The best-received earnings results in the ASX industrials sector had a few things in common. Pendal equities analyst ANTHONY MORAN explains

- Pricing power, interest expense, business cycles matter

- The weather makes a big difference to earnings too

- LIVE WEBINAR SEP 7: Register for Crispin Murray’s bi-annual Beyond The Numbers webinar

WHAT did the best-received results have in common this ASX earnings season?

Among industrials — which includes industries such as transportation and machinery — it was all about pricing power, cost of debt and where a company sits in its business cycle, says Pendal analyst Anthony Moran.

This marked a return to more typical themes after cost control, staffing and inflation dominated post-Covid reporting, Moran says.

The power of pricing

“Calendar 22 was a story of strong inflation … and companies were then all about doing what they could to keep up with inflation.

“What we’ve seen in the past six months is that input costs have eased in some cases,” Moran says, citing freight and energy costs.

“Some companies with pricing power have not only kept up with prices, but also been able to achieve some margin expansion. James Hardie is a really good example of that.”

In James Hardies’ case, volumes declined as the construction sector in the United States struggled, but margins increased.

“They’ve shown a lot of pricing power because they’ve got a very strong value proposition and a very strong market position. And we’ve seen some of their input costs come off,” Moran says, adding that it was a similar story for Boral in Australia.

“The contrasting example is [plumbing manufacturing company] Reliance Worldwide. By the nature of their products, they only have limited pricing power, particularly in the US.”

Cost of debt

Interest expense — the cost of debt — was a second theme emerging in the industrials sector.

“I’ve had a numebr of companies surprise to the upside, materially, on interest expense for financial year 2024,” says Moran.

“Because interest rates have gone up so much, it’s meant a few stocks have had 5 per cent downgrades just on interest expense.

“Amcor surprised on the extent of their interest expense step up in fiscal year 2024.”

Fellow packaging group Orora had a similar interest headwind, which took the edge off a positive 2024 outlook.

With interest rates higher and interest expenses normalising, an imbalance in price-to-earnings and Enterprise Value / EBITDA metrics in some stocks over recent years is coming back into alignment, Moran says.

“One of the reasons the PE ratio looked so cheap was the low interest expense, even when a company had a lot of debt on its balance sheet.”

Business cycles matter

A third theme of the earnings season was where companies are in their business cycles, Moran says.

“Not all sectors and countries economies are moving on one track.

“There are a variety of industry cycles running at different stages.

“So companies are seeing a range of end-demand experiences — and that could be driven by the country in which they operate”.

Moran refers to James Hardie and Reliance as cases in point.

Pendal Focus Australian Share Fund

Now rated at the highest level by Lonsec, Morningstar and Zenith

Due to the vagaries of the US housing cycle, strategies of home builders and the preponderance of fixed rate mortgages, there has an unexpected uptick in new housing starts, but the renovation sector remains in the doldrums.

“While James Hardie’s volumes were quite weak last half, it has exposure to this upside in new homes and that’s benefited their outlook.

By contrast, Reliance is exposed to the repair and remodel market … and hasn’t benefited from upside in new homes.”

And don’t forget the weather

As always, the weather matters, Moran says — particularly for building materials companies such as BlueScope and Boral.

“BlueScope has a diversified exposure to the Australian construction industry. Its volumes surprised to the upside in the last half year, and they will be flat in the current six months. It’s not seeing any great weakness,” Moran says.

“It’s not just resilient demand though — it’s also the good weather, which has moved from La Nina in FY22 to more benign conditions recently.

“That’s quite significant for Australian construction companies.”

About Anthony Moran

Anthony Moran is an analyst with over 15 years of experience covering a range of Australian and international sectors. His sector coverage has included Australian Industrials and Energy, Building Materials, Capital Goods, Engineering & Construction, Transport, Telcos, REITs, Utilities and Infrastructure.

He has previously worked as an equity analyst for AllianceBernstein and Macquarie Group, spending a further two years as a management consultant at Port Jackson Partners and two years as an institutional research sales executive with Deutsche Bank.

Anthony is a CFA Charterholder and holds bachelor’s degrees in Commerce and Law from the University of Sydney.

Pendal’s head of government bond strategies TIM HEXT explains the latest inflation data and what it means for the economic outlook

- Why bonds, why now? Pendal’s income and fixed interest experts explain

- Browse Pendal’s fixed interest funds

ANNUAL inflation fell below 5 per cent in July and looks on track to hit 4 per cent or lower by the end of the year as 2022’s higher numbers drop out.

The monthly Consumer Price Index data has been getting more and more comprehensive since first released in October.

More items have joined the monthly cycle and the Bureau of Statistics is now also publishing underlying measures.

On this front the falls are slower, with CPI excluding volatile items (fruit and veg, fuel and travel) falling from 6.1% to 5.8%. Trimmed mean (cutting off the highest and lowest 15%) fell from 6% to 5.6%.

Looking deeper though, the picture is mixed.

Despite a shift lower in goods inflation, services inflation remains stubborn as this ABS graph shows:

The biggest contribution to falling inflation is housing.

Although rents remain strong, the cost of new dwellings is leveling out. At 22% of the basket, housing is important.

Going the other way is insurance.

Anyone who has received a renewal this year can attest to that. However, it is only 2% of the basket.

The other main point we have made before is the ongoing impact of government subsidies on inflation.

These have largely stopped as we emerge from the pandemic, but they well and truly remain in energy.

Electricity rebates from the states meant the average 19.2% rise in prices on July 1 became only a 6% post-subsidy rise for consumers — which is what the CPI measures.

