It’s been a busy time for fixed-interest investors. In this bumper edition, our head of government bond strategies TIM HEXT outlines his views on the latest inflation data, the RBA review and YFYS reforms

FIRST to the latest Australian inflation data for the March quarter.

Since the introduction of monthly inflation data we know about 70 per cent of the quarterly story ahead of time – and the latest data came in largely as expected.

Headline inflation was 1.4% (7% annual). Underlying, or trimmed mean inflation (the RBA’s preferred measure) was 1.2% (6.6% annual).

Inflation remained strong in housing at 1.9% for the quarter, though that was boosted by gas prices up 14%.

Health was strong at 3.8% led by pharmaceutical products and medical and hospital services.

Education was high at 5.3% for the quarter, but it is only measured annually in February.

Finally, insurance was up 1.9%.

This all led to non-tradable (ie services) inflation at 1.9%, not far off the 2.1% from last quarter.

The domestic economy is not really relenting.

Goods prices continued their fall to 7.6% as supply chains return to normal. Tradables inflation was just 0.3% for the quarter.

This week’s quarterly data showed goods inflation almost flat-lining as supply chains return to normal, while services inflation jumped to 6.1%.

Given it’s a one-third / two-thirds split between goods and services, this leaves the medium-term annual inflation pulse nearer 4%.

No more hikes, but don’t expect cuts

The RBA will be encouraged that inflation is falling. Their 4.75% forecast for 2023 looks too high and will likely be revised down in May.

This means no more rate hikes, with the fixed-rate cliff doing the work on the domestic economy for the rest of 2023.

However, those looking for rate cuts late this year or early next year will be disappointed.

The easier work on inflation is done.

The harder work of reining in services inflation and the domestic economy is very much a work in progress.

It will not be smooth or pretty and will require rates stuck at this level for the rest of this year.

Overall the latest data supports our duration-friendly view on markets, but as always levels will determine our risk.

Find out about

Pendal’s Income and Fixed Interest funds

The RBA Review

Plenty was written about the RBA review last week. Most recommendations look reasonable and a review was definitely overdue.

But two things stood out to me about the report and its recommendations:

1. What about fiscal policy?

The report perpetuated the view that monetary policy is more important than fiscal policy

Most people still think monetary policy — not fiscal — is the most important lever in controlling inflation and activity.

They have elevated central banks, often with the help of central banks themselves, to a level of impact that just isn’t true.

Reading the dissection of RBA actions since 2016 must have been painful for Governor Phil Lowe, who I suspect — after being painted as the main culprit — wanted to cry out “but what about fiscal policy!”.

In fairness fiscal policy was not the focus of the report. It does occasionally reference fiscal policy, but when mentioned it’s given second billing.

From the section of the report dissecting events in the low inflation period of 2016-2019:

Some people consulted by the Review pointed to fiscal policy and the role it was playing in Australia.

During this period, fiscal consolidation weighed more heavily on domestic demand than the RBA had expected.

Prior to the outbreak of the COVID-19 pandemic, the 2019–20 Budget projected a balanced fiscal position for the financial year. At the same time, the cash rate was at historic lows.

The review heard from some that fiscal settings should have been looser to assist monetary policy to bring inflation closer to its target and boost employment.

This is quite soft language.

In reality it was absurd to try to balance the budget as some sort of fiscal bravado when there was clearly excess capacity in the economy and inflation wasn’t a problem.

From the section on the overshoot in inflation since 2021:

For example, while the Review (and many consulted by the Review) considers the strong and rapid fiscal and monetary policy response at the onset of the pandemic to be appropriate given the threat to lives and livelihoods, the cumulative effects of the measures over time contributed to the overshoot of inflation in Australia.

Indeed, Murphy (2022) found that, combined, the fiscal and monetary stimulus added 3.0 percentage points to inflation during 2022.

Of this, 0.6 percentage points were attributable to monetary policy being more accommodative than would normally be the case given prevailing economic conditions.

This suggests 80% of the overshoot problem was fiscal not monetary. Yet reading the report you’d think the opposite.

Maybe a major inquiry into fiscal actions through Covid should follow the RBA report.

