Here are the main factors driving the ASX this week according to portfolio manager RAJINDER SINGH. Reported by portfolio specialist Chris Adams

- Find out about Rajinder’s Pendal Sustainable Australian Share Fund

- Find out about Crispin Murray’s Pendal Focus Australian Share fund

- NEW ON-DEMAND WEBINAR: Watch our bi-annual Beyond The Numbers webinar

CONFLICT in the Middle East has prompted heightened market volatility and rallies in oil and gold prices.

In the US, Fed watchers saw enough rhetoric from committee members last week to suggest the Fed would stay on hold at the next meeting on November 1.

However, slightly stronger-than-expected September consumer and producer price data raised concerns that the Fed might not be able to sit on the sidelines for too long — especially with tailwinds from volatile components such as energy.

There was speculation that China was about to pull the long-awaited stimulus lever to address their economic doldrums — but this was overwhelmed by other events.

Ten-year government bond yield fell 19bps in the US and 8bps in Australia last week. The US dollar was stronger while the AUD was again weaker.

Most commodities apart from energy and gold were weaker.

Equity markets generally managed to finish up for the week. The S&P 500 rose 0.47% and the S&P/ASX 300 gained 1.42%.

US economy and macro

We saw a number of instructive comments from Fed committee members which point to their current thinking.

We also saw the release of the Fed minutes from the previous meeting.

Both indicated the Fed is increasingly comfortable keeping rates unchanged next month.

There is also a developing theme of Fed members explicitly noting that the recent increase in bond yields could substitute for increases in the federal funds rate.

Fed president Raphael Bostic reiterated that he saw no reason for more hikes, saying policy was “sufficiently restrictive” to lower inflation to the 2% target. “I don’t think we need to do anything more,” he said.

Find out about Pendal Sustainable Australian Share Fund

This followed similar recent comments from other Fed presidents Philip Jefferson and Lorie Logan.

President Christopher Waller said policymakers could “watch and see” as financial markets tightened and “do some of the work for us”.

The September Fed meeting minutes noted that “almost all” participants judged that it was appropriate to keep the target range for the federal funds rate unchanged.

“The data arriving in coming months” would help clarify the extent of additional tightening needed to return inflation to the Fed’s 2% target.

All participants agreed the rate-setting Federal Open Market Committee “was in a position to proceed carefully” in setting monetary policy at coming meetings.

It was also noted that GDP growth “had been expanding at a solid pace” but real GDP growth was expected to “slow in the near term”.

A survey of US small businesses showed sentiment remained at depressed levels.

Consumers were feeling similarly subdued and inflation expectations remained at elevated levels, according to University of Michigan research.

We saw US inflation data from three other sources last week:

1. Producer Price Index (PPI)

The headline PPI advanced +0.5% in September. This was a touch stronger than expected and put the yearly gain at +2.2% (up from +2% in August).

Energy goods prices rose 3.3% monthly while and food prices grew +0.9%. Though the core PPI measure (which excludes food, energy and trade) matched consensus with a 0.2% monthly gain

2. Consumer Price Index (CPI)

The eagerly awaited CPI report also came in a bit higher than expectations at +0.4% monthly and +3.7% yearly, versus consensus of +0.3% and +3.6% respectively.

Shelter and energy were the key drivers for headline CPI. Core CPI advanced +0.32%, which translated into a +4.1% yearly gain.

The breakdown of the CPI indicates a few noteworthy trends:

- Services inflation remains consistently higher and stronger, though some forward-looking indicators suggest rent should have a moderating effect going forward.

- Commodities and food effects have dampened over the course of the past 12-18 months.

- Energy has a deflationary effect, though this could easily change with base effects and current prices.

Markets didn’t take this CPI too well on Thursday.

It was the third data overshoot for September (after US non-farm payrolls and the PPI), prompting markets to question whether the Fed had indeed finished hiking — and whether rates had seen their highs.

3. Import prices

To cap off the stronger-than-expected inflation numbers, US import prices came in at up +0.1% in September.

The core import price metric (seasonally adjusted) also edged up +0.1%.

Initial jobless claims (a weekly report that measures the number of Americans who filed for unemployment benefits for the first time) continue to remain low at 209,000, indicating that US labour markets are still tight.

China macro and economy

Early indicators following China’s October Golden Week holiday suggest tourism spending in China jumped 130% year on year, but was up only 1.5% from 2019.

Macau and its casinos benefited during the holiday period, but travel abroad held below pre-Covid levels.

This aligns with views of continued sluggish activity in the Chinese economy, especially on the consumer consumption component.

Credit growth and credit impulse largely stabilised. Chain’s official “Total Social Finance” credit growth — a measure of the total amount of credit provided by the financial system — stabilised at 9% yearly.

Markets were excited by a Bloomberg report that Chinese policymakers were weighing the issuance of at least 1 trillion yuan ($137 billion) of additional sovereign debt for spending on infrastructure such as water conservancy projects.

That could raise this year’s budget deficit to well above the 3% cap set in March, according to one of Bloomberg’s sources.

An announcement could come as early as this month, though deliberations were ongoing and the plans could change.

The discussions underscore mounting concern among China’s top leaders over the trajectory of the world’s second-biggest economy — and how growth compared to the US.

It would also mark a shift in Beijing’s stance.

Beijing has so far avoided broader fiscal stimulus despite a deepening property crisis and rising deflationary pressure which have put its 5% annual growth goal at risk.

Australia macro and economy

There was not much data last week, other than a couple of business and consumers surveys.

NAB’s latest business survey showed easing in conditions in September.

Business conditions fell to +11 in September from an upwardly revised +14 in August (originally reported as +13). That’s still above the long-run average of around +6.

Surveyed business confidence was stable at +1.

Quarterly measures of price pressures also continued to ease, including labour costs (-120bps to +2%), purchase costs (-110bps to +1.8%) and final product prices (-70bps to +1.0%).

Acceleration in inflation following a minimum award wage increase in July now looks to have faded. Though in level terms overall inflation pressures remained elevated (about 4% annualised for final prices).

Australian consumer sentiment rebounded +2.9% to 82 in October, according to a Westpac Melbourne Institute survey. This was driven by improved perceptions of family finances — up from very subdued levels.

That said, in level terms sentiment was still tracking around 20% below the longer-term average.

On the housing market, the “time to buy a dwelling” index rebounded 4.8% monthly from very subdued levels, while the house price expectations index rose +3.8% to a new cycle high of 160.4.

Some 70% of respondents expected house prices to rise over the next 12 months.

Oil and energy

The market is watching to see whether the Israel-Hamas conflict stays contained, or spills into other oil-producing countries nearby.

Spiking energy prices have historically caused damage to the global economy, though we note that the “oil intensity” of GDP growth in the US, EU and China has fallen materially over time.

All eyes remain on Saudi Arabia and Iran and how they respond.

About Rajinder Singh and Pendal’s responsible investing strategies

Rajinder is a portfolio manager with Pendal’s Australian equities team. He has more than 18 years of experience in Australian equities.

Rajinder manages Pendal sustainable and ethical funds including Pendal Sustainable Australian Share Fund.

