Australia has joined other sovereign nations in issuing an inaugural Commonwealth green bond. Senior ESG and impact analyst MURRAY ACKMAN explains what it is and why Pendal invested in it

- Australia has joined 30 other sovereign issuers by issuing its own green bond

- Investors willing to pay a premium for the bond, market oversubscribed

- Why bonds, why now? Pendal’s income and fixed interest experts explain

- Browse Pendal’s fixed interest funds

THE Commonwealth Government just issued its first green bond.

It has a June 2034 maturity with $7 billion issued.

The Green Treasury Bond also came with a “greenium” (meaning investors were willing to pay a premium to hold it) of around two basis points, which is roughly consistent with global peers.

Green bonds are meant to finance solutions for climate change and environmental challenges, but not all bonds are equal.

At Pendal — and at our specialist sustainable investing business Regnan — we’ve seen quite a few green-labelled bonds that don’t have any meaningful impact. Some are simply doing business as usual.

For governments, this is a particular risk.

At Pendal we are not interested in green bonds made up of already-completed projects that they were going to work on anyway, such as public transport or other infrastructure projects.

But we were very active in buying this bond – mainly across our sustainable funds, through which investors expect the majority of bonds to finance specific projects in the environmental or social space.

How did we judge this new bond? We asked a few questions:

- Does this green bond fund new things?

We want the first Commonwealth green bond to support new projects.

This is known as additionality – that is, funding something that would not have been funded but for this green bond.

Half the proceeds will go towards existing commitments and half will go towards new commitments.

In our view, this is quite reasonable and is better than some other green bonds from governments.

Ideally, we would like to see completely new projects, but we recognise that there are complications in doing this for a first issuance.

- Does it fund revolutionary projects?

Government has a different risk profile to the private sector and that gives it an opportunity to fund catalytic change — things that lead to a step change.

The list of projects funded include some that will help with the transition to a low-carbon economy – with the focus on renewable energy, clean transport, climate change adaptation, and a circular economy.

Find out about

Pendal’s Income and Fixed Interest funds

Electricity generation is the biggest source of emissions in Australia, so upgrading the grid to allow greater renewable energy connectivity will be essential in reducing emissions.

Electrification using renewable energy will significantly reduce emissions. The green bond includes investments in modernising the electricity grid and developing new transmission infrastructure through concessional financing.

This bond also funds projects that relate to this – from community batteries and electric vehicle charging infrastructure to loans for energy-saving home upgrades.

However, there are some sectors that cannot easily switch to electricity – for instance, industrial activity, which requires certain inputs for chemical reactions.

Taking a page from Joe Biden’s Inflation Reduction Act, which has made hydrogen use and production more viable, this bond will also help fund the development of regional hydrogen hubs.

We would like to see more catalytic change, but for the very first Commonwealth Green Bond, we are pleased with the scope of projects.

- Is clear reporting available?

The Commonwealth’s commitment is to distribute an annual impact report no later than 18 months after first issuance.

This will be reporting at a portfolio level rather than each bond line, which is fairly typical.

The government has also made the commitment to have independent verification of allocation and impact reporting.

This will assist in establishing annual reporting with independent verification as industry standard.

We are hopeful that this bond will demonstrate what the minimum requirements are for clear and transparent reporting for green bonds in Australia.

What else do we know about this bond?

A green bond should be a reflection of an issuer’s philosophy — not an apology for their actions.

Prior to issuing, the government announced funding to progress leadership on climate action in Government operations, which includes financing to support all Commonwealth entities in publicly reporting on their climate risks, opportunities and management.

This bond is consistent with recent government action to respond to climate change as well as engage in environmental repair through this bond.

The government has put in a lot of effort to make sure it got its inaugural green bond right.

The market has agreed, being nearly three times oversubscribed.

We anticipate that there will not be a new green bond for at least a year or two, so we believe it should perform well in the secondary market.

It provides integrity to the Australian green bond market and will provide a clear example of expectations for the market in future.

About Murray Ackman and Pendal’s Income and Fixed Interest boutique

Sustainable finance and impact investing director Murray Ackman joined Pendal in 2020 to provide fundamental credit analysis and integrate Environmental, Social and Governance factors across credit funds.

Murray has worked as a consultant measuring ESG for family offices and private equity firms and was a Research Fellow at the Institute for Economics and Peace where he led research on the United Nations Sustainable Development Goals.

Research and engagement analyst Paula Angel Valdes joined Pendal in November 2025. Prior to joining the company, Paula served as a senior analyst at Morningstar Sustainalytics in Amsterdam, where she specialised in ESG risk and impact assessments, controversy analysis, and contributed to the enhancement and implementation of methodological refinements for the firm’s Controversies product.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia. In 2020 the team won the Australian Fixed Interest category in the Zenith awards.

Regnan Credit Impact Trust is a defensive investment strategy that puts capital to work for positive change

Pendal Sustainable Australian Fixed Interest Fund is an Aussie bond fund that aims to outperform its benchmark while targeting environmental and social outcomes via a portion of its holdings.

We have updated and reissued the Product Disclosure Statement (PDS) for the Pendal Fixed Interest Fund (the Fund) effective on and from Thursday, 6 June 2024.

The following is a summary of the key changes reflected in the PDS.

Updates to significant risks disclosure

The Fund’s investment strategy involves specific risks.

We have updated the significant risks disclosure applicable to the Fund to ensure that our disclosure continues to align with the nature and risk profile of the Fund and the current economic and operating environment.

Updates to asset classes and asset allocation ranges disclosure

There has been no change to the way the Fund is invested.

We have, however, removed the reference to ‘currency’ from the Fund’s asset classes and asset allocation ranges description to more accurately reflect the fact that ‘currency’ is not an asset class.

Updates to ongoing annual fees and costs disclosure

The estimated ongoing annual fees and costs for the Fund have been updated to reflect financial year 2023 fees and costs. These include changes to estimated management costs and estimated transaction costs.

We now also disclose the maximum management fee we are entitled to charge under the Fund’s Constitution.

Additional information on how to apply for direct investors

We have provided additional information for non-advised investors (investors without a financial adviser) investing directly in the Fund who may also be required to complete a series of questions as part of their online Application, to assist us in understanding whether they are likely to be within the target market for the Fund.

Updates to our complaints handling process

We have provided additional details about our complaints handling process and the Australian Financial Complaints Authority.

Here are the main factors driving the ASX this week, according to Pendal’s head of equities CRISPIN MURRAY. Reported by portfolio specialist Chris Adams

- Equities quiet, may see period of consolidation

- The Fed unlikely to cut rates in June/July

- Find out about Pendal Focus Australian Share fund

- Watch Crispin’s most recent Beyond the Numbers webinar

EQUITY markets have been quiet and were down marginally last week.

Combined with a lack of follow-through on the Nvidia result and weakness in US software, this suggests we may see a period of consolidation.

The S&P 500 fell 0.49% while the S&P/ASX 300 was off 0.34%.

In the US, Personal Consumption Expenditure (PCE) inflation data was marginally lower than expected, which kept the chance of a pre-election rate cut alive.

Economic growth data was a touch softer than expected, but this week’s employment data should provide a clearer picture.

Australian inflation data was worse than expected and – despite softer retail sales – the prospect of rate cuts seems remote.

BHP’s attempt to take over Anglo American has ended for now. UK rules mean it can’t try again for another six months.

US inflation outlook

April’s PCE data was incrementally positive for the inflation outlook, but the Fed remains in “wait and hope” mode.

It is unlikely to cut rates in June or July.

