The latest quarterly CPI data shows inflation is on the right path. But there’s still more work to do, writes Pendal’s head of government bond strategies, TIM HEXT

- December-quarter inflation lower than expected

- Housing still needs to cool

- Why bonds, why now? Pendal’s income and fixed interest experts explain

- Browse Pendal’s fixed interest funds

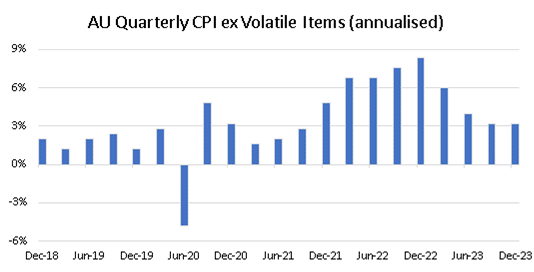

Inflation on track towards 3%

THE market was not disappointed with today’s December-quarter CPI inflation data.

The theme since early November has been inflation moderating globally — and today’s Australian numbers back that up.

The headline Consumer Price Index was 0.6% and underlying 0.8% for the quarter. Annual numbers were 4.1% and 4.2% respectively.

These numbers were slightly lower than expected due to electricity subsidies and international travel.

We also got a comparison of December 2023 with December 2022. Weak fuel prices saw that number at 3.4%.

The Reserve Bank is entering 2024 with inflation somewhere around 4% annually but with the three-month annualised number nearer 3%.

Next week’s RBA statement will urge caution

The RBA will be encouraged by these inflation numbers.

Their panic rate hike in November looks like a mistake — but they will claim some credit for the easing pace.

Their caution will come from non-tradable inflation. Non-tradables are prices largely driven by domestic factors — predominately services.

The RBA can have more impact in this area than in tradables, where we are a global price taker.

Non-tradable inflation has eased from 6% to 5.4% but this is still inconsistent with the RBA inflation band.

The RBA would need to see non-tradable inflation nearer 4% if inflation was to fall closer to the 2-3% target band. Non-tradables are around two-thirds of the CPI.

The biggest driver of non-tradable inflation is wages, which are now around 4%.

Therefore there should be some optimism that over 2024 non-tradable inflation can ease further — though recent hikes in areas like education will continue to put pressure on this.

The path of inflation this year

The key battleground for inflation remains housing, which makes up 22 per cent of the CPI.

New dwelling cost growth is easing, but at a slower rate than hoped.

Find out about

Pendal’s Income and Fixed Interest funds

Rents are still growing, though closer to 5% than 10%. Utilities are held down by subsidies that will be reviewed later this year.

The RBA won’t gain confidence in the medium-term inflation path for inflation until they see housing moderate nearer to 4% in the CPI. (Housing CPI includes the cost of a new dwelling, rents and utilities but not house prices).

The RBA is expecting CPI at 3.9% by June and 3.5% by December.

They may tweak the June number lower but are unlikely to change the December number for now.

Implications for monetary policy

The market still has cash priced for 3.85% — or two cuts — by the end of 2024, with the first around September.

This is driven more by the fact the US is priced for 4% Fed Funds or 1.5% lower by year’s end.

The US is likely to deliver these cuts since their inflation is near target (unlike the RBA).

But the RBA should eventually deliver lower rates — and we think pricing is fair for now.

Hurdles include oil prices (which have sneaked higher in the past week) and resilient employment markets.

Yes, the long-and-variable lags of monetary policy could see last year’s hikes further weigh on the economy, accelerating the need for cuts.

But we think risks lie more to the latter than the former — which makes us still positive on duration.

About Tim Hext and Pendal’s Income & Fixed Interest boutique

Tim Hext is a Pendal portfolio manager and head of government bond strategies in our Income and Fixed Interest team.

Tim has extensive experience in banking, financial markets and funding including senior positions with NSW Treasury Corporation (TCorp), Westpac Treasury, Commonwealth Bank of Australia, Deutsche Bank, Bain & Co and Swiss Bank Corporation.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia.

Find out more about Pendal’s fixed interest strategies here

About Pendal

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

In 2023, Pendal became part of Perpetual Limited (ASX:PPT), bringing together two of Australia’s most respected active asset management brands to create a global leader in multi-boutique asset management with autonomous, world-class investment capabilities and a growing leadership position in ESG.

Here are the main factors driving the ASX this week, according to Pendal portfolio manager PETE DAVIDSON. Reported by investment specialist Chris Adams

- Find out about Pendal Focus Australian Share fund

- Crispin Murray: Five key questions for 2024 (and how we’re going so far)

THE US market continues to hit all-time highs with the S&P 500 up another 2.38% last week. The S&P/ASX 300 gained 2.8%.

US macro data remains good, with solid fourth-quarter GDP growth and better consumer spending.

There was positive commentary on consumer resilience in US Q4 earnings season. But the ratio of companies beating expectations is running below the five-year average.

There were also concerns on electric vehicles as Tesla missed consensus expectations for both sales and margins. The lithium sector remains under pressure.

In Australia, the federal government proposed changes to the Stage 3 income tax cuts, providing extra relief to lower and middle-income earners.

This should help underpin consumer demand since these groups have a higher propensity to spend.

On Wednesday the Australian Bureau of Statistics will release the December-quarter CPI print, which may reset the tone for rates this year.

The market is now looking for two cuts this year, taking us back to 3.85%. There is some potential for a pivot, which would help markets.

Chinese authorities are looking to mobilise some US $278 billion to stabilise its slumping stock market. A recent cut to the reserve ratio requirement for banks may also boost credit.

Hopes of a China rebound from this stimulus supported oil prices (Brent crude +4.2%) which ended higher for a second straight week.

Crude also received support from a big inventory draw-down due to cold weather in the northern hemisphere as well as ongoing Middle East tensions and positive US GDP data.

US politics is pointing towards a Trump victory for Republican nomination, which the market seems comfortable with.

Treasury yields were a touch firmer last week, with yield curves slightly steeper as well.

US data and rates

Overall, US data is solid, though real-time, pulse-type information points to a slowdown.

The advance estimate for Q4 GDP growth was 3.3%, helped by surprising growth in inventories, which continued to build on a large gain in Q3.

However, Fed surveys on manufacturing, new orders, new shipment are all turning down. The Empire Fed, Philadelphia Fed, and Richmond Fed readings all imply a slowdown.

Employment data is on the weaker side with jobless claims ticking up, though that’s probably weather-dependent.

January non-farm payrolls came off the blocks strongly last year, with lots of jobs. A March rate cut from the Fed is less likely if that result is repeated.

Core PCE inflation has fallen to below 3% for the first time since March 2021.

The 6-month annualised change fell to 1.9%, matching last month for the lowest reading since September 2020, when the economy was wracked by the pandemic.

The market will keep a keen eye on any shifts in language or rhetoric from this week’s meeting of the Fed’s rate-setting Federal Open Market Committee.

The Fed’s latest summary of economic projections implied 75 bps of cuts in 2024 – a shallower cutting cycle than current market expectations. There have been big downward revisions to market expectations for central bank policy rates. This reflects faster-than-expected disinflation in major economies and a dovish pivot in central bank communication from several central banks, including the Fed.

China outlook

There was movement at the station last week when Beijing announced a US $278 billion package to support its stock market.

There was also some focus on Alibaba co-founder Jack Ma buying up the company’s stock.

The People’s Bank of China announced it would cut the required reserve ratio by 50bp from February 5. The cut was not a total surprise, but the market was expecting only 25bps.

Markets have been expecting some form of liquidity injection in the lead-up to the Chinese lunar new year, when seasonal cash demand tends to pick up. An injection of roughly CNY 1 trillion cash into China’s banking system is a positive surprise.

