Here are the main factors driving the ASX this week according to Aussie equities analyst ELISE MCKAY. Reported by portfolio specialist Chris Adams

- WATCH NOW: Crispin Murray’s latest bi-annual Beyond The Numbers webinar

- Find out about Pendal Focus Australian Share fund

A NUMBER of new data points show the economy is holding up just fine.

Surveys of manufacturing purchasing managers are heading higher globally. This is supportive for global growth and strength in commodities, particularly in a tighter supply environment.

In the US, the Institute for Supply Management (ISM) manufacturing PMI index entered expansionary territory for the first time since September 2022. A similar manufacturing survey in China also delivered its highest reading in 12 months.

Initially this manufacturing strength was taken negatively. But as we received ISM services and labour data, the market changed its tune.

Payrolls were a big beat, but this was offset by a rise in labour force participation and moderation in wages. This points to an economy with big supply-side tailwinds, supporting the ability to grow strongly while keeping inflation in check and avoiding overheating.

Progress on inflation should keep the US Federal Reserve on track to cut rates this year, though good economic data may limit the pace of the cutting cycle. This scenario remains positive for equities.

There seems to be differing opinions emerging at the Fed, with a lack of consensus on whether the strength of the economy being supply or demand driven. Recent data suggests the former.

Consensus has historically been important. There have been very few dissenting votes during Powell’s tenure.

The market is now pricing a 53% probability for a June cut. The total of implied expected cuts for 2024 has fallen to 67bps.

This week we will see US CPI data, minutes from the rate-setting Federal Open Market Committee (FOMC), European Central Bank (ECB) policy decisions and the start of US first-quarter earnings season.

The ECB is expected to start rate easing cycle in June rather than this month.

The S&P 500 fell 0.93% last week while the S&P/ASX 300 was down 1.55%.

US economics and policy

Fed speak

Since Fed chair Jay Powell’s last dovish speech on March 20 we’ve heard differing opinions in comments from several FOMC members.

There are three key areas of focus:

- A lack of consensus on whether (disinflationary) supply or (inflationary) demand are driving economic strength.

- Differing views on how to balance the dual mandate of maximising employment and keeping inflation stable. The question is whether the Fed should accept a longer path back to 2 per cent inflation to ensure a soft landing.

- Timing risk: If the Fed can’t justify cutting rates in June, it may have to wait until March 2023 — after the US presidential election.

Does a decision to cut rates need to be unanimous? No, but reaching a consensus is desirable and Fed has a track record of bridging the gap between those who want to move versus those who prefer to wait.

In 2015 when moving off zero rates, the Fed managed to reach consensus when its promise of “gradualism” was enough to get all members on board.

US payroll data

March non-farm payrolls beat expectations by a huge margin, rising 303k versus 214k expected. The three-month average gain of 276k / month is the highest level since March 2023.

However, a rapid rise in US immigration has reduced the effectiveness of non-farm payroll growth as a historical indicator, with an estimated 200k / month increase in labour supply versus a historical growth rate of 100k / month.

It’s more relevant to look at other measures to determine whether the labour market is tightening or not.

On such measures, the unemployment rate down 3bps to 3.83% and average hourly earnings (AHE) were largely in-line with expectations.

The unemployment rate benefited from a 498k surge in the number of employed people. The labour force participation rate increased to 62.7% with prime age sitting at 83.4%.

AHE increased 0.3% month-on-month and 4.1% year-on-year, continuing its downwards trend. Though it is still running ahead of the 3.5% rate estimated to be compatible with the Fed’s 2% inflation target.

US manufacturing health

The ISM services index — a survey that gauges how busy factories are and how confident purchasing managers are about the future — fell to 51.4 in March. That was below expectations of 52.8 and down from 52.6 last month.

Typically a score of above 50 indicates manufacturing is expanding and the economy might be growing, while scores below 50 suggest a slowdown, with fewer orders and production.

About three quarters of the decline came from lower supplier delivery times. Business activity improved slightly from 57.2 to 57.4 — its highest level in six months.

Importantly, we did see “prices paid” drop to a four-year low of 53.4 (down from 58.6) suggesting upward pressure on prices from labour cost is easing further.

This has also been a good lead indicator for underlying core personal spending (excluding housing), suggesting a return to pre-Covid inflation levels are on the way.

Bond yields

Bonds moved 19bps higher last week off the back of strong payrolls. They are up 52bps in 2024.

This move has been driven almost exclusively by better growth expectations in 2024.

US prices back on track

The Fed’s preferred read on inflation is the Personal Consumption Expenditures index, which tracks the prices Americans pay for everything from groceries and petrol to rent and haircuts.

The latest data was released on Good Friday.

Core PCE (which excludes volatile measures such as food and energy prices) rose by 0.26% in February — which was in line with consensus expectations of 0.3%, and up 2.8% year-on-year.

January data was revised up from +0.42% to +0.45%, driven by medical services inflation from the Producer Price Index, which tracks business costs.

This brings annualised inflation for the last 3 months to 3.52%.

Core goods inflation accelerated 0.31% after three consecutive negative prints, primarily driven by a jump in prices for video and IT equipment.

Find out about

Pendal Focus

Australian Share Fund

Crispin Murray,

Head of Equities

Core services (excluding rent) increased 0.18%, but three-month annualised is now tracking at 3.7% due to the big January print.

US consumer spending

Personal income grew 0.3% in February — slightly weaker than expected.

Consumer spending rose 0.8% (versus consensus of +0.5%) in February, with much stronger services consumption (+0.9% in February and +1% in January).

Airfares, recreational services (such as gambling) and financial services were the biggest drivers of services spending. In contrast, goods consumption only increased 0.5%.

US economic growth

The Atlanta GDPnow index monitors a range of economic data such as manufacturing figures, consumer spending and trade numbers, to create a real-time estimate of GDP growth.

The latest data from the Federal Reserve Bank of Atlanta estimates US GDP growth is tracking towards 2.5% for the first quarter of 2024 (at April 4).

Meanwhile the Evercore ISI Trucking survey has improved to the highest level since October 2022 and is showing signs of stabilisation, although still depressed levels by historical standard. There is usually good correlation between trucking survey and US real GDP growth.

Destocking of inventories by retailers appears mostly in the rear-view mirror although, there are not signs of significant restocking activity either.

Surveys of US companies by researcher Evercore ISI are now back in the “solid” 50-55 range on a 100-point scale, having rebounded from the “struggling” 45-50 band.

Global growth

Inflation is coming down in most economies around the world.

Eurozone inflation, having peaked at 10.6%, is now back to 2.4% and within its “normal” historical range.

As mentioned above, surveys of purchasing managers (PMIs) have been heading higher, which is supportive for global growth and strength in commodities, particularly when combined with a tighter supply environment.

- In the US, the ISM manufacturing index was 50.3 for March 2024 (versus consensus of 48.3) and was in expansionary territory the first time in since September 2022.

- China’s NBS manufacturing PMI picked up to 50.8 in March 2024 from 49.1 in February, the highest reading in 12 months and ahead of consensus. This was well received by the market with the Hang Seng Index rallying 3%.

Historically, copper is the biggest metal beneficiary of re-accelerating global manufacturing PMIs, with an average 25% move over the 12 months following a PMI trough, slightly ahead of zinc and nickel.

Unemployment rates in most major economies have also remained low and in check, with some signs they are beginning to rise.

Australia

Inflation data for February came in below expectations, moderating to 3.4% (consensus at 3.5%) and unchanged from January. This is the equal slowest since November 2021.

Goods inflation eased to 2.9% year-on-year (from 3.1%) but services lifted to 4.2% (from 3.7%).

Markets

It was a generally soft week for markets with bright spots among some commodities such as oil, copper and gold.

Consumer discretionary (-2.8%) was one of the worst-performing sectors in the US. Trading updates caused concern despite strength in recent consumer spending and labour-market data.

Investors are concerned that recent management commentary from consumer-facing companies suggests some signs of weakness.

Find out about

Pendal Smaller

Companies Fund

Luxury goods house Ermenegildo Zegna was down 15% on Friday as they guided first-quarter revenues lower.

Costco missed consensus US sales estimates for February. Lulu Lemon, Nike and Ulta have all recently issued disappointing forward guidance.

Last month, McDonalds called out a “challenging consumer environment” while Darden Restaurants recently missed on revenues.

Oil was up 4% last week and over 18% for the year, after an Israeli strike escalated worries of a broader Iran-Israel war. This is feeding into gasoline futures which are up 80c this year — not helpful for inflation.

Global supply of public equities is getting smaller, with a net decline of $120 billion so far this year, compared with a total net decline of $40 billion in 2023.

The number of listed companies in the US has fallen from >7k in 2000 to <4k today.

US earnings season is due to start next week and expectations are set for a bullish 2024.

