Where will interest rates be at the end of 2022 and 2023? Here’s a view from Pendal’s head of government bond strategies TIM HEXT

THE Reserve Bank is keen to make its recent dramatic about-turn on rates look like an evolution — and not the revolution it is.

This week’s statement edged us a little closer to a June hike. The RBA dropped its usual reference to being “patient” — and its commitment to highly accommodative monetary policy.

The statement finished with:

“Over coming months, important additional evidence will be available to the Board on both inflation and the evolution of labour costs.

“The Board will assess this and other incoming information as its sets policy to support full employment in Australia and inflation outcomes consistent with the target.”

We get Q1 CPI on April 27, which will likely be around 1.7% and 1.2% underlying.

We also get Q1 Wages Price Index on May 18. This will be less spectacular but will not stop a June tightening.

Meanwhile there is a good chance one of the next few unemployment numbers will be sub 4%.

The RBA will therefore be able to say in May that inflation is sustainably within its band in the medium term and can tighten in June.

A May hike is not impossible. But with a federal election and the desire to evolve the narrative June is odds on.

News to some

Many (including us) expected all this. But judging by yet another sell-off of around 0.15% it was news to some.

Three-year physical bonds (as measured by the April 2025 Commonwealth Bond) are now nudging 2.5%.

Ten-years are nearly at 3% and with a large new syndication of a 2033 Commonwealth Bond next week will likely break 3%.

Find out about

Pendal’s Income and Fixed Interest funds

The short end is now predicting cash rates to peak around 3.5% in early 2024.

If mortgage holders were aware of this impending doom house prices would be off 10% tomorrow.

Mortgage brokers I’ve spoken with are telling clients rates shouldn’t go up by more than 1% to 1.5%.

The average size of a new mortgage is now well over $600,000 – so an extra $20,000 a year in interest is coming borrowers’ way if markets are correct.

We still think a 2.5% cash rate is neutral.

Inflation is currently peaking. Although it will remain elevated into 2023 we think by late next year the RBA won’t likely need to push cash rates higher than 2.5%.

Rates should finish 2022 around 1.25% and 2023 around 2.5%.

Therefore markets are now cheap in the medium term.

However with the US Federal Reserve determined to keep pushing its rates higher – and ramping up the hawkish rhetoric – all markets globally will likely remain under pressure.

For those of us concerned with the short term as well as the medium term, the challenge will be to balance these two in the months ahead.

About Tim Hext and Pendal’s Income & Fixed Interest boutique

Tim Hext is a Pendal portfolio manager and head of government bond strategies in our Income and Fixed Interest team.

Tim has extensive experience in banking, financial markets and funding including senior positions with NSW Treasury Corporation (TCorp), Westpac Treasury, Commonwealth Bank of Australia, Deutsche Bank, Bain & Co and Swiss Bank Corporation.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia.

Find out more about Pendal’s fixed interest strategies here

About Pendal

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

In 2023, Pendal became part of Perpetual Limited (ASX:PPT), bringing together two of Australia’s most respected active asset management brands to create a global leader in multi-boutique asset management with autonomous, world-class investment capabilities and a growing leadership position in ESG.

What’s next for rates now the Reserve Bank has lost its patience? Assistant portfolio manager ANNA HONG explains

THE Reserve Bank this week took a small step towards a June rate hike.

In February and March, Governor Phil Lowe’s monthly statements referred to the board’s willingness to be “patient” as it “monitors how the various factors affecting inflation in Australia evolve”.

This month the word “patient” was conspicuously absent — though the omission was anticipated by the market.

“Over coming months, important additional evidence will be available to the board on both inflation and the evolution of labour costs,” Dr Lowe said.

“The board will assess this and other incoming information as its sets policy to support full employment in Australia and inflation outcomes consistent with the target.”

Some are expecting a hike in May. But the reference in this month’s statement to upcoming inflation data on April 27 and wages data on May 18 suggests a pre-election rate rise in May is unlikely.

It’s more likely next month’s statement will feature a further change of language that paves the way for a rate hike in June.

Only twice in Australian history has the RBA changed interest rates during an election — the first was a rate hike, the second a rate cut.

Find out about

Pendal’s Income and Fixed Interest funds

Both times there was a change in government.

Dr Lowe declined to cut rates in May 2019 — just 11 days before the last federal election — even though unemployment was drifting higher.

We expect this time will be no different.

The first election rate change occurred in November 2007.

Back then RBA Governor Glenn Stevens decided to raise interest rates 17 days out from the election to manage rising inflation.

This action — and two more rate hikes in early 2008 — helped Australian inflation peak in September 2008. Though the global financial crisis may have played a bigger role.

There are similarities between our current state and November 2007.

But inflation is now more supply-side led. And the RBA has this time chosen to remain dovish for longer, continuing to leave cash rates at 0.1%.