The market is now looking for additional stimulus packages for housing and the economy, which could be supportive for the Australian resource sector.

Changes to Stage 3 income tax cuts

The Albanese government proposed changes to the legislated Stage 3 tax cuts (to apply 1 July).

Low-and-middle-income earners (<$150k) would receive a bigger tax cut at the expense of higher-income earners (>$150k).

The rationale is that the post-Covid inflation crisis and cost-of-living pressures facing lower earners requires changes to the original package which was designed and legislated in 2019.

The changes are designed to be budget-neutral, but could be more stimulatory since lower-income earners may be more likely to spend additional disposable income. There is also focus on the political backlash, with the federal opposition continuing intense criticism of Albanese for breaking repeated promises that he would proceed with the original plan.

Australian inflation and policy

There is potential for a Reserve Bank pivot at its February 6 meeting. Recent communications indicate policy is already tight enough.

Past cycles suggest risks are skewed towards rate cuts earlier than the current market expectations.

Q4 CPI data due out on Wednesday will be important.

If the trimmed mean CPI reading is well below RBA expectations of 1% quarter-on-quarter, the RBA could revise down its forecasts for inflation to be within the 2-3% target range by the end of this year (rather than late 2025).

Lower travel and accommodation charges and lower fuel prices could all help the inflation picture.

Historical revisions to RBA forecasts have been big at times, so this has the potential to surprise on the downside in February – though the revisions will depend partly on the Q4 CPI outcome.

Recent data provides clearer signs of a softening labour market. While the unemployment rate remains low, its increase in recent months is larger than at the start of most RBA rate-cutting cycles.

The market now expects the RBA to cut rates twice later in 2024, bringing the cash rate down from a 12-year high of 4.35% to 3.85%.

Headline inflation is expected to only touch the upper end of the RBA’s target 2-3% band in Q1 2025. The RBA is likely to be the last central bank in the “dollar-bloc” countries to join the global easing cycle.

Australia’s property market has now fully recovered from the 2022 downturn, according to data from real estate website Domain.

Sydney, Brisbane, Adelaide and Perth have reaching new house price peaks, returning to pandemic-boom highs, Domain reports.

Demand is strong, but the country has a housing supply problem, with no near-term solution from rate changes.

That said, there are signs that student visa growth has peaked and is moderating. This may help ease population and housing pressures at the margin.

Markets

ASX 200 aggregate earnings are forecast to fall this year, largely due to softer resource and bank sectors.

Industrials are expected to be positive, providing some offset.

At this point the market seems quite happy to look through the earnings valley this year and seems prepared to pay higher valuations for banks (which are up 2.97% CYTD versus -0.53% for the S&P/ASX 300).

The S&P/ASX 300 Resources index gained 3.47% last week on improved sentiment around China, but remains down 4.6% so far this year.

About Crispin Murray and Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia. Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions.

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

Here are the main factors driving the ASX this week, according to Pendal’s head of equities CRISPIN MURRAY. Reported by investment specialist Chris Adams

- Find out about Pendal Focus Australian Share fund

- Crispin Murray: Five key questions for 2024 (and how we’re going so far)

US equities (S&P 500) gained 1.19% last week and reached a new all-time high – 106 weeks after the previous peak on 7 January 2022.

This happened against a rising US Dollar, an escalation in Red Sea tensions, and despite bond yields rising as Fed Governor Christopher Waller tried to cool the market’s view on the pace of rate cuts.

A combination of positive US economic news, confidence on inflation, and cash on the sidelines beginning to chase the market were behind the move higher.

US corporate earnings season has been solid so far, with some small signs of hope from the regional banks and indications that the consumer is holding up okay.

The Australian market (S&P/ASX 300) was softer, down 1.05%, as sentiment on China continues to wane and drag on the resources sector.

Inflation

There was little incremental information on the inflation front.

The latest Expected Change in Inflation survey from the University of Michigan fell from 2.9% in November to 2.8% on a five-year view in December.

This is constructive in terms of expectations around wages and is at the lower end of the post-pandemic period, but is still above the average pre-Covid level of 2.5%.

The market is aware of the effects that Red Sea disruptions are having on freight rates as well as oil and gas prices, but it is not yet affecting bond yields.

This is probably because the impact has been mainly to Europe-Asia shipping routes.

That said, there is now some spill-over apparent in US-China routes, but the upcoming Chinese New Year may be exacerbating this.

Deflation in Chinese export prices is also acting as an offset.

Business and consumers are not yet showing any concern around the ability to access products, so we don’t see the hoarding noted during the pandemic – however, an escalation of the crisis could shift that sentiment.

Elsewhere, the Consumer Price Index (CPI) in the UK was worse than expected.

This is a reminder that the pathway to deflation may be rockier, even though the main cause was volatile components such as air fares, which are expected to reverse.

In addition, underlying economic data is soft (e.g. retail sales), suggesting inflation pressures should be easing.

Growth

Most recent signals support the view that the economy ended 2023 well and that it is not in recession.

US December headline and core retail sales were solid at 0.6% month-on-month, which is stronger than expected and reinforces the anecdotal evidence that Christmas spending picked up.

The overall trend implies real consumer spending was up 2.3% in Q4 2023, which also implies the economy is holding up.

The University of Michigan Consumer Sentiment indicator rose much more than expected, up 9.1 to 78.8.

This is the largest rise since 2005, though the overall level remains subdued.

Forward expectations of sentiment also rose; falling fuel prices and rising stock prices probably played a large role in this.

Initial Unemployment claims declined 16,000 to 187,000, indicating the labour market is holding up.

December housing starts were also stronger than expected, only falling 4.3% from November in what is traditionally a weak month.

New housing permits rose 1.9%, indicating more optimism over future demand.

Multifamily units under construction have risen to record levels, which is supportive to economic activity but also means supply should help ease pressure on rents – supporting lower inflation.

Policy

Fed Governor Waller dampened expectations on the potential scale of rate cuts for 2024.

He put a lot of store on the next CPI report, as it will incorporate seasonal adjustment revisions for 2023 which may change the rate of disinflation.

This suggests that the March meeting is “live” for a cut.

Waller reiterated his perspective that rates can fall to ensure real rates do not rise as inflation falls, but he also saw ‘no reason to move as quickly or cut as rapidly as in the past’, which reflects the starting point being one where the economy is holding up better than in previous cycles.

He also indicated no rush to slow quantitative tightening.

Bond yields rose in response, as Waller is one of the governors who triggered the shift in sentiment on rates last year.

The European Central Bank’s Christine Lagarde also reiterated the message that rates won’t be cut until the summer, with the market anticipating April as an option.

She also noted that “the risk would be worse if we went too fast and had to come back to more tightening,” highlighting central bank reticence on declaring victory over inflation too early.

One big positive for Europe is that winter has been mild and gas prices have fallen sharply, which translates into lower power prices.

Geopolitics

The Red Sea remains the most immediate issue in terms of the knock-on effects on inflation.

But elsewhere, Trump won big in Iowa – with neither Haley nor De Santis emerging as clear alternatives.

The latter subsequently withdrew from the nomination process, which places considerable importance on the New Hampshire Primary on 23 January.

It is an opportunity for Haley, as independents are able to vote; if she can run close, that will potentially give her momentum for her home state of South Carolina on 3 February.

Should she fail, however, the race could be over before Super Tuesday on 5 March.

China

A raft of data for 2023 was released last week.

Q4 GDP came in at 5.2% growth year-on-year, lower than the 5.3% expected (and having grown 3.0% in 2022).

