Here are the main factors driving the ASX this week, according to investment analyst JACK GABB. Reported by portfolio specialist Chris Adams

THE biggest down day for the S&P 500 since May set the mood last week, triggered in part by credit rating agency Fitch downgrading the US to AA+.

Stronger-than-expected employment data, higher upcoming US debt issuance and further gains in Japanese yields added fuel to the flames.

Treasuries and equities sold off, with stock-bond correlation the highest it’s been since the 1990s.

The US 10-year yield rose 8bps and the yield curve steepened. The S&P 500 ended the week down 2.26% despite 79% of companies beating consensus estimates in the first week of reporting season.

In Australia, the RBA held rates steady. This surprised most economists but was largely in line with the market, which was pricing in a 30 per cent chance of a hike.

In contrast, the Bank of England raised rates another 25bps to 5.25% and signalled rates were likely to stay higher for longer.

Australia equities fell (S&P/ASX 300 -1.17%), but less than most overseas markets.

Overall, data for the week was generally consistent with slowing inflation, despite continued earnings and jobs strength.

Central banks remain concerned around the stickiness of services inflation, but expectations for further hikes continue to fall.

Arguably, the key debate around central banks is how long rates stay elevated.

Oil is also worth watching. Brent crude is now up 15% and West Texas Intermediate (WTI) is ahead 17% for the quarter to date.

This is driven by a record drop in US stockpiles and a decision by Saudi Arabia and Russia to extend production cuts.

Gasoline is the sixth-biggest component of US CPI.

US economics and policy

The data last week was generally consistent with slowing inflation and a soft landing. Two Fed members pointed to the labour market coming into better balance.

Despite uncertainty about a potential lagged impact of rate hikes and whether a recession can be avoided, expectations for further hikes continue to come down.

The market is pricing the probability of another Fed hike by November at just 18%, versus 32% in Australia.

Still, at least one Fed member still sees the need for further hikes. Governor Michelle Bowman said “additional rate increases will likely be needed to get inflation on a path down to the FOMC’s 2% target”.

Labour market data remains solid.

Non-farm payrolls came in at 187k new jobs, versus 200k expected, and the prior two months were revised down 49k.

Employment data has shown increasing signs of cooling this year, though 200k jobs per month is still strong by historical standards.

On the other hand, wages rose more than expected with average earnings +4.4% year-on-year versus 4.2% expected.

Along with a low unemployment rate (3.5% vs 3.6% expected), this suggests the labour market remains tight and inconsistent with a 2% inflation target.

We will get two more inflation prints (the first this Thursday) before the next Fed meeting in September.

Find out about

Pendal Horizon Sustainable Australian Share Fund

Consensus is forecasting headline CPI at 3.3% versus 3% prior. Excluding food and energy, the forecast is 4.8%, unchanged from prior.

Assuming no surprise — and the CPI prints confirm the June trend, hike expectations likely remain low.

Soft landing odds rising, bears capitulating

The bears have continued to capitulate, with Bank of America the first of the major US banks to officially reverse its recession call.

Bears now forecast US GDP growth of 0.7% in 2024 — 0.7 percentage points higher than was previously assumed.

However, inflation expectations have been revised to 2.8% in 2024 (+0.4 points) and 2.2% in 2025 (+0.1 points).

Unemployment is seen peaking at 4.3% in Q1 2025 versus the prior expectation of a peak at 4.7% in Q4 2024.

Soft landings are uncommon, with only three in the eleven recessions since World War II.

Concern remains over the lagged impact of rate hikes. While the US yield curve has steepened materially (and Australia is now back in positive territory), it has now been inverted for 13 months.

Ultimately, interest rates are coming down — the important factor will be why.

If it’s in response to a recession, the precedent for equities is not positive based on historical patterns.

US earnings season

Some 422 S&P 500 companies had reported Q2 earnings by the end of last week — with 79% beating analyst expectations.

This is more a function of low expectations rather than stellar corporate performance.

Based on Goldman Sachs data:

- 55% of companies have beaten consensus estimates by at least one standard deviation, versus historical average of 48%.

- Only 12% of companies have missed consensus estimates by at least one standard deviation, versus historical average of 13%.

- EPS growth has been tracking at -6% versus -9% expected.

A few noteworthy results:

- Apple (-7.1%) — Now well below its historic $3 trillion market cap after reporting a third straight quarter of declining sales and guiding to a similar performance in Q4

- Amazon (+5.6%) — Q2 beat and guidance across retail and AWS (cloud) was strong

- Uber (-6.1%) — Reported its first-ever operating profit, but shares declined on slower growth

- PayPal (-15.2%) — Declined on lower transaction take rates and margins

- Caterpillar (+6.1%) — reported a big earnings beat, but noted Chinese demand was worse than was forecast only three months ago

- Starbucks (-0.6%) — Better margins offset lower comparable sales

- Expedia (-14.1%) — Q2 gross bookings missed expectations

- Booking (+1.7%) — Revenue and profits beat. FY booking growth guidance raised to >20% from low-teens

- Atlassian (+14.1%) — Reported better guidance. Cloud revenue growth seen +25-27% YoY

UK and Europe

The BoE hiked 25bps, as expected.

Rates are now seen as “restrictive” — though not necessarily “sufficiently restrictive” with markets pricing in another 50bps before the year’s end.

Doing less than that would likely require a big negative surprise in wages, employment and services inflation.

Commentary was perceived as more realistic on inflation than past optimism.

The statement and the press conference both sent a strong signal that the monetary policy committee had a preference for rate smoothing, ie maintaining higher rates for longer rather than pushing for higher peaks.

In Europe, the ECB reported that underlying inflation had probably peaked.

Recent easing has been driven by non-energy industrial goods, while a decline in services also appears to have started.

China

Incremental policy announcements continue in the wake of the recent Politburo meeting.

There is still scarce detail, but three announcements caught our eye:

- China’s state planner released a policy document focused on removing government restrictions on consumption and improving infrastructure.

- The People’s Bank of China announced it would “guide” commercial banks to adjust mortgages interest rates lower, step up its monetary support for the economy and help banks control liability costs.

- Local governments are under pressure to use up this year’s quota of special-purchase bonds by the end of September. The question remains whether they will be allowed to pull forward 2024 issuance into this year, which could have a meaningful impact on spending.

Beijing has stopped short of providing major monetary or fiscal stimulus and uncertainty remains whether the measures will be enough.

The challenge was highlighted again last week with data showing continued weakness in manufacturing and property sectors.

- Manufacturing PMI remained below 50 in July, though slightly better at 49.3 versus 49 in June.