Ultimately it would be more important for future episodes of massive disruption.

The report does reference closer coordination between fiscal and monetary policy but actual actions were outside its remit. It should not sit outside of the remit of those who pursue efficient public policy.

2. “Give me a one-handed Economist. All my economists say ‘on one hand…’, then ‘but on the other…” — President Harry Truman

Monetary policy will be more volatile, not less.

Will decisions be wiser under the new RBA plan? Policy is an art not a science.

A separate monetary policy board, and likely more pressure to return to targets sooner, will lead to more rate volatility. There is likely to be less patience on over-shooting or under-shooting targets.

Inflation has spent more time outside the 2-3% range than inside since the target was introduced in 1993. Yet the average is almost exactly 2.5%.

Ultimately, the RBA has been generally correct in its patience.

The RBA will now only have two of nine votes on cash rates (three if the Treasury Secretary is included).

This would not be welcomed by the RBA, despite a brave face.

I suspect the governor will work behind the scenes to persuade voting members of the RBA view prior to a vote.

But the independent members — who will love having a seat at the most important economics table in town — are not there to rubber stamp.

Encouraged to be opinionated, they will not always play ball with the RBA view.

The report celebrates a diversity of views, believing “a stronger culture of constructive challenge and openness to diverse views” is vital.

This sounds good and is important. But as anyone who has been in a decision-making seat before will testify, democracy has its challenges.

Unfortunately, we will not see why the dissenters dissented. Only the vote, not the reasons, will be disclosed.

The votes also will not be attributed, leaving us guessing, at least in the short term.

The report also does not go back 30 years to analyse the times the market got it very wrong. Let’s face it, the independent board members will often be heavily influenced by markets and the media’s running commentary.

As someone who has been making market calls for more than 30 years, I am perhaps more honest (and dare I say humble?) than many commentators.

Remember 2011 to 2014?

Markets were very slow and sceptical on RBA rate cuts, believing inflation was still a post-GFC problem when central banks didn’t.

I suspect among the six independents the market’s view would have found some favour and made the appropriate cuts less likely.

What about 2008?

Despite worsening global problems the market had hikes, not cuts, priced in right up to June 2008.

The only major episodes I can think of where markets were right and central banks were asleep at the wheel is 1994 and 2021.

Unfortunately for the RBA there is a massive recency bias.

Benchmark Reform for Your Future Your Super (YFYS)

Earlier this month Australian Treasury released a draft report for benchmark reform under Your Future Your Super (YFYS).

The benchmarks are extremely important as the performance measure for MySuper products when conducting tests.

As 13 of the 76 MySuper products discovered in 2021, underperformance against benchmark of more than 0.5% for two years in a row could be catastrophic, as new flows are halted.

Therefore when reforms are suggested to fixed income benchmarks were are very interested, since it’ss safe to assume MySuper products will adjust holdings to more closely match the new benchmark.

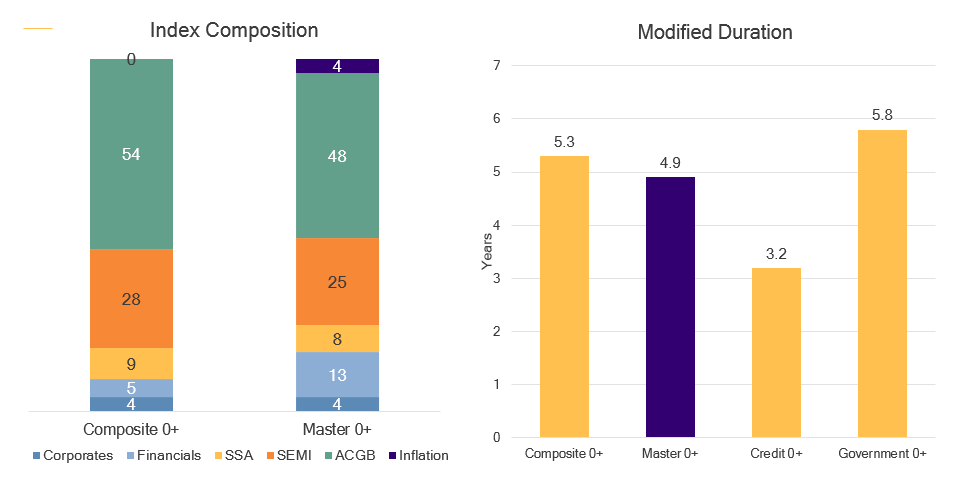

Among many proposed changes across asset classes, there is a change in the default Australian fixed income benchmark from the Bloomberg Ausbond Composite 0+ Index to the Bloomberg Ausbond Master 0+ Index.