Interestingly, the GDP deflator was -0.5%, which is the largest fall since 1998-99.

This means Chinese economy grew less than the US in nominal terms (the latter growing 4.8%) and actually declined in US Dollar terms.

Given the weakness in Q4 2022, this reinforces how subdued the Chinese economy remains.

The negative inflation and Producer Price Index highlight how the economy is being driven by the supply side, while underlying consumer demand remains weak for structural reasons.

Growth of 6.8% in industrial production and 4.0% in fixed-asset investment for the twelve months ending December 2023 was better than expected – however, retail sales were weaker at 7.4% (versus 8.0% consensus).

The property sector remains soft, with property investment falling 12.3% year-on-year (worse than the -10.9% expected and having already fallen 10% in 2022).

New home sales fell 12.7%, while the value of new home sales fell 17%.

New home completions actually rose 15.4% for the year, due partly to lagged effects and the efforts made to finish projects that were tied up with funding issues.

Unemployment rose to 5.1%.

The National Bureau of Statistics also released a new youth unemployment figure, which excludes those at university and school – this came in at 14.9% versus 21.3% in the old measure.

There were 9.02 million new births in 2023, according to official data, which was more than the market expected but which still means the overall population fell marginally.

The current lack of confidence in the Chinese economy can be seen in stock market weakness and in bond yields falling to cycle lows.

Expectations for 2024 GDP growth currently lie around 4.5%, with piecemeal stimulus propping up growth and an emphasis on infrastructure investment, which should support commodity demand.

Australia

December employment data was weaker than expected, with jobs falling 65,000 versus market expectations of a 15,000 rise, though November was revised up to 73,000.

The three-month run rate has stepped down from 30,000-40,000 to 15,000-20,000 per month and year-on-year employment growth is 2.8%.

Full-time roles fell 107,000 and part-time roles rose 41,000, while hours worked fell 0.5% month-on-month and landed at +1.2% year-on-year – the slowest since March 2022.

Unemployment was flat at 3.9%, as the participation rate fell back from a record high of 67.3% to 66.8%.

All of this indicates the economy is cooling and helped support the market’s view that rates have peaked.

Markets

The S&P 500 market broke to a new all-time high, clearing the peak we saw on 7 January 2022.

This came on option expiry day, which released the gamma overhang in the market, and had been flagged by some bears as a point where the market could roll over.

It was interesting that this occurred despite a higher move in bond yields, and suggests that there is still some scepticism on the economy reflected in positioning.

The early phase of US earnings season has been in line with normal experience, with about half of the companies reporting beating expectations so far.

Earnings revisions remain on track for a 3% uptick year-on-year.

The ASX was weaker due to continued challenges in resources due to softer commodity prices and poor sentiment on China.

We have begun to see more deferrals in mine developments, reflecting cost pressures, and weakness in base metal and lithium prices.

Growth stocks outperformed despite bonds rising, reflecting improving sentiment on the underlying economic outlook.

About Crispin Murray and Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia. Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions.

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

Where are we on inflation at the start of 2024? And how is Pendal’s team positioned? Here’s a quick overview from our head of government bond strategies TIM HEXT

- Inflation on track in the US

- Australian inflation still above target

- Why bonds, why now? Pendal’s income and fixed interest experts explain

- Browse Pendal’s fixed interest funds

WELCOME back to those returning from a summer break.

If you’ve been off since mid-December you could be forgiven for thinking nothing happened — since bond rates are largely unchanged.

Though there was some year-end excitement as the “everything rally” pushed yields lower and risk markets higher.

A notion of lower inflation potentially allowing US rate cuts seemed to change into a stronger narrative of imminent big cuts.

The new year has now sorted that one out.

Inflation outlook in the US

As always, the main market driver in 2024 will be inflation. Here’s a brief insight into where we are now.

I will talk more about the current pulse than just annual rates — since annual rates are quite backward-looking and take longer to reflect current conditions.

In the US the Fed’s preferred inflation measure is the core PCE (personal consumption expenditure) price index. This excludes food and energy.

The Fed prefers this measure over CPI because it better reflects changes in consumer spending — instead of relying on fixed weights that only change periodically.

Find out about

Pendal’s Income and Fixed Interest funds

It also relies on business surveys which are more reliable than consumer surveys. And it has less exposure to rents (CPI includes the notion of owner-equivalent rents, which makes up 25% of the basket).

The good news is that in the US core PCE pulse is now running at 2%.

In other words Q4 — similar to Q3 (see below) — is expected to show the three-month annualised core PCE at 2%. That’s bang on the Fed target.

It was 5% in Q1 and 3.7% in Q2.

The main reason for this move is falling margins, as now fully-open goods and services markets see businesses become more competitive again.

The final impact of the pandemic is washing through the system.

US core CPI is now moving between 0.2% and 0.3% per month, indicative of a 3% annual rate.

This should also settle lower as leading indicators on rents suggest lower levels ahead.

Inflation Outlook – Australia

Australia’s fourth-quarter CPI will be released on January 31.

Thanks to monthly data we already know roughly two-thirds of the number. Expectations are for a 0.7% headline and 0.8% underlying quarterly outcome.

Three-month annualised this would see inflation near 3% as well, though rents in Australia are unlikely to provide the same relief as in the US.

Electricity subsidies (if and when they come off) are an added uncertainty in Australia. These softened the 20% price hikes down to only 10% in recent CPI numbers.

The hope is that falling wholesale prices might offset any removal of subsidies.

The RBA forecast of 3.5% inflation by mid-2024 looks reasonable.

Unlike the US, this would leave inflation still 1% above target, making the case for rate cuts more difficult.

But if inflation can stabilise closer to 3% in the medium term — as the current pulse suggests — then the need for tight monetary policy would lessen.

The hope would be wage outcomes could then moderate from the current 4% levels.

Portfolio positioning

Growth, labour markets, geopolitical events and the usual mix of factors will, as always, be in play in 2024.

For bond markets though, inflation outcomes are now on the “good news” side of the ledger for the first time since Covid.

We are running our portfolios from the long-duration side, though adjusting positions depending on market levels and probabilities of cuts priced into markets.

It also makes us favourably disposed to risk markets.

Though we note — and caution — that the long and variable lags of monetary policy will see a slower economy and more pressure on earnings than in 2023.

About Tim Hext and Pendal’s Income & Fixed Interest boutique

Tim Hext is a Pendal portfolio manager and head of government bond strategies in our Income and Fixed Interest team.

Tim has extensive experience in banking, financial markets and funding including senior positions with NSW Treasury Corporation (TCorp), Westpac Treasury, Commonwealth Bank of Australia, Deutsche Bank, Bain & Co and Swiss Bank Corporation.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia.

Find out more about Pendal’s fixed interest strategies here

About Pendal

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

In 2023, Pendal became part of Perpetual Limited (ASX:PPT), bringing together two of Australia’s most respected active asset management brands to create a global leader in multi-boutique asset management with autonomous, world-class investment capabilities and a growing leadership position in ESG.

Here are the main factors driving the ASX this week, according to Pendal’s head of equities CRISPIN MURRAY. Reported by investment specialist Chris Adams

- Find out about Pendal Focus Australian Share fund

- Pendal’s Crispin Murray reviews the lessons from 2023 and outlook for 2024

MARKETS kicked off the year with a small sell-off, catching their breath from the November-December rally, before staging positive returns last week.

The S&P/ASX 300 rose 0.14% and the S&P 500 1.79%.

