Despite a cloudy narrative, Pendal’s emerging markets team remains overweight in Chinese equities via a highly selective set of stocks. Here, they explain why

- China bond market moves look rational

- Good results among domestic companies

- Find out about Pendal Global Emerging Markets Opportunities fund

This article is more than 12 months old. Find our latest insights here

THERE’S been a lot of focus recently on what bond market signals are telling us about the outlook for growth.

This is true for emerging markets such as Brazil and Mexico as well – though investors have tended to overlook some dramatic moves in Chinese bonds.

The US five-year bond yield has fallen slightly this year.

Medium-term bond yields have risen in many emerging markets, amid concerns that a strong US dollar might delay interest rate cuts, or even (as is the case in Indonesia) prompt interest rate hikes.

In China, though, the five-year bond yield has fallen from 2.4% to less than 1.9%.

This has led China’s central bank (also known as the People’s Bank of China or PBoC) to worry about a bubble in Chinese government bond prices.

As a result the PBoC has been gently intervening in markets to try to prevent bond yields falling too far or too fast.

Bond yield moves look rational

Despite the central bank’s concerns, these moves in yields look rational to us.

Inflation in China is low and quite possibly negative. The latest inflation measures are +0.5% for CPI, -0.8% for PPI (both to July) and -0.7% for the GDP deflator.

Deflation increases the real yield on bonds, while real estate and equities are potentially hurt by deflation in a leveraged economy.

Find out about

Pendal Global Emerging Markets Opportunities Fund

As well as the signal from inflation, the credit environment is also signalling an ongoing deflationary economic slowdown.

July lending data shows a contraction in bank loans as corporates and households look to pay down debt.

This is the first contraction in lending in the economy since 2005, including during Covid and the GFC.

Given the historical pattern of a decade-long, debt-driven real-estate boom followed by what looks like a debt-deflationary slowdown, there is a temptation to see China falling into the same kind of balance sheet recession that Japan experienced after its late 1980s boom.

Only just this year has Japan’s Nikkei equity index exceeded its 1989 peak.

Do Chinese equities also face a similar “lost decade” as Japan did in the 1990s?

One group that might be worried are the western multinational companies that have been reporting sharp downturns in their China sales in recent quarters.

From beer to luxury products to cosmetics to cars, a clear pattern has emerged of results commentary warning about Chinese demand.

We feel a more detailed look at company results shows a different, more promising pattern.

Good results among Chinese companies

In the above consumer segments – as well as areas such as travel, tourism and e-commerce – many Chinese domestic companies are reporting good results and earnings growth.

Consensus estimates of future earnings are also being revised up.

We feel this reflects Chinese consumers pivoting to different products and lower price points, as well as a new preference for domestic Chinese brands.

For example, foreign car makers have fallen from 64% market share in China to 38% over the past four years.

A similar pattern is emerging in other products, including beer and cosmetics.

With these companies performing well, China’s broad equity market weakness in recent years (especially for Hong Kong-listed names) has pushed some stocks to attractive valuations – especially compared to falling bond yields.

Yes, China’s economy is struggling for growth.

Its credit environment is particularly difficult and there has so far been no turnaround in the wider real estate market.

Yet there are opportunities to be found in Chinese equities.

We remain overweight Chinese equities in the portfolio, with exposure to a highly selective set of stocks.

About Pendal Global Emerging Markets Opportunities Fund

James Syme, Paul Wimborne and Ada Chan are co-managers of Pendal’s Global Emerging Markets Opportunities Fund.

The fund aims to add value through a combination of country allocation and individual stock selection.

The country allocation process is based on analysis of a country’s economic growth, monetary policy, market liquidity, currency, governance/politics and equity market valuation.

The stock selection process focuses on buying quality growth stocks at attractive valuations.

Find out more about Pendal Global Emerging Markets Opportunities Fund here

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

Here are the main factors driving the ASX this week, according to Aussie equities analyst and portfolio manager ELISE MCKAY. Reported by portfolio specialist Chris Adams

- Markets are pricing in a 33bps Feb cut in September

- The Australian Boomer is continuing to boom

- Register now: join Crispin Murray’s Beyond the Numbers webinar

- Find out about Pendal Focus Australian Share fund

REPORTING season has shown that the consumer is holding up better than expected – helped largely by Baby Boomers – and credit conditions have improved, benefiting the REIT sector. Capital discipline has been rewarded.

The S&P/ASX 300 gained 1.01% last week, but the US market was muted.

The S&P 500 was up 0.27%, while the NASDAQ was down 0.91% as NVIDIA’s (down 7.7%) result was not good enough for the market.

NVIDIA reported strong revenue, with data centre sales up 154% year-over-year (YoY) and ahead of expectations, signalling that AI demand is intact. However, its gross profit margin guidance disappointed, resulting in much more muted EPS upgrades.

It was a quiet week on the macro front.

US Personal Consumption Expenditures (PCE) inflation data is no longer a major market mover, unlike earlier this year, as the Fed has moved its primary focus from inflation to labour.

With a September rate cut now a given in the US, the labour data released this Friday (6 September) will be key to helping determine the size.

While the market is pricing a 50% chance of a 50-basis-point (bps) rate cut, the Atlanta Fed GDPNow Tracker is forecasting a robust 2.5% real Gross Domestic Product growth for Q324 – suggesting that we are still on track for a soft landing.

US policy and macro

PCE data

July’s PCE inflation was in line with expectations on both a headline (up 0.2% month-on-month (MoM) and 2.5% YoY) and core (up 0.16% MoM and 2.6% YoY) basis.

This is the third consecutive month where we have seen the MoM number come in below the Fed’s forecast. As a result, we expect that the Fed committee will need to revise down its Q2 2024 inflation forecast at next month’s meeting, which is currently sitting at 2.6%.

There was nothing in this print to upend the view that the Fed has moved from being inflation-first to labour market-first.

The market’s question now is whether the Fed cuts by 25bps or 50bps in September. This Friday’s labour data will be key in this regard.

PCE Core goods inflation is back in deflationary territory, with a MoM print down -0.1%.

The Fed’s preferred metric, Core services (excluding housing), increased from 0.16% last month to 0.21% MoM. But the trend is in the right direction, with the three-month annualised rate now at +2% YoY.

Personal consumption

Consumption growth has maintained decent momentum – with real consumption spending coming in at 0.4% MoM (versus consensus at 0.3%), driven primarily by goods expenditure (up 0.7% MoM).

Spending on autos picked up meaningfully to 4.1% MoM, but even stripping this out, goods expenditure still grew a robust 0.4% MoM.

Consumption appears to have accelerated from the 2.9% annualised rate in Q2. This is at odds with income growth, which is on the weaker side.

Personal incomes grew 0.3% MoM in July and real after-tax income rose by just 0.1% MoM, with the annualised number only just over 1%.

With consumption running roughly 2% above income growth, consumers are saving less in order to fund their lifestyles. The savings rate dropped to 2.9% in July – the second lowest rate since 2008 and well below the pre-Covid average of about 6%.

It is reasonable to assume that, should the labour market continue to soften, we should see people start to save more in precaution, thus dampening consumption growth. However, this is yet to be seen in practice.

US pending homes sales

The strength in consumer spending has not made its way into a stronger housing market. Pending home sales fell 5.5% in July, versus expectations of 0.2% growth.

This index is now at a new all-time low for its 24-year history.

Mortgage rates have been dropping and are now, on average, 70bps lower in August than in May, but this has not yet reached levels sufficient to support mortgage demand.

Unlike in Australia, mortgage rates can be fixed at the outset for the full term in the US. As a result, the differential between existing mortgages and market rates makes it too expensive for many homeowners to move, which should continue to weigh on the supply of homes for sale.

Upcoming Fed meeting

The next meeting is scheduled for 17-18 September.

Over the past week, the market has moved to price in a 33bps cut in September (i.e. roughly halfway between a 25bp and a 50bp cut) and about 100bps of cuts by the end of the year.

We would likely need to see an unemployment rate at 4.3% in this Friday’s labour data to support a 50bp cut. This remains to be seen, though weekly claims data is supportive of an unemployment rate below 4.3%, with the four-week average claims running at 232k.