The PCE – the Fed’s preferred measure of inflation – was in line with expectations, with Headline up 0.26% and Core up 0.25% month-on-month (or 2.8% year-on-year), versus a 0.3% run-rate in the last two months.

The market read this as marginally positive as the “super core” data – which adjusts for some of the imputed service components – fell from 0.3% month-on-month in March to 0.17%, which is consistent with 2% inflation.

But it is too soon to be bullish on inflation, as the trend remains too high – with three-month and six-month annualised growth at 3.5% and 3.2%, respectively.

The year-on-year reading is in the high 2% range, and in the past few months the outlook for inflation at the end of 2024 has also shifted there from the sub-2.5% range.

As a result, the Fed remains on hold – waiting for three months of data that indicates inflation is fading again.

We note that the base effect of slowing inflation in the second quarter of 2023 will also work against readings in the second half of 2024.

Digging into the details, core services inflation is moderating again but is still above the trend of late 2023, suggesting it sticks in the 3% range.

Meanwhile, goods deflation has now ended.

The bull case here is that retail margins, which are materially higher than pre-Covid, will be driven lower by competition in a softer economy, which could help bring inflation down.

The upshot of all this for markets is that we are unlikely to see rate cuts in either June or July. The question is, then, whether the Fed will cut ahead of the Presidential election.

The market is currently implying a 4% chance of a cut in June, 17% in July, and 63% in September.

Pendal Focus Australian Share Fund

Now rated at the highest level by Lonsec, Morningstar and Zenith

US economic growth

Here, the incremental news was softer, though it remains on trend for somewhere around 2% in 2024.

Headline first-quarter GDP was revised down from 1.6% to 1.3% (as expected) – driven mainly by lower consumption growth and lower net exports and inventory accumulation, while investment was stronger.

However, the drag from inventory and exports overstates economic softness.

Final sales to private domestic purchasers is a better indicator, which rose 2.8% versus 3.1% in the initial estimate.

Data on personal consumption was also softer, with consumer spending up 0.2% in April following 0.7% growth in March.

Personal incomes rose 0.3% and the savings rate was steady at 3.6%.

Real consumer spending – adjusted for inflation – was weaker than expected (-0.1% in April), continuing the signal of a slightly weaker consumer.

Services remains the strongest component, but this is fading. Spending on goods is down 1% on a three-month annualised basis.

This has seen second-quarter GDP forecasts reduced, though this is only the first month of the quarter.

The Atlanta Fed GDPNow estimate has shifted from the 3% range into the high 2% range. Market consensus is at 2%.

Anecdotally, in some sectors, US corporates are still constructive.

Booking.com and Airbnb are saying leisure travel demand is solid, while Uber is seeing no “trade-down” activity in restaurant delivery. Demand for digital advertising is also holding up.

The conclusion at this point is that US economic growth is decelerating at a moderate pace, but still heading for about 2% in 2024.

News of Trump’s conviction has led to a small shift back towards Biden in the betting odds, with the Real Clear Politics Betting Average showing Biden at about 39% and Trump at about 48%.

Europe

The European Central Bank (ECB) is expected to cut rates for the first time in this cycle this week.

The markets are pricing two-to-three rate cuts by the year’s end.

However, growth data, wages and inflation have been stronger than expected in last couple of months, so ECB President Lagarde may be cautious in the press conference and not commit to cut rates again in September.

Australia

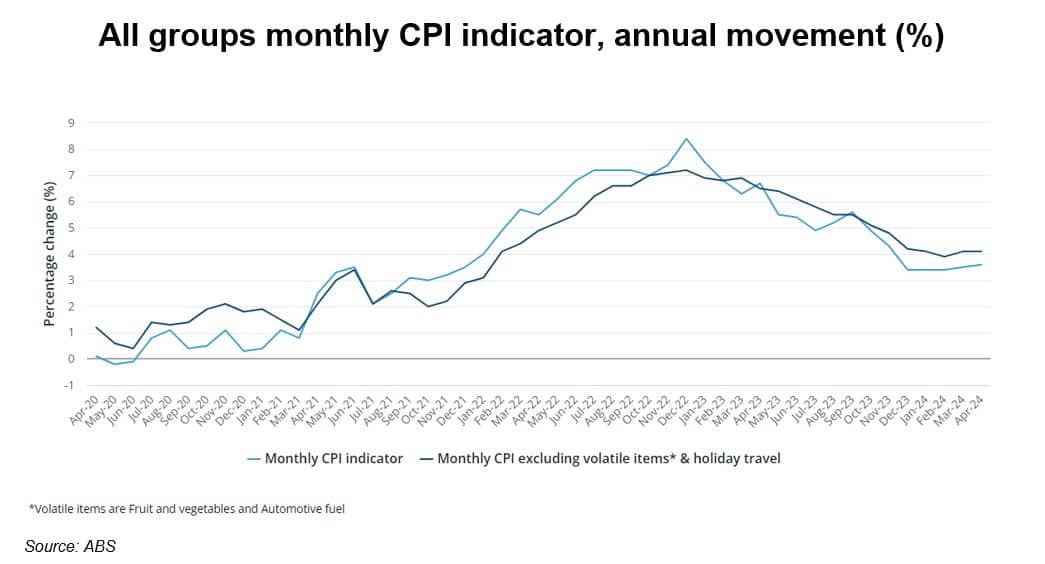

The April Consumer Price Index (CPI) rose 0.73% month-on-month, taking it to 3.6% year-on-year, versus 3.4% as expected.

Core CPI rose 0.24% to 3.8% year-on-year.

This pushes out expectations around rate cuts. Inflation is falling, but it remains too high for the RBA’s comfort.

The food, clothing and health components drove the upside surprise.

Construction costs have accelerated in the past few months.

High construction costs are a structural issue for Australian inflation, as it leads to a lack of supply of housing, retail space, distribution centres and other physical capacity.

Subsidies are helping ease some pressure, with the electricity component down 1.9% month-on-month and rent inflation slowing due to higher Commonwealth rent assistance.

Elsewhere, retail sales for April were softer than expected at 0.1% month-on-month and 1.3% year-on-year.

The read-through is messy due to the timing of Easter and school holidays, but the trend is flat-lining and has been reliant on population growth, which is now slowing.

On the positive side, there has been a pick-up in credit growth on the back of rising house prices.

This suggests that the stabilisation in interest rates is feeding through, and policy may no longer be as restrictive as it was.

The takeaway is that Australian inflation looks stickier than most countries and is being held up by structural problems. Even though the consumer is softening, rates look set to stay on hold for some time.

Markets

Markets appear to be consolidating and there are signs of deteriorating breadth.

Despite the S&P 500 being up about 11% calendar-year-to-date, 45% of stocks are down.

Higher bond yields are weighing on equities and ten-year bond yields are rising towards key resistance levels.

Positioning is getting more extended. Cash levels in US equity mutual funds are as low as we have seen in decades, though hedge fund exposure has room to rise further.

At this point, we see markets in something of a holding pattern and we believe liquidity can continue to support them through the September quarter.

The Magnificent Seven have become the “Fab Five” of Amazon, Apple, Microsoft, Google and Nvidia.

Indicators suggest that mutual and hedge fund managers are still underweight these stocks in aggregate, so there is still potential for them to squeeze higher.

When the 27% year-to-date index return of these stocks is removed, the roughly 6% or more return from the rest of the S&P 500 looks closer to a roughly 3% return from the S&P/ASX 300.

The AI thematic helping drive the Fab Five is also seeing bifurcation in the tech sector.