Pendal offers a range of responsible investing strategies including:

- Pendal Sustainable Australian Share Fund

- Crispin Murray’s Pendal Horizon Fund

- Pendal Sustainable Australian Fixed Interest Fund

- Pendal Sustainable Balanced Fund

- Regnan Credit Impact Trust

- Regnan Global Equity Impact Solutions Fund

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Responsible investing leader Regnan is part of Pendal Group.

The United Arab Emirates is enjoying an economic boom and should be on the radar of emerging markets investors, argues Pendal’s JAMES SYME

- Government reforms leave UAE booming

- Find out about Pendal Global Emerging Markets Opportunities fund

- Watch a recent Emerging Markets overview webinar with James Syme

MANY of us give little thought to the United Arab Emirates unless we’re stopping over briefly on the way to Europe.

But led by Abu Dhabi and Dubai, the UAE is fast emerging as an attractive destination for investment, not just tourism.

“Since Covid, the UAE has staged a really powerful comeback,” says James Syme, who co-manages the Pendal Global Emerging Markets Opportunities fund.

Syme and his team follow a top-down, country-level approach to emerging markets, believing that investment analysis should start at a national level in this asset class.

You can read James’s recent views on Brazil here and Indonesia here.

“In the UAE, we’ve seen a big recovery in overnight visitor numbers,” says Syme. “We’ve also seen a full recovery in oil production which took a big hit during Covid.

“But perhaps more importantly, we’ve seen a number of structural changes that are helping support the recovery.”

The UAE is a union of seven emirates: Abu Dhabi, Dubai, Sharjah, Ajman, Umm Al-Quwain, Fujairah, and Ras Al Khaimah. Each emirate is governed by its own monarch, and one of these monarchs serves as the president of the UAE.

The current president, Abu Dhabi’s Sheikh Mohamed bin Zayed Al Nahyan, has led a series of reforms that have driven an economic boom in the region.

Among the reforms is the creation of a new visa category for non-nationals that allows residency for up to 10 years.

Find out about

Pendal Global Emerging Markets Opportunities Fund

“On that sort of timeframe, people become interested in investing in property and building a stake in the country rather than simply renting, working and moving on,” says Syme.

“That’s really helped support the movement of foreign nationals into the country.

“The UAE is not a democracy, but its leadership is sensitive to the needs of its citizens and has undertaken reforms that have really started to feed growth.”

A regional centre of finance

Other reforms have been aimed at supporting the development of Abu Dhabi and Dubai as financial centres for the region.

“We’ve seen a significant number of listings and IPOs — in 2022, the region had about a quarter of all of global IPO volume.

“As a result, we’ve seen a lot of hedge funds, asset managers and investment banks setting up offices in Abu Dhabi and Dubai, hiring locally, renting offices and buying properties.

“So, there’s a significant boom in it as a financial destination.”

Syme says the Gulf is attractive to the finance industry because it has similar time zone advantages to London — the workday overlaps Asia in the morning and the US in the afternoon.

“Why industrial clusters occur is always a bit of a mystery, but the UAE certainly seems to be the regional winner over Bahrain or Qatar or Riyadh.

“Already having an expat community and strong travel and transport links is a great advantage.”

The two main local carriers, Emirates and Etihad, have also maintained their global routes just as Asian airlines cut back, leaving a significant share of the world’s very-long-haul traffic going through Dubai or Abu Dhabi, says Syme.

And behind it all, oil production is booming – with production back to 3.5 million barrels a day.

“Recovering global tourism, recovering global trade and the recovery in oil production and prices, plus deep structural changes, have driven a boom in the region,” says Syme.

From an investment point of view, Syme says his fund has exposure to domestic sectors in retail, commercial and residential real estate and the commodity side of the economy in both Dubai and Abu Dhabi.

“It remains an active area of search for us. It’s one of our overweights that’s been doing well and which we think is perhaps flying below the radar.”

About Pendal Global Emerging Markets Opportunities Fund

James Syme, Paul Wimborne and Ada Chan are co-managers of Pendal’s Global Emerging Markets Opportunities Fund.

The fund aims to add value through a combination of country allocation and individual stock selection.

The country allocation process is based on analysis of a country’s economic growth, monetary policy, market liquidity, currency, governance/politics and equity market valuation.

The stock selection process focuses on buying quality growth stocks at attractive valuations.

Find out more about Pendal Global Emerging Markets Opportunities Fund here

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

Here are the main factors driving the ASX this week according to Pendal investment analyst ANTHONY MORAN. Reported by portfolio specialist Chris Adams

- Find out about Pendal Focus Australian Share fund

- NEW ON-DEMAND WEBINAR: Watch Crispin Murray’s bi-annual Beyond The Numbers webinar

THE dominant narrative of resilient global economic momentum and higher-for-longer rates continues.

US 10-year government bond yields rose 7bps last week, driven by higher oil prices, a slightly higher-than-expected inflation print and resilient economic and corporate data.

At the margins there was data suggesting China’s economy is turning a corner.

Commodities were strong overall and US dollar took a breather after its strong rally over the quarter-to-date.

The European Central Bank took a dovish turn after increasing rates last week. President Christine Lagarde indicated the tightening cycle was most likely done. The problem for Europe is they are heading into a recession.

The S&P 500 fell 0.12% and the S&P/ASX 300 gained 1.82% last week.

Oil drives sentiment

Oil continues to be a major driver of sentiment with Brent crude up a further 3.6% last week to $94/bbl. It has risen more than 25% so far this quarter.

This is an upside risk to inflation.

There is an argument oil may be reaching a peak since OPEC supply discipline has driven the rally.

We are now at OPEC’s desired price levels, but we are beginning to see a supply response with US weekly oil production hitting its highest level since Covid.

The long-oil position is crowded. Commodity trading adviser allocations to oil are estimated to be at the highest level since mid-2021.

US economy and macro

In the US, August headline inflation data accelerated to 0.6% month-on-month, primarily due to petrol.

The August core CPI was +0.3% month-on-month, above the 0.2% expected by consensus and the 0.2% print in July.

However, the market wasn’t too worried on the day, since it wasn’t a big miss and showed favourable composition.

The beat in core inflation was primarily driven by higher airline fares (passing through fuel cost increases) and higher car insurance costs.

Car insurance is a lagged flow-through of the Covid surge in car prices. This will roll over as car prices have done, but airline fares should rise next month.

The core deflationary drivers of flat goods inflation and slowing rents remained consistent in August, giving the market some comfort that inflation would continue to slow.

The data can be sliced and diced to support either a hawkish or dovish thesis.

The fact that both can be argued tells us something about the stability of CPI relative to market expectations.

The market was flat on the day of the release. There wasn’t much in there to challenge expectations that the Fed will keep rates on hold this week.

Other economic data supported the “Goldilocks theme” of slowing without a recession.

- Industrial production was +0.4% in August versus +0.1% expected, though mostly driven by oil production. Manufacturing production is flat (excluding autos).

- August US retail sales grew +0.6% versus consensus at +0.2% but the surprise was driven by higher petrol prices. Excluding that, core retail sales growth slowed to +0.2%, which is pretty much in the Goldilocks zone for the deflation trade

Looking ahead, we need to keep an eye on the risks of US government shutdown and the potential impact of the United Auto Worker strikes.

Iron ore

Iron ore rose 7.7% last week and is up 10.5% so far this quarter.

Strength in iron ore is surprising given the depressed state of the Chinese property market. Though this has been offset by steel demand from infrastructure investment and by restocking in low port inventories.