- New home sales among the 100 biggest real estate developers fell 33% year-on-year in July, down 33.5% month-on-month

Still, the Politburo has acknowledged the problem and Chinese stocks were the best performers last week.

Australia economics and policy

The RBA held rates at 4.1%, in-line with market expectations but contrary to most economists who had forecast a 25bp hike.

The commentary was on the dovish side, omitting a previous statement that “the path to deliver 2-3% target while the economy still grows is a narrow one”.

However growth expectations moderated.

GDP is now seen at a trough of 0.9% this year, down from 1.2% previously. GDP is expected to be 1.6% in 2024.

CPI is forecast to decline to around 3.25% at the end of 2024, returning to the 2-3% target in late 2025, suggesting interest rates may remain elevated for longer.

Further easing in goods inflation is expected to drive the decline.

Key risks include services inflation, which remains strong amid rising labour costs. Rent inflation has also increased.

Energy prices are forecast to add significantly to inflationary pressures in coming years with electricity prices forecast to add 0.25% to headline inflation in FY24.

The RBA continues to see a “high degree of uncertainty around the speed and extent of the decline in inflation expected in the period ahead”.

Four key domestic uncertainties were detailed:

- The outlook for China remains uncertain

- The outlook for household consumption is subject to competing forces

- Inflation could be more persistent than expected

- Goods prices could decline significantly

Consensus is pricing one more hike, then a steep drop-off in rates in 2024.

Australian Equities

Nearly all sectors ended in the red last week, led by utilities, real estate and financials.

This echoed similar moves in the US. Energy and consumer discretionary were the best sectors.

Energy was comfortably the strongest so far this quarter in Australia and the US on the oil price rebound.

About Jack Gabb and Pendal Focus Australian Share Fund

Jack is an investment analyst with Pendal’s Australian equities team. He has more than 14 years of industry experience across European, Canadian and Australian markets.

Prior to joining Pendal, Jack worked at Bank of America Merrill Lynch where he co-led the firm’s research coverage of Australian mining companies.

Pendal’s Focus Australian Share Fund has an 18-year track record across varying market conditions. It features our highest conviction ideas and drives alpha from stock insight over style or thematic exposures.

The fund is led by Pendal’s head of equities, Crispin Murray. Crispin has more than 27 years of investment experience and leads one of the largest equities teams in Australia.

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

In 2023, Pendal became part of Perpetual Limited (ASX:PPT), bringing together two of Australia’s most respected active asset management brands.

Find out more about Pendal Focus Australian Share Fund

Contact a Pendal key account manager

Full-year reporting season is underway for 2023. Here Pendal investment analyst ELISE MCKAY explains the questions investors should be asking

- Earnings season about more than revenue and margins

- Look for macro impacts, pricing power and AI

- Find out about Pendal Focus Australian Share fund

AUSSIE equities earnings season kicks off this week.

What should investors be looking for in full-year results?

Look beyond revenue and profit margins to how companies are managing the macro-environment, says Pendal investment analyst Elise McKay.

“Have companies maintained the ability to pass through higher prices? What’s happening to wages? Are further cost reduction programs announced?”

“On the revenue side we are looking for the ability of companies to continue to pass through cost inflation, in a slowing economic environment,” McKay says.

“We are also looking for any forward demand indicators – any key performance indicators that will show how the business might perform in future years.

“What will drive revenue? For example, at [milk and infant formula group] A2, what is the birth rate in China doing?

Look at labour

“A key theme over the past 12 months has been availability of labour. We will be looking closely at headcount trends and wage inflation,” McKay says.

“The recent Fair Work Commission decision to lift wages 5.75 per cent highlights the wage inflation issue that we have in the economy.

“We’ve had a number of businesses across the tech sector announce headcount reductions and it will be interesting to see what sectors and companies follow in their footsteps to address their cost bases.

“And then more broadly, how will higher interest rates impact on earnings per share.”

Macro-environment is key

Similar to the June quarterly earnings season on Wall Street, the macro-environment will play an important role, McKay says.

“On Wall Street, up until 28 July, 48 per cent of companies had reported with a better than average result, 55 per cent were ahead of expectations and only 13 per cent missed.

“Yet despite this, the average ‘beat’ has only resulted in the stock going up 28 basis points, versus the average of one per cent.

“So even though companies are delivering better earnings, their share prices aren’t going up on the news.

“The recent market outperformance has been driven by the macro environment, not the earnings. We are still very much in a macro-driven market.”

Keep an eye on AI

McKay says another theme on Wall Street has been artificial intelligence, and she will be watching closely to see how local companies respond.

“You presume locally most companies are thinking about it. It would be a massive red flag if they’re not. You want to understand how companies are thinking about AI as both an opportunity and a threat.”

Find out about

Pendal Horizon Sustainable Australian Share Fund

About Elise McKay and Pendal Australian share funds

Elise is an investment analyst and portfolio manager with Pendal’s Australian equities team. Elise previously worked as an investment analyst for US fund manager Cartica where she covered a variety of emerging market companies.

She has also worked in investment banking and corporate finance at JP Morgan and Ernst & Young.

Pendal Horizon Sustainable Australian Share Fund is a concentrated portfolio aligned with the transition to a more sustainable, future economy.

Pendal Focus Australian Share Fund is a high-conviction equity fund with a 16-year track record of strong performance in a range of market conditions. The Fund is rated at the highest level by Lonsec, Morningstar and Zenith.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Despite higher-than-expected monthly data, the outlook for inflation should be mildly friendly over the next few months, says Pendal’s TIM HEXT

- Why bonds, why now? Pendal’s income and fixed interest experts explain

- Browse Pendal’s fixed interest funds

THE RBA will be encouraged things are moving in the right direction on the inflation front.

The June quarter inflation numbers came in this week at 0.8% for the quarter, or 6% annual.

Underlying inflation (the trimmed mean where they remove the highest and lowest 15%) came in at 0.9%, or 5.9%.

These outcomes were both 0.2% lower than expected.

The RBA is now forecasting 4.5% by year end. Given we are at 2.2% for the first six months of 2023 this seems a little high if anything.

We forecast 4.2% by year end, unchanged from before.

We last saw a 0.8% result in Q3 2021, just before the very large numbers kicked in.

However this may prove to be a low point for the quarterly number this year as utility prices kick in again in Q3 and Q4.

We expect 1.1% in Q3 and 0.9% in Q4 as goods prices moderate but services remain elevated.

The high and lows of these numbers

Let’s start with the items that are accelerating.

Rents are finally kicking in, up 2.5% for the quarter and 7.3% for the year. They are finally catching up with other rental indicators and should remain at 2.5% a quarter for a while yet.

