Here are the main factors driving the ASX this week according to portfolio manager Jim Taylor. Reported by portfolio specialist Chris Adams

WE were running with a dual-track market last week.

Initially, a procession of Fed officials made some ground in convincing the market that the chances of significant rate cuts in the back end of 2023 was a pretty unlikely scenario.

At the same time there seemed to be some bipartisan movement with regard to agreement on lifting the debt ceiling.

Then on Friday Fed Chair Powell raised the possibility of a June pause in rate hikes — and the Republican negotiators walked from discussions over the debt ceiling.

Overall last week, bonds were down, equities gained and commodities held up.

US ten-year government bond yields rose 21bps to 3.68%. The S&P 500 was up 1.71% and the S&P/ASX 300 rose 0.47%.

US reporting season has produced a much better outcome than anticipated seven weeks ago while Australia also saw a couple of good results to round out the mini reporting season.

US Fed speak

There were mixed messages from Fed members over the course of last week.

- Neel Kashkari (President of the Minneapolis Federal Reserve and known hawk) warned that the Fed would probably tighten more, even as colleagues signalled that a June pause is preferable, noting that “we need to finish the job”.

- Austan Goolsbee (President of the Chicago Federal Reserve and the most dovish of the Fed voting members) emphasised the importance of being “extra mindful” of the impact of rate hikes on credit conditions.

- Lorie Logan (President of the Dallas Federal Reserve) noted “we have made some progress” and “the data in coming weeks could yet show that it is appropriate to skip a meeting. As of today, though, we aren’t there yet.”

- Philip Jefferson (Federal Reserve Governor and nominee for vice chair) said that “on the one hand, inflation is too high, and we have not yet made sufficient progress in reducing it,” but also that “history shows that monetary policy works with long and variable lags, and that a year is not a long enough period for demand to feel the full effect of higher interest rates.”

On Friday Fed Chair Jay Powell had the final word.

He took a dovish tone, flagging that rates may not need to rise as much as previously thought, given the potential effect from a slowdown in bank lending.

Midcaps on

the move

Hear from lithium industry pioneer

Ken Brinsden and Pendal’s

Brenton Saunders

On-demand webinar

“Developments there, on the other hand, are contributing to tighter credit conditions and are likely to weigh on economic growth, hiring and inflation,” he said.

“Until very recently, it has been clear that further policy firming would be required. As policy has become more restrictive, the risks of doing too much versus doing too little are becoming more balanced” and “given how far we have come, we can look at the data and evolving outlook and make careful assessments.”

Australia macro

May’s RBA Board meeting minutes showed that they considered hiking by 25bp or leaving rates on hold.

The decision to hike, though ‘finely balanced,’ was based on data confirming that the labour market remained tight and a hike was needed to guard against upside risks to the outlook for inflation.

Looking forward, members “agreed that further increases in interest rates may still be required, but that this would depend on how the economy and inflation evolve”.

Labour and wages data

The surprising strength in February and March’s employment data reversed in April.

The unemployment rate rose from 3.5% to 3.7% and 4,300 jobs were lost, rather than an additional 25,000 created as per consensus expectations.

The three and six month moving averages for employment growth are slowing, painting a picture of a still tight labour market, but giving some degree of comfort around the trend.

Hourly wage rates (ex-bonuses) in Australia rose 0.84% quarter-on-quarter and 3.66% year-on-year in Q1 of 2023.

This is broadly in line with expectations and represents the strongest growth in Public and Private wages for about a decade.

Find out about

Pendal Horizon Sustainable Australian Share Fund

The RBA’s forecast in the May Statement on Monetary Policy was 3.6% year-on-year.

A lack of productivity gains means that unit labour costs are well above the RBA’s 2-3% inflation target.

Wage increases including bonuses and commissions rose a stronger 3.9% year-on-year, and 4.1% year-on-year for the private sector.

There is a strong chance we start to see public sector wage pressures begin to build from here.

US macro and policy

Signs continue to be mixed in the US economy.

On the downside, the Citigroup Economic Surprise Index — which looks at the difference between economic forecasts and actual result — turned negative after a positive start to the year.

The EVRISI Trucking Survey — which has the highest correlation to real GDP of any single sector survey — is currently in recession territory.

That said, the May NAHB index of homebuilders’ activity and sentiment rose to 50 from 45, above the consensus expectation of 45.

The absolute level is still very depressed, but this index has now risen for 5 straight months. Homebuyers are being pushed into buying new homes, given the dearth of existing homes to purchase.

The share of new homes in the total home sales data has moved from 10% to 13%, hence the homebuilders are doing better than the mortgage demand data would indicate.

April new housing starts rose 2.2%, while building permits fell 1.5%.

The rise in April starts is more or less evenly split between single- and multi-family units. The small decline in April building permits, meanwhile, is entirely due to a 7.7% slump in the multi-family component, which is volatile on a month-to-month basis but has been pretty flat for a year.

In contrast, single-family dwelling permits rose by 3.1%. This is the third straight increase, reflecting lower construction costs and lack of existing home sales.

The bigger picture here is that residential construction is now stabilising, after being a huge drag on fixed investment in 2022. Single-family starts fell at an 8.8% annualised rate in the first quarter, following declines of 52% and 21% in Q3 and Q4 2022, respectively.

Retail Sales

April retail sales rose 0.4%, below the consensus of 0.8%. Sales ex-autos were up 0.4%, in line with the consensus.

The April rebound in total retail sales follows two straight months of decline, but still leaves spending comfortably below its recent January peak.

Manufacturing

April industrial production rose 0.5%, in contrast to consensus expectations of no change.

Manufacturing output rose 1.0%, significantly higher than the consensus expectation of 0.1%. Manufacturing output ex-autos rose at a much more modest 0.4%.

The ~10% spike in vehicle manufacturing is unlikely to be sustained, given production levels are above pre-Covid highs.