Importantly, Beijing has been happy to let steel production remain strong rather than delivering expected steel production cuts.

Pendal Focus Australian Share Fund

Now rated at the highest level by Lonsec, Morningstar and Zenith

This has resulted in Chinese steel exports remaining high (+35% growth yearly) which makes it someone else’s problem and keeps steelworkers employed.

China

Beijing continues to add layers of incremental stimulus.

Last week we saw a 50bps cut in the banking reserve requirement ratio, which should stimulate lending.

There were marginal signs that the economy may be starting to turn less negative.

August economic activity data, while still weak, perhaps indicates a corner has been tuned.

Industrial production was up 4.5% yearly versus +3.7% in July; fixed asset investment gained 2% (prior +1.2%) and retail sales jumped 4.6% (prior +2.5%).

August financing data was much better than expected with total social financing (a broad measure of credit and liquidity) up 9% year-on-year.

Australia

Employment data was strong with +65,000 jobs in August.

But strong labour supply growth from population growth and a lift in participation (a record high of 67%) has kept the unemployment rate flat at 3.7%.

A shift to part-time work potentially reflects growth in second jobs.

Hours worked dipped but the trend has been strong.

Immigration is preventing tightening in the labour market but shifts inflationary pressures from wages to rents and other areas.

Markets

Resources led the equity market last week, driven by stronger iron ore and some China positivity.

Fortescue Metals (FMG, +9.38%), Rio Tinto (RIO, +6.96%) and BHP (BHP, +5.77%) were among the best performers last week in the ASX 100.

Soul Pattinson (SOL, +7.18%) and Whitehaven Coal (WHC, +6.89%) rose on a coking coal supply outage in Queensland.

Financials also outperformed, likely due to firmer bond yields and resilient economic data.

The smaller names such as Bank of Queensland (BOQ, +4.60%) and Virgin Money UK (VUK, +4.49%) did better than the majors.

The market liked Ramsay Health Care’s (RHC, +5.01%) progress on asset sales.

There were positive noise from Malaysian government about potentially working with Lynas (LYC, +4.66%) on investment in downstream rare-earth processing.

Incitec Pivot (IPL, +4.32%) continued its strong run of recent months.

IPL delivered a positive business update as price and cost discipline helped margins in its US explosives business and the Australian explosives business recontracted at better margins. It is still seeing operational issues at Phosphate Hill.

Viva Energy (VEA, -7.64%) was weaker after Vitol sold 16% of the company in a block trade, taking its stake to about 25%. The next major piece of news for VEA will be an ACCC ruling on its proposed purchase of the On The Run chain of petrol stations and convenience stores.

BlueScope Steel (BSL, -6.90%) fell on weaker steel spreads and the US autoworker strike, which will hurt steel demand.James Hardie (JHX, -4.92%) fell on weak sentiment towards homebuilders in the US due to high mortgage rates, despite strong new sales data from the number two national homebuilder Lennar during the week.

About Anthony Moran

Anthony Moran is an analyst with over 15 years of experience covering a range of Australian and international sectors. His sector coverage has included Australian Industrials and Energy, Building Materials, Capital Goods, Engineering & Construction, Transport, Telcos, REITs, Utilities and Infrastructure.

He has previously worked as an equity analyst for AllianceBernstein and Macquarie Group, spending a further two years as a management consultant at Port Jackson Partners and two years as an institutional research sales executive with Deutsche Bank.

Anthony is a CFA Charterholder and holds bachelor’s degrees in Commerce and Law from the University of Sydney.

China’s outlook is one of the most important factors investors need to weigh up right now. Here our head of income strategies AMY XIE PATRICK analyses the latest signals

- New data from China shows positive signs

- Why bonds, why now? Pendal’s income and fixed interest experts explain

- Browse Pendal’s fixed interest funds

THE latest data shows China’s economic activity starting to stabilise.

Is this a turning point in the economic cycle?

That remains to be seen.

It’s been only a few months since hopes for a re-opening led boom in economic activity were dashed.

We think activity is now stabilising on a cyclical basis, and China’s economy can continue to gradually recover into the end of the year.

But structural drags on the economy are heavy and deep rooted.

In his article we explain how far the current recovery could extend; which structural issues are most limiting; and what are the implications for global growth and investing.

A pick-up in activity

Last week we saw the latest release of hard economic data from China.

As Reuters reports here, monthly industrial output sped up and retail sales grew faster.

By most accounts, the data beat market expectations.

Yes, expectations were fairly low to begin with and therefore easy to beat. But these latest numbers suggest that sequentially, things are improving for the world’s second-biggest economy.

The fixed income team at Pendal thought this would be the case.

Electricity output is a good place to look for how the Chinese economy is going.

Electricity output is driven by energy use in the economy. Although this can fluctuate depending on weather, supply issues and other exogenous factors, a rise in energy use tends to happen when activity levels within the economy are rising.

This is why the Li Keqiang index (a proxy measure for Chinese growth) relies on electricity output as one of its three components to track economic activity.

Electricity output has been rising over the past few months, and points to upside to come in the hard data.

Climbing out of deflation

Another place to look for the health of demand in the Chinese economy is producer prices.

Although they track commodity prices closely, given that China is such a large global consumer of commodities, a falling PPI has usually been synonymous with a slowing of Chinese demand.

China’s Producer Price Index (PPI) – a measure of the change in selling prices received by domestic producers for their output – has been in deflationary territory since October 2022.

But it bottomed in June at -5.4% and has been clawing its way back in the last few months.

This may be good news for the Chinese economy, since generating positive inflation momentum is one way to combat debt-deflation dynamics.

But it has mixed implications for the rest of the world.

As the Bloomberg chart below shows, there has long existed a close relationship between China’s PPI and US inflation.

The relationship was likely solidified after China joined the World Trade Organisation in 2001 and became a heavy-weight influence over most tradeables (goods) inflation.

The dislocation between 2016-2018 was likely as a result of Trump’s trade wars against China. The dislocation since 2022 has been the dominance of services-led inflation in the US.

In fact, China’s deflation has been incredibly helpful for inflation in the developed world in the last 18 months.

Without it, goods inflation would still be high, and the market would not be so sanguine about the future path of the US Fed and other central banks.

The turning point in China’s PPI may signal that the freebie of goods price deflation is coming to an end for the rest of the world.

This may not lead to a big second wave of inflation. But it may mean a stickier path for US and other developed world inflation.

It will put the focus squarely back on local labour market dynamics and whether policy settings have become sufficiently restrictive to slow wage growth.

How meaningful a recovery?

This recovery stands out because the aim of recent piecemeal measures on stimulus was not about starting a new property cycle.

The aim has been to contain the fall-out of the property downturn while finding ways to pivot towards other sources of growth.

To that end, recent measures targeted at relaxing macro-prudential restrictions on home buying are more about easing off on the brakes rather than stepping on the gas pedal.

I would argue these measures have been working.

A huge blockage in the property system formed when property transactions slowed.

Since pre-sale down-payments were a key source of developer funding, it limited the ability of developers to continue or even initiate construction on properties they had pre-sold.

Find out about

Pendal’s Income and Fixed Interest funds

This meant buyers couldn’t take delivery of finished property. But due to the way the mortgage system works in China, they were already on the hook for servicing a part of the mortgages.

