PENDAL has been recognised – and awarded – at the 2024 Zenith Fund Awards

Pendal was recognised in the Multi Asset – Diversified and the Sustainable and Responsible Investments (Income) categories – the latter of which it won.

“As has been our focus in previous years, [the] awards recognise and honour excellence in funds management across all asset classes and disciplines,” said Zenith managing director Jason Huddy.

“We believe that this is fundamental to continuing to raise the standards of funds management in our industry for the ultimate benefit of investors.”

To view the full list of 2024 winners, visit the events page

Find out about

Pendal Property

Securities Fund

Find out about

Pendal’s

cash funds

Find out about

Pendal Global Emerging Markets Opportunities Fund

Here are the main factors driving the ASX this week, according to Pendal portfolio manager PETE DAVIDSON. Reported by investment specialist Chris Adams

- Find out about Pendal Focus Australian Share fund

- Crispin Murray: Five key questions for 2024 (and how we’re going so far)

WITH global monetary policy (ex-Australia) easing and more fiscal stimulus from China, it appears as if the economic and market cycle will hold or possibly even re-accelerate.

Equity markets are optimistic as we approach year-end, rebounding from the August correction which was driven by some weaker US data points and the Yen carry-trade unwind.

This increased level of confidence saw the S&P 500 rise 0.87% and the S&P/ASX 300 rise 0.81% last week. The latter is up more than 8% since the start of July on a total return basis.

This optimism has been partly fuelled by positive economic surprises, especially since early September. Most prominent are the latest employment reports in the US and Australia, which suggest labour market concerns were overdone.

Betting odds are pointing to a Trump victory and the market seems more comfortable with this outcome.

This looks set to be the closest election in US history.

Harris is picking up the college-educated and female vote, while Trump is gaining amongst non-college educated males and minorities. Gold may spike if there is post-election uncertainty.

High valuations and already bullish sentiment pose risks to the market. However, there is no clear catalyst for a downside move and the global rate cycle (ex-Australia) is helping.

US macro and policy

On the whole, stronger US data is pointing to a soft or even no-landing scenario.

Retail sales data suggests the US consumer is still looking good, the Fed is now cutting, and the fact that monetary policy is becoming less restrictive is helpful.

Interestingly, the savings rate has been revised up to 4.8%, which supports a stronger consumer.

That said, bank credit is tight and most data doesn’t reflect what is happening in the small business economy, where there are anecdotes of pressure.

The housing market is also soft.

The US labour market is interesting. Businesses have been pulling back from hiring activity over the past year to cut costs, despite GPD growth. This has also been reflected in falling aggregate hours worked.

With fewer people quitting their jobs, it is plausible that a slowdown in the labour market will be seen in the form of layoffs this cycle, which does feed into the risk of recession.

China macro and policy

China appears to be shifting gear with a set of new policies from late September to support its economy and property market.

The measures include bank reserve requirement ratio cuts, capital injections to banks, as well as moves to support local government debt restructuring and boost the capital market.

There have been additional policies focused on supporting and stabilising the property market, including funding to reduce the inventory of unfinished and unsold housing stocks.

These measures appear targeted at easing specific pressure points, such as local government balance sheets and unsold housing.

Thus far, there has been no large consumer-related fiscal package. But at least there is some movement at the station.

Markets are anticipating additional stimulus packages for housing and the economy. This can’t hurt the Aussie resources sector.

However, there is the risk that a US tariff package could take as much as 2% off growth.

Beijing is watching the US Presidential Election closely and, if tariffs look likely, may implement more fiscal and monetary in response.

Europe macro and policy

The labour market in Europe (EU) remains tight, despite very low GDP growth.

Consumer spending is tilting towards the labour-intensive services sector.

The German economy remains weak – as does its manufacturing sector, even relative to the rest of the EU. Yet, its unemployment rate is only 0.5% above the cycle low and labour costs continue to rise at a pace inconsistent with sustained 2% inflation.

One factor is the bloc’s severe energy pricing disadvantage, with the European Commission estimating that industrial power prices in the EU are 158% higher than in the US, while industrial gas prices are 345% higher.

Australia macro and policy

Australia’s GDP growth remains positive but muted, not helped by the fact that it is one of the few places in the world where financial conditions (as measured by the Goldman Sachs Financial Condition Index) have increased over the past twelve months – and markedly so.

The labour market remains in decent shape, though growth in government jobs in areas like education and healthcare are a key factor.

The yield curve shows that confidence around rate cuts is waxing and waning – with expectations of cuts ticking down in the past week.

Further rate cuts overseas might assist. Some indicators are pointing to higher unemployment, which might also make the outlook for rate cuts more likely.

Housing finance approvals are rising in Australia, even though the RBA has not yet started to ease policy.

However, the strongest growth is in approvals for either owner-occupiers or investors to buy established dwellings. Finance approvals for the construction of new dwellings remain weak.

Markets

The outlook for FY25 ASX earnings remains muted, due largely to the resources and banking sectors. Industrials are expected to be provide some positive offset.

Meanwhile, investor sentiment is strong – with a benign outlook for inflation and growing confidence in a soft-landing.

So the market seems quite happy to overlook near-term earnings and is prepared to pay high valuations for banks, if not for resources.

We are into AGM season; most companies are simply affirming previous guidance.

Some notable improvers on AGM Day were AMP (better flows), Evolution Mining (a beat in production, Red Lake going better) and Bank of Queensland (low impairments).

About Crispin Murray and Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia. Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions.

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

Here’s what the latest jobs data means for markets, according to Pendal’s head of government bond strategies TIM HEXT

- Why bonds, why now? Pendal’s income and fixed interest experts explain

- Browse Pendal’s fixed interest funds

THE Australian job market continued showing strong resilience in September.

Jobs increased by 64,000, of which 51,000 were full time.

Labour supply also showed strong growth.

A record participation rate of 67.2% and strong population growth drove growth in labour supply, only slightly below jobs growth. As a result, unemployment was steady at 4.1% (though it fell from 4.14% to 4.07% before rounding).

This continues an impressive run for jobs, despite an economy growing at only 1%.

Job growth this year has been averaging almost 40,000 a month – above longer-term averages nearer 25,000.

As population growth moderates, the RBA will be hoping job growth moderates with it to stop labour markets getting tighter rather than looser.

Next week, we get the quarterly break down of jobs by sector.

If the trend of the past few years is to continue, the majority of growth will be in the Construction sector and the Health and Social Assistance sector. This is all driven by state and Federal Government spending, which is independent of interest rates.

Until the governments get their infrastructure and NDIS spending under control, something that will not happen near term, unemployment will stay reasonably low.