Soft landing data After strong 3% growth in GDP for Q224, of which two-thirds was driven by consumption, the Atlanta Fed GDPNow Tracker is looking for a robust 2.5% in Q324. This has ticked up following strong consumption data.

Australia policy and macro

Australia’s July Consumer Price Index (CPI) fell from 3.8% YoY in June to 3.5% YoY in July.

This was 10bps higher than expected, but the timing of an electricity subsidy accounted for the difference.

The trimmed mean CPI slowed to 3.8% YoY from 4.1% YoY and is trending down broadly in line with the RBA’s most recent forecasts for Q324.

Retail sales were up 2.3% YoY in July but flat month-on-month and below consensus expectations of +0.3%.

This is somewhat surprising given the strong start to FY25, flagged by several consumer discretionary companies during reporting season.

One possible explanation is that the stronger players in each category – think Temple & Webster (TPW), Endeavour (EDV), Universal Stores (UNI) – are taking market share.

As previously flagged, the Australian Boomer is continuing to boom.

UBS estimates that the total retirement benefits paid out over FY24 rose to a record high of $160 billion, equivalent to roughly 11% of household income.

This has been driven by record-high levels of retirement assets, which now total $3.9 trillion (about 147% of annual nominal GDP).

Retailers that cater for an older demographic (e.g. Nick Scali (NCK)) have benefited in this environment.

We also saw the latest capex data for Q2 2024.

It suggests that mining companies are becoming more cautious on the outlook for investment in the sector, with FY24 estimates downgraded and forward estimates tracking for a fall in FY25.

That said, we have seen some companies buck this trend during reporting season, with both Fortescue (FMG) and Mineral Resources (MIN) guiding to increased capex spend.

Find out about

Pendal Focus

Australian Share Fund

Crispin Murray,

Head of Equities

Eurozone inflation

The August print was in line with expectations, keeping the European Central Bank on track to cut by 25bps at the September meeting.

Headline inflation is now running at 2.2%, while core inflation is running at 2.8%.

Services inflation (at 4.2%) remains stubbornly sticky and may have been assisted by one-off factors such as the Olympics.

NVIDIA result and AI

NVIDIA yet again beat expectations and raised guidance in its quarterly results last week.

Revenue grew 15% to US$30 billion for the quarter (versus consensus of 10% growth) and guided to US$32.5 billion for Q3 2025 (versus the market at US$31.5 billion).

Data centre demand remains strong and broad-based across hyperscale, consumer internet and enterprise customers.

The demand for sovereign AI has strengthened further, with low double-digit billions in sales forecast for FY25 (increased from high-single digits). This reflects sovereign states’ desire to build AI models that are based on local datasets, language and cultures.

However, the disappointment was on gross profit margin guidance at 75% for 3Q 2024, which was 40bps below expectations and implied guidance for gross profit margins in the low-70s for Q4 2024.

This reflects the introduction of the new Blackwell family of chips, which start at a higher cost before reaching scale during 2025.

Revenue upgrades on a bullish outlook for data centre demand were mostly offset by cost upgrades, limited EPS upgrades to low-single digits.

Valuation does not look unreasonable in our view, with NVDA trading roughly 15% below its five-year average multiple.

NVDA’s 154% YoY growth in data centre revenue is supportive for the local Australian-listed plays, like Goodman (GMG), NextDC (NXT), Macquarie Telecom (MAQ) and Infratil (IFT), of which the first three are held across a variety of Pendal’s Australian equities portfolios.

Find out about

Pendal Smaller

Companies Fund

Australian markets

The final week of reporting season was a good one, though the S&P/ASX Small Ordinaries was a touch softer (down 0.19%).

Financials (up 2.21%) and REITs (up 2.20%) were the best-performing sectors, while Technology (down 1.65%) and Consumer Discretionary (down 1.30%) were the weakest.

A few industry-level observations emerged from reporting season, including:

- Bank net-interest-margins (NIMs) surprised on the upside and domestic general insurance trends have strengthened.

- The contractors and services companies have been getting it done – those already in good shape (e.g. Seven Group (SVW) and Ventia (VNT)) have excelled in an easier labour environment, while the tough operating environment in recent years has helped whip the rest of the sector into much better shape (e.g. Downer (DOW) and Worley (WOR)).

- Consumer discretionary has been a mixed bag, but the highest-quality operators have continued to take share and grow in a challenging retail environment (e.g. Breville Group (BRG), Temple & Webster (TPW), JB Hi-Fi (JBH), Universal Stores (UNI), Super Retail (SUL)).

- Travel has been more challenged and FY25 is likely to be more volatile, particularly for the travel agents and those exposed to hotel bookings (e.g. Flight Centre (FLT), Webjet (WEB), Corporate Travel Management (CTD) and Siteminder (SDR)). On the other hand, Qantas (QAN), continues to trade well.

Our property team of Peter Davison and Julia Forrest note the following regarding the REIT space:

- REITs have broadly seen better rent growth (up 4.1%), with malls particularly strong (up 5.8%) and office still the weakest sub-sector (up 2%).

- Nearly every REIT is highlighting far better credit conditions, longer tenor and lower margins.

- Debt costs, as measured by the three-year swap rate, have fallen by almost 60-80bps in the past two months – boding well for leveraged names and property fund managers.

- Regional malls are all trading well, with positive leasing spreads, low occupancy and very good demand for regional mall space. Importantly, buying interest for larger property assets is now reaching larger-scale mall assets. There has been very good demand for recent unlisted offerings by Scentre Group for its Tea Tree and Westlakes mall assets in Adelaide. This is a meaningful change in market dynamics.

- Melbourne is the weakest residential market, while Brisbane, Perth and Adelaide are very strong. Retirement living (land-lease communities) is also very weak in Melbourne.

- Apartment markets are all very weak on delivery concerns and affordability issues. Only luxury apartments are making money.

- Industrial assets are still recording high rent growth (about 4.6%).

- Office is still the weakest sector, with 2% rent growth.

About Elise McKay and Pendal Australian share funds

Elise is an investment analyst and portfolio manager with Pendal’s Australian equities team. Elise previously worked as an investment analyst for US fund manager Cartica where she covered a variety of emerging market companies.

She has also worked in investment banking and corporate finance at JP Morgan and Ernst & Young.

Pendal Horizon Sustainable Australian Share Fund is a concentrated portfolio aligned with the transition to a more sustainable, future economy.

Pendal Focus Australian Share Fund is a high-conviction equity fund with a 16-year track record of strong performance in a range of market conditions. The Fund is rated at the highest level by Lonsec, Morningstar and Zenith.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Here are the main factors driving the ASX this week, according to Pendal’s head of equities CRISPIN MURRAY. Reported by portfolio specialist Chris Adams

- US economy slows, but no signs of a recession yet

- Green light confirmed for a series of rate cuts in the US

- Find out about Pendal Focus Australian Share fund

- Coming soon: register to join Crispin’s Beyond the Numbers webinar

MARKETS continued trailing back toward their July highs last week, driven by commentary from Federal Reserve Chairman Jay Powell.

Powell expressed confidence that a soft landing is achievable and said that the Fed would focus on keeping the labour market strong as it makes progress towards its inflation target.

The “Fed put” is back in terms of monetary policy, providing important insurance against recession risk.

US bonds rallied and the market is now pricing in a roughly 50% chance of a 50 basis point (bp) rate cut in September.

The US Dollar weakened, which is supportive for risk assets, and crypto rallied, indicating that liquidity is coming back to markets.

The S&P 500 gained 1.47%, while the S&P/ASX 300 finished up 0.90%.

The main check on equities is the fear of September, which is seasonally the weakest month.

Local earnings results remain supportive, albeit with some pockets of weakness which tend to reflect specific industry issues rather than broader economic malaise

Pendal Focus Australian Share Fund

Now rated at the highest level by Lonsec, Morningstar and Zenith

US economy: green light confirmed for a series of rate cuts

Two years ago, Powell used his Jackson Hole address to signal that the Fed would risk recession to restore price stability.

His speech at the same venue last week was as close as you get in central bank world to a declaration of victory.

The message was the labour market will not be a source of inflationary pressure. Instead, it is cooling – and the Fed does not want it to cool any further.

Powell noted that “the time has come for policy to adjust” and that “the direction of travel is clear, and the timing and pace of rate cuts will depend on incoming data, the evolving outlook and the balance of risks”.