This all too easily snowballed into a crisis of confidence, which fed into a further slowdown in property sales, property prices and so on.

A crucial way to alleviate the blockage was to get sufficient funds to developers to finish what they‘d started.

Property completions have been up strongly this year as backlogs of paused works have resumed.

But this is a very different kind of property stimulus compared to the past. It certainly won’t lead to new waves of strong demand anytime soon.

This is why land sales are still contracting.

Developers only buy new plots of land when they see strong demand prospects in the pipe, as you can see in this Bloomberg chart:

Even without a new wave of property demand, it’s a good to see things are moving again in the Chinese property space.

The property sector accounts for more than a quarter of Chinese economic activity, so the flow-through effects will be positive.

Bigger challenges lie ahead

China’s structural problems have not changed.

They centre on an economy that saves too much, causing growth to rely on debt-driven investment rather than by income-led consumption.

China’s national savings rate is over 45%, compared to an OECD average of just over 20%.

The high propensity to save by the private sector in China is partly due to a lack of safety nets.

This increases the burden on the working age population to care for old and young and save for their retirement.

Housing affordability is another issue. Chinese cities have some of the worst housing affordability ratios in the world.

This means parents have to save in anticipation of their offspring one day needing help on a down-payment.

Fiscal measures aimed at easing the burden on households and boosting the social safety net are essential for supporting consumption in China.

Helicopter money is traditionally unacceptable to Chinese socialist principles. It is the main reason why even in the depths of the COVID crisis, the extent of fiscal stimulus unleashed by Beijing paled in comparison to what we saw in the rest of the world.

However, faced with the prospect of a nasty property crisis, fiscal stimulus to the consumer is now being embraced by policy-makers as the lesser of two evils.

Fiscal measures can lead to more near-term upside for the Chinese recovery, but cannot remove a higher-order headwind to consumption.

That headwind is the crowding out of entrepreneurial spirit as President Xi has consolidated his political power in recent years.

Xi’s motives are likely triggered by geopolitical insecurity (including Trump’s anti-China policies).

The outcome is a disruption of incentives for the private sector to borrow, invest and consume.

Investment implications

Against low expectations of any Chinese economic revival priced into Chinese assets, any upside surprise in data in the next few months is likely to have a bigger effect than disappointments.

This limits the ability of bearish China bets to work in Chinese markets, be they rates, currency or equities.

We have closed our short RMB bias now to be neutral, and are short China rates.

It is harder to play for upside in other risky assets though, because not much downside relating to China was priced into those markets in the first place.

Even US companies with big exposures to China’s growth outlook have remained resilient.

However, if Chinese economic momentum is basing here, it reduces the immediacy of tail risks for risk assets more broadly, which is supportive.

A more resilient US economy likely also plays into a supportive backdrop for risky assets ranging from credit to equities.

Our income funds are currently not shying away too much from risky assets, but we are mindful of this being a tactical play.

It is difficult to chart a path of “not too hot, not too cold” growth for the US economy when unemployment is at record lows.

Therefore, it is vital to take the extra risk in the most liquid way so as to preserve the ability to actively de-risk.

When that time comes, bonds will come back into play.

As for currencies, be mindful of a tug-of-war playing out on the US dollar.

It is counter-cyclical in nature, so a stronger global manufacturing cycle should weaken the greenback.

However, if China’s revival causes a sticky inflation headache, the greenback’s ability to weaken will be limited by higher for longer rates in the US.

About Amy Xie Patrick and Pendal’s Income and Fixed Interest team

Amy is Pendal’s Head of Income Strategies. She has extensive expertise and experience in emerging markets, global high yield and investment grade credit and holds an honours degree in economics from Cambridge University.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia. The team oversees some $20 billion invested across income, composite, pure alpha, global and Australian government strategies.

Find out more about Pendal’s fixed interest strategies here

About Pendal Group

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

A growing population and the uneven impact of rising interest rates are two factors supporting company earnings right now. Pendal’s head of equities CRISPIN MURRAY explains

- Rising population supports company earnings

- Company earnings driven by nominal, not per capita, GDP

- Find out about Pendal Focus Australian Share fund

MOST people would be aware from the recent per-capita recession headlines that Australia’s population growth is outstripping economic growth.

But Australia’s rapidly growing population is also a key reason why corporate earnings are holding up, says Pendal’s head of equities Crispin Murray.

“All up, we’re probably looking at about a 3 per cent rise in the population today versus where we were a year ago,” says Murray.

Population growth has been supported by direct immigration as well as temporary visas, he says.

“That’s people coming to Australia with money in their pockets needing to spend when they arrive to set themselves up and needing to get accommodation, which is driving up rents.

“This is part of the reason that we’re seeing resilience in the top line of companies because they’re basically driven by nominal GDP, not per capita GDP.”

Population growth is also helping offset the effects of the so-called ‘mortgage cliff’ forcing households into higher, variable mortgage payments as low-rate fixed loans expire.

As Pendal’s head of bond strategies Tim Hext recently noted, we are about half-way through that step-up period – and so far most fixed-mortgage holders seem to be adjusting ok.

Likewise, the effects of the mortgage cliff have been muted in company reports this earnings season.

“The mortgage cliff is real – but what is offsetting it is population growth,” Murray said at his bi-annual Beyond The Numbers webinar last week.

“With each company we met over reporting season, we talked about the issues facing them and whether they were seeing the consequences of this mortgage cliff.

“But so far, the consequences are very limited.”

Uneven interest rate burden also supports earnings

The uneven impact of rising interest rates across the community is also holding up corporate earnings, points out Murray.

“Clearly, the concentration of mortgage debt is predominantly in the under-45s and particularly in the under-40s. That’s where the core pressure remains.

“As you get older, you see a big skew to savings and the people with the savings are clearly getting the benefit of higher interest rates.

“While we have seen some draw-down on savings overall, you’re actually still seeing everyone over the age of 35 adding to their savings pool.”

Data comparing spending patterns in the last three months to the last four weeks shows a distinct change in trend for under-35s – but little change for older groups.

“There is a quite complex set of trends happening in the economy, which is why I think we’ve proven to be more resilient.

“There’s a lot of focus on the pressures on people under 45, but less awareness of the spending which is happening in the older demographics.

“It’s an important thing to be aware of.”

About Crispin Murray and Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia. Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions.

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

Businesses believe the economy remains on a decent footing, which indicates a soft landing looks on track for now, writes Pendal’s head of bond strategies TIM HEXT

- Why bonds, why now? Pendal’s income and fixed interest experts explain

- Browse Pendal’s fixed interest funds

SPRING will well and truly arrive on Australia’s east coast this Saturday.

The forecast here in Sydney is for 31c.

Weather apps are now so accurate that not only am I confident it will be 31c – I also know it will happen at 2pm.

Here in Pendal’s Income & Fixed Interest team we’re always looking for ways to improve our forecasting ability.

We constantly test economic and market indicators that have a track record of predicting bond and credit markets.

We test hundreds of indicators before narrowing them down to a small number help create quantitative models to assist our portfolio positioning.

Even better if the indicators are not widely tracked. Inflation and unemployment numbers are obsessed over but we need to get ahead of those.

While the level of an indicator is important, we’re usually more interested in the direction of travel.