To recap 2023:

- The ASX rose 12%, with tech (+28%) and consumer discretionary (+21%) the lead sectors. Consumer staples (+1%), utilities (+3%), healthcare (+4%) and energy (+5%) all lagged

- Globally, the US rose 26%, Europe lifted 26% and Japan gained 29%

- US 10-yr Treasury yields ended up flat for the year at 3.88%, having peaked at 5.02% in October

- The AUD was flat and the DXY (a trade-weighted measure of the USD) fell 2%

- Iron ore rose 22%, gold increased 13% and copper lifted 2%, while oil fell 10% and lithium dropped around 80%

Markets start 2024 with a positive view that disinflation is proceeding faster than previously expected, growth will hold up, and the Fed has reinstated the “Fed put”.

Investors are positioned for this with a systematic strategies limit long in equities.

However, there is still a lot of cash on the sidelines, which may be squeezed into equities.

The breadth of the market is improving, which is usually a positive signal.

The liquidity environment is constructive in the near term, with reverse repurchase agreements (or repos) continuing to be drawn down and a limit on Treasury issuance. Both these factors are likely to reverse after Q1, however.

On the data front last week, we saw slightly negative US Consumer Price Index (CPI) data brushed off by the market.

The Producer Price Index (or PPI) was more positive, while jobless claims data indicated that the economy is holding up fine.

In Australia, inflation data was marginally positive.

We also saw conflicting signals from Fed speakers on the potential for quantitative tightening to be re-evaluated, but there is a growing suspicion this will occur to offset a tightening of liquidity in H2.

Middle East tensions escalated, with the US and UK both launching attacks on the Houthis in Yemen.

This had no sustained effect on oil prices, but freight rates have risen on the need to redirect shipping, which represents a risk to the disinflationary growth narrative.

The market continues to price for six-and-a-half interest rate cuts in the US, starting in March.

Current implied expectations are that the ECB and Bank of England will both start cutting in April and May, respectively.

The market is only pricing two cuts for Australia in 2024, the first occurring between June and August.

Five key questions for 2024

In our last note of 2023 we highlighted some key questions for markets in 2024. We can now assess these in light of recent data and developments:

1. Will disinflation continue to surprise to the upside?

Recent data has been mixed but is supportive of the market’s belief that disinflation will facilitate rate cuts.

US December CPI came in a bit stronger than expected, with the headline index up 0.3% month-on-month – driven, in part, by electricity prices.

However, there was sufficient ambiguity for markets to largely brush off the reading.

Looking forward, the continued drop in fuel prices and rents should help the headline CPI continue to fall.

Core CPI rose 0.31% month-on-month.

The Goods component was flat month-on-month following six months of decline.

The question is whether this signals an end to goods deflation, which has played an important role in positive inflation surprises.

New and used car prices rose, which may not be sustainable.

The recent weakening of the USD and the issues in the Red Sea may also be factors which could lead to an end of goods price deflation, so this remains an issue to watch.

Core Services ex-rents rose 0.4% month-on-month.

This, too, was higher than expected – driven by recreation services, airfares and medical services.

Airfare increases has been seen by a number of inflation bulls as unsustainable, partly due to fuel costs coming down.

These categories are also measured differently in the core Personal Consumption Expenditure (PCE) measure that the Fed prefers.

As a result, the market has not changed its expectations for the December PCE reading, which is that the three-month annualised Core reading could drop to 2.0%.

US PPI came in below expectations at -0.1% month-on-month and 1.0% year-on-year, making this three negative readings in a row.

Some inflation bulls have also cited the potential for more competition to drive corporate profits margins lower.

These rose substantially though the pandemic, and while they are no longer rising, they have not yet normalised.

While this is good for the rate outlook, it would be negative for corporate profitability.

One countersignal is wages data, which is proving to be more stubborn; the Atlanta Fed twelve-month wage tracker held at 5.2% in early January.

The market has priced a 65% probability of a March rate cut in the US, with 165bps of easing expected for the year.

European inflation was in line with the ECB forecast, but higher than consensus expectations (headline 2.9% and core 3.4%).

This may delay the first rate cut in Europe until May or June.

We note that Europe has experienced another warmer winter so far and gas prices have come in well below the assumptions made by the ECB.

2. Will the US economy continue to grow?

This question, alongside the first, is likely to drive the outlook for rates and corporate earnings.

US jobless claims have remained very benign, with initial applications near historic low levels and continuing to hold flat.

This reiterates constructive employment data from the week before and helps underpin the economy.

Anecdotes from retailers indicate there was a late surge in Christmas spending, which held up well overall as a result.

Early January sales are on the soft side, although this may be weather-related.

The consensus expectation is 0.7% GDP growth in 2024, but the upside risk comes from higher consumer demand – benefiting from real disposable income growth combined with the support from an easing of financial conditions.

If the Fed is comfortable with inflation, then it does not need to force the economy into sub-trend growth levels.

Some estimates suggest the potential impact of easier financial conditions could go from a GDP headwind to potentially adding 0.5% to growth.

3. The impact of geopolitics and elections

Threats to shipping via the Red Sea have seen a dramatic decline in traffic, with companies opting for the longer path around Africa.

This effectively reduces supply and impacts freight rates and has raised some concerns about the flow-on effect to the price of goods and the risk of slowing the rate of disinflation.

That said, the trade between Europe and Asia is most heavily affected, with a more limited impact on US routes.

There has also been a material increase in shipping capacity post-pandemic, so the impact will be far more muted than what we saw during Covid.

In Taiwan, the Democratic Progressive Party candidate Lai Ching-te won the party’s third consecutive Presidential term, as expected.

However, the party won 51 of 113 parliamentary seats and lost its majority for the first time since 2012 (again, expected, and unlikely to move the status quo in terms of the level of tensions).

4. China’s ability to sustain moderate growth

Real-time indicators suggest the Chinese economy has started the year softer.

Consumers continue to lack confidence, with the gap between retail sales growth and the pre-Covid trend continuing to widen.

This is tied to weak property market.

Inflation data also remains weak, which leaves scope for continued policy stimulus driven by a supportive fiscal situation.

5. Australia’s ability to engineer its own soft landing

Australian monthly CPI for November was lower than market expectations, up 0.33% month-on-month and 4.3% year-on-year (down from 4.85%).

Core inflation was also lower, up 0.25% month-on-month and 4.77% year-on-year (down from 5.05%).

Housing was the main contributor to inflation for the month, along with rents and new dwellings.

Electricity prices rose to a lesser degree, helped by new Victorian government subsidies.

Services inflation rose 0.7% month-on-month to 4.71%, after a similar fall the previous month.

The three-month trend is now 3.6%.

Goods rose 0.16% to 3.95%, held down by lower fuel, clothing and recreational equipment, with food higher.

December data should see another step down as the base effects fall out, fuel prices are lower, and Western Australian power subsidies kick in.

Last week, the December Politburo meeting and the Central Economic Work Conference took place, where key economic targets are set (but not announced until March).

Signals were for policy support focused on fiscal policy, though there were no major initiatives which was seen as slightly disappointing.

Australia

Employment data was much stronger than expected (up 61,500) despite a marginal rise in unemployment (to 3.9%) given the continued rise in labour supply.

Total hours worked were flat, which implies average hours worked was lower.

This indicates that businesses are looking to save costs by lowering hours rather than layoffs – possibly due to the difficulty of rehiring in the past.

Forward indicators on unemployment still indicate it should be set to rise further, though these signals have so far not been validated.

Markets

The Fed cutting rates is not necessarily a green light for equity markets, as in the end, the economy gets the final say.

If a recession were to occur, the de-rating of earnings would overwhelm the benefits that the lower rates would bring.

This is why GDP growth next year is key.

We are also seeing some interesting shifts in market internals on the back of this. Notably, mega-caps have done their dash and market breadth is rising.