There was no specific lead on whether we see a 25bp or 50bp cut in September; this depends on employment data.

However, the key point is that we will see a series of cuts into next year.

This is supportive for equities as it reduces the tail risk of a recession. Should the economy slow quicker than expected, it will still affect the market – but the downside is limited, as it would be mitigated by more accelerated easing.

The more material tail risk is a re-acceleration of inflation as the economy cools, but this looks unlikely for now.

US economy: slowing but no signs of recession

There were a number of data points supporting the notion of an economy which is slowing, but not sliding into recession.

- US payroll data saw its annual revisions and was adjusted down 818k for the year – this is much larger than normal and gives fuel to bearish arguments. It was expected, to some degree, given the gap between this data set and the Household Survey. The key observation is that the economy wasn’t as strong as previously thought and that cracks in the labour market started earlier. But this does not imply that the odds of recession have risen. We note this data is often revised again and the final estimate has been above the preliminary for the past five years.

- Jobless claims data remained benign again last week

- The Flash US composite Purchasing Managers’ Index (PMI) data was solid, falling to 54.1 versus 54.3 the previous month, but above the consensus of 53.2. Services rose to 55.2 from 55.0 and beat expectations of 54.0. Manufacturing was weaker at 48.0 versus 49.6 last month and the 49.5 expected. There was a drop in the employment component to 48.9 from 51.6, which highlights there are still risks to employment data.

- New home sales were stronger than expected, which could signal that the impact of lower mortgage rates is beginning to flow through. This may help clear the inventory issue holding back new home construction.

The Atlanta Fed GDP Now measure is still hanging in there at 2.0% for Q3. It has dropped from just under 3%, which relates to home construction, which may turn soon.

Europe

Stronger PMI data was put down to a combination of the Euros, Olympics and Taylor Swift.

Underlying growth remains soft, with Germany quite bleak.

The European Central Bank’s (ECB) indicator of negotiated wages fell materially from 4.74% to 3.55%. This should remove one of the barriers to future ECB rate cuts.

Markets

Last week’s weakness in the US Dollar was interesting.

The US Dollar Index (DXY) fell 1.7% – just breaking down through a technical resistance level – and is down 4.9% in the quarter to date.

This reflects the more benign US inflation outlook, allowing the Fed to move faster on rate cuts.

A falling US Dollar, combined with weaker oil and lower bond yields, is typically helpful for equities.

The other potential positive is that a weaker US Dollar may allow Chinese policy to be more stimulative. This remains the key concern for global growth and has weighed on commodity prices and resource stocks.

The oil price is resting on technical support levels. Iraq is making noise about breaking its quotas, so the Saudi reaction will be interesting.

Australia

The ASX continues to grind higher.

Resources didn’t drag last week – the main sector moves were driven by stock-specific factors relating to results, notably Wisetech Global driving tech and Brambles lifting industrials.

Thus far, the take-outs from reporting season are:

- The market is looking for beta – any promise of upside is being enthusiastically embraced rather than being challenged, as seen in Wisetech last week and Pro Medicus the week before.

- Good industry structures and capital discipline are being rewarded (e.g. insurance).

- Some signs of a turn in industrials which have been navigating a post-covid hangover (e.g. Brambles, Ansell and Reliance Worldwide)

- Consumers are receptive to product innovation and good value propositions (eg Breville Group and Super Retail)

- The steel industry is suffering as a result of China’s over-production and exports

- Earnings volatility and rising capital intensity are being penalised by the market (eg A2 Milk and Ampol).

About Crispin Murray and the Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia. Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions.

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

What can we learn from the latest RBA meeting minutes? Head of government bond strategies TIM HEXT offers readers a look inside the meeting of “two-handed” economists

- Less spare capacity in economy than previously thought

- Why bonds, why now? Pendal’s income and fixed interest experts explain

- Browse Pendal’s fixed interest funds

IF anyone complains about RBA transparency, they are not paying attention.

The minutes from the central bank’s early August meeting were released today, though I am not sure minutes is the correct word – at 3,667 words, transcript might be a better term.

Together, with the post-meeting press conference, the RBA is putting its best foot forward in communicating with the public, as encouraged by the RBA review.

There was so much to say but so little confidence in anything.

Even the new Deputy Governor Andrew Hauser chose a recent speech to warn of false prophets and said we should have little confidence in any forecasts.

In the minutes we were treated to such gems as:

- “It was not possible to either rule in or rule out future changes in the cash rate.”

- “Members will rely on the data and evolving assessment of risks to guide the Boards decisions.”

- “Members observed that a range of uncertainties could influence the outlook for inflation, including the evolution of the labour market, household saving behaviour and the extent of spare capacity, as well as global geopolitical developments.”

However, the one thing the RBA was keen to say is that if the Board was to do anything near term it is hiking – not cutting.

It believes there is less spare capacity in the economy than previously thought. If that does not improve, then inflation will be too slow to fall.

Very little spare capacity when GDP is barely growing?

Sounds like the Board still believes we have a supply problem. Otherwise, its message could be summarised as “we need a recession to beat inflation”, which is a variation of Paul Keating’s “recession we had to have”.

I am not sure it would want that headline.

We disagree with the RBA’s current concerns, finding more agreement with the ex-RBA chief economist – now Westpac Chief economist – Luci Ellis.

She describes the RBA as “skating to where the puck used to be” due to the fact that the RBA is focused on where the labour market was, not is.

Recent data showing increasing participation and supply, falling hours worked per person, and improving real incomes means the puck has moved.

In the months ahead, the RBA should be increasingly comfortable with labour market dynamics helping lower inflation. This should change its narrative and see it follow other central banks by cutting rates early next year.

Remember, the RBA stated in February 2022 that “while inflation has picked up, it is too early to conclude it is sustainably within the target range” and that “there are uncertainties about how persistent the pick-up in inflation will be as supply side problems are resolved”.

In May 2022, it hiked.

Outlook

Markets for now are largely ignoring the RBA anyway. Three-year bonds remain near 3.5% and ten-year bonds finally seem to be holding just below 4%.

At these levels, bond markets are no longer super cheap but, at the risk of becoming a two-handed fund manager, they are also not expensive. It is important to remember the cycle has turned and, when that happens, yields will trend lower for an extended period.

About Tim Hext and Pendal’s Income & Fixed Interest boutique

Tim Hext is a Pendal portfolio manager and head of government bond strategies in our Income and Fixed Interest team.

Tim has extensive experience in banking, financial markets and funding including senior positions with NSW Treasury Corporation (TCorp), Westpac Treasury, Commonwealth Bank of Australia, Deutsche Bank, Bain & Co and Swiss Bank Corporation.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia.

Find out more about Pendal’s fixed interest strategies here

About Pendal

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

In 2023, Pendal became part of Perpetual Limited (ASX:PPT), bringing together two of Australia’s most respected active asset management brands to create a global leader in multi-boutique asset management with autonomous, world-class investment capabilities and a growing leadership position in ESG.

Here are the main factors driving the ASX this week, according to Pendal’s head of equities CRISPIN MURRAY. Reported by portfolio specialist Chris Adams

- The gravest fears for a material market sell-off look to be over

- Positive first week for ASX reporting season

- Find out about Pendal Focus Australian Share fund

- Register here to join Crispin’s upcoming Beyond the Numbers live webinar

A BOUNCE-BACK in equities accelerated last week as the market gained confidence that the US economy was not entering recession, liquidity remained supportive and the bulk of the Japanese yen carry-trade unwind had played out.

The S&P 500 rose 3.99%, breaking through technical resistance levels to get within 2% of the July high, while the S&P/ASX 300 gained 2.57% and is also within 2% of its highs.

Key US data points indicated the labour market was holding up. Retail sales and Walmart results pointed to a solid consumer and survey data suggested August may be stronger relative to July.

Since a back-track from the Bank of Japan, the yen has stabilised and the Topix has staged a strong recovery. This materially reduces the risk of a negative liquidity spiral.

The VIX (a measure of stock market volatility) has unwound its spike and is back to the levels of late July, which means the forced cutting of positions should have finished.

So, the gravest fears for a material market sell-off look to be over.

With negative seasonal effects and limited new positive news, we expect that the market can now consolidate. It has shown impressive resilience and that should help underpin returns into the year end.