The difference is that the Master Index includes everything in the composite plus inflation bonds and credit Floating Rate Notes (FRNs).

This increases the outstanding universe from $1.4 trillion to $1.65 trillion as $60 billion of inflation bonds and almost $200bn of credit FRNs are included

You can see a summary of the differences below:

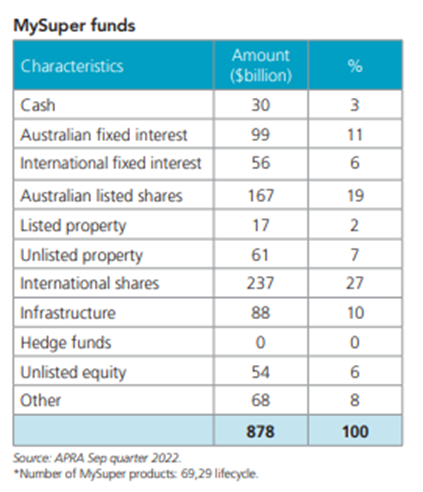

It’s estimated that more than $900 billion of Australia’s $3 trillion of super money is invested in MySuper products.

Some 60% of all super accounts are in these products. The majority sit in industry funds, but retail funds are also big providers.

Data from the Australian Super Funds Association (see below) suggests as of late last year almost $100 billion sat in Australian fixed interest, consistent with a 10-15% allocation.

Of course there are also non-MySuper products that reference the Composite Bond Index, which may seek to match the change or are indirectly captured by YFYS.

The Composite bond index spent its first 20 years, after starting in 1989, as roughly 70 per cent government and 30 per cent credit.

A massive government issuance since the GFC (and now Covid) has seen credit diluted down to 17%, of which supranationals are over half.

Introducing more Australian credit vias FRNs will see genuine credit (non-supras) almost double from 9% to 17%.

Inflation should also have a home in default products.

It could be argued that protecting purchasing power should be the first requirement of any investment, so 4% of the Master Index is far too low in my view.

However, at least it is a start in the right direction.

Market Impact of YFYS reforms

The YFYS changes are likely to be introduced in August, though fund providers will likely seek to adjust prior to that date, possibly from July 1.

We must also recognise that part of the reason for the proposed change is that some funds already have holdings closer to the new benchmark than the old.

Holding some inflation and credit FRNs and topping up duration with derivatives (mainly government bond futures) is a smart and commonplace strategy.

Ultimately, investors benefit from this.

Though the performance test has never been about optimal portfolios, but rather performance against benchmark. This will reduce tracking error for many funds.

There will still need to be some important changes.

The reduction of 0.4 years of duration is very large.

This may be worth around 15-20 basis points if we use the recent large index lengthening (March 31) of 0.2 years as a guide.

We can also reference the recent $14 billion AOFM 2034 issue that cheapened the market by around 10 basis points.

Demand for credit FRNs, which are predominately Australian banks, should be strong.

Fortunately, as the Term Funding Facility unwinds, banks will have plenty of issuance to do. This will still provide a decent tailwind for bank spreads.

Finally, inflation should see net demand.

For a small and at times challenged liquidity market — where $150m tenders can move the market 5 basis points — any large shifts will have a decent impact.

Physical inflation bonds have always enjoyed a decent discount to Inflation Zero Coupon Swaps (ZCS), since ZCS has been the favoured inflation hedge of super funds so they can deploy capital elsewhere.

This discount should narrow quite quickly and we recommend funds invest in physical bonds until the gap is closed.

Conclusion

We are increasingly factoring these changes in to our investment decision-making in the next few months.