These rebates vary by states. They will reduce the inflation impact in 2023 but risk pay-back next year if the rebates end in 2024 as planned.

It may not feel like it, but electricity is actually only 2.2% of the CPI basket, so these massive moves aren’t game-changers — though there are second-round impacts.

What’s next

For the RBA though, the picture remains clear.

Inflation is moving to 4%. This reduces any urgency around further rate hikes.

Find out about

Pendal’s Income and Fixed Interest funds

The fixed-rate cliff is also now peaking, so overall rates are still rising independent of the RBA.

However, in 2024 the battle to get inflation back into the 2-3% band will be challenging and rate cuts seem a distance away.

Dr Michele Bullock takes over as RBA governor on September 18.

She will be keen to establish her inflation credentials so any move to a dovish outlook is unlikely.

For now, rates remain range-bound – as do risk markets.

About Tim Hext and Pendal’s Income & Fixed Interest boutique

Tim Hext is a Pendal portfolio manager and head of government bond strategies in our Income and Fixed Interest team.

Tim has extensive experience in banking, financial markets and funding including senior positions with NSW Treasury Corporation (TCorp), Westpac Treasury, Commonwealth Bank of Australia, Deutsche Bank, Bain & Co and Swiss Bank Corporation.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia.

Find out more about Pendal’s fixed interest strategies here

About Pendal

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

In 2023, Pendal became part of Perpetual Limited (ASX:PPT), bringing together two of Australia’s most respected active asset management brands to create a global leader in multi-boutique asset management with autonomous, world-class investment capabilities and a growing leadership position in ESG.

Here are the main factors driving the ASX this week according to our head of equities CRISPIN MURRAY. Reported by portfolio specialist Chris Adams

- LIVE WEBINAR SEP 7: Register for Crispin Murray’s bi-annual Beyond The Numbers webinar

- Find out about Pendal Focus Australian Share fund

MACRO signals were slightly softer last week, easing concerns about excess growth.

Fed chair Jerome Powell could have been seen as a touch hawkish in a speech at the annual Jackson Hole retreat last week.

But a careful reading indicates he is not expecting an economic re-acceleration which would necessitate further rate hikes.

People are still looking for further stimulus from China, but none is yet forthcoming.

In the US, AI chip maker Nvidia — which triggered the June quarter rally — reported its Q2 results and again blew away expectations.

But this time the stock stalled and did not fuel a NASDAQ rally — hindered perhaps by fuller valuations and the overhang of bond yields.

All combined, the market squeezed a little higher, with the S&P 500 up 0.84%, and bonds stabilising.

The S&P/ASX 300 fell 0.39% in what was the busiest week for company reporting, with substantial variations in stock performance.

The underlying theme is the economy seems fine and earnings are largely holding up for industrials.

While there are pockets of weakness in certain retail categories, these are outweighed by positive signals in travel, commercial demand and building materials.

There are no signs of recession and — with rates on hold — it is hard to see what would trigger one.

The only issue is at some point inflation trends may force the Reserve bank to re-evaluate, but that remains a little way off.

Signals from Jackson Hole

Chair Powell projected a stern tone last week, speaking of maintaining restrictive policy until inflation got back to 2% — as opposed to the “2% range”.

The Fed chair said nothing to change the market’s view that there would be no hike in September, noting the Fed could afford to “proceed carefully”, while remaining prepared to move if needed.

He also noted lags in the effect of monetary policy and the risk of doing too much as well as too little.

All this points to the Fed probably believing it has done enough and can afford to wait to see whether the economy cools further or not.

Should the economy show signs of re-accelerating, it is clear hikes will be back on. But we are well away from that case.

The limited move in 10-year bond yields (-2bps over the week) indicates there is little change to market expectations.

Also speaking at the Jackson Hole conference, European Central Bank president Christine Lagarde struck a hawkish tone on medium-term structural issues.

Lagarde referenced potential supply shocks associated with the energy transition and its call on capital as well as geoeconomic fragmentation.

She also highlighted a labour supply issue, where workers wanting fewer hours could drive up real wages, leading to supply shocks and greater second-order effects. Though she also noted Artificial Intelligence technology could provide some offset.

These are longer-term issues and go more to the potential for rates to stay higher for longer and to stabilise at a higher rate than the previous cycles, rather than a short-term signal.

Nvidia

The poster child for the AI zeitgeist delivered well above market expectations, with Q3 guided revenue of $US16 billion — 18% higher than Q2 and 170% higher than the same quarter last year.

This was 27% ahead of consensus expectations and implied earnings per share (EPS) for Q3 was 39% ahead of consensus.

This is driven by Nvidia’s data centre business, which is closely leveraged to AI. Sales in Q2 were 29% higher than market expectations.

Management indicated they expect supply to improve sequentially through 2024, suggesting they are avoiding bottlenecks holding back their growth.

The market is revising earnings upwards substantially on this theme.

Goldman Sachs, for example, raised its data centre revenue estimates 58% for FY24 and FY25 and EPS estimates by 55% and 52% respectively.

The chip-maker also announced a $US25 billion stock repurchase program, having done $3 billion in Q2.

The AI theme is alive and well and can underpin the broader ecosystem thematic.

While Nvidia’s stock was up 6% week-on-week, it fell back from the immediate post-result reaction.

This signal is worth noting. After a move of about 215% so far this year, it suggests positioning is now full and the earnings beat is helping sustain that, rather than drive it further.

US retail earnings

A number of smaller US discretionary retailers put out negative news, signalling that trading conditions deteriorated from July to August.