This can be tracked in the relative performance of the Russell 2000 vs the S&P 500.

For small-caps, this is a particularly positive signal for them to outperform.

Another interesting disconnect is that the market has a very different perspective on the economy than some of the traditional leading indicators of growth, shown by the rotation away from defensives to cyclicals.

This makes early 2024 interesting, as the cyclicals would be sensitive to any weak growth.

In Australia, the ASX saw a broad-based rally with only utilities underperforming.

Rate-sensitive sectors such as REITs and tech led the market.

Energy was supported by the bounce in oil and the continued fallout of the potential STO-WDS merger.

Lithium stocks also had a strong bounce back given how oversold they have become.

Lastly, this environment looks to be positive for the AUD, which continues to look good technically.

About Crispin Murray and Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia. Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions.

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

The US election will take the spotlight, but EM investors need to keep tabs on dozens of other national polls this year. Here’s an overview from Pendal’s Emerging Markets team

- Elections to come in India, Indonesia, South Africa and Mexico

- Global geopolitics will significantly impact emerging markets

- Find out about Pendal Global Emerging Markets Opportunities fund

THIS is the biggest election year in history, with half the planet’s population due to elect a national leader.

More than 50 countries will hold national elections in 2024 – including many emerging markets.

“2024 has the highest concentration of elections, possibly in modern history,” says Paul Wimborne, co-manager of Pendal Global Emerging Markets Opportunities fund.

“And emerging markets are very much part of this line up. There has already been presidential elections in Taiwan and later in the year there will be elections in India, Indonesia, South Africa and Mexico.

Those countries represent 40 per cent of the MSCI Emerging Markets Index by weight and 1.9 billion people.

Investors will need to consider the ramifications of elections with the potential to affect the global macro environment that matters so much to emerging equity markets.

We’ve already seen the re-election of Taiwan’s pro-sovereignty Democratic Progressive Party draw the ire of Beijing.

Find out about

Pendal Global Emerging Markets Opportunities Fund

Financial markets continue to be directly impacted by sanctions on China; the impact of Russia’s invasion of Ukraine on commodity prices and trade; and an evolving set of overlapping conflicts in the Middle East and Red Sea.

Here’s a quick look at the elections that will affect EM investors:

Taiwan (Jan 13)

The Taiwanese election, held in mid-January, was won by Willian Lai Ching-te from the governing Democratic Progressive Party (DPP).

It’s the first time the same party has won a third Presidential term since direct elections were introduced in 1986.

“DPP is the more pro-independence of Taiwan’s main parties and it received just over 40 per cent of the vote,” Wimborne says.

“Taiwan also had a legislative election where the KMT, a more pro-Beijing party, won 52 seats out of 130. DPP won 51 seats. It means the winning President doesn’t have a legislative majority.”

For emerging market investors, an election like Taiwan’s is crucial in understanding where opportunities, and risks, lie.

“In Taiwan’s case, the President does not have a clear mandate, so that really suggests a status quo outcome.

“Clearly the election is very important from a geopolitical point of view with the relationship between the country and China the key issue.

“For investors, the holding of the election reduces the short-term uncertainty because we know what the outcome is.

“And it also tells us in the medium term, the cross-strait tension between Taiwan and China is probably here to stay.”

India (April-May) and Mexico (June 2)

Investors in emerging markets worry mostly about unexpected results which could move equities, bonds, property markets, currencies and other asset classes, Wimborne says.

“In India, there is an election in the next couple of months. The market has priced in continuity, and it would be a shock of Narendra Modi doesn’t win.

“In Mexico, the market is assuming the most likely result is the current incumbent AMLO’s (Andres Manuel Lopez Obrador) preferred candidate will win, and his party will retain power.

AMLO, having served a single six-year term, is unable to run again.

Russia (March 15-17)

March brings the presidential election in Russia.

The last election in 2018 is widely thought of as neither free nor fair. Incumbent Vladimir Putin received 77.5% of the vote then, and the political system in Russia has become intensely more repressive since.

Economic strain is substantial. Many Russians have seen their ambitions destroyed and the country may have taken more than 100,000 casualties so far in its invasion of Ukraine.

A Putin victory has to be the expectation, but there is the possibility of protests and crackdowns that may alter Russian policy.

Venezuela (sometime in 2024)

Similarly, the first half of the year should see a presidential election in Venezuela. Like Russia, the country is in no meaningful sense a democracy.

The leading opposition candidate Maria Corina Machado was barred from politics in June 2023 – so a victory for the governing coalition (probably for the incumbent Nicolás Maduro) has to be the expectation.

In the run-up to the election, Venezuela has made claims on almost all of the territory of neighbouring Guyana, with possible military action backed by Iran, Russia and China.

This would lead to a substantial worsening of global geopolitics with varying potential outcomes.

Israel

While Israel does not have an election scheduled, the current emergency government formed after the Hamas attacks in October 2023 may not last throughout 2024.

The country has undergone five elections between 2019 and 2022 in search of a viable coalition.

A snap election could lead to anything from a mandate to negotiate a political settlement to the current crisis to a shift to an even more overtly nationalist government that would deepen the conflict with both the Palestinians and with Israel’s neighbours.

United States (Nov 5)

The greatest ‘unknown’ in this election year for emerging markets is the United States.

“The US election is the one that has the potential to cause most uncertainty across emerging markets,” Wimborne says.

“It’s difficult to predict who is going to win — and then it’s also difficult to predict what policies would be, particularly if Trump wins.

“What would US policy be in terms of geopolitics and domestic priorities, as well as what that means for interest rates and the US dollar?”

UN Security Council (mid-2024)

In addition to these national polls, five non-permanent members of the UN Security Council are due to elected in mid-2024.

Although most of the power sits with the five permanent members (who have vetos), it is here where any attempts to resolve these conflicts will start.

Among the countries likely to be elected are Pakistan and Somalia.

Pakistan is close to China and Iran and in dispute with India. Somalia is in a dispute with Ethiopia which has the potential to further worsen the geopolitics of the Red Sea region.

Global geopolitics are fraught as we go into 2024 and all these elections have the potential to lead to a substantially better or worse world.

Investors will need to follow them closely and react accordingly.

Portfolio implications

For investors, all this uncertainty means they must stick to their strategies and processes, says Wimborne.

“Stick to your game plan and then react to changes if the outcomes aren’t as the market predicted.

“You need to build a resilient portfolio and know where the risks are being taken.

“Look at the portfolio as a whole and understand what would happen if the oil price moves or bond yields change, or currencies move.

“Have a cohesive portfolio where you understand the risks, and when the facts change, respond in the appropriate way.”

About Pendal Global Emerging Markets Opportunities Fund

James Syme, Paul Wimborne and Ada Chan are co-managers of Pendal’s Global Emerging Markets Opportunities Fund.

The fund aims to add value through a combination of country allocation and individual stock selection.

The country allocation process is based on analysis of a country’s economic growth, monetary policy, market liquidity, currency, governance/politics and equity market valuation.

The stock selection process focuses on buying quality growth stocks at attractive valuations.

Find out more about Pendal Global Emerging Markets Opportunities Fund here

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

Here are the main factors driving the ASX this week, according to Pendal’s head of equities CRISPIN MURRAY. Reported by investment specialist Jonathan Choong

- Find out about Pendal Focus Australian Share fund

- Pendal’s Crispin Murray reviews the lessons from 2023 and outlook for 2024

THERE was nothing to de-rail the market’s bullishness last week, after the US Federal Reserve signalled its inflation mission had been accomplished.

The reaction was very positive with the S&P 500 up 2.5%, now 25% higher year-to-date.