We are also keen to hear from investors whether there is appetite for a fixed income product or unit trust based off the Master index.

We do not currently plan to change the benchmark of our two flagship funds (Pendal Fixed Interest and Sustainable Australian Fixed Interest) but look forward to an active dialogue with investors if their needs change.

About Tim Hext and Pendal’s Income & Fixed Interest boutique

Tim Hext is a Pendal portfolio manager and head of government bond strategies in our Income and Fixed Interest team.

Tim has extensive experience in banking, financial markets and funding including senior positions with NSW Treasury Corporation (TCorp), Westpac Treasury, Commonwealth Bank of Australia, Deutsche Bank, Bain & Co and Swiss Bank Corporation.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia.

Find out more about Pendal’s fixed interest strategies here

About Pendal

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

In 2023, Pendal became part of Perpetual Limited (ASX:PPT), bringing together two of Australia’s most respected active asset management brands to create a global leader in multi-boutique asset management with autonomous, world-class investment capabilities and a growing leadership position in ESG.

Pendal’s JAMES SYME warns investors to take care before jumping into South Korea or Taiwan on the back of bullish semi-conductor export expectations

- Taiwan, South Korea exports historically weak

- Look instead to the likes of Mexico

- Find out about Pendal Global Emerging Markets Opportunities fund

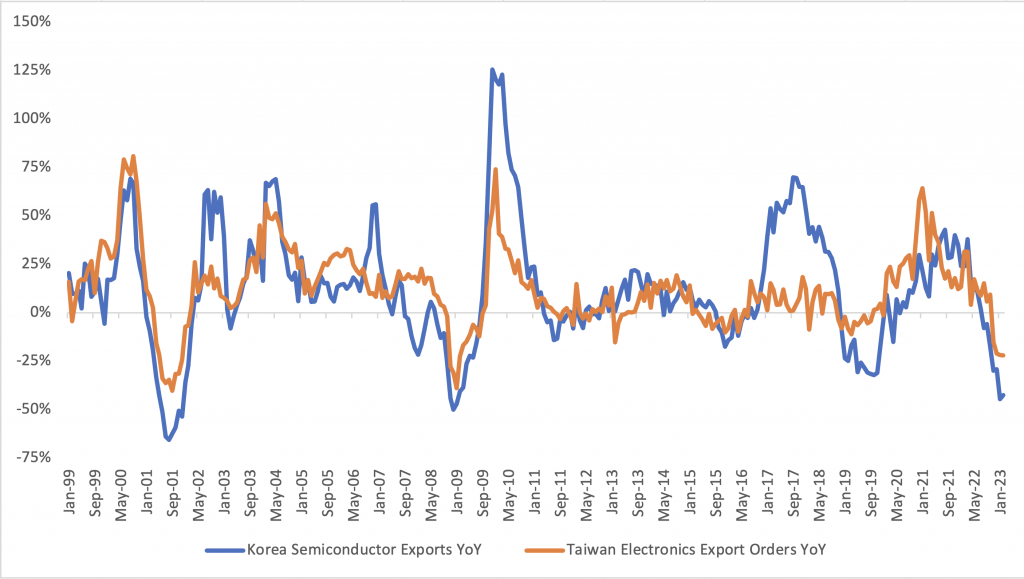

EMERGING MARKETS investors will be aware that media and analysts have recently been weighing up the prospects of a return to growth for key Asian tech hardware export markets.

But Pendal’s James Syme warns investors to take care before jumping into South Korea and Taiwan on the back of bullish semi-conductor export expectations.

Expectations that South Korea and Taiwan can lead an emerging markets recovery are overdone as both countries continue to face historically weak conditions in their key semi-conductor and electronics export industries, argues Syme.

An analysis of economic conditions and export data shows little evidence of recovery, with some key metrics as weak as they were during past global recessions like the tech wreck of 2001 and the financial crisis of 2008.

“We’ve seen a lot of a lot of investors go back to the playbook of what worked for the last couple of years — Chinese Internet stocks and Korean and Taiwanese tech hardware names,” says Syme, who co-manages Pendal Global Emerging Markets Opportunities Fund.