All eyes are on Fed Chair Powell and his Jackson Hole speech this Friday.

In Australia the first major week for results was positive.

Banks, telecom and discretionary stocks are seeing upgrades and the broader read on the economy suggests things are holding up well.

US growth – recession risk reduced, the soft-landing narrative has resumed.

A series of data points, while not strong, highlight the economy is holding up and the payrolls panic is now dissipating.

- Survey data is supportive — Indicators such as the Evercore ISI Company Survey are ticking higher in August.

- Solid US retail sales growth — Headline retail sales rose 1.0% month-on-month in July, helped by a weather-related bounce back in auto sales. But even the underlying ex-auto data was solid, growing +0.3% month-on-month and taking the three-month annualised rate back to 4.9%, the highest level since late 2023. The market was relieved there were no signs of renewed weakness and encouraged by the improvement in some of the discretionary sectors such as consumer electronics, hardware and auto. Survey data such as the Evercore ISI Retailers Sales Survey indicate August may be good, with firm back to school sales. Decelerating income growth remains the risk to consumption.

- Strong Walmart sales — Walmart, along with Amazon, is the proxy for US retail sales at ~10% of market. It reported 4.2% sales growth, which is ~150bps above the US average. This is driven by its E-com business, but also signals disinflation easing. General merchandise saw the first positive sales growth since Q4 2021. It is interesting to note that Walmart represents 15% of total US retail sales growth, while Costco (with 3% market share) is capturing 6% of total growth and Amazon is getting 45% of the growth.

- Initial jobless claims eased off — The market was focused on this as a read on non-farm payroll data, given the latter prompted recent volatility. A longer term look at continuing claims, which are correlated to job losses, also suggests we are not at recessionary levels.

We did see some weakness in housing starts and also in the homebuilder survey, despite the recent move lower in US mortgage rates.

This is an interest rate-sensitive sector and will motivate the Fed to cut rates.

Inflation gives them scope to do so:

- July’s headline consumer price index (CPI) rose +0.2% month-on-month and is at 2.9% year-on-year. Core CPI is up +0.2% for the month and 3.2% for the year.

- “Super-core” inflation is running below the 2% target on a three-month annualised basis.

This suggests inflation is not a barrier for rate cuts, that there is no need to hold rates in the 5% range, and that we should see 75-100bp of cuts by the end of the 2024.

On the political front, the RCP Betting Average data indicates that Kamala Harris is currently the clear favourite to win this year’s Presidential election. Her win probability is sitting at ~53% versus ~46% for Donald Trump.

We are beginning to see some indication of policy from Harris. The most relevant for our market was the potential for first time home buyer support for new homes, which would be positive for James Hardie.

Australia

We saw more strong employment data, with employment rising 58k month-on-month versus market expectations of about 10k. Full time employment rose 62k.

Both the three and six-month rise in employment is accelerating, which highlights that the economy is fine.

Hours worked also rose, up 0.4% month-on-month, although there were material reductions to prior months, which should help productivity measures look better.

Unemployment did rise, up 0.1% to 4.2%. This is due to labour participation rising to record levels of 67.1%.

The bottom line is the economy remains in good shape, and the consumer should hold up while the labour market remains as it is.

We also saw the RBA talking hawkishly about the outlook for inflation and clearly signalling rates won’t be cut until next year. The market is expecting the first cut in February.

Markets

The rally in markets has broken the technical downtrend and now looks likely to test the highs, but will probably consolidate in a trading band through to October, in our view.

Technical indicators such as the stock advance/decline ratio show some good strength, albeit now as positive as we saw at the market low in October last year.

The proportion of stocks above their 200-day moving averages also suggests the market is unlikely to break down.

Pendal Focus Australian Share Fund

Now rated at the highest level by Lonsec, Morningstar and Zenith

Bonds are hovering around the support levels of 3.80% (for US 10-year treasuries). We would probably need to see more weak data for them to go lower from here.

All this suggests we are back to the best of both worlds – inflation low enough to cut rates combined with a slowing economy that is avoiding recession.

ASX reporting season

Australia also had a strong week, benefiting from the broader global market bounce and a good start to reporting season.

The first big week of results season was a clear positive for the market:

- Large index stocks are all doing well. Commonwealth Bank saw positive earnings revisions on better margins and lower bad debts. Telstra also saw positive revisions. CSL was revised down 4%, but this was seen more as them being conservative.

- Stocks exposed to the domestic economy all point to solid back drop. JB Hi-Fi said June and July retail sales were good. Seven Group, a bellwether for industrial demand, was positive on the outlook.

- Popular growth names like Pro Medicus and Car Group were comfortable with their outlooks

- Any negative surprises tended to be limited and generally stock specific. Cochlear and Origin Energy had cost issues, while Seek’s challenges relate to job advertisement volumes, which are more tied to labour turnover than job losses.

M&A activity is providing additional support. Orora received a takeover approach while Sims sold off a business at a good price.

It is worth highlighting the substantial sector rotation between banks and resources.

Another ~7% relative move last week takes calendar year-to-date outperformance of banks versus resources to more than 30%, which is a material move in a historical context.

This reflects domestic economic resilience and better margins, while China remains weak with an uncertain outlook.

Iron ore weakness is weighing on Resources. China’s largest steel maker, Baowu, warned China’s steel industry is facing a crisis more serious than the downturns of 2008 and 2015.

This prompted both Tangshan and Yunan provinces to announce steel production cuts in an attempt to improve margins.

We also continued to see weakness in lithium with a poor auction for material in China leading to talk of stock having to be dumped on the market.

We are approaching levels where we may see supply adjustment.

About Crispin Murray and the Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia.

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

The past few years have played havoc with market assumptions. Here, Pendal’s AMY XIE PATRICK explains what’s really going on with inverted yield curves and other misunderstood investing concepts

- Bonds not a “servant asset class” to equities

- Owning bonds at this stage of the cycle could be useful

- Why bonds, why now? Pendal’s income and fixed interest experts explain

- Browse Pendal’s fixed interest funds

THE past few years have played havoc with conventional market assumptions.

Inverted yield curves don’t mean recessions are imminent. Expensive valuations can get more expensive. An aggressive hiking cycle need not bring about recession. Bonds don’t have to go up when equities go down.

These kind of outcomes cause head-scratching among modern-day market participants.

But viewed through a longer-term lens (think multiple cycles and regimes) it becomes clearer.

Let’s have a look at each of these broken relationships.

Are yield curves a recession predictor?

An inverted yield curve happens when short-term interest rates are higher than long-term ones — an unusual occurrence traditionally viewed as a sign of economic slow-down or looming recession.

In my view, inverted yield curves don’t signal imminent recession.

Yes, every US recession has been preceded by an inverted yield curve.

But if you look back through enough history, you’ll discover that the lag between the moment of curve inversion and when a recession eventually hits is highly variable (three months to two years).

As far as recession indicators go, the inverted yield curve is about as useful as a wet paper bag.

So, what does an inverted yield curve tell us? Simply that the market expects interest rate cuts at some point down the line, and that current policy settings are restrictive and will be normalised (for whatever reason) in the future.

Two things cause policy settings to normalise from restrictive territory: either growth slows, or inflation cools. It can also be both, but disinflation is possible without slower growth. 2023 was evidence of that.

Valuations are not a trading tool

Valuations should provide investors with information on risk-reward dynamics, but they have never been a good timing tool for investment decisions.

With the hype of generative artificial intelligence (Gen AI) building over the past year has come plenty of scepticism over where that now puts overall equity valuations. That scepticism is probably what makes expensive tech stocks more expensive when markets are benign.

It takes a reality that falls short of expectations to make those stocks cheaper. Maybe even then, they won’t be outright cheap.

Hikes weren’t the only thing that happened

The rate hikes of 2022 and 2023 were supposed to cause a recession.

What we didn’t expect was a break from fiscal prudence and outright austerity.

The market lacked muscle memory for how to incorporate the pandemic fiscal response. Nowhere was it larger or more enduring than the United States.

The result of this stimulus, which happened in multiple forms over most of the world, was to put cash into people’s pockets.

That liquid spending power mutes the effect of interest rate hikes. Who cares if the cost of borrowing is soaring when there’s all this cash in my pocket?

That doesn’t mean those rate hikes will never matter. The effects will reveal themselves when the cash runs out.