Key points included the growing impact of theft and some signs of credit deterioration.

Dick’s Sporting Goods, Macy’s and Dollar Tree all fell sharply.

Previously signals from likes of Walmart and Ross Store had been more positive, so the full picture is still unclear.

This is worth watching as a possible change in trend.

Markets

Australian earnings season is painting a picture of an economy that remains in good shape with very little evidence of slowdown.

Qantas is seeing good travel demand. Wesfarmers has indicated no signs of weakness in Bunnings or K Mart.

Woolworths notes that demand remains decent, though there are signs of downtrading to cheaper items.

BlueScope Steel expects strong demand for building products through to year end.

Fuel retailers Viva Energy and Ampol are seeing strong commercial demand for fuel — and Domino’s is seeing signs of life in pizza demand.

Where there were poorly-received results, it was often company-specific such as Coles struggling with a surge in theft, Ramsay Health Care facing cost pressures, or Wisetech investing in new products.

There was also some offshore impact such as Reliance Worldwide’s exposure to the repair and remodelling market in North America and Iluka’s headwind from muted zircon demand in China.

The other feature of the current markets is the impact of prior investor positioning.

We are seeing unloved names performing well if there is no bad news (eg Altium and Domino’s Pizza) and well-owned names struggling if there is no new good news (eg Wisetech, Coles, Cleanaway).

The risk looking forward is whether waning momentum in revenues will leave companies exposed to ongoing cost pressures.

About Crispin Murray and Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia. Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions.

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

The mortgage cliff may not yet have appeared, but we’re only halfway through the roll-off of Covid-era fixed-rate loans, points out Pendal assistant PM ANNA HONG

- Why bonds, why now? Find out more from Pendal’s income and fixed interest team

AUSTRALIAN house prices look to have turned the corner.

But what about mortgage stress?

We’ve repeatedly heard the mortgage cliff warnings since the Reserve Bank started hiking rates.

Yet the cliff doesn’t appear to have appeared.

It’s bank reporting season and the latest updates show mortgage arrears remaining relatively stable, only picking up slightly in the June quarter.

Delinquencies have hardly budged.

It appears that the system is coping just fine. Of course, this does not mean that everyone is.

Despite the positive picture, we are by no means out of the woods.

Most Aussie borrowers who fix their mortgage do so for three years or less.

This means 85 per cent of pandemic-era fixed-rate loans are set to expire by the end of 2024.

As you can see in the graph below, we’re only half-way through the roll-off.

We are at the peak and will remain here into year-end.

The true test of the Australian residential mortgage resilience will only come if significant increases in unemployment collide with repayment stress.

For now, the path to expected higher unemployment is due more to immigration lifting labour supply above demand.

Importantly though, this does not mean people losing their jobs.

For some, the stress is and will be very real.

But for the system, higher rates will be more of a speed bump than a cliff.

What does this mean for investors?

Perhaps, the RBA may yet achieve the narrow path they set out on.

Find out about

Pendal’s Income and Fixed Interest funds

About Anna Hong and Pendal’s Income and Fixed Interest team

Anna Hong is an assistant portfolio manager with Pendal’s Income and Fixed Interest team.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia.

With the goal of building the most defensive line of funds in Australia, the team oversees some $20 billion invested across income, composite, pure alpha, global and Australian government strategies.

Find out more about Pendal’s fixed interest strategies here

About Pendal Group

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

A long-awaited and bigger-than-expected rate cut in Brazil could usher in a positive cycle of growth for Latin America’s biggest economy. JAMES SYME explains

- Brazil cuts rates

- Positive cycle ahead

- Find out about Pendal Global Emerging Markets Opportunities fund

- Watch a recent Emerging Markets overview webinar with James Syme

INVESTORS are underplaying the likelihood of further rate cuts in Brazil, which is showing signs of entering a classic emerging markets virtuous cycle of capital inflows, strengthening growth and rising markets.

That’s the view of James Syme, who co-manages Pendal Global Emerging Markets Opportunities fund.

Brazil cut its key interest rate by a larger-than-expected 50 basis points in its August meeting.

The central bank took the rate from 13.75 per cent to 13.25 per cent, ending eight months of keeping borrowing costs on hold.

Markets expect further cuts to 12 per cent by the end of the year and 9.25 per cent by the end of next year.

But Syme says those expectations are likely short of the mark and a positive cycle of rate cuts and economic growth lies ahead.

“Emerging markets tend to overshoot to the downside and then to upside.

“We think Brazil is setting up to be in a cycle of much more positive news, and that should be reflected in equity prices as well.

“We’ve been talking about rate cuts coming in Brazil for a couple of years and they have now surprised markets with the size of the first cut.

“We don’t think this is the last of those surprises.”

Self-reinforcing cycles

Emerging markets tend to move in self-reinforcing cycles of rate cuts and economic growth attracting capital flows, which strengthen the currency, allowing for reduced inflation and further rate cuts, says Syme.

Find out about

Pendal Global Emerging Markets Opportunities Fund

“There’s a traditional view among investors that markets reflect the real world.

“You have a set of fundamental conditions and the output of them is what happens in markets, whether it’s exchange rates or stock markets or individual share prices, or bond yields.

“But we think what happens in markets also drives what happens in the real world.

“That means what happens with currencies, interest rates and bond yields has a real world effect.

“We think we’re heading to a point where we’re going to see that in Brazil, where a stronger currency, a stronger equity market, and declining bond yields feed back into the Brazilian economy.