Consensus expects 3% year-on-year EPS growth for the aggregate S&P 500 index, a deceleration from the 8% growth posted in 4Q23 earnings season.

This quarter’s expected growth rate is the highest pre-season bar set by consensus since Q2 2022.

Notably, aggregate results have exceeded pre-season EPS growth estimates in each of the previous four quarters by an average of 4%.

Bottom-up consensus expects the S&P 500 will post 10.9% net margins in Q1, a 28bps quarter-on-quarter contraction but a 2bps year-on-year expansion.

Energy, materials, and health care are expected to post year-on-year margin contractions >100bps.

The 10 S&P 500 stocks with the largest market caps are expected to expand margins by nearly 400bps year-on-year while the remaining 490 firms in the index will see margins fall by 57bps.

Looking back at Q1 2024 performance, areas like AI, copper and obesity drugs all performed well and are expected to continue to be focus areas for the remainder of the year.

About Elise McKay and Pendal Australian share funds

Elise is an investment analyst and portfolio manager with Pendal’s Australian equities team. Elise previously worked as an investment analyst for US fund manager Cartica where she covered a variety of emerging market companies.

She has also worked in investment banking and corporate finance at JP Morgan and Ernst & Young.

Pendal Horizon Sustainable Australian Share Fund is a concentrated portfolio aligned with the transition to a more sustainable, future economy.

Pendal Focus Australian Share Fund is a high-conviction equity fund with a 16-year track record of strong performance in a range of market conditions. The Fund is rated at the highest level by Lonsec, Morningstar and Zenith.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

The RBA looks set to re-build our financial system’s plumbing. Pendal’s head of government bond strategies, TIM HEXT, explains what it could mean for investors

- The RBA has announced the “Ample Reserves” system

- It will set a price for Open Market Operations and offer unlimited quantity

- Why bonds, why now? Pendal’s income and fixed interest experts explain

- Browse Pendal’s fixed interest funds

THE plumbing of Australia’s financial system is a bit like the plumbing in your house – of little interest until something goes wrong.

For those few who do take an interest in the RBA and our financial system’s plumbing, the Assistant Governor Chris Kent gave a speech on Tuesday: “The Future of Monetary Policy Implementation”.

By the end of this year, he explained, Australia will have a new system called “Ample Reserves”.

In short, the central bank will set a price for “Open Market Operations” (repos) and offer unlimited quantity – instead of setting the quantity and letting the market determine the price, as was the previous system.

Banks have been flush (so to speak) with liquidity since early 2020, courtesy of RBA quantitative easing and the term funding facility over the pandemic.

These are now slowly rolling off, reducing excess reserves in the system.

The RBA is worried that the pre-pandemic “corridor and low reserve” system may not work so well.

That system relied on the RBA accurately forecasting government inflows and outflows into the system (think taxes and welfare payments) and offsetting them by adding or draining the cash back into the system through repos and reverse repos.

READ NEXT: Private credit has its place in portfolios. So do bonds. In her latest article, Pendal head of income strategies Amy Xie Patrick explains why, as rates normalise, investors should remember that those roles are different.

You lend them securities and they give you cash that you then pay interest on or vice versa.

The corridor meant banks could always borrow or lend unlimited funds with the RBA at 0.25% above or below target cash, but hardly ever did.

With Ample Reserves, banks can go to the RBA and offer unlimited securities to repo in return for cash (OMOs) at a pre-set margin to the official cash rate.

The price and frequency of these operations are yet to be determined but look like at least weekly and something like the target cash rate plus five basis points (currently 4.40%).

The RBA will release more details later in the year after market consultations.

Find out about

Pendal’s Income and Fixed Interest funds

So, what does this mean for investors?

The good news for leveraged portfolios is that there is now an “ample” supply of central bank liquidity at a reasonable price.

For investors, the good news is that overnight cash should eventually drift back towards target cash levels rather than sit at the ES level.

This would mean closer to 4.35% than 4.25% at current cash targets.

The bad news for investors, however, is that bank bills are less likely to drift too far above cash again.

Also, for relative value funds, government bond baskets (where bonds trade to futures) are less likely to get too cheap again.

Overall, it is a new era for the RBA.

It is not only temporarily moving out of the asbestos-ridden 65 Martin Place while expensive and long overdue renovations are undertaken, but it now has a new way of ensuring system liquidity is always rock solid.

About Tim Hext and Pendal’s Income & Fixed Interest boutique

Tim Hext is a Pendal portfolio manager and head of government bond strategies in our Income and Fixed Interest team.

Tim has extensive experience in banking, financial markets and funding including senior positions with NSW Treasury Corporation (TCorp), Westpac Treasury, Commonwealth Bank of Australia, Deutsche Bank, Bain & Co and Swiss Bank Corporation.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia.

Find out more about Pendal’s fixed interest strategies here

About Pendal

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

In 2023, Pendal became part of Perpetual Limited (ASX:PPT), bringing together two of Australia’s most respected active asset management brands to create a global leader in multi-boutique asset management with autonomous, world-class investment capabilities and a growing leadership position in ESG.

Pendal assistant portfolio manager ANNA HONG unpacks the latest monthly CPI data and highlights some of the key takeaways for investors

- The last mile will not be a smooth run

- There remains optimism that inflation will fall closer to 3% by mid-year

- Why bonds, why now? Find out more from Pendal’s income and fixed interest team

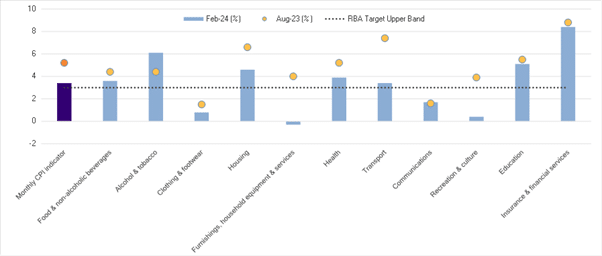

AUSTRALIAN monthly CPI of 3.4% year-on-year (YoY) came in a touch lower than market consensus.

Meanwhile, trimmed mean CPI (with the top and bottom 15% cut off) came in at 3.9%.

Though the monthly CPI shows clear signs of disinflation, it appears that the last mile will not be a smooth run.

The Reserve Bank of Australia references the quarterly CPI measure in its decision-making, and February’s numbers update the quarterly CPI basket.

We expect headline and underlying inflation, released in late April, to be around 0.8% for Q1.

It is evident that the rate hikes have taken a toll on the Australian consumer, with real consumption in negative territory.

Goods inflation is back below 2%, while services remains sticky – above 5%.

The table below highlights improvements over the past six months along with the need for further falls.

We have also had important updates in a few key service areas this month.

Housing

Rents remain elevated at 7.6% (YoY), which is not a surprise given the apartment supply challenges driven, in part, by the current immigration wave.

Adding to this is the 4.9% (YoY) increase in new dwelling prices (the cost of building) in February.

Builders have been able to pass higher labour and material costs onto homeowners.

Education

Education prices are measured only once a year (in February) and represent 4.4% of the CPI basket.

Education prices rose 5.9% (YoY) over February, with the main contributor being primary and secondary schools passing on the high wage rises for teachers announced in late 2023.

Teachers’ wages will show more moderate growth in 2024, however, so next year’s number should be lower.

Looking ahead, tertiary education inflation remains high, as lags in indexation came through this February.

Health

The news on the health front (which is 6.2% of the CPI basket) was better than education.

Health fund rises approved for April (also measured once a year in the CPI) were set at an average of 3.1%.

The RBA needs services inflation at or below 4% before it will be comfortable with inflation.

Find out about

Pendal’s Income and Fixed Interest funds

What does this mean for investors?

It was unlikely that the RBA was going to cut in the first half of 2024 – these numbers and the slowing of the disinflation impulse all back this up.

However, there remains optimism that inflation will fall closer to 3% by mid-year, which would allow rate cuts from August.

In the meantime, movements from the US Federal Reserve in between will also play a role in the last mile.

About Anna Hong and Pendal’s Income and Fixed Interest team

Anna Hong is an assistant portfolio manager with Pendal’s Income and Fixed Interest team.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia.

With the goal of building the most defensive line of funds in Australia, the team oversees some $20 billion invested across income, composite, pure alpha, global and Australian government strategies.

Find out more about Pendal’s fixed interest strategies here

About Pendal Group

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Private credit has its place in portfolios. So do bonds. As rates normalise, investors would do well to remember those roles are different, writes Pendal head of income strategies Amy Xie Patrick

- Asset classes like private credit have important roles to play in portfolios

- Why bonds, why now? Pendal’s income and fixed interest experts explain

- Browse Pendal’s fixed interest funds

INCREASINGLY I find myself a lone voice on conference panels speaking in favour of public market debt offerings such as bonds.

When I look left and right, I see experts in private credit, private equity, unlisted property and venture capital.