NAB’s Monthly Business Survey is the richest domestic economic information source.

NAB surveys almost 600 firms on a monthly basis, creating numerous indicators of changes in the economy.

Our testing consistently shows many of the outputs have a strong performance in predicting future market moves — so we pay close attention from a qualitative and quantitative perspective.

What does this month’s survey show? Business managers believe the economy remains on a decent footing and has even slightly picked up from July.

The soft landing looks on track, at least for now.

Courtesy of NAB here are the results:

What the data means

The data in the first section is on a net-balance basis. In other words, firms expecting a deterioration are subtracted from those expecting an improvement.

For conditions and confidence, the average has been around six for several decades.

Therefore, businesses are not confident about the future, but still see current conditions as favourable and even improving.

Mining, transport and utilities lead the way. Retail is weaker but holding up, though confidence is very low.

In summary, rate hikes should matter more (and might in the future) – but for now we are holding up well.

Labour costs remain elevated but showed some relief after July’s surge.

Final product and retail prices also eased, though levels remain elevated and consistent with inflation closer to 5% than 2.5%.

Finally, capacity utilisation still shows tight capacity. On average capacity is at around 81%. A reading of 85.1% is near the highs of mid 2022 and is not showing the freeing up of capacity we would have expected.

Overall, when thinking about where the economy is right now, it’s important to separate the nominal economy from the real economy.

Find out about

Pendal’s Income and Fixed Interest funds

In the nominal economy, population growth of almost 450,000 in the past 12 months has seen some expansion in the economy and increasing demand for goods and services provided by business.

Business, concerned about the future, have been reluctant to add to capacity.

However, on the real side inflation and higher rates has meant on an individual basis we are tightening our belts.

Our money quite simply is not going as far as it was, so individually we are buying fewer goods and services.

Business knows this, and when the population growth falls back to around 250,000 next year the nominal economy will also start feeling this.

For now though our models show rate hikes are still more likely than cuts, though the RBA looks happy to sit out the next few months.

About Tim Hext and Pendal’s Income & Fixed Interest boutique

Tim Hext is a Pendal portfolio manager and head of government bond strategies in our Income and Fixed Interest team.

Tim has extensive experience in banking, financial markets and funding including senior positions with NSW Treasury Corporation (TCorp), Westpac Treasury, Commonwealth Bank of Australia, Deutsche Bank, Bain & Co and Swiss Bank Corporation.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia.

Find out more about Pendal’s fixed interest strategies here

About Pendal

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

In 2023, Pendal became part of Perpetual Limited (ASX:PPT), bringing together two of Australia’s most respected active asset management brands to create a global leader in multi-boutique asset management with autonomous, world-class investment capabilities and a growing leadership position in ESG.

Here are the main factors driving the ASX this week according to our head of equities CRISPIN MURRAY. Reported by portfolio specialist Chris Adams

- NEW ON-DEMAND WEBINAR: Watch Crispin Murray’s bi-annual Beyond The Numbers webinar

- Find out about Pendal Focus Australian Share fund

EQUITY markets continue to drift lower and now sit at an interesting juncture.

Last week the S&P/ASX 300 fell 1.21% and the S&P 500 lost 1.26%.

The bullish perspective is:

- This is a period of consolidation at a seasonally weak time of year

- In the US we are seeing slower inflation and wage growth while the economy holds up — which may mean no recession

- Interest rates have peaked

- This implies earnings are set to grow and valuation ratings rise to drive the market higher

The bearish perspective is:

- Key market leader Apple is falling on concerns over potential Chinese bans, dragging mega caps lower

- The US dollar looks to be breaking back higher

- Bond yields are rising again despite lower inflation data

- Oil is also breaking higher after Saudi Arabia and Russia announced an extension to supply cuts

- Delayed effects of monetary tightening will lead to the economy slowing more materially

- Bond yields, currency and oil are moving in the wrong direction

- In combination with weaker growth, these are warning signs for the market

In Australia we saw the departure of Philip Lowe as Reserve Bank governor, which coincided with abysmal data on productivity and weak GDP data.

This highlights the fundamental challenges facing our economy.

A reliance on immigration and commodities to support growth leaves us vulnerable to an inflation surprise or a growth problem (or both) if the current environment shifts.

US economy

Positive signals continued on the inflation front.

The Atlanta Fed Wage Tracker fell from 5.7% to 5.2% in August, further supporting the “immaculate disinflation” thesis.

The “job switcher” category has now almost fallen into line with the “overall” category.

This supports the case that the main wage-inflation driver was the ramping up of many businesses post-pandemic — and as time goes by this is being resolved.

Combined with slowing growth, companies are becoming wary of chasing too many new hires.

This can be seen in the “job-workers” gap that Goldman Sachs has been estimating. This indicates how job openings have fallen away without unemployment needing to rise materially.

The counter to this view is that wages growth has softened due to a recent drop in inflation which may itself be overstated.

Inflation may start to rise again, given oil price moves and an end to the benefit of supply chain problems unwinding.

This may suggest the declining wage trend is overstated.

On this front the outcome of the United Autoworkers dispute will be an interesting test for persistent wage pressures.

There are 146,000 members seeking a 46% pay increase over four years ($32/hr to $47/hr at the top rate) plus the right to represent workers at electric vehicle battery factories (among other demands).

The union has given the big auto makers until Thursday to come to an agreement.

Economic news continues to support a soft landing. Goldman Sachs, for example, has reduced recession risk to 15%.

One area of contention in the economic debate is how consumers will behave.

Many expect spending to come under pressure with reduced excess saving, a fall in government support in areas such as student loan payments and lower small business rebates, childcare payments and Medicaid coverage.

Goldman Sachs presents a more optimistic view on the consumer which looks at the impact of higher real wages, more hours worked and increased interest income.

They expect this will allow real income growth of 3% in 2024.

This is skewed to higher-income earners due to interest payments, but should translate into consumption growth of 2% without relying on drawing down of savings.

China

Chinese property developer Country Graden got a stay of execution.

It received approval from onshore creditors to extend payments, allowing them to make payments on offshore bonds ahead of a Tuesday deadline. If this went unpaid it would have triggered default clauses on other loans.

Housing remains the key challenge, with sales slowing.

There has been further lifting of homebuyer curbs in tier-two cities. Beijing’s clear message is easing developer liquidity stress and supporting demand for durable goods.

It is worth noting a signal from the Chinese bond market, which reversed last week.

Rising yields suggest the market may be beginning to believe we have seen a peak in growth concerns.

Another issue to watch is Chinese domestic politics. There are stories of unrest over economic performance, while Xi chose not to attend the G20.

Australian economy

Australian GDP grew 0.4% in the June quarter and 2.1% year-on-year.

While in line with expectations, this highlighted some economic challenges. GDP per capita fell 0.3% for the quarter given strong population growth.

When it comes to company earnings, aggregate spending is what counts.

Looking at the breakdown of data:

- Quarterly growth in household consumption was weak at 0.1%. This was partly due to the PCE deflator of 6.1% year-on-year — so nominal consumption is 7.7% year-on-year, but volumes are essentially flat

- Savings rates have fallen to 3.1% — a cycle low.

- Business investment remains strong, with mining up 5.6% year-on-year and non-mining up 9.1%.