Attention will then turn to where full employment is.

As we covered off in our Australian Quarterly, the RBA believes it is nearer 4.5% unemployment. We think this too high. The US Federal Reserve revealed recently that it believes it is nearer 4% for the US economy.

Globally, we see the trend for lower inflation but strong employment being repeated across most developed markets.

The theme underlying this is relief on inflation as supply chains fully normalise, as well as strength in employment driven by big-spending governments.

Bond markets have moderated rate cut expectations this month.

What’s next?

After today’s employment numbers, a February rate cut of 0.25% has gone from 100% chance to only 75%. Anything lower than 50% gets our attention as a good risk-reward trade given our view of a likely cut.

Markets will range trade for now, but the next important data in Australia is Q3 CPI, which is due on 30 October.

This should be market-friendly (our forecast is headline 0.1% and underlying 0.7%) and see the RBA revise down its future inflation expectations in its early November Monetary Policy Statement.

This will leave the door wide open for a rate cut in February.

About Tim Hext and Pendal’s Income & Fixed Interest boutique

Tim Hext is a Pendal portfolio manager and head of government bond strategies in our Income and Fixed Interest team.

Tim has extensive experience in banking, financial markets and funding including senior positions with NSW Treasury Corporation (TCorp), Westpac Treasury, Commonwealth Bank of Australia, Deutsche Bank, Bain & Co and Swiss Bank Corporation.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia.

Find out more about Pendal’s fixed interest strategies here

About Pendal

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

In 2023, Pendal became part of Perpetual Limited (ASX:PPT), bringing together two of Australia’s most respected active asset management brands to create a global leader in multi-boutique asset management with autonomous, world-class investment capabilities and a growing leadership position in ESG.

Investors looking to fund nature repair often lack high-quality opportunities. But a proposal to restore national parks in Victoria could be just the thing, say MURRAY ACKMAN and DAVID LINDENMAYER

- $224m green bond to fund forest regeneration and regional investment

- ANU monitoring and oversight

- Why bonds, why now? Pendal’s income and fixed interest experts explain

- Browse Pendal’s fixed interest funds

A PROPOSED green bond offers the opportunity to unlock hundreds of millions in private capital to support the expansion of national parks in Victoria’s central highlands, including a “Great Forest National Park“.

The park is under consideration by the Victorian government as a possible use for public land in Gippsland and North-East Victoria previously allocated to timber harvesting.

No decision has yet been made. But advocates say the national park would attract an extra 379,000 visitors annually, add more than $42.5 million to the local economy every year.

It could also support 750 direct and indirect jobs in environmentally sensitive industries such as invasive species management and ecotourism.

Carbon stock gains from improved protection and avoiding logging is estimated at 55.4 million tonnes. The proposed regeneration of 18,000 hectares of regenerated mountain ash forest would sequester 202,500 tonnes of CO2 by 2035.

Some 214 billion litres of water would be added to the catchment each year, enhancing water yields and supply for more than five million people in Melbourne.

Jacinta Allan’s state government has this year overseen the end of logging in Victoria’s state forests and the closure of state-owned forestry business VicForests.

But decades of logging have left behind some 15,000 hectares of unregenerated forest that now requires extensive restoration, says world-leading forestry expert Professor David Lindenmayer.

Lindenmayer proposes an Australian-first $224 million green bond that would fund the forest’s restoration using private capital.

Find out about

Regnan Credit Impact Trust

Murray Ackman,

Sustainable Finance and

Impact Investing Director

“The giant mountain ash forest outside of Melbourne produces almost all the water for the city,” says Lindenmayer, who has spent more than 40 years studying Australia’s forests.

“It is the most carbon-dense forest in the world.

“In any other city on the planet, there would be an amazing national park right next door to the city. But as a consequence of 60-70 years of intensive logging operations, the forest in many places is degraded.

“It’s still beautiful – but it’s now an endangered ecosystem. There’s a lot of work to be done to put the forest back together again and a lot of thinking to be done about true nature repair.

“How do you bring investment into a place like this?

“How do you rejuvenate the forest, create ecotourism opportunities, assist First Nations people to work on country, and bring Victorians to a place that many don’t even know exists?”

How a green bond could help

The term ‘green bond’ is used to describe a bond issued to raise finance for projects that have a positive impact on the environment, says Murray Ackman, a senior ESG and impact analyst at responsible investing leader Regnan and asset manager Pendal.

The Victorian government has an established track record of issuing green bonds, with the first issued in July 2016, while the federal Albanese government issued its first green bond in June this year.

“From an investor perspective, everyone’s talking about nature repair and biodiversity but there are generally no investable opportunities,” says Ackman.

“So, for us, the exciting thing about this Victorian green bond is that world experts and leaders in academia have come together to propose a viable, exciting, and reliable way to invest in nature repair.”

As longstanding investors in these types of bonds, Pendal’s Income and Fixed Interest team hopes to increase supply in high-quality bonds which have the potential to bring about significant impact.

Investing in nature

Green bonds issued by state governments could attract significant investment for restoration of biodiversity at scale, says Ackman.

Some three billion hectares of agricultural land is degraded globally, impacting close to half the world’s population – with more than US$14 trillion of investment required for restoration.

“For investors, having external monitoring for nature repair is exciting. Nature repair is slow and there is expenditure you need to do each year for the life of the bond.”

Strong demand for green bonds could create an opportunity for investors, says Ackman

“These types of bonds tend to price close to the ordinary curve, though there is often increased demand, so slightly beneficial pricing for the issuer.

“We have also noticed quality green, social and sustainability bonds have heightened demand in the secondary market and tend to outperform.“

Expert monitoring

Ackman says a key feature of the proposed Victorian green bond is the external, expert monitoring provided by Lindenmayer’s team at ANU.

“It is not unusual for a government to issue a use-of-proceeds bond – but the appeal of this one for investors is the government signing up for measured nature repair and reporting every 12 months,” he says.

Lindenmayer says the Victorian opportunity is unique because it is founded on four decades of research collected by his team that provides a robust baseline for monitoring forest regeneration.

Pendal Sustainable Australian Fixed Interest Fund

An Aussie bond fund that aims to outperform its benchmark while targeting environmental and social outcomes via a portion of its holdings.

“Our background data goes back 42 years in these forests – we’ve monitored the forest, the plants, the animals, the carbon, all those kinds of things. So, there’s an unparalleled baseline against which to compare.

“Investors can have confidence that this is properly monitored and reported – whether it is 2000 new nest boxes or replanting 500 hectares of forest every year it will be carefully monitored so that the people investing in the bond will see what’s been done.