Find out about

Pendal Focus

Australian Share Fund

Crispin Murray,

Head of Equities

The upshot is that the chance of a large rebound in manufacturing activity in the US for the remainder of CY23 looks unlikely.

US Results Season

The blended earnings growth rate for Q1 S&P 500 EPS currently stands at -2.2%, compared to the -6.7% expected at the end of March.

Of the 95% of S&P 500 companies that have reported for Q1, 78% have beaten consensus EPS expectations, better than the 73% one-year average and the five-year average of 77%.

In aggregate, companies are reporting earnings that are 6.5% above expectations, better than the 2.8% one-year average positive surprise rate but below the five-year average of 8.4%.

About Jim Taylor and Pendal Focus Australian Share Fund

Drawing on more than 25 years of experience investing in top-performing Australian companies and a background in accounting, Jim manages our Long/Short Fund and co-manages our Imputation Fund. He is a Chartered Accountant with membership of the Australian Institute of Chartered Accountants.

Pendal Focus Australian Share Fund is managed by Crispin Murray. The fund has beaten its benchmark in 14 years of its 18-year history (after fees), across a range of market conditions. Find out more about Pendal Focus Australian Share Fund here.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

What can we learn about the RBA’s mindset in its latest meeting minutes? Pendal’s head of government bond strategies TIM HEXT has a few insights

THE Reserve Bank is very low on confidence about the economic outlook, based on the newly-released minutes from its last policy meeting on May 2.

In fairness these are uncertain times, but the very well-resourced RBA is expected to have better insights than anyone.

The main question is how big an impact have we seen from 3.75% of rate hikes in 12 months.

There was little guidance or insights in the minutes, other than observations that retail sales and output are slowing.

Instead, we had general comments like this:

“Members judged that the forecasts were still consistent with the economy remaining on the narrow path on which inflation comes down steadily and the unemployment rate increases but remains below pre-pandemic levels. At the same time, members acknowledged that there were significant uncertainties, and that history highlights the challenges of staying on such a path.”

It seems the RBA decided back in early February that three more hikes were needed, and the pause in April was just to make sure the March credit wobbles didn’t return.

In other words, the onus was on the April data to be weak enough to discourage another hike in May — which it wasn’t.

Now the narrative has changed.

The RBA seems happy with 3.85% at least for a few more months.

The onus remains on the data to be strong enough against expectation for another hike. This has not stopped markets pricing something in.

A reliance on lagging data

By definition, the RBA is always data dependent.

Find out about

Pendal’s Income and Fixed Interest funds

But for now, it’s the lagging data like employment — and very laggy data like wages and inflation — driving decision making.

This risks a policy mistake of overtightening.

As the RBA itself expects, wages won’t peak till later this year. Even that may be too early as more public sector agreements come through.

In this respect I am reminded of the last time this happened in February and March 2008.

Credit wobbles had been building all through 2007. Even equity markets were finally taking notice in early 2008.

Bear Stearns was teetering.

Yet the high CPI print of late January 2008 — on the tail of a mining investment boom — saw the RBA hike twice, from 6.75% to 7.25%.

Wage growth did not peak till 2009.

I am not suggesting another GFC looms. The financial system has been massively redesigned since then (US regional banks aside).

But it shows that relying on inflation and wage numbers to set month by month policy can be dangerous, leaving you well behind the current pulse.

Slow start on RBA review recommendations

On a final note, if I was the RBA governor I would be already implementing a number of the RBA review recommendations that don’t need legislation.

For example, I would already be changing the meeting schedule to eight a year, followed by a press conference each time.

This would show an evolving RBA that doesn’t need a big shake-up.

Maybe there’s an explanation why changes haven’t happened yet. Maybe they’re still coming.

It would show an RBA stirred into action, not shaken.

About Tim Hext and Pendal’s Income & Fixed Interest boutique

Tim Hext is a Pendal portfolio manager and head of government bond strategies in our Income and Fixed Interest team.

Tim has extensive experience in banking, financial markets and funding including senior positions with NSW Treasury Corporation (TCorp), Westpac Treasury, Commonwealth Bank of Australia, Deutsche Bank, Bain & Co and Swiss Bank Corporation.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia.

Find out more about Pendal’s fixed interest strategies here

About Pendal

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

In 2023, Pendal became part of Perpetual Limited (ASX:PPT), bringing together two of Australia’s most respected active asset management brands to create a global leader in multi-boutique asset management with autonomous, world-class investment capabilities and a growing leadership position in ESG.

Here are the main factors driving the ASX this week according to our head of equities Crispin Murray. Reported by portfolio specialist Chris Adams

MARKETS are range-bound due to two competing factors.

On one hand, there is concern that a recession could harm company earnings.

On the other hand, there is hope that a possible end to rate hikes could support the market’s valuation.

As a result, the US S&P 500 index is oscillating between 3800 and 4200.

At the moment, risk is skewed towards markets breaking higher, due to better-than-feared earnings and signs that inflation is easing.

In Australia, the S&P/ASX 300 gained 0.75% last week while the S&P 500 was off 0.24%. Bond yields shifted slightly higher.

The only move of any note was a fall in base metal prices, with copper down 4%. This reflected ongoing disappointment in the China-recovery story.

In the US we saw slightly better inflation numbers and signs that credit conditions were tightening (indicated in the latest Fed survey of senior loan officers at banks, known as Senior Loan Office Opinion Survey).

These raise the odds of the Fed holding rates flat in June.

On the stock front we saw an announcement of consolidation in the lithium space, with a proposed tie up between Australia’s Allkem (AKE) and US-listed Livent.

US inflation

A number of reassuring inflation data points emerged last week.

- The US headline CPI for April came in a touch softer than expected, rising 0.4% monthly and 4.9% annually. The effect of energy is now negative and impact from food flat month-on-month.

- Core CPI was also better than expected, up 0.41% monthly and 5.5% yearly.

- The impact of the shelter component is beginning to roll over, as flagged by lead indicators. Those same indicators suggest this component still has some way to fall, which could ultimately shave up to 2% off core CPI.

