What are the main factors now affecting fixed income investors? Pendal’s head of income strategies AMY XIE PATRICK explains how her view has evolved in recent months

- There could be heightened volatility and bouts of “everything sell-offs”

- A hard landing isn’t off the table, but it’s too soon to position for it yet

- Why bonds, why now? Pendal’s income and fixed interest experts explain

- Browse Pendal’s fixed interest funds

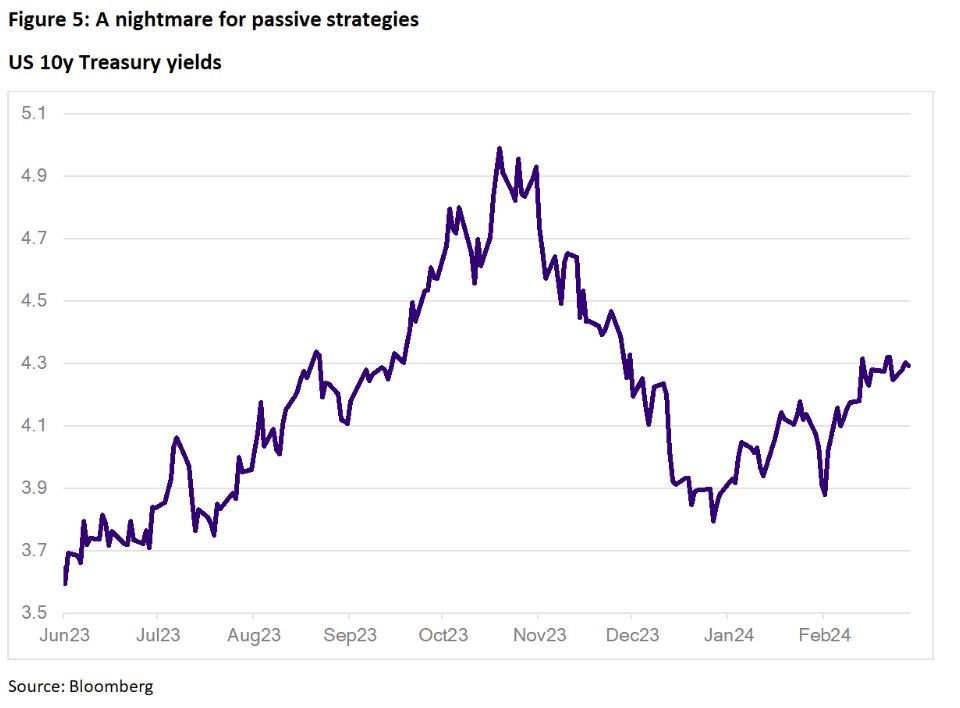

Will US 10-year yields end the year closer to 3% or 5%?

Three months ago, I would have put a 70% probability on 3%.

Today, I’m a fence-sitter – though there are arguments for both sides of the fence.

The main thing that’s changed is…well…nothing. The consumer is still incredibly resilient. It’s not clear where that resilience is coming from, but here’s a theory.

Excess savings buffers have been wearing down since the pandemic, but one thing after another has offset the economic effect.

In 2023, an increasing budget deficit found its way into the pockets of US consumers. In Australia, an influx of immigration kept aggregate consumption at a healthy level, even if individually we were feeling more mixed.

The latest saving grace has been disinflation.

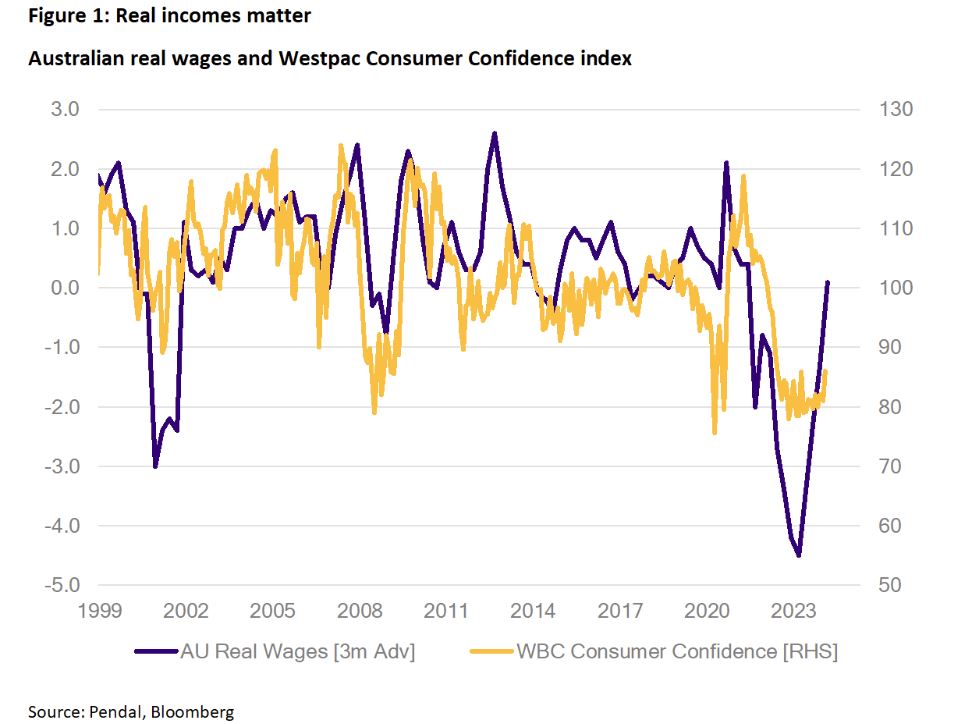

Prices move faster than wages on the way up and on the way down. Put another way, real incomes are eroded in periods of high inflation, and boosted when inflation falls.

This has a direct impact on consumer sentiment, which feeds into consumption.

In Australia there is a strong relationship between real incomes and sentiment. Real wages seem to lead sentiment by about three months.

Even as savings buffers wane, a fall in inflation has boosted real consumer spending power.

Disinflation is no longer enough

Ironically, falling inflation has been my main reason for liking bonds over the past six months.

Big moves lower in bond yields in the fourth quarter of 2023 seemed like vindication for those views.

But as Pendal’s income and fixed interest team watched the data roll in over December and January, we realised disinflation alone would not be enough to justify a large gap between the market’s pricing and the Fed’s dots.

By the end of 2023, interest rate markets had priced in more than seven rate cuts from the Fed in 2024. Though the median of the Fed’s projections saw only three cuts.

Implicit in my previous view was an assumption that falling inflation would be accompanied by a slowing economy.

As labour markets loosened, consumption would also slow to reflect greater uncertainty on jobs.

If such a macro picture was to play out in the data (and it still might), the Fed and other central banks would be able to lower rates more concertedly.

They wouldn’t need to worry about a rebound in inflation because the gravitational forces of slowing demand would be there to help.

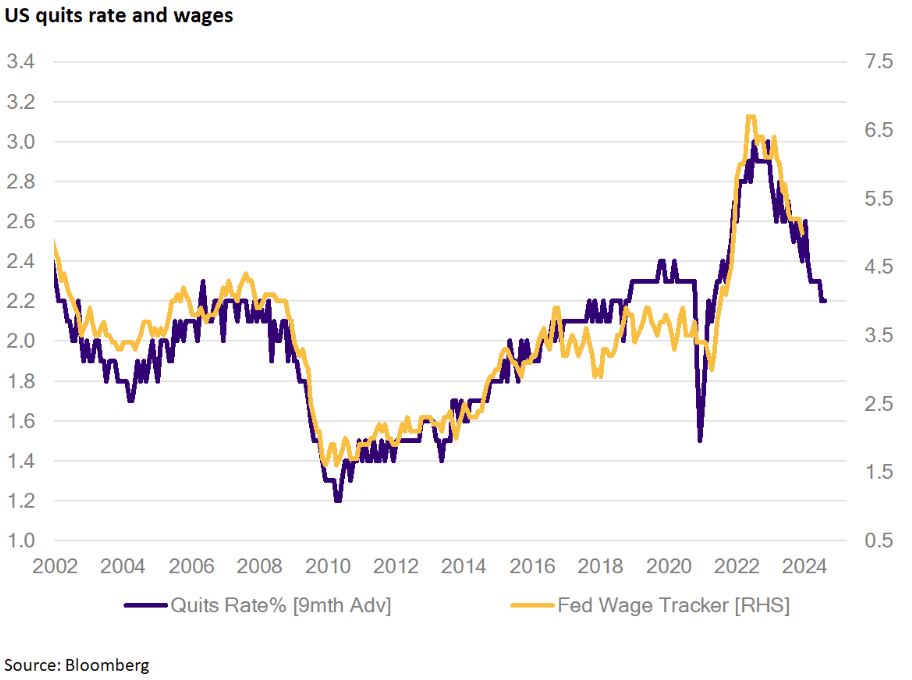

As Figure 2 shows, the disinflation thesis is still intact.

There has been a long-held relationship between the quits rate and wages.

The reasoning is fairly intuitive: we feel less bold about quitting when the prospects of other jobs decline. Empirically, the quits rate seems to lead wage growth by around three quarters.