“There will be independent data collected to show what’s happening and what the biodiversity dividend from the investments will be. How many more golden whistlers? How many more greater gliders? How many more tonnes of carbon?

“All those things will be reported so it cannot be greenwashed.”

New jobs, tourism benefits

Victoria is the most land-cleared and degraded state in Australia, making it a fitting place to launch a green bond project like this, says Lindenmayer.

“This is a bond that will give life to the regions. It is estimated the GFNP will attract an extra 379,000 visitors annually, add more than $42.5 million to the local economy every year and support at least 750 direct and indirect jobs.

“The Great Forest National Park is a fantastic place – an extraordinary environment so close to Melbourne with so many things going for it.

“The best people in finance and investment are seeing an extraordinary opportunity.

“It just needs the state government to step up.”

About Murray Ackman and Pendal’s Income and Fixed Interest boutique

Sustainable finance and impact investing director Murray Ackman joined Pendal in 2020 to provide fundamental credit analysis and integrate Environmental, Social and Governance factors across credit funds.

Murray has worked as a consultant measuring ESG for family offices and private equity firms and was a Research Fellow at the Institute for Economics and Peace where he led research on the United Nations Sustainable Development Goals.

Research and engagement analyst Paula Angel Valdes joined Pendal in November 2025. Prior to joining the company, Paula served as a senior analyst at Morningstar Sustainalytics in Amsterdam, where she specialised in ESG risk and impact assessments, controversy analysis, and contributed to the enhancement and implementation of methodological refinements for the firm’s Controversies product.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia. In 2020 the team won the Australian Fixed Interest category in the Zenith awards.

Regnan Credit Impact Trust is a defensive investment strategy that puts capital to work for positive change

Pendal Sustainable Australian Fixed Interest Fund is an Aussie bond fund that aims to outperform its benchmark while targeting environmental and social outcomes via a portion of its holdings.

Here are the main factors driving the ASX this week, according to Pendal’s head of equities CRISPIN MURRAY. Reported by portfolio specialist Chris Adams

- Find out about Pendal Focus Australian Share fund

- Tune in: register to watch Crispin’s Beyond the Numbers webinar

EQUITY markets remain in good shape with the US Federal Reserve’s put option, combined with China’s stimulus, reducing downside economic risk and supporting market liquidity.

Last week’s US inflation data was a bit stronger than expected, leading to a rise in bond yields and a stronger US dollar.

However, equities continued to rise as the narrative of a soft landing remained on track.

The current debate on rates is more about how far below 4 per cent they will go, rather than whether we will see a series of cuts in the next few meetings.

The S&P/ASX 300 rose 0.83% last week and the S&P 500 was up 1.13% in the US.

Equity market gains have come despite the CBOE Volatility Index (the “VIX”) rising above 20, after hovering between 10 and 15 for most of the past year.

This reflects the upcoming US election, which the market sees as unpredictable, though not necessarily a negative.

China’s updates on stimulus have lacked detail and indicate the initial market reaction was overstated. This led to a retracement in commodities and Chinese equities.

US earnings have just started with good results from Wells Fargo and JP Morgan.

The Australian market was quiet last week.

We saw Arcadian Lithium (LTM) agree to a takeover offer from Rio Tinto (RIO), but the bid is quite unique in nature and unlikely to herald a wave of M&A in the sector.

US soft landing watch

US September CPI data was slightly stronger than expected.

The headline figure rose +0.18% month-on-month and 2.4% year-on-year which is a three-year low.

However, core CPI rose 0.31% monthly, taking the yearly gain to 3.3% (up from 3.2% in the previous month).

- Core goods rose +0.17% – the most since May 2023, though it’s still down 1.2% on a three-month annualised basis.

- Core services (excluding rent and owner’s equivalent rent, ie “super-core”) were up 0.4% monthly – the highest since April. Medical care, apparel, auto insurance and airfares drove the increase.

The market’s reaction was muted; the numbers have been surprising on the downside for some time, so there was room for slightly higher numbers.

In addition, the Fed is saying it’s comfortable with the trend and not focused on these “super core” measures.

The upshot was bond yields continuing to move higher. It also reinforced the view that the next two moves by the Fed should be 25bp cuts.

Jobless claims have become the most-tracked weekly indicator as the market watches for signs of economic deterioration.

Concerns here had subsided. The data spiked higher last week, though this was tied to hurricanes Helene and Milton as well as US port strikes, so shouldn’t be interpreted as a concerning signal.

It does highlight that we are set for a couple of months of messy data because of the two hurricanes.

In aggregate the US economy looks to be holding up well. The Atlanta GDPNow indicator is running at 3.2% for Q3, well above consensus of 2% growth.

Pendal Focus Australian Share Fund

Now rated at the highest level by Lonsec, Morningstar and Zenith

China stimulus watch

A meeting of China’s policy-implementation body, the National Development and Reform Commission, disappointed a market craving a big, headline stimulus announcement.

The only number mentioned was RMB200 billion, versus hopes of RMB3 trillion-plus.

It was more water pistol than bazooka.

This should have been expected given the commission’s role is to implement certain policies rather than determine them.

This was interpreted as a signal that the Chinese government saw reaction to the stimulus as overly dramatic and was looking to cool expectations and speculative activity.

An extreme example was Hong Kong-listed, Chinese residential property developer Vanke, which rose 360% from HKD3.90 to about HKD14 in two weeks, before retracing to HKD7.31.

On Saturday, the more-important Ministry of Finance outlined its plans, flagging:

-

No near-term plans for additional central government bond issuance (though the National People’s Congress could choose to do this later in the month).

-

RMB400 billion additional local government bond issuance which utilises the gap between debt ceiling and debt outstanding.

-

A big one-off increase in debt quota to enable the swap of local government debt. No specific number was given, but last year they did RMB2.2 trillion. It could be above RMB3 trillion, supporting financial stability and helping overall economic activity by enabling local governments to pay wages and maintain services.

-

RMB 2.3 trillion available for use by the end of 2024, from bonds already issued but unused under the existing target. The target is unchanged – the key question is whether it can all be used.

-

Local governments will be able to use proceeds of their special bond issuance to buy unsold apartments and convert them to affordable housing to help address excess housing inventory.

-

Injection of tier-one capital into state-owned banks. There was no specific number, but around RMB 1 trillion is expected.

-

Indications the 2025 fiscal deficit could be more than 3% GDP, supporting more spending next year.