Ironically, for the next economic cycle to begin, this current cycle needs to find a landing.

Soft or hard landing probably doesn’t matter too much – either way, interest rates will come down and borrowing can then become affordable to fuel the next wave of spending.

Bonds reveal their true colours

In the two decades after the Global Financial Crisis — and indeed because of the GFC — central banks extended a “put” to equity markets. If things got bad enough, they would cut interest rates.

Since bond yields and policy rates are inextricably linked, lower yields would lead to a boost in bond prices.

The negative correlation between bonds and equities during this period somehow made its way into tautology.

We are taught in Finance 101 that bonds are a “defensive” asset class, but what we ignored was that the only thing that afforded the “central bank put” was the absence of any real inflation impulse.

Bonds have never been a servant asset class to equities.

The same fundamentals that matter to bonds have always mattered: where inflation goes, where growth goes, and where central banks will take interest rates. That’s why bonds always rally at the start of recessions.

Whether central banks are late or right, a rapid cutting cycle will accompany any recession. The irony is that most recessions are baked in before the first rate cut.

What caused so much grief in 2022 was that higher inflation was a bigger problem than growth. Bonds did their job: yields rose and prices fell in anticipation of higher policy rates.

Since a high-inflation problem is a problem for all asset classes, bonds couldn’t help when equities derated. This time, the inflation backdrop meant that the central bank put was unaffordable.

Supportive part of the cycle for bonds

Bonds respond to the economic cycle.

As an asset class price returns tend to be mean reverting, with the forty-year bond bull run being an anomaly rather than the norm.

What matters more for bonds now isn’t whether the US fiscal situation is out of control, or whether Asian central banks have stopped buying US bonds. Political noise injects volatility bond markets, but their course will be set by the forces of the cycle.

For the next 12 months, what matters is inflation and growth, and on both fronts there’s reason to believe that bonds will be quite useful.

The path of disinflation has been bumpy and slow, but most major economy inflation data are coming within sight of central bank targets. This alone removes the need to fear more hikes and opens the door for easing.

Growth is also softening. No aspect of growth or demand is falling off a cliff, but it’s telling that oil has not been able to rally despite two unfortunate wars taking place in oil-heavy regions.

Europe has been teetering on the edge of recession for almost two years. China is going through its own version of the GFC aftermath. The bright spots have been where most fiscal ammunition was deployed during the pandemic.

The news here is that excess cash from pandemic-related fiscal stimulus is running out. A high US deficit alone won’t replenish that cash – that requires an ever-increasing higher deficit. That positive fiscal impulse is absent from current events.

The not-so-new news is that even if rate cuts were to start immediately, they are unlikely to offset the rise of average borrowing costs as older fixed-rate loans reset. This is especially true in the US.

Effects like these contribute to those long and variable lags of monetary policy.

What’s good for bond won’t always be good for equities

Given the positive correlation between bonds and equities, the market now thinks what’s good for bonds is also good for equities.

That’s true, but only up to a point.

As mentioned, lower inflation and growth are both good for bonds, but only the first of those things is good for equities.

When looking at risk premia across equities, credit and global market volatility, we can see that a soft landing is what’s priced in.

Earnings growth expectations over the next 12 months look very healthy. Trump tax cuts have already been baked into market prices even though polls have seen his chances of winning slide from 70% to now below 50% since Kamala Harris entered the race.

Exuberant sentiment can never in itself cause a market to turn, just like how valuations are poor timing tools. However, when risky assets are priced for very little downside this means that in the event of a negative catalyst, the downside becomes asymmetrically larger than any upside that can be gained from here.

At the start of every cycle’s softening trend, it’s impossible to discern whether the softening will accelerate – resulting in a hard landing.

The early part of the softening is good for bonds and equities, especially as the world comes off a high inflation problem. The risk is increasing that lower inflation will be engulfed by much lower growth.

Owning bonds at this stage of the cycle makes a lot of sense.

They will pay you a positive income and could deliver capital appreciation if inflation continues to come off – especially if that is accompanied by a worsening growth outlook.

The risk is another inflation shock, but there is sufficient consistency in lower prices and wages to argue for removing higher policy rates for the rest of this cycle.

Not owning equities can feel painful when the tech and AI driven story keeps gaining new legs.

So, owning bonds against this FOMO (fear of missing out) is a no-brainer – not because bonds are there to save us when equities fall, but because the growth speed bump that causes equities to fall is exactly the economic fundamental that will be a boon for bonds.

About Amy Xie Patrick and Pendal’s Income and Fixed Interest team

Amy is Pendal’s Head of Income Strategies. She has extensive expertise and experience in emerging markets, global high yield and investment grade credit and holds an honours degree in economics from Cambridge University.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia. The team oversees some $20 billion invested across income, composite, pure alpha, global and Australian government strategies.

Find out more about Pendal’s fixed interest strategies here

About Pendal Group

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

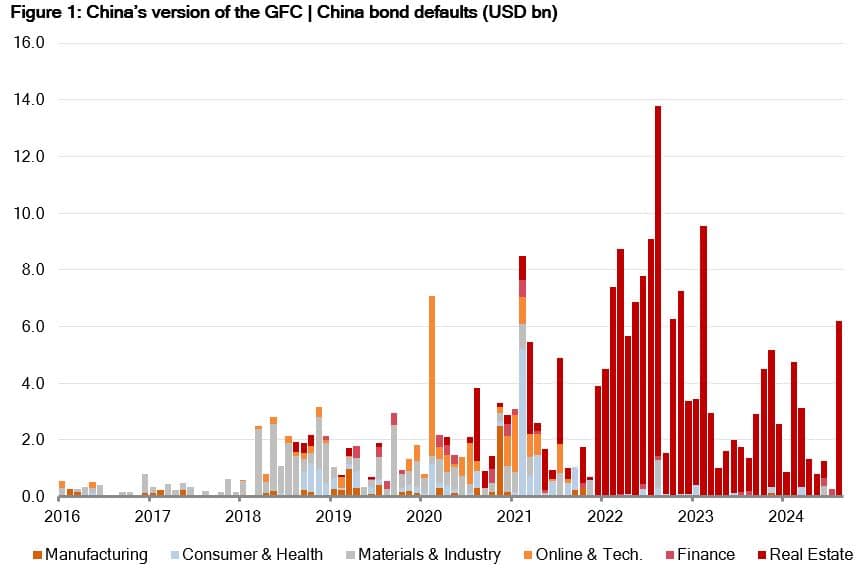

What is the state of play in China? Head of income strategies AMY XIE PATRICK offers an overview of China’s recent Third Plenum and the implications on world economies.

- Property fall-out akin to China’s own Global Financial Crisis

- The cyclical picture for China “not going to get better” in near term

- Why bonds, why now? Pendal’s income and fixed interest experts explain

- Browse Pendal’s fixed interest funds

IN China, the Third Plenum ended with little fanfare.

The market didn’t expect much by way of stimulus policies since almost all hopes of that kind have been repeatedly dashed over the past two years.

As a forum focused on the medium term, it addressed structural over cyclical issues facing China’s economy. The overarching message was about prioritising sustainable long-term growth over short-term sugar hits.

The property market fall-out

We’ve written at length in the past about the nature of China’s economy and its intricate ties to the property sector. We won’t rehash those details here.

The economy’s dependency on real estate means that there are significant withdrawal symptoms to be addressed in the aftermath of the massive Chinese housing slump.

The fall-out is akin to China’s own version of the Global Financial Crisis (GFC).

Source: Bloomberg

It took the US economy close to a decade to heal over the wounds from the GFC. During that time, authorities focused on banking sector repair and regulation.

Fiscal policy remained conservative, leaving quantitative easing (QE) to provide indirect support through the financial markets. Private sector businesses and households focused on balance sheet repair. Low interest rates could do little to incentivise demand for borrowing during this repair phase.

China has many of the same constraints today.

Financial sector reforms are vital for ensuring that new excesses don’t build up in place of previous property-related bets.