Find out about

Pendal’s Income and Fixed Interest funds

Insurance was up 5.3% for the quarter – no surprise for anyone who has received a payment notice recently.

International travel was up 6.5% in the quarter, again of little surprise.

On the high, but moderating side was new home dwellings.

They rose by 1% in the quarter, though that’s a long way down from the peak. The supply side issues in building seem to be finally working their way through.

On the low side, five of the 11 categories actually saw prices slightly fall.

Most of these were due to government subsidies, highlighting the impact both federal and state governments are having on dampening inflation.

Health, education, electricity and gas were impacted by government subsidies, highlighting the impact governments are having on dampening inflation. Q3 and Q4 will see utilities rebound sharply.

More genuine were falls in motor vehicles, telecommunications and domestic holiday travel as supply constraints ease.

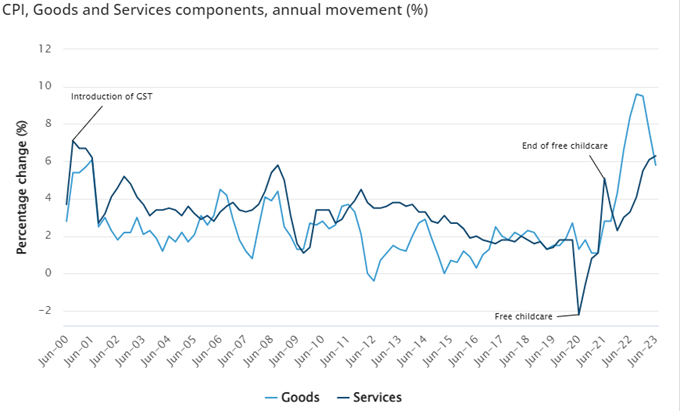

Goods versus Services

Services inflation is finally higher than goods.

The ABS provided us with this graph below, which highlights services inflation above 6% — not seen since GST started in 2000.

Given the strong link to wages this highlights the RBA point that wage growth above 4% with no productivity is not consistent with target inflation.

The RBA

Despite strong employment data this number should continue to provide the RBA headroom to stay on hold.

August will be Dr Lowe’s second last meeting in charge and having moved 4% in a little over 12 months there is room for further patience.

It will be interesting to see if the inflation forecasts are lowered again, although they lowered them in May and hiked anyway so perhaps it doesn’t matter too much.

Three-year swap is now around 4.25%, and the market has one more hike priced in.

I suspect the RBA will keep one more hike up its sleeve and if unemployment has not risen by October they may execute.

This would be Michele Bullock’s first meeting in charge where she may choose to stamp her mark as an inflation-fighting governor.

About Tim Hext and Pendal’s Income & Fixed Interest boutique

Tim Hext is a Pendal portfolio manager and head of government bond strategies in our Income and Fixed Interest team.

Tim has extensive experience in banking, financial markets and funding including senior positions with NSW Treasury Corporation (TCorp), Westpac Treasury, Commonwealth Bank of Australia, Deutsche Bank, Bain & Co and Swiss Bank Corporation.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia.

Find out more about Pendal’s fixed interest strategies here

About Pendal

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

In 2023, Pendal became part of Perpetual Limited (ASX:PPT), bringing together two of Australia’s most respected active asset management brands to create a global leader in multi-boutique asset management with autonomous, world-class investment capabilities and a growing leadership position in ESG.

Economic weakness in China is affecting emerging markets commodity exporters. That means the key to success is looking instead for domestic growth stories, argues Pendal’s JAMES SYME

- China’s weakness affects EM exports

- Focus instead on domestic growth

- Find out about Pendal Global Emerging Markets Opportunities fund

- Watch a recent Emerging Markets overview webinar with James Syme

EMERGING markets investors often focus on commodity-intensive countries – many of which rely on China as one of the world’s top importers.

That may not be an attractive angle right now due to China’s weaker economy.

But it doesn’t mean there isn’t opportunity in the EM space, says Pendal PM James Syme.

Look instead for domestic growth stories that do not depend on exporting to China, argues Syme, who co-manages Pendal Global Emerging Markets Opportunities Fund.

“It’s been very good for the portfolio having the overweight positions in Mexico and Brazil — but we’re cautious on metals, cautious on China, and cautious on Latin American commodity stocks,” says Syme.

Why domestic demand matters in emerging markets

Emerging markets naturally go through business cycles where growth leads to inflation and pressure on the trade balance, which eventually leads to higher interest rates and a downturn, says Syme.

“Then eventually at some point inflation is very low, there’s loads of capacity in the economy, and the economy naturally grows. That’s the cycle that happening now in emerging markets.

“It tends to be boosted by what happens with global financial conditions and the US dollar. One of the big patterns we see at the moment is that after a decade of a strong US dollar, we may now be seeing a weaker dollar.

“That really opens the way for strong domestic growth booms in some of these emerging markets.”

Opportunity in Latin America

Some of the markets best-placed to benefit from this change are found in Latin America, argues Syme.

Brazil and Mexico should see significant interest rate cuts over the second half of 2023 and into 2024, further stimulating what is already quite robust domestic demand, he says.

“We’re very positive on Brazil and Mexico. They’re two of the largest overweights in the portfolio.”

Typically, Latin American GDP growth and equity market returns are highly correlated with commodity prices — especially metals.

Latin America is a large producer of oil, with Brazil, Colombia and Mexico all being major producers. It is also a big exporter of soft commodities which are filling supply gaps created by the Russia-Ukraine conflict.

But it is the metals part of the commodity cycle that tends to correlate with growth most strongly, says Syme.

Find out about

Pendal Global Emerging Markets Opportunities Fund

“We’re very positive on the outlook for the domestic economies of Brazil and Mexico, but this is not because we’ve got a particularly positive view on metals.

“Although there are some significant supply constraints, particularly around copper, the world’s largest demand source for industrial metals continues to be China, the Chinese economy looks very weak and within the Chinese economy, it’s the most commodity intensive sectors that look the weakest.

“So, we have no copper, we have no Latin American gold miners, we have no Latin American iron ore miners. Generally, our exposure to the commodity complex in Latin America is very low.”

Instead, emerging markets portfolios need to be positioned to capture the beneficiaries of domestic growth, says Syme.

Leading opportunities include banks and financial stocks, alcohol producers and brewers, domestic airlines, fast food and building materials like cement, he says.

About Pendal Global Emerging Markets Opportunities Fund

James Syme, Paul Wimborne and Ada Chan are co-managers of Pendal’s Global Emerging Markets Opportunities Fund.

The fund aims to add value through a combination of country allocation and individual stock selection.