“In these kinds of emerging markets, these are very positive, self-reinforcing cycles.”

Domestic demand stocks to benefit

Syme says investors can best take advantage of the rosy outlook by focusing on companies exposed to domestic demand.

“It’s going to be about banks and other financials, consumer durables and autos, services and leisure, construction and capital investment, and real estate,” he says.

“Now, that doesn’t mean we’re going to end up with exposure to all those sectors because we need to be selective at a sector and stock level as well. But those are the main beneficiaries.”

A rising level of new stock issuance is also a vote of confidence in Brazil’s outlook.

“Companies are raising capital to take advantage of the improving economic situation. We see that as a statement of a positive intent by corporate Brazil.

“One of our newer holdings in the fund is the company that operates the Brazilian stock market, which is a business that could really benefit from this.”

More rate cuts likely

Syme says the opportunity for rate cuts in Brazil is illustrated by the gap between its interest rates and inflation measures compared to other economies.

“Brazil’s inflation level is about the same as the US — but US rates are at 5.5 per cent.

“That’s a nearly eight percentage point gap so just the carry alone should attract lots of capital into Brazil.

“We think that economic data should pick up quite strongly as rate cuts come through.

“This is how emerging markets investing works — the bad times are bad, and the good times are good.

“A lot of the markets we like are doing very well right now including Mexico, India and Indonesia.”

About Pendal Global Emerging Markets Opportunities Fund

James Syme, Paul Wimborne and Ada Chan are co-managers of Pendal’s Global Emerging Markets Opportunities Fund.

The fund aims to add value through a combination of country allocation and individual stock selection.

The country allocation process is based on analysis of a country’s economic growth, monetary policy, market liquidity, currency, governance/politics and equity market valuation.

The stock selection process focuses on buying quality growth stocks at attractive valuations.

Find out more about Pendal Global Emerging Markets Opportunities Fund here

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

Here are the main factors driving the ASX this week according to our head of equities CRISPIN MURRAY. Reported by portfolio specialist Chris Adams

- LIVE WEBINAR SEP 7: Register for Crispin Murray’s bi-annual Beyond The Numbers webinar

- Find out about Pendal Focus Australian Share fund

A COMBINATION of northern hemisphere summer doldrums and limited data is keeping news-flow reasonably quiet.

US and Australian bond yields are both re-testing cycle highs, capturing a lot of attention.

Rising bond yields and a stronger US dollar saw equities fall last week, continuing their consolidation from the end of July. The S&P 500 fell 2.05% and the S&P/ASX 300 lost 2.34%.

The market is also focused on weakness in China’s economy.

Along with talk of inventory reductions, this encouraged a continued sell-off in the lithium complex. Though iron ore miners maintained their remarkable resilience.

Softer Australian employment data helped drive our dollar lower versus the USD.

In local ASX results, season operational performance has largely been solid. But there have been concerns about debt costs for the more leveraged companies.

China

The Chinese economy remains under intense scrutiny.

This was maintained last week by concern of the imminent default of property developer Country Garden, missed payments from investment company Zhongrong Trust and a continuation of weak economic data.

The challenges are symbolised by Beijing’s decision to stop publishing data on youth unemployment — which stands at about 21 per cent.

Data on land sale volumes and consumer confidence are also suspended in the name of maintaining confidence.

Confidence is the key issue:

- High youth unemployment deters consumer spending

- Fears about the solvency of private developers discourage new home purchases, due to the risk that dwellings may not be completed

- Investment trust defaults such as Zhongrong’s may trigger redemption requests, leading to a liquidity squeeze

This lack of confidence can be seen in a lack of private investment, which is down 7 per cent in the first seven months of 2023, versus state-owned-enterprise investment up 12 per cent.

Concern over property lies at the heart of the confidence problem. New housing starts are down more than 60 per cent from the 2019 peak.

There was a widely-held expectation that the market would stabilise following such a dramatic decline.

But July data indicates the weakness continues.

Goldman Sachs cut its forecast for 2023 new housing starts from -10% to -20% on the previous year and expects the property sector to detract 1.5% from GDP growth.

Beijing’s 2023 GDP target of 5% was initially seen as something of a low-ball target which could be exceeded.

Now the market is cutting GDP forecasts to sub-5% as we see recent trends in retail sales, auto sales and other indicators start to slow.

There have been a number of policy initiatives, including some interest rate easing and bringing forward some spending by local governments.

But these measures have been incremental and unable to reverse deteriorating sentiment.

While this is a bearish portrait, some China-related stocks and sectors on the ASX have held up — notably the miners.

The bulls are taking the view that things are so bad, they’re good — which would increase the chance of a more convincing policy response such as the one we saw in 2015.

They are drawing a comparison with the period prior to the reversal of the Zero-covid policy, where there were incremental signals before the major policy change.

There’s also a theory that Beijing is biding its time, reasoning there would be no point launching an initiative in high summer as it wouldn’t get traction. Beijing may be waiting until September, the theory goes.

If a major policy response doesn’t materialise, we see some risk around bulk commodity producers at these levels.

US macro outlook

US GDP surprised to the upside with 5.8% growth in the second quarter.

The market is trying to understand how this can happen.

Some relates to higher investment.

It’s too early for the Inflation Reduction Act (IRA) to be felt, but the 2022 CHIPs and Science Act (CHIPS stands for Creating Helpful Incentives to Produce Semiconductors) of 2022 is having some effect.

Consumption, however, is the main driver.

One observation is that business tax refunds have surged since March, adding an additional $100 billion in potential spending power.