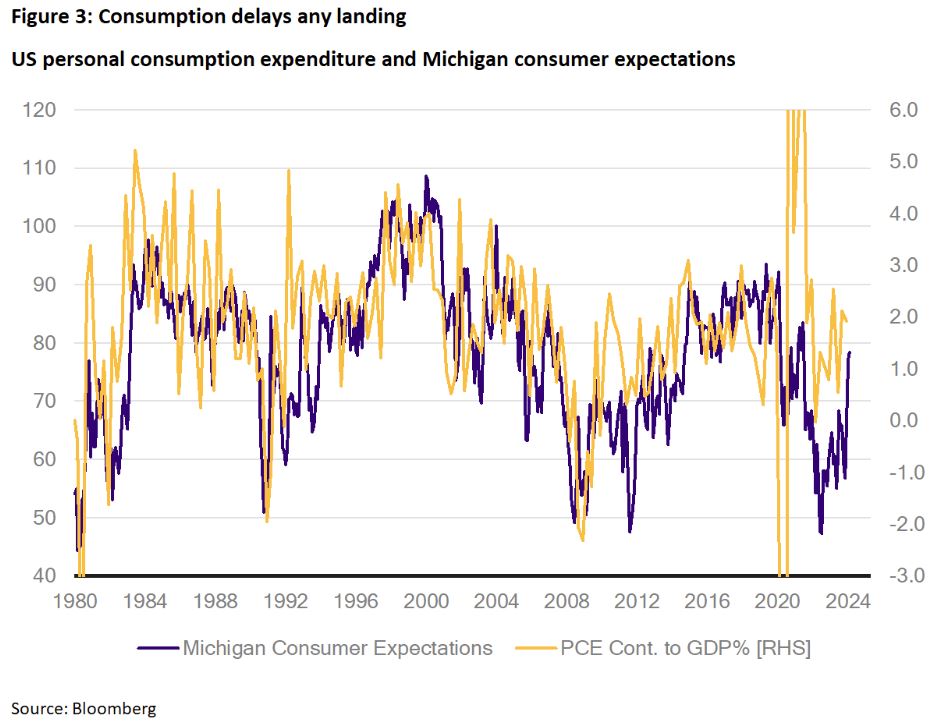

The data for US consumption tells a different story, which throws a spanner in the works for bond enthusiasts.

Personal consumption expenditure (or PCE) turned a corner in 2023 and remains robust.

Consumer sentiment is rebounding more sharply because real incomes are rising.

Since consumption counts for about 70% of US GDP, it’s hard to build a case that the economy is faltering just yet.

What if there is no landing?

Consumption is now so resilient it’s got the market questioning whether there will be any landing, let alone a hard landing.

In the US, it’s not just consumption.

Manufacturing seems to be stabilising, housing has turned a corner, and the fiscal drag is barely noticeable. Could the next move from the Fed be a hike?

I’m not yet ready to get quite so carried away, but I concede that it’s simply too early to start positioning uber-defensively in portfolios.

Regardless of whether I agree with the no-landing narrative, good portfolio management requires me to entertain that scenario and consider the ramifications for investment decisions.

A no-landing scenario would imply we’ve already moved past any mid-cycle slowdown.

It would support equity analyst earnings growth estimates of around 7.5% this year for the S&P 500 index.

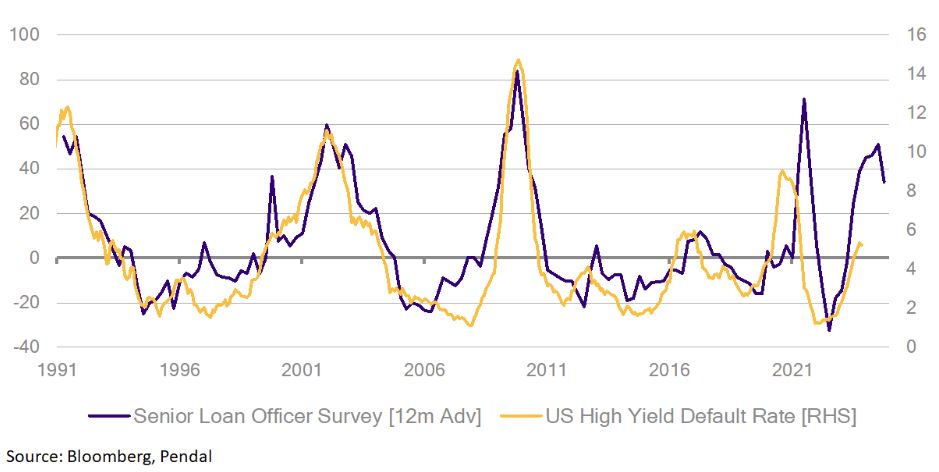

It would give comfort to the idea that high-yield credit spreads can stay lower than what should be implied by recent rising default rates because the worst is already over.

It would also challenge the market and the Fed’s current thinking on rate cuts for this year.

In fact, some argue that if the US economy is still managing to grow above trend with a 5.5% Fed Funds rate, then monetary policy isn’t all that restrictive.

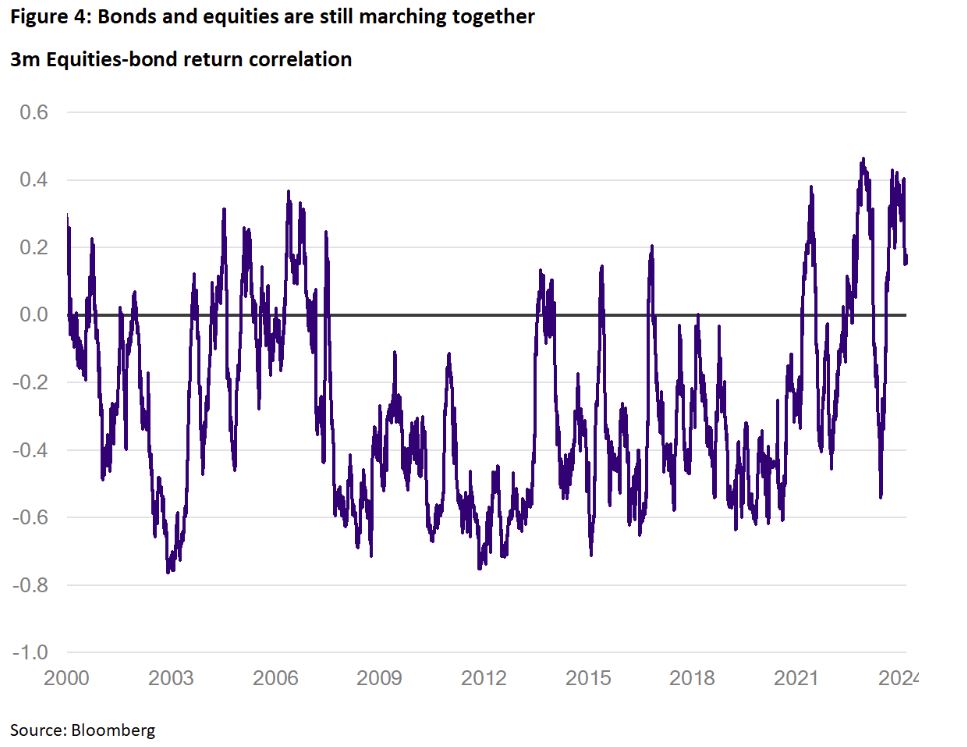

Taken to its conclusion, this train of thought poses risks to bonds.

Since bond and equity returns have been positively correlated since late-2022 – excluding the Silicon Valley Bank blip last year – the idea of no-landing also poses a threat to risky assets.

Volatility is an opportunity

As I entertain the possibility of a no-landing scenario, at least for 2024, I am drawn to a few investment implications.

The first is that I need to be truly active on duration this year.

Set-and-forget on bonds won’t work. Our income strategies carried over five years of duration at the end of 2023, which is more than the AusBond Composite Index (Australia’s most popular fixed income benchmark).

Roughly speaking, that translates to a 5% performance move for the portfolio for every 1% move in yields.

Today, these portfolios carry less than one-tenth of that exposure (so nearly no duration at all).

Not only did this help our funds benefit from the strong moves lower in global bond yields at the end of 2023, but also helped us to avoid the decent back-up in yields since the start of 2024.

The second is that I should expect flashbacks to 2022, where almost everything sold off together.

The main driver will come from bonds and knock-on to other asset classes.

Since our income funds can only be long or square in risky assets, maintaining a liquid portfolio so that we can de-risk out of the riskiest pieces quickly will count for a lot in that environment.

The third is that it’s too soon to get uber-defensive.

Investment grade credit is still a good place to stay in risk while avoiding over-extension.

Bringing this allocation down too much and too soon may mean leaving good quality returns on the table.

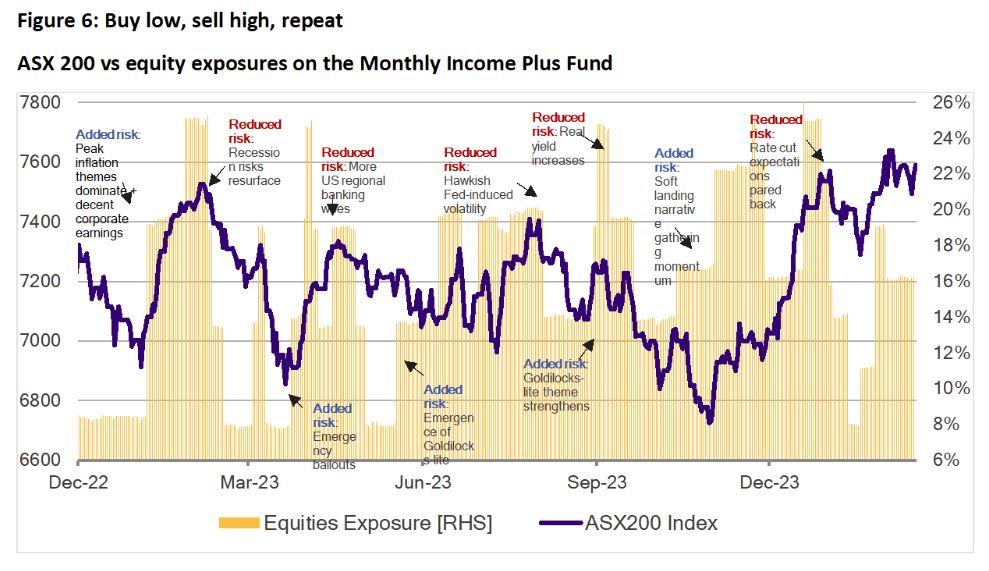

On top of that, I need to remain open to buying opportunities in riskier assets such as equities.