The market’s reaction will be interesting. Key points to note include:

-

There is no “bazooka-stimulus” headline number, especially compared with the reaction to the GFC which was cumulatively the equivalent of about RMB 20 trillion today in terms of proportion of the GDP. So there is no short-term upside surprise. Bulls could choose to point to the use of existing funds and remaining bond issuance to conclude around RMB 3 trillion of stimulus. But this looks like a degree of re-badging – not new funds – so we remain hostage to how this money will actually be spent.

-

The policy is designed to reduce tail risks and prevent the doom loop of local governments continuing to cut back on spending.

-

No direct boost to consumer spending. This is negative.

These measures may help prop up the equity market. But it’s unclear if this is sufficient to support commodity markets, which need to see real demand stimulated in the short term.

China’s Politburo and National People’s Congress both meet in late October. The latter would need to approve any policy requiring higher deficit spending.

One final observation: Beijing may be holding something in reserve against the risk of a Trump victory in the US election and the risk of material tariff increases.

US election watch

With barely three weeks to go, Trump gained some momentum in the betting odds last week, moving to a 54% chance of a win (according to RCP Betting Average) versus 46% for Harris.

This is his biggest lead since Harris entered the race.

The seven key battleground states (assuming Minnesota goes Democrat) are Arizona, Nevada, Wisconsin, Michigan, Pennsylvania, North Carolina and Georgia.

Most recent polls have Trump in front in all but Wisconsin, though with a very fine margin.

Market volatility has picked up, but the forward curve has this falling back post-election. To date, this has not impacted equities and is supported by credit spreads staying low.

The most likely election outcome is a Democrat or Republican presidential win without sweeping both the House and Congress – and hence being constrained in what they can achieve.

The main difference in market impact relates to bonds, with Trump’s threat of higher tariffs and less immigration potentially leading to higher inflation in late 2025, and therefore to higher yields.

This may have limited impact on equities as it could be seen to come with higher growth.

Oil watch

The latest expectation is that the US will seek to limit Iran’s ability to export oil with sanctions (and a crack-down on attempts to break them).

Saudi Arabia may step up to increase production to fill the supply gap, allowing them to re-take share and ensure oil prices don’t run up into the year’s end.

These measures may encourage Israel to avoid escalation, but the response still waits to be seen.

Markets

Despite geopolitical uncertainty, the outlook for equities is positive. Inflation is under control, economic growth is solid, financial conditions are easing and corporate earnings are growing.

Initial US results out last Friday were well received in the financial sector with JP Morgan (+4.4%), BlackRock (+3.6%) and Wells Fargo (+5.6%) all beating consensus.

The US market is seeing leadership from industrials, consumer discretionary and financial stocks and less reliance on the Magnificent 7 tech stocks, which is a positive signal.

It is also worth noting the US software index broke to new highs having been range-bound for the whole year.

Australia reflected these themes last week with banks beginning to bounce after a recent fall. The slower trajectory of rate cuts helps them.

Tech also had a good week, as did industrials.

From a portfolio perspective we tend to be overweight technology and industrials and we have added to discretionary exposure.

About Crispin Murray and the Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia. Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions.

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

Here are the main factors driving the ASX this week, according to analyst and portfolio manager ELISE McKAY. Reported by investment specialist JONATHAN CHOONG

- Labour market data “noisier than usual”

- Geopolitical risks surge on Middle East tensions

- One demand: tune into Crispin Murray’s Beyond the Numbers webinar

- Find out about Pendal Focus Australian Share fund

DESPITE the relatively flat index performance belying underlying trends, it was a volatile period last week.

In Australia, the ASX 300 experienced a modest decline of 0.75%, which masked significant sectoral movements. The energy sector surged by 6.75%, driven by geopolitical tensions and rising oil prices, while consumer discretionary fell by 2.5%.

Globally, the resolution of the East Coast Ports strike was swift, yet geopolitical risks remain heightened – particularly with the Israel-Iran conflict.

Energy markets swiftly adjusted to geopolitical risks, though sustained higher oil prices are uncertain due to excess supply and global players’ preference for stable pricing.

Anticipation is also building around China’s imminent announcement of additional fiscal stimulus.

Macro data was relatively quiet, with the standout being a stronger-than-expected jobs report on Friday. This bolstered US markets, which rallied on optimism that the Federal Reserve will achieve a soft landing.

Jobs data supports a likely 25 basis point (bp) cut rather than a 50bp cut in November, with the possibility of a larger cut in December if necessary.

Bond markets quickly priced in these expectations.

Economic data

Jobs

Friday’s robust jobs report challenges the prevailing narrative of a gradually softening labour market and contradicts other indicators, such as hiring and quits rates, which point to upcoming weakness.

Markets traded up strongly on bets that the Fed will achieve a soft landing.

September payrolls surged by 254k, significantly exceeding the consensus estimate of 150k growth, with an additional upward revision to previous months.

Consequently, the three-month average for private sector job creation has risen to a mild 145k, which further indicates a soft landing.

After peaking at 4.25% in July, the unemployment rate has fallen to 4.05% over the past two months – defying expectations for it to remain flat.

Labour market data is noisier than usual, with October expected to be another mixed month due to the impact of strikes and Hurricane Helene.

Business response rates for the first estimate haven fallen to 62%, down from September 2023 and below the 77% average of the 2010s. Typically, compliance reaches 90-95% by the third estimate.

Given the breadth of other indicators pointing to a softening labour market, it is worth questioning whether the strength seen in the September 2024 jobs report is an outlier, rather than a true read of a goldilocks-type scenario.

Other data:

- JOLTs data for August 2024 shows the hiring rate slowing to 3.3% and the quits rate falling to just 1.9%.

- The employment subcomponent of Services ISM is in contraction territory.

- The NFIB small business survey has net 15% of firms with plans to hire, which is indicative of a softer labour market.

- A modest increase in initial jobless claims, albeit still at generally low levels.

Wages

Average hourly earnings accelerated to an annualised 4% year-on-year (YoY) in September 2024, up from a low of 3.4% in July 2024.

Again, this data can be lumpy so it remains to be seen whether this is an uptrend that can be sustained. The JOLTS quits rate suggests the trend should move lower.

ISM survey data

The Services ISM data surprisingly jumped to 54.9 in September 2024, driven by strength in new orders and business activity. At the same time, however, the employment index was weaker and fell into contractionary territory.

This has now joined the employment data for Manufacturing, which is in recessionary territory at 43.9. Note that the Manufacturing ISM data remained flat at 47.2 in September this year.

Find out about

Pendal Focus

Australian Share Fund

Crispin Murray,

Head of Equities

Oil

Geopolitical risks have surged following an escalation in the Middle East, pushing Brent crude oil prices up by 8% last week to $78 per barrel (/bbl). Discussions between the Biden administration and Israel regarding potential strikes on Iranian oil facilities have heightened these concerns.