A lot of this relates to small business and is tied to the Covid-era policy of employment-retention tax credits.

This policy, which remains in place until 2025, is seeing business tax refunds run at four times pre-pandemic levels.

The policy’s original costing was US$85 billion over 10 years. It has cost US$150 billion in the past 12 months alone.

This is a good example of how some stimulative fiscal settings have become entrenched and are helping the economy outperform expectations.

The stronger economic outlook can also be seen in the Atlanta Fed’s GDP NOW measure, which is indicating an almost 6% growth in GDP for the third quarter.

We suspect this is overstated. But it still retains a healthy buffer over the 1& to 2.5% range of forecasts from consensus.

The New York and Philadelphia Fed regional manufacturing surveys appear to be bottoming, reinforcing the soft-landing case.

They are also signalling a pick-up in prices received, which may give the Fed some pause for thought.

This more resilient economy means markets are expecting interest rates to stay higher for longer, and reinforce the view that real rates need to stay higher for this cycle.

Combined with structural pressure on the government budget deficit from funding costs and more legislated spending — plus extra supply and lower offshore demand for treasuries — this helps explain the increase in bond yields.

It also suggests that while the market is bearish on bonds — allowing potential for a near-term reprieve — we should not expect a sustained reversal in yields.

Markets

Australian equities were down last week, in line with the US.

Only REITs (+1.27%) held up, largely due to the influence of Goodman Group.

Lithium names were weak on a macro trade against them.

Domestic high-yield names were also soft, partly due to the realisation that bond yields were staying higher.

About Crispin Murray and Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia. Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions.

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

Pendal’s head of government bond strategies TIM HEXT explains the latest wage data and what it means for rates and bonds

- Why bonds, why now? Pendal’s income and fixed interest experts explain

- Browse Pendal’s fixed interest funds

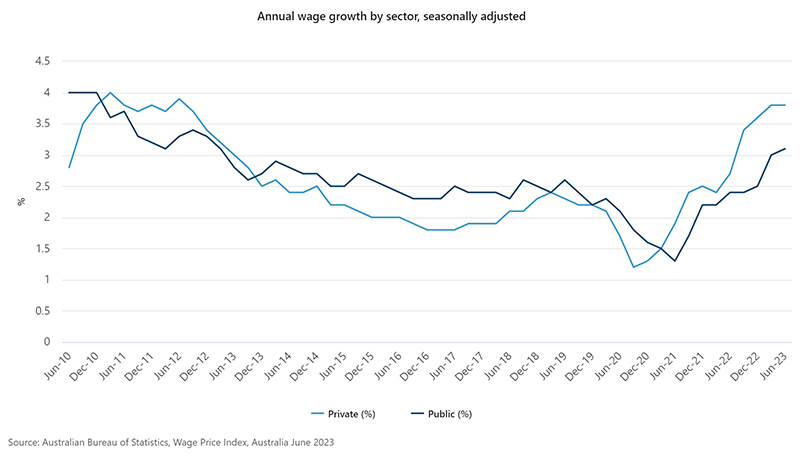

WAGE growth – a key indicator that the Reserve Bank monitors when weighing up rates decisions – was surprisingly benign in the June quarter.

The Bureau of Statistics published the latest Wage Price Index on Tuesday.

The index, which measures changes in salary across 18 industries, showed overall wages grew by only 0.8% in the period.

We’ve now had three quarters in a row of 0.8%.

This indicates an annual rate of only 3.2%. Though a 1.1% number last September gives us an annual rate of 3.6% with rounding.

More surprising is that public sector wages grew only 0.7% in the quarter.

This remains below private sector wages — mostly because three-year agreements in the public sector are slower to respond to changing dynamics.

The opposite was true as wage growth fell across most of the last decade — as you can see in the ABS graph below.

This lower public sector result comes despite a trend for public sector workers to get at least 4% in agreements.

The federal government is now offering 4% next year to unions (and 3.5% and 3% the following years).

Unions have rejected this.

The NSW government has agreed to 4% from July for more than 80,000 workers covered by the Public Service Association.

Teachers and nurses across a number of states have received 4% wage increases over the past 12 months.

Governments offered additional incentives and payments to avoid higher increases given the inflation backdrop.

Wages across the economy are likely to settle on 4% rises for several years yet.

Actual inflation is going to be around 4% and unless unemployment has a very large rise employees will maintain a level of bargaining power.

This 4% is the new 2.5% that we got used to last decade.

GDP data shows a different story

Note that the Wage Price Index is but one measure of renumeration.

Find out about

Pendal’s Income and Fixed Interest funds

It measures salary across 18 industries on a like-for-like jobs basis through time.

It does not account for overtime, bonuses, shifts across industries or the extra 0.5% of super paid each year as we move from 9.5% to 12%.

During strong job markets the index underestimates the total renumeration employees are receiving.

When measuring total compensation of employees we rely on GDP data.

This points to total compensation growing closer to 6%, which partly explains the resilience of the economy.

Since even this data lags by three months, Pendal also tracks data from a number of business liaison surveys to create our own diffusion index.

This currently points to wages being a touch above 4%, in line with the RBA forecast for year end.

What it means for rates and bonds

Overall, the wages number continues to buy the RBA time, with steady cash rates for now.

The market now has a bit less than one hike priced in – and that’s towards year-end or early 2024, so there’s no clear opportunity around mispricing.

Short-ends should remain rangebound for now.

Longer bonds remain vulnerable to higher long-end rates globally.