- The market liked the fact that non-shelter service was only up 0.11% month-on-month, helped by lower travel and hotel pricing. This may not be sustainable.

- The trimmed-mean core (which excludes CPI components with the most extreme monthly movements), came in at 0.38% monthly. It was 0.4% in March and 0.4% in February. This is also heading in the right direction.

- Producer Price Index (which measures the change in prices received by US producers for their goods and services) was also lower than expected. The headline index was down to 3.2%. Core rose 0.2% monthly, versus 0.3% expected.

While inflation data has improved, it remains too high for the Fed’s liking.

There are also signs this may be flowing through to longer-term expectations.

Five-year inflation expectations have risen to 3.2% annualised — a new high for this cycle.

This data series is volatile and did reverse after spiking to 3.1% last year.

But central banks fear this kind of shift, because it represents an embedding of inflation expectations.

Tighter US credit conditions

Each quarter, the Fed surveys senior loan officers at US banks about their lending practices and the current state of the credit markets.

The latest Senior Loan Officer Opinion Survey (SLOOS) suggested a small tightening of credit conditions.

The market remains undecided about how far bank failures will slow the economy. The expected impact ranges from 0.4% to 1.2% of GDP.

The case for the lower end is that the tightening is limited to regional banks rather than global systemically important banks such as Bank of America and JP Morgan Chase.

Lending from the regional banks is already constrained, so this limits the additional impact.

The counter argument relates to the scale of the deposit reduction and how policy makers are dealing with crisis.

So far, the approach has been to allow banks to go under before allowing bigger banks to take them over, with risk -sharing deals.

As a result, regional banks are now extremely cautious, which may lead to a more material effect on lending.

The combined market cap of US regional banks is now less than JP Morgan Chase.

A combination of slowing inflation and slowing credit growth raises the likelihood of a pause in US rates.

US rates may now have peaked, which has been supportive for the market.

We remain mindful that the scale and pace of hikes in this cycle has not been seen for 40 years.

There is still a degree of unpredictability around the economic impact we need to factor into portfolio construction.

China

After rebounding in March, China credit growth came in weaker than expected for April at RMG1.2 trillion versus consensus at RMB2.0 trillion.

It remains stable at 10% year-on-year.

The total amount of credit growth at this time of year is below 2020 and 2021 — s well as pre-Covid.

This highlights a lack of confidence in the corporate sector, and particularly in the household sector.

The housing market remains subdued, which is affecting commodity markets.

Markets

Realised volatility in the US equity market continues to fall — and is now lower than almost any point in 2022.

This suggests a market that is becoming less unsure about the outlook.

The recovery in growth stocks — especially mega-cap US tech — is stunning.

This is explained partly by their ability to manage earnings, but also in the growing belief in Artificial Intelligence as a driver of long-term growth.

This trend also explains the outperformance of US versus Australian equities year-to-date.

One result is that breadth in the market has fallen to low levels. This is usually a negative signal for the overall market.

We are also seeing a significant breakdown in base metal prices. Copper — historically regarded as a good proxy for global growth — is breaking down to new 2023 lows and approaching levels not seen since China reversed its zero-Covid policy.

Adviser Sam is invested

in making our world

A better place.

Watch as Sam meets a

mum rebuilding her life

thanks to responsible

investing

About Crispin Murray and Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia. Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions.

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

After ‘mildly encouraging’ US inflation data, markets believe the Fed is done with rate hikes. But they may be over-estimating the potential for cuts, says Pendal’s TIM HEXT

US INFLATION data out Wednesday was mildly encouraging.

Headline CPI was 0.4% for the month and 4.9% annual. If we exclude food and energy the monthly number was also 0.4% — though slightly higher annually at 5.5%.

All this was as expected.

The mild encouragement in the latest data — which saw yields fall and equities rally — came from something called “core services inflation excluding rent”.

Excluding rent gives us a better idea of the inflation pulse outside housing. It’s important because rents tend to swamp the CPI, accounting for 41 per cent.

This measure came in at 0.11% — the smallest monthly rise since July last year.

For the first time there are signs we may settle at a pace closer to the Fed’s 2% target.

Rents

Rents are always slow to move, but can be somewhat predicted.

This is because CPI rents cover the stock of rents, not new rentals. However, with 2-3% monthly turnover in rentals they eventually catch up with new rents.

This is good news for the US, since new rents (measured by the Zillow index) are falling.

In Australia, though, the opposite is true.

New rents are rising — and we can expect overall rents to keep rising in the Australian CPI.

However, rents only make up 6% of the CPI in Australia.

We measure housing costs more widely than the US, with new dwelling costs included.

Overall housing is 25% of the CPI in Australia against 41% in the US.

Find out about

Pendal’s Income and Fixed Interest funds

Market Implications

Markets now believe the Fed is done with hiking.

Without a new surge in employment or inflation this looks fair.

After all, the US cash rate has now caught up with the Fed’s own expectation of where they see rates topping out, known as the Fed Dots.

US markets cannot stand still though, so they’ve factored in 75 basis points of cuts.

This will be a test for the Fed’s resolve on inflation.

Even though the pace of inflation will fall soon to around 0.2-0.3% a month, it will still leave inflation above the Fed’s 2% target.

Without a significant credit crunch or slowdown this does not leave room for rate cuts.

Perhaps the market is saying there is a 50% chance of no moves and 50% chance of 1.5% lower rates, because a recession would mean larger and quicker rate cuts.

On average there is a six-month lag between the last hike and first cut in the US.

For now we remain rangebound in yields with a small trend lower.

Inflation data should be friendly going forward but employment data may take some time to moderate.

About Tim Hext and Pendal’s Income & Fixed Interest boutique

Tim Hext is a Pendal portfolio manager and head of government bond strategies in our Income and Fixed Interest team.

Tim has extensive experience in banking, financial markets and funding including senior positions with NSW Treasury Corporation (TCorp), Westpac Treasury, Commonwealth Bank of Australia, Deutsche Bank, Bain & Co and Swiss Bank Corporation.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia.