Putting Iran’s oil market into perspective, the country produces approximately 3.5 million barrels per day (mb/d), with around 50% exported primarily to China despite US and EU sanctions.

The remaining production is consumed domestically, with Iran being self-sufficient in refined products such as gasoline, diesel, and jet fuel.

Iran also controls the strategic Strait of Hormuz, a vital shipping route where about 17% of global oil production and 19% of global LNG supply pass through.

China is another key player and the world’s largest crude oil importer. Not only is it Iran’s main client, but 40-50% of its imports originate in the Persian Gulf and must pass through the Strait of Hormuz to get to China.

The market is focused on three hypothetical scenarios:

- Damage to Iranian oil infrastructure could affect downstream assets (such as refineries), midstream assets (like pipelines and terminals) and upstream assets (including production fields). An attack on refinery assets would be less impactful than on midstream or upstream assets.

- Tightening enforcement of sanctions.

- Broader disruption of regional oil supplies via (a) regional trade routes, (b) attacks on oil infrastructure outside Iran, or (c) interruption of trade through the strait of Hormuz.

On the first scenario, it seems politically unlikely that President Biden would support a strike on Iranian oil facilities given the potential for higher oil prices and the impact on the upcoming election.

However, even if such a strike were to occur – with or without US support – the medium-term impact on oil prices might be muted due to excess capacity in the market.

The third scenario, particularly the closure of the Strait of Hormuz, would be the most disruptive, though it is considered unlikely due to its importance to Iranian exports and global trade.

Globally, this excess capacity is estimated at approximately 6 mb/d against a global market size of around 100 mb/d. For instance, Saudi Arabia is currently producing 9 mb/d versus a capacity of 12 mb/d, while other OPEC members such as the UAE also have excess capacity (estimated at around 1 mb/d).

Even if there was an attack targeting Iran’s oil production, OPEC has historically acted quickly to mitigate disruptions – typically offsetting 80% of lost production within two quarters.

Goldman Sachs (GS) has estimated the impact of two hypothetical scenarios relative to a baseline forecast for $77/bbl on average in Q424 and $76/bbl average in 2025.

Scenario 1: A 2 mb/d disruption for six months could see Brent crude temporarily peak at $90 per barrel if OPEC quickly offsets the shortfall and reach the mid-$90s in 2025 without OPEC intervention.

Scenario 2: A persistent 1 mb/d disruption, possibly due to tighter sanctions, could push Brent to the mid-$80s if OPEC gradually offsets the shortfall, and to the mid-$90s in 2025 without an OPEC offset.

Given the current oil price of $78/bbl, the impact on inflation and economic growth appears limited at this stage.

Oil prices would need to exceed $100/bbl to have a meaningful impact on inflation. Academic research finds that a 10% shock to oil prices translates to an increase of about 7bps to core inflation.

Find out about

Pendal Smaller

Companies Fund

Australia

Retail sales for August 2024 surpassed expectations, rising by 0.7% month-on-month (MoM) and 3.1% YoY – the fastest since May 2023 and ahead of expectations.

The strength was broad-based except for household goods spending, which has declined for the past two months.

This stronger trend should continue over the coming months as tax cuts come through and are eventually spent.

Eurozone inflation

In Europe, inflation has dipped below the target for the first time in three years, reaching 1.8% compared to the 2% target.

Inflation is cooling all around the world, maintaining the momentum of the worldwide rate-cutting cycle.

The European Central Bank (ECB) is expected to cut later this month.

The US Federal Reserve’s decisive 50bp cut last month provided global thought leadership and created room for other countries to ease more without further depreciating their currencies.

China

China took a break for Golden Week, which is a week-long break in celebration of the National Day. This holiday was first introduced in 2000 as a way of stimulating China’s economy by encouraging domestic tourism, travel to visit family, and general consumption.

As the nation returns from this break, the government is expected to announce further fiscal stimulus at a press conference to further boost the consumer and support economic growth.

Morgan Stanley anticipates a RMB2 trillion package, with potential announcements as early as today. The support could span local government financing, infrastructure capex, bank capitalisation, and consumption/social benefits.

As highlighted by Jack Gabb in last week’s equities note, while more substantial support (up to RMB10 trillion) is needed, this move is a step in the right direction.

Australian markets

Despite the market declining by 0.75% for the week, sector dispersion was notable.

The energy sector surged by 6.75% due to geopolitical risks driving oil prices higher, while consumer discretionary fell by 2.5%.

Santos (STO) and Woodside (WDS) were the top performers, moving in lockstep with the 8% rise in oil prices.

Reflecting on September, the ASX 200 achieved a 3% total return, highlighted by the rotation of resources into banks reversing.

Small-cap stocks also recovered some of their year-to-date underperformance relative to large and mid-cap stocks.

About Elise McKay and Pendal Australian share funds

Elise is an investment analyst and portfolio manager with Pendal’s Australian equities team. Elise previously worked as an investment analyst for US fund manager Cartica where she covered a variety of emerging market companies.

She has also worked in investment banking and corporate finance at JP Morgan and Ernst & Young.

Pendal Horizon Sustainable Australian Share Fund is a concentrated portfolio aligned with the transition to a more sustainable, future economy.

Pendal Focus Australian Share Fund is a high-conviction equity fund with a 16-year track record of strong performance in a range of market conditions. The Fund is rated at the highest level by Lonsec, Morningstar and Zenith.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Here’s what you need to know about the latest stimulus announcements in China, according to Pendal’s head of income strategies Amy Xie Patrick

- China allocating RMB2trn to “big bazooka” stimulus

- Issues can be fixed, but China needs to spend more

- Why bonds, why now? Pendal’s income and fixed interest experts explain

- Browse Pendal’s fixed interest funds

THE final week of September was an eventful one in Beijing.

China’s central bank, the People’s Bank of China (PBoC), kicked off proceedings by lowering a key policy rate by 0.20% and reducing the required reserve ratios (RRR) for large banks by 0.50%.

This was swiftly followed by announcements of a slew of other stimulus plans and measures aimed at lifting China’s ailing economy.

Since then, there has been much talk of China’s “big bazooka” stimulus.

Some think that policymakers have made a commitment to do “whatever it takes” to rescue growth. With China on holiday this week for National Day (国庆节) and Golden Week (黄金周), this article explores whether this stimulus will be a silver bullet or simply a handful of mood-boosters.

This time is different

There are several key differences between this slew of measures and what we’ve witnessed over the past two years of “policy incrementalism” from Beijing.