The country allocation process is based on analysis of a country’s economic growth, monetary policy, market liquidity, currency, governance/politics and equity market valuation.

The stock selection process focuses on buying quality growth stocks at attractive valuations.

Find out more about Pendal Global Emerging Markets Opportunities Fund here

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

A new signal from China caused excitement among investors this week. AMY XIE PATRICK explains what it means

- Take caution with China’s latest property signal

- Why bonds, why now? Pendal’s income and fixed interest experts explain

- Browse Pendal’s fixed interest funds

THE latest message from China’s top decision-making body caused a stir this week when investors noted softer language on property.

For the first time since 2016, President Xi Jinping’s signature slogan that “houses are for living, not for speculation” was missing from a note that followed the Politburo’s July meeting.

That caused excitement in the market about the potential for a meaningful stimulus push via the property sector.

China’s property industry accounts for up to 20 per cent of GDP once related sectors are added.

But the market is getting ahead of itself.

The line has likely been dropped because it’s simply no longer needed.

Buyers are no longer speculating. They are actively selling in an attempt to exit the property game altogether.

In fact, one of our investment themes here in Pendal’s Income and Fixed Interest team, is that there will be no silver bullet from China to turn around its economy.

Deleveraging leads to fire sales

Beijing’s attempts to de-leverage property developers effectively shut them out from official channels of funding in 2020.

The unofficial channel relied on off-the-plan pre-payments from buyers – but relying on this channel alone is a bit like a Ponzi scheme.

Developers need to keep selling properties they promise to build in the future, to secure the funds to finish what they’ve already pre-sold.

As defaults among Chinese property developers started to snowball last year, buyers soon came to the realisation that they may never get delivery of properties they’d made down payments on.

To cut their losses, owners of partially completed apartments started to list them at discounts on the secondary market.

Indicators suggest property prices are now falling as fast as they did during the initial outbreak of the pandemic, with no relief in sight.

Breaking bad

It is impossible to understate the extent of this shock to the Chinese psyche.

The economic model has had property at its core for the best part of a generation.

Every crisis has been met with property sector stimulus. This spurred consumer spending on all things related to buying a new home.

It gave local governments revenue from selling plots of land.

It spurred borrowing from Chinese households to get on the property ladder because as far as they knew, Chinese house prices only ever went up.

Confidence in the property sector has now been shaken to the core.

It forces Chinese households to recognise the real state of their balance sheets. At the margin, income will be directed towards balance sheet repair rather than new consumption.

I have some sympathy with commentary that draws parallels between Japan’s bubble bursting in the late ’80s.

In the long run, this is a good story for China.

It allows the economy to break away from its addiction to building endless apartments and move on to find healthier alternatives. What those alternatives might be is yet to be determined.

Economic debris

The bad news right now is that the debris from the current property carnage is clogging up China’s economic engine.

Policy response has so far been limited.

Find out about

Pendal’s Income and Fixed Interest funds

Interest rates and reserve ratios have been cut. But what use is making the price of borrowing cheaper in a system where there is no appetite to borrow because of shattered confidence?

Clearing this debris requires either allowing developers to borrow again or someone to absorb losses.

The former is unlikely given the pain endured to come this far down the deleveraging path. The latter is unpalatable given the sheer extent of losses that potentially exist.

As an example, Chinese property developer Evergrande recently wrote down US$52 billion of losses on the value of its assets – and faces a $44bn funding gap for completing its construction pipeline.

If that funding gap can’t be bridged, further write-downs will follow.

The extent of unrealised losses sitting within this sector may simply be too big for the private sector to bear.

But the state also faces a moral hazard dilemma if it tries to share the burden.

Against this backdrop, it is easier to understand why stimulus efforts have been so lacklustre to date.

What it means for markets and investors

Chinese asset prices have largely priced in a soggy growth story from here.

The rest of the world has had the luxury of ignoring China’s woes because strong consumption supported by excess savings has more than offset China’s drag.

What happens when those savings run out has most certainly not been priced into global asset prices.

The Politburo meeting also highlights a renewed focus on currency.

Beijing dislikes extreme moves over a short period of time. But in the absence of a property-driven growth engine, Beijing probably doesn’t mind a weaker currency.

Since domestic demand is hard to lift, a weaker yuan should at least help to channel some international demand in China’s direction.

Here are some broad-brush implications for positioning:

- Lean against yuan strength. Volatility can be smoothed but the trend can’t be stopped. A cheaper currency would help Chinese growth at the margin by lifting exports.

- Avoid betting on lower Chinese yields. Slashing interest rates won’t work to stimulate the economy when no one wants to borrow. Near term, the Chinese rates market may have priced peak pessimism.

- Maintain a long duration bias in global duration. When excess savings run out, China’s drag will become more evident on global growth.

About Amy Xie Patrick and Pendal’s Income and Fixed Interest team

Amy is Pendal’s Head of Income Strategies. She has extensive expertise and experience in emerging markets, global high yield and investment grade credit and holds an honours degree in economics from Cambridge University.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia. The team oversees some $20 billion invested across income, composite, pure alpha, global and Australian government strategies.

Find out more about Pendal’s fixed interest strategies here

About Pendal Group

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

Here are the main factors driving the ASX this week according to our head of equities CRISPIN MURRAY. Reported by portfolio specialist Chris Adams

EQUITY and bond markets trod water last week after well-received inflation data – and ahead of more US quarterly earnings reports, plus meetings at the Fed, European Central Bank and Bank of Japan this week.

The S&P 600 gained 0.7% while the S&P/ASX 300 was up 0.13%.

In US equities we saw a rotation from tech to banks.

There was some wariness of tech stocks ahead of results, given their big recent runs. Bank results are so far better than many feared. This rotation provided breadth to the market.

Positive surprises on inflation and economic resilience – combined with the AI thematic – have driven markets in 2023.

We now appear to be entering a phase of consolidation, rather than a major correction.

The improvement in market breadth is a constructive signal, as is an economy with little tangible sign of deterioration.

In Australia, strong employment data is a reminder of domestic economic resilience. It is hard to see how inflation falls sufficiently in this environment – but the market is waiting for this week’s inflation data before worrying too much about rates again.

Key market issues

At the start of the year we outlined six issues we thought most important for markets going into 2023.

It’s worth revisiting now to see how they’ve transpired.

In short, the key issues have evolved, but there haven’t been any definitive developments.

It’s worth noting the miracle of a soft-landing is now a real possibility – something no-one really believed six months ago.

Since then we’ve also added two new issues to keep tabs on:

- Artificial Intelligence: To what extent is AI a material driver of long-term earnings and will it continue to fuel a re-rating of tech?