“But when we look at the data, we see no evidence of that at all.”

South Korean exports of semiconductors were down 42.5 per cent year on year in February. Taiwanese electronics exports fell 22 per cent for the same period.

“We’ve only seen those levels in 2008, 2001 and in 1990,” says Syme.

Find out about

Pendal Global Emerging Markets Opportunities Fund

“It may or may not be the case that the global economy is tipped into recession by Fed interest rate hikes — but looking at the current state of the tech hardware industry, it looks and feels like there’s a major recession.

“It might be that we’re seeing the tail end of a drop off in the developed world before China recovers, but our process is based on looking at what’s happening, not imagining what might happen — and when we look at what’s happening, things are difficult.”

Syme says one key indicator — the number of days of inventory in the global semi-conductor industry — has “exploded higher, even to way above where it was in the bad days of ‘08”. That implies reduced demand while this inventory bulge is worked through.

Economic data from South Korea and Taiwan are important indicators of the state of the world economy. Both countries publish a good amount of data with long time series, which can be used as a benchmark for global demand.

South Korea is a major exporter of cars, machinery and steel. Taiwan is a leading exporter of semiconductors and electronics.

Overall exports for South Korea were down 7.5 per cent in the year to February, while Taiwan’s exports fell 17 per cent over the same timeframe.

Exports are not the only indicator of tough economic times.

Purchasing manager surveys in both countries show expectations of contraction. Korean industrial production in January showed a disappointing 12.7 per cent contraction, while Taiwan’s industrial production fell 10 per cent in February to be down 21 per cent year on year.

“It’s just a really weak set of data,” says Syme.

“Now, things could recover from here, but a lot of the mood around technology right now looks difficult.

“There’s a bit of hope that Artificial Intelligence products like ChatGPT will lead to demand for server hardware.

“But if you look at the start-up ecosystem, if you look at demand for tech hardware for crypto mining, and if you look at job moves from the global scale players like Amazon, Microsoft, Google and Netflix, it looks really difficult.”

Syme says earnings expectations for South Korea and Taiwan are now trending down after being some of the best-performing earnings markets during COVID.

“Despite a recovery in China and ongoing growth in other major economies like India or Indonesia, we think it’s far too soon to be looking for Taiwan and Korea to lead.”

Look to the likes of Mexico

Instead, Syme says investors should stick to the emerging markets that are suited to current global economic conditions.

“Mexico continues to deliver in terms of exports and remittances. And Poland, Hungary and Czech are looking a lot better than a year ago.

“So, you wouldn’t say that it’s all red lights in terms of the outlook for the global economy — it’s sector specific.

“There’s an enormous shortage of people in the United States who are able and willing to drive trucks and serve food and clean and build things — that it is an enormous opportunity for Mexico, which is a supplier of people who can do that.

“The developed world has a shortage of labour — but there’s no shortage of DRAM or NAND flash or CPUs or GPUs.”

About Pendal Global Emerging Markets Opportunities Fund

James Syme, Paul Wimborne and Ada Chan are co-managers of Pendal’s Global Emerging Markets Opportunities Fund.

The fund aims to add value through a combination of country allocation and individual stock selection.

The country allocation process is based on analysis of a country’s economic growth, monetary policy, market liquidity, currency, governance/politics and equity market valuation.

The stock selection process focuses on buying quality growth stocks at attractive valuations.

Find out more about Pendal Global Emerging Markets Opportunities Fund here

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

Pendal’s income and fixed interest team favours high-quality Australian assets likely to provide investors with a stable income and protection from the uncertainty ahead. Assistant portfolio ANNA HONG explains why

- Why bonds, why now? Find out more from Pendal’s income and fixed interest team

THE current rate hiking cycle may resume in Australia as soon as next month, after a short pause in April.

That’s the suggestion from the Reserve Bank’s latest meeting minutes, released yesterday.

Even though inflation has moderated, it is still higher than targets set by the central banks, because household spending remains resilient.

A fall in inflation from 8% to 4% is the easy part – the normalisation of goods supply chains has ensured that.