Depending on your investment goals, there are solid reasons for each of these to feature in a portfolio.

But I generally disagree with the use of private debt to replace the job that active bonds are supposed to do in a portfolio.

What is private debt (otherwise known as private credit or direct lending)?

Private debt is a type of credit.

Credit is a sub-asset class of fixed income where companies are borrowers and investors are lenders.

In the public debt space these loans take the shape of bonds or syndicated loans.

Both are freely-traded instruments whose values may change with every transaction. Sometimes, in the absence of any transaction, prices can change as market conditions change.

On the other hand, private debt is lending undertaken directly between companies and investors.

Borrowers are typically companies looking for more advantageous terms than they can get from a bank.

These companies may face more onerous bank lending terms due to lower credit quality, an unproven business concept or the riskiness of a project.

Investors include private debt funds, insurance companies and so on.

In Australia, private debt funds benefit from the conservative nature of our major banks. This leaves a significant slice of smaller and medium-sized enterprises “unbanked”.

It also provides a return opportunity for private debt managers who have the risk appetite and capability to assess and manage the risks.

As a result, private credit portfolios are able to generate higher levels of yield and income than portfolios of investment-grade corporate bonds.

Unprecedented growth

Five-to-ten years ago most private debt funds in Australia would have had only 20-30% exposure to the residential property market.

An unprecedented period of strong inflows into these funds followed as end investors searched for yield in a low-interest-rate world.

Today, the average private debt portfolio in Australia would have 50% or more exposure to the residential market.

This alters the risk and compositions of these portfolios compared to more diversified positions a decade ago.

Growth in these exposures has been forced rather than intended, since there haven’t been enough non-property opportunities to participate in.

In the world of equities, small and micro-cap fund managers are usually frank about the capacity of their offerings.

Good managers will cap the growth of their funds to sizes commensurate with the liquidity and the likely pool of good opportunities in their market.

Private debt funds have generally not done this in the face of strong inflows.

As a result, I expect the overall quality of portfolios will continue to get dragged by the concentration in property.

No volatility

Lack of market volatility is another attraction of private debt funds over publicly traded bonds.

This was a particularly strong draw after 2022 when most asset classes other than cash and oil were under water.

Why is there no volatility? Because there is next to no liquidity in private debt.

From time to time, private debt positions may transition between different fund managers. But these are bilaterally arranged deals unseen by the rest of the market.

Even if a manager sells a position from her portfolio to another manager at a sub-par value, it does not force every other private debt manager to take a paper loss on similar assets in their portfolios.

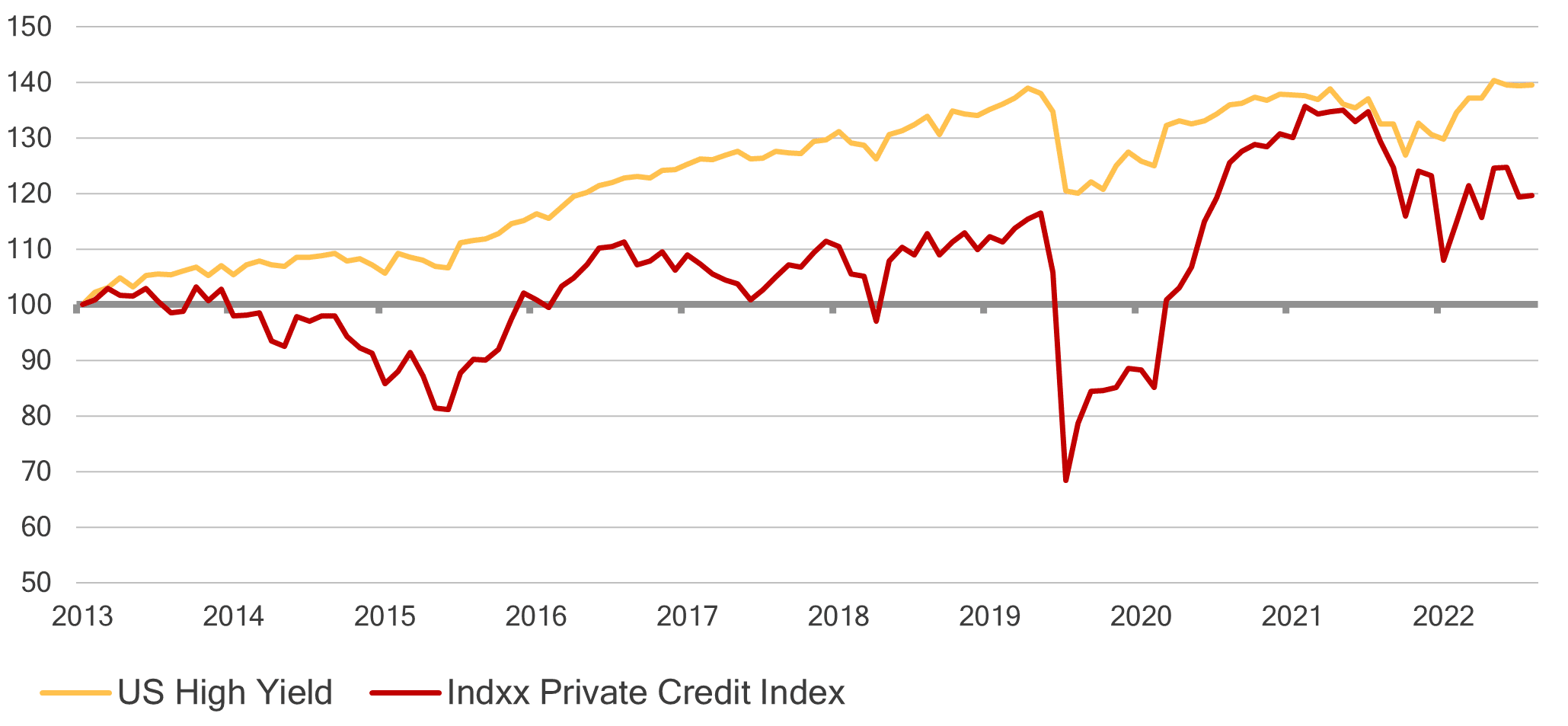

By no means does the red line in Figure 1 (see below) paint the lived experience of every private debt investor.

But it reminds us that just because something doesn’t move, that doesn’t mean it’s sellable at the price it was bought.

Figure 1: What if private debt were publicly traded? US high yield and an index of asset managers who specialise in private debt

Source: Bloomberg

Of course, no private credit index has enough history to tell us anything reliable about the true volatility of the sub-asset class.

But we can consider the red line above as a proxy.

It tracks the share prices of listed companies whose main business is in direct lending and private credit.

It’s no surprise that the undulations of the red line follow those of public high-yield markets. But the draw-downs are deeper, reflecting greater risks in private debt.

Historically, this has been true of every private version of asset classes, from debt to equity to property.