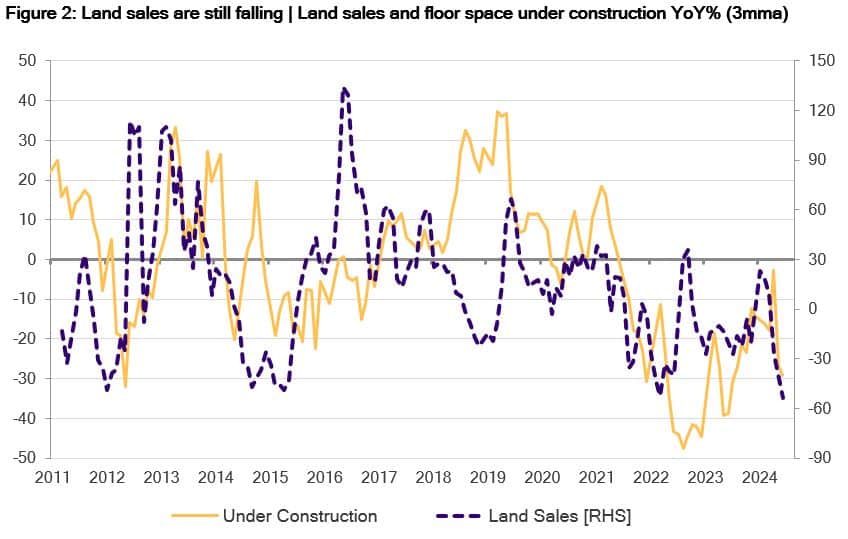

Fiscal policy is unable to provide much boost because local governments who dish out much of this stimulus are hamstrung by the devastating hit to their revenues as land sales collapsed with the housing slump.

Monetary policy can’t help because lower interest rates threaten the stability of the yuan and ultimately the stock of China’s foreign currency reserves.

With home prices now able to fall as well as rise, households won’t be persuaded to add more property to their portfolios just because mortgage rates fall at the margin. There are bigger capital holes to fill in their existing property portfolios.

Source: Bloomberg

Structural over cyclical

The cyclical picture for China is not going to get better in the near term.

Beijing has been unwavering in its resolve to de-lever and de-risk the property sector. These goals have been in play since after the GFC, but each time something got in the way.

Here’s a timeline:

- In 2013, deleveraging efforts ended with a devaluation experiment which resulted in China losing a quarter of its foreign currency reserves.

- In 2015, deleveraging efforts led to a slowdown in demand that swept across commodities and ignited a wave of defaults in the US energy sector.

- In 2017, deleveraging efforts had to be slowed as fighting Trump’s trade war became a priority.

- In 2020, deleveraging efforts had to swiftly U-turn to offset the pandemic.

- Since 2021, the deleveraging commitment has stuck.

While communication from the Third Plenum renewed the government’s commitment to the growth target, more noise was made about the longer-term transition goals for the economy. The hope is to fill property void with high-tech and innovation.

There was also talk of a smoother mechanism for fiscal transfers between central government and local governments. Fiscal reform is a lengthy process, and the overarching goal would be to ease the pain from anaemic land sales revenues rather than greatly increase local governments’ fiscal firepower.

Structurally, changes are afoot on the technology front in China.

Since 2017, the real estate sector’s contribution to final demand in the Chinese economy has fallen from close to 25% to now under 20%, while contributions from the high-technology sectors have growth from 11% to just under 15% (data from IEA).

Renewables power generation capacity now makes up more than 85% of total annual newly added power capacity whereas thermal power has dwindled to under 5%.

The picture 15 years ago was almost the mirror opposite.

In electric vehicles (EVs), thanks to government subsidies and consumer incentives, sales in China make up close to 40% of total vehicle sales. This compares to only 21% in Europe and 10% in the US.

Thank goodness for asynchronous cycles?

China’s unwavering resolve since 2021 to deleverage the property sector has been successful thanks, in large part, to the strength of the global recovery from the pandemic shock.

This acted as economic immunity for the rest of the world from China’s property crisis and prevented a feedback loop that would have otherwise thwarted Beijing’s efforts again.

Subsequently, China’s domestic deflation and weak demand has helped developed market inflation to normalise via the goods channel.

Source: Bloomberg

But now is where things start to get tricky.

There is little reason to hope for big-bang stimulus from China. The policy focus is about strengthening local institutions, balance sheet repair, and positioning new engines of long-term growth.

At the same time, growth is weak or softening in other parts of the world:

- Europe has been dancing on the precipice of recession for the best part of two years.

- Asia’s recovery from the pandemic was weaker than other areas in the world due to its strong links with China.

- Excess cash and savings from pandemic fiscal stimulus are running out for economies like the US and Australia.

China’s investment focus on technology and renewables will not provide the offset needed to steady the ship of the global economy in the near term.

From inflation to deflation?

Of course, it wasn’t long ago that central banks had the opposite inflation problem to what exists today.

No matter how low they kept interest rates and how hard they engaged in QE, inflation continued to undershoot its target in the pre-pandemic era. Part of the problem was the balance sheet recession caused by the GFC. The other issue was continued price deflation in goods and tradeables.

This deflation can be traced back to China producing more than it could consume and relying on global demand to absorb its excess manufacturing capacity.

With a new investment wave in high-tech sectors coming from China comes risks of more deflation from too much capacity in China. This is already apparent in EVs, where the competitive price pressures from Chinese EV producers have forced companies like Tesla to slash prices to defend market share.

The difference between today and a decade ago is the competitive realm. It has moved on from commoditised manufactured goods to high-tech.

“Good enough” is far harder to achieve in high-performance computer chips than plastic children’s toys. Nevertheless, with global trade partners all trying to “de-risk” from China, alternative hopes for long-term growth are few and far between.

These concerns about overinvestment may be just as valid in the west as it is for China. It has certainly been a feature of the latest US earnings season, with growing market scepticism on the pace and scale of company investments into artificial intelligence.

When overinvestment leads to overcapacity, technological success will have a hard time finding its way into company earnings success. Just look at the Chinese stock market.

About Amy Xie Patrick and Pendal’s Income and Fixed Interest team

Amy is Pendal’s Head of Income Strategies. She has extensive expertise and experience in emerging markets, global high yield and investment grade credit and holds an honours degree in economics from Cambridge University.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia. The team oversees some $20 billion invested across income, composite, pure alpha, global and Australian government strategies.

Find out more about Pendal’s fixed interest strategies here

About Pendal Group

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

What does the recent global market volatility mean for emerging markets investors? Here’s an update from Pendal’s Global Emerging Markets Opportunities team

- Key EM factors: Decline in US yields and expectations of Fed rate cut

- We may see monetary stimulus from Asian EM central banks

- Mexico and Brazil set up for fixed-income inflows and significant rate cuts

- Find out about Pendal Global Emerging Markets Opportunities fund

WE’VE seen significant volatility in global financial markets – including emerging markets – in recent weeks.

The main cause was a combination of softer US economic data coinciding with an increase in policy interest rates in Japan.

As a result, we experienced multiple dislocations in fixed interest and currency markets, as “carry trades” were aggressively unwound. Carry trades involve investors borrowing a low-yielding currency to invest in a higher-yielding currency.

This caused a rapid risk-off move across most global financial markets.

In the emerging markets space, market segments with the highest exposure to international investors saw the greatest volatility and weakness.

In EM equities, the pain was concentrated in the information technology (IT) sector, and across Korea and Taiwan. Among currencies, the high-yielding Brazilian Real and Mexican Peso saw the sharpest sell-offs.

What’s next?

The key question now is: what happens next?

We find it hard to be overly positive about the IT sector, despite a reset in valuations from market weakness.

Find out about

Pendal Global Emerging Markets Opportunities Fund

The entire sector has re-rated substantially in recent years, despite essentially soft demand in important end-demand segments such as PCs and mobile phones.

This optimism has been attributed to a potential demand shift from widespread adoption of generative artificial intelligence.

But beyond some key semiconductor names held in our portfolio, we have not seen sufficient evidence of this opportunity.

From a country view, this translates into ongoing caution towards Korean and Taiwanese equities.

Where the opportunities are

In our view, the last six weeks of price moves create opportunity in emerging market interest rates – especially their role as potential drivers of broad domestic demand and local financial markets.

The sell-off prompted repricing of US policy interest rate expectations.

Yields in the middle part of the US Treasuries yield curve have declined by more than 0.5%.

Meanwhile the 12-months-ahead futures-derived expectation for the US Federal Funds policy interest rate are down nearly 1% since May.