About Tim Hext and Pendal’s Income & Fixed Interest boutique

Tim Hext is a Pendal portfolio manager and head of government bond strategies in our Income and Fixed Interest team.

Tim has extensive experience in banking, financial markets and funding including senior positions with NSW Treasury Corporation (TCorp), Westpac Treasury, Commonwealth Bank of Australia, Deutsche Bank, Bain & Co and Swiss Bank Corporation.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia.

Find out more about Pendal’s fixed interest strategies here

About Pendal

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

In 2023, Pendal became part of Perpetual Limited (ASX:PPT), bringing together two of Australia’s most respected active asset management brands to create a global leader in multi-boutique asset management with autonomous, world-class investment capabilities and a growing leadership position in ESG.

Here are the main factors driving the ASX this week according to our head of equities CRISPIN MURRAY. Reported by portfolio specialist Chris Adams

- LIVE WEBINAR SEP 7: Register for Crispin Murray’s bi-annual Beyond The Numbers webinar

- Find out about Pendal Focus Australian Share fund

THE US equity market is catching its breath, down 0.27% last week (S&P 500) with limited news-flow and waning recession fears.

JP Morgan joined Morgan Stanley and Bank of America in removing their recession forecasts.

Meanwhile, US post-result earnings revisions continue to come in better than expected.

Offshore bond yields moved higher, despite US CPI coming in slightly softer than expected. US 10-year government bond yields rose 12bps and two-year yields 13bps last week.

This led to some rotation away from tech towards healthcare in the US, exacerbated by a market that has been generally long the former and short the latter.

This may signal some mean reversion with a 33% relative outperformance in tech so far in 2023.

Energy was also stronger on fears of union-led strikes at three Australian LNG projects. European gas prices are up 30% this month.

Chinese CPI and PPI both went negative year-on-year for only the second time since 2009 (the other time was during Covid). Concerns around China’s economic outlook continue to grow.

Australian equities were also flat (S&P/ASX 300 +0.26%). Early results from reporting season are slightly favourable in aggregate.

Commonwealth Bank’s (CBA, +2.48%) result eased fears on bank margins while Suncorp (SUN, -5.02%) and QBE Insurance (QBE, -3.52%) flagged higher near-term claims inflation in Australia.

In combination, this led to some reversal in performance between banks and insurers. We don’t believe this will last too long.

James Hardie (JHX, +13.37%) and Nick Scali (NCK, +13.59%) were the pick of the results last week. Both these cyclicals are doing better than feared, with margins helped by lower input costs.

Finally, the Aussie economy has found another way to defy doomsayers with payments platform Airwallex estimating a $7.6 billion economic boost from the FIFA Women’s World Cup.

And that was before Saturday night’s result.

US inflation and the effect on interest rates

Core July CPI rose 0.16% for the second consecutive month, which was seen as slightly better than consensus expectations.

The breadth of inflation also continues to fall –‑ the percentage of CPI components with deflation has now increased to 25%.

Annualised headline CPI ticked a little higher –- largely the result of energy deflation starting to reverse.

If core CPI is adjusted for observed rents and the volatile component of used autos is removed, it is running at a three-month annualised rate of 2.2%, which is back towards the Fed’s target.

All this is positive and we are likely to see lowish CPI prints in September and October.

This view is expected to let the Fed hold rates steady in their September meeting. The question remains whether this is enough to remove the last hike they still currently predict.

Lower inflation reduces the risk of the Fed being forced to drive the economy into recession, since it suggests there needs to be less of a rise in unemployment to bring inflation back to target.

One caveat is that three current tailwinds are unlikely to be sustained:

- Airfares are running at -8% and are likely to normalise

- Used car prices are set to fall for a couple more months, but then stabilise

- The medical care service component is falling 4%. This is an imputed number, which will be reset for the October CPI (released in November). It relates to health insurance and will start rising — though we note this component is not included in the PCE Deflator measure favoured by the Fed.

On this basis, we could be back to 28-30bp monthly increases in inflation come the December quarter.

This would probably deter the Fed from cutting rates in the first quarter of 2024.

Inflation hawks are concerned that the recent easing of pressure has been exaggerated by the reversal of Covid-related distortions.

Wage pressure remains a key signal for Fed intentions.

While this is a lagging indicator, the employment gap continues to rise. This is not consistent with wages dropping enough to satisfy the Fed.

At this point it would probably take a much weaker US economy in early 2024 to change the view that the Fed does not starting cutting rates in Q1.

There is still a view that we could see a recession, with some pointing to the shift upwards in real rates, which can more than offset the recovery in real wages.

Bond yields – what’s driving the rise in long-end rates?

The US 10-year government bond yield has backed up and is approaching the 4.2% highs of last October and November.

This is interesting because inflation data has improved and the short end of the yield curve is also holding in.

This suggests yields are not being driven higher by an expectation of higher interest rates.

There are several theories on what is driving this move:

- Some see the economy’s resilience despite higher interest rates as a signal that real rates need to remain higher for longer.

- Potential concerns over the long-term fiscal position of the US, given the rise in debt / GDP at a time when fiscal spending growth and interest costs remains high. If real rates need to remain higher for longer to contain inflation, this becomes more of an issue for the sustainability of the US fiscal position.

- The US sovereign credit rating downgrades from Fitch, which is a symptom of the above two points.

- Japanese Government Bonds (JGB) act as something of an anchor for world rates and the recent change in strategy by the Bank of Japan has seen JGB yields rise –- though they stabilised at below 60bps last week.