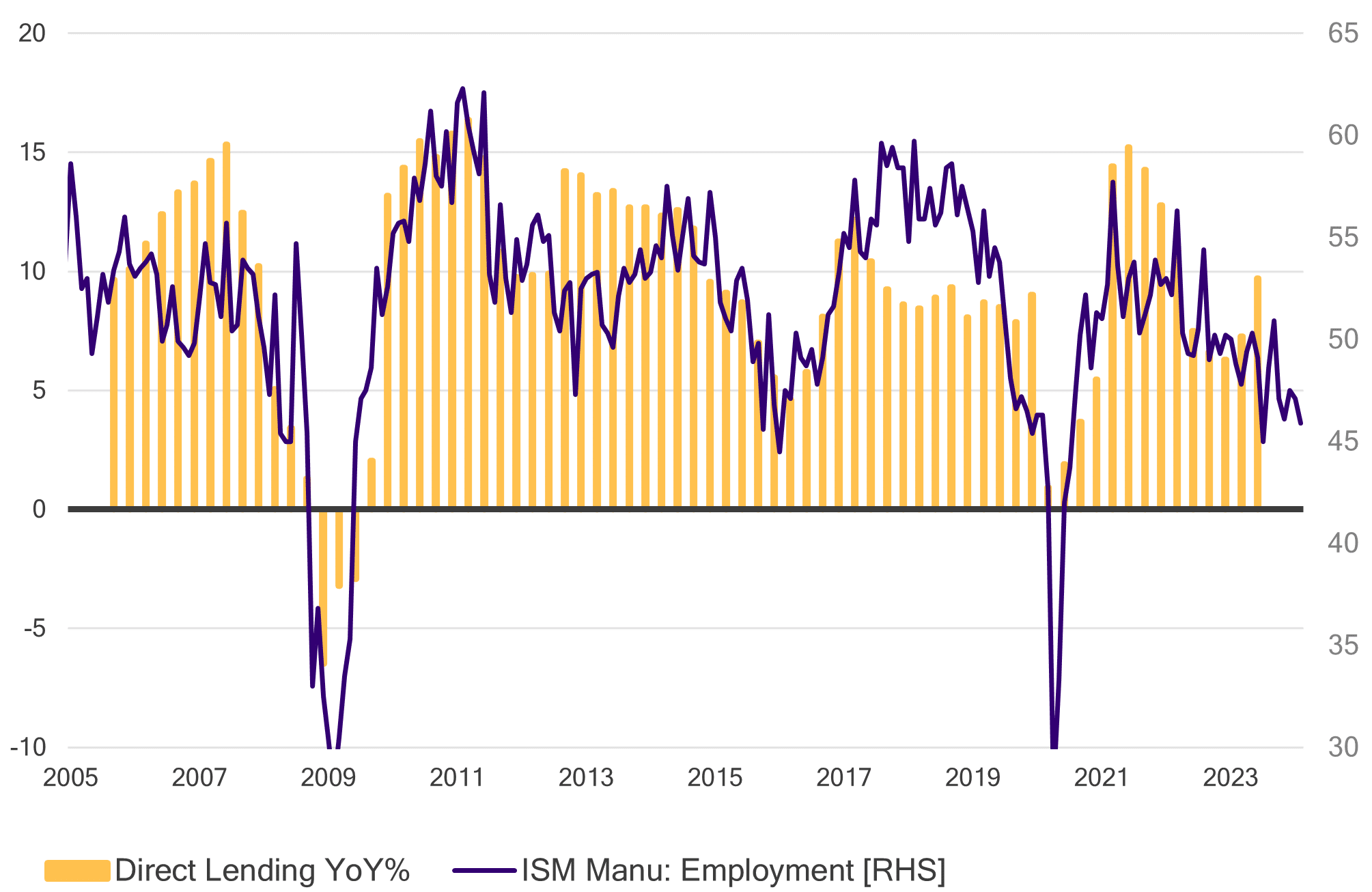

A cyclical asset class

The market volatility makes sense when you see that private debt is a cyclical asset class.

Figure 2: The cyclicality of private debt

Source: Bloomberg

This direct-lending data comes from the Cliffwater Direct Lending Total Return Index.

The index measures the unlevered and gross-of-fee performance of US direct loans by looking at the asset-weighted performance of the underlying assets of the direct-lending companies.

The ISM manufacturing employment index signals cyclical trends in the overall economy. When overlaid to the year-over-year returns of the Cliffwater index, we can see the returns to direct lending follow the cycle.

The data for the latest periods of returns from US direct lending are not yet available. But we can see from the ISM index that the trajectory of those returns are likely to be headed lower as the economic cycle softens.

Government bonds, on the other hand, have always rallied into every economic recession.

There has been a long-held relationship between the quits rate and wages.

Valuations

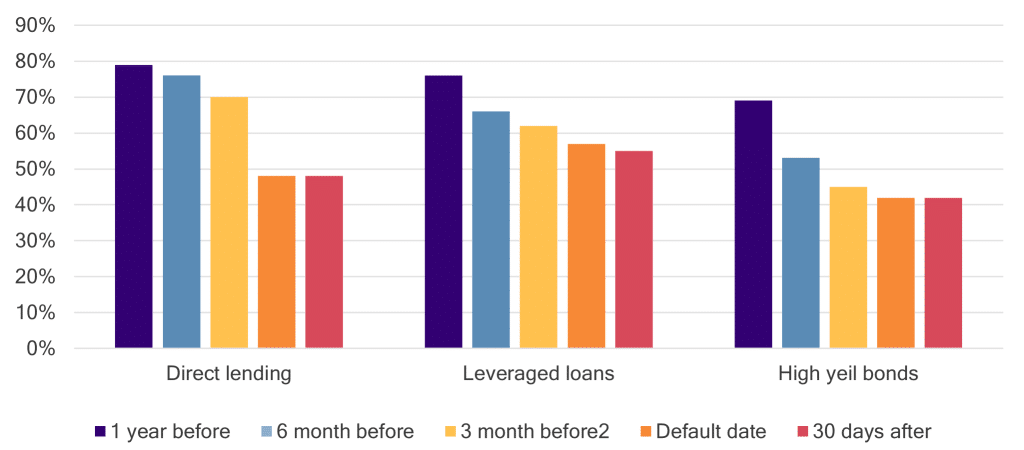

Rather than speculate about private debt valuations and methodology, I’d look to recent findings from KBRA Direct Lending Deals on the state of valuations ahead of defaults among the US community of private debt managers.

The same data is currently unavailable in Australia, but the KBRA analysis references a US$1.7 trillion industry.

The study addresses a key assertion of the private debt industry that they are in stronger lender positions than banks.

The reasoning includes closer relationships with companies, more senior positions in the capital structure and stronger protections when borrowers get into trouble.

If that were true, you should expect that recovery rates on defaulted positions in private credit portfolios should have an average value in excess of what is achieved in public bond and loan markets.

The KBRA results showed the opposite.

Private credit firms were able to recover only 48 per cent of the value of loans made to defaulted companies over the last year, compared to 55 per cent in syndicated loans.

The seniority and protected position assertions may also lead managers and valuation agents to be overly optimistic when assessing potential loss in their portfolios.

Figure 3: Mind the gap. Private vs public debt valuations ahead of defaults

Source: Bloomberg

As Figure 3 illustrates, in the three months leading up to default, direct-lending portfolios tend to mark troubled assets at a higher value than both the markets of leveraged loans and high-yield bonds.

The phenomenon may be more simply explained by the wisdom of crowds.

Given many market participants are looking at the same thing in leveraged loans and high-yield bonds, there are more opinions weighing in on what the right asset value should be at any point in time.

In private debt, it’s usually just the opinion of the manager and a third-party valuation agent.

The dangers of private debt replacing traditional fixed income

Even the most conservative private debt managers in Australia will have a higher level of credit risk through their portfolios than a bond or credit manager.

In addition, even the most liquid of private debt funds will not be able to offer daily liquidity for their clients.

I highlight these two points because I think they get to the heart of how most investors see the role of fixed income in their portfolios.

At the very least, it is a part of the portfolio that they don’t expect to worry about when their equities, property and Bitcoins are falling out of bed.

Most investors also expect to be able to tap their fixed income allocations for some liquidity once their cash has been used up.

In orderly normal market sell-offs, high-quality investment grade bonds offered for sale by one manager will usually find a home with another – even if it’s at a lower price that the former would like.

Perhaps the same can be said of private debt, though the discounts would have to be far steeper.

This highlights the need for some non-credit fixed income in the portfolio as well. This is where exposure to government bonds comes in.

Government bonds don’t have to be defensive.

The experience of 2022 reminded markets that bonds move as much with inflation as they do with growth. Since inflation was the bigger problem then, bonds could not rally as equities sold off.

If growth becomes the bigger problem, bonds should perform – just as they have in every recession in the past. This has been regardless of the starting point in yields.

Recession is the worst-feared scenario for equities, property and probably Bitcoin. It is also the worst-feared scenario for leveraged and private credit because corporate defaults skyrocket.

As KRBA’s findings have shown, the relatively benign valuations on private debt portfolios may only mask the impending shock to come in such an environment.

With most private credit funds requiring investors to provide two-to-four months’ notice on capital redemptions, that may be just the perfect amount of time for the value of their investments to go from whole to sub-par.

Conclusions

Asset classes such as private credit have important roles to play in portfolios.

They provide a way to amplify returns – and in some cases even diversify the sources of those returns.

In times of ultra-low interest rates, the space they occupy in portfolios have grown to crowd out traditional fixed income.

But now that interest rates have normalised, it is time to ask whether traditional fixed income needs to find its way back in.

If fixed income is supposed to be the true diversifier – with an ability to protect or defend in times of economic stress – private debt will not fulfil that purpose.

If fixed income is supposed to be a source of liquidity in times of market stress, a greater consideration needs to be made for government bonds.

That liquidity was available even in the depths of severe financial crises.

It proved invaluable for investors who used that flexibility to take advantage of beaten down prices in other asset classes.

Again, private credit will not serve investors well who are in need of that liquidity or flexibility in those stressed market environments.

It’s been easy to get away with replacing private debt for traditional fixed income for a decade. Let’s not wait for a deeper episode of economic stress to remind ourselves of the value of bonds.

About Amy Xie Patrick and Pendal’s Income and Fixed Interest team

Amy is Pendal’s Head of Income Strategies. She has extensive expertise and experience in emerging markets, global high yield and investment grade credit and holds an honours degree in economics from Cambridge University.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia. The team oversees some $20 billion invested across income, composite, pure alpha, global and Australian government strategies.