After all, the ASX 200 was largely directionless and volatile until the back end of 2023, yet our Monthly Income Plus portfolio was able to seize on the opportunities afforded by the volatility.

Hard landing is not off the table

While I am not ready to buy-in to the no-landing camp, I acknowledge data now supports that narrative.

Having a plan for how to navigate a no-landing market environment is key. Having the flexibility to enact that plan is vital. Portfolio liquidity will be very important this year.

It is worth stressing that a hard landing isn’t off the table.

Just as my subjective odds for a no-landing scenario in 2024 has increased, the odds I assign to a hard landing has diminished.

It is probably just as likely to happen in the first half of 2025 as in the second half of 2024.

How we get there will be one of two ways.

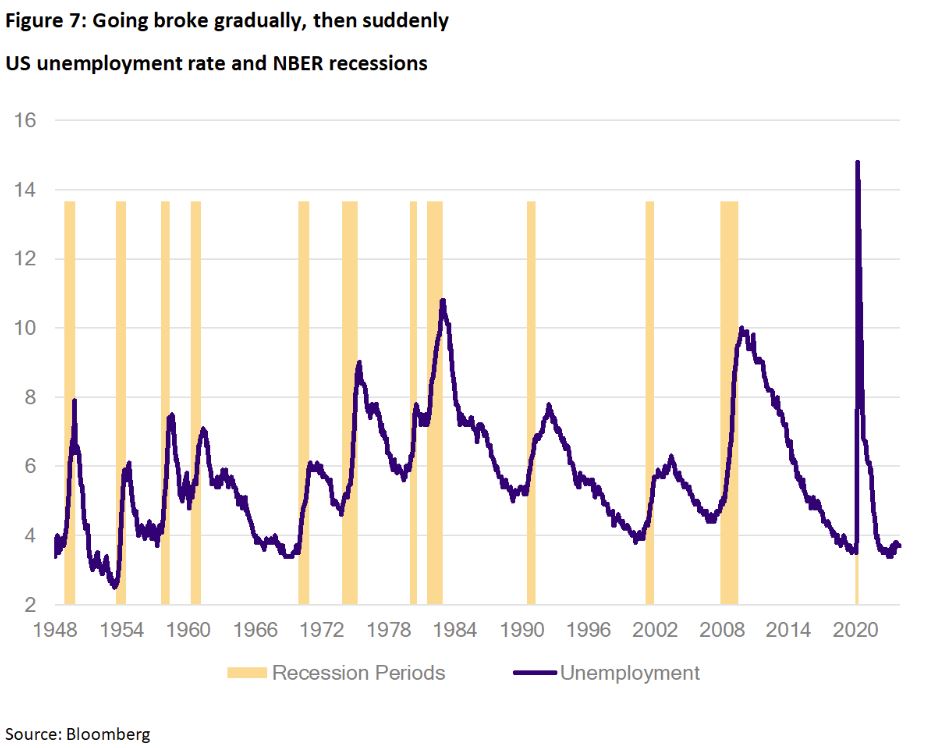

The first would be something that looks like a soft landing, but carries on softening.

Historical experiences of recessions tells us that it happens gradually, then suddenly (to paraphrase Hemingway).

The explanation for this is not unanimously agreed upon, but it probably has something to do with how hard it is to find a neutral policy point when the economy is at full capacity or full employment.

When the economy is at full employment every extra bit of demand pushes prices higher, causing inflation to soar. Any weakening in demand creates extra capacity and the potential for layoffs as companies cut costs.

The trickiest bit to all of this is knowing that monetary policy hits the economy with a lag, but not knowing how long that lag really is.

The safest bet for central bankers with price stability in their mandates is to err on the side of caution, over-tighten to get inflation under control, and hope they can ease policy in time to avoid a really hard landing.

The track record on that last bit hasn’t been great, though.

This cycle poses extra challenges in figuring out the lags.

Did the post-pandemic fiscal stimulus lengthen the lags? Has a largely fixed-rate US mortgage market dampened the pass-through effect of higher interest rates?

Has immigration weakened the link between interest rates and our housing market?

I wish I had all the answers, but I do know this: not all households and corporates managed to fix the rate on their debt at super-low rates.

Corporate defaults have been rising in spite of strong economic growth which means there is buckling at the edges.

Rising delinquencies on consumer loans and credit cards are signs that policy has become restrictive.

At some point, the edges creep into the middle. The lagged effects finally show up, tail risks become the central risk, and the gradual recession becomes a sudden one.

The second way to a hard landing is via no landing. This would push the timing more towards next year.

A no-landing scenario raises the chances that inflation will resurge.

I’m not a massive subscriber to this view as I think there is enough in the inflation and wage data to support a continued disinflation trend.

But I acknowledge that markets will not take kindly to any disappointment on inflation.

A more likely version of this path to hard landing is that during a no-landing phase, central banks feel reluctant to cut rates.

As the lagged effects of restrictive policy catch up with the real economy, the economy eventually falls into a hard landing.

This may also be why the US yield curve has stayed inverted.

Active decisions in times of uncertainty

Let’s bring this back to positioning implications.

The summary of my view change from a few months ago is that I am still not seeing a step down in consumer appetite.

That means disinflation alone is insufficient for driving a strong rally in bonds.

In addition, near-term risks may be skewed to further bond volatility as the market tries on the no-landing narrative.

For our income portfolios, our long bias on duration has eased, and I’m happy to tactically take duration exposures all the way down to minimal levels.

I still like bonds and higher yields offer great asymmetry.

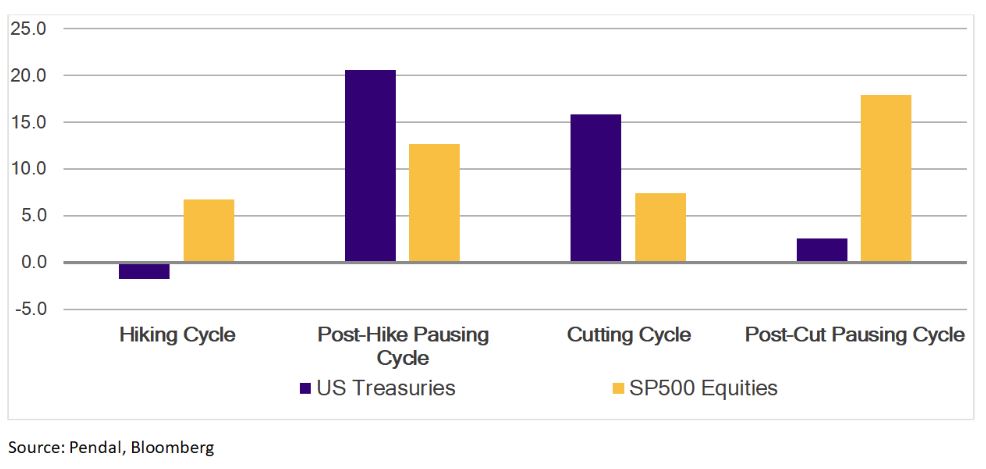

But I really like bonds because I think the hiking cycle (at least in the US) is over.

In an active portfolio, the way to express this is to buy-on-dips and be prepared to take the gains when you have them.

At least for the next couple of months.

I also won’t say no to buying dips in risky assets along the way.

Equities (and credit) do well as long as growth holds up. The prolonged “everything sell-off” in 2022 had as much to do with a deteriorating growth outlook as it did soaring inflation.

It’s hard for anything to do well in the face of stagflation.

In 2024, as long as the growth backdrop remains healthy, everything sell-offs are likely to be good buy-the-dip opportunities.

The core returns driver in our income strategies continues to be high-quality, investment-grade credit.

The pace of corporate bond issuance in Australia has started this year with a bang, all met with very strong demand.

While selective, our portfolios have not shied away from participating in those opportunities.

But I’m keeping an eye on default rates.

As Figure 9 shows, tightening credit conditions tend to lead to higher default rates with a decent lag.

Even though lending standards have begun to loosen, default rates are still rising.

So far, global credit spreads have shrugged off higher default rates, which would be correct if the soft landing has already happened.

However, if this old relationship holds, having a higher quality and liquidity bias in our credit portfolios will give us the resilience and flexibility to navigate an uglier market environment.

About Amy Xie Patrick and Pendal’s Income and Fixed Interest team

Amy is Pendal’s Head of Income Strategies. She has extensive expertise and experience in emerging markets, global high yield and investment grade credit and holds an honours degree in economics from Cambridge University.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia. The team oversees some $20 billion invested across income, composite, pure alpha, global and Australian government strategies.

Find out more about Pendal’s fixed interest strategies here

About Pendal Group

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

Here are the main factors driving the ASX this week according to portfolio manager JIM TAYLOR. Reported by portfolio specialist Chris Adams

- Find out about Pendal Focus Australian Share Fund

- Register for Crispin Murray’s bi-annual Beyond the Numbers webinar

LAST week saw the release of highly anticipated January US Personal Consumption Expenditures (PCE) data.

While it showed an increase on previous months, it was in-line with consensus, and there has already been a significant change in expectations around rate cuts in 2024.

So, the market’s reaction was fairly muted – with the S&P 500 ending the week up 0.99%.