This can be seen in the divergence between the iShares Semiconductor ETF and the Global X Cloud Computing ETF, which have traded largely in tandem in 2022 and 2023.

However, the AI theme has seen semiconductors materially outperform since early 2024 – a trend which has accelerated in the last two weeks.

In this vein, the US Software sector was down 5.4% on Thursday, which was biggest day of underperformance in more than 10 years.

This was on the back of a quarterly result for Salesforce.com, which was in line with expectations but saw softer revenue guidance – leading the stock to drop about 20%.

The key debate is whether slowing revenue is company-specific or a broader macro issue.

We have seen this divergence in an Australian context in the performance of Goodman Group (GMG), which has also decoupled from a previously close correlation with a fellow industrial property company in the US, Prologis.

GMG has outperformed massively since Q3 2023 on the back of GMG’s pivot towards data centres.

Australian market

The S&P/ASX 300 rose 0.85% in May.

The thematic winners included aluminium/alumina names like Alumina and South32, as prices caught up with copper, as well as AI-related names such as Goodman Group and NextDC.

Other good performers such as Aristocrat Leisure, Xero, Technology One, Bendigo & Adelaide Bank, and AGL were driven by stock-related news.

Thematic losers were discretionary retailers such as Super Retail, Bapcor and Nick Scali as anecdotes of softer trading came out.

Some caution around the outlook for corporate travel saw Corporate Travel Management and Flight Centre softer.

The market was relatively quiet in the last week, with limited rotation. A weaker iron ore price saw some of the miners underperform.

About Crispin Murray and the Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia. Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions.

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

How Nvidia is impacting the global economy | Aussies relaxed about inflation outlook | Three charts that show the advantage of an active approach to fixed income

Despite a narrative around re-emerging inflation, Australian investors are remarkably relaxed about the outlook. Here Pendal’s head of government bond strategies TIM HEXT explains the latest inflation data

- April CPI came in higher than expected

- Australian market relaxed about inflation outlook

- Why bonds, why now? Pendal’s income and fixed interest experts explain

- Browse Pendal’s fixed interest funds

APRIL’S inflation numbers point to a 3.6% increase in the annual Consumer Price Index.

That’s slightly higher than March (3.5%) and more than the 3.4% the market was hoping for.

Excluding volatile items (food and energy) the CPI was steady at 4.1%.

It bears repeating that the monthly CPI number does not measure all items.

Sixty per cent of items are collected every month, while 30% are collected once a quarter (with roughly 10% in each of the three months), and 10% are collected annually.

Forecasters are still having to constantly refine their models and learn something new every release.

The ABS is constantly improving that collection and is hoping to release a comprehensive monthly number later next year.

What’s up and down in monthly price moves?

International travel led the way, up 10.6% after sharp falls earlier in the year.

Fruit prices were up 7.3%, fuel prices were up 2.2%, and medical and hospital services were up 2.7%.

Surprisingly, clothes and footwear were up 4% on average – a rare and large rise in goods prices.

Find out about

Pendal’s Income and Fixed Interest funds

What was encouraging, though, was some rent relief – inflation “only” rose 0.5%, which is the lowest increase in a long time.

Electricity and gas prices fell slightly and will obviously collapse as subsidies hit in Q3.

What does this mean for the RBA?

The rise in goods prices – mainly furniture, footwear and clothing – will not go unnoticed by the RBA and will require further investigation.

The narrative has been that goods prices (about a third of CPI) should only grow 1-2%, allowing services (the other two-thirds of CPI) to be 3-4% and still get near the inflation target.

However, overriding these concerns are the impacts of upcoming government subsidies.

Electricity subsidies should deduct 0.5% from CPI in Q3 and the RBA will need to reduce its end-of-year (2024) inflation forecast from 3.8% to 3.3%.

Lower oil prices in May should see the monthly CPI start falling again and end the year closer to 3%.

How are markets viewing inflation?

Despite the narrative that inflation has re-emerged over recent months, the Australian market is remarkably relaxed about the inflation outlook.

Implied 10-year inflation levels, based off inflation swaps, remain reasonably well anchored at 2.77%.

Over the past 12 months, this level has largely been treading water – between 2.70% and 2.90%.

The market is backing the RBA to do its job.

Implications for investors

Three-year yields in Australia have backed up above 4% once more following this inflation number.

We view this as an opportunity to add duration, as our medium-term view on inflation is positive.

US inflation numbers come out on Friday and should show lower rental outcomes feeding through to lower outcomes.

As mentioned before, the CPI track in Australia should improve into the third quarter.

We will dig around and see if the goods inflation story in this number is temporary or a sign of emerging pressures.

The Pendal Australian equities team’s insights are very useful in this regard.

Unless our concerns ramp up, we will be happy to be long duration into the winter months.

About Tim Hext and Pendal’s Income & Fixed Interest boutique

Tim Hext is a Pendal portfolio manager and head of government bond strategies in our Income and Fixed Interest team.

Tim has extensive experience in banking, financial markets and funding including senior positions with NSW Treasury Corporation (TCorp), Westpac Treasury, Commonwealth Bank of Australia, Deutsche Bank, Bain & Co and Swiss Bank Corporation.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia.

Find out more about Pendal’s fixed interest strategies here

About Pendal

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

In 2023, Pendal became part of Perpetual Limited (ASX:PPT), bringing together two of Australia’s most respected active asset management brands to create a global leader in multi-boutique asset management with autonomous, world-class investment capabilities and a growing leadership position in ESG.

Here are the main factors driving the ASX this week according to Aussie equities analyst and PM ELISE MCKAY. Reported by portfolio specialist Chris Adams

- Nvidia delivers blow-out 1Q result

- Pendal Australian equities portfolios positioned to benefit

- Find out about Pendal Focus Australian Share fund

THE global economy appears to have left last decade’s monetary policy era well behind and embraced a far more exciting fiscal policy era.

Kicked off by Covid spending, and quickly bolstered by the energy transition and defence focus, we now see further momentum in a sovereign artificial intelligence race and the generative AI build-out.

This was highlighted by last week’s blow-out Nvidia first-quarter result.

The stock gained 15% over the week, suggesting that investors continue to underestimate the speed, scale and scope of the AI revolution.

Nvidia is perhaps more than just another stock. At present it appears to be a key driver of markets – touching almost every aspect of the global economy.

Its influence is felt everywhere – from the geopolitical need for sovereign AI and the productivity and capex boom affecting economic growth, to increased demand for commodities to help power data centres, and the wealth effect of rising stock markets, which helps consumption.

Our portfolios are positioned to benefit.

In the large-cap portfolios, we have NextDC (NXT) and Goodman Group (GMG), which benefit from increased demand for data centres.

In our midcap fund, we hold NXT and Megaport (MP1), which is exposed to networking, as well as newly listed copper stock Capstone (CSC).

The small-caps team own another data centre play Macquarie Technology Group (MAQ), along with copper miners Sandfire (SFR) and CSC.

In this week’s note we check the pulse of the global consumer – with the European consumer strengthening, the Australian consumer under pressure, and a bifurcation occurring between US consumers who own shares (like higher-income households) and those at the lower end.

On the inflation front, a bounce in May’s Flash S&P Global Composite Purchasing Manager’s Index (PMI) plus more hawkish Federal Reserve speak and minutes resulted in US 10-year Treasury bond yields moving up five basis points (bps) to 4.47%.

Goldman Sachs was prompted to push out its first rate-cut assumption from July to September 2024.

