the charge.

The S&P/ASX 300 gained 1.97%, while the S&P 500 rose 1.36%.

Commodities had it tough, with the oil price falling through US$80 for the first time in four months.

This provides some comfort around the near-term direction for headline inflation, which flows through to interest rates, policy, the dollar, and the performance of mega-cap growth stocks.

The global central bank easing cycle was kicked further into gear, with the Bank of Canada and European Central Bank (ECB) both cutting rates.

With that said, the ECB cut felt hawkish, with President Lagarde at pains to suggest the scope and pace of the rate cutting cycle from here is far from certain.

Economic data has been plentiful but lacking in real substance ahead of the US CPI this week, though Friday’s blow-out US jobs data print – which drove US bond yields up 15 basis points (bps) – pointed to a resilient labour market which continues to be a unique feature of this cycle.

Another feature is the bifurcated spending patterns of young versus older consumers, which is making the central banks’ job of navigating policy a whole lot harder.

The market has been oscillating between “bad news is good news” and fears that major economies are beginning to show signs of consumer stress based on the maxim that “monetary changes have their effect only after a considerable lag and over a long period”.

It seems the market is okay with bad news provided that news is not too bad.

Australia macro and policy

Reserve Bank of Australia (RBA)

RBA Governor Bullock delivered testimony to the Senate, which struck a government-friendly tone.

She noted that that the RBA’s estimate of the non-accelerating inflation rate of unemployment (NAIRU) was currently 4.3%, only 20bps above the current unemployment rate of 4.1%.

This was caveated by significant uncertainties around the estimate.

The RBA expects new energy rebates to reduce headline inflation by about 50bps in the next financial year, but that it won’t have a material impact on underlying trimmed-mean inflation or boost consumer spending given the relatively small size.

Bullock also pointed out that the RBA thinks monetary policy is taking about 18 months to flow through, suggesting in “a general sense that there is about 50bps of policy tightening to come”.

Q1 GDP

Economic growth was subdued in the first quarter, rising 0.1% quarter-on-quarter and 1.1% year-on-year. It is running at 0.9% on a six-month annualised basis.

This reflects a broader slowdown in the economy as the 2023 softness in households – in response to higher taxes and interest rates crimping real incomes – has expanded to public and private investment.

Both declined in Q1 and saw a smaller contribution to annual growth.

Public investment does remain at high levels, despite falling for the second consecutive quarter.

State and Federal budgets suggest that the spending pipeline peaks in FY25, as some major transport projects also reach completion.

Dwelling investment fell 0.5% to be 3.4% lower year-on-year. This is expected to continue falling, with detached housing projects falling steeply as the Homebuilder Subsidy boost falls away.

Other data

The Fair Work Commission raised Award and Minimum wages by 3.75% from 1 July 2024, which was largely as expected and below the 5.8% increase in 2023.

Dwelling prices across the eight-city average rose 0.8% month-on-month in May, up from 0.5% in April, representing the largest monthly gain since October 2023.

According to CoreLogic, national rents rose 0.7% month-on-month in May, down from 0.8% in April, representing the lowest monthly gain since December.

The slowdown is probably attributable to lower net migration and the impact of affordability on rental patterns, they noted.

Retail volumes have fallen below the pre-Covid trendline, though price remains well above it.

Conditions in Victoria look particularly weak, with anecdotes that events such as the Australian Open, the Grand Prix and Taylor Swift concert have masked underlying softness.

There are suggestions that changes to state taxes are taking a toll on sentiment.

Find out about

Pendal Focus

Australian Share Fund

Crispin Murray,

Head of Equities

US macro and policy

Non-farm payrolls rose 272k in May, versus 180k consensus expectations and 175k in April.

The three-month moving average is running at 249k per month, only modestly down from 261k per month in the preceding three-month period.

There was a strong skew to the “experience” pasts of the economy, where spending remains strong – potentially supported by older cohorts – with leisure and hospitality adding 42k jobs versus 26K in the good-producing segment of the economy.

Government jobs also strengthened following a weak April.

Average hourly earnings rose 0.4% versus the 0.3% expected and 0.2% seen in April. It is running at 4.1% year-on-year, which is still too high for the Federal Reserve’s comfort.

Unemployment is running at 4.0% versus the 3.9% expected. This is the first time at 4% in two years.

April JOLTS job opening came in at 8.06 million versus the 8.35 million expected and the 8.25 million seen in March.

This means the job-opening-to-unemployed ratio is at 1.24 – the lowest since January 2020 and down from 2.0 when rates began rising in March 2022.

The Quits rate – seen as a lead indicator for wage pressures – held steady at 2.2% and continues to suggest the employment cost index (ECI) should moderate over the next six months.

The ISM Manufacturing Index fell from 49.2 in April to 48.7 in May, driven by weakness in the new orders sub-index, which suggests ongoing weakness in manufacturing.