The question remains whether the uptick is a blip in the road to further disinflation – as the Fed suggests – or if it is the start of a more significant uptrend.

Locally, the market took Australia’s Consumer Price Inflation (CPI) data for January in its stride, with the S&P/ASX 300 returning 1.68% for the week.

Bonds rallied across the curve, with US 10-year Treasury yields falling 7 basis points (bps).

Commodities were mixed, with Brent crude oil up 2.5% and iron ore down 1.6%.

Bitcoin fired up and is back to its highest level since 21 March.

The Nasdaq and S&P 500 both hit records and were up for the seventh week in the past eight – with the S&P 500 now up in sixteen of the past eighteen weeks, its best run since 1971.

Fedspeak

Last week saw several members of the US Federal Reserve (the Fed) making the case for rate cuts in 2024, while also exercising some caution. In summary:

- Atlanta Fed President and FOMC voting member Raphael Bostic noted that he expects the first cut in the summer.

- Boston Fed President and non-voting member Susan Collins suggested that the path of easing may not be as rapid as in previous cycles.

- New York Fed President (and FOMC Vice-Chair) John Williams observed that there is still “a ways to go” until inflation is back to target.

- Cleveland Fed President and voting member Loretta Mester said that she thinks three cuts for 2024 currently sounds about right.

This week will see Chair Jerome Powell testify before Congress.

The recent convergence between market expectations around rate cuts and the Fed’s own dot-plots should be helpful.

US inflation

January’s PCE index rose 0.34% month-on-month, up from 0.12% in December.

This was the fastest monthly rise for a year but was largely in-line with consensus expectations.

It was up 2.40% year-on-year, down from 2.62% in December.

The Core measure rose 0.42% month-on-month and 2.85% year-on-year.

The Goods component (about 23% of the PCE basket) continues to do much of the heavy lifting, falling 0.05% month-on-month in January.

Core Services (about 65% of the basket) was up 0.58% month-on-month in January after increasing 0.29% in December.

This was despite Housing – which is 15% of the basket – rising at 0.50%, which was lower than the aggregate Core Services inflation.

These results have driven the three and six-month annualised figures back above the Fed’s 2% inflation target.

Personal income rose 1.0% which was well ahead of expectations.

However, once the annual increase in social security payments and the effect of dividends were stripped out, core wages and salary growth rose 0.4% which was in-line with expectations.

US growth

Both initial and continuing jobless claims came in a little above consensus expectations, while January new home sales grew 1.5% which was slightly weaker than expected.

February’s ISM Manufacturing Survey came in at 47.8 – down from 49.1 and well below the 49.5 expected.

The Consumer Confidence Index for February was also weak at 106.7 versus the 114.8 expected and down from 110.9 in January – the first drop in three months.

Find out about

Pendal Horizon Sustainable Australian Share Fund

Australian economy

The CPI fell 0.33% month-on-month in January, following the 0.66% rise in December.

The annual rate rose 2bps to 3.40%, which was a touch under consensus expectations of 3.6%.

The Core measure – which excludes volatile items and travel – was flat month-on-month and the annual rate fell 9bps to 4.13%, which was also lower than expectations.

Food (ex-meat), furnishings, clothing and travel prices are all declining, while rent, home maintenance and utilities are all going up.

The latest round of fortnightly Enterprise Bargaining Agreement (EBA) data showed that wages growth had eased from 4.1% in December to 3.7% in January – though January’s data covered just 9,000 workers versus 199,000 in December.

While the more modest pace suggests we may have seen the peak in wages growth, it also suggests that wages growth is likely to remain relatively elevated.

Interestingly, union wage agreements are continuing to run about 100-150bps higher than non-union agreements.

Retail sales grew 1.1% in January versus the 1.5% expected, suggesting that retail sales are near stalling at current levels.

It is worth noting that the Reserve Bank of New Zealand (RBNZ) kept rates unchanged at 5.5% despite some speculation it would hike.

Rates in New Zealand are unchanged since May last year and the RBNZ remains of the view that sustained high rates are constraining economic activity and prices.

US earnings scorecard

About 97% of the S&P 500 has reported Q4 2023 earnings.

Of this, 73% of companies reported a positive EPS surprise (which is below the five and ten-year averages of 77% and 74%, respectively) and 64% of companies reported a positive revenue surprise.

In aggregate, companies are reporting earnings 4.1% above estimates – again lower than the five-year average of 8.5% and the ten-year average of 6.7%.

The year-over-year earnings growth rate for the S&P 500 is 4.0%, the second-straight quarter of earnings growth.

Looking forward, consensus is expecting 3.6% earnings growth for Q1 2024 and 9.2% for Q2 for overall calendar-year 2024 earnings growth of 11.0%.

The 12-month forward price-to-earnings ratio is 20.4x, which is above the five and ten-year averages of 19.0x and 17.7x.

Australian reporting season wrap

Reporting season began well, with FY24 earnings projections largely unchanged in the first couple of weeks.

Then it faded into the close, with financial year earnings revised down 1.5% over the month – the weakest outcome since February 2009.

Consumer Discretionary, Financials and REITS saw positive revisions, while the sharpest downgrades came in Communication Services, Energy, Consumer Staples and Materials.

Dividend projections were also scaled back.

There are three factors at play:

- Softening margins: seven out of ten GICS sectors (excluding Financials) saw margin compression, with Consumer Discretionary providing one pocket of resilience.

- Interest cost projections are still rising, with consensus estimates higher for every sector bar one.

- High capex projections.

Despite this, the majority of stocks in the index made gains in the wake of their results – with the market price-to-earnings ratio expanding around 0.7x as a result.

Valuation change was the dominant element of price moves during reporting season.

Single-day stock price volatility in reporting season has been elevated since Covid and remains so, though this reporting season was a touch less volatile than previous episodes.

Meanwhile, 35% of companies beat expectations, which was in-line with the historical average, while 46% missed, which was higher than the 34% historical average.

About Jim Taylor and Pendal Focus Australian Share Fund

Drawing on more than 25 years of experience investing in top-performing Australian companies and a background in accounting, Jim manages our Long/Short Fund and co-manages our Imputation Fund. He is a Chartered Accountant with membership of the Australian Institute of Chartered Accountants.

Pendal Focus Australian Share Fund is managed by Crispin Murray. The fund has beaten its benchmark in 14 years of its 18-year history (after fees), across a range of market conditions. Find out more about Pendal Focus Australian Share Fund here.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

January data suggests inflation continues to moderate. But we shouldn’t read too much into this better-than-expected outcome, writes Pendal’s head of government bond strategies TIM HEXT

- Monthly data supports the theme of moderating inflation

- The months ahead will see a more balanced CPI outcome.

- Why bonds, why now? Pendal’s income and fixed interest experts explain

- Browse Pendal’s fixed interest funds

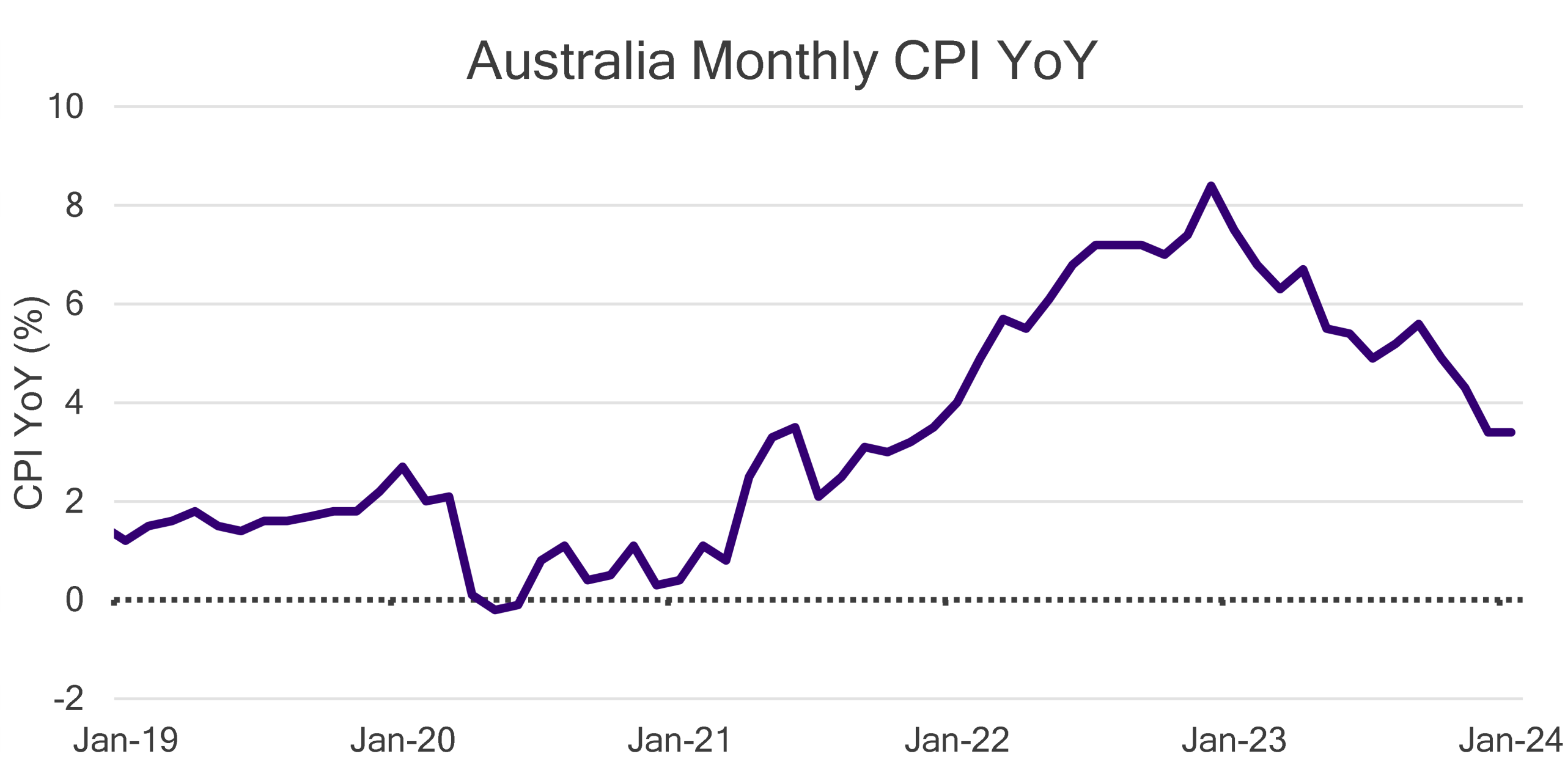

THE January inflation numbers showed a continuation of the theme of moderating inflation.