But the PMI sub-components data, plus unemployment claims, were consistent with the narrative that employment and inflation measures are on track to weaken over the coming months.

Confidence remains high that the next move will be down.

The market is now only pricing a 10% chance of the Fed cutting rates in July, while this rises to 50% by the September meeting.

Though last week was very busy in Australia, with a mini-reporting season seeing the likes of Xero (XRO), Technology One (TNE), James Hardie (JHX) and ALS (ALQ) all delivering results, this week looks a little quieter.

The S&P/ASX 300 fell 1.11%, while the S&P 500 returned 0.05% last week.

The US market is closed Monday for the Memorial Day long weekend and then we get personal income and spending data on Friday.

Economics and policy

The Fed

The May FOMC meeting minutes were released and were relatively hawkish. In addition, we had almost 20 statements from various Fed members.

The broad takeaway is that there is no sense of urgency to cut, and it looks as if like the fastest route to a cut would come through an unexpected deterioration in the labour market, rather than inflation alone.

Unemployment claims

The four-week average weekly unemployment claims inched up to 220k, off the lows of 201k earlier this year.

While we haven’t seen a meaningful increase in claims, the slowing rate of hiring (the first step taken by businesses in response to rising borrowing costs and reduced demand) would suggest claims will eventually follow.

S&P Global PMIs

The flash S&P Global Composite PMI survey rose to 54.4 in May – up from 51.3 in April and well above consensus expectations of 51.2.

The market responded negatively, with US 2-year bond yields rising 7bps on the day.

It is worth noting that this index has been a poor indicator of growth in GDP since the COVID pandemic.

More importantly, the sub-components data was consistent with the narrative that employment and inflation data are on track to weaken over the coming months, supporting potential US rate cuts later this year.

Expectations of the first cut have now been pushed back to September.

On the negative side, the composite employment index recovered half of the unexpectedly soft April decline.

Find out about

Pendal Focus

Australian Share Fund

Crispin Murray,

Head of Equities

However, it remains soft at 49.9 – suggesting equally as many firms are reducing employment as there are those increasing it.

This is consistent with materially weaker jobs growth and signals that businesses expect demand growth to soften.

The output prices indices for both Services and Manufacturing supported the global disinflation story:

- While the services output price index ticked up from 53.7 to 54.0, it suggests that CPI services ex. rents will soon be rising at a 2.5% three-month annualised rate, down from 7.1% in April.

- The manufacturing output price index moderated from 54.9 to 54.5 and also suggested manufacturers built up inventories of finished goods in May, which may prompt price cuts to free up cash flow and be positive for disinflation.

The Nvidia (NVDA) result

Another “beat and raise” print for Nvidia, which reported 1Q24 revenue of $26 billion – beating consensus expectations by 6%.

Earnings per share (EPS) of $5.59 were in line with expectations.

Guidance for 2Q24 is revenue of $28 billion and EPS of $6.30, which are 8% and 3% ahead of consensus expectations, respectively.

A 10:1 stock split was also music to the ears of retail investors.

Incredibly, data centre revenue growth accelerated again from 409% year-on-year in 4Q23 to 427% year-on-year in 1Q24.

The velocity of demand for graphics processing units (GPUs) continues to grow, with demand expected to outstrip supply until at least 2025.

This is not just from the larger cloud service providers (the “hyperscalers”) – individual corporates (“enterprise”) are now the largest incremental buyers in aggregate.

In addition, sovereigns are now coming in and buying to build their own secure infrastructure stacks.

For example, Japan is making a US$740 million investment in a project led by telco KKDI, Skura Internet and Softbank to build up Japan’s AI infrastructure.

NVDA also talked about supplying 100 “AI Factories” – data centres operated independently of the hyperscalers, which may also provide opportunities for companies such as NextDC (NXT).

Amazingly, NVDA now has 81% share of wallet for data centre processors and continues to gain on its peers (Intel and Advanced Micro Devices, or AMD).

It is estimated that there are 15-20k generative AI-related start-up companies.

We are still in the experimental phase of what this new ecosystem will mean for the economy.

Long-term, the AI revolution is expected to drive significant productivity gains, however, the more immediate concern is the inflationary impact the boom in share prices may have on consumer spending.

This was reflected in the FOMC meeting minutes, with at least two participants hawkishly noting that “financial conditions appeared favourable for wealthier households, which account for a large portion of aggregate consumption, with hefty wealth gains resulting from recent equity and house price increases”.

NVDA stock closed up 9% on the day and added about US$275 billion in market cap (equivalent in size to Salesforce, Netflix, and AMD).

To put this in perspective, NVDA made a cyclical low in October 2022 – trading at 25x next-12-month (NTM) price/earnings (P/E) with a US$280 billion market cap.

Since then, earnings have grown roughly ten times and the stock is now trading at 31x NTM P/E with a US$2.5 trillion market cap.

This is supportive for shareholders more broadly; the boom in the US tech sector alone has added about 10% of GDP to US household net worth this year.

According to Fidelity, the number of millionaires in the 401(k)-retirement savings scheme has hit a new record, with 485k in 1Q24 – up 15% for the quarter and 43% for the year.

Fidelity has more than 23 million plan participants with an average balance $126k, which is up 16% year-on-year.

So the rich are getting richer and that’s supportive for the companies skewed at the higher end of the consumer market, as the beneficiaries of such gains are likely to spend a bit more.

We note that households own 39% of the $73 trillion US market in cash equities – that rises to 65% inclusive of mutual funds and ETFs.

The UK

Core CPI inflation came in at 3.9% year-on-year in April, which was down from 4.2% in March but above consensus expectations of 3.6%.

Find out about

Pendal Smaller

Companies Fund

Disappointingly, services inflation only declined by 10bps from 6% to 5.9%, which was well ahead of consensus and Bank of England (BOE) expectations of 5.4%-5.5%.

This has pushed out expectations for a cut from June (with a 10% probability now) to August.

Further, the BOE will not being updating on policy or giving any speeches until after the UK election on 4 July.

Wage pressures remain firm in the UK, with the three-month average private sector regular pay growing at 5.9% year-on-year.

Several leading indicators, such as the Indeed wage tracker and HMRC pay data, are pointing to a potential increase from here.

Europe

The flash S&P Eurozone Composite PMI rose from 51.7 in April to 52.3 in May – its highest reading for twelve months.

This suggests that output across the combined manufacturing and services sector has continued to grow.

This is supportive for Eurozone GDP growth, which should be bolstered further by the expectation that the European Central Bank (ECB) will cut rates in June.

Further optimism came from output prices, which rose at the slowest rate in six months and are rising at a level that is consistent with inflation meeting the ECB’s 2% target.

The data was particularly constructive for Germany, where output rose for a second month running and the pace of growth strengthened and hit a twelve-month high.

Germany has been under pressure for some time, suffering from a range of cyclical problems (like the gas crisis, higher rates, weaker Chinese demand) and structural issues (like its reliance on China imports, the auto industry shift to EVs, and unfavourable demographics).

Real GDP has been flat since 2019, compared with 5% growth for the rest of the Euro area and 9% growth in the US.

A cyclical upswing is underway – with lower inflation boosting real household incomes, which should support consumption growth in coming months.

Combined with lower inflation dynamics allowing the ECB to ease, growth in Germany should pick up over the next twelve months, leaving behind two years of stagnation.

Europe, and Germany in particular, should benefit from the huge wave of liquid natural gas (LNG) supply coming online over the next couple of years. This should result in lower energy prices and act as a tailwind for consumers and the energy-intensive manufacturing industry.