US yields also fell by 30 basis points (bps) and have now ended up where they started at the beginning of the year.

Market price action is positive, with breadth widening and momentum indicators breaking higher and indicating the pathway to moderate growth and falling rates (ie a soft landing) is in sight.

Near-term consolidation will likely occur in the short term before another move higher into the start of 2024, which bodes well for risk assets.

In addition, last week we saw mildly positive inflation data on a net basis, with US economic data supportive of no imminent recession.

In Europe, the ECB and BoE both took a more cautious stance on the prospect of rate cuts – with the former struggling with weak economic data and the latter more understandable given England’s inflation.

China’s policy meetings were mildly disappointing. There were no strong policy signals, but the background message appears to be that fiscal stimulus would continue to be used to prop up growth.

The S&P/ASX 300 was up 3.5% for the week. The Australian economy continued to signal that things were better than sentiment suggested with a strong employment report.

This was reflected in a break higher in the Australian dollar to more than 67 cents.

Economics and policy

Inflation data came in as expected and continues to trend downward on a net basis.

In November, US CPI was higher at 0.1% month-on-month and 3.1% year-on-year.

Core CPI was firmer at 0.28% month-on-month and 4% year-on year.

There was a bit for the bulls and bears – with core goods seeing material disinflation despite a strong auto inflation component, which should unwind.

The service component was not quite as favourable, with rent growth remaining higher than expected. This is somewhat discounted, as more real-time measures of rents are now flat year-on-year.

Core services ex-OER (Owner’s Equivalent Rent) and rent also saw a small re-acceleration over a three-month period.

Medical services and health insurance were the main drivers in this underlying core services pick-up, but it should be noted that these services are known to lag the most – suggesting that inflation is not, in fact, rebuilding.

This will make the next PCE print (the Fed’s preferred measure for inflation) important, as we are seeing a divergence here from the CPI.

We also saw weaker PPI data in the US, and Michigan inflation expectations also fell back down.

In other US economic news retail sales bounced back, up 0.3% versus expectations, though negative revisions reduced part of this.

The underlying trend looks to be around 2.5% growth, which is consistent with the outlook for a soft landing. This means the overall inflation trend is still supportive for the Fed to shift its policy signal, with the headline target of 2% now plausible.

The Fed

In its meeting, the Fed clearly shifted its policy bias.

The market was initially wary that Chairman Jerome Powell would seek to settle things down given a fall in financial conditions since he spoke, and a warning from Fed member Christopher Waller.

But we got a set of dovish signals:

- The dot-plots signalled a move from two to three expected cuts in 2024

- Powell noted there had been discussions on how long to keep rates on hold before cutting. This was expected to be a topic for a more detailed discussion going forward

- Powell noted good progress on inflation, including core and core services

- He also talked about the risk of over-tightening. This was an important shift, relating to the central bank’s desire to avoid having to cut rates too far this cycle

- When pushed about the current easing of financial conditions, Powell did not use the opportunity to diffuse the reaction.

All up, the meeting was taken as a green light for markets.

The following day, Fed member John Williams of New York did try to diffuse the message – particularly given the move to March cuts by the market. But it was met with little reaction since the market believed the data would support a cut then.

The market is now expecting six rate cuts in 2024.

There is a concern from some that the Fed has been too dovish, which may prevent a proper slowdown – resulting in a resurgence of inflation.

European Central Bank

President Christine Lagarde took a more cautious stance than Powell, repeating her message of no cuts in the first half of the calendar year, but her message was largely ignored given the perceived weakness across Europe.

She said the ECB had not discussed the timing of cuts, though the market has been pricing in 150 bps of rate cuts in 2024.

China

November data looked better year-on-year.

For example, retail sales were up about 10%, though they have been weak sequentially.

The outlook remains consistent. GDP growth is steady in the low fives for 2023 and the market expects this slowing between 4.5% and 4.8% in 2024.

Last week, the December Politburo meeting and the Central Economic Work Conference took place, where key economic targets are set (but not announced until March).

Signals were for policy support focused on fiscal policy, though there were no major initiatives which was seen as slightly disappointing.

Australia

Employment data was much stronger than expected (up 61,500) despite a marginal rise in unemployment (to 3.9%) given the continued rise in labour supply.

Total hours worked were flat, which implies average hours worked was lower.

This indicates that businesses are looking to save costs by lowering hours rather than layoffs – possibly due to the difficulty of rehiring in the past.

Forward indicators on unemployment still indicate it should be set to rise further, though these signals have so far not been validated.

Markets

The Fed cutting rates is not necessarily a green light for equity markets, as in the end, the economy gets the final say.

If a recession were to occur, the de-rating of earnings would overwhelm the benefits that the lower rates would bring.

This is why GDP growth next year is key.

We are also seeing some interesting shifts in market internals on the back of this. Notably, mega-caps have done their dash and market breadth is rising.

This can be tracked in the relative performance of the Russell 2000 vs the S&P 500.

For small-caps, this is a particularly positive signal for them to outperform.

Another interesting disconnect is that the market has a very different perspective on the economy than some of the traditional leading indicators of growth, shown by the rotation away from defensives to cyclicals.

This makes early 2024 interesting, as the cyclicals would be sensitive to any weak growth.

In Australia, the ASX saw a broad-based rally with only utilities underperforming.

Rate-sensitive sectors such as REITs and tech led the market.

Energy was supported by the bounce in oil and the continued fallout of the potential STO-WDS merger.

Lithium stocks also had a strong bounce back given how oversold they have become.

Lastly, this environment looks to be positive for the AUD, which continues to look good technically.

About Crispin Murray and Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia. Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions.

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

What did investors learn in 2023? What are the main issues facing us in 2024? Here’s an overview from Pendal’s head of equities CRISPIN MURRAY

- Find out about Pendal Focus Australian Share fund

- Fixed income: Pendal’s 2024 outlook for bonds, credit and cash

2023 year in review

EACH year Pendal’s head of equities Crispin Murray outlines the major factors that will affect investors in the coming 12 months.

Here Crispin reviews the big issues of 2023 and how they played out.

Further down he outlines the major factors for 2024.

1. Inflation persistence and tightening of financial conditions

Inflation fell faster than hoped in 2023 and key exogenous factors such as oil broke the right way.

Core inflation looks set to fall below 3% by the end of 2023 — and is within striking distance of the RBA’s 2% target.

This has been achieved without the need for a more severe economic slowdown.

2. Scale of US versus domestic economic slowdown

Wages – one of the lead indicators of underlying inflation – fell in 2023 without the need for materially higher unemployment.

This was because job openings shrank quickly and participation rates increased.

One hypothesis is that those holding back from labour markets stepped back in as excess savings were deployed alongside higher immigration.

Meanwhile job openings shifted down as firms worked through post-pandemic shortages.

3. Earnings leverage to downturn

No downturn meant no leverage came through. US earnings per share (excluding energy) is forecast to rise 4%, while the 2024 forecast is around 5%.

4. Did markets price in an economic downturn?

This proved to be important. Sentiment and positioning were very negative at the start of the year.

Therefore, the impact of the economy growing with inflation falling was exaggerated. US markets are up some 25 per cent year-to-date.

5. China’s economic performance as it exits zero-Covid

This disappointed after a promising first quarter. A lack of recovery in the property sector continued to impact consumer confidence.

Contrarily, this probably helped global equities. With stimulus helping steel and iron markets, oil demand was not squeezed too much and contributed to a more benign inflation outcome.

6. Could the RBA engineer a soft landing in Australia?

Australia saw stronger-than-expected growth in 2023. The mortgage cliff has – to date – been navigated through higher immigration, an ability to work more hours, higher wages, more excess savings, and supportive fiscal policy.