Find out more about Pendal’s fixed interest strategies here

About Pendal

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

In 2023, Pendal became part of Perpetual Limited (ASX:PPT), bringing together two of Australia’s most respected active asset management brands to create a global leader in multi-boutique asset management with autonomous, world-class investment capabilities and a growing leadership position in ESG.

The latest bottle and can recycling technology isn’t just good for the planet. It’s an investing opportunity as well, argues Regnan’s MAXINE WILLE

- Circular economy drives take-up of reverse vending machines

- Find out more about the Circular Economy

- Find out about Regnan Global Equity Impact Solutions fund

EACH year, 1.4 trillion beverage containers are used around the world, representing a huge amount of material that potentially could be collected, reused and recycled.

It’s also an opportunity for “impact investors” looking for a way to make money and make the world better, believes Maxine Wille, an analyst at Regnan Global Equity Impact Solutions fund.

The global leader in what’s known as “reverse vending machines” is TOMRA, which is listed on the Oslo Stock Exchange and has about 80,000 installations across more than 60 markets, says Wille.

“Rather than paying money and getting a bottle out of the machine — which is what you would do at a normal vending machine — you feed it back into the reverse vending machine [and get paid] and the container is either recycled or reused,” she says.

“We are long-term shareholders.”

TOMRA was recently one of three companies given concessions by the Victorian government in Australia to develop the state’s container deposit scheme, which is due to start in November 2023.

TOMRA already operates in NSW, as this video shows:

The Victorian scheme will reward consumers with a 10-cent refund for every eligible can, carton and bottle they return.

The Norwegian group has been chosen as a network operator.

It will establish and maintain a network of refund collections points, distribute refund amounts to consumers, and report on participation and redemption rates.

“TOMRA is still very clearly the innovation leader in this space,” Wille says.

“What you want from a reverse vending machine is security – you don’t want the machine to be tricked or duped. And you want the machine to be as convenient and quick as possible for customers.”

A recent TOMRA technological breakthrough has improved both security and ease-of-use, Wille says.

“You used to have to feed one bottle at a time, but now TOMRA has pioneered a machine where you can throw in a bag of over 100 mixed bottles and cans at once.

“You throw them in, and the machine sorts them.

Find out about

Regnan Global Equity Impact Solutions Fund

“We look to invest in innovation leaders within a particular industry. We want to be confident that they can stay market leaders as a result of delivering the most innovative product.”

The reverse vending machine market is growing quickly in Australia and throughout the European Union.

“There are still a number of countries likely to implement a deposit return schemes, just like Victoria did,” Wille says.

One of the main incentives in Europe is the European Union’s directive on single-use plastics that nominates a 77 per cent collection rate for plastic bottles by 2025, increasing to 90 per cent by 2029.

“Reverse vending machines and deposit return scheme are the most effective, and proven, way to achieve these very high recycling targets.”

About Maxine Wille

Maxine is an investment analyst with Regnan’s impact equity team, which manages the Regnan Global Equity Impact Solutions Fund. Maxine previously worked with Hermes’ Impact Opportunities Equity Fund.

About Regnan

Regnan is a responsible investment leader with a long and proud history of providing insight and advice to investors with an interest in long-term, broad-based or values-aligned performance.

Building on that expertise, in 2019 Regnan expanded into responsible investment funds management, backed by the considerable resources of Perpetual Group.

The Regnan Global Equity Impact Solutions Fund invests in mission-driven companies we believe are well placed to solve the world’s biggest problems.

The Regnan Credit Impact Trust (available in Australia only) invests in cash, fixed and floating rate securities where the proceeds create positive environmental and social change. Both funds are distributed by Perpetual Group in Australia.

Find out about Regnan Global Equity Impact Solutions Fund

Find out about Regnan Credit Impact Trust

For more information on these and other responsible investing strategies, contact Head of Regnan and Responsible Investment Distribution Jeremy Dean at jeremy.dean@regnan.com.

There wasn’t much to move markets in the 2023 federal Budget, leaving next year’s stage 3 tax cuts as the main discussion point, says our head of bond strategies TIM HEXT

OVER the 2022-23 tax year, the government has drained ever so slightly more money (revenue) from the economy than it injected (spending).

That’s resulted in a forecast $4 billion surplus in this week’s federal Budget.

In other words, the government has neither added nor taken away from economic activity.

How has this improvement happened?

About half of the improvement from original forecasts is old-fashioned bracket creep and increased employment.

That is, we the workers are paying more.

The other half comes courtesy of the corporate sector: directly through higher commodity production and prices, but also through higher general corporate earnings.

Last time this happened, pre-GFC, we ended up with the Future Fund (helped also by the sale of Telstra).

In fairness to this government though, then prime-minister John Howard didn’t take over from a pandemic economy.

Like all things post-pandemic, it takes time to get back to normal.

Inflation Impact

Markets have largely ignored this Budget.

Looking at the entrails, the part which interests us most is the impact of measures on inflation.

The government argues its cost-of-living relief measures — mainly around rent and energy — will reduce inflation by 0.75% in 2023-24.

If these are delivered as subsidies, not rebates, it will feed through to the Consumer Price Index. This is partly offset by a re-introduction of tobacco excise — increases of 5% a year for the next four years.

Find out about

Pendal’s Income and Fixed Interest funds

Tobacco makes up 2.75% of the CPI, so that adds 0.15% back, giving a net decrease of 0.6%.

Boosts to welfare and wages in sectors such as aged care are also inflationary, though the Budget avoids assessing those.

It will be interesting if the RBA lowers its inflation forecasts further next time, having recently lowered the 2023 forecast from 4.75% to 4.5%.

We were already at 4% for our forecast. We will further analyse the detail to see if that needs revising after this Budget.