Find out more about Pendal’s fixed interest strategies here

About Pendal Group

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

Here are the main factors driving the ASX this week, according to Pendal investment analyst JACK GABB. Reported by portfolio specialist Chris Adams

- Find out about Pendal Focus Australian Share fund

- NEW: Watch Crispin Murray’s bi-annual Beyond The Numbers ASX outlook

THE first central bank domino fell last week.

The Swiss National Bank pushed through a surprise 25bp cut to 1.5%, pre-empting expected moves by the US Fed and European Central Bank as soon as June.

The Fed kept rates unchanged but reiterated that it expects three cuts this year.

The ECB continues to flag June as the month by which it should know whether to cut. And even Bank of England hawks have dropped their push for more hikes.

It is small wonder then that the Reserve Bank of Australia walked back commentary warning of further hikes.

In short, most central banks appear increasingly poised for a scramble to cut rates, despite plenty of macro-level data suggesting there’s no need to do anything quickly.

Against that backdrop the S&P 500 rose 2.31% (its best week since January) and hit another record high – its 20th year-to-date.

The S&P/ASX 300 also managed reasonable gains, up 1.29%.

Though neither matched Japan. The Nikkei jumped 5.6% on further signs the economy was strengthening – forcing the Bank of Japan to raise rates for the first time in 17 years.

Bonds rallied on higher rate-cut expectations, with yields on longer-dated Treasuries ending the week on lows.

It’s been a volatile month and a tough quarter for commodities, though most moved higher last week.

In particular lithium spodumene rose 18.2%, recovering from an oversold position.

Oil ended the week flat, giving up mid-week gains. Brent crude remains up 11% YTD, but lower gas prices and freight rates are acting as an inflationary offset.

Commodity Trading Adviser positioning in commodities was unchanged from the previous week with strategies continuing to hold “max long” positions in oil and gold, silver and copper.

Rate expectations

The US Fed remains odds-on to cut in June. Expectations were up 19% last week despite better-than-expected economic data released after the meeting.

We also note the Core Personal Consumption Expenditures (CPE) index – the Fed’s preferred gauge of inflation – is accelerating.

In Australia, stronger unemployment data offset the RBA’s shift to a more neutral stance, with a full cut now not priced in until November (versus September previously).

However, if the Fed and ECB cut in June, pressure will mount for the RBA to follow sooner.

US outlook

The Fed held rates unchanged for the fifth meeting in a row, as expected.

More importantly, it stuck to its view of three cuts by year-end. This was the main driver of a positive market reaction, though we recall the market started the year pricing in seven cuts.

As has previously been discussed, US inflation continues to move in the right direction despite the odd bump.

The Fed “judges that the risks to achieving its employment and inflation goals are moving into better balance”, according to Fed chair Jay Powell.

However it was a lot closer than the market reaction suggested.

Changes in the “dot plots” of each member’s expected rate levels very nearly skewed the median towards two cuts – which would likely have driven a different market reaction.

The market was also happy to shrug off a reduction in expected cuts next year from four to three, as well as a lifting in long-term rate expectations from 2.5% to 2.6%.

Other key changes to 2024 forecasts included raising expected inflation from 2.4% to 2.6%, expected GDP from 1.4% to 2.1% and cutting expected unemployment from 4.1% to 4%.

Powell also said it would be appropriate to begin tapering so-called quantitative tightening “fairly soon”.

Better GDP and employment forecasts weren’t the only indicators that the US is economy is doing well.

In data released after the Fed meeting, existing home sales rose 9.5% month-on-month to 4.38 million – the highest point over the past year and ahead of an expected 3.95 million.

The Conference Board Leading Index (a composite index that averages ten key economic variables) also rose 0.1% for the month, versus an expected 0.1% fall. It was the index’s first rise since February 2022.

As we highlighted back in November, this index has bottomed at a median of 61 days before the end of every recession since the 1969-70 downturn – and stocks have gained a median 23.4% in the year after these troughs.

The most recent trough was April 2023. Since then the S&P 500 is up 26%.

In short, the data is coming in stronger. However, as one commentator put it: “This is a Fed that wants to cut rates.”

The next Fed meeting is May, though the market is only pricing in a 16.5% chance of a cut then.

Instead, committee members are likely to wait for more CPI prints. Three more are due before the June decision, with the last one the day before their next meeting.

Pendal Focus Australian Share Fund

Now rated at the highest level by Lonsec, Morningstar and Zenith

It seems inconceivable that the Fed could cut in November given the US presidential election.

So that leaves just four meetings (June, July, September and December) to put through three cuts.

Australia

There were no surprises from the Reserve Bank’s mid-week meeting (rates were held at 4.35%), though we noted a change in language “in response to some data that makes us more confident about the path we are on”.

The RBA effectively walked back commentary warning of further hikes, by “not ruling anything in or out” rather than the previous “a further increase in interest rates cannot be ruled out”.

Semantics maybe, but there’s no doubt the previous stance was increasingly at odds with other central banks eyeing rate cuts sooner.

At this point the Fed is rated 85% chance of a cut by the end of June, the ECB above 90% and the RBA at only 40%.

There are three factors affecting the outlook for Australian interest rates:

1) Labour market challenges remain

One issue the RBA has to contend with is continued strength in the labour market.

Data after the RBA meeting revealed unemployment declined to 3.7% in February, down from 4.1% prior (4% expected). Some 116,500 jobs were added in the month versus 40,000 expected (500 prior).

While the data can be volatile, it nevertheless challenges a dovish view and sent rate cut expectations lower.

We note that is a parallel with the Fed, where Powell has previously noted that “in and of itself, strong job growth is not a reason for us to be concerned about inflation”.

This is only an issue if workers are spending and driving up inflationary pressures. Still, it is something to watch.

2) Then there’s the tax cuts

Some $20 billion in annual income tax cuts will begin kicking in from July 1.

This is clearly inflationary – some estimates say it is worth two-to-three rate cuts – and may well encourage the RBA to pause while gauging the inflationary impact.

3) Borrowers are coping

Commentary from the RBA Financials Stability Review added more weight to a hold-for-longer view.

Despite mortgage repayments rising 30-60% since May 2022, borrowers are seen as being able to cope if rates stay higher for longer.

While arrears would rise, they are expected to remain low at less than 1% in terms of home loans 90 or more days in arrears.

Japan

As expected, the Bank of Japan became the last central bank to exit the era of negative interest rates, raising the benchmark to an eye-watering 0.0-0.1% from -0.1% – the first increase in 17 years.

The move marks a step back towards mainstream central bank policy after decades of experimentation.

While negative rates no doubt helped stem the tide of deflation, ultimately it was quantitative easing, Covid and Russia’s invasion of Ukraine that drove inflation back above 2%.

As a former BOJ director in charge of monetary policy said: “the negative rate did nothing, nothing at all” to stoke inflation.

Interestingly, the start of Japan’s last three hiking cycles (going back to 1986) has preceded a global recession.

Though we note that is clearly at odds with most of the current macro data.

Markets

It was a good week for nearly all sectors in the US last week.

Tech stocks continued to do a lot of the heavy lifting – apart from Apple, which fell on an anti-trust investigation.

Artificial intelligence was again front and centre with Nvidia up for the 11th straight week after holding its GTC event (the ‘Woodstock of AI’) which packed in some 11,000 people.

Industrials also did well with bellwether FedEx reporting a third-quarter beat.

Real estate was weaker, with Equinix down on a short report.

Elsewhere Nike and Lululemon reported weaker results – the latter warning it had seen a shift in the shopping behaviour of its high-end US consumers.

Overall though it was a good week, pushing the price/earning multiple back to January 2022 levels. Materials led in Australia, offsetting weakness in utilities and consumer staples.

About Jack Gabb and Pendal Focus Australian Share Fund

Jack is an investment analyst with Pendal’s Australian equities team. He has more than 14 years of industry experience across European, Canadian and Australian markets.

Prior to joining Pendal, Jack worked at Bank of America Merrill Lynch where he co-led the firm’s research coverage of Australian mining companies.

Pendal’s Focus Australian Share Fund has an 18-year track record across varying market conditions. It features our highest conviction ideas and drives alpha from stock insight over style or thematic exposures.

The fund is led by Pendal’s head of equities, Crispin Murray. Crispin has more than 27 years of investment experience and leads one of the largest equities teams in Australia.

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

In 2023, Pendal became part of Perpetual Limited (ASX:PPT), bringing together two of Australia’s most respected active asset management brands.

Find out more about Pendal Focus Australian Share Fund

Contact a Pendal key account manager

As investors prepare for lower rates, our head of income strategies AMY XIE PATRICK sat down with portfolio specialist DALE PEREIRA to answer some common client questions

DALE PEREIRA (Pendal’s head of client solutions): As economic growth slows and inflation comes under control, markets are expecting interest rates to fall in the US and Australia this year.

How are you managing fixed income portfolios in this environment?