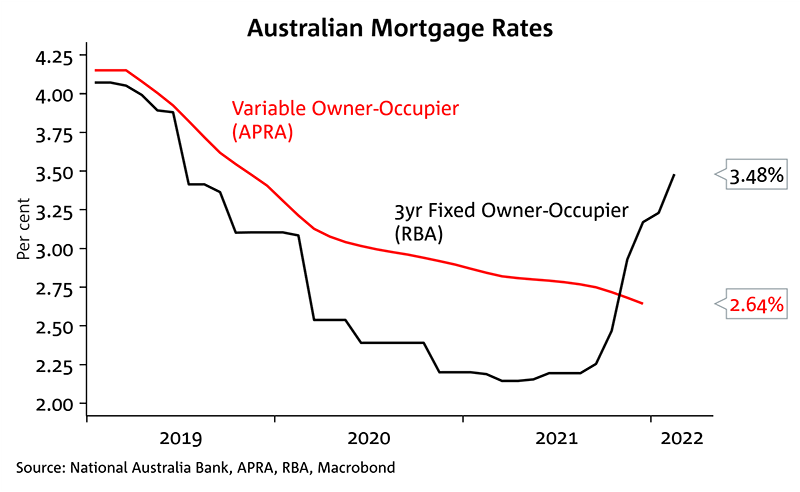

Despite that, the banks are already repricing for the future.

Advertised fixed rates have risen more than 60% from an average of 2.14% to 3.48%, according to APRA and RBA data.

In addition, the serviceability buffer was raised from 2.5% to 3% in the new home loan assessments.

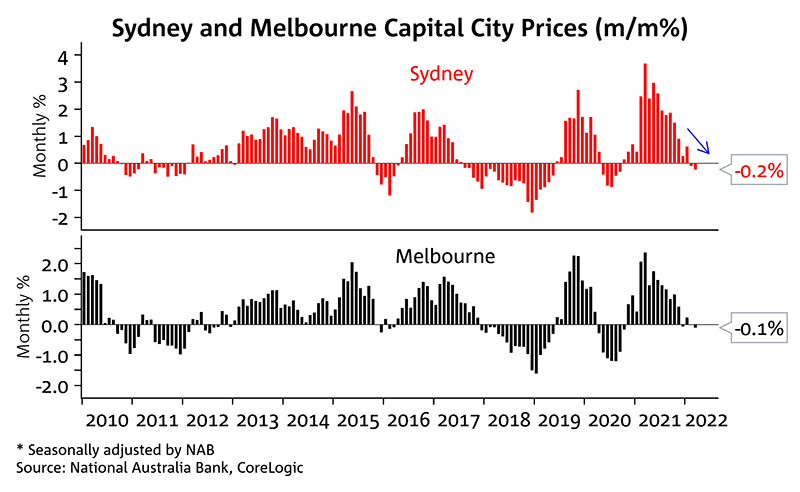

This has led to Sydney and Melbourne house prices cooling off, signalling that a phase of high capital gains may be behind us.

With a surge in fixed-rate borrowing well and truly behind us, variable rate rises are not far away.

The market is predicting more than 3% of rate hikes in the next few years. If that’s correct it will be interesting to see how mortgage holders cope.

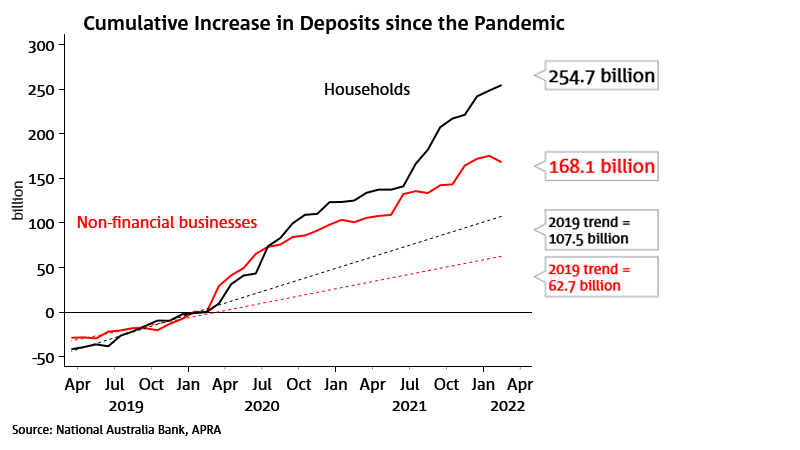

Household deposits continue to rise — up $255 billion since the pandemic — indicating Australian households have a war chest to cushion the blow.

But that’s not necessarily good news.

Delayed action in tackling inflation may result in a long, drawn-out battle to curb price rises fuelled by supply chain issues.

Will the supply chain issues ease sufficiently to prevent a protracted rate hike cycle?

The RBA will be cautiously watching this dynamic.

Looking ahead, we have the RBA Financial Stability Review coming up, in addition to the NAB Business Conditions and CBA Household Spending Intentions.

We are keen to understand the RBA’s assessment of the impending mortgage stress and its concerns around the ability of the wider economy to withstand rate rises.

NAB Business Conditions and CBA Household Spending Intentions will provide a good gauge on forward-looking business and consumer confidence.

If those indicators remain elevated we may see costs of living get another leg up.