Inflation remains a bigger issue in Australia than the US and Europe, so the RBA cannot yet declare victory.

Key questions for 2024

Let’s now look forward. Here are the questions to consider in 2024:

1. Where is the strength in the US economy?

Will the monetary-tightening lags eventually flow through and trigger a much-anticipated recession?

Or will the easing of financial conditions, combined with rising real wages and more fiscal support, help drive growth?

Consensus GDP is 0.7% growth while the Fed is indicating 1.4%. A US recession will knock earnings estimates and be negative for markets.

2. What happens to inflation?

Markets are focused on the challenge of the last mile – ie getting from 3% to 2% inflation.

The Fed acknowledges this may be tough, but to date it hasn’t been the case. The quicker this progresses, the more rate cuts we should get in the US. In turn, this is likely to drive PEs higher.

There is also a counter thesis. In this scenario the Fed repeats the mistakes of the Burns Fed, reading too much into shorter-term lower inflation, only to see inflation re-accelerate as growth holds up.

This would likely force the Fed to shift back towards a more hawkish stance – a clear negative for markets.

3. How will the US election (and others) impact markets?

The 2024 US presidential election is already billed as the most unpredictable and important for decades.

There remain questions as to whether Biden or Trump end up running, or whether a credible independent could impact the outcome.

There is a scenario where no one achieves the required majority in the electoral college.

With so many unknowns there is one conclusion we can draw. The Biden administration will throw everything at ensuring the economic backdrop will be as favourable as possible.

This may extend to the Fed itself and become part of their shift in stance.

We also have elections in Taiwan (Jan 13), UK (May), EU (June 6), India (April), Indonesia (Feb) and Russia (March).

4. What will US rates do?

This is tied to the first three issues. The market has now priced in up to six cuts. Has this gone too far?

5. Will the Chinese economy continue to muddle through?

Will the balance of negative structural issues offset by policy continue to deliver moderate growth with no material surprises? Or will we see structural issues alleviate or deepen?

6. In Australia, can inflation be muted, allowing the RBA to cut rates?

Will the increasing impacts of higher rates begin to squeeze the economy enough to lower inflation?

Or will inflation persist, forcing the RBA into further hikes, running the risk of a faster slowdown?

7. Is the market position becoming too positive?

We are in a very different place when it comes to sentiment and positioning compared to a year ago.

We are more vulnerable to a deterioration in the current benign outlook. But we still have room to rise if the rate cycle plays out as the market now expects.

The issue we resonate with the most is the shift in the Fed’s mindset to underpin the economy rather than build inflation credibility.

Combined with a preparedness to keep using fiscal policy to support growth, this means liquidity and growth are less of a headwind, supporting the market and favouring higher-beta names.

The risk is positioning, which suggest a lot of good news is priced in – making us vulnerable to any inflation surprises.

So, as ever, the market remains unpredictable. This creates opportunity and highlights the importance of thematic positioning.

About Crispin Murray and Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia. Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions.

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

ASX investors have seen a flurry of corporate transactions and associated equity raisings in recent months. Here Pendal equities analyst ANTHONY MORAN explains the opportunities

- Negative reaction to M&A can uncover opportunities

- Orora and Treasury Wine recent examples.

- Find out about Pendal Focus Australian Share fund

NEWSPAPER headlines have been full of merger and acquisition activity and associated capital raisings in recent months.

Chemist Warehouse-Sigma Healthcare. Brookfield-Origin. Newcrest-Newmont. Allkem-Livent. Woodside-Santos.

The activity is likely to continue in 2024, especially in the resources space.

Investors haven’t always been impressed with recent deals – but that doesn’t mean there isn’t opportunity, says Anthony Moran, an analyst with Pendal’s Aussie equities team.

Negative reactions and sell-offs following M&A deals can provide opportunities for investors, says Moran.

“Any deal that is large enough to be raising equity tend to be shareholder destructive in the short term,” he says.

“The market tends to over-react to the downside and that’s understandable because the market doesn’t like diluting the positive investment case for a company.

“M&A introduces a whole new element of uncertainty. There are going to be risks around the businesses being bought, and investors have to learn about them,” he says.

“Also, Australia’s track record of large M&A is extremely weak. It’s just a safer bet that a deal won’t go too well, almost regardless of the details.”

Opportunities from negative reactions

The negative reaction to M&A can provide potential investment opportunities, Anthony explains.

“Market over-reactions around M&A are exacerbated at the moment with fears that the economic cycle is rolling over.”

Investors are concerned that companies are buying businesses that may have puffed up earnings or been trading on a cyclical peak, he says.

“They are worried that the acquiring company has not done enough due diligence and that gives them a reason to sell off the acquiring stock.

“But if you can do the work on the acquired businesses and start to get an understanding and more informed perspective on the probability of the success of a deal, then the sell-off could be quite an attractive investment opportunity.”

Take a long-term view of M&A

Amcor’s purchase of US-based flexible packaging company Bemis in 2019 worked well with significant cost synergies extracted and an improved top line.

But initially, after the deal was announced, Amcor was sold off.

Pendal Focus Australian Share Fund

Now rated at the highest level by Lonsec, Morningstar and Zenith

A similar example was Boral’s 2016 purchase of US-based fly ash producer Headwaters.

Following the announcement of the deal Boral was initially sold-off – then bid up as investors got excited by the potential growth prospects of the Headwaters business.

Ultimately there were few natural synergies between the businesses and as the underlying low quality of the Headwaters business became apparent, Boral underperformed over several years.

It recent months, two ASX-listed companies — both held in Pendal equities funds — have acquired businesses and are now trading on historically low multiples.

“Packaging group Orora (ASX: ORA) bought a France-based specialty premium glass manufacturer that supplies high-end glass bottles for luxury spirits and is a global leader,” Anthony says.

“But investors are worried that post COVID, the growth in luxury spirits, in particular, is rolling over.

There are concerns Orora paid too much, the industry is going to become more competitive and the ESG burden of decarbonising returns will hurt returns,” he says.

Treasury Wine Estate (ASX: TWE) bought a US luxury wine company that has grown quickly in recent years.

Investors are concerned that the growth in earnings will not be sustainable, and that US consumer demand will wane.”

Anthony says that while it is much too early to tell whether the Orora and Treasury purchases are good deals, the kneejerk reaction from markets, selling off the companies, provides an opportunity for investors.

“Take the time to do the work on the underlying assets purchased. Talk to other industry participants and find out how these businesses are positioned, what’s sustaining their returns and what the outlook is.

“And bear in mind that doing the deals haven’t changed the underlying assets in the rest of the businesses.

“The de-rating has hit both the acquisition business and the legacy businesses. That means the legacy businesses have gotten cheaper.”

About Anthony Moran

Anthony Moran is an analyst with more than 15 years of experience covering a range of Australian and international sectors. His sector coverage has included Australian Industrials and Energy, Building Materials, Capital Goods, Engineering & Construction, Transport, Telcos, REITs, Utilities and Infrastructure.

He has previously worked as an equity analyst for AllianceBernstein and Macquarie Group, spending a further two years as a management consultant at Port Jackson Partners and two years as an institutional research sales executive with Deutsche Bank.

Anthony is a CFA Charterholder and holds bachelor’s degrees in Commerce and Law from the University of Sydney.