- The US-dollar index (DXY): It’s off 2.4% since the start of 2023, which has supported markets and commodities. But is this the beginning of a more material move or a period of consolidation?

Here’s a look-back at the original six issues:

1. The persistence of inflation – which will determine how tight financial conditions should be

Inflation has proven more persistent than expected for much of 2023, though in recent weeks it’s started to surprise on the downside.

Importantly, this recent change has begun without the economy showing material signs of weakness.

Despite the rise in two-year bond yields – US government bonds are up 42bps in 2023 and Australian yields up 61bps – 10-year bond yields have remained flat (down 4bps in the US and Australia so far this year).

Lower commodity and input prices along with improved supply chains have eased inflationary pressures.

The key area of contention remains services inflation, which is tied to wage growth and productivity.

Wages are trending lower.

Forward indicators such as the Indeed Wage Tracker are slowing materially, down from about 9% annual growth in late 2021 to 4.8% by June.

The Atlanta Fed wage tracker has seen the gap between overall wage growth and wage growth for job switchers narrow materially, as the latter has decelerated faster.

This suggests the worker shortage is dissipating.

The remaining concern is the continued strength of the labour market, which may make the Fed question whether wages will fall back as far as they need to.

Weak productivity is another reason to be wary of how quickly services inflation falls back.

The upshot is that there is still more to do.

Wages need to reduce to 3% or below to be consistent with 2% inflation. The latter is heading in the right direction and offering hope.

2. The scale of the economic slowdown in the US and other developed markets

The economy has clearly held up better than most expected.

The market was pricing a 65% chance of recession at the start of the year. We remain at the same level some seven months later.

Higher rates have not wreaked havoc as many feared. The debate has shifted to how long the potential lags in effect may be.

Bulls point to “total financial conditions” – a measure of changes in key indicators such as mortgage rates, credit spreads, equity markets and currency moves – having already tightened to a peak. Lead sectors such as housing are turning the corner and an inventory de-stocking phase is now slowing.

Combined with the better inflation data, confidence is building of a soft landing.

Bears continue to point to yield curves and other lead indicators as signs the economy will roll over.

The Fed has now released its own “total financial conditions” index (alongside others from the likes of Goldman Sachs, Bloomberg and regional Federal reserves).

The Fed’s index – which measures the expected impact on growth – shows total conditions as more restrictive than indicated by other indices, suggesting we may see a weaker economy by the year’s end.

That said, even the Fed’s measure of total financial condition tightening has peaked – and the expected impact on growth is waning.

The March banking crisis was seen as evidence of how tightening can affect the economy in unpredictable ways.

But it’s increasingly looking like the “all-in” policy response from the Fed and US Treasury has successfully stemmed second-order consequences.

The question remains: will we defy the “laws of economics” this cycle and avoid a recession?

The accumulated stimulus from the pandmic – combined with green investment, re-shoring and a deflationary China – may help pull off a soft-landing miracle. But there is still no clarity emerging.

3. The leverage of earnings to that downturn

With no sign of recession, there is no insight on the degree of operating leverage.

Earnings have proven more resilient than many expected, particularly in tech.

4. Whether markets have already priced in the downturn

In hindsight a lot of bad news was priced in at the start of the year.

Markets have done much better than expected, squeezing higher on cautious positioning and resilient outlooks for the economy and earnings.

The S&P 500 is up 19.24%, the NASDAQ 34.69% and the S&P/ASX 300 a more subdued 6.03%.

The bulk of this move is valuation re-rating. The S&P 500 has gone from 16.8x P/E to 19.6x.

This suggests less pessimism – but also less buffer in the case of an economic downturn.

5. How China’s economy performs as it exits Covid-zero

China has been a material disappointment.

Q1 saw a strong re-opening bounce, but it faded far more quickly than expected.

Housing has been weak. At best, it can be expected to stabilise.

Exports have suffered on slowing global growth – particularly in goods – although there are some signs of stabilisation.

Consumers remain cautious and this is more likely to be structural factors at play.

Q2 weakness was exacerbated by inventory de-stocking, so there should be some improvement in Q3 even without stimulus.

July’s Politburo meeting is usually focused on the economy. But the mail we are getting is not to expect too much.

The growth rate, while slower than expected, is still consistent with Beijing’s target. It is also unclear how effective stimulus would be.

So any measures are more likely to be specific industry-orientated actions, rather than a “big bang” type of stimulus.

6. Can the RBA engineer a soft landing in Australia?

Australia’s relative appeal has deteriorated.

When it looked like the rest of the world was facing a recession, our immigration-driven resilience was a relative positive.

Now with the rest of the world seemingly more likely to pull off the soft landing, the Australian economy is seeing more stubborn inflation due to higher population growth, combined with rising wage growth and weak productivity.

At the same time the much-anticipated mortgage cliff has not yet had a meaningful impact.

The latest employment data reinforced the strength in the economy.

The politicisation of the rate-setting process and an RBA flip-flopping between inflation hawkishness and social concerns also runs the risk of undermining confidence in policy making and de-anchoring inflation expectations.

So the risks here have risen.

Central bank policy

The Fed, ECB and BOJ meet this week. To summarise:

- The Fed is widely expected to hike for the last time, with rates up 25bp to a 5.25% to 5.5% range. They will probably look to maintain the expectation of one more hike, but may signal that it won’t be in September. The reason for this is they will not want the market bringing forward the first rate cut which is now priced for March 2024.

- The ECB is also expected to hike, but again, this could be the last. The Dutch central bank noted there was no certainty of hikes beyond July. Awareness of the monetary lag could also lead to a less hawkish message.

- The key issue for the Bank of Japan is whether to move the targeted cap on government bond yields from 50bp to 75bp. If they do, we could see a continued rise in yields and a stronger yen. If nothing changes we may see a re-test of the calendar year to date highs.

Markets

US earnings season kicked off with a focus on banks – where results were not as bad as feared.

One of the key issues was margins, which did deteriorate but not as much as expected. Big banks retain strong liquidity and haven’t chased deposits, which seems to have helped.

The other concern was around exposure to commercial real estate, particularly office.

The positive news here was that reserves against this exposure had stepped up from 3-4% to 8-9% – but without a hit to capital, providing more of a buffer.

Heading into the main phase of earnings, revisions have been at the weaker end of the historic range. Clearly if this persists it will add to the argument for market consolidation, or even a pull-back, given the recent run.

It is also worth noting how low stock correlations have been in 2023.

They are now probably as low as they go, which would indicate macro factors may begin to re-emerge.