Global consumer pulse-check

This change in Europe is starting to come through in consumption measures.

The Euro area Goldman Sachs Consumer Health Indicator has improved, from the 30th percentile in early 2023 to the 60th percentile more recently.

The US is also around the 60th percentile on the same measure.

It is downbeat in the UK, where it has ranged between the 30th and 40th percentile for 2023 and into 2024.

Australia is also around the 40th percentile.

More broadly, Australian consumer sentiment has continued to decline despite a supportive budget, according to the Westpac Monthly Survey.

The decline was driven by softer perception of personal financials and an increase in unemployment expectations – signalling a softer outlook for the labour market.

Within Australia, those under 40 years old are facing the greatest pressure.

Analysis from CBA on consumer card transactions in 1Q24 showed that cuts to real discretionary and essential spending are skewed to younger cohorts – particularly the average 25–29-year category.

On the other hand, those at or heading into retirement seem well-placed to enjoy it – with a strong propensity to spend.

This is particularly favourable for those consumer companies most exposed to older age cohorts, such as Flight Centre (FLT).

Meanwhile in the US, overall spending remains healthy but bifurcated, with companies increasingly calling out a weaker lower-end consumer.

These consumers are also most exposed to a weakening labour market, with each 1% increase in the overall unemployment rate lowering spending by 1.2% for households in the bottom income quintile but only 0.4% in the top-income quintile.

Of Australian-listed companies, Block (SQ2) is exposed to the lower-end US consumer through its Cash App offering.

Markets

While the NASDAQ had a decent week (up 1.4%) off the back of an exceptional NVDA quarterly, the rest of the market was pretty soggy.

Looking at US large caps, winners are taking more of the spoils – with the largest ten companies now accounting for 26% of S&P 500 earnings, yet 35% of market cap.

While large caps are reporting positive earnings, this is not the case for small caps.

It was interesting to note that the number of companies mentioning AI during quarterly earnings calls has jumped from about 10% in 2022 to 41% in the most recent quarter.

The breadth of sectors that are considered AI beneficiaries has expanded from semiconductors into AI infrastructure plays, such as copper and power.

In particular, utilities have been in focus as a potential AI beneficiary given the substantial energy requirements to power data centres.

Global data centre power demand is expected to more than double by 2030.

This has been reflected in mutual fund positioning, with the smallest underweight to utilities in ten years.

More broadly, hedge and mutual fund positioning has rotated towards cyclicals – with increases across consumer discretionary, financials and energy as investor confidence about economic growth has strengthened.

Copper

Copper dropped 5.5%, giving back some of its 23% year-to-date gains and coming off all-time highs of $5.12/lb reached during the week.

This has been an interesting market, with differences emerging between the two most liquid markets for the metal: the Chicago Metal Exchange (CME) which is largely investor driven, and the London Metal Exchange (LME) which is largely a physically based market.

Pricing between the two is usually within a 2%-3% range, but huge demand from investors has overwhelmed the physical market – pushing the spread by more than 10%.

This huge dislocation has led to risk mitigation as the medium-term speculative positioning is at odds with a lack of physical tightness in the market today.

In fact, the physical market is trading in contango, with spot demand less than current supply.

However, traders are widely expecting that a supply deficit will start building from 2H24 and that long-term structural drivers, such as decarbonisation and AI-related demand, are very supportive for a tight market.

Previously, the ASX had only one sizeable copper player – Sandfire (SFR) – but that has recently been joined by the Australian listing of Capstone (CSC).

Gold

Gold also fell on the week, down 3.3% (but still up 13% in 2024) despite real yields going higher.

Usually, they would trade inversely, reflecting lower demand for inflation-proof assets.

However, this relationship hasn’t held with new buyers emerging from central banks and the Chinese retail market.

Global central bank purchases have increased three times since Russia invaded Ukraine.

Emerging market central banks (like China, Poland, Turkey, India and Qatar) have been big net buyers.

There is further room for this momentum to continue, with only 6% of emerging market official reserves being held in gold versus 12% in developed markets.

About 20% of all gold mined throughout history is sitting in central bank reserves.

Incremental retail demand out of Japan (reflecting the devaluation of the yen) and China (showing movement of wealth out of property) has also been supportive.

While the Chinese government’s recent moves to support the property market are helpful, we don’t think they are yet at a level to disrupt this trend.

Despite the bullishness in gold, the miners have lagged.

This reflects a combination of positioning – and the possibility that western investors are trained to sell gold miners on the move higher in real rates – as well as hiccups in operational performance.

Australia

Within Australia, Tech (+2.45%) performed off the back of some strong results from Xero (XRO, +8.41%) and Technology One (TNE, +12.18%) while Utilities (+2.35%), Energy (+1.19%) and Industrials (+0.80%) were also in the green. Consumer Discretionary (-4.24%) and Communication Services (-3.73%) were the worst sectors, with Wesfarmers (WES, -6.68%) and Telstra (TLS, -5.99%) weighing on the market.

About Elise McKay and Pendal Australian share funds

Elise is an investment analyst and portfolio manager with Pendal’s Australian equities team. Elise previously worked as an investment analyst for US fund manager Cartica where she covered a variety of emerging market companies.

She has also worked in investment banking and corporate finance at JP Morgan and Ernst & Young.

Pendal Horizon Sustainable Australian Share Fund is a concentrated portfolio aligned with the transition to a more sustainable, future economy.

Pendal Focus Australian Share Fund is a high-conviction equity fund with a 16-year track record of strong performance in a range of market conditions. The Fund is rated at the highest level by Lonsec, Morningstar and Zenith.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Pendal’s head of income strategies AMY XIE PATRICK argued in favour of an active approach to fixed income at this year’s Lonsec Symposium

- Pendal employs AI to analyse “central bank speak”

- Active management matters the most when markets are volatile

- Why bonds, why now? Pendal’s income and fixed interest experts explain

- Browse Pendal’s fixed interest funds

I RECENTLY had the pleasure of participating in a fixed income panel at the Lonsec Symposium.

It was the most engaging panel session I’ve attended in a long time – and if nothing else, it tells me that this asset class has become a hot topic.

In case you weren’t able to attend, here’s a summary of my main observations from the Symposium.

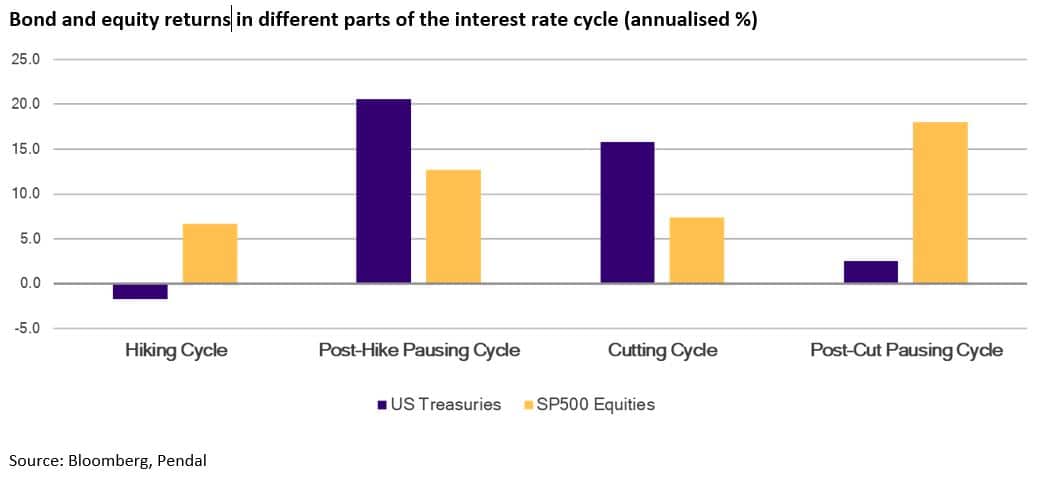

1. What’s better than a rate-cutting cycle for bonds?

In 2022, the Pendal Income and Fixed Interest team embarked on an exercise to see how bonds and equities performed in different parts of the rate cycle.