Prices were 3.4% higher than January 2023.

More impressively, prices were down 0.3% in January from December – though this number is not seasonally adjusted and January is usually a weaker month.

This continues the downward path to inflation, in place since the 8.4% high in December 2022.

Source: ABS, 2024

Monthly CPI price data sets are not comprehensive, but quarterly are.

Only around 60% of the basket is tracked every month, while 30% is collected once a quarter (with different items in different months) and 10% is annual (with education in February, health insurance in April, and council rates in September).

So effectively, most monthly CPI prints cover 70% of the basket. The others are kept flat.

The list of prices going down in January is quite long; fuel, clothing, furnishings, and recreation all helped reduce inflation.

However, utilities went up (but less than expected), while food prices rose a bit more than expected.

Overall, we shouldn’t read too much into this better-than-expected outcome and the market reaction has also been quite muted.

It does make us more confident on our 0.8% forecast for the March quarter CPI due late April – and if anything, we might lower it to 0.7%.

This would see annual inflation (as measured quarterly, not monthly) also fall to 3.4% – near the RBA forecast of 3.3% of CPI by June.

However, we will have to wait for the September quarter 2023 number of 1.2% to drop out in October for CPI to have a chance of hitting 3%.

The months ahead will see a more balanced CPI outcome.

For items only measured once a quarter, January is goods-heavy, while February and March are more services-heavy – and services are where the higher pressures are. This will be especially so when education hits the February numbers.

If anyone is interested in a breakdown of the path back to low inflation this year, please read my article in our recent Australian Quarterly Update.

Find out about

Pendal’s Income and Fixed Interest funds

Oil remains the main x-factor to these forecasts and prices have edged steadily higher in recent weeks, though still in range for now.

The RBA will remain confident that its inflation forecasts are being met.

This does not mean rate cuts in the months ahead, but if the Fed were to start cutting in May, it still opens the door for lower rates here in the second half of 2024.

We remain biased to being overweight duration but will continue to adjust positioning based on market levels in a range-trading market.

About Tim Hext and Pendal’s Income & Fixed Interest boutique

Tim Hext is a Pendal portfolio manager and head of government bond strategies in our Income and Fixed Interest team.

Tim has extensive experience in banking, financial markets and funding including senior positions with NSW Treasury Corporation (TCorp), Westpac Treasury, Commonwealth Bank of Australia, Deutsche Bank, Bain & Co and Swiss Bank Corporation.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia.

Find out more about Pendal’s fixed interest strategies here

About Pendal

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

In 2023, Pendal became part of Perpetual Limited (ASX:PPT), bringing together two of Australia’s most respected active asset management brands to create a global leader in multi-boutique asset management with autonomous, world-class investment capabilities and a growing leadership position in ESG.

Here are the main factors driving the ASX this week, according to Pendal’s head of equities CRISPIN MURRAY. Reported by investment specialist Chris Adams

- Find out about Pendal Focus Australian Share fund

- Register for Crispin Murray’s bi-annual Beyond the Numbers webinar on March 8

LAST week was quiet on the macro front, with little data to add to the debate on disinflation and growth.

Fed speakers remain patient, as an economy holding up well allows them to wait and see if improving inflation trends are confirmed.

The US equity market was singularly focused on the Nvidia result, which once again beat consensus expectations, taking the stock – and the market – to new highs.

The S&P 500 ended up 1.68% for the week.

US earnings have been good, index momentum is strong, breadth is reasonable, the macro backdrop is supportive, and seasonality is positive – with March/April historically the best two months in 1H.

So, while consolidation is possible, the market remains in an uptrend.

The Australian market was largely flat, in a week dominated by results (S&P/ASX 300 +0.12%).

Earnings season is telling us the economy is okay; there is the odd pocket of softness, but generally, trends are continuing as before.

Industrial and tech companies are doing better, while large consumer-facing companies are wary of delivering a message which is too positive for fear of a media backlash.

Economy and inflation

United States

There was little relevant data last week.

We are seeing some survey data – such as the Evercore ISI Company Survey Diffusion index – indicate that the industrial sector is beginning to improve in the US.

This had been dragged lower by substantial destocking in 2023.

Even a gentle recovery here would help underpin economic growth.

A number of Fed members made comments during the week, generally emphasising the importance of not overreacting to January’s CPI data.

Governor Chris Waller was the most cautious, saying that the chance of January’s CPI being noise versus a signal was a fifty-fifty chance. He does tend to be at the more hawkish end of the debate.

Vice-chair Philip Jefferson and New York Fed chief John Williams took a more benign view.

Williams noted that disinflation tends to be bumpy but is moving in the right direction, and that while core inflation is still above the 2% target, it is below 3%. He also noted there was no need to shift the view on neutral rate levels.

These comments continue to suggest a likely first cut in May or June.

Economic resilience gives the Fed capacity to be patient; it would be a tougher call if there was a weaker economy, but inflation hasn’t fallen sufficiently.

Europe

Europe also saw some marginally positive industrial survey data, as the Euro Area S&P Global and Global Composite PMIs – a measure of confidence – ticked up.

We also first signs of wage growth data easing in Europe.

China

Sentiment remains poor and authorities continue to try to support the stock market.

The National People’s Congress annual meeting in March looms large.

The market will be looking to this event to provide signals on growth targets, fiscal deficit, local government bond quota and potential central government bond issuance.

Markets

Nvidia is the bellwether for the AI theme which, in turn, is the leading theme in the market.

Its Q4 result was strong and better than expected, leading to a US$250 billion rise in market cap on the day and a current market cap of more than US$2 trillion.

The market liked several messages from management, including:

- Revenue was diversifying, implying a more sustainable earnings stream.

- The company absorbed a large hit from China, where regulation shrank its market from about 25% to mid-single digit of revenue in the quarter.

- New production innovation from late 2024, which has five to ten times the computational power and should underpin the outlook for 2025.

- Enterprise and sovereign demand are gaining share.

The spread into enterprise is particularly interesting as that goes to the use case and the potential for generative AI to accelerate productivity and earnings in other sectors.

Find out about

Pendal Horizon Sustainable Australian Share Fund

Overall, the US market appears to remain well underpinned as it breaks to new highs.

The percentage of stocks above their 200-day moving average has remained in the 70-80% range in 2024, which compares to a trough of near 20% in October last year.

Sentiment is very bullish, but this is not a reason in and of itself for the market to drop.

For example, the market stayed near current levels of bullishness – as measured by the Consensus Inc % Bullish measure – for extended periods across 2014-15 and late 2016-18.

Earnings season

Earnings season in Australia remains mixed, with no clear macro themes emerging.

REIT and retailer results suggest that the consumer continues to hold up relatively well.

But there are pockets of softness – for instance, the supermarket sector as price inflation falls, but no pick-up in volumes in response.

Advertising remains very soft, but industrial companies are generally seeing activity remain at the same cadence.

Cost control has been a point of differentiation at the company level, but it tends to be disciplined control rather than large restructuring announcements.

One recurring theme is that large companies, particularly with a consumer focus, are mindful about the media and government reaction to their results.

There is a less positive spin and more focus on evidence of reinvesting to help customers.

In some cases, it appears as though companies are prepared to sacrifice valuation ratings to avoid facing backlash.

Industrial and tech companies are more immune to this issue and are, therefore, faring better.

About Crispin Murray and the Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia. Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions.

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

Despite some negative surprises among ASX industrials this earnings season, there are still opportunities for stock pickers. Pendal analyst ANTHONY MORAN explains his approach

- Industrials hit by changes in customer behaviour.

- Opportunities in sold off stocks, but watch margin pressures

- Find out about Pendal Focus Australian Share fund

THERE have been plenty of negative surprises among industrial stocks this ASX earnings season, showing how companies across the economy are changing their behaviour, says Pendal equities analyst Anthony Moran.

It’s an environment that provides opportunity for stock pickers – if you know what to look for.

“Several industrials companies have demonstrated weakness for the December six months and it’s been a surprise,” Moran says.

“There is more weakness than expected and that’s manifesting in corporate results.”

Moran nominates packaging group Amcor where volumes were down 10 per cent for the December quarter, year-on-year.

“That’s quite astounding for a company that sells packaging for centre-of-the-aisle groceries.

“It highlights that there is weak demand in certain sectors, and the de-stocking impact has exceeded expectations,” Anthony says. Pendal holds Amcor.

More broadly, it shows that companies across the economy are trying to manage higher interest costs by reducing working capital and maximising their cash balances, he says.

“Amcor saw it. Fletcher Building experienced it through the New Zealand construction cycle.