- Supply and demand can also be a nearer-term factor, but one that historically does not add much to bond yields. Foreign central banks have reduced demand of US treasuries for a variety of reasons. US banks –- another historically large buyer –- have less liquidity as money supply falls. At the same time, Treasury supply is high given deficits and fiscal spending.

Whatever the reason, this remains an important issue to watch.

The risk is that if bond yields continue to break higher it may start to weigh on equity markets as the relative appeal of the two assets shifts.

There is no sign of this yet, although it may have acted as a drag on technology stocks in the last two weeks.

China deflation and property developer concerns

Last week we saw both Chinese annualised CPI and PPI turn negative for only the second time since 2009 (the other occasion was during the Covid lockdown).

This has coincided with weak export data (-14.5% in July).

At the same time China’s biggest private property developer Country Garden is warning of big first-half losses triggered by high levels of debt and continued weakness in Chinese property sales.

This is raising concerns over refinancing risks, potential default and the need to restructure debt.

This is not having the same contagion effect of last year’s Evergrande issues. But the combination of these signals reinforces concerns that structural factors are overwhelming Beijing’s ability to stem poor confidence affecting the economy.

The risk here to Australian equities in around commodity prices, which have so far held up on the expectation of policy support.

If confidence in a policy response wanes, this could see weakness in the Australian resource sector.

On the other side, there is still the possibility that policy makers change tack, launching a massive program to reflate the economy.

Potential Australian LNG strike

The price of gas inEurope moved 30% higher last week to about EUR37 per megawatt hour (mwh) on fears of a potential strike at Chevron’s Wheatstone and Gorgon facilities and Woodside’s North West Shelf –- all in Western Australia.

Combined, they represent 10 per cent of the global seaborne LNG market –- a reminder of the importance of Australian supply to global markets.

There are signals the strike may be a bargaining tactic rather than a true threat, but it does highlight the way gas markets pricing works.

In the event this supply is removed, that energy has to be substituted.

The first substitute is coal, which would require gas prices of EUR40-50/mwh.

If this was insufficient -– for example if we saw a cold Northern hemisphere winter -– oil would need to be priced as an alternative which implies EUR70-100/mwh.

This equates to an LNG price of US$20-30 per metric million British thermal units (MMBtu) as opposed to the recent price range of US$9-10 MMBtu.

Gas prices have remained lower than market expectations this year due to a lack of recovery in industrial demand — particularly in Europe -– due to ongoing inventory run-downs.

This boosted the European and global economy as it helps inflation and keeps power prices lower, supporting consumption.

Any disruption to this risks reducing growth expectations.

Markets

The market looks to be consolidating, with no major change in sentiment other than the liquidity overhang and a seasonally weaker time of year for equities.

One interesting sectoral point is the strong outperformance early cyclicals, driven by tech and homebuilders. This has left the sector near extremes in terms of historical outperformance of defensives.

The risk of some reversal here is high, given the shift in sentiment on the US economy has largely played out.

In Australia, performance was largely driven by results so far.

Retailers did better on more positive anecdotes, notably from Nick Scali.

Banks outperformed on CBA’s message that margin pressure has eased.

Insurers noted claims inflation in Australia remained very high –- running at about 15% in motor insurance due partly to higher repair costs.

The early theme in reporting season was a bounce among cyclical stocks with low expectations when market fears weren’t realised.

About Crispin Murray and Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia. Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions.

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

China’s property sector woes continued this week as another big property developer found itself in trouble. AMY XIE PATRICK explains

- Take caution with China’s latest property signal

- Why bonds, why now? Pendal’s income and fixed interest experts explain

- Browse Pendal’s fixed interest funds

China’s property sector woes continued this week as another big property developer found itself in trouble.

Privately-owned Country Garden — China’s biggest property developer based on last year’s contracted sales — missed US$22.5 million in payments on two bonds.

The company is described as facing “periodic liquidity stress” in a Reuters report. In other words, it’s running out of money.

The bonds now enter a 30-day grace period. To avoid a default, Country Garden must find enough funds to meet coupon payments before the grace period expires.

The market has been bracing for more trouble since a spate of property sector defaults in China during 2022 — including the high-profile default of Evergrande.

At the end of July, Country Garden’s US dollar bonds were trading at 20% to 25% of face value. A high risk of default had been priced in.

Now that two coupon payments have been missed, the probability of default has skyrocketed, causing bonds to dip further to 8c on the dollar, closing in on all-time lows seen last November.

The market values these bonds at such low recovery rates because of rules in China that restrict foreigners from owning physical assets onshore.

If Country Garden defaults on the bonds, it’s likely creditors on their US dollar denominated senior unsecured bonds would stand behind onshore equity holders in the queue to get their money back.

What’s next?

On this occasion, Country Garden will probably find enough money to pay the coupon within the 30-day grace period.

The company’s chairwoman holds stakes in Country Garden Services, an affiliated entity and is expecting a dividend payment of around US$60 million this month.

One could speculate that some of those funds are already slated for curing the missed coupon payments.

But this doesn’t solve the “periodic liquidity stresses”.

For the remainder of the year, Country Garden needs to find US$2 billion of funds to satisfy other payments of principal and coupon on outstanding US dollar denominated bonds.

On top of this, the company needs ongoing cash to complete projects already pre-sold to customers.

As the confidence crisis in the property sector deepens in China, the feedback loop has been vicious.

Levered property developers need strong and sustained momentum in new pre-sales to fund the completion of older pre-sales.

In Country Garden’s case, a minimum of monthly contracted sales of RMB 28-30 is needed to complete a pipeline of earlier pre-sold homes.