AMY XIE PATRICK (Pendal’s head of income strategies): “We manage our portfolios to a simple philosophy when it comes to the interest rate cycle.

“When the RBA is hiking interest rates, we like to take our credit exposures in floating-rate form.

“This means the income returns of the portfolio will be able to keep up with the rising interest rate environment.

“But when the RBA is cutting interest rates, we like to switch our exposures to fixed rate. This locks in a higher level of income, even as interest rates fall to much lower levels.

“It’s the same as a homeowner taking out a mortgage, only in reverse.

“When you think the RBA is going to cut interest rates, you want your mortgage rate to be variable so those rates fall as the RBA slashes rates.

“When you think the RBA is going to raise rates, you fix the rate on your mortgage at low levels.

“We do the same thing for Pendal Monthly Income Fund portfolio – but we want as high a yield as possible.”

Dale: Are you fixing the rate of your credit portfolio now?

Amy: “We’re not rushing to do it just yet.

“Bond yields do look really attractive compared to the last decade. But when you take a longer-term perspective, these are just more normal levels of interest rates.

“The RBA is also not entirely convinced that it’s won the inflation battle, especially with strong immigration flows still pushing up demand in our economy.

“So we’ve been dipping our toes in, but we’re not yet ready to fix the whole portfolio.

“By doing it in slices, it maintains flexibility in our portfolio as well as protection in case bonds have another sharp sell-off like they did last October.

Dale: What signals indicate it’s time to turn your income portfolio towards fixed-rate assets rather than floating-rate bonds?

Amy: “Wages matter to the RBA almost more than any other central bank.

“I’d want to see wage inflation in Australia roll over and head convincingly down to that 3.5% type of level where the RBA feels is consistent with their 2% to 3% inflation target.

“Our proprietary wage indicators at Pendal have stopped rising, but they appear a bit sticky at just over 4%.

“That doesn’t mean there won’t be opportunities along the way in rates.

“We will seize these opportunities with our active interest rate process just like we did during the regional banking crisis in the US last year and during the fourth quarter of 2023.”

Dale: Most of us think of fixed income as a defensive asset class. When equities are strong and the market isn’t worried – and isn’t looking for protection – why bother with bonds?

Amy: “My career in markets has taught me that bonds will do their own thing.

Find out about

Pendal’s Income and Fixed Interest funds

“There is no hard rule that says bonds have to go up when equities go down.

“The main things that drive bond performance are growth and inflation. The macro fundamentals are usually what matters to bond market direction.

“For example, in 2022 bonds didn’t work to protect against falling equities because inflation was a far bigger problem than slowing growth.

“Today growth is still not a problem, but inflation is coming down all over the world. The shocks from the pandemic are finally working their way out of the system.

“If the downward inflation trend continues, bonds can still do well regardless of whether the economy slows from here.

“Look at 2023, Australia grew more than 2% and yet Aussie government bonds returned more than 5%.

“The US economy grew at over 3% and global bonds returned close to 6%.

“Those data points tells us you don’t need to be bearish on the economy in order to be bullish about bonds in your portfolio. “

“While cutting cycles are great for bonds, actually the best time for bond returns is simply when the hiking cycle stops.

“Bonds tend to outperform equities in this part of the cycle.

“That means you’re coming into the best period for bond returns right now. And wouldn’t it be a shame to say no to bonds and miss out on all this opportunity?”

Dale: Why would you invest in a bond portfolio rather than a term deposit?

Amy: “For some investors, term-deposit returns on cash are enough – they’re more than happy to take those returns after years of really slim pickings in this area.

“But for most investors who chose term deposits over fixed income last year, their biggest frustration was missing out on the upside.

“Both bonds and equities outperformed term deposits in 2023.

“This year, locking in 5% term deposits might sound nice at first.

But you would also be locking up your capital for a year.

“It makes it harder to move your money around when things change, which means you can’t deploy it quickly or easily to buy the dip if we get a decent correction in markets.”

About Amy Xie Patrick and Pendal’s Income and Fixed Interest team

Amy is Pendal’s Head of Income Strategies. She has extensive expertise and experience in emerging markets, global high yield and investment grade credit and holds an honours degree in economics from Cambridge University.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia. The team oversees some $20 billion invested across income, composite, pure alpha, global and Australian government strategies.

Find out more about Pendal’s fixed interest strategies here

About Pendal Group

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

Find out about

Pendal’s Income and Fixed Interest funds

Here are the main factors driving the ASX this week, according to Pendal’s head of equities CRISPIN MURRAY. Reported by investment specialist Chris Adams

- Momentum remains strong across most equity markets

- A period of consolidation is still likely, however

- Find out about Pendal Focus Australian Share fund

- Watch Crispin’s Beyond the Numbers webinar – now on-demand

INFLATION concerns prompted consolidation in most equity markets last week, following unconvincing US CPI and PPI data.

This inflation data means that the market is now expecting fewer rate cuts this year.

The S&P 500 finished down 0.09%, while bond yields continued to rise. US 10-year yields are now 53 basis points higher than their lows in December.

Generally, higher commodity prices added to the angst as they may act as a further headwind for the “last mile” reduction in inflation to 2%.

This early sign of potential market consolidation following a strong run was concentrated in previously high-momentum sectors.

In Australia, this saw banks underperform (-4.4% for the week), though they still have a total return of 9.06% for the calendar year-to-date.

Resources continued to underperform (-2.93% for the week) as iron ore fell further (-5.2%).

That said, there were signs of a sentiment shift in oil (+4.1%) and copper (+3.9%).

With both banks and resources down, the S&P/ASX 300 lagged global markets, falling -2.14%.

Inflation watch

US February Headline CPI rose 0.44% month-on-month to 3.2% year-on-year.

It is running at 3.4% on a six-month and 3.4% on a three-month annualised basis, respectively.

Meanwhile, the Core CPI measure was up 0.36% month-on-month and 3.8% year-on-year.

It is running at 4.3% on a six-month and 3.4% on a three-month annualised basis, respectively.

While the Headline index was broadly in line with expectations, Core was hotter than the expected 0.32% month-on-month.

The three-month annualised rates are picking up, increasing the risk that inflation proves stickier than expected.

Breaking down the Headline year-on-year increase:

- Core goods (-0.3%) are back towards the previous four-year mean levels of 0.1% year-on-year growth, as is Food & Beverages which grew 2.3% year-on-year and at a mean of 2.4% over four years.

- Energy (-1.7% year-on-year) is well below the four-year mean of 5.2%.

- Core Services (5.2% year-on-year) remains elevated, given a 2.9% four-year mean.

Within the Core basket, services are still not showing any sign of breaking lower.

At the same time, the deflation in goods is coming to an end and may no longer provide a tailwind for a lower CPI.

Other measures of “sticky” inflation, such as the Atlanta Fed Sticky Core CPI and Cleveland Fed Median CPI, confirm the risk that inflation remains stuck in the range of 3.0%-3.5%.

February’s PPI data was also stronger than expected, rising 0.6% month-on-month – versus consensus expectations of 0.3% – to 1.6% year-on-year.

This was driven by sharp jumps in both food and energy prices.

Core PPI was up 0.3% month-on-month (with a consensus of 0.2%) to 2.0% year-on-year, due to both services and goods.

The combination of this data allows the market to predict the February Core Personal Consumption Expenditures (PCE) inflation data, which the Fed uses as its preferred inflation measures.

This is implied to come in around 0.3% month-on-month, with an upward revision to January leading to a 2.8% year-on-year gain.

The three and six-month annualised rates are expected to be higher, shifting expectations around the first rate cuts as a result.

Other leading inflation indicators are mixed.

There is a lot of focus on rising US gasoline prices, which reflects both oil prices creeping higher and increased refinery crack spreads.

There is some offset from freight rates declining, though they remain at historically elevated levels.

Interest rates

Given recent inflation data, the market is now only pricing in a 2% chance of a rate cut at the FOMC meeting this week, while May is priced at 6% and 60% for June.

Median expectations have now shifted to only two-and-a-half cuts in 2024.

The market will be looking at whether the Fed shift its median dot plot expectations from three to two rate cuts.

Chair Powell’s tone will also be scrutinised, though the general view is that he will not want to be too hawkish given:

- there is still three months’ worth of inflation data to come through before the June meeting

- there are some signs that consumer demand is cooling

- he will be as wary of extrapolating two months of hotter data as he was when extrapolating the cooler data late last year

- the perception that the Fed will not want to wait until July or September for the first cut as it becomes politicised by the Presidential election.

Economic growth outlook

US February Headline retail sales grew 0.6% month-on-month – a smaller-than-expected bounce back from a weak January figure.

The discretionary component of Core retail sales is negative year-on-year, though other categories are holding the overall number in the 2-3% range.

Clothing and furniture sales are particularly weak.