“Treasury Wine Estates saw it in their US wine business and in their Asian premium business. At Treasury there is more destocking then expected along with a weaker consumer.” Pendal holds Treasury Wines.

Where to look for opportunities

The macro shifts hitting individual companies throw up opportunities for investors, Moran argues.

“There are companies that have cyclical weakness, and their valuations can be attractive.

“You want to look for a company that has the ability to grow above its end market and has the potential to accelerate its share, even in a declining market.

James Hardie (held by Pendal) is an example, he says.

“It’s shown strong growth in the last 12 months even as the repair-and-remodel cycle has been down double digits in the US.

“You want companies that are able to do that,” he says.

Another example is Orora (also held by Pendal) which is a major packaging distributor which has spent time implementing a new operating model, that is now showing sustained market gains, Anthony says.

Pendal Focus Australian Share Fund

Now rated at the highest level by Lonsec, Morningstar and Zenith

Delivering good performance from a core business, even if the market is not growing, is attractive to investors, Anthony says.

“Aristocrat Leisure is doing that at the moment. The US casino market is stable, but Aristocrat is delivering good performance.” Pendal holds Aristocrat.

Look for companies emerging from down cycles

He says investors should consider looking for industries that are emerging from down cycles, particularly if they are worried about the economic outlook.

Another theme coming through earnings season, particularly across industrials, is margin disappointment, Anthony says.

“In Fletcher Building’s case, the sensitivity of the margins surprised but that’s what you get in big volume downturns.

“But for someone like Hardie, it did disappoint on its margin outlook, and that’s because some of the cost relief they got during Covid is starting to normalise up.

Transurban is another example where they recorded another year of cost growth above inflation and that’s crimping their margins.

“The headline is that costs are still an issue for a number of companies and for most industries pricing power is coming off. It means investors need to watch margins,” Anthony says.

“The next 12 to 24 months is going to be the great normalisation of the post-Covid super-cycle in margins, at least for the industrials sector.”

About Anthony Moran

Anthony Moran is an analyst with more than 15 years of experience covering a range of Australian and international sectors. His sector coverage has included Australian Industrials and Energy, Building Materials, Capital Goods, Engineering & Construction, Transport, Telcos, REITs, Utilities and Infrastructure.

He has previously worked as an equity analyst for AllianceBernstein and Macquarie Group, spending a further two years as a management consultant at Port Jackson Partners and two years as an institutional research sales executive with Deutsche Bank.

Anthony is a CFA Charterholder and holds bachelor’s degrees in Commerce and Law from the University of Sydney.

Here are the main factors driving the ASX this week, according to portfolio manager RAJINDER SINGH. Reported by portfolio specialist Chris Adams

- Find out about Rajinder’s Pendal Sustainable Australian Share Fund

- Find out about Crispin Murray’s Pendal Focus Australian Share Fund

- Register for Crispin Murray’s bi-annual Beyond The Numbers webinar on March 8

GLOBAL equity markets took a breather last week, while bonds continued to sell off as they have so far throughout February.

Stronger-than-expected US inflation numbers weighed on both asset classes. Core CPI — and the services components in particular — stayed stubbornly high.

Other key US data releases were mixed.

Overall, these indicators increase the likelihood that the US Federal Reserve will want to accumulate more evidence of sustained disinflation before making its next change in rates.

Markets already had moved to a view of a first cut in May or maybe even June, rather than March as hoped earlier in the year.

In other international economic news, two G7 countries – Japan and the UK – dipped into technical recessions.

Commodities have been relatively resilient, with oil holding onto its previous gains, and copper and lithium enjoying some relief after a difficult 2024 so far.

In Australia, the unemployment rate edged up and Australian bonds followed US bond yields higher.

We saw reporting season moving up a gear with numerous important results coming out.

Early indicators suggest that in aggregate, companies are delivering revenue in line with expectations, but with upside on earnings due to better margin management.

The S&P/ASX 300 gained 0.23% while the S&P 500 fell 0.35%.

US macroeconomics

Last week, we saw two important US inflation indicators: the producer price index (PPI) and consumer price index (CPI).

The headline PPI advanced 0.3% in January, which was a stronger than the 0.1% expected.

The acceleration in core PPI was an even bigger surprise, increasing by 0.5% versus consensus of 0.1%.

Another concern is that some components of PPI, especially health care, were strong in January and these are aligned with those used in the Fed’s preferred measure of inflation – the personal consumption expenditures (PCE) core services ex-housing (CSEH) index.

Some economic forecasters increased their predicted PCE inflation as a result.

The CPI report was the most influential of the week’s economic indicators.

Headline CPI for January came in higher than expectations, up 0.3% month-on-month and 3.1% year-on-year versus consensus increases of 0.2% and 2.9%, respectively.

Core CPI advanced 0.4% and 3.9% year-on-year, which also was higher than consensus.

Strength in housing-related Owners Equivalent Rent (OER) and Core Services ex-Housing drove this result.

This was the highest Core CPI reading in eight months, prompting a sell-off in the S&P 500 and an increase in bond yields.

While CPI is still decelerating, the concern is that the pace of this decline has stalled – requiring the Fed to keep rates up higher for longer.

The case for this is supported by the gap that has opened up between Core CPI and PCE Core Services ex-Housing measure.

There were some noteworthy trends in the CPI components:

- Services inflation remains consistently higher and stronger, though some forward-looking indicators suggest rent should have a moderating effect.

- Commodities and food effects have continued to reduce slowly over the last 12-18 months.

- Energy is having a deflationary effect, though this could easily reverse with base effects and changing prices.

Find out about Pendal Sustainable Australian Share Fund

Following the release of the CPI numbers, the Fed’s Chair, Jerome Powell, held a closed-door meeting with US House members.

Here, he reportedly said words to the effect that the CPI numbers were consistent with the Fed’s expectations and that they would look at the upcoming PCE report to give them some more information.

Elsewhere, January retail sales were also disappointing, down 0.8% month-on-month.

Housing starts were soft, down 14.8% month-on-month in January, but poor weather has been blamed for depressing both indicators.

Initial Jobless Claims remained low at 212,000, indicating that US labour markets still appear resilient.

On Tuesday, we saw the release of the NFIB small business survey, which showed that US business sentiment remains at recessionary levels.

However, the survey also showed small businesses continue to moderate price rises.

In terms of consumer sentiment, the University of Michigan update showed consumers feeling significantly more optimistic than the low levels in 2023.

Historically, this has correlated with S&P 500 market performance.

Global macroeconomics

US goods imports data demonstrates the sharp decline in China’s share of the US market.

As a percentage of total US imports, China has fallen from a peak of more than 20% prior to Covid back to 13.7% in December 2023 – roughly the same level as 2004.

Mexico has overtaken China with 15.3% of US imports, which at least partly reflects the outcome of “near-shoring”.

Elsewhere, the EVRISI survey of company sales in China shows that sales have fallen back to near-record lows and are only just above the Covid trough.

Japan and the UK dipped into technical recessions with a second quarter of economic contraction in Q4 2023. Germany also contracted but had been flat in the previous quarter.

Japan’s three-decade economic slide continues, with the country slipping from the third to fourth-largest economy in the world after the US, China and Germany.

Australian macroeconomics

The unemployment rate rose to 4.1% (consensus 4.0%), which is the first time above 4% since Jan 2022.

Employment was flat, the number of unemployed rose 22,000, and the number of hours worked dropped 2.5%, though there may be seasonal effects at play.

It’s only one month of data, but it is in line with other indications that the Australian economy is starting to show signs of slowing.

The trend in employment growth slowed considerably towards the end of 2023.

Also, the shift from full-time to part-time employment as the composition of hours worked indicates a degree of under-utilisation within the Australian labour force, which is important in helping slow inflation.

ASX earnings season

It’s still relatively early days, but it’s been a decent start to ASX half-year reporting season.

Australian companies seem to have navigated relatively subdued revenue growth by increasing margins and delivering decent EPS outcomes.

An analysis of management commentary indicates that companies are, if anything, a bit more optimistic (or at least less pessimistic) about current positioning and the outlook for the year ahead.

About Rajinder Singh and Pendal’s responsible investing strategies

Rajinder is a portfolio manager with Pendal’s Australian equities team and has more than 18 years of experience in Australian equities. Rajinder manages Pendal sustainable and ethical funds, including Pendal Sustainable Australian Share Fund.

Pendal offers a range of other responsible investing strategies, including:

- Pendal Sustainable Australian Share Fund

- Crispin Murray’s Pendal Horizon Fund

- Pendal Sustainable Australian Fixed Interest Fund

- Pendal Sustainable Balanced Fund

- Regnan Credit Impact Trust

- Regnan Global Equity Impact Solutions Fund

Part of Perpetual Group, Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management. Responsible investing leader Regnan is now also part of Perpetual Group.

What’s next for rates and how should fixed-interest investors be positioned? CommBank chief economist STEPHEN HALMARICK and Pendal’s head of government bonds TIM HEXT discuss their views in a new on-demand webinar

Below are the highlights. Watch the webinar here

- Soft landing likely with rate cuts around September

- Bond rally to be sustained

- Watch now: How to conquer the rates peak webinar with CommBank’s Stephen Halmarick and Pendal’s Tim Hext

AS chief economist at Australia’s biggest bank, Stephen Halmarick has better access to real-time consumer data than almost anyone.

The day after the RBA’s February rates decision, Halmarick sat down to share his insights in a webinar with Pendal’s head of government bond strategies Tim Hext.

“The Reserve Bank kept a mildly hawkish tone … at its board meeting,” Halmarick said after the no-change decision.

“Governor Michelle Bullock isn’t yet ready to declare victory against inflation.”