About Crispin Murray and Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia. Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions.

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

The unemployment rate remains low. Pendal assistant PM ANNA HONG explains what that means for rates and bonds

- Why bonds, why now? Find out more from Pendal’s income and fixed interest team

TODAY’S jobs data shows the headline unemployment rate stuck around 3.5% and the participation rate falling by only 0.1%.

The good news is, we’ve got jobs.

But does it mean more rate hikes are on the cards?

Yes and no.

The unemployment rate is a slow-moving indicator, reflecting what has already happened rather than what will happen.

People tighten their belts, which results in a slowdown in economic activity way before we lose our jobs.

This can be observed through spending habits, retail sales and the inflation trend which clearly shows disinflation flowing through in the Australia CPI number.

Australia’s CPI peaked at 7.8% in December 2022 and continued to slow down to 5.6% in May.

That’s despite our unemployment rate tracking sideways at 3.5% since reaching a low of 3.4% in October 2022.

Furthermore, high net migration has already materially reduced the number job openings in Australia.

Job advertisements in NSW, VIC and ACT have weakened, especially in the segments such as hospitality, tourism and retail which are most sensitive to the inflow of foreign workers.

What does this mean for bond investors?

It’s not yet time to raise the “mission accomplished” flag, but we are closer to the end of the rate hiking cycle.

There may be one or two more rate hikes, though much of the market pricing already reflects than.

Find out about

Pendal’s Income and Fixed Interest funds

This is especially evident in Australian three-year and ten-year government bonds price moves after the release of the unemployment data – it moved in about a 0.06% range.

Is there a risk of over-hiking by the central banks? Yes.

In that scenario, something will break and we favour duration protection at around 4% yield to deliver capital gains for the portfolio.

What if we get a soft-landing?

That means that the RBA can chart a path back down towards neutral, which should give long bonds a nice capital kick.

About Anna Hong and Pendal’s Income and Fixed Interest team

Anna Hong is an assistant portfolio manager with Pendal’s Income and Fixed Interest team.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia.

With the goal of building the most defensive line of funds in Australia, the team oversees some $20 billion invested across income, composite, pure alpha, global and Australian government strategies.

Find out more about Pendal’s fixed interest strategies here

About Pendal Group

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Here are the main factors driving the ASX this week according to portfolio manager JIM TAYLOR. Reported by portfolio specialist Chris Adams

MARKETS strengthened last week ahead of the US June CPI report and surged again when the cooler inflation data met with approval.

There was some consolidation on Friday as second-quarter US company results started to come through, though things were okay on that front.

The CPI print, bolstered by a supportive and instructive Producer Price Index (PPI) print, means the market now has peak Fed rates firmly in its sights.

Investors are pricing in one more 25bp rise in July. Some are even saying that would be one hike too many.

The notion of a soft landing in the US gained further traction with a good labour market print and stronger consumer sentiment.

As a result, there was a notable improvement in the breadth of the equity market rally, though mega-cap tech performed strongly as well.

Commodities rose, notwithstanding some poor economic data out of China. The DXY — a trade-weighted index of US dollar strength — headed to 12-month lows.

The S&P 500 rose 2.44% and the S&P/ASX 300 was up 3.73%.

Central bank watch

Fed commentary last week was mostly hawkish, persisting with the line that there is more to be done.

Mary Daly of the San Francisco Fed noted that “we are likely to need a couple more rate hikes this year”.

Fellow non-voting FOMC member Loretta Mester, of the Cleveland Fed, agreed there was “more tightening needed”.

The market, though, was not buying this line. Scepticism may have been bolstered by the resignation of St Louis Fed president James Bullard.

Bullard had been among the most hawkish members of the FOMC, pushing for stronger moves to fight inflation over the past two years. He leaves to take up an academic post.

There was a slightly softer line from Atlanta Fed president Raphael Bostic (another non-voting member), who said policy makers “can be patient” given that we are “in restrictive territory”.

Michael Barr (who is on the Fed board of governors and was the only voting member to speak), noted the Fed had made progress and was “close” to a sufficiently restrictive level — but “still have a bit of work to do”.

Elsewhere the Reserve Bank of New Zealand left the official cash rate unchanged at 5.5%, as expected.

This was its first pause since it started lifting rates in October 2021.

US macro

June’s CPI came in 0.2% higher than May — below the +0.3% consensus expectation.

On an annualised basis it was 3% — also below the consensus of 3.1% and the lowest rate since March 2021.

Core CPI (which excludes food and energy), was up 0.2%. This was down from 0.4% in May and below the expected 0.3%.

Annualised Core CPI is running at 4.8%, versus 5% expected. It is at its lowest since October 2021.

Importantly, the shelter component has now fallen from a peak of 9.5% down to 5.5%. Based on effective rents, this will continue to fall for the rest of the year.

Used car prices fell 4.2% — the biggest monthly drop since the pandemic’s early days. This component accounts for about 4% of the CPI basket.

This well-received reading was supported by the PPI which rose 0.1% in June on a headline and core basis. This was below consensus expectations of 0.2% and the third straight month of a 0.1% gain.

Find out about

Pendal Horizon Sustainable Australian Share Fund

Core PPI is running at 2.4% versus 2.6% in May. But the annualised three-month rate is 1.0% — its slowest rate since early 2020.

It is expected to be at 1.5% in August and may turn negative given leading indicators of downward pressure on prices.

All this was seen as a signal of further weaking pressure on the CPI.

As inflation falls, there was some resilient economic data prints, which fed the narrative of a soft landing.

- Consumer sentiment measured by the University of Michigan’s index rose from 64.4 in June to 72.6 in July — well above the consensus of 65.5. That said, it’s worth noting that 5-to-10-year inflation expectations remain elevated versus pre-pandemic levels.

- Initial jobless claims fell to 237K from 248K, well below the 250K consensus

Australian macro

The Westpac-Melbourne Institute consumer sentiment index improved by 2.7% in July, up from a 0.2% in June.

However it remains in “deeply pessimistic” territory.

Underlying sub-indices were mixed.

Perception of family finances have fallen to new cycle lows, but perceptions around the broader economy and the housing market have seen something of a rebound.

China macro

Beijing is grappling with a deflationary problem, which bodes poorly for growth.

Its CPI was flat at 0% year-on-year for June — the lowest print since February 2021.

The PPI is deflationary, running at -5.4% year-on-year versus -4.6% in May.

This suggests already-weak domestic demand continues to soften. Services consumption is recovering, albeit slowly, while housing demand remains subdued.

There were some signs of life in credit.

Aggregate financing — a broad measure of total credit — was CNY 4.2 trillion higher in June, versus CNY 3.1 trillion expected.