This softness has flowed through into the Atlanta Fed GDPNow tracker, which has declined due almost entirely to lower expectations on personal consumption.

All this highlights that the economy is slowing down gradually which, combined with potentially lower Q2 inflation, should still be enough to allow the Fed to cut in June.

Japan

The Bank of Japan is under scrutiny, with last week’s wage data seen as the catalyst for a rate hike.

To put this significance into perspective, the last time the BOJ hiked was in 2007 – an era before iPhones, Bitcoin, Uber or Instagram.

The market is implying an 80% chance of the BOJ ending yield curve control and negative rates.

The bigger issue for global markets is how the balance sheet will be managed going forward – whether there will be some form of quantitative easing – and the likely extent of rate hikes in the next 12-18 months.

Australia

The monthly NAB Business Survey suggests business confidence remains subdued, however, current conditions are marginally better than January – notably in the trading and profitability category.

Forward orders were slightly lower than in January, but the pricing outlook improved which should support margins.

Australian bond yields followed the US higher.

This, combined with the Fair Work Commission wage settlement for aged care workers which impacts overall wages growth, could delay the first cut from the RBA.

Markets

Momentum remains strong across most equity markets.

A period of consolidation is likely, with the potential for a 5% drawdown in the US market.

But underlying technicals – such as the increasing breadth of the uptrend – remain positive.

Copper is another market to watch – it has risen to its highest levels in twelve months despite all the pessimism on China.

The ASX has been a narrower market, with increased liquidity in the largest stocks a feature.

Looking over the year to date, it is interesting to see how concentrated the rally has been in the large cap industrials.

The returns from the Big Four banks, Macquarie Group (MQG), Goodman Group (GMG) and Wesfarmers (WES) – which are 26% of the index – can explain over 100% of the index return in 2024.

On both price-to-earnings and price to pre-provision-profit, the banking sector is at all-time high valuation (going back as far as 1996).

About Crispin Murray and the Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia. Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions.

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

Here are the main factors driving the ASX this week, according to portfolio manager OLIVER RENTON. Reported by portfolio specialist Chris Adams

- Find out about Pendal Focus Australian Share Fund

- Tune into our latest on-demand webinar: Beyond the Numbers

IT was a light week in terms of macro data.

We saw February non-farm payrolls and the Job Openings and Labor Turnover Survey (JOLTS) released which, overall, were supportive of inflationary pressure continuing to ease.

The Fed’s Chair Powell’s comments to Congress were taken positively.

Australian economic data painted a picture of an economy which is slowing, but still growing – albeit with some softer pockets.

There were few surprises from the opening days of China’s National People’s Congress sessions.

Beijing confirmed a target of 5% GDP growth for 2024.

The S&P 500 fell 0.23%, while the S&P/ASX 300 gained 1.85% due to a strong Friday.

US economy and inflation

There were a number of data prints which supported the view of a slowing economy and easing inflation.

While non-farm payrolls rose 275,000 in February – well ahead of consensus expectations – there were large downward revisions to December and January’s data.

As a result, net new jobs grew 108,000.

Average hourly earnings rose 0.1% versus consensus expectations of 0.2%, while the unemployment rate rose from 3.7% to 3.9%.

The “Quits” rate in the JOLTS data continued to fall.

This is important because there is a close correlation between it and the Employment Cost Index measure of private sector wages and salaries, with a lagged effect.

This suggests that the latter could fall below 4% in coming months.

The February ISM services index dropped from 53.4 to 52.6, below the 53.0 expected by consensus.

Demand-based components showed some strength – with New Orders rising 1.1 points to 56.1.

Employment and inflation components, however, fell.

It was also interesting to note that the Congressional Budget Office increased its estimate of population growth in the US in 2023 from 0.5% to 1.1%.

It also raised the 2024 estimation from 0.5% to 1.2%, noting the impact of undocumented migrants.

Fedspeak

Atlanta Fed President and FOMC voting member Raphael Bostic said that he expects the Fed’s first rate cut, which he pencilled in for the third quarter, to be followed by a pause.

In separate commentary, he expressed concern that businesses are too exuberant and could unleash a burst of new demand after easing boosts price pressures.

Meanwhile, in his testimony to Congress Fed Chair Powell noted that easing will probably be appropriate “at some point this year” and that the number of cuts depend on the data.

The market took Powell’s comments positively, with US Treasury yields falling and gold rising.

US election

Donald Trump had wins in both the courtroom and on the campaign trail last week.

The US Supreme Court said Trump can appear on presidential ballots this year.

The unanimous decision overturned a Colorado Supreme Court ruling barring Trump from running again due to his efforts to overturn his 2020 election loss.

Republican candidate Nikki Haley dropped out of the presidential contest after losing all but one of the Super Tuesday primaries – though she has not endorsed Trump’s candidacy.

Senate Minority leader Mitch McConnell subsequently endorsed Trump, which he’s previously been reluctant to do.

Australia

Australia’s GDP increased 0.24% in Q4 2023, which was largely in line with expectations.

The economy grew 1.55% year-on-year.

Consumer spending was positive but subdued, rising 0.1% for the quarter.

As a component, spending on discretionary items fell 0.9% quarter-on-quarter.

Housing construction activity fell, but this was offset by non-housing construction.

Importantly, labour productivity is improving following last year’s plunge, with the six-month annualised growth in productivity rising back towards 3%.

The current account surplus rose to $11.8 billion, which was well ahead of the $5-6 billion expected by the market due to a larger-than-expected rebound in net exports.

Europe

The ECB has reached its 2% inflation target, according to a Bloomberg Economics Nowcast.

The gauge, which uses 32 variables from unemployment to energy costs, fell to 1.95% after January’s drop in producer-prices was added.

Find out about

Pendal Focus

Australian Share Fund

Crispin Murray,

Head of Equities

China

The first week of the National People’s Congress session did not yield much in the way of surprises.

The 2024 GDP growth target has been set at “around 5%”, which was largely as expected.

There has been rhetoric around AI, automation, technology, renewables, new energy vehicles (NEVs) and biotech as drivers of economic growth.

A special sovereign bond issuance plan, estimated to be around RMB 1 trillion for 2024, is designed to help mitigate the risk of local governments struggling to pay debt.

Markets

The small 0.23% fall in the S&P 500 meant that it only equalled its best run on record of rising in sixteen of the last eighteen weeks – last seen in 1971.

We note that on a historical basis, a strong start to the year typically has some persistence.

Going back to 1950, when the S&P 500 has risen in January and February, it has gone on to record gains over the remaining ten months of the year 92.9% of the time, with an average return of 8.1%.

That said, we also observe that this is starting to look like a relatively long run without a 2% retracement on a historical basis.

The put/call ratio is at the bottom end of its range, suggesting that sentiment remains very bullish.

In other news, as expected, OPEC+ agreed to extend the current curbs on oil supply through to June in order to support prices.

However, the gas price remains weak due to the combination of a mild European winter, high levels of gas in storage, and emerging concerns about increased supply from Qatar.

We also saw index changes on the ASX.

QBE Insurance (QBE) replaced Newmont (NEM) in the S&P/ASX 20, while Flight Centre (FLT) and Pro Medicus (PME) moved into the S&P/ASX 100, and Alumina (AWC) and Region Group (RGN) fell out.

About Crispin Murray and Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia. Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Find out more about Pendal Focus Australian Share Fund here.

Contact a Pendal key account manager here.

Drawing on more than 25 years of experience investing in top-performing Australian companies and a background in accounting, Jim manages our Long/Short Fund and co-manages our Imputation Fund. He is a Chartered Accountant with membership of the Australian Institute of Chartered Accountants.

Pendal Focus Australian Share Fund is managed by Crispin Murray. The fund has beaten its benchmark in 14 years of its 18-year history (after fees), across a range of market conditions. Find out more about Pendal Focus Australian Share Fund here.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

While the US-based ‘Magnificent Seven’ takes the spotlight, several ASX-listed companies are leveraging of AI technology, reports Pendal analyst ELISE McKAY

- Xero is close to testing an AI-based business companion

- NEXTDC is building local AI infrastructure

- Find out about Pendal Focus Australian Share fund

ON A TOUR of the US late last year, Pendal Aussie equities analyst Elise McKay met with dozens of companies – and found generative AI was a topic in almost every meeting.

“There’s strong evidence that over the longer term generative AI will have a big impact across the business landscape,” McKay said at the time.

Aussie equities investors should keep an eye on how companies are investing in AI, as well as which infrastructure suppliers are best placed to benefit in a fast-evolving market.

Below is an update from McKay, outlining how her expectations are playing out after the recent ASX results season.

Here she focuses on ASX-listed data centres player NEXTDC and software maker Xero – both held by Pendal.

XERO (ASX: XRO)

Generative AI – a machine-learning model that is trained to create new data, content and insights – is being embraced globally as corporates leverage “large language models” and infrastructure available off the shelf.