The measures are broad and more coordinated, addressing everything from financial system stability to the longer-term demographic crisis.

They have also been communicated with a greater tone of urgency and determination, strategically timed to boost sentiment during the current week-long national holiday.

Most importantly, there is finally a willingness to directly address the struggles faced by Chinese households as a result of the property crisis.

The bursting of the Chinese property bubble is akin to the Global Financial Crisis (GFC) for the world’s second-largest economy.

In fact, had the rest of the world followed the same fiscal austerity as China in the wake of Covid, this crisis would have developed its own acronym by now. We would be blaming that acronym for a global recession.

When such a crucial driver of growth and wealth creation suddenly shuts off, it leaves holes in balance sheets and chasms in sentiment.

The private sector will focus on balance sheet repair as its priority, which means no amount of making borrowing cheaper and more available can stimulate activity during this phase. As a result, the government must spend and invest to plug the hole.

China’s issues can be fixed…

At the heart of China’s economic struggles are three key ailments.

Firstly, as already discussed, the economy needs to recover from the property crisis. This process takes time, and the first job of authorities during this time is to make sure the crisis doesn’t take down the entire system.

The interest rate and RRR cuts announced in late September help to ensure that the banking system has plenty of liquidity.

The capital injection programs are to ensure that troubled but important banks do not infect the rest of the system with their problems. Very similar actions were taken in the US after the collapse of Lehman Brothers in 2008.

The next job is to stabilise prices in the housing market. The supply-demand imbalance of China’s real estate market is due to both oversupply (from over-building) and insufficient demand (partly due to lack of affordability).

Second is a lack of a social safety net, which results in households saving far too much. This has only been exacerbated by the negative wealth effect of the housing bubble bursting.

Fiscal measures that make childcare, health and retirement more accessible and affordable will naturally bring down saving and encourage more spending, thus naturally transitioning the economic engine from investment to consumption.

Lastly, an unprecedented demographic crisis looms large, thanks to the one-child policies introduced in the late-1970s. While this policy was officially abolished in 2016, birth rates have failed to rise meaningfully in China due to the social infrastructure having been rewired for over a generation to cater to one-child families.

Add to this that many Gen Z-only children with hard-earned degrees can only find Meituan bike delivery jobs, it’s quickly obvious that birth rates won’t turn around by themselves.

All three problems are intertwined and can be solved with appropriate incentives and policies.

A stronger system of social safety nets, including cheap and affordable childcare, coupled with free homes for families willing to have more children would go a long way to tackling these fundamental issues.

…but they’ll need to spend a lot more

The newest set of stimulus measures circle up to RMB2trn for fiscal measures directly targeted at households and consumers. Measures include monthly cash subsidies to families who are willing to have more than one child.

While it’s a step in the right direction, the quantum of funds earmarked for these measures is not going to be nearly enough.

In addition, there are likely to be significant hurdles to implementation, all while the market awaits eagerly for signs that this “bazooka” stimulus is making a meaningful difference to China’s economic trajectory.

Incentivising parents (who are only children themselves) to have more than one child is going to be costly business – so is establishing a larger and more equitable social safety net for the masses.

While RMB2trn is not small, it is at least five times too small to be of long-lasting consequence.

Rather than a silver bullet, the latest slew of Chinese stimulus plans are about providing a floor under market prices and sentiment. Mood-boosters are nice, but the economy needs more than just sugar hits if Beijing wants a better and more sustainable growth trajectory.

Implications for portfolio positioning

Since there are significant departures in the latest wave of stimulus announcements, Chinese assets have responded dramatically – with the CSI300 equity index up nearly 30% over the past week.

Bear in mind that with the almost halving of the value of this market since its peak in 2021, the recovery may still have legs in the near term.

There is also speculation that the significance of China’s stimulus could lead to global reflation. I don’t yet buy into this argument.

As mentioned earlier, these measures are a step in the right direction, but lacking in details and firepower. The medium-term risk to markets is a slow path to implementation, resulting in little to no change in Chinese data over the next few months.

It is also notable that despite the rally of onshore Chinese assets, broader asset classes have yet to buy into the idea of reflation. Oil, for example, had continued its slide until geopolitical developments in the Middle East caused a temporary price surge.

In short, this round of Chinese stimulus is good news for investors who are directly involved in Chinese assets. But our portfolios are reluctant to get sucked in to “China-adjacent” positions.

Our income strategies welcome the buoyed sentiment to risky assets but are not relying on a quick translation from rhetoric to Chinese data to justify our exposures to equities and emerging markets.

The uneven spread of market reactions to this latest news from China also serves as a healthy reminder that dislocations and uncertainties naturally grow when the global economic cycle slows.

About Amy Xie Patrick and Pendal’s Income and Fixed Interest team

Amy is Pendal’s Head of Income Strategies. She has extensive expertise and experience in emerging markets, global high yield and investment grade credit and holds an honours degree in economics from Cambridge University.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia. The team oversees some $20 billion invested across income, composite, pure alpha, global and Australian government strategies.

Find out more about Pendal’s fixed interest strategies here

About Pendal Group

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

In their latest quarterly report, the Income & Fixed Interest team discusses some of the biggest trends affecting Australian fixed income investors right now

- Download Pendal’s September quarter income and fixed interest report (PDF)

- Why bonds, why now? Pendal’s income and fixed interest experts explain

- Browse Pendal’s fixed interest funds

Pendal’s income and fixed interest team recently published its quarterly deep-dive into the themes driving Australian markets (PDF).

In this edition, head of government bond strategies Tim Hext dives into Australia’s employment market, focusing on where it’s headed and why it’s an important economic signpost for central bank monetary policy.

Senior credit analyst Terry Yuan discusses APRA’s change of tune on bank hybrids and what the changes could mean for investors.

Pendal’s head of cash strategies Steve Campbell explains why Australia is unlikely to join the rate cut club anytime soon, while head of income strategies Amy Xie Patrick examines whether income can be both rewarding and defensive.

Finally, credit and ESG analyst Murray Ackman offers an overview of Australia’s challenged nature repair market and the Federal Government’s plan to encourage investment in that space.

Find out about

Pendal’s Income and Fixed Interest funds

About Pendal

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia.

Here are the main factors driving the ASX this week, according to Pendal investment analyst JACK GABB. Reported by portfolio specialist Chris Adams

- Find out about Pendal Focus Australian Share fund

- NEW: Watch Crispin Murray’s bi-annual Beyond The Numbers ASX outlook

LAST week was all about China, after a raft of coordinated policy measures signalled a major pivot in the outlook for the economy.

The move triggered a rally in risk assets globally and, in Australia, the major unwinding of bank outperformance versus resources.