- Government spending is strong at 1.8% quarterly, driven by investment at state and federal levels. This highlights how fiscal policy is putting pressure on monetary

- Quarterly exports were strong at 4.3%, again helped by mining

- Nominal GDP fell for the quarter, but is up 3.6% year-on-year

The real shocker in the data is productivity, which fell 1.6% for the quarter, 2.1% year-on-year — and is now back to 2016 level in absolute terms.

This means unit labour costs are rising 7.5%, which is usually tied to services inflation.

Employee compensation growth is strong at 1.6% quarterly and 9.6% yearly. Households continue to find ways to supplement income.

Australia is an economy with slowing growth, reliant on government spending, business investment and commodity exports. All of this is either unsustainable or volatile.

Meanwhile productivity is very weak, which will probably either lead to profits coming under pressure, higher unemployment or more price inflation as companies pass costs on.

Markets

There is a lot of attention on the US dollar, which appears to be breaking higher.

This is usually associated with liquidity tightness and weaker markets.

Oil continues to push higher, supported by Saudi and Russian plans to extend production cuts.

However it is unlikely to be allowed to go much higher, given the impact that can have on global economy and substitution.

Apple had a poor week, falling about 6 per cent on China’s threat of an iPhone ban. This is possibly a warning about shifting too much of its supply chain out of the country.

This week’s annual Apple product day will be an important test of sentiment, given its lead status for tech and the market overall.

It may help inform whether bull or bear thesis plays out.

About Crispin Murray and Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia. Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions.

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

ASX-listed accounting software provider Xero recently held its major Xerocon conference in Sydney. Pendal equities analyst ELISE McKAY attended.

- LIVE WEBINAR SEP 7: Register for Crispin Murray’s bi-annual Beyond The Numbers webinar

- Find out about Pendal Focus Australian Share fund

XERO’S annual Xerocon event is known as ‘Coachella for accountants’ – a reference to a Californian rock concert with a cult-like following.

The ASX-listed cloud-accounting platform has a pretty strong following itself now, with more than 3.7 million subscribers in 180 countries.

And that’s led to a pretty good understanding of the state of small-to-medium businesses (SMBs).

Pendal equities analyst Elise McKay has been following Xero closely for years and attended the recent Xerocon event in Sydney.

Here are some take-aways relevant to Xero investors and anyone interested in the state of small business in Australia.

Sales growth under pressure

Small businesses are seeing slower sales growth in Australia, Canada, NZ, the UK and the US, Xero reports.

While all five countries averaged double-digit sales growth in the first half of 2022, this has since slowed to single-digit growth everywhere except the US (where sales were 5% lower).

After adjusting for inflation, Australia was the only country where small businesses typically reported volume growth (an increase in the number of units sold).

“On the positive side, Xero reports that wage pressures are starting to ease in Australia, NZ and the UK,” says McKay.

“Xero now sees wages growing in-line with the long-term average of its data — and materially lower than record highs in 2022.

“While they’re holding up, it’s a difficult time to be running a small business,” says McKay.

One of the ways Xero is responding is by integrating third-party payments systems (such as Stripe or Paypal or Square) which can speed up customer payments.

“There’s been an increase in the number of days before SMBs are paid, putting more pressure on cash flows,” McKay says.

“An integrated payment solution such as a Pay Now button offers customers more ways to pay. As a result, the small business can get paid faster,” she says.

The impact of artificial intelligence

Not surprisingly, SMBs are reporting mixed views on the extent to which artificial intelligence will disrupt their industries.

Like a number of other software developers, Xero expects AI will mostly benefit businesses where the technology is used to boost human expertise rather than replace it.

Xero is adding AI where it can speed up repetitive tasks or provide better insights that help humans focus on higher-value strategic activities.

“For example, helping to better enable reconciliations or provide better forecasting tools around things like cash flow,” says McKay.

“And potentially using generative AI to improve customer support.”

The value of brand

Anyone watching the recent FIFA Women’s World Cup would know Xero made a significant investment in branding at the event.

“The success of the world cup event was not only great for women’s sport, but also Xero’s brand equity,” says McKay.

“Brand equity is a leading indicator of market share.”

The Xerocon event also highlighted the importance of the SMB “eco-sphere”, Mckay says.

Xero now has more than 1000 partners in its ecosystem — relationships which help improve the ‘stickiness’ of the group’s products.

Xero’s app store is also a revenue stream.

“As small businesses adopt more apps, and have more linkages to Xero, they become more integrated and that provides a greater lifetime value.”

That also helps Xero develop cross-selling opportunities and build awareness of its products in new audiences.

About Elise McKay and Pendal Australian share funds

Elise is an investment analyst and portfolio manager with Pendal’s Australian equities team. Elise previously worked as an investment analyst for US fund manager Cartica where she covered a variety of emerging market companies.

She has also worked in investment banking and corporate finance at JP Morgan and Ernst & Young.

Pendal Horizon Sustainable Australian Share Fund is a concentrated portfolio aligned with the transition to a more sustainable, future economy.

Pendal Focus Australian Share Fund is a high-conviction equity fund with a 16-year track record of strong performance in a range of market conditions. The Fund is rated at the highest level by Lonsec, Morningstar and Zenith.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Australia is in a ‘per-capita recession’, which means economic growth is not keeping pace with population growth. TIM HEXT explains the problem and what’s likely to happen next

- Why bonds, why now? Pendal’s income and fixed interest experts explain

- Browse Pendal’s fixed interest funds

AUSTRALIA’S national accounts — quarterly estimates of economic flows such as GDP, consumption, investment, income and saving — land two months after the end of a quarter.

Many therefore ignore them as old news.

But they are the most comprehensive picture of the Australian economy from a macro and micro lens.

So what does the latest data — released today — reveal about Australia at the end of June?

In short, it is a very mixed picture. More than ever how you are feeling depends on where you sit.

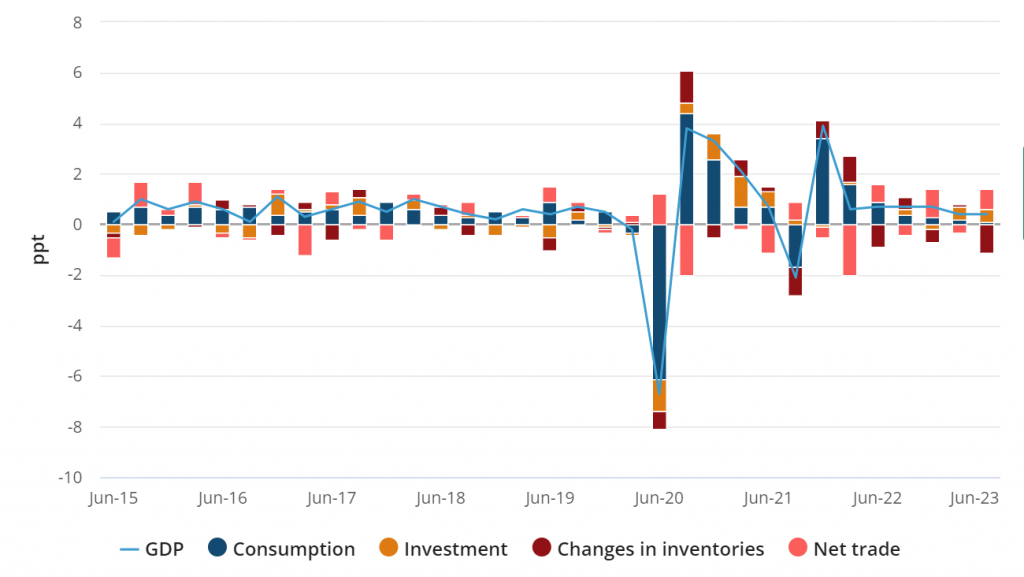

This ABS graph below shows the various contributions:

First, the good news. We are avoiding a recession.