There were CNY 3.02 trillion in new loans. This should eventually feed through to increased new activity.

Deputy Governor Liu Guoqiang of the People’s Bank of China (PBOC) sought to calm concerns over the economy.

The bank retained “ample policy room to deal with unexpected challenges and changes”, he said. There was a need “to be patient and confident in the economy’s continued and steady growth”.

Find out about

Pendal Focus

Australian Share Fund

Crispin Murray,

Head of Equities

There are also signs Beijing is easing pressure on China’s tech sector. The PBOC noted that most of the issues at Ant Group and Tencent had been dealt with.

Earnings expectations

As we move into US quarterly reporting season, the market is expecting a 7.1% year-on-year decline in earnings for the second quarter of 2023.

This is slightly worse than the -7% expected on June 30.

If this transpires, it would be the biggest quarterly earnings decline since Q2 2020, when earnings fell 31.6%.

It would also be the third straight quarter of declining earnings.

So far 6% of S&P 500 companies have reported, with 80% delivering a positive EPS surprise and 63% a positive revenue surprise.

JP Morgan, Citigroup, Wells Fargo and Delta Airlines kicked off the season with decent results.

Leading into the Australian reporting season in August, the market is expecting 0.7% aggregate EPS growth for FY23. This is down from more than 10% a year ago.

Banks are expected to deliver 15.1% EPS growth on the back of higher margins, though this is expected to fall 5.3% in FY24 as those tailwinds recede.

Resources are the drag, with expected EPS down 17.4% in FY23.

Industrials (excluding resources, banks and listed property trusts) are expected to see 19.5% EPS growth for FY23.

Markets

A perceived end to the US hiking cycle saw technology-related stocks go on a tear last week.

The S&P 500 is now 3% higher than when the Fed started hiking rates in March 2022.

In Australia the IT sector rose 6.25%, led by Square (SQ2, +15.54%).

Materials (+5.76%) were also strong despite ongoing Chinese economic weakness. Part of this was strength in the gold miners on a weaker US dollar.

Evolution Mining (EVN, +17.08%) was the best performer in the ASX 100. Generally stronger commodity prices also buoyed Alumina (AWC, +9.33%) and South32 (S32, +7.63%).

About Jim Taylor and Pendal Focus Australian Share Fund

Drawing on more than 25 years of experience investing in top-performing Australian companies and a background in accounting, Jim manages our Long/Short Fund and co-manages our Imputation Fund. He is a Chartered Accountant with membership of the Australian Institute of Chartered Accountants.

Pendal Focus Australian Share Fund is managed by Crispin Murray. The fund has beaten its benchmark in 14 years of its 18-year history (after fees), across a range of market conditions. Find out more about Pendal Focus Australian Share Fund here.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Among emerging markets, Brazil is providing investors with opportunities, argues Pendal senior fund manager JAMES SYME

- Brazil took its medicine and is now reaping rewards

- Growing investor opportunities in emerging markets

- Find out about Pendal Global Emerging Markets Opportunities fund

- Watch a short Emerging Markets overview webinar with James Syme

BRAZIL’S central bank, Banco Central do Brasil, was one of the first global monetary authorities to start lifting interest rates.

It was tough medicine but now the top-ten economy is reaping rewards earlier than its peers,” argues James Syme, co-manager of Pendal Global Emerging Markets Opportunities fund.

Syme and his London-based team EM take a top-down, country-level approach to the asset class.

“Brazil’s central bank has run orthodox monetary policy for three or four years, more so than most other central banks,” Syme says.

“When they started hiking rates in the first quarter of 2021, Covid was still a huge problem in Brazil. But inflation expectations pushed above target, and they ultimately pushed rates to 13.75 per cent.”

The early shift is now paying dividends.

“Brazil took the medicine and on the back of that it got anchored inflationary expectations and a strong currency,” Symes says.

“First-quarter 2023 GDP came in at 4 per cent, and consensus was 3.1 per cent. The May inflation number was expected to come in above 4 per cent but came in below 4 per cent.

“There has been very significant disinflation in the economy and inflation is now around the central bank’s target range.”

Banco Central do Brasil will cut rates at some point in the next year, Syme says, though they will do it cautiously.

He expects rate cuts, ultimately, will exceed 300 basis points.

“When these rate cuts come through, they will happen in an economy that’s already, on the domestic front, growing quite strongly,” he explains.

“Across the domestic economy there are strong positive numbers and beats relative to consensus, despite there being no rate cuts yet. And that’s a really exciting environment.”

Stable currency

A reason why Brazil will keep growing, according to Syme, is the stable currency, the Brazilian real.

It was sold off during Covid, losing nearly 50 per cent of its value against the US dollar. More recently it has appreciated against the greenback.

“That strength in currency reduces the cost of imported goods, which are a meaningful part of the inflation basket,” Syme says.

“So in economies like Brazil, a strong currency reduces inflation which enables more rate cuts..

“In emerging markets, typically everything goes wrong, or everything goes right.

“If things go right, you typically get capital inflows, a stronger currency, a better inflation outlook, the prospect for yields to fall, equities going up along with economic growth, and that eases any political stresses.

“And we think that is where Brazil is now.”

EM stand-outs

Brazil is the stand-out example of a number of emerging economies that pre-Covid struggled economically but are now providing investors’ with opportunity, Syme argues.

“We are seeing broadly similar patterns in India, Indonesia and Mexico.

Find out about

Pendal Global Emerging Markets Opportunities Fund

“Long, deep downswings tend to be followed by long upswings and that’s broadly what we expect will happen with these economies.

“Brazil really has been the surprise. We thought rate cuts would be needed to really get the economy going.

“But it seems that through what higher commodities and prices are doing to the economy and through the natural tendency for the domestic economy to recover, Brazil is doing well already with the potential for more good news when the cuts come through.”

About Pendal Global Emerging Markets Opportunities Fund

James Syme, Paul Wimborne and Ada Chan are co-managers of Pendal’s Global Emerging Markets Opportunities Fund.

The fund aims to add value through a combination of country allocation and individual stock selection.

The country allocation process is based on analysis of a country’s economic growth, monetary policy, market liquidity, currency, governance/politics and equity market valuation.

The stock selection process focuses on buying quality growth stocks at attractive valuations.

Find out more about Pendal Global Emerging Markets Opportunities Fund here

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

Here are the main factors driving the ASX this week according to our head of equities CRISPIN MURRAY. Reported by portfolio specialist Chris Adams

EQUITIES continue to rally even as bond yields rise on the back of the Fed’s “hawkish pause” which held rates steady but added in a second rate rise by the year’s end to the “dot plot”.