Portfolio implications

For many investors, the current dilemma in portfolio decisions relates to the relative importance of the geopolitical instability in Europe versus the inflation trajectory.

With Australian Government 10-year bonds appearing to have found support in the 2.8% to 3% range, a balanced portfolio can increase its defensiveness knowing that most of the inflation concerns are already priced in.

Furthermore, 10-year real yields are now positive (more than 0.3%).

That carry can provide good protection for investors.

About Anna Hong and Pendal’s Income and Fixed Interest team

Anna Hong is an assistant portfolio manager with Pendal’s Income and Fixed Interest team.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia. In 2020 the team won the Australian Fixed Interest category in the Zenith awards.

With the goal of building the most defensive line of funds in Australia, the team oversees A$22 billion invested across income, composite, pure alpha, global and Australian government strategies.

Find out more about Pendal’s fixed interest strategies here

About Pendal Group

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Here are the main factors driving the ASX this week according to portfolio manager Jim Taylor. Reported by portfolio specialist Chris Adams.

Find out about Pendal Focus Australian Share Fund

Find out about Pendal’s sustainable Pendal Horizon Fund

THERE’S been increased chatter about yield curve inversion and potential recession, on top of speculation around inflation, commodity prices and the conflict in Ukraine.

Fed Chair Powell is showing signs of frustration with the view linking curve inversion to an inevitable recession — particularly since recent data indicates the US economy remains very strong.

The minutes from March’s Federal Open Market Committee meeting — due this week — are expected to contain details on the Fed’s thoughts about quantitative tightening.

Australian data also suggests ongoing economic strength, but the signs are more worrying in Europe. German data in particular shows an increased risk of recession.

Policy decision and timing in Europe are complicated by a strong inflationary pulse. This is underpinned by continued capacity constraints, second-order effects of the Ukraine war and China’s Covid response.

Despite all this US equity markets remained largely unchanged. The S&P 500 gained 0.1% last week.

The Australian market continued its bounce. The S&P/ASX 300 lifted 1.2% last week on the back of a 3.62% increase in resources.

Australian economy

A strong economic recovery has prompted a $150 billion expected improvement in public finances for 2025-26. This is underpinned by lower unemployment benefits and higher income from commodities.

Last week’s Federal budget set aside about 75% for fiscal repair and deployed 25% into new spending initiatives. This comes on top of an already strong economy.

Measures addressing the cost of living were probably the most significant feature, totalling around $10 billion.

This equates to 1% of household income for the next six months and includes:

- Expanded tax offsets worth $420 for about 10 million low or middle income taxpayers, payable in the second half of 2022.

- One-off $250 payment for about 6 million welfare recipients to be paid in April

- 50% reduction in fuel excise for the next six months

Australian retail sales increased 1.8% month-on-month in February — better than expectations of 0.9%.

Sales now are only 0.7% below the pre-Omicron peak in November. NSW did best with 3.6% growth and WA was the laggard at -2.9%. Fashion and eating out dominated with about 15% growth.

Statistics released during the week indicate housing credit growth continues to accelerate to a post-GFC high, while residential approvals have rebounded strongly from a Covid-induced delay.

It is also worth noting that the Budget expanded the First Home Loan scheme. Property prices have rolled over modestly.

Business credit growth is also strong, running at 10% year-on-year. This is also a post-GFC high.

Other data showed household wealth was growing as quickly as ever.

Pendal Focus Australian Share Fund

Now rated at the highest level by Lonsec, Morningstar and Zenith

On the jobs front, vacancies are up 47% year-on-year to a record high of 424,000.

The ratio of job vacancies to unemployed persons has also spiked to a record high 75%.

Normally for every job vacancy there are three-to-four unemployed people available. Now there are only about 1.25.

The transmission of this feature of the current cycle into wage growth continues to be very muted. But we are keeping an eye on negotiations surrounding minimum wages.

Australian businesses are still reporting that the tight labour market is a key constraining factor in their operations.

US economy

In the US 431,000 new jobs were added in March based on payroll data.

This was below expectations, though the January and February figures were revised up 95,000.

This marks the 11th consecutive month of job gains above 400k — the longest stretch since data was first recorded.

The participation rate also climbed 0.2% to 62.4% — compared to a pandemic trough of 60.2% in April 2020. There is evidence that women and retirees continue to return to the workforce.

The unemployment rate fell to 3.6%, one of the lowest on record.

Average hourly earnings rose 0.4%, after rising only 0.1% in February. The annual growth rate remains high at 5.6%, but all eyes will be on April to see if the trend of moderation continues.

Core PCE inflation rose 0.35% month-on-month in February and is running at 5.4% year-on-year versus 5.2% year-on-year in January. This was in line with consensus and is the lowest monthly gain since September 2021.

The breadth measures moderated substantially in contrast to the CPI data, due to different index constructs. Specifically the PCE has a higher weighting to healthcare and a lower weighting to petrol and housing which results in lower overall readings of PCE versus the CPI.

Indicators of manufacturer and retailer pricing power remain at extremely high levels. It is unlikely that inflation can be slowed materially until this recedes. At this point there is little evidence of demand destruction caused by rising prices.