What lessons can fixed-income investors take from 2023 into 2024? Pendal’s head of income strategies AMY XIE PATRICK summarises the outlook with fellow PMs TIM HEXT, GEORGE BISHAY and STEVE CAMPBELL

- Pendal’s 2024 outlook for bonds, credit and cash

- Why bonds, why now? Pendal’s income and fixed interest experts explain

- Find out about Pendal fixed interest capabilities

I LOVE this time of year. Not only is there plenty of holiday cheer, there is also time to survey the landscape as we head into a new year.

Five key observations that stand out to me from 2023:

- Recession never arrived, though it was widely expected at the start of the year

- Inflation came off without a significant rise in unemployment

- Riskier assets saw healthy returns while bonds had another challenging year

- US 10-year real yields pushed past 2%

- Small and regional US banks have not solved their fundamental problems.

Interestingly in October, when the real yield on 10-year US treasuries tested 2.5%, the bond sell-off halted.

Perhaps the market was saying: “sure, growth is strong now, but the party won’t last forever”.

How we fared in 2023

Pendal’s fixed income team reassessed the situation when we saw the economic data wasn’t weakening.

We identified that, in Australia, the fixed-rate mortgage cliff was a red herring.

George Bishay, our head of credit and sustainable strategies, moved away from a more conservative stance and started to re-risk his credit portfolios.

From banks to utilities, industrials to infrastructure, George has been cherry-picking his way through the primary market since things calmed after the US banking crisis.

“As long as inflation can continue to come down, bond market volatility can be contained,” says George.

“As long as bonds are no longer aggressively selling off, I’m happy to be tactically raising my credit exposures.”

Tim Hext, Pendal’s head of government bond strategies, recognised that just because inflation had peaked, it didn’t mean the fight was over.

While keeping duration positions small during the year, volatility threw up many opportunities in the physical bond space that he was able to take advantage of.

“You can’t ignore the fact that they’ve continued to pump out fiscal stimulus in the US,” says Tim.

“Australian bond markets have been passengers in the US-led sell-off.

“However patient the RBA wants to be, CGLs (Commonwealth Government Loans) couldn’t fight the strong tide of US Treasuries.”

Steve Campbell, our head of cash strategies, has had similar views, but was able to position a little differently in his portfolios.

“The cash funds were predominantly longer than the benchmark over 2023, despite the Reserve Bank continuing to tighten monetary policy,” Steve says.

“The additional yield and the steepness of the curve helped protect the cash funds’ performance from the move higher in yields over the period.”

As Pendal’s head of income strategies, I have the privilege of all this expertise around me.

The income funds benefited from the wisdom of my peers, positioning at first defensively and then risking up on credit.

Positioning long enough in duration earlier in the year in time for the Silicon Valley Bank crisis, then pulling back in to weather the bond storm.

Find out about

Pendal’s Income and Fixed Interest funds

In more defensive moments, Steve made sure extra cash in the income funds kept up with or beat offerings on term deposits – with the added advantage of liquidity.

I’ve enjoyed having that liquidity at my disposal this year. The income funds can take on exposures in Australian equities and emerging markets.

Although both those asset classes generated positive returns this year, there was plenty of volatility along the way.

Thanks to liquidity provided by Steve, the high yield he has offered on cash and our active asset allocation process, the income funds have been able to take advantage of this environment.

Where to from here?

Here’s a quick 2024 outlook on bonds, credit and cash from our income and fixed interest portfolio managers.

Bonds

Bonds have had three challenging years in a row – will there be a fourth? I ask Tim Hext.

That’s very unlikely, he argues.

“My framework for 2024 is for falling inflation and yields. Though as always, I’ll be flexible within the framework, since it likely won’t be a straight line down.”

That’s a good point to remember, I believe. It’s been a while since we’ve had straight-forward, unequivocal bond rallies.

“If the US Fed cuts rates as expected, markets will price in cuts here,” says Tim. “Though the RBA will likely be slow to react, since they rely on the lagging indicator of inflation to set policy.

“I’m watching the new RBA monetary policy board and how that works.

“Also, don’t forget stage-three tax cuts come in July.”

And the line I like the most from Tim: “Even if policy is on hold here for most of 2024, markets will not be standing still.”

This paints a backdrop against which our active investment process can shine.

Credit

Would rate cuts mean bad news for riskier assets like credit?

“Not necessarily,” says George Bishay.

“Like the past year, if the market can feel that inflation can be contained and the growth picture holds up, that’s basically a Goldilocks scenario and equities should do fine.”

Where Australian credit goes is largely led by where US equities have gone before, George often reminds our team.

If the Goldilocks picture can continue, George will be happy to hold on to the risk he now has. But he’s also ready to act if that isn’t the case.

“That’s why I’ve been very discerning in the type of risk I’ve been adding over the year,” George says.

“You can’t ignore the tail risks out there. As the US banking crisis showed us earlier in the year, sentiment can sour very quickly.

“I’ve kept to top-quality issuers, stayed in senior positions in capital structures and always had an eye on liquidity when I’ve been adding risk this year.”

Thanks to George’s nimble approach, I’m not worried about the income funds’ ability to pull credit risk in at the right time.

Cash

Will cash still be in vogue if a new cutting cycle starts in 2024? I ask Steve Campbell.

“Let’s not confuse the RBA with the Fed,” Steve reminds me.

“I expect fourth-quarter inflation to be lower than the RBA’s forecast. That should mean the Reserve Bank is done hiking.

“But any talk of a new RBA rate-cutting cycle is premature. Inflation is still too high and the labour market is still too tight.

“I expect the cash rate to remain unchanged over 2024, though with bouts of volatility.

“Significant global monetary policy tightening since early 2022 and related spill-overs will become more obvious in the coming year as economic growth slows further.”

Because of the uncertain environment ahead, Steve argues that “highly liquid cash strategies rather than term deposits are a better way for investors to capitalise on any bouts of volatility.”

If things go south and bonds still can’t protect you, it’s critical to have a deeply experienced cash manager by your side.

If Steve is right about bouts of volatility, our active and tactical return booster levers – which buy equities or emerging markets – should continue to get a work-out in 2024.

But if he is also right about a further slowing of economic growth, I expect tactical forays into riskier exposures in the income funds will become less frequent.

Recession odds for 2024

The consensus on US recession stands in stark contrast to this time last year.

Economies have been far more resilient than markets anticipated – and markets in turn have adjusted their expectations.

Soft-landing is now the narrative.

Worryingly, fundamentals have deteriorated as the lagged effects of monetary policy tightening play through.

There doesn’t need to be another Silicon Valley Bank-like shock to send the US economy into recession in the second half of next year.

In fact, I’d put the odds at about two-thirds.

It just takes the continuation of the same economic trends we’ve witnessed in recent months.

Slack is coming back into labour markets. Fewer people are quitting, fewer employers are saying it’s hard to find workers.

Lending standards have tightened, meaning credit growth will keep contracting and default rates will keep climbing.

Delinquency rates in consumer loans have risen for seven quarters straight (not months).

The concentrated exposure of smaller US banks to the commercial real estate sector is an unresolved tail risk.

Nothing in that list is dramatic, but the collective force is more likely than not to bring on a recession in 2024.

For much of 2023, the narrative was about too much supply and not enough demand for US government bonds.

If a recession hits next year, demand for safe-haven assets will overwhelm supply, even if the fiscal taps remain on.

Equity markets tend to peak about six months ahead of a recession.

The next few months is a chance to get your house in order.

Consider rotating back into fixed income and cash – and look for good active management.

About Amy Xie Patrick and Pendal’s Income and Fixed Interest team

Amy is Pendal’s Head of Income Strategies. She has extensive expertise and experience in emerging markets, global high yield and investment grade credit and holds an honours degree in economics from Cambridge University.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia. The team oversees some $20 billion invested across income, composite, pure alpha, global and Australian government strategies.