GDP is 2.1% higher than a year ago, though slowing.

It’s been 0.4% for two quarters now and will likely end the year near 1.2% — slightly higher than the RBA forecast of 0.9%.

Inventories are unlikely to be a drag next quarter, but net trade should also stabilise.

Now the bad news. We are clearly in a per-capita recession.

In other words, this level of economic growth is not enough to keep pace with population growth.

Which means the average person is going backwards in their standard of living.

Our population grew by 0.7% in Q2, the economy only 0.4%. GDP per capita is now 0.3% lower than a year ago and 0.6% lower than six months ago.

We are importing growth, not growing from within.

Per-capita recession

Why are we in a per-capita recession?

We are seeing more hours worked as employment rises along with our population. But we are going backwards in GDP per hour worked — down a staggering 2% in the quarter.

This is one of the worst results since deregulation in the 1980s.

Remember this is a volume measure — not price or value.

Productivity is going backwards. It has now gone nowhere since 2016.

Put simply, the RBA is facing labour costs rising at 4% — with stagnant or even negative productivity.

Unless businesses wear the squeeze, inflation is not coming back too far below 4% for some time.

Consumers tighten belts

How is the consumer holding up in the face of rate rises?

Household consumption barely grew in the June quarter at 0.1%. Services were up 0.2% but goods were flat.

Find out about

Pendal’s Income and Fixed Interest funds

We are tightening our belts in discretionary spending, which fell 0.5%.

This is consistent with a soft landing and is not disastrous, at least for now.

Motor vehicle sales are still strong, so maybe cashed-up baby boomers are buying four-wheel drives for their lap of Australia.

Pandemic stimulus savings are a thing of the past — the savings rate has fallen to a cycle low of 3.2%.

In the national accounts savings is a residual (income less consumption) and not directly measured — so it is not always an accurate indicator.

But it shows buffers are falling, albeit very differently across age groups.

The growth we did have came through a rebound in export volumes and ongoing government investment.

This continues a pre-pandemic theme and shows as a country our ongoing reliance on these two sectors, which is concerning.

Likely we will commission another productivity report — having ignored previous recommendations — and kick the can down the road.

The immigration lever

In the near term, the RBA would be a little less comfortable about this national accounts picture.

But we think labour supply via immigration will push unemployment back up to 4% and ease some wage pressures.

This should buy the RBA more time while the full impact of 4% in rate rises in little over a year feeds through. (We are still only 80% of the way there).

If Australia was a company these accounts would be causing analysts to downgrade their outlook. Workers are less productive and costs are rising.

But some of this may still be the lingering impact of the pandemic. Cue discussions on working from home.

The RBA will be hoping this can turn around in the year ahead.

Immigration will slow in the next 12 months to around 1%, because the sharp increase in foreign student numbers was a one-off return from the pandemic.

An outright recession (not just a per capita one) is not a base case — but the chances of it will rise.

Dr Bullock will be facing the dilemma of a slowing economy under full employment and high wages as she takes over as RBA governor in a fortnight.

We wish her luck trying to work out what all this means for rates.

About Tim Hext and Pendal’s Income & Fixed Interest boutique

Tim Hext is a Pendal portfolio manager and head of government bond strategies in our Income and Fixed Interest team.

Tim has extensive experience in banking, financial markets and funding including senior positions with NSW Treasury Corporation (TCorp), Westpac Treasury, Commonwealth Bank of Australia, Deutsche Bank, Bain & Co and Swiss Bank Corporation.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia.

Find out more about Pendal’s fixed interest strategies here

About Pendal

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

In 2023, Pendal became part of Perpetual Limited (ASX:PPT), bringing together two of Australia’s most respected active asset management brands to create a global leader in multi-boutique asset management with autonomous, world-class investment capabilities and a growing leadership position in ESG.

Here are the main factors driving the ASX this week according to Aussie equities analyst ELISE MCKAY. Reported by portfolio specialist Chris Adams

- LIVE WEBINAR SEP 7: Register for Crispin Murray’s bi-annual Beyond The Numbers webinar

- Find out about Pendal Focus Australian Share fund

GLOBAL equity markets remained relatively quiet last week as northern-hemisphere investors made the most of the last days of summer.

Economic data was largely thought to be supportive of a soft landing and markets responded accordingly.

The Nasdaq gained 3.27% and the S&P 500 lifted 2.55%.

A softer-than-expected US employment report on Friday supported the view that the Fed did not need to hike rates again.

The market is now pricing in a 94% chance that Fed holds rates steady in September and 65% chance of a hold in November.

The consensus view is firmly a soft landing, goldilocks scenario.

Data suggests the US is on track to deliver a very solid quarter of GDP growth, with the Atlanta Fed’s GDPNow measure at 5.6% growth.

The market takes a more nuanced view, however, believing consumer strength won’t be sustained with a wave of headwinds closing in.

Real personal spending growth has continued to run hotter than expected. But headwinds associated with a lower savings rate, resumption of student loan repayments and run-down of pandemic excess savings suggest strong personal consumption growth won’t be sustained into Q4.

This raises concerns that a stronger-than-expected economy may over-ride improving trends in inflation and wages, leading to further uncertainty in rates and the Fed.

This runs counter to the soft-landing scenario now priced into the market (and which recent data supports).

Despite dovish data on Friday, US 10-year bond yields counter-intuitively moved 10bps higher. Some pointed to stronger ISM manufacturing data (and particularly a move up in the price index) as less contractionary.

Though lower market liquidity in a quiet week may have exacerbated the move.

In Australia, July inflation data came in well below expectations at 4.9%, down from 5.4% in June.

Softness was largely driven by more volatile items. Excluding these, inflation picked up in July, mainly driven by higher electricity prices and housing purchase-price inflation.

Meanwhile we wrapped up a volatile reporting season with one in eight stocks moving more than 10 per cent up or down – nearly double the average.

This was despite results that were largely in line with expectations and earnings revisions no bigger than normal.

The S&P/ASX 300 gained 2.6% for the week.

The Reserve Bank is expected to keep rates on hold this Tuesday.

The latest Chinese manufacturing data was mixed. Beijing announced a number of easing measures to support the property sector, consumption and currency. This is a step in the right direction, though more is needed.

The global disinflation story continues.

This is supportive for markets as we come close to the end of the tightening cycle and growth in the world’s largest economies remains largely intact.

US economics and policy

At 5.6%, the Atlanta Fed GDPNow – a measure of the growth of the US economy – continues to run well ahead of consensus estimates (which are in the mid-2% range for Q3 GDP).

Who is right? And why the difference?

The Atlanta Fed methodology is model-based and extrapolates the latest economic data for the remainder of a quarter. This compares with human forecasting, which is more likely to mean revert.