The motivation?

Being in the middle of the steepest hiking cycle I’d ever witnessed in my career. I wanted to see just how ugly it could get for bonds.

To do this, we needed to look at data going back as far as the 1970s and the era of hyperinflation.

The results gave us a surprise beyond our original curiosity.

Of course, bonds do well when central banks are slashing interest rates, but it turns out that what’s even better for bonds is when central banks come to the end of hikes.

Opinions are divided about whether cuts will come this year, how many and how soon. On the margin, some debate whether another one or two hikes might be necessary.

This first chart cuts through all that noise – what it tells us is that as long as the conviction has shifted away from hikes, then good times lie ahead for bonds.

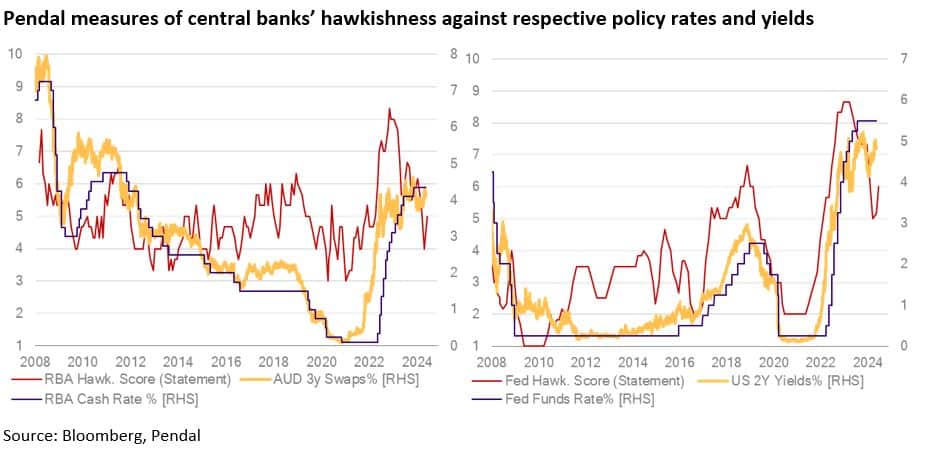

2. So, is this the post-hike pause?

Yes, I think so. But having an objective way to discern how policymakers are leaning is key.

At Pendal, we employ the AI power of large language models to help us decipher “central bank speak” – be it from their statements, minutes or general speeches.

This thinking is not novel, but our methods are unique.

When you do nothing to the raw language coming out of central bankers’ mouths, generative AI tools have a hard time delivering useful results for investors; ten attempts may well lead to ten different answers.

By design, language models prioritise syntax (language) over logic. Our methods look for ways to clean the raw language to make it as straightforward as possible.

The crucial test for whether our measures are useful is the presence of a relationship to local policy rates and yields.

When Pendal’s hawkishness scores peak, policy rates and front-end yields usually peak as well.

What these charts show is that both the RBA and the Federal Reserve have passed their peak hawkishness. Peak policy rates and yields won’t be far away, if not already behind us.

This is most likely the post-hike pause where bonds do their best work.

3. Don’t just close your eyes and buy

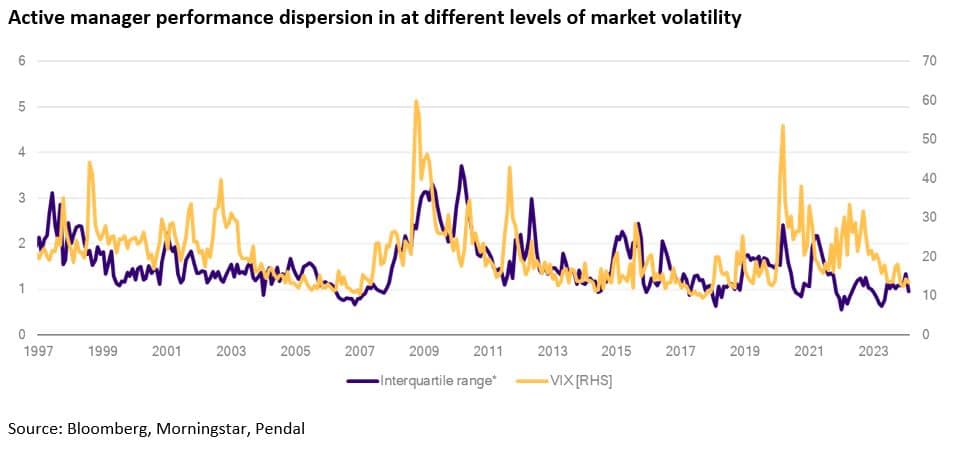

Yes, bonds are back. Yes, the time is now. But the road for fixed income has been bumpy.

Active management matters the most when markets are volatile.

As the above chart shows, when volatility spikes, the dispersion between active managers’ performance in fixed income really stretches out.

What you can’t see from the chart is that first-quartile managers during the calmer times are rarely able to keep their positions in more volatile times. This makes sense because you need different active tools in different volatility regimes.

Volatility today is about as low as it has ever been in the last three decades.

Now is the time to ensure that not only is your fixed interest exposure allocated to an active manager, but that the managers you choose have what it takes to weather the next spike in volatility.

About Amy Xie Patrick and Pendal’s Income and Fixed Interest team

Amy is Pendal’s Head of Income Strategies. She has extensive expertise and experience in emerging markets, global high yield and investment grade credit and holds an honours degree in economics from Cambridge University.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia. The team oversees some $20 billion invested across income, composite, pure alpha, global and Australian government strategies.

Find out more about Pendal’s fixed interest strategies here

About Pendal Group

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

Here are the main factors driving the ASX this week according to Pendal investment analyst ANTHONY MORAN. Reported by portfolio specialist Chris Adams

- Economic data points to a slowing US economy

- Australia’s Budget is increasingly stimulatory

- Find out about Pendal Focus Australian Share fund

IT WAS a bullish few days for assets last week as the US monthly consumer price index broke its run of hawkish surprises.

Instead, the inflation print delivered in line with expectations, validating a recent decline in bond yields and the US Dollar Index.

We also saw a continuation in the run of softer, but not disastrous, economic news – reinforcing the narrative’s switch back from “no landing” to “soft landing”.

In response, US equity markets hit fresh highs; the S&P500 gained 1.60%, the S&P/ASX 300 rose 0.98%, while commodities and bonds also moved higher over the week.

As a result of recent data, the market is now pricing 45 basis points (bps) of rate cuts in the US this year – with an 85% chance of a first cut by September.

At the same time, the Atlanta Fed GDPNow tracker estimates that the US economy will grow 3.6% in Q2 2024.

On balance, this combination is positive for markets and – given the slower pace of change in the data – may support this environment through the Northern summer.

However, Federal Reserve Chairman Jay Powell noted that while he expects inflation to come down, his confidence is not as high as it had been and that it may take longer than expected for restrictive policy to help bring inflation down to target.

So, bond yields overshot in mid-April, but it is hard to see them moving much lower from here in the short term given the large pullback from peak.