The Dallas Fed’s Exuberance indicator is providing a different perspective on the state of the US housing market.

While materially lower than pre-GFC levels, it still shows just how strong the environment has been compared to any other era going back to 1981.

The move in the mortgage rate is rapidly impacting equity values in the space, though current activity levels remain very robust.

Europe and China economies

Surveys of economic activity in the Eurozone and China point to significantly slower activity.

The Ukraine war and higher commodity prices are dragging on Europe, while Beijing’s zero-Covid policy is seeing further shutdowns in China.

We expect the economies of the EU and the US to begin to diverge materially from here, given the much lower exposure of the US economy to these headwinds.

Sustainable and

Responsible Investments

Fund Manager of the Year

About Crispin Murray and Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia. Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

How the federal budget will affect rates and bonds, why ASX stocks and Australian bonds look good, how to find competitive advantage among international shares

Not surprisingly in an election year, the federal government is already spending its recent windfall in the Budget. TIM HEXT explains what that means for rates and bonds

WHETHER you like the federal government or not it’s a fact their time in power has not been a happy one.

Natural disasters and pandemics have defined the past three years.

But some good fortune has finally come their way in the past year as Australia’s terms of trade have boomed.

Even the Ukraine conflict, which of course is a terrible disaster, has seen prices take off for many of our exports.

This has delivered the government a huge windfall via company taxes and some royalties. Added to this is the massive fiscal spending delivering a stronger economy domestically.

Over the course of four months or so, the federal Budget has improved by about $115 billion over the next four years.

Not surprisingly with an election imminent Treasurer Josh Frydenberg (pictured above) has spent $30 billion of it — on top of a previously announced $16 billion in pre-election handouts.

Find out about

Pendal’s Income and Fixed Interest funds

What it means for rates and bonds

From a bond market perspective this adds further fuel to an already strong economy.

Dealing with supply shocks by subsidising demand only helps keep prices elevated.

But politics trumps economics.

The 22c fuel excise reduction plays to this although I doubt Australia’s reduced demand will impact global prices much.

The RBA is already on the precipice of finally admitting they need higher rates — and this budget will only encourage them more.

But with markets forecasting 2% rates in Australia by early next year — and 3% by the end of next year — there is quite simply too much priced in.

We think the US will get to those levels, but investors assuming Australia must follow are missing a couple of factors.

Firstly, our inflation is significantly lower.

Secondly, our floating rate mortgage market means any rate hikes have more impact sooner.

It may seem strange but when the RBA actually starts to moderately tighten rates, bond markets will likely rally.

About Tim Hext and Pendal’s Income & Fixed Interest boutique

Tim Hext is a Pendal portfolio manager and head of government bond strategies in our Income and Fixed Interest team.

Tim has extensive experience in banking, financial markets and funding including senior positions with NSW Treasury Corporation (TCorp), Westpac Treasury, Commonwealth Bank of Australia, Deutsche Bank, Bain & Co and Swiss Bank Corporation.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia.

Find out more about Pendal’s fixed interest strategies here

About Pendal

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

In 2023, Pendal became part of Perpetual Limited (ASX:PPT), bringing together two of Australia’s most respected active asset management brands to create a global leader in multi-boutique asset management with autonomous, world-class investment capabilities and a growing leadership position in ESG.

Here are the main factors driving the ASX this week according to our head of equities Crispin Murray. Reported by portfolio specialist Chris Adams.

Find out about Crispin’s Pendal Focus Australian Share Fund

Find out about Crispin’s sustainable Pendal Horizon Fund

EQUITY markets continue to bounce despite increasingly hawkish rhetoric from the Fed.

The S&P/ASX 300 gained 1.6% last week and is now up 0.8% for the 2022. The S&P 500 gained another 1.8% to be down 4.3% for the year. The NASDAQ is still down 9.3% in 2022 after gaining 2% last week.

It’s remarkable that this takes place against a sharp increase in two-year US bond yields, a surging oil price and a US dollar grinding higher.

These factors are usually headwinds for equity markets, as seen in late 2018.

There are several potential reasons for the ongoing recovery in equities. These include:

- Sentiment and positioning being too negative, leading to a technical bounce

- A poor outlook for bonds, driving rotation to equities

- Equity inflows remaining positive despite softer investor sentiment indicators

- Economic growth supporting earnings, underpinning a view that the market can de-rate without a bigger correction

- A belief that the pre-requisites for economic slowdown are being put in place and rates will not need to rise as far as the Fed is saying

We remain wary in the near term. The Fed needs financial conditions to tighten – and rising equities works against this objective.

Potential scenarios

We see three potential scenarios that are more likely than a continued strong equity market rebound:

- The market consolidates and treads water for a few months as we gauge central bank ability to contain inflation. This would be consistent with the history of US bull markets, which shows that the third year is often lacklustre — particularly if the first two are very strong. As an aside, if we are near the end of the post-March 2020 rebound it would be by far the shortest bull market in US history.