Xero – a cloud-based finance and accounting software maker – is a good example.

At its inaugural investor day, Xero announced a generative AI tool called JAX (short for Just Ask Xero).

The tool is designed to help customers with personalised insights and tasks such as raising and sending invoices to customers.

Xero plans to test the tool with customers later this year.

Xero first started working on its generative AI strategy about eight months ago and made a key hire in Eitan Sharon as its data and science lead in November.

Within months of Eitan joining, Xero had a functional tool in place, demonstrating the speed with which these products can be built and deployed.

NEXTDC (ASX: NXT)

With rapid growth in demand for generative AI tools comes demand for infrastructure to run and support training and inference models.

Training refers to the process of building AI models, while inference refers to how those models are deployed in an application or business setting.

Focus is expected to shift from AI training to inference over time – which may advantage some players and disadvantage others.

Australian data centre operator NEXTDC (ASX: NXT) hopes to play a significant role in both markets.

NXT is expected to launch its first Nvidia-based “AI factory” in coming months.

It’s our expecation the AI factory will use graphics processing units made by Nvidia – the $US 2 trillion-dollar NASDAQ-listed chipmaker that has become the face of the artificial intelligence hardware manufacturing race.

This would be complementary to existing NXT data centre infrastructure which is ideally positioned to hosts inference model technology – which requires proximity to clients to limit latency.

NXT has recently signed contracts with hyper-scale players in Sydney and Melbourne to support their cloud deployments.

AI deployments would be over and above these contracts, and — if following the US trend — at a size significantly larger than what has recently been signed.

There are now also contracts being tendered in market for sizeable AI deployments for both training and inference needs. These are reportedly significantly larger in size again than recent contracts.

Demand for onshore AI infrastructure

NXT’s customers are expected to differentiate their needs depending on whether they are contracting for training or inference work.

But in both cases, Australian clients prefer onshore AI infrastructure technology due to data sovereignty issues and the need for low latency.

Training models can be located close to wherever access to power is available and priced cheaply, while inference models need to be in metro locations.

Find out about

Pendal Horizon Sustainable Australian Share Fund

This is well-suited to NXT’s footprint which is spread geographically across six states and territories of Australia and closely located to CBDs.

NXT is well positioned to win its fair share with available inventory in all markets and great relationships across the customer base.

Access to power

Access to power is one of the big issues that continues to face the AI industry

Data centres, crypto currencies and AI consumed 2% of global energy demand in 2022, the International Energy Agency estimates.

The IEA forecasts global demand for energy from these sources to grow at 8% to 23% from 2022 to 2026.

In the US, data centres accounted for about 4% of energy demand in 2022. They are expected to account for half of US electricity demand growth over the next three years.

Clearly the AI industry needs resolve this issue to meet demand.

The issue will be attacked from multiple angles including increased compute efficiency (eg Huang’s law), new cooling technologies (eg direct-to-chip cooling, liquid immersion) and innovative power solutions (eg small modular reactors).

About Elise McKay and Pendal Australian share funds

Elise is an investment analyst and portfolio manager with Pendal’s Australian equities team. Elise previously worked as an investment analyst for US fund manager Cartica where she covered a variety of emerging market companies.

She has also worked in investment banking and corporate finance at JP Morgan and Ernst & Young.

Pendal Horizon Sustainable Australian Share Fund is a concentrated portfolio aligned with the transition to a more sustainable, future economy.

Pendal Focus Australian Share Fund is a high-conviction equity fund with a 16-year track record of strong performance in a range of market conditions. The Fund is rated at the highest level by Lonsec, Morningstar and Zenith.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

The December-quarter GDP numbers just stopped short of the “no-growth” scenario we were slowly sliding towards last year. Pendal’s head of government bond strategies TIM HEXT explains what it means for markets

- Weakness largely derived from consumer spending

- On a nominal basis, the picture looks better

- Why bonds, why now? Pendal’s income and fixed interest experts explain

- Browse Pendal’s fixed interest funds

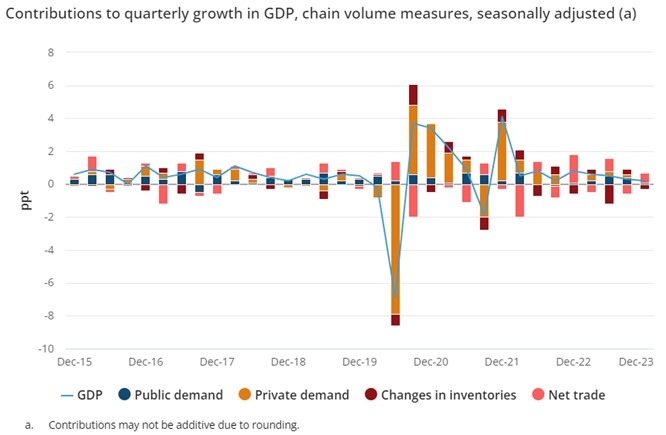

THE December-quarter GDP numbers just stopped short of the “no-growth” scenario we were slowly sliding towards last year.

Q4 GDP came in on forecast at just 0.2%, as you can see in the ABS graph below.

After 2.3% growth in 2022, 2023 finishes with GDP at 1.6%.

Source: ABS, 2024

In per capita terms, we went backwards for the third quarter in a row (-0.3% for the quarter) and are down 2.4% over 2023.

The weakness is largely from consumer spending, which is going almost nowhere – this was up 0.1% for the quarter and 0.1% for the year.

Remember, this was a year where almost 600,000 people entered the country so, on average, we are all spending less than in 2022.

Interestingly, we are earning more, but it is all being swallowed up by inflation, interest rates and tax creep.

In fact, compensation of employees was up 8.1% in 2023, but taxes paid 11.5%. The Stage 3 tax cuts (beginning July) will only partly remedy this.

READ NEXT: What are the main factors impacting income strategies right now? In a new article, Pendal’s head of income strategies AMY XIE PATRICK explains how her view has evolved in recent months. Read the article here

If you feel like money is going out just as fast as it comes in, you have good reason.

The GDP you hear reported is a volume measure (called chain volume) of output for the economy.

Most of us think in nominal terms.

On a nominal basis things look better – with GDP at 1.4% for Q4 and 4.4% for 2023.

Higher prices and improving terms of trade has helped cushion the blow in the real economy.

Government and business investment propping up the economy

So, if consumer spending – which makes up 50% of the economy – is flatlining, then where is the modest growth coming from?

Government spending and investment continues to be strong.

Government spending was up 0.6% for the quarter and 2.7% for the year, while government investment was slightly down for the quarter but up a massive 13.6% in 2023.

Private investment was up as well, but modest overall.

Data centres and warehouses are driving solid growth.

Concerningly though, dwelling investment was down 3.8% for the quarter and down 3.1% on the year.

Hopes of a building boom to help the housing shortage fly in the face of higher interest rates.

Rents go up, so inflation goes up, so interest rates go up, so housing investment falls – if you follow the logic of rate hikes to tackle rental inflation, you are smarter than me.

Hours worked still falling

The GDP numbers also include data on hours worked.

Find out about

Pendal’s Income and Fixed Interest funds

This fell for the second quarter in a row and is now down 1% from mid-year.

The RBA will take some comfort that firms are responding to slower conditions by reducing hours of existing employees and not hiring new ones, rather through layoffs – at least for now.

So, what does this mean for markets?

First of all, the rate hikes have worked.

While the fixed rate cliff has been more of a speed bump, the RBA will be pleased that higher rates are reducing demand in the economy.

Lower immigration in the year ahead will also help.

At the same time, the supply side of the economy is another year away from the pandemic and has now largely normalised.

This will give the RBA further comfort that its path back to inflation below 3% is realistic and achievable.

This, in turn, opens the door to rate cuts later in the year.

We still think three cuts – in September, November and December – are realistic.

By then, the US Federal Reserve should be well into rate cuts, and inflation – while sticky around 3% – would be considered under control.

In turn, GDP would be allowed to push back up towards 2% or above without threatening the inflation outlook – and this would be a good outcome for all and meet the objectives of the RBA.

About Tim Hext and Pendal’s Income & Fixed Interest boutique

Tim Hext is a Pendal portfolio manager and head of government bond strategies in our Income and Fixed Interest team.

Tim has extensive experience in banking, financial markets and funding including senior positions with NSW Treasury Corporation (TCorp), Westpac Treasury, Commonwealth Bank of Australia, Deutsche Bank, Bain & Co and Swiss Bank Corporation.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia.

Find out more about Pendal’s fixed interest strategies here

About Pendal

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

In 2023, Pendal became part of Perpetual Limited (ASX:PPT), bringing together two of Australia’s most respected active asset management brands to create a global leader in multi-boutique asset management with autonomous, world-class investment capabilities and a growing leadership position in ESG.