But getting back to the Reserve Bank’s 2% to 3% target range or US Federal Reserve’s 2% target will be a much tougher ask.

To get there, service inflation will need to moderate from the current 6% level back down to 3%, something that for now seems unlikely.

This is because monetary policy is a blunt tool that only impacts the demand side of inflation.

Meanwhile, the current inflation flare-up is shaped largely by supply: issues with supply chains, labour market tightness, energy constrictions and issues with housing stock lead the charge.

The persistence of inflation will drive future rate decisions.

Impact of rate hikes

Meanwhile, the impact of the rate hikes that have been already passed by central banks will continue to work its way through the system, increasing risks to global financial stability.

different story in 2023, with consumers staring at empty wallets.

Cracks were always going to appear after the ferocity of rate hikes in 2022-23.

Find out about

Pendal’s Income and Fixed Interest funds

The tightening of financial conditions led to the March madness that claimed the scalp of three regional banks in the United States and a 176-year Swiss bank. RIP Credit Suisse July 5 1856 – March 19, 2023.

Those events were a stark reminder that tightening conditions will have an impact on risky assets.

The RBA’s recent Financial Stability Review highlighted that knowing what assets you own is incredibly important, especially in light of the Silicon Valley Bank collapse.

Just like doing a regular health check and making sure your insurance is up to date.

What it means for investors

Having a defensive allocation in a balanced portfolio insures against adverse market outcomes.

Among safe-haven assets, we favour Australian government bonds and very high-quality credit from well-capitalised Australian issuers, due to the strength of the Australian financial system.

Why?

Australia is one of the strongest AAA-rated sovereigns in the world.

Australia has a pathway to surplus that most developed nations can only hope for.

That’s anchored by the Budget outcome to January 2023, which was $13.6 billion better than expected, driven mainly by $8.5 billion of upside revenue surprise and $5.1 billion less spending than expected.

Australian banks are the best capitalised major institutions in the world allowing them to be the pillars of support for the Australian economy.

Hence, in Pendal’s income and fixed interest portfolios, we favour high-quality Australian assets likely to provide investors with a stable income and protection from the uncertainty ahead.

About Anna Hong and Pendal’s Income and Fixed Interest team

Anna Hong is an assistant portfolio manager with Pendal’s Income and Fixed Interest team.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia.

With the goal of building the most defensive line of funds in Australia, the team oversees some $20 billion invested across income, composite, pure alpha, global and Australian government strategies.

Find out more about Pendal’s fixed interest strategies here

About Pendal Group

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Here are the main factors driving the ASX this week according to our head of equities Crispin Murray. Reported by portfolio specialist Chris Adams.

THE market continues to grapple with the implications of stress in the US banking system.

There are two questions.

One is the extent to which this is a genuine crisis versus a more manageable, short-term shock.

The other is the degree to which credit growth will slow as an exodus of deposits constrains the ability of banks to lend.

At this point the market is swinging to the more benign view that credit tightening will shave somewhere in the vicinity of 0.5% off GDP growth.

This implies a lower peak in rates than expected before the Silicon Valley Bank collapse. But it also means the pace of subsequent cuts may not be as sharp as some have been looking for recently.

The market is pricing in an 80 per cent probability of one last hike in May — and then for rates to fall around 60bp through to year end.

The S&P 500 has rallied about 7% since its March 13 low after the Silicon Valley Bank collapse.

It has been trading in a range of 3600 to 4300 for almost a year.

The recent rally in the face of a financial shock has been driven by the prospect of US rates peaking, inflation softening and the economy remaining resilient, all combined with bearish positioning.

The market valuation discount rate effect from the prospect for lower rates has outweighed the negative impact from the financial sector.

This was bolstered last week by receding fears of a bank-induced credit shock, retail sales holding up better than expected, bank deposit outflows settling down and a better-than-expected start to US bank results.

The S&P 500 returned +0.82% for the week and US ten-year Treasury yields rose 21bps to 3.52%. The S&P/ASX 300 gained 2%.

There are two schools of thought for the economy and markets:

- The successful soft landing — potentially with a mild recession

- A sharper economic downturn, driven by a shock to the banking system or the need for rates to be held higher for longer as inflation remains sticky, leading to a more significant decline in corporate earnings.