- The market falls back to set new lows reflecting falling liquidity, concerns over slower growth dragging on earnings and a lack of certainty. Slower economic growth eases inflationary pressure, allowing interest rates to peak at levels the market or Fed are currently expecting, without triggering a recession. This enables a market recovery. Fed chair Jerome Powell notes there have been similar “soft landings” in US monetary history in 1967, 1984, 1994 and 1998. Each involved the yield curve going flat, with the Fed funds rate subsequently getting cut.

- Similar to scenario two — except we end up in recession due to policy error or as the only way inflation can be contained. History indicates that when you see oil rise more than 100% year-on-year it triggers a recession. So too does persistent inflation at current levels.

Pendal Focus Australian Share Fund

Now rated at the highest level by Lonsec, Morningstar and Zenith

US monetary policy

Powell last week noted the need to move “expeditiously” back to a neutral rate setting.

This kind of language is usually a signal. It’s widely interpreted as an increased chance of a 50bps move in rates in May and possibly in June.

Powell also reiterated that the Fed would need to go above the neutral rate, which is currently estimated at 2.5%.

This is all about getting to the neutral rate as quickly as possible, since anything below that is still stimulatory. The challenge is doing so without prompting a financial shock.

As discussed last week, this rally in equities and credit is loosening the overall Financial Conditions Index. By some measures, it has unwound a third of the recent tightening. The Fed will need to engineer more tightening to achieve its goals.

The market is moving to a view that the Fed is worried real rates run the risk of being too low through 2022 — and therefore the best way to avoid a recession is faster near-term rate increases plus early quantitative tightening.

Inflation outlook

There are small positive signs that freight rates may be easing at the margin. A slowing economy will help this process.

This is countered by continued pressure in commodity markets.

The focus is shifting to food inflation, where we see:

- A sharp rise in fertiliser prices, which are tied to gas prices. The Tampa contract (a measure of ammonia prices) is up 43% in April compared to February/March.

- Glyphosate prices are already high, affecting weed control

- The price of diesel — necessary to run equipment — has more than doubled in the past 12 months

- Labour shortages

- Propane storage levels are at their lowest levels in seven years. Propane is used in about 80% of grain dryers to reduce moisture and allow storage.

The UN Food and Agriculture Organisation’s Food Price index has hit all-time highs, eclipsing the previous highs which played a role in the Arab Spring. This is before many of the effects of the Ukraine conflict have flowed through.

Europe

The European economy continues to weaken based on sharp falls in a number of sentiment indicators.

For example, the German IFO Business survey of future business conditions reported its biggest ever single-month decline.

Sentiment indicators are not far off what was seen at the onset of the Covid pandemic.

We are now seeing some fiscal policy response, predominantly in the form of fuel subsidies. The latter may be more effective politically than economically, given they underpin demand in a supply constrained environment.

Despite fiscal moves the chance of recession in Europe is still priced at greater than 50%.

Australia

There is speculation the federal budget will include a temporary reduction in the fuel excise (currently 44.2c per litre). A 5c cut for six months would cost about $1 billion.

Infrastructure spending of up to $18 billion is expected. But it’s hard to see this flowing through quickly due to difficulties in executing projects and the tight labour market.

More broadly we reiterate our view that Australia is better placed than many other countries.

There is less need to raise rates, allowing them to remain lower for longer.

The economy is benefiting from pent-up demand as restrictions roll back. Australia is largely self-sufficient in key commodities and is a beneficiary of rising prices here.

This underpins our relatively positive view of the domestic equity market.

This is reinforced by the degree to which the Australian market has underperformed the S&P 500 since the GFC.

While recent outperformance has been material, it is a blip on a longer-term view. This gives us confidence in the potential for further outperformance.

Sustainable and

Responsible Investments

Fund Manager of the Year

Markets

A continued rise in 10-year US government bond yields (up 33bps last week to 2.48%) has taken them back to the top end of a 30-year downward trend.

The consensus is bearish — with a view that yields rise to 3%.

Sharp moves such as last week’s are often followed by a period of retracement, so we wouldn’t be surprised if there was some relief in the near term.

The rise in 10-year yields signals that the US market is still not of the view that we are entering a downturn. This may explain why equities have been able to rally through this increase.

It is worth highlighting how rate-sensitive sectors have been affected in the US.

Homebuilders continue to fall on expectations of a housing downturn, as have consumer discretionary companies seen as tied to housing, such as Home Depot. We have not really seen the equivalent of this in the Australian market.

Australian equities continued to grind higher last week.

Resources (+6.3%) and Energy (+5.3%) recovered from the prior week’s fall. Technology (+3%) began to bounce, but remains the weakest sector over 2022 to-date, down 15.5%.

About Crispin Murray and Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia. Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Understand debt, disruption and demographics and you’ll understand why it could be a good time to buy bonds. Pendal’s ANNA HONG explains

AUSTRALIAN 10-year bonds yields are at a four-year high.

Where will they go from here?

To answer that we need to ask another question: what level of interest rates can the Australian economy withstand?

We think a neutral cash rate of 1.5% to 2% is bearable. But 3% will be an overshoot that strains the Australian economy.