Official figures, and internal data from the Commonwealth Bank, show the economy is slowing and growth this year is likely to be below trend, he said.

“Household sectors will be under ongoing stress. But business investment intentions are holding up nicely. And state government infrastructure spending is still pretty solid.”

Soft landing

Halmarick believes the Australian economy is heading for a “soft landing”, based on weak consumer spending.

“It’s not till we get the rate cuts through the door that we see consumers start to pick up,” he says.

“We think the unemployment rate by the end of this year will be closer to 4.5 per cent.

“There will be more people employed but there will also be more people joining the labour market.

“It’s important to remember that nobody needs to lose their job for the unemployment rate to go up.”

Halmarick expects inflation to keep falling this year, giving the central bank confidence to cut the official cash rate in September.

US inflation almost under control

Pendal’s head of government bond strategies Tim Hext says the US economy is close to getting inflation under control.

He believes the first rate cut in the US will happen in May, followed by several more this year.

“The RBA always follows what happens globally,” Hext says in the webinar.

“This cycle has been all about inflation and that’s what will allow the Reserve Bank to start cutting rates.”

Hext believes there will be three or four cuts within six months of the first reduction in the local cash rate, which he tips will be in September.

Geopolitical factors and other risks

What are the key risks to this scenario?

Halmarick points to geopolitical factors and risks around supply chains, as well as the performance of China.

“Domestically the key risk is the fall in household real income,” he says “The other big issue is the housing market.

“I’m particularly interested in rental markets. Rents are chewing up so much more of people’s money.”

Hext says the list of worries about the economy is getting smaller, not bigger.

One potential concern is the Reserve Bank’s aggressive reduction in its inflation forecast – it expects headline inflation to be 3.2 per cent by the end of 2024.

There’s a risk that won’t be met, says Hext.

And he says oil – via primary and secondary effects – can also have an impact on inflation.

Significantly, the Reserve Bank seems more relaxed about wages.

Both Stephen and Tim agree that the upcoming tax cuts in the middle of the year will not make a significant difference to inflation or growth, relative to the already legislated Stage 3 tax cuts.

What does it mean for fixed income investors?

With a soft landing the most likely outcome, the current bond rally should be sustained, argues Hext.

Last year investors could buy “real yields” on 10-year bonds above 2 per cent – meaning the investor gets 2 per cent above the inflation rate on a government bond.

“That’s very generous for taking very little risk,” Hext says. “It’s not sustainable unless you have a massive productivity boom.

“If inflation heads towards 3 per cent and real yields start to head back towards where productivity is at the moment – somewhere between zero and 1 per cent – then 10-year bonds should land around 3.5 per cent and the cash rate around 3 per cent.

“Right now we are a bit above 4 per cent so there’s a fair bit of juice left in 10-year bonds,” he says.

“The rally should be sustained. Bonds still represent some value though they’re not as cheap as a year ago.

“Under a soft-landing scenario, it is quite risk friendly. “

Which asset classes should investors consider?

“You should have more duration than normal in bonds, you should be comfortable about owning credit, and it’s not a bad environment for equities,” argues Hext.

About Tim Hext and Pendal’s Income & Fixed Interest boutique

Tim Hext is a Pendal portfolio manager and head of government bond strategies in our Income and Fixed Interest team.

Tim has extensive experience in banking, financial markets and funding including senior positions with NSW Treasury Corporation (TCorp), Westpac Treasury, Commonwealth Bank of Australia, Deutsche Bank, Bain & Co and Swiss Bank Corporation.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia.

Find out more about Pendal’s fixed interest strategies here

About Pendal

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

In 2023, Pendal became part of Perpetual Limited (ASX:PPT), bringing together two of Australia’s most respected active asset management brands to create a global leader in multi-boutique asset management with autonomous, world-class investment capabilities and a growing leadership position in ESG.

The latest US CPI data surprised to the upside. Pendal’s head of government bond strategies, TIM HEXT, explains what it means for investors

- Why bonds, why now? Pendal’s income and fixed interest experts explain

- Browse Pendal’s fixed interest funds

THE inflation numbers were released this week and surprised to the upside.

Headline for January was up 0.3% (3.1% year over year) and core up 0.4% (3.9% year over year).

This meant that CPI has, for now, failed to follow the PCE (the Fed’s preferred inflation measure) below 3%.

This was only a small miss, 0.1% higher than expected, but was still against the narrative of falling inflation.

After all, the US needs monthly inflation numbers hitting 0.2% before the Fed can relax.

In the US, CPI is heavily influenced by what is called Owner’s Equivalent Rent.

Unlike most countries which only measure rents for those actually renting (in Australia this is 6% of the CPI), the US CPI tries to capture the idea that owners are ‘consuming’ their residence by putting an equivalent rent on it.

This is almost 25% of the CPI basket, on top of the 7.5% for actual rent. Together, they make up housing inflation.

Analysts use Zillow private sector rent numbers as a good lead indicator, but the downward trend there was not matched in this CPI.

Maybe next time.

There was other noise in the numbers, but the market was focused on core services.

The narrative of core goods falling (down 0.3% in this number) contrasts with core services (ex-shelter), which were up 0.7% on the month.

It’s hardly time for the Fed to declare victory.

The focus will now turn to whether core PCE can stay down around 2% annualised or drift higher towards CPI at 3%.

The PCE has a smaller weight to shelter of only 15%. This will help keep it lower than CPI for now.

Historically, core CPI has been around 0.3-0.5% above core PCE as housing has increased at a faster pace than other services.

The following graph, courtesy of Citigroup, shows that these gaps between CPI and PCE do open up quite often, especially when house prices are on the move.

Source: Citigroup, 2024

For now, the markets will grant inflation a bit of leeway.

Yes, cuts from The Fed are being pushed out and bond yields are drifting higher.

Inflation break-evens (long-term expectations) only moved 0.05% higher (from 2.25% to 2.3% for 10 years).

But the market is on notice.

If this becomes a trend in the months ahead, then risk markets will start to take notice, as rates will stay higher for longer and the chances of a recession also increase.

Goldilocks beware.

Find out about

Pendal’s Income and Fixed Interest funds

Our view is that the overall trend to lower inflation is still intact, but the sugar hit from lower oil prices and improved supply chains we saw late last year is now entering a period of more balanced risks.

This is also helped at the margin by the small improvement in the US budget deficit, which is taking some of the steam out of the economy.

We expect the fallout from today’s numbers to persist very near term, as momentum funds lean against a vulnerable market.

This will open up opportunities to once again build exposure into long-duration positions.

The US now has less than four cuts this year (1%) and Australia less than two (0.5%), from almost six and three respectively at the end of 2023.

About Tim Hext and Pendal’s Income & Fixed Interest boutique

Tim Hext is a Pendal portfolio manager and head of government bond strategies in our Income and Fixed Interest team.

Tim has extensive experience in banking, financial markets and funding including senior positions with NSW Treasury Corporation (TCorp), Westpac Treasury, Commonwealth Bank of Australia, Deutsche Bank, Bain & Co and Swiss Bank Corporation.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia.

Find out more about Pendal’s fixed interest strategies here

About Pendal

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

In 2023, Pendal became part of Perpetual Limited (ASX:PPT), bringing together two of Australia’s most respected active asset management brands to create a global leader in multi-boutique asset management with autonomous, world-class investment capabilities and a growing leadership position in ESG.

Here are the main factors driving the ASX this week, according to Pendal’s head of equities CRISPIN MURRAY. Reported by investment specialist Chris Adams

- Find out about Pendal Focus Australian Share fund

- Crispin Murray: Five key questions for 2024 (and how we’re going so far)

GLOBAL equity markets continued to rise last week despite another sell-off in bonds.

The market continues to see stronger economic data — and is now pushing out the expected timing of rate cuts in the US to May or June, rather than March.

Equities were supported by a good US earnings season and the prospect of higher growth to underpin positive earnings revisions. The S&P 500 gained 1.4% for the week.

There was little new insight on the US economy, though a Federal Reserve survey of US bank lending showed early signs that credit tightening was coming to an end. In addition, annual US CPI revisions produced no surprises.

Oil bounced on rising concerns about geopolitical risk but remained in its recent trading range. Brent crude gained 5.6%.

In Australia the Reserve Bank held rates steady and gave a mixed signal on the outlook, effectively conceding they do not really know which way things will break. The S&P/ASX 300 fell 0.65%.

Early half-yearly results were mixed among ASX-listed companies, but largely reflected stock-specific issues.

Sentiment on China continued to deteriorate ahead of the Lunar New Year with base metals lower, which in turn dragged on the resource sector (-3.36%).

US growth outlook

The latest Fed Reserve bank-lending survey pointed to a significant reduction in the number of banks tightening financial conditions.

Credit tightening has been an area of concern for recession bears. Easing here would support the soft-landing case.

Lending standards may be a lead on improving US manufacturing data.

Anecdotally, we are hearing of companies that have reached inventory target levels — and are now waiting on consumer signals before dialling up production.

Jobless claims continued to stay low in the US, averaging 212k per week. This indicates February payrolls will be more than 200k.

The Atlanta Fed GDPNow — a monthly forecasting model created by the Federal Reserve Bank of Atlanta —continues to signal good growth of just under 3.5% for the first quarter of 2024.

Fiscal policy — which has not tightened in the US despite low unemployment — is one factor which explains the resilience of growth.

US Inflation

Inflation news remains supportive, despite better-than-expected economic growth.

This is good for equities, since we’re still seeing the economy holding up with rates able to come down.

The Atlanta Fed’s wage-tracker continues to improve, with 12-month wage growth falling to 5%.