Add to that a swathe of positive economic data in the US and a further drop in oil, and it couldn’t have been much better on the macroeconomic front.

Chinese stocks had their best week since the GFC, with the CSI 300 up 15.7% and the Hang Seng up 13.0%. If past stimulus reactions are any indicator, this market has a lot further to go.

The S&P 500 rose 0.64%, led by materials and consumer discretionary, while Japan also posted further gains (Nikkei up 6.2%).

The S&P/ASX 300 rose 0.16%, with materials up 9.34% and financials down 4.38%.

Treasuries were subdued, though there was a milestone moment, with yields on China’s 30-year bonds poised to fall below Japan for the first time in two decades.

China pivot

Two months after disappointing at the Plenum, Chinese policymakers made a material pivot towards providing more support.

The range of measures, both monetary and fiscal, represent the most significant stimulus package announced since Covid. Key measures include:

- a 0.5% cut to the Reserve Requirement Ratio (RRR) and guiding to a further potential 0.25-0.5% cut by end 2024

- a 10% cut in down payment requirements for second mortgages to 15%

- a 0.5% cut in existing mortgage rates

- a potential US$142bn capital injection into banks

- more than US$100bn of funding from the People’s Bank of China (PBOC) to brokers, funds and insurers to purchase equities

- a potential 2 trillion RMB ($285bn) fiscal injection (1.6% of GDP).

While credit has not been the problem, the messaging from an unscheduled Politburo meeting was clear. Specifically, it called for the government to:

- strengthen employment for college graduates

- provide sufficient fiscal spending support and to stabilise the real estate market

- consider the forceful implementation of the recently announced rate cuts

- vow to complete the country’s annual economic goals (GDP target = 5%)

- improve policy to support the birth rate.

Trick or treat?

With another Politburo meeting scheduled for the end of October, expectations remain high that we will see incremental stimulus support – particularly given it appears China’s policymakers will do whatever is required to meet economic goals.

However, there is no doubt that the scale of the challenge remains huge given the collapse in property prices and associated plunge in consumer confidence.

Rate cuts have not, thus far, been sufficient to stem challenges here.

Therefore, the focus has been on the fiscal element of any stimulus.

Assuming the RMB 2 trillion flows through, that is half the RMB 4 trillion announced post-GFC (equivalent to 10% of GDP), which saw the CSI rebound more than 100%.

A GDP-equivalent level of stimulus today would be more than RMB 10 trillion. It’s also worth noting a RMB 1 trillion package announced last October failed to trigger a sustained rebound.

While we now head into a quieter period for the Golden Week holiday, history suggests that market support will continue through to year’s end, with the impact of past major stimuli (2008, 2015, 2020) lasting roughly six months. We also note that the market is very underweight China.

A key unknown is the outcome of the US election.

Trump has flagged tariffs of up to 60% on Chinese goods. If delivered, that could drive 2025 growth 2% lower (from around 4% to 2%). Offsetting that would require material additional stimulus and/or RMB devaluation.

Pivot repercussions for Australian equities

The China pivot has broad implications across risk assets, however, one of the most immediate beneficiaries is the resources sector which recouped some of its year-to-date underperformance on the back of rebounding commodity prices.

Banks were the main funding source, with ASX 300 Materials up 9% for the week and Financials down 4%.

Banks had reached extremely overbought levels, trading four standard deviations above their 20-year average PE.

There had been some fundamental support, with an improved competitive backdrop, conservative provisions and potential buybacks, but the banks would have required 30-40% upgrades to justify share prices at the peak.

There is scope for a further unwind, but it is contingent on China in the short term and rate cuts or bad debts in the medium term.

While the major miners had been trading at relatively cheap levels prior to the stimulus, this seemed justified by weak commodity prices against a backdrop of rising capex.

The China stimulus has provided immediate relief on the price side (for iron ore, if not lithium) but long-term concerns on supply–demand imbalances have not changed.

Commodity prices

Iron ore (up 12.3%) and base metals (copper up 8.7%, aluminium up 5.5%) led gains. Oil posted further declines (Brent crude down 4.1%).

We note that iron ore seasonality should also provide a further tailwind as we approach the end of 2024. Over the past five years it has averaged a 4% gain in November, 14% in December and 8% in January.

Commodity trading advisor (CTA) strategies – a systematic approach to investment – continue to be “max long” in both gold and silver and now have been signalled to move to “max long” copper on the metals rally. CTAs are “max short” oil.

Oil fell on news that Saudi Arabia may abandon its US$100/bbl target as it plans to increase output to regain market share.

News of an agreement in Libya between eastern and western administrations also drove higher supply expectations, with estimates it could result in an increase of up to 500,000 barrels per day (bpd) which is roughly 0.5% of global supply.

The move came despite increasing conflict in the Middle East, but further escalation over the weekend could yet trigger a rebound.

Pendal Focus Australian Share Fund

Now rated at the highest level by Lonsec, Morningstar and Zenith

US macro and policy

It was a quieter week in the US following the Fed’s rate cut, with interest rate expectations largely unchanged.

Data continues to show the US economy is in good shape, with 2Q annualised GDP coming in at 3.0% versus the 2.9% expected, and initial jobless claims at 218k versus the 223k expected.

The annual update of National Economic Accounts also showed upwards revisions to a whole range of data, including GDP and gross domestic income (GDI).

Savings were also marked up hugely – the 2Q savings rate increased to 5.2% from 3.3% (excess savings increased from US$400bn to US$570bn).

This goes some way to assuaging consumer spending fears, particularly given disposable income (up 3.1%) is tracking ahead of spending (up 2.7%).

Lastly, core Personal Consumption Expenditures (PCE) beat expectations, coming in a 0.1% month-on-month versus expectations of 0.2%, which may bolster the argument for another 0.50% cut in November.

Weaker datapoints were hard to find, though there was a note of caution in the University of Michigan survey of inflation expectations of 5-10 years, which rose to 3.1% – the highest since November 2023.

The Richmond Fed Manufacturing data also printed its lowest level since early 2020. The data tracks manufacturer sentiment across Virginia, Maryland, North and South Carolina, most of West Virginia and the District of Columbia.

Of its three component indexes, shipment decreased from -15 to -18, new orders increased from -26 to -23, and employment fell from -15 to -22.

The US Presidential Election will take place on 5November, with the next Fed meeting on 8 November.

Rhetoric during the week was primarily directed towards laying out plans to boost US manufacturing.

Trump’s approach is primarily via lower taxes, lower energy costs and less regulation (like mass exodus of manufacturing from China and so on), while Harris is focused on federal incentives (like investing in biomanufacturing, aerospace and artificial intelligence).