Under those conditions, the Australian Government 10-year bond yield becomes interesting at current levels around 2.75%.

Why? Because the global trajectory of three key factors — debt, disruption and demographics — hasn’t changed despite recent events, especially in developed economies.

Demographics

Even though headline population growth is positive, it’s largely driven by net migration which has been impacted by Covid.

Australia’s fertility rate is below the replacement rate and life expectancy is on the rise. This means we have an ageing population. Adding higher interest rates to that mix will significantly impact GDP growth.

Disruption

Technology has transformed every facet of our lives and it’s not about to stop.

With continued technological progress we can expect goods prices to move downwards as we reap the rewards of manufacturing and logistical efficiencies. (Once the current supply-shock eases of course.)

This means that while inflation is a now-problem, it will not be a long-run issue which central banks need to tackle with never-ending rate hikes.

Debt

Finally, consider the debt overhang.

As a nation we continue to indulge in our favourite activity – buying property.

The Australian household debt picture is nuanced, however.

We’re one of the most indebted nations in the world, but we’re also rather good at things like pre-payment, so we can get ahead of the debt mountain.

This pragmatism will lead to many households tweaking spending decisions as interest rates rise. At a time when disposable income has already been hit by oil prices, the RBA will be cautious about adding further strain.

The dynamics of Debt, Disruption, Demographics means that the most probable outcome is a neutral cash rate of around 2%.

Rates higher than that will lead to curtailing of GDP growth, straining the Australian economy.

This may be welcomed in restraining inflation in the near-term but not in the medium-term.

Portfolio Implications

With current Australian Government (ACGB) 10-year bond yields at 2.75%, aggressive rate hikes are almost fully priced in.

Cash sitting on the sidelines will find value here as the Reserve Bank continues to delay rate hikes.

Economists’ consensus has the first hike occurring in August — therefore investors may need to wait until late 2023 for cash returns to exceed 1.5%.

The risk versus reward makes this an attractive option for balanced portfolios.

Bonds are still a defensive instrument, given forward uncertainties, especially in the geopolitical space.

Investors will need them in their portfolios.

Any investor currently underweight bonds should be looking to get back to neutral. We think the next three-to-six months may bring levels which are attractive for investors looking to go overweight bonds.

Find out about

Pendal’s Income and Fixed Interest funds

About Anna Hong and Pendal’s Income and Fixed Interest team

Anna Hong is an assistant portfolio manager with Pendal’s Income and Fixed Interest team.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia. In 2020 the team won the Australian Fixed Interest category in the Zenith awards.

With the goal of building the most defensive line of funds in Australia, the team oversees A$22 billion invested across income, composite, pure alpha, global and Australian government strategies.

Find out more about Pendal’s fixed interest strategies here

About Pendal Group

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Get ready as China edges away from Covid-zero, what rate expectations mean for bond buying, the likely path for ASX stocks and which global equities sectors look good

Here are the main factors driving the ASX this week according to our head of equities Crispin Murray. Reported by portfolio specialist Chris Adams.

Find out about Crispin’s Pendal Focus Australian Share Fund

Find out about Crispin’s sustainable Pendal Horizon Fund

THE S&P 500 gained 6.2% last week, recouping half of its year-to-date decline.

This was most likely a combination of:

- Lower commodity prices offering hope that the disruption from the Ukraine conflict may be less than feared

- The Fed’s comments post rate hike prompting greater confidence that it can balance policy tightening without triggering recession

- Signs the Covid outbreak in China may be contained

- Policy signals from Beijing which were supportive of equity markets

The Australian market was less leveraged to this bounce, but still gained 3.3% (S&P/ASX 300). It is now down only 0.8% for the calendar year to date.

Bond markets were not as optimistic as yields continued to rise. US 10-year government bonds rose 16bps to 2.15% and the 10y–2y yield curve flattened further to 21bps.

We still see the recent bounce as a counter-trend rally.

Policy makers are treading a difficult path to resolve inflation without sending the economy into a downturn. This is driving uncertainty which we expect will weigh on markets in the near term.

This is exacerbated by the removal of liquidity.

In this vein, the Fed’s rate hike this week has not tightened the overall Goldman Sachs Financial Conditions Index, given the offsetting effect of stronger equity markets.

To put this in context, conditions have only tightened half as much as in the previous cycles of 2015 and 2018 — yet we are at a far looser starting point and inflation is a much bigger problem.

To resolve the inflation problem financial conditions need to tighten further, which is likely to act as a cap for the market.

US monetary policy

The Fed raised rates 25bp last week as expected. It was an 8-1 vote with one dissenter wanting 50bp. The overall message was seen as hawkish, with strong rhetoric on inflation.

It is worth noting the signals from changes in the Fed’s median forecasts from the meeting:

- Core inflation (ex food and energy) is currently running at 5.2% and is expected to end CY22 at 4.1%. This is up from a 2.7% expectation in December 2021. It is expected to be 2.6% at the end of CY2023, up from 2.3% in December.

- The US GDP growth forecast for CY2022 was cut from 4.0 to 2.8. The market is currently expecting sub 2% growth.