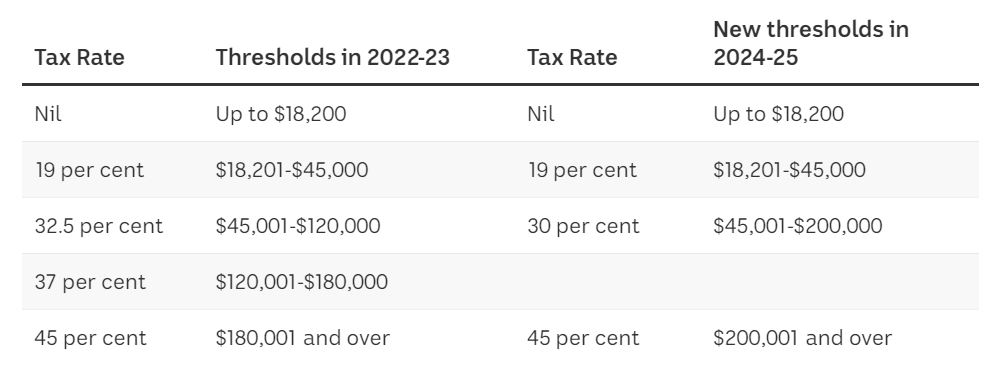

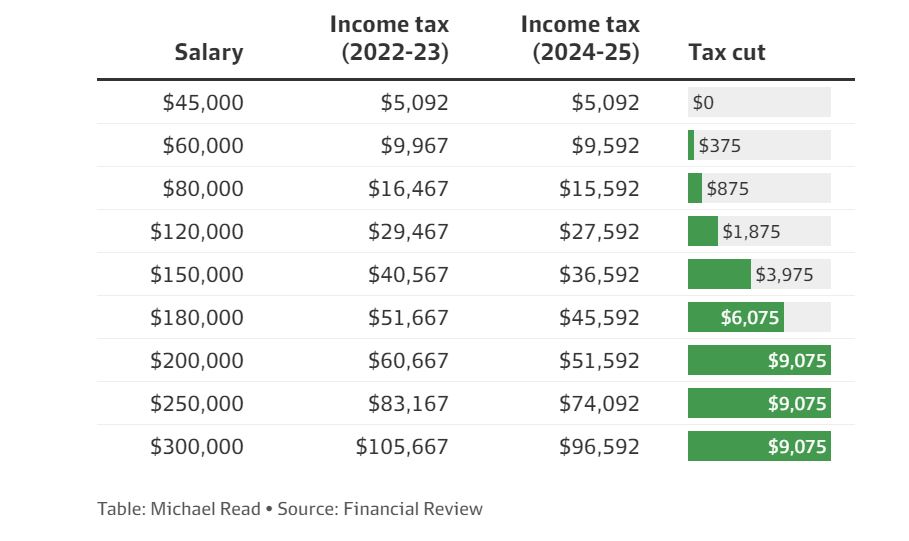

Stage 3 tax cuts centre stage

We expect discussions to turn quickly to the Stage 3 tax cuts due in July 2024.

This is due to their sheer scale and the impact they will have on consumer’s pockets. Below you can see tables from ABC News and The Australian Financial Review showing the impact of these cuts, which are already in law:

If you earn $100,000 a year, close to average full-time earnings, you get an extra $1375.

Most likely this barely compensates you for a number of years of bracket creep.

But if you earn $200,000 you get $9075 extra after the stage 3 changes.

These changes will cost the government $243 billion in lost revenue over the next decade.

Though I am less concerned about their affordability (after all, the government via the RBA owns the printing press) than the economic impact.

I am not arguing against the tax cuts, but I expect Labor may look for modifications to make them more progressive.

Lower income earners have a higher propensity to spend than save. But the economic backdrop against which they will take place is important.

We expect inflation to be nearer 3% and GDP nearer 1% by mid next year.

This will make the tax cuts economically affordable, since their boost to inflation and activity will be manageable.

But it does mean the RBA may be more reluctant and slower to cut rates.

Either way the budget discussions will quickly turn to this important change leading into next year’s budget.

As mentioned, the cuts are already law so if the government wants to modify them it will need to get the legislation through well before the next Budget.

About Tim Hext and Pendal’s Income & Fixed Interest boutique

Tim Hext is a Pendal portfolio manager and head of government bond strategies in our Income and Fixed Interest team.

Tim has extensive experience in banking, financial markets and funding including senior positions with NSW Treasury Corporation (TCorp), Westpac Treasury, Commonwealth Bank of Australia, Deutsche Bank, Bain & Co and Swiss Bank Corporation.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia.

Find out more about Pendal’s fixed interest strategies here

About Pendal

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

In 2023, Pendal became part of Perpetual Limited (ASX:PPT), bringing together two of Australia’s most respected active asset management brands to create a global leader in multi-boutique asset management with autonomous, world-class investment capabilities and a growing leadership position in ESG.

Here are the main factors driving the ASX this week according to portfolio manager RAJINDER SINGH. Reported by portfolio specialist Chris Adams

- Find out about Rajinder’s Pendal Sustainable Australian Share Fund

THE Reserve Bank managed to wrong-foot most of the experts last week, raising rates after April’s pause.

The US Fed also raised 25bps, but signalled it was now open to pausing further rate rises.

A number of important US data releases continued to paint a mixed signal for the economy.

The Australian market went through its unofficial third-quarter reporting season at last week’s Macquarie Australia Conference.

There was volatility in bond markets last week. Equities and commodities were mostly softer, but helped by a strong rally on Friday. The S&P/ASX 300 fell 1.17% while the S&P 500 was down 0.78%.

It was mostly stock-specific news that moved share prices in Australia. Two of the big four banks reported, which was instructive of future performance for the sector.

US employment and manufacturing data

It was a big week for US employment data.

Firstly, the Job Openings and Labor Turnover Survey (JOLTS) confirmed other recent data that the US jobs market was solid, but gains were slowing.

JOLTS is typically used as a measure of labour market tightness. Last week’s numbers confirmed that some of the post-pandemic pressures were starting to ease.