The biggest area of differences are:

- Real consumption: GDPNow has extrapolated strong July data while forecasters are expecting weakness in August and September

- Inventory: GDPNow has levels rebounding, which is not yet seen in actual levels across the economy

While GDPNow is a pretty accurate predictive tool, it only has one month of data for the quarter so far.

Find out about

Pendal Horizon Sustainable Australian Share Fund

This raises a concern that a stronger-than-expected economy may swamp improving trends in inflation and wages.

This could create a dilemma for the Fed, leading to further uncertainty which runs counter to the soft-landing scenario now being priced into the market.

US employment data

August’s employment report had non-farm payroll ahead of expectations at 187k new jobs versus 170k expected, but significant downward revisions (-110k) to the prior two months.

The three-month average is now 150k. This is still above the equilibrium needed to keep pace with labour force growth, but it’s moving in the right direction (and is the lowest since 2021).

The unemployment rate surprised to the upside, rising 30bps to 3.8%. This is now the highest unemployment rate since February 2022.

This reflects higher labour force participation which is now at 62.8% – the highest since February 2020 – as well as a higher number of unemployed.

Average hourly earnings also came in below expectations with the private sector rising 0.2% month-on-month, versus 0.3% expected.

In combination with Tuesday’s JOLTS data, which showed lower job vacancies in June (revised lower) and July, this suggests labour market conditions are continuing to loosen.

This should translate into weaker wage pressure, where we are looking for growth in a range of 3.0-3.5% growth, which is more consistent with inflation at 2%.

US inflation

The Fed’s preferred read on inflation – Personal Consumption Expenditures – is a measure of the total amount of goods and services purchased by Americans.

The latest data released on Thursday showed core PCE prices rising 0.22% in June, slightly ahead of consensus (0.20%). The annualised three-month rate is 3.3% and is up 4.2% year-on-year.

Core goods inflation declined further (-0.45% month-on-month) – the second negative read in a row.

This should provide some comfort to the Fed, since Chair Jay Powell said sustained progress was “needed” at Jackson Hole.

Disappointingly, core services (excluding rent) rose 0.5%, breaking the downward trend evident since January. More than half of the increase was due to a volatile financial services component.

US consumer spending

Personal income grew 0.2% in July, slightly weaker than expected. There was a deceleration from +0.6% to +0.4% in wages and salaries.

Consumer spending rose 0.8% in July with all categories stronger, driven by strong retail sales (assisted by Amazon’s Prime Day sale) and discretionary services.

The “Barbenheimer” effect of the popular Barbie and Oppenheimer films showed in the data. Recreational services spending (such as movie tickets) were particularly strong at +10.7% for the month.

Stronger spending and higher taxes contributed to a decline in the savings rate to 3.5%.

Restarting student loan payments should cause a significant headwind to consumption in Q4.

Find out about

Pendal Focus

Australian Share Fund

Crispin Murray,

Head of Equities

Meanwhile, about 75% of pandemic excess savings have now been spent. The remaining 25% are held by higher income households, which are less likely to spend it.

US manufacturing

August US manufacturing data sent a mixed message to the market on Friday.

While remaining in contractionary territory at 47.6 (marginally above consensus at 47) there was a focus on the Institute for Supply Management “prices paid” data.

A surprise jump from 42.6 to 48.4 (versus consensus at 44) raised some concern about how this might roll into core goods inflation, which is now in deflationary territory.

Australia

Inflation data for July came in well below expectations, moderating to 4.9% (consensus at 5.2%) from 5.4% in June.

Softness was largely driven volatile items such as fuel, fruit and veg, as well as travel.

Excluding volatile items and travel, inflation picked up in July, mainly driven by higher electricity prices and housing purchase price inflation.

China

Manufacturing PMI increased to 49.7 in August, the highest reading since March. This was broadly consistent with anecdotal information that the pace of inventory destocking was slowing.

However, non-manufacturing PMI declined to 51, the lowest reading of 2023, as the “reopening boost” from covid faded and construction activity weakened.

We are seeing a drip-feed of policies and support for markets, with concerns around housing, leverage, shadow-banking and capital flight still in focus.

Last week, Beijing delivered a number of easing measures to support the property sector, consumption and currency. It is a positive step in the right direction but more is needed.

Summarising the key announcements:

- China Banks: Cuts to mortgage down-payment ratios and mortgage rates for new and existing mortgages. Looking to stimulate the property sector and address concerns about the risk of a collapse given the increased number of credit risk events among major developers and financial institutions in the past couple of weeks.

- As part of the overall easing package, the PBoC also announced it would cut the reserve requirement ratio for foreign exchange deposits by 200bp to 4% from 6%, effective from September 15. On the same day a year ago, the PBoC cut the FX RRR to 6% from 8%. A cut to 8% from 9% was made on May 15, 2022.

- Ministry of Finance: Cut stamp duty rates by 50% to 5bps. This marks the sixth stamp duty cut in history and the first since 2008.

- China Securities Regulator: Announced it will lower minimum margin requirements for margin finance effective September 8.

- China Securities Regulator: Will tighten IPO activities and major shareholder divestments. This includes major shareholder divestment restrictions if stocks trade below IPO price.

- US Commerce Secretary Raimondo and China counterpart Wang Wentao established a “commercial issues” working group, to find trade/investment solutions, and to meet twice annually. They agreed to set up an “export control enforcement information exchange” to serve as a platform to reduce misunderstandings on export restrictions

- China’s Finance Minister Liu Kun and the National Development and Reform Commission pledged to strengthen policy support and speed-up Govt spending to support the economy

In an example of how China could restimulate the birth rate, South Korea plans to cut mortgage rates for new parents to 1-3% below loans offered by commercial banks.

Markets

August was one of the most volatile Australian earnings seasons in the past 15 years with one in eight stocks moving more than 10% up or down.

This is nearly double the average move and comes despite results being largely in-line with expectations and earnings revisions no larger than normal.

For stocks up more than 10%, 85% of the move was explained by valuation re-rating. For those that moved down more than 10%, 65% of the move was from earnings downgrades.

This possibly implies an overly-bearish outlook going into reporting season.

Cyclical sectors were better than expected, whilst defensives were more likely to disappoint.

Operating margins contracted slightly, resulting in a 2% average hit to EPS.

The bigger impact was increased financing costs, with average interest expense up ~50% year-on-year, which dragged EPS down 6% on average.

Should interest rates stay at current levels, this implies a further 7-14% headwind to EPS in the next couple of years as fixed-rate debt rolls off. The other recurrent theme was upwards revisions to capex budgets, with a median +17% increase in capex for the half and +6% increase in consensus forecast for capex spending over FY24 / 25, largely driven by resources sector. This is driven by cost overruns and inflation rather than growth.

About Elise McKay and Pendal Australian share funds

Elise is an investment analyst and portfolio manager with Pendal’s Australian equities team. Elise previously worked as an investment analyst for US fund manager Cartica where she covered a variety of emerging market companies.

She has also worked in investment banking and corporate finance at JP Morgan and Ernst & Young.

Pendal Horizon Sustainable Australian Share Fund is a concentrated portfolio aligned with the transition to a more sustainable, future economy.

Pendal Focus Australian Share Fund is a high-conviction equity fund with a 16-year track record of strong performance in a range of market conditions. The Fund is rated at the highest level by Lonsec, Morningstar and Zenith.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.