Polls were largely unchanged.

Australia macro and policy

September might have been the biggest month of global monetary easing since April 2020, but for the RBA it was business as usual – with the central bank holding rates steady at 4.35%.

The statement made clear that while inflation has fallen, it remains some way above the midpoint of the 2-3% target.

The trimmed mean CPI measure was 3.4% in August (from 3.8% prior), but the RBA has described this as temporary given finite cost-of-living relief (mostly on energy) and has a 3.5% projection for year-end.

However, relief appears likely to be extended given the timing of the Federal Election – offsetting an estimated 47% increase in out-of-pocket household electricity expenses between October 2024 and September 2025.

With headline inflation falling (2.7% in August), growth slowing (the RBA noting a slightly softer outlook versus August), oil down, the AUD up, and most central banks cutting, pressure on the RBA to cut is likely to increase.

Where to from here?

In the US, growth is still slowing and likely bottoming in Q4.

The unknown is whether the Fed can continue to cut rates without inflation rebounding.

Consensus has inflation continuing to fall. However, with rates moving lower, the dollar dropping and hard assets inflating, the risk is inflation rebounds quicker than expected.

Shelter, for example, is one-third of the CPI and growing at 5% per annum.

Australia is six months behind the US in terms of when inflation peaked. Its outlook is also more heavily influenced by China – thus, whether the latter’s pivot can be maintained will be key to offsetting Australia’s deteriorating growth outlook.

About Jack Gabb and Pendal Focus Australian Share Fund

Jack is an investment analyst with Pendal’s Australian equities team. He has more than 14 years of industry experience across European, Canadian and Australian markets.

Prior to joining Pendal, Jack worked at Bank of America Merrill Lynch where he co-led the firm’s research coverage of Australian mining companies.

Pendal’s Focus Australian Share Fund has an 18-year track record across varying market conditions. It features our highest conviction ideas and drives alpha from stock insight over style or thematic exposures.

The fund is led by Pendal’s head of equities, Crispin Murray. Crispin has more than 27 years of investment experience and leads one of the largest equities teams in Australia.

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

Find out more about Pendal Focus Australian Share Fund

Contact a Pendal key account manager

While August inflation data shows inflation has eased, more progress is required before we’ll see rate cuts in Australia, writes Pendal’s head of government bond strategies TIM HEXT

- RBA not celebrating just yet

- We still expect four rate cuts next year

- Why bonds, why now? Pendal’s income and fixed interest experts explain

- Browse Pendal’s fixed interest funds

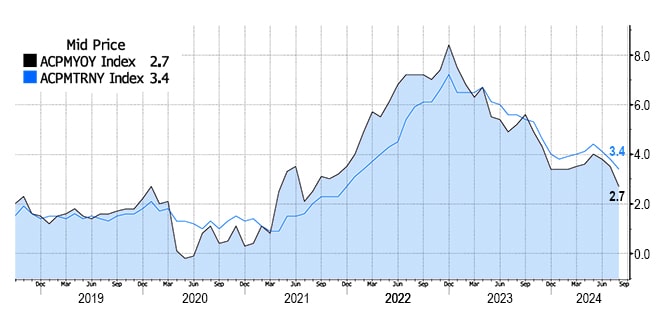

A SHARP fall in headline inflation was reported today, in the latest monthly CPI series for August.

Prices since August last year are only 2.7% higher and are back in the RBA’s target band of 2-3% for the first time since a 3% reading in October 2021.

Market forecasters did a great job in a volatile series, as 2.7% was spot on expectations.

Though encouraged, the RBA will not be celebrating yet.

Massive government subsidies, largely on electricity, are the main reason headline inflation is falling fast.

Electricity prices, accounting for the subsidies, fell 14.5% in August and are now 20% lower in Q3. They make up only 2.4% of the CPI weight, but 20% on 2.4% still impacts CPI by 0.5%.

Trimmed mean (underlying) inflation, which cuts out the highest and lowest-weighted 15% of price moves, is still at 3.4%.

This is the RBA’s main focus, and the central bank would need to be convinced that this will be sustainably at, or very near, 3% to begin cutting rates.

Our initial forecast for underlying inflation for Q3 is 0.7% (headline will be near flat). This annualises at 2.8%.

However, the RBA would likely need to see Q4 at a similar level, though if unemployment were to rise enough in October and/or November, it could tip the balance.

We don’t get Q4 CPI numbers till late January, which makes the current market forecast of an 80% chance of one rate cut by year-end optimistic.

Source: Bloomberg

Another inflation-friendly factor during August was falling fuel prices. These fell 3% in August and are 7.6% lower than a year ago.

Pump prices are lower again in September, though a recent bounce in crude oil prices should see what we pay go up again in early October.

In terms of the higher inflation sectors of recent times, there were no major moves.

Rents were up 0.6% on the month again and still look locked into around 6-7% annual growth.

Insurance prices were up 2.8% for the quarter and remain near double-digit annual growth.

Service inflation (around two-thirds of the CPI) is at 4.2% – still too high – but with wage growth topping out at 4% and likely to ease back, the RBA should be getting a bit more comfortable.

Implications

This data doesn’t change our view.

We still expect four rate cuts next year, likely at a quarterly pace beginning in February.

Market pricing is not too dissimilar, though pricing almost one cut by December.

While the RBA will ignore the subsidy-led lower headline inflation, we feel it is underestimating how this feeds back into wider prices.

A higher inflation loop (inflation leads to wages leads to inflation) of 2022 and 2023 is now a lower inflation loop.

We also expect Federal Government electricity subsidies to become a permanent feature.

The shift by the RBA yesterday to neutral (hikes are no longer being actively discussed) is step one in the move towards an easing.

By year-end, the US Federal Reserve will have its cash rates around Australia’s cash rate and we expect both to move nearer to neutral in 2025.

About Tim Hext and Pendal’s Income & Fixed Interest boutique

Tim Hext is a Pendal portfolio manager and head of government bond strategies in our Income and Fixed Interest team.

Tim has extensive experience in banking, financial markets and funding including senior positions with NSW Treasury Corporation (TCorp), Westpac Treasury, Commonwealth Bank of Australia, Deutsche Bank, Bain & Co and Swiss Bank Corporation.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia.

Find out more about Pendal’s fixed interest strategies here

About Pendal

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

In 2023, Pendal became part of Perpetual Limited (ASX:PPT), bringing together two of Australia’s most respected active asset management brands to create a global leader in multi-boutique asset management with autonomous, world-class investment capabilities and a growing leadership position in ESG.