The US Employment Cost Index is back near pre-pandemic levels. Unlike Australia, productivity is strong in the US, which is supportive of the disinflation thesis.

The annual revision of US CPI was also helpful since it contained no surprises (unlike last year). Some feared the progress on disinflation may have been overstated. This has not been the case.

Overall, three-month annualised core CPI stayed at 3.3% with goods a bit higher (-1.2% from -1.6%) and services lower (4.8% vs 5.1%).

There are some signs to be mindful of on inflation.

The service prices component of the ISM Manufacturing Index rose materially and we continue to have freight disruption due to the Red Sea.

There are some concerns the January CPI due this week may be higher than expected. There has been a seasonal effect recently as certain industries load price increases in that month.

There are offsets to these concerns. Chinese deflation remains material, providing a very different context to the situation during Covid. At this point the market has all but given up on a March cut in US rates.

Find out about

Pendal Horizon Sustainable Australian Share Fund

A May cut is regarded as lineball. June is priced as a near-certainty.

China

Chinese deflation continues.

Its consumer price index (CPI) dropped 0.8% in January (year-on-year) versus -0.5% expected.

Core CPI rose 0.4%. This was the lowest since June 2022 when the economy was in the midst of its zero-covid policy.

The producer price index (PPI) was down 2.5%, in-line with forecasts.

The Lunar New Year holiday may provide some respite from bad news on the Chinese economy.

There remains a lot of speculation about whether its weak stock market will trigger a more aggressive policy response.

Last week Beijing replaced the head of its China Securities Regulatory Commission with a banking veteran who was serving as deputy party secretary for Shanghai.

This is a signal that China president Xi Jinping was not pleased with how the sell-off has been managed. Though the issues are more to do with the economy than anything the regulator is able to control.

We doubt this is a sufficient catalyst for China to become more aggressive on stimulus, since the equity market is still not widely owned and the issues are more structural (related to consumer and private business confidence).

Credit data in terms of total new loans was stronger than expected. Though this was also the case last January and did not follow through then. So we do not place too much faith in this signal.

We note that Chinese fiscal policy was not as supportive in 2023 as it could have been.

This provides room for expansion. Any announcements are likely to come out ahead of the National People’s Congress starting March 5.

Australia

The RBA stayed on hold last week.

The message from the press conference was “each way.”

On one hand Governor Michele Bullock noted inflation was too high and needed to fall. This was important because it was tied to cost-of-living pressures.

On the other, she said recent developments were encouraging. The first cut would not require inflation to be in the 2-3% range if confidence was high that’s where it was heading.

Bullock’s testimony to the parliamentary committee was a little less hawkish but with no forward guidance.

There is an expectation that the economy is slowing and there are some anecdotal signs of this, notably with talk of job cuts.

However, retailers have seen decent sales, the housing market fired last weekend and the US is holding up better than expected.

We also note New Zealand inflation data has been worse than expected, prompting expectations of another hike.

On balance, we suspect the market’s current expectation of an August rate cut may be optimistic.

Markets

Three-quarters of the way through US earnings season we are seeing positive earnings revisions.

The market was expecting 3% EPS growth for CY24 and Q1 is currently signalling around 7%. Stripping out the “Magnificent Seven” tech stocks this is still coming in around 6%.

This strength is supported by resilient margins, as input and labour costs are coming in less than expected.

On the negative side, we’ve seen a step-up in layoff announcements.

This may be a seasonal factor — we saw similar announcements in January 2023. It also has not flowed through yet into claims data.

We are seeing cash deployed. Stock buy-backs were down in the first three quarters of 2023, but began to rise from Q4 and now stand at about US$150 billion.

We have also seen a strong start to investment-grade credit issuance, which is also supportive for funding requirements.

The US market is up 5.52% so far this year. But similar to last year, much of the gains are driven by the Magnificent Seven (which are up 15% while the rest of the market is flat).

We note that gains in the “Mag 7” stocks are supported by earnings growth.

In Australia, resources were weak last week due to concerns over China.

Meanwhile a collapsed deal between Santos and Woodside weighed on the energy sector (-3.53%).

Healthcare (+1.36%) and technology (+1.01%) were the best sectors.

That reflects a benign environment for quality growth stocks with rates likely to fall while the economy holds up.

About Crispin Murray and Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia. Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions.

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

Here are the main factors driving the ASX this week according to portfolio manager JIM TAYLOR. Reported by portfolio specialist Chris Adams

LAST week was a big one for economic data and US company reporting, amped up by the Federal Open Market Committee’s (FOMC) meeting and Chairman Powell’s press conference.

US reporting season is tracking in-line with historical trends, and the results from five of the “Magnificent Seven” which reported were generally well received – with a strong showing from Meta crowning the week of results.

US economic data was all largely as expected and supportive of the soft-landing scenario, until the monster Non-Farm Payroll print on Friday night potentially put paid to the notion of a March rate cut.

Powell had strongly indicated at the FOMC press conference that a March cut had not been the Fed’s base case.

Commodities were generally weaker and oil gave back all of the gains from the previous week.

The week’s upshot is that expectations around the extent of rate cuts in CY2024 now look more appropriately centred.

The S&P/ASX 300 rose 1.82% while the S&P 500 gained 1.34%.

Interest rates

The Fed removed the previous reference to “any additional policy firming that may be appropriate” from its statement.

Instead, it noted that it will “carefully assess incoming data, the evolving outlook, and the balance of risks” in determining adjustments to the interest rate.

In addition, Powell noted that he didn’t think it likely that the Fed could reach a required level of confidence by March to cut rates at that time.

The market is now focused on the May 24 meeting for a potential first cut.

This gives the Fed the opportunity to see three additional PCE, CPI, PPI and employment data, as well as the first quarter employment cost index (ECI).

Elsewhere, the Bank of England voted 6-3 to keep rates steady as expected; there were two votes for a hike and one for a cut.

US economic data

It was a big week for labour-market data.

JOLTS

The JOLTS job opening data rose to 9,026k in December.

This was above the upwardly revised 8,925k openings in November and ahead of the 8,750k expected by consensus.

Importantly, the JOLTS quit rate held steady at 2.2%.

This is regarded as a key lead on the employment cost index (ECI), which is the Fed’s preferred measure of wage growth and suggested moderation here.

ADP employment

The ADP employment report delivered 107k increase in private payrolls, which was well below the 150k expected by consensus.

ECI

The ECI rose 0.9% quarter-on-quarter for Q4 2023, down from 1.1% in Q3 and versus consensus expectations of 1.0%. This is the smallest increase since December 2019.

Wage gains slowed to 0.9% from 1.2% in Q3, while the year-on-year rate fell to 4.3% down from 4.6% in Q3 and from the high point of 5.2% in Q2 2022.

While hawks on the FOMC are possibly looking for a reading below 4%, the annualised increase in Q4 came in at 3.8% while a drop in the quits rate over recent months bodes well for further slowing ahead.

Initial jobless claims

Initial jobless claims rose to 224k from 215k, and ahead of the 212k expected by consensus.

Data around layoffs suggests that jobless claims could head toward 250k in the next few months.

This is still low by historical standards during an employment slowdown, but is something that the Fed may have their eye on.

During the week, we also had UPS and PayPal – among others – announcing up to 10% in workforce reductions.

Non-farm payrolls

The market had been generally happy with the jobs data through the week.

Then came the hammer blow from non-farm payrolls, which rose 353k in January – almost twice the consensus expectation of 185k.

Net previous revisions were also up 126k.

The headline payroll gain comprises 317K private and 36K government jobs, and gains were broadly spread across the economy.

The unemployment rate was unchanged at 3.7%, which was just below consensus.

The available work force has been growing because of migration.

Average hourly earnings rose 0.6%, versus 0.3% expected, however, this data series is not as reliable as the ECI which is favoured by the Fed.

The market’s reaction was initially negative on concerns that a firm labour market could push out expected rate cuts.

However, several analysts noted that Powell had stressed in his press conference that the Fed was not looking for a fall in employment as a pre-condition for rate cuts.

Find out about

Pendal Horizon Sustainable Australian Share Fund

Australia

Consumer price index (CPI)

The December quarter CPI came in weaker than expected.

Headline CPI rose 0.59% for the quarter (versus 0.80% expected) and 4.05% year-on-year.

This is 45 basis points below the RBA’s forecast made in November.

The trimmed mean inflation rose 0.78% for the quarter, also weaker than the 0.9% consensus expectation.

This measure was 4.18% year-on-year and 3.12% at an annualised quarterly rate.

The result was explained by strong pressure on electricity prices from ongoing subsidies, as well as greater disinflation from tradable goods.

Strong disinflationary pressure on core goods is increasingly offsetting relative resilience in core services pricing.

Retail sales

Retail trade fell 2.7% for the month-on-month in December, worse than the expected -1.7% and reversing the 1.6% gain in November.

There were material seasonal adjustments to the December figure, without which this figure would have been a 5.3% month-on-month decline.

Weakness was broad-based across states and led by non-food spending.

Clothing and soft goods fell 5.7%, household goods was down 8.5%, and department stores were 8.1% lower. Eating out fell 1.1% month-on-month, while spending on food rose 0.1%.

About Jim Taylor and Pendal Focus Australian Share Fund

Drawing on more than 25 years of experience investing in top-performing Australian companies and a background in accounting, Jim manages our Long/Short Fund and co-manages our Imputation Fund. He is a Chartered Accountant with membership of the Australian Institute of Chartered Accountants.

Pendal Focus Australian Share Fund is managed by Crispin Murray. The fund has beaten its benchmark in 14 years of its 18-year history (after fees), across a range of market conditions. Find out more about Pendal Focus Australian Share Fund here.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.