We also need to keep a close watch on company earnings for any sign of impact from a slowing economy.

US macro

Inflation

The monthly US CPI provided the week’s marquee data point.

The upshot is that the print was reassuring, but it needs to ease further to allow rate cuts.

The backdrop was concerning as the April core Producer Price Index (PPI) had come in at 0.5% month-on-month versus the 0.2% expected.

However, the market’s reaction was muted given that:

- March was revised down from 0.2% to -0.1%, leaving year-on-year core at 2.37%, which was in-line with consensus

- There was slower growth in components of the PPI that fed into the core Personal Consumption Expenditures (PCE) deflator – the Federal Reserve’s preferred measure of inflation – such as insurance and airfares.

The University of Michigan’s monthly survey of inflation expectations data had also seen an uptick in one-year-forward expectations from 3.2% to 3.5%.

However, core CPI came in at 0.29% month-on-month in April, which was in line with consensus.

Importantly, it slowed from March – breaking the sequence of upside surprises that has been causing market anxiety this year.

The market also liked seeing year-on-year core CPI slowing to 3.6% – the lowest reading since April 2021. This helped take the risk of a rate hike off the table and gave some support for rate cuts this year.

Digging into the data, we can see that the deflationary impulse from Goods remains but is shrinking.

Core Goods inflation was down 0.11% month-on-month, but up 0.4% once used cars and trucks were excluded.

The big change was a healthy deceleration in core Services (excluding rent/owners-equivalent-rent or OER) from 0.65% month-on-month in March to 0.42% in April.

This is the lowest reading since December, but still well above target.

Rent/OER continued to trend lower.

Looking forward, on the positive side, gasoline pricing may have peaked and insurance repricing has largely occurred, possibly reducing their upwards pressure on inflation.

On the downside, rent growth appears to have stopped slowing.

Shelter cost is particularly important; if it is stripped out, CPI has been largely in line with the Fed’s target since June last year.

The concern is that this has flattened out and the deflationary impulse from rent will start to ease off.

There are some encouraging signs in the housing market, which may flow into rental availability: single family housing inventory is increasing and the year-on-year price growth in housing appears to be slower.

As a result, the Fed may want to keep rates on hold until a loosening housing market is more entrenched.

Economic data

Other data pointed to a slowing economy, but not one falling off a cliff.

This reinforced the notion of a soft landing and so, in this case, bad news was good news.

US retail sales were flat during the month, with higher gasoline spending draining consumer wallets. We note this follows a couple of strong months of spending, so cannot yet call it a trend.

Softer retail sales were perhaps not a surprise, given real average hourly earnings fell 0.2% month-on-month in April.

Initial jobless claims are increasing but, again, it is too early to call this a convincing trend – particularly as it is not showing up in continuing jobless claims data yet.

The NAHB Index (a measure of homebuilder sentiment) fell to 45 in May, but this is likely to reflect the recent rise in mortgage rates, which has since unwound.

Industrial production is going sideways and manufacturing output fell 0.3% month-on-month. Both the Philadelphia Fed and Empire Manufacturing surveys were also softer.

China

Recent data suggests that the Chinese property market is not healing.

Macquarie Macro Strategy research suggests that existing home prices in 70 major cities fell 6.8% year-on-year in April – the fastest decline on record.

A sharp fall in mortgage interest rates is not supporting the market.

Beijing announced a number of supportive measures, including:

- removal of mortgage floor rate

- lowering of minimum downpayment requirements

- directives for local governments to acquire homes at “reasonable” prices and turn them into affordable housing.

There is some market debate about this.

It is incrementally positive on the policy side, but there is also concern that the actual size of this stimulus will not be enough to make a material difference.

What we can see is further evidence of a twin-track economy emerging, with industrial production strong but consumption weak.

Industrial production grew ahead of expectations at 6.7% in April – with Autos (up 15%), semiconductors (up 32%) and solar panels (up 11%) all strong, while steel, cement and coal were all weaker.

On the other hand, fixed asset investment (FAI) grew 3.6% and retail sales grew 2.3% year-on-year, both weaker than expected.

So exports – and possibly inventory builds – are currently underpinning Chinese growth.

For example, Chinese exports of autos grew 34% year-on-year in the period January to April, driven by electric vehicles (EVs).

The issue is that the Biden Administration has just announced a 100% tariff on imported EVs, as well as increased tariffs on semiconductors, batteries and solar cells.

This only affects 4% of Chinese exports to the US, but it does set a protectionist precedent for other countries; the EU is also reportedly looking to introduce protective tariffs in some areas.

This potential threat to exports – and possible implication for the resource sector – needs to be watched closely given the current state of the Chinese economy.

Pendal Focus Australian Share Fund

Now rated at the highest level by Lonsec, Morningstar and Zenith

Australia

Our key takeaway from the Federal Budget is that it was increasingly stimulatory.

The $300 per household energy subsidy, rental subsidies and additional spending all adds up to healthy stimulus for households, coming in on top of the Stage 3 tax cuts in July.

But might this stimulus be needed?

Unemployment surprised, with a jump from 3.9% to 4.1% in April.

There was a big jump in part-time employment (up 44.6k new jobs) while full-time employment fell 6.1k roles.

The key issue was the participation rate, which was up 0.1% to 66.7%, while the number of hours worked remained flat.

Employment is now growing slower than the population (ex-children and non-residents).

The government is looking to cut net migration, from 528k in FY23 to 395k in FY24 (upgraded from 375k) and then to 260k in FY25. That would take some pressure off housing, which should be deflationary.

The question is – will it be enough?

Commodities

Copper was up 7.7% for the week.

The catalyst may have been the combination of China property support measures, a weaker US Dollar, and trade measures which hinder movement of Russian and Chinese physical copper to US.

But short-dated contracts traded at a record high to longer-dated futures, indicating a physical shortage due to shorts being squeezed.

Short copper positions are at record highs, as are long positions.

One thing to note is that Chinese copper indices are depressed and inventories are at record highs.

There are many potential moving parts here, but it is a disconnection from normal copper markets which needs to be watched, given China consumes about 55% of the world’s copper.

About Anthony Moran

Anthony Moran is an analyst with over 15 years of experience covering a range of Australian and international sectors. His sector coverage has included Australian Industrials and Energy, Building Materials, Capital Goods, Engineering & Construction, Transport, Telcos, REITs, Utilities and Infrastructure.

He has previously worked as an equity analyst for AllianceBernstein and Macquarie Group, spending a further two years as a management consultant at Port Jackson Partners and two years as an institutional research sales executive with Deutsche Bank.

Anthony is a CFA Charterholder and holds bachelor’s degrees in Commerce and Law from the University of Sydney.

The allure of higher interest rates and certainty of returns from term deposits is strong, but the income advantage of bonds over term deposits remains clear, writes head of income strategies AMY XIE PATRICK

- Higher interest rates in 2023 made term deposits seem attractive

- Active income strategies have a role to play

- Why bonds, why now? Pendal’s income and fixed interest experts explain

- Browse Pendal’s fixed interest funds

THE RESERVE BANK held the Overnight Cash Rate steady at 4.35% on May 7 for the fourth consecutive meeting.

At first look, this makes 12-month term deposits seem attractive.

The 2022 “everything sell-off” still haunts many investors, while the allure of higher interest rates and certainty of returns is hard to turn down.

At the margin, however, investors we speak to are starting to wonder whether there is more to life than term deposits — even in a higher interest rate environment.

Our answer? Yes!