The ISM Service Index hit 53.8, up from 49.4 in the previous month and ahead of consensus sat 51.0.

While strong, this index has been in a range and has not been a strong indicator of spending habits.

Central banks

The Bank of Canada became the first G7 central bank to cut rates, shifting down 25bps to 4.75%.

The Chair left the door open to further cuts, saying they are confident inflation is heading to the 2% target.

The ECB reduced rates from 4% to 3.75%, however, the accompanying commentary was clearly designed to discourage expectations of a near-term continuation of cuts.

The rate-setting committee “is not pre-committing to a particular rate path” and rates are “not close to neutral”, according to accompanying statements.

This was reinforced by April core inflation in the EU ticking up from 2.7% to 2.9%. ECB President Lagarde noted a “strong likelihood” of further cuts in the months ahead, but stressed that “the speed of travel and time it will take” are very uncertain.

Markets

We observe that there has been a significant increase in demand for upside exposure among professional investors in the past week.

The funding spreads – the cost to fund a levered long position in futures, swaps or options –jumped to 70bps, the highest level since January 2018.

Most sectors in the S&P/ASX 300 gained for the week, led by Financials (3.88) and Consumer Staples (3.40%).

Information Technology fell 0.67%, while Materials was off 0.50% on some weakness in the resource sub-sector.

About Jim Taylor and Pendal Focus Australian Share Fund

Drawing on more than 25 years of experience investing in top-performing Australian companies and a background in accounting, Jim manages our Long/Short Fund and co-manages our Imputation Fund. He is a Chartered Accountant with membership of the Australian Institute of Chartered Accountants.

Pendal Focus Australian Share Fund is managed by Crispin Murray. The fund has beaten its benchmark in 14 years of its 18-year history (after fees), across a range of market conditions. Find out more about Pendal Focus Australian Share Fund here.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

We have updated and reissued the Product Disclosure Statements (PDSs) for the following Pendal funds effective on and from Thursday, 6 June 2024:

- Pendal Australian Equity Fund

- Pendal Australian Share Fund

- Pendal Focus Australian Share Fund

- Pendal Government Bond Fund

- Pendal Imputation Fund

- Pendal MidCap Fund

- Pendal Monthly Income Plus Fund

- Pendal Property Investment Fund

- Pendal Property Securities Fund

- Pendal Short Term Income Securities Fund

- Pendal Smaller Companies Fund

(the Funds).

The following is a summary of the key changes reflected in the PDS for each Fund.

Updates to significant risks disclosure

Each Fund’s investment strategy involves specific risks.

We have updated the significant risks disclosure applicable to each Fund to ensure that our disclosure continues to align with the nature and risk profile of each Fund and the current economic and operating environment.

Updates to ongoing annual fees and costs disclosure

The estimated ongoing annual fees and costs for the Funds have been updated to reflect financial year 2023 fees and costs. These include changes to estimated management costs, estimated performance fees (where applicable) and estimated transaction costs.

We now also disclose the maximum management fee and performance fee (where applicable) we are entitled to charge under each Fund’s Constitution.

Additional information on how to apply for direct investors

We have provided additional information for non-advised investors (investors without a financial adviser) investing directly in each Fund who may also be required to complete a series of questions as part of their online Application, to assist us in understanding whether they are likely to be within the target market for the Fund.

Updates to our complaints handling process

We have provided additional details about our complaints handling process and the Australian Financial Complaints Authority.

We have updated and reissued the Product Disclosure Statement (PDS) for the Pendal Managed Cash Fund (the Fund) effective on and from Thursday, 6 June 2024.

The following is a summary of the key changes reflected in the PDS.

Updates to significant risks disclosure

The Fund’s investment strategy involves specific risks.

We have updated the significant risks disclosure applicable to the Fund to ensure that our disclosure continues to align with the nature and risk profile of the Fund and the current economic and operating environment.

Updates to the Fund’s description

The description of Pendal’s investment process for Australian cash and short-term securities has been updated to better reflect Pendal’s investment approach for the Fund.

Updates to the Fund’s risk level description

There has been no change to the Fund’s risk level of ‘Very low’.

We have, however, standardised the Fund’s risk level description in the PDS with the format used for other Pendal funds.

Updates to ongoing annual fees and costs disclosure

The estimated ongoing annual fees and costs for the Fund have been updated to reflect financial year 2023 fees and costs. These include changes to estimated management costs and estimated transaction costs.

We now also disclose the maximum management fee we are entitled to charge under the Fund’s Constitution.

Additional information on how to apply for direct investors

We provide additional information for non-advised investors (investors without a financial adviser) investing directly in the Fund who may also be required to complete a series of questions as part of their online Application, to assist us in understanding whether they are likely to be within the target market for the Fund.

Updates to our complaints handling process

We have provided additional details about our complaints handling process and the Australian Financial Complaints Authority.