In 2021, monthly sales averaged around RMB 40-45 billion. Today monthly sales are down to around RMB 12 billion and falling.

This is what is causing the “periodic liquidity stress” — though I would describe it as existential rather than periodic.

An end to endless demand

The breadth of Country Garden’s operations is vast.

Many of its unfinished projects are in China’s third-tier (or lower) cities.

When the population thought property prices could only go up, these cities benefited from endless demand. But the current crisis has turned everything on its head.

Populations in these less prosperous are in net outflow. These are not the cities that first-time buyers are rushing to anymore.

The company considered an equity raise, but decided to scrap the idea at the end of last month, likely as a result of “no takers” after testing the waters for indications of interest.

The only hope left is help from the government. So far, Beijing is not rushing to their “model” developer’s aid.

Hundreds of thousands of buyers waiting on delivery of Country Garden homes could be affected if the company goes to the wall.

Half-finished building projects would freeze while assets were sold, haircuts negotiated, and left-over funds paid out.

Find out about

Pendal’s Income and Fixed Interest funds

But it is one way to break the vicious cycle between defaulting developers and plummeting buyer confidence.

With the right haircut, the assets of Country Garden are attractive to other developers in a stronger liquidity position.

A default at Country Garden forces the company to take these inevitable haircuts, and lets stronger companies resume the completion of unfinished projects.

Once buyers started getting delivery of finished homes, the urgency to dump these homes at fire sale prices in the secondary market would start to reduce, allowing home prices to stabilise.

Stable house prices then lead to a more stable confidence around the sector and the economy more broadly.

This is not the sugar hit the market has hoped for. But it is likely the structural change that is badly needed in the Chinese economic growth model.

In the meantime, we expect a slight loosening of restrictions on developer access to funding, to prevent a domino effect of Country Garden’s current cash crunch on the rest of the sector.

What it means for global growth

The investment implications from the latest casualty in China’s property crash are fairly straightforward.

China’s weight on the global growth picture will become more apparent as the rest of the world burns through its buffers.

That means being more overweight in duration of developed markets than through China bonds directly.

As China tries to pull other levers to lessen the pain, a weaker currency becomes the easiest release valve. Buy US dollars against the yuan on dips in the pair.

And as China races ahead on electric vehicle production, tread with caution on traditional autos sector exposures.

Most are finding it hard to keep up with the fast-growing Chinese alternatives.

About Amy Xie Patrick and Pendal’s Income and Fixed Interest team

Amy is Pendal’s Head of Income Strategies. She has extensive expertise and experience in emerging markets, global high yield and investment grade credit and holds an honours degree in economics from Cambridge University.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia. The team oversees some $20 billion invested across income, composite, pure alpha, global and Australian government strategies.

Find out more about Pendal’s fixed interest strategies here

About Pendal Group

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

Here Pendal’s head of government bond strategies TIM HEXT points out what to pay attention to in the RBA’s latest monetary policy statement

- Why bonds, why now? Pendal’s income and fixed interest experts explain

- Browse Pendal’s fixed interest funds

WHEN the Reserve Bank releases its quarterly monetary policy statement I look for two things.

Firstly, what are the forecasts?

There’s usually new information there, though often the preceding monetary policy decision mentions them earlier.

The second thing I look for are the two blue breakout boxes usually featured in the statement.

“Box A” and “Box B” are typically special interest topics – importantly, topics of special interest to the RBA.

They offer an insight into what topics our central bankers are discussing and investigating internally.

Sometimes there are clues as to what may follow.

In the latest statement released on Friday, Box A contains a rather technical article titled The Bond-Overnight Index Swap Spread and Asset Scarcity in Government Bond Markets.

Box B’sarticle is Insights from Liaison, which summarises discussions with 230 Australian businesses, industry bodies, government agencies and community organisations between May and August.

The first would appear to be of interest to very few, outside of bond geeks like me.

Clearly though, the RBA is looking at the pros and cons of quantitative tightening, which should be of interest to investors. More on this another time.

The business liaison box is significant. The RBA has often referred to this extensive program, but has only recently started sharing specific data.

Box B reveals a growing view that businesses are seeing an easing in both demand and costs, consistent with an increasingly neutral RBA.

Of particular interest is the graph below:

This graph shows an easing of expectation for wage rises in the year ahead.

Perhaps this is not surprising as actual inflation falls to 4%.

But the most popular indicator of wages, the Wage Price Index, is not forecast to peak until the end of this year at slightly above 4%.

This liaison shows the RBA will likely stare down commentators who talk about higher wages meaning further rate hikes.

Overall, the RBA’s August monetary policy statement should be reassuring for Australian bond investors.

However, a recent US fiscal surge seems to be weighing on US bonds and therefore curbing gains here.

But let’s save that topic for next time.

Find out about

Pendal’s Income and Fixed Interest funds

About Tim Hext and Pendal’s Income & Fixed Interest boutique

Tim Hext is a Pendal portfolio manager and head of government bond strategies in our Income and Fixed Interest team.

Tim has extensive experience in banking, financial markets and funding including senior positions with NSW Treasury Corporation (TCorp), Westpac Treasury, Commonwealth Bank of Australia, Deutsche Bank, Bain & Co and Swiss Bank Corporation.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia.

Find out more about Pendal’s fixed interest strategies here

About Pendal

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

In 2023, Pendal became part of Perpetual Limited (ASX:PPT), bringing together two of Australia’s most respected active asset management brands to create a global leader in multi-boutique asset management with autonomous, world-class investment capabilities and a growing leadership position in ESG.