Term deposit returns in 2023

Since 2022 was such a volatile and disappointing year for both defensive and risky assets, many investors found it better for their peace of mind to leave their capital in cash products at the start of 2023.

After all, one of the reasons bonds and equities had sold off together in 2022 was because inflation had been a problem and so interest rates had been raised across the globe.

In Australia, the RBA raised the Overnight Cash Rate from 0.1% to 3.1% in the space of six months.

This meant that at the start of 2023, 12-month term deposit rates on offer with the major banks exceeded 3.5%.

Since the economic backdrop looked far from straightforward, one-year return rates of between 3.5%–4% looked pretty attractive to lock in.

Indeed, last year was eventful and volatile.

US regional banks threatened to bring another credit crunch into the global financial system. Chinese property developers continued to be in dire straits with no sign of rescue from Beijing. Inflation continued to be a concern despite passing its peak. And at one point in the year, it seemed like the rise in bond yields was about to bring a repeat of 2022.

Yet, what we see below was the final scorecard of asset class performance in 2023, including 12-month Australian term deposits.

What Figure 1 highlights is that while the decision to turn to term deposits made complete sense following the market chaos of 2022, it is one you then have to stick with for the whole year – even as you see opportunities unfold again.

In short, locking in certainty isn’t a bad thing in certain environments, but it’s good to understand that this would also lock out opportunity along the way.

In today’s environment, what else should investors consider instead of term deposits?

It might be helpful to separate the market environment into four simple regimes, as depicted in Figure 2.

These regimes can be either high or low in volatility, as well as high or low in the interest rate backdrop.

The top-left quadrant of the diagram was a lot like the post-GFC period, where interest rates were low and headed ever lower. Most of that period was benign in terms of market volatility, minus a few short and sharp events.

Term deposits were unattractive in that regime and most investors went searching for yield in riskier assets.

In such a regime, high-quality (investment-grade) floating rate corporate bonds are likely to do a better job at generating income than term deposits.

Not only does a low-volatility backdrop support asset classes such as credit, but a floating rate bond will also not be hurt by interest rate rises should the RBA start to tighten monetary policy.

The bottom-left quadrant of the diagram is like the Covid crisis of 2020, even though it was relatively short-lived. Interest rates were low at the start of the pandemic, but they were slashed further as global central banks tried to provide economic stimulus.

Government bonds were useful to own back then, even if it seemed pointless to own them before the volatility hit since the interest they carried was so low. It seems that no matter how low interest rates get, government bonds still rally when the economy comes under stress.

Term deposits were also not a bad option if capital preservation was all that was required, but they could not have delivered the capital gains that government bonds did during that troubled period.

In the bottom-right quadrant, we see a period of both high interest rates and high volatility. This is a lot like 2022, where being in cash or term deposits would have at least saved you from the drawdowns in other major asset classes.

However, high volatility can set in because of concerns about growth as well, which would prompt central banks to cut interest rates in a hurry. Here again, term deposits cannot offer that upside.

The last quadrant is on the top-right and is probably closest to where we are right now. Interest rates are high, but volatility is low.

Term deposits are easily beaten by fixed-rate corporate bonds in such an environment because not only will yields be higher, but the fixed-rate nature of those bonds will also help to deliver capital gains should rates and yields fall from here.

Figure 3 is a stylised illustration* of how a 12-month rolling term deposit, a five-year floating rate corporate bond, and a five-year fixed rate corporate bond are all likely to perform in a gentle RBA easing cycle.

For simplicity, let’s assume that each of these investments are taken on in a passive way.

For the bonds, the investor holds them to maturity and for the term deposit, they are simply rolled at the end of every year into a new 12-month deposit.

The income advantage of bonds over term deposits is clear.

Even at today’s higher interest rates, the higher yield from corporate bonds (the credit spread) helps bonds generate a better income stream for investors.

At lower interest rates, only the fixed-rate five-year bond can continue to deliver a consistent income stream.

By years two or three, that income stream will look very generous compared to market interest rates that will be on offer.

What is an “active income strategy”?

In each of the four quadrants illustrated in Figure 2, active income strategies have a role to play. Let’s first define what an active income strategy is.

In the first instance, the role of any income strategy is to deliver income. Therefore, the “income engine” of these strategies needs to be made up of assets that pay regular income.

You might think of shares that pay a dividend, but those dividends are at the discretion of the company which is not contractually obliged to pay dividends (or any set level of dividends).

That’s why Pendal’s income strategies like to rely on corporate bonds for their income engine.

Here, we mean high-quality corporate bonds with defined coupons. Hybrids don’t count because once again, they have a provision that allows issuers to skip coupon payments should certain conditions arise.

The income engine itself ought to be actively managed – a high-volatility regime calls for a more cautious approach to taking on more corporate exposures and vice versa.

But other levers are needed on top of that.

When yields are low and volatility is high, government bond exposures are beneficial, but only up to a point. As the reflationary episode after the pandemic showed, you don’t want to overstay your welcome in government bonds when yields are super low.

Equally, higher yields are not a shoo-in for government bonds either, as the last two years have shown.

Active portfolio management to help time when and how much government bond exposure to take should be a key feature of active income strategies. After all, government bond exposures serve different purposes for income funds (as seen in the different quadrants of Figure 2).

In some cases, it is to provide diversification and defensiveness to the credit risk in the portfolio. In other cases, it is to help boost income returns on top of what the income engine is able to generate.

Lastly, we believe an active income strategy should offer investors a compelling way to chase returns when there is more upside on offer.

Rather than adding on more credit exposures to the portfolio, which will have negative quality and liquidity consequences down the road, active income strategies ought to be able to stay liquid while participating in more of the upside.

That liquidity is not only beneficial to investors who may want constant access to their capital, but also beneficial to the agile positioning of the portfolio.

An income strategy that pursues additional exposures only by piling on more corporate bonds will find it hard to dial that back if the market takes a sudden turn for the worse.

That’s not a big problem if it’s only a short-term hiccup, but it could be difficult to resolve should a longer-term bear market set in.

On the other hand, an active income strategy that pursues the addition of exposures through only liquid means will be able to switch off that exposure very quickly and efficiently should there be an unexpected shock.

If it turns out to be only a short-term hiccup, the liquidity of those exposures permits a quick restoring of exposures. If it’s something more fundamentally negative, then those timely risk-reductions would have been hugely beneficial for preserving capital for investors.

Conclusions

Higher interest rates in 2023 made term deposits seem attractive. But despite a volatile year for markets, term deposit returns looked disappointing versus bonds and equities.

Term deposits are great for capital preservation, but by locking in your rate of return, you may also be locking out a lot of upside opportunity.

It may be helpful to consider active income strategies as an alternative to term deposits.

Their income engines comprise corporate bonds offering a compelling yield advantage to term deposits, even if interest rates stay where they are for a long time.

The other active levers within Pendal’s income strategies are also designed to mitigate risk and improve returns regardless of the market backdrop.

Best of all, unlike term deposits, investors won’t be locked in if better opportunities present themselves along the way.

About Amy Xie Patrick and Pendal’s Income and Fixed Interest team

Amy is Pendal’s Head of Income Strategies. She has extensive expertise and experience in emerging markets, global high yield and investment grade credit and holds an honours degree in economics from Cambridge University.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia. The team oversees some $20 billion invested across income, composite, pure alpha, global and Australian government strategies.

Find out more about Pendal’s fixed interest strategies here

About Pendal Group

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

The case for investing Thailand | How the federal Budget will affect inflation | A simple way to explain ESG investing