In emerging Asia, some economies have failed to fully close the output gap that the Covid slowdowns created.

This has been accompanied by undershoots in inflation and core inflation. But local central banks have been unable to respond with interest rates cuts in the face of stubbornly high US bond yields and interest rates, and a stronger US dollar.

If the Federal Reserve is now to move to reducing policy interest rates, emerging Asian central banks can respond more directly to domestic growth and inflation conditions.

Some Emerging Asian central banks have local issues that may constrain this effect – notably Bank of Korea’s concerns regarding household leverage and the Reserve Bank of India’s worries about growth in unsecured lending.

But we see output gaps, low core inflation and concerns about currency weakness in Indonesia and China – and both of these markets (which are held as overweight positions in our portfolio) could see significant monetary stimulus in the next few quarters.

Mexico and Brazil

Mexico and Brazil also look well placed in the medium term.

Firstly, despite the currency weakness caused by market volatility, the interest rate gaps that drove bond market inflows remain (Brazilian policy interest rates: 10.5%; Japanese policy interest rates were just hiked from 0.1% to 0.25%), and a period of market stability is likely to see a resumption of inflows.

Secondly, we believe the Peso and Real went into the sell-off with some challenges from weaker export revenues, but in no sense overvalued.

Mexico had a trailing current account surplus in the first quarter of 2024, while Brazil’s trailing deficit to June was only 1.4% of GDP – small by historical standards.

Thirdly, real interest rates in both countries remain very high compared to historical levels, with US rates and yields the dominant constraint on cuts.

The faster the US Fed moves to cuts, the faster Banxico and the Brazil Central Bank can follow – which should be highly stimulative for both economies.

It has been a challenging period in global markets, but we believe the fall-out is ultimately positive for emerging equity markets, and particularly positive for the markets we hold as overweight positions in the portfolio.

About Pendal Global Emerging Markets Opportunities Fund

James Syme, Paul Wimborne and Ada Chan are co-managers of Pendal’s Global Emerging Markets Opportunities Fund.

The fund aims to add value through a combination of country allocation and individual stock selection.

The country allocation process is based on analysis of a country’s economic growth, monetary policy, market liquidity, currency, governance/politics and equity market valuation.

The stock selection process focuses on buying quality growth stocks at attractive valuations.

Find out more about Pendal Global Emerging Markets Opportunities Fund here

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

Here are the main factors driving the ASX this week according to portfolio manager JIM TAYLOR. Reported by investment specialist Chris Adams

- Find out about Pendal Focus Australian Share Fund

- Register now: Crispin Murray’s Beyond the Numbers webinar

MARKETS were volatile last week, driven by the blow-off from a US employment report and Yen carry trade reversal in the previous week.

Thursday’s US jobs data provided a circuit-breaker to last week’s employment data doom.

Ultimately, the US equity market finished flat on the week, with the S&P 500 down 0.02%, the NASDAQ down 0.17%, and Australia’s S&P/ASX 300 falling 2.12%.

The US bond market gave up some of its strong month-to-date gains, while commodities were generally softer.

In the absence of much economic data to guide markets, key insights for the week have been derived from US reporting season messages.

Here, commentary highlighted heightened pressure on lower-income consumers, as all the Covid handout savings are gone and extra income is probably, at the margin, harder to generate.

There was also continued softness in big-ticket and discretionary spending, evidence of consumers “trading-down” to cheaper alternatives, and some spillover to travel and lodging demand.

Here’s how the Disney CFO summed it up: “The lower-income consumer is feeling a little bit of stress and shaving a little bit off their time at the parks. The high-income consumer is traveling internationally a bit more.”

As a broad observation on markets, there are two areas where we are evolving to a new (old) normal:

- Inflation. This is falling everywhere but the easy wins – like in goods – are behind us. The rate of decline is slowing, meaning progress to a “2%-ish” target has become a little more volatile and lumpier, and positive surprises on inflation aren’t a one-way bet anymore.

- Earnings. The general state of play in most developed economies is that there are distinct hot and cold parts of the economy, and this gets reflected in the disparity of earnings across stock market sectors. The market may have forgotten this over the last two to three years as the excess savings run down effect has been significant in bolstering activity levels across the board. These have been run down and we now need to readjust to the new environment.

Last week’s stock market volatility was on par with both the GFC and Covid.

This week, we see some genuinely meaningful numbers like PPI, CPI and retail sales – so we expect the volatility to roll on.

That said, some of the panic and calls for emergency rate cuts looks way overcooked.

Central banks

The Fed stepped in quickly to make its position clear amid the market’s fuss.

Chicago Fed President Austan Goolsbee said, “the law doesn’t say anything about the stock market; it’s about the employment and it’s about price stability.”

“As you see jobs numbers come in weaker than expected but not looking yet like recession, I do think you want to be forward-looking at where the economy is headed for (in) making the decisions,” he continued.

San Francisco Fed President Mary Daly made the point that inflation is near the target, that the labour market is slowing and that “it’s to a point where we have to balance those goals”.

She also noted that while rates have been left unchanged, the shift in rhetoric to acknowledge the need to balance between two goals is a policy adjustment in itself.

Elsewhere, Bank of Japan’s Deputy Governor Uchida said it would stick with the current policy setting “for the time being” and “won’t raise interest rates when financial markets are unstable”, in what is seen as a bit of backpedalling following the response to the last rate hike.

Find out about

Pendal Focus

Australian Share Fund

Crispin Murray,

Head of Equities

US macro and policy

The ISM Services non-manufacturing Purchasing Manager’s Index (PMI) rose from 48.8 in June (its lowest level since May 2020) to 51.4 in July.

The ISM Employment Index also picked up – from 46.1 to 51.1.

This rebound in new orders and a rise in employment helped quell recession fears stoked by the employment report the previous Friday.

Better sentiment on employment was bolstered by initial jobless claims, which came in at 233k versus 240k consensus and the prior week’s upwardly revised 250k.

It is interesting to note that the Bloomberg consensus probability of a US recession in the next twelve months has fallen from 60% this time last year to 30% today.

Goldman Sachs has increased its own recession probability in response to recent data but had been running well below consensus at 15% – now standing at about 25%.

Australia macro and policy

As expected, the RBA held rates steady at 4.35%.

Its statement observed that “momentum in economic activity has been weak, as evidenced by slow growth in GDP, a rise in the unemployment rate, and reports that many businesses are under pressure”.

It also noted that inflation had “fallen substantially” but remains “too high” in underlying terms and with upside risks.

As a result, Governor Bullock struck a decidedly hawkish tone, being very clear that “a near-term reduction in the cash rate does not align with the Board’s current thinking” for the remainder of the year.

She also noted that the Board gave “very serious consideration” to holding rates steady for some time or even to raising.

Australia macro and policy

US reporting season

Beneath all the noise, it has been a positive reporting season.

With 91% of the market having reported, the blended earnings growth rate for Q2 S&P 500 EPS currently stands at 10.8%. This compares to the 8.9% expected at the end of the quarter.

The blended revenue growth rate is 5.2%.

And 78% of the market has beaten consensus EPS expectations, which is level with the 78% one-year average and a bit higher than the five-year average of 77%.

Sales expectations are also being routinely beaten.

Companies are reporting earnings that are 3.5% above expectations, which is below the 6.5% one-year average positive surprise rate and the five-year average of 8.6%.

A significant feature of this reporting season has been the weakness in results and outlook commentary in the leisure sector:

- Airbnb pointed to slowing demand as Q3 guidance for revenue and earnings came in soft, with management calling out “shorter booking lead times globally and some signs of slowing demand from US guests”.

- Lyft’s guidance pointed to a 2-4% deceleration in bookings next quarter.

- Hilton Hotels lowered the top end of its FY guidance amid “softer trends in certain international markets and normalizing leisure growth more broadly”.

- TripAdvisor noted a normalisation of experiences demand, moderating pricing and trading down in travel spend.

It is hard to decompose this trend between normalisation of the post-Covid travel boom and a more cautious consumer.

About Jim Taylor and Pendal Focus Australian Share Fund

Drawing on more than 25 years of experience investing in top-performing Australian companies and a background in accounting, Jim manages our Long/Short Fund and co-manages our Imputation Fund. He is a Chartered Accountant with membership of the Australian Institute of Chartered Accountants.