The number of layoffs continued to trend higher. Overall job openings — while still high — fell from 9.97 million in February to 9.59 million in March.

The drop in job openings was concentrated in construction and retail trade, which implies the re-opening story is slowing.

Find out about Pendal Sustainable Australian Share Fund

Initial unemployment claims printed 242,000 for the week ending April 29, down from a revised 229,000 in the prior week. The four-week moving average rose to 239,000.

The latest Challenger Report, which tracks employment trends, indicated that hiring trends for the first four months of 2023 were the weakest since 2016.

The final big US employment data point late in the week was non-farm payrolls.

US payroll employment rose a solid 253,000 in April, soundly beating expectations of +180,000 — though there were notable downward revisions to prior months.

The headline US unemployment rate fell to 3.4%. Participation was flat at 62.6%.

The same report indicated that average hourly earnings were robust, up 0.5% month-on-month and still growing solidly at 4.4% year-on-year.

Overall, these datapoints paint a picture of a jobs market that remains solid, though the momentum is clearly slowing.

The absence of a decrease in average hourly earnings rate will be watched closely by Fed policy makers.

In terms of private business conditions indicators, the US Manufacturing PMI — a monthly index measuring the economic health of the manufacturing sector — was released on Tuesday.

The headline number was 47.1, which is still in mild contraction territory. New orders at 45.7 indicate there is no turning point any time soon.

A decent correlation between US bank lending conditions and the PMI indicates further softness, given recent concerns in the US financial system, particularly in regional banks.

The Fed meeting

The Fed raised rates 25bp to a range of 5% to 5.25% at last week’s meeting, despite recent concerns over stress in the US banking system.

However the rate-setting Federal Open Market Committee hinted at a pause in the hiking cycle by removing “the committee anticipates that some additional policy firming may be appropriate” from its post-meeting statement.

The FOMC balanced this hint toward a June pause with a message that it retains a hawkish bias.

The committee said it would take into account the totality of the data “in determining the extent to which additional policy firming may be appropriate”.

On his conference call, Fed chair Jay Powell also noted:

- “We’re no longer saying that we anticipate” further increases; which was “a meaningful change”

- The US labour market remained tight. Labour demand still exceeded supply, though some progress was being made

- It’s possible the US would have a “mild recession,” but Powell’s forecast remains for modest growth

- The Fed funds rate was at a 16-year high — “not far off” from a restrictive level

In a Q&A, Powell said market expectations for rate cuts in 2023 might be incorrect if inflation was sticky.

This might dampen the view of a very short pause, before cuts are in needed at the back end of 2023.

All in all, there was quite a bit of nuance for the market to digest. US two-year Treasuries in particular experienced significant intraday volatility.

Europe macro

Eurozone inflation rose 0.7% in April. Over 12 months it was up 7%, compared to a 6.9% figure in March.

This was broadly in line with consensus. The underlying Consumer Price Index was still persistently high at 5.6%.

After three hikes of 0.5 percentage points, the European Central Bank followed with a more moderate 25bp increase to 3.25%. This matched market expectations.

Unlike the Fed, ECB president Christine Lagarde made it clear she was not about to pause and expected to hike further.

“We have more ground to cover and we are not pausing,” she said. “That’s extremely clear.”

Some ECB members advocated for a bigger hike. But in a partial concession the ECB statement said it expected to halt reinvestments under its stimulatory Asset Purchase Program from July.

That should increase the run-off rate from 15 billion Euro to 25 billion Euro per month.

China macro

China’s markets were closed part of the week for the May Day Golden Week holiday. However we did see the release of manufacturing data from China’s National Bureau of Statistics (NBS).

NBS manufacturing PMI unexpectedly declined to 49.2 in April, below consensus expectations of 51.4. New orders fell to 48.8 from 53.6, indicating lacklustre demand.

Despite the moderation, non-manufacturing PMI stayed elevated at 56.4. Services and construction both pulled back slightly — but were still firmly in the recovery zone.

RBA outlook

The RBA defied consensus expectations and lifted the cash rate by 25bps to 3.85%, despite pausing its run of rate hikes in April.

The bank’s forward guidance was interpreted as being on the hawkish side. Governor Phil Lowe noted that “some further tightening of monetary policy may be required”.

The timing of the rate hike surprised many RBA watchers who had only just revised down rate expectations following a softer-than-expected first-quarter CPI print on April 26.

Just prior to the announcement, the market was priced for an 11 per cent chance of a 25bp hike, while 22 of 30 surveyed economists expected the RBA to remain on hold.

The RBA only slightly adjusted its inflation forecasts, which indicate 4.5% by end 2023 and 3% by mid-2025.

These are a touch weaker than February’s forecasts, but they have inflation getting back to the top edge of the 2-3% target band at the same time as previously.

GDP is forecast to slow this year a little more than previously expected to 1.25% (previously 1.6%), before strengthening to 2% by mid-2025 (previously 1.7%).

This left RBA watchers generally struggling to explain last week’s hike.

There was debate around communication issues, as well as the potential role of the government’s recent RBA review and recommendations.

The RBA statement’s focus on the services component of inflation is worth noting.

“Services price inflation is still very high and broadly based and the experience overseas points to upside risks,” the statement said.

“Unit labour costs are also rising briskly, with productivity growth remaining subdued.”

As pandemic shortages ease, goods inflation has started to roll over.

But the RBA is clearly concerned about the increasing contribution of services inflation to overall inflation levels in the Australian economy.

Markets

The S&P 500 is up a healthy 8.3% this year.

But there are some concerns about market breadth with the “average” stock underperforming mega caps in the S&P50.

US quarterly earnings season is closing out, with 86 per cent of companies having reported.

Actual earnings so far been down about 3 per cent, which is better than an expected drop of about 7 per cent.

Sales growth has been strong and margins better than feared.

Some commentators hope we’ve seen the worst of the negative earnings revisions.