- The Federal Open Market Committee moved from expecting three to four hikes in CY22 to seven. The Fed Funds rate is expected to be 1.9% at the end of CY22, versus 0.9% in December. The market was expecting a signal of six hikes.

- Rates are expected to peak at 2.8% in 2023. The December expectation was a peak of 2.1%, in 2024

Year-end inflation expectations have effectively risen 1.4% since December, yet expected rates are up only 1%. So real rates will still be -2.2% at year-end, versus an implied -1.8% in December 2021.

Chair Jerome Powell said the Fed would devise a plan for quantitative tightening at their next meeting (May 3-4), to be implemented shortly thereafter. They have previously signalled this will equate to a 25bp rise in rates.

It is also worth noting that the Fed’s balance sheet has continue to expand even in the last week, as Quantitative Easing has only just come to an end.

Powell’s messaging was hawkish and conveyed a resolve to beat inflation akin to Mario Draghi’s ‘whatever it takes’ speech.

He noted the Fed was “acutely aware of responsibility to bring inflation down” and that real rates could be marginally positive by the end of CY23.

This provided some reassurance to markets.

Pendal Focus Australian Share Fund

Now rated at the highest level by Lonsec, Morningstar and Zenith

Despite the Fed’s current view that rates will peak at 2.8%, the market is implying a 2.3% peak in 2023. This highlights how the market is still shaped by the post-GFC policy experience.

However there is an inconsistency in the Fed’s messaging. Its own forecasts indicate inflation will fall with no rise in unemployment (which remains at 3.5%).

The Fed does not see rates needing to rise above 3% this cycle — ie no need to go above “neutral”. This is despite inflation running far hotter and labour markets tighter than in previous hiking cycles.

To reconcile this inconsistency we need to believe the supply side resolves the problem and dampens inflation and that the corporate sector will be able to resist efforts by labour to recoup the erosion of real wages.

The equity market appears to believe this — as reflected in its bounce.

In our view the Fed really has no idea what rates will need to rise to.

The current plan is to get back to neutral — just more quickly than previously expected. At that point the Fed will have a better idea of how sensitive the economy is to rising rates.

There is a wide range of potential outcomes.

There were nine hikes in the 2015-2018 cycle and 17 between 2004-2006.

We can gain a different perspective on US rates through application of the Taylor rule. This looks at the GDP deflator and slack in the economy to assess where interest rates should be.

Even adjusting for one-off factors driving inflation the implied interest rate is 5%. This is effectively double where the market expects rates to peak.

There are many reasons why this may not play out. But it highlights potential uncertainty on the path for rates in this environment.

European policy

The Bank of England also raised rates last week. But it sent a far more dovish signal, indicating the economy will not be able to absorb the number of rate increases currently priced in.

The only way rates will rise that much is if we see a substantial fiscal stimulus in the upcoming budget.

Sustainable and

Responsible Investments

Fund Manager of the Year

European Central Bank president Christine Lagarde changed the previous week’s more hawkish message. There is now greater emphasis on watching the economy data before acting.

The market is ascribing a 50% chance of recession in Europe by the end of the year, reflecting the already slowing data.

China

Chinese equities were extraordinarily volatile last week — technology particularly so. This is worth watching since it’s been a lead for the rest of the tech sector.

Chinese tech had fallen 80% from its peak — akin to the NASDAQ bust of the early 2000s.

The sector fell almost 30% in the previous week before bouncing 50% last week and gaining about 30% in a day.

The catalyst was a statement from the head of the Financial Stability Committee which addressed five of the key issues weighing on the market.

In nutshell it emphasised:

- Stabilisation of the property market

- Ensuring new loans would continue to be issued

- Concerns over ADR de-listing would be addressed, with the US and China in dialogue to resolve accounting issues

- Commitment to make regulations on the technology sector more transparent

- Efforts to resolve HK regulatory issues

Concerns over Covid diminished somewhat as case numbers appeared to be brought under control.

Commodities

We saw substantial volatility in commodity prices last week. Oil dropped from US$113 a barrel to US$98 before rebounding to US$108.

Price volatility is being driven primarily by:

- Chinese lockdowns reducing demand by 0.5m barrels-per day (bpd).

- Signs that more Russian oil is finding its way into global markets via back channels. It is now estimated that 1.5m bpd is not finding its way into markets, rather than the previous 2.5m estimate.

- The huge spike in volatility has triggered more margin calls, which has led to some position liquidation

Volatility will continue to be high, but we expect prices to trend higher again due to the low level of spare inventory, the ongoing threat of further sanctions and the risk of an unexpected act threatening supply.

US economy

The data remains supportive, but it’s worth watching some softening (from a high base) in the trucking survey which is a decent lead indicator. There is also a slowdown in sales from European-facing companies.

Housing signals remain positive. Prices are up 15% year-on-year. The supply of houses on market remains at historical lows — and well below the levels seen running into the GFC.

There are also positive signals from US airline carriers. Air traffic is rising above previous expectations, though the market remains wary of the effect of oil prices.

Markets

While equity markets have bounced, we have doubts this can be sustained for the reasons above.