The market is not convinced of the need for that hike, with CPI data indicating inflation is coming down.

There has been some good news recently.

While it has been a relatively narrow cohort driving the market’s momentum, we have seen some broadening in recent weeks. For example, the Russell 3000 index of US small caps is up 5.8% in June.

The S&P 500 gained 2.6% last week and has broken through the 4350 resistance level, with technical investors suggesting it could now retest the highs of January 2022 at about 4800.

The economy also looks to be holding up, with industrial companies like Honeywell signalling things are not as dire as some would suggest.

All that said, complacency is high.

Markets can enter the doldrums in the Northern Hemisphere summer. The liquidity environment may turn negative as the US Treasury rapidly refill their coffers, having run them down during the debt ceiling stand-off.

This could prompt a decent retracement in equities.

The S&P/ASX 300 gained 1.8% for the week, helped by a 3.06% gain in the resource sector as people hope that Beijing will blink and pull the traditional property and infrastructure stimulus lever in response to a disappointing economic recovery.

US inflation

While there are myriad ways to measure inflation, the overall trend is one of incremental improvement on signs that underlying inflation is falling.

The headline US Consumer Price Index (CPI) rose 0.1% in May and is running at 4.0% annualised. This was broadly in line with expectations.

The impact of food and energy has swung about from driving about 4% of inflation in mid-2022, to now having zero impact in aggregate.

The breadth of inflation across different categories is also moving in the right direction. The number of categories growing at greater than 5% has fallen from almost 75% in mid-2022 to roughly 40% now.

Core CPI rose 0.4% month-on-month and on a three month-moving-average basis remains stuck in the low 0.4% range.

This is still higher than the Fed wants to see.

However the market is taking a sanguine view, expressing confidence that inflation will head lower in coming months, driven by:

1. Used car prices falling back. These added 15bp in May, but auction prices are falling. Auto assembly is also ramping up, which means more new car inventory, more competition and reduced margins, helping inflation.

2. Rents are set to drop. Owner Equivalent Rent is stuck at 0.5% month-on-month on the lagged effect of previous rent rises. But this has largely played out now, according to Cleveland Fed. Owner equivalent rent should fall materially based on leading indicators.

In combination, there is a view that these trends can shift annual core CPI from 5.3% to 4.2% by the end of 2023.

As an indication, inflation ex-rents and used vehicles is running at a three month annualised rate of 2.8%.

Personal Consumption Expenditure (PCE), which the Fed place emphasis on, could fall from 4.7% to 3.7%. It is declining more slowly due to the effect of higher health care and financial services representation in the basket.

Finally, the University of Michigan survey of inflation expectations showed that the median expectation of inflation in one year had dropped by 0.9% — more than was expected — to 3.35%.

The ten-year median fell by 0.1% to 3%, which was in line with expectations.

Fed meeting

The Fed’s meeting was described as a hawkish pause.

Chair Powell kept rates unchanged, as previously flagged, but simultaneously sent a more cautious message via the commentary and dot plots.

The FOMC is now signalling two more hikes this year, versus only one back in March.

In his commentary, Powell suggested he is considering moving to hikes in alternate meetings. This is relevant because it would mean a hike in July – as the market expects – but then a second in November.

This is a long time away and a lot could change by then. So while the market moved, two year yields only rose by 12bps.

The Fed’s statements and actions appear to be at odds. Why pause when you are also raising the amount of hikes you believe are required to bring inflation into range?

The logic could be:

1. Having pre-committed to a pause, they didn’t want to do an about-face

2. With inflation falling, the Fed may see risk-reward as more balanced between inflation and recession, so can be more patient

3. The Committee may be more hawkish than Powell and this statement was the quid pro quo for a pause

4. The Fed is concerned the market would react too positively to the pause, leading to looser financial conditions

US bonds have rallied from March, fuelled in part by concern over the economic impact of the banking crisis. However the economy has held up better than feared and, while inflation is falling, it remains sticky at around 3.5-4.0%.

So the current yield curve suggests the market is no longer looking for rapid easing in 2H 2023.

The reason the Fed remain wary is that while the momentum of the economy is slowing, the absolute level of activity remains high.

This is reflected in a tight labour market and stubbornly high wage pressure, manifesting in unit labour costs and wage expectations.

The Fed’s six-monthly monetary policy report (MPR) was released to Congress.

It noted the labour market remains “very tight”, despite some signs of easing, versus the “extremely tight” of the previous report.

They therefore believe that core services inflation “remains elevated and has not shown signs of easing”.

It does indicate that they still expect some impact from credit tightening post the bank failures. It also included the imputed level of rates based on the Taylor Rule, which would be 6%.

Rest of the world

The European Central Bank raised rates 25bp to 3.5% and signalled another hike in July, blaming resilience in employment and inflation signals surprising to the upside.

The market is pricing in an 80% chance of a further hike in September.

There is a lot of chatter around potential stimulus in China, which did see a small rate cut in its seven-day reverse repo rate last week, signalling the direction of policy.

Issues such as youth unemployment rising to 20% are seen as driving the requirement for Beijing to act, with commodity plays strengthening in response.

Australia

Good employment data validated the message from the RBA that more rate hikes are needed.

Australia is in a different place to the US, reflecting accelerating wage increases, poor productivity, rising house prices and strong immigration underpinning the economy.

The domestic bond market woke up to this last week with some big moves in yields.

- Two year bond yields rose 19bps to a new cycle high of 4.2%. This is the highest level since 2011 and we have now seen yields move 136bp higher since the lows of the US bank crisis. This has had no impact on equities.

- Five year yields also broke out to new cycle highs of 3.95%. This is also the highest since 2011.

- Ten-year yields are holding in better at 4.03% — not yet back to the 4.2% seen in October.

The net result is that the ten year versus two-year yield curve has inverted for the first time since 2008.

This is a negative signal for the economy, although we note that the curve first inverted in mid-2006 and equities continued to rally through to late 2007.

So this is not necessarily a flag for near-term falls in equities.

Markets

The S&P/ASX 300 continues to rally and is up 4.89% CYTD, versus 15.78% for the S&P 500 and 31.35% for the NASDAQ.

Miners led the market last week on hopes of China stimulus, with Resources up 3.06%. They are now outperforming the S&P/ASX 300 over CYTD, up 7.19% despite the price of iron ore being flat and lithium falling about 30%.

Information Technology continues to run, up 4.26% for the week, following the US lead.

Healthcare (-5.69%) was a laggard, largely down to a downgrade from CSL.

About Crispin Murray and Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia. Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions.

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.