Brent crude oil dropped another 5 per cent to $75.30. It’s now below the level before last month’s OPEC production cut and significantly below pre-Ukraine war levels.

Macro uncertainty is definitely a factor. But some are also pointing to an unwind of speculator positions exacerbating moves in a relatively low-volume period.

Gold is trading at close to all-time highs around US$2017/Oz. But the commodity has struggled to get past this level on previous occasions since many buyers — especially retail — choose to sit out of the market at these levels.

It is worth noting the AUD Gold price is well above previous levels at more than A$3000/Oz.

About Rajinder Singh and Pendal’s responsible investing strategies

Rajinder is a portfolio manager with Pendal’s Australian equities team. He has more than 18 years of experience in Australian equities.

Rajinder manages Pendal sustainable and ethical funds including Pendal Sustainable Australian Share Fund.

Pendal offers a range of responsible investing strategies including:

- Pendal Sustainable Australian Share Fund

- Crispin Murray’s Pendal Horizon Fund

- Pendal Sustainable Australian Fixed Interest Fund

- Pendal Sustainable Balanced Fund

- Regnan Credit Impact Trust

- Regnan Global Equity Impact Solutions Fund

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Responsible investing leader Regnan is part of Pendal Group.

Government policy is an increasing risk factor for investors, argues Pendal head of equities CRISPIN MURRAY

- Government policy an increasing risk factor for investors

- Resource and energy companies at risk

- Find out about Pendal Focus Australian Share fund

GOVERNMENT policy is an increasing risk factor for investors, particularly in the resources and energy sectors, says our head of equities, Crispin Murray.

“As an investor, you really need to have conviction — and part of that comes from your ability to understand all the risks within an investment case,” Murray says.

“You are always worried about unpredictable events, and this is where the influence of government becomes a bigger issue, particularly around unpredictable policy.”

Murray, speaking at The Australian Financial Review Live conference, says sovereign risk can be more unpredictable than competitor risk.

“Competitors are largely focused on returns, so you can anticipate what they’re likely to do.

“But governments overlaying policy agendas can create more unpredictable outcomes.”

“Largely speaking, competitors are focused on returns — so you can anticipate what they’re likely to do.

“If you have governments with other policy agendas overlaying, that can create quite unpredictable risks.”

Murray uses the recently introduced federal safeguard mechanism in Australia as an example.

The safeguard mechanism effectively regulates the emissions of Australia’s 215 biggest polluters, including many fossil fuel companies, forcing them to reduce carbon output.

It comes into effect from July.

“They are still negotiating on details, but it means we’re asking mining companies, as an example, to quickly cut their scope one emissions,” Murray says.

“That means cutting diesel emissions over the next seven years – and there’s no proven commercial solution to that.

“That creates an extra cost and is going to deter investment.

“In isolation that is not going to be a huge issue. But when you add a few other things in — new taxes and things like that — it can very quickly start weighing on the market.”

Resource and energy companies are hit hardest.

“Where you have an unpredictable fiscal environment where the rules can change, retrospectively … that ultimately deters capital from wanting to be deployed,” Murray explains.

“Maybe as a society we are saying we don’t want capital deployed in the resources or energy sectors anymore, but that is the sort of example that will ultimately have an impact on society.”

Companies and investors will need to work into financial models the cost of carbon — even though in Australia there is no mandated carbon price — because under the safeguard mechanism many companies will have to purchase carbon offsets.

“I think we will see carbon price go up more than people realise,” says Murray.

“And it’s not beyond the realms of possibility that we will see a carbon price by the end of the decade.”

Adviser Sam is invested

in making our world

A better place.

Watch as Sam meets a

mum rebuilding her life

thanks to responsible

investing

About Crispin Murray and Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia. Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions.

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

Here are the main factors driving the ASX this week according to portfolio manager Jim Taylor. Reported by portfolio specialist Chris Adams

MOST eyes were on a generally positive US reporting season last week, with the S&P 500 up 0.89% while the S&P/ASX 300 fell 0.28%.

US economic data was mixed, but did little to change the current narrative of slowing economic growth.

In Australia the headline consumer price index (CPI) for Q1 2023 was a little ahead of consensus expectations, but lower than Q4 2022.

The market is now expecting the RBA to maintain current rates at its May meeting.

Elsewhere, quarterly production reports from the miners have been generally disappointing, with higher costs and lower volumes, for a variety of reasons.

Australian inflation

Headline CPI came in at 1.38% for Q1 2023.

While this was above consensus expectations of 1.30%, it was well below the 1.90% of Q4 2022.

Annual growth is running at 7.0% versus 7.8% in Q4 2022.

Measures of underlying inflation were marginally softer than expected.

The trimmed-mean CPI rose 1.2%, down from 1.7% in Q4 2022 and below the 1.4% consensus expectation.

It is also 0.2% lower than the RBA estimate in February’s Statement on Monetary Policy.

Midcaps on

the move

Hear from lithium industry pioneer

Ken Brinsden and Pendal’s

Brenton Saunders

On-demand webinar

The breadth of the inflation impulse continues to diminish.

The share of items in the CPI basket rising more than 3% year-on-year fell to 60%, from 76% in the previous quarter.

The moderation in inflation is driven by goods, with year-on-year growth falling from 9.5% to 7.6%.

Price discounting by retailers saw falls across furniture (-4.6 per cent), major and small appliances (-3.8 per cent and -3.6 per cent) and clothing (-3.2 per cent).

Services inflation accelerated from 5.5% to 6.1% year-on-year. Rental prices increased 4.9% within the basket, the largest annual rise since 2010.

US Economic data

There were some mixed messages from economic data last week, but on balance seems enough to lock in a 25bp hike from the Fed for May.

Inflation

The core Personal Consumption Expenditure (PCE) deflator rose 0.3% month-on-month for March, in line with consensus.

Upward revisions to the result for January and February mean the annualised number came in at 4.9%, above the 4.7% expected by consensus.