Pendal Focus Australian Share Fund is managed by Crispin Murray. The fund has beaten its benchmark in 14 years of its 18-year history (after fees), across a range of market conditions. Find out more about Pendal Focus Australian Share Fund here.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Pendal’s head of income strategies, AMY XIE PATRICK, explains what the recent market volatility means for fixed-income investors

- Trending ‘unwinds’ contributing to risk-off sentiment

- Volatility expected to stabilise and then fall

- Why bonds, why now? Pendal’s income and fixed interest experts explain

- Browse Pendal’s fixed interest funds

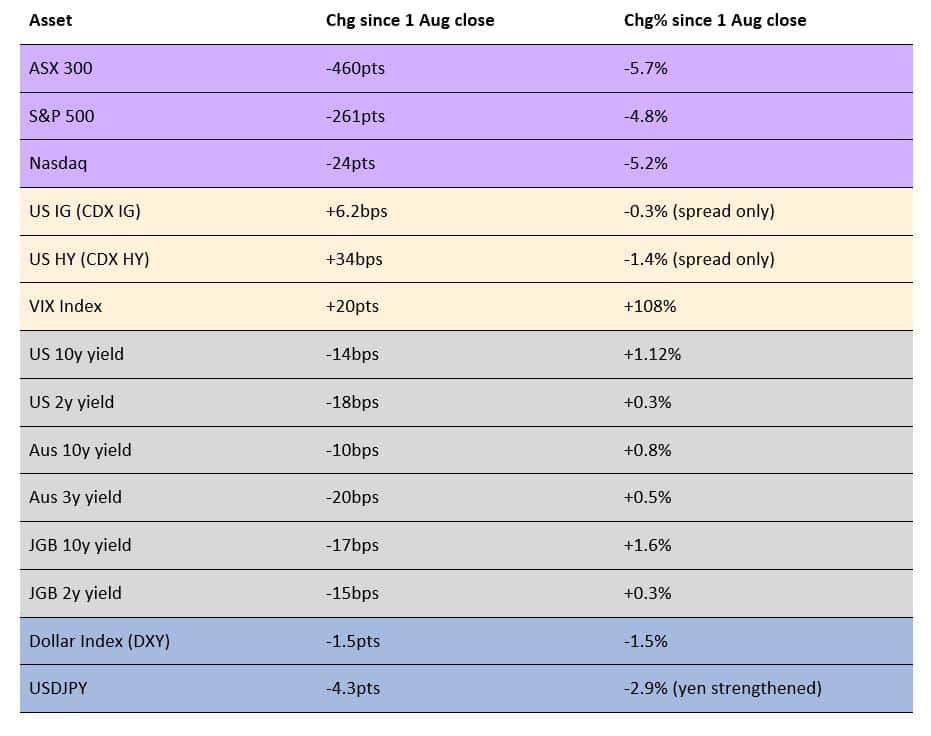

BIG market moves have rocked sentiment since the beginning of August.

The table below shows market moves in equities, credit, volatility and bonds since August 1.

These are classic “risk-off” moves.

Figure 1: Risk off!

Major benchmark moves since market close on Thursday 1 August 2024

Whiplash

For bond investors, it’s not so much the fall in yields that was interesting to witness in the price action of the past few market sessions. It’s the fact they rebounded significantly from the lows seen on Monday, August 5.

US 10-year yields, for example, backed up 19bps from Monday’s session lows and US two-year yields rebounded by more than 30bps.

Perhaps the market remembers the whiplash from early 2024.

Rate markets rushed to over-interpret the Fed’s end to hiking as the start of the next concerted easing cycle. But they were disappointed by an overt “wait-and-see” stance from Fed officials.

In Australia, our markets priced in four rate cuts from the RBA earlier this year, but had to swiftly walk that back when resilient economic and sticky inflation data failed to support those hopes.

Only a few weeks ago, Australian short-end rate markets were pricing in a 50 per cent chance of the August RBA meeting raising the overnight cash rate a further 0.25% to 4.60%.

Following a more benign-than-feared June CPI release, the meeting ended with another hold decision — and an RBA that still “rules nothing in or out”.

Is this an emergency?

In the US, market pricing currently sees a 100% chance of a 0.50% cut in September, followed by consecutive 0.25% cuts in subsequent Federal Open Market Committee meetings.

The argument seems to be that had the Fed seen the full suite of July data at its end-of-July meeting, the central bank would have opted to cut.

On top of this, some big-bank economists are now calling for back-to-back 0.50% cuts – even an inter-meeting emergency cut.

Are things really dire enough to justify a panic to easing?

We argue the data isn’t there yet.

The US labour market report was the main cause of the market’s negative reaction on August 2.

The gain in employment fell well short of market expectations. Unemployment rose from 4.1% to 4.3% while the market anticipated no change.

Employment gains, however, were still gains.

Coupled with a slight fall in average hourly earnings, this is the kind of data that would have had bond and equity markets partying a couple of months ago.

Monday night’s release of a healthier-than-expected set of ISM Services data pointed to no evidence that a recession is waiting on our doorstep.

Similarly, second-quarter earnings season in the US so far shows an earnings beat of 5.2% versus analyst expectations.

This puts total earnings growth from the companies that have reported so far at over 11%.

In recessions, earnings typically fall by 10% or more – so the corporate picture also doesn’t have the US in a recession. Yet.

Various unwinds

A bigger reason for the risk-off market sentiment could be a combination of recent events:

- A “great rotation” away from expensive tech to less expensive small caps, as investors become sceptical that AI-related hype can meet with real results

- The “yen-unwind”, as the Bank of Japan starts to remove the cheapness of yen funding from international carry and risk-seeing trades

- The “great de-grossing”, as risk-parity funds rush to reduce exposures as volatility rises.

By themselves, these trends naturally run out of energy.

The rotation into small caps should end because 40 per cent of Russell 2000 companies are not profitable.

Carry trades should unwind when the excesses in their momentum to the upside have been unwound.

And the risk-shedding of risk-parity funds will end so long as there are not marginally incremental waves of risk-shedding.

Volatility should stabilise, then fall.

Watch the economy

We think fundamentals or a systemic shock are needed to ignite the next recession. Unfortunately, there are a few fundamental developments to worry about.

Over the next year, analyst earnings expectations for the S&P 500 have growth at more than 10% per quarter. That’s not to say it can’t happen — but not even a soft landing seems to be baked in there.

Default rates have continued to climb among US corporates, but even including the moves of the past week, credit spreads are near their cycle lows.

The New York Fed’s recession probability index has climbed to new cycle highs. We know that after a lag, the VIX Index (a gauge of market volatility) also follows.

Vacancy rates in US office real estate have continued to rise and now sit at over 20 per cent. As a result, delinquency rates in US commercial real estate are climbing.

Not just yet

The conclusion of our analysis is that it’s not quite “the big one” just yet.

Following big positive runs in bonds, we need to take a calm breath and ask whether the fundamentals justify the pricing of emergency cuts.

If not, profit-taking comes first. Waiting for the next opportunity to buy bonds comes next.

Zooming out, we’re in the ripe part of the cycle for owning some bonds in portfolios, regardless of your stance on risky assets.

Without a recession, bond yields should continue to fall steadily as central banks around the world normalise their policy settings from restrictive levels.

Some have more work to do than others. Many have already started the journey. That’s because we won’t be talking about inflation as a problem for much longer.

With a recession, bonds will pay for themselves.

Bonds are not guaranteed to perform all the way to the end of a recession, but they’ve always been useful at the start of recessions.

Since the start of recessions are hard to predict, bonds provide great insurance for the unpredictable.

Add to that the 4% types of annual income returns you can currently get on US or Australian 10-year bonds and it basically amounts to being paid to take out insurance.

That’s a nice change from the insurance inflation we’ve all been experiencing for the past two years.

About Amy Xie Patrick and Pendal’s Income and Fixed Interest team

Amy is Pendal’s Head of Income Strategies. She has extensive expertise and experience in emerging markets, global high yield and investment grade credit and holds an honours degree in economics from Cambridge University.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia. The team oversees some $20 billion invested across income, composite, pure alpha, global and Australian government strategies.

Find out more about Pendal’s fixed interest strategies here

About Pendal Group

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.