The first scenario keeps the market at current levels with perhaps some upside to valuation rating.

The latter sees the market returning towards lows.

In the near-term, markets could remain benign as we enjoy a phase where inflation continues to ease while the economy holds up.

We also have the benefit of a reasonable liquidity environment. In this environment volatility stays muted and market focuses more on stock specifics.

Our view is that the risk increases as we approach the debt ceiling negotiations in July and August, which could coincide with emerging signs of the economy weakening more meaningfully.

Given this, we continue to balance the portfolio in terms of skew between cyclicals and defensives and focus on stocks with less exogenous risk and greater control over their outcomes.

US policy and economics

It’s worth reflecting on the contrasting views on some key questions facing markets:

1) How will the banking crisis affect growth?

Annual deposit growth in the US has very rarely been negative — as it is now. The scale of the decline is by far the largest on record.

Declining deposits constrict a bank’s ability to lend. The market is concerned about how large this impact will be.

This remains to be seen. But there are reasons why this financial shock may not be as bad as people fear.

These include:

- We’re already in a cautious lending environment, so the change in credit availability may be more limited.

- The funding issue mainly affects small and regional banks. While they are important providers of credit, this limits the scale of the issue, since bigger banks are less affected.

- Alternate sources of capital are increasingly available, such as private credit where substantial capital remains to be deployed.

- Bank balance sheets are far more secure since the GFC, therefore they are less vulnerable to shock.

The minutes from the last Federal Open Market Committee meeting released last week suggest the Fed staff were more fearful of a significant credit shock than the FOMC members.

Interestingly, more recent submissions indicate initial fear is dissipating, emphasising the dynamic nature of this issue. Friday’s US bank results were also supportive for sentiment around banking.

JPM and Citi both beat earnings expectations materially, driven by better-than-expected margins.

JPM’s CEO Jamie Dimon chose to be more constructive on the banking shock, noting it involved far fewer players and required fewer issues to be resolved.

This week we will see the Senior Loan Officers Opinion Survey (SLOOS) on credit conditions, which will be an important signal for the Fed.

2) How fast is inflation falling?

There are clearly more signs that the lead indicators of inflation are easing.

US import prices excluding food and fuel dropped 0.5% month-on-month in March and are running at -1.6% annualised, versus a peak of about 7% in 2022.

The Producer Price Index (PPI) readings are also slowing. The US Core PPI is running at 3.4% annualised in March, down from above 9% in 2022.

Historically, PPI measures have been a decent lead on broader inflation.

This is a constructive trend. But on the other hand, Fed officials continue to highlight the issue of tight labour markets and persistent inflation.

FOMC members Christopher Waller and Raphael Bostic emphasised this on Friday.

Waller noted core inflation had only moved sideways since the end of 2021 and said there was much work to be done.

This was reinforced by the latest Atlanta Fed wage tracker data, which did not support the recent average hourly earnings drop in wage growth.

3) The risk of recession

A high proportion of US economists are now expecting a recession, according to surveys.

It should be noted that the Fed themselves are now forecasting a mild recession.

The signals supporting this view are more ambiguous. Consumer spending is slowing but not more than anticipated by the market.

“Real-time” indicators of credit and debit card spending from Bank of America show spending is now flat year-on-year. The mix breakdown shows retail spend is deteriorating, while services growth may have peaked.

Last week’s revisions to jobless claims data revealed a more material rise in claims, which is more consistent with signals on job losses.

Adviser Sam is invested

in making our world

A better place.

Watch as Sam meets a

mum rebuilding her life

thanks to responsible

investing

History suggests that once claims pick up they can break materially higher very sharply.

The counter to this is that real-time indicators of layoffs remain at normal levels, including notices to employees.

We are also seeing labour supply beginning to return, which should enable wages to slow without a significant rise in unemployment.

China

Sentiment improved last week, which was reflected in mining stocks performing well.

This was driven by lower inflation numbers and strong credit data.

This suggests the economy is seeing early signs of picking up post-winter, with improvements in the housing market and consumer spending.