Find out about

Pendal Horizon Sustainable Australian Share Fund

The Core PCE services ex-housing figure, which is closely watched by the Fed, came in at 0.24% month-on-month. This is the lowest reading since July last year and down on the 0.36% result for February and the 0.44% average increase over the prior three months.

Consumer inflation expectations as measured by the Conference Board continue to be contained. The median inflation expectation for twelve months hence fell from 5.5% in March to 5.3% in April. This is the lowest level since April 2021.

Wages and employment

While inflation trends are reassuring, strength in employment costs seems enough to keep the Fed on track for a rate hike this month.

The Q1 2023 Employment Cost Index (ECI) rose 1.2% versus consensus expectations of 1.1%. It is up 4.9% year-on-year.

Within this, private sector wages-ex-incentives rose 1.3%, or 5.2% annualised, which is an increase from the 4.3% recording in Q4 2022.

While this is a break in the trend of slowing wage growth, data from Bank of America which looks at consumer deposit data to measure after-tax wage and salaries, suggests that the three month moving average has fallen to 2.0% annualised. This is down from the peak of 8.0% by the same measure in Q2 2022.

Elsewhere, weekly jobless claims fell from 1,868k to 1,858k. This is fewer claims than consensus expected and underscores the notion of a resilient labour market.

However layoffs continue and are broadening out from the tech sector. The largest layoff announcements for April are from David’s Bridal (9,000 jobs), 3M (4,000 jobs) and EY (3,000 jobs).

US GDP

US GDP grew by 1.1% quarter-on-quarter in Q1 2024. This is down from 2.6% in Q4 2022 and below consensus estimates of 1.9%.

Consumer spending remains robust, up 3.7% quarter-on-quarter versus 1.0% in Q4 2022. However this was more than offset by weaker inventory investment, which took 2.3% off Q1 growth.

Housing also dragged, with residential investment taking 0.17% off growth.

That said, this was less than the 1.4% and 1.2% drag form the third and fourth quarters of 2022, respectively.

Find out about

Pendal Focus

Australian Share Fund

Crispin Murray,

Head of Equities

New home sales have proved stronger than expected. Sales increased 9.6% to an annualized 683,000 pace in March.

There is an argument this is driven by low turnover in the existing homes markets, with owners unwilling to sell and re-finance at higher rates.

Markets

The air-pocket in US earnings that some feared has not materialised in this quarter.

Aggregate earnings for the S&P 500 have fallen 3.7% in Q1, versus expectations of 6.7% as at the end of March. Aggregate revenue has grown 2.9%.

Of the 53% of companies that have reported, 79% are ahead of consensus EPS expectations, versus a five year average of 77%. 74% have beaten consensus revenue expectations, versus a 69% five year average.

In aggregate, earnings are 6.9% above expectations, below the five-year average of 8.4%.

Some key takeaways:

- UPS: Noted that parcel volume trends deteriorated over the quarter, with US domestic volumes down in the high single-digits year-on year in March, versus low single digits in January.

- Microsoft: Revenue was up 7% and net income ahead of expectations. Management noted that customers are exercising some caution.

- Amazon: The market liked the strength in the international business, however reacted negatively to management’s observation that the cloud-based business is seeing slower growth as customers become more prudent in spending.

About Jim Taylor and Pendal Focus Australian Share Fund

Drawing on more than 25 years of experience investing in top-performing Australian companies and a background in accounting, Jim manages our Long/Short Fund and co-manages our Imputation Fund. He is a Chartered Accountant with membership of the Australian Institute of Chartered Accountants.

Pendal Focus Australian Share Fund is managed by Crispin Murray. The fund has beaten its benchmark in 14 years of its 18-year history (after fees), across a range of market conditions. Find out more about Pendal Focus Australian Share Fund here.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

As ‘stewards of capital’ Pendal undertook 562 ESG engagements on behalf of investors in 2022. Here, CEO Richard Brandweiner explains why this is important

- Download Pendal’s Responsible Investment and Stewardship Annual Report (2022)

THE concept of responsible investing has evolved hugely over the past decade, and the pace of change is accelerating.

Not necessarily in clear directions, however.

We’ve reached a point where there wouldn’t be many boards or management of major Australian listed companies not taking Environmental, Social and Governance (ESG) risks seriously.

A cursory glance at MSCI ESG ratings shows an improvement in scores across the market in recent years.

As one of the leading sustainable investors in the country, Pendal has played an important role in this transition, driving companies to change.

This is something we are very proud of.

It’s also reasonable to believe that the potential alpha available from targeting “box-ticking sustainability improvers” has eroded over time.

Curiously, companies that are deprived of capital as a result of poor ESG behaviours may well have higher expected returns, at least over shorter time periods.

This reflects their higher risk and lower multiples. Certainly, higher fossil fuel prices over the past year made excess returns very challenging for sustainable investors.

Nevertheless, we know that changing consumer preferences, increasing transparency and a significant shift in the direction of policy settings are real.

These will demand ever more vigilance on behalf of corporates to stay on top of their sustainability agenda.

Box-ticking increasingly unhelpful

So, what does this new ESG environment look like?

Firstly, box ticking will become increasingly less helpful.

The challenge for investors is identifying authentic leadership that can leverage non-financial factors to generate real economic value.

Since many of the basic hygiene factors are already considered, it will become particularly difficult for systematic processes like those used by the mainstream ESG score providers to assess this.

It is here that Pendal’s deep fundamental research resources will be well placed.

Secondly, the next horizon is one of impact.

What are the externalities created by a company? To what extent is a company, through its product and services, making the world a better or worse place?

Many see this as the third axis of investing.

The first was return, the second was risk — and the third is impact.

Notoriously difficult to measure, full of unintended consequences and spurious correlations, impact is nevertheless a real component of allocating capital.

It is the “so what” of owning a business and holding management accountable.

In 2023, the Federal treasurer has started asking sincere questions of the role of financial markets in impacting our society as whole.

The influence that we have on our system as stewards of capital has never been lost on us.

This report aims to highlight how we have carried out this responsibility.