In our view the bounce lacks the conviction seen in March 2020 and Dec 2018, suggesting markets may still fall back.

From a technical perspective the breadth of the market rebound was reasonable, but not compelling. Also, the put/call ratio in option markets, as an indicator of fear, never rose to extreme levels.

Markets are running into technical resistance levels. This will be another thing to watch.

The Australian market was driven by technology, financials and healthcare last week. The headline return was decent given the decline in the resource sector and energy being flat for the week.

Rising yields and fewer concerns on some form of global financial shock helped the financials. Stock moves were mainly driven by a reversal — ie the names that had performed the worst bounced back the most.

About Crispin Murray and Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia. Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

The US Federal Reserve has raised interest rates for the first time since 2018. Pendal’s head of government bond strategies TIM HEXT explains what it means

THE US Federal Reserve raised rates by 0.25% this morning, as expected.

However the Fed’s forecast for future rates were also raised, slightly catching the markets by surprise.

It was viewed as a ‘hawkish hike’, as we expected. You cannot begin a hiking cycle downplaying its impact – you need overall conditions to tighten.

A couple of interesting points.

The Fed is forecasting (via their dot plots) rates to be 1.9% by the end of this year – this means seven hikes in the next seven meetings.

They then expect 2.8% by the end of 2023. But by the end of 2024 they expect 2.4%. Neutral rates are generally considered to be around 2%, although that too is dynamic.

The Fed expects inflation to be 4.3% at year end and then 2.7% in 2023 and 2.3% in 2024.

This will be achieved through not only tighter policy but base effects (high numbers from a year ago drop out of year-on-year numbers) and of course reopening of supply chains.

We think these estimates are reasonable, though we agree with the Fed that surprises may be more to the upside. Markets believe inflation will average 2.8% for the next ten years, so are less convinced.

Sustainable and

Responsible Investments

Fund Manager of the Year

In the Q&A with Chair Powell there was a lot of criticism about the rapid change of course.

As recently as November the message was that the Fed could be patient as inflation pressures were largely transitory. I am paraphrasing, but Powell’s response was that the situation was rapidly evolving.

As we mentioned numerous times recently it seems the inflation impact of events in the Ukraine has outweighed the risk-off or growth impact in the Fed’s mind.

Where does this leave the RBA?

As recently as this week the RBA minutes from the March meeting were maintaining the line, or as some would say fiction, that “while inflation had picked up, members agreed it was too early to conclude that it was sustainably within the target band.”

Sounds like the Fed in November.

The Q1 CPI in Australia will be released on April 27. Headline is likely to be 1.4% or 4.3% Y/Y.

We think the RBA rhetoric will change in May to be that “inflation appears to be sustainably within the 2-3% band” paving the way for a June hike.

They will likely go 0.4% first off taking the official cash rate to 0.5%. We would then expect hikes in August and November (after the next two CPIs) to finish the year at 1% cash.

There is a chance the RBA tries to cling on a little longer and the first hike is August, but either way rates finish the year at 1%.

Find out about

Pendal’s Income and Fixed Interest funds

In the medium term it is interesting that curves are now flat in the US — that is, five year rates in the US are now flat to the 10-year rate at around 2.15%.

This suggests markets believe the Fed in that rates will peak in 2023 before levelling out of even coming back down.

This normally happens later in a hiking cycle but in these days of high transparency markets are far more forward looking.

Implications for Investment Markets

Equities seem to have taken the Fed actions in their stride, maybe also encouraged by the oil price tapering.

Economies remain strong and earnings healthy, although no doubt talk of slowdowns will build with the rate hikes. The Fed did downgrade their GDP forecast for 2022.

Australian 10-year bonds are now around or just above 2.5%.

As mentioned before this is not necessarily cheap but I am prepared to say bonds are no longer expensive and that balanced portfolios should be reducing underweights.

Bonds are still a defensive instrument and if the hiking cycle eventually produces a recession, as seven out of the last 10 hiking cycles in the US have, investors will need them in their portfolios.

Finally, cash is back and is short-priced odds to be the top-performing asset class in 2022 (ignoring some commodities).

While mortgage holders will suffer from higher rates, for every $3 of debt there is $2 of domestic savings (the other $1 borrowed from offshore).

Cash rates will remain below inflation for a long time yet, eating away at purchasing power, but there may at least be some relief for savers.

About Tim Hext and Pendal’s Income & Fixed Interest boutique

Tim Hext is a Pendal portfolio manager and head of government bond strategies in our Income and Fixed Interest team.

Tim has extensive experience in banking, financial markets and funding including senior positions with NSW Treasury Corporation (TCorp), Westpac Treasury, Commonwealth Bank of Australia, Deutsche Bank, Bain & Co and Swiss Bank Corporation.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia.

Find out more about Pendal’s fixed interest strategies here

About Pendal

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

In 2023, Pendal became part of Perpetual Limited (ASX:PPT), bringing together two of Australia’s most respected active asset management brands to create a global leader in multi-boutique asset management with autonomous, world-class investment capabilities and a growing leadership position in ESG.