Inflation is being held in check by production growth also ramping up along with consumer demand.

Markets

As concerns over the banking shock mellow, the implied Fed funds rate has crept higher.

However, it still suggests 60bps in cuts by the end of the year, which indicates caution over the economic outlook.

This is also reflected in consensus expectations for earnings as we go into US first-quarter 2023 reporting season. The market is expecting 7% annual decline in earnings in Q1 and 6% declines in Q2.

This is conservative and may have the potential to surprise on the upside.

The bigger issue is the expected recovery. The market has 9% annualised earnings growth in Q4 and 14% in Q1 2024. This seems inconsistent with the economic outlook.

Bears suggest that when earnings start to roll over, they can then plunge suddenly as companies throw in the towel and start to cut costs.

But it’s important to note that while this may have been the case in 2008 and 2020, you can also get extended periods of stagnant earnings, such as in 2014-15.

Australia

The S&P/ASX 300 has lagged the US in 2023, reflecting less skew to tech and the issues with banks.

Last week we saw some catch-up, mainly driven by resources after positive signals on China and less fear around US growth.

Banks lagged the market but did begin to see some price stability return.

Heading into bank reporting season, the key issue will be competition in mortgages where back-book re-pricing may be accelerating and the cost of deposits increasing.

About Crispin Murray and Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia. Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions.

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

Here are the main factors driving the ASX this week according to portfolio manager PETE DAVIDSON. Reported by portfolio specialist Chris Adams

Banking sector concerns are receding and there is now greater confidence on the US interest rate outlook.

This has helped support equities.

The S&P/ASX 300 gained 3.2% last week. The S&P 500 was up 3.5% and the NASDAQ 3.4%.

We also seeing some merger and acquisition activity, notably in the small-cap resource sector.

A sense that rates may be near their peak — and growth is slowing — could support further corporate activity.

US banking

The Fed’s weekly balance sheet data showed a decline of about $US28 billion last week, compared to an expansion of about $US94 billion the week before.

This suggests bank liquidity requirements have decreased, and pressure from deposit outflows may have eased.

At the height of the banking crisis, withdrawals from the Fed’s discount window reached GFC levels.

Last week’s withdrawal remains large in absolute terms. But the market is interpreting the fact that they have rolled over and are declining as a sign the banking crisis has peaked.

Inflows into US money market funds have also decelerated,

After spiking to about $US120 billion in each of the prior two weeks, last week saw about $US66 billion inflows.

Midcaps on

the move

Hear from lithium industry pioneer

Ken Brinsden and Pendal’s

Brenton Saunders

On-demand webinar

Concerns about deposit safety at smaller banks also appear to have eased.

Data shows the banking system as a whole is losing deposits. But last week’s outflows came from large and international banks, while small banks held steady and saw a marginal increase in deposits.

Right now small bank credit growth remains strong at around 8% per annum. Commercial real estate (CRE) loans remain a concern and an area to watch.

Small, regional banks dominate CRE lending. Weakness in office assets could be a potential risk, since physical occupancy in US office markets remains low as a result of work-from-home.

But underneath all this, US and European banks are well-regulated and capitalised and the response from policy makers so far has been decisive.

Corporate credit

Corporate credit spreads widened in response to the banking crisis, but have now started narrowing again. This reflects improved confidence in US banks.

Australia’s corporate bond market was effectively closed to new issuance and secondary liquidity for two weeks due to concerns about the overseas banking sector.

But swift action by policy makers seems to have restored confidence and the local corporate bond market has re-opened.

Last week ANZ issued a large three-and-five-year deal.

Toyota Australia issued $625 million of debt. Volkswagen Australia and Worley (WOR) are also looking to issue new bonds.

Secondary market liquidity has been somewhat challenged, but is improving by the day.

US macro data

Last week was largely uneventful on the data front.

The Fed’s preferred measure of inflation — the Core Personal Consumption Expenditure (PCE) index — came in at +0.3% month-on-month for February versus +0.4% expected and +0.6% in January.

A +0.3% monthly rate annualised is just a touch below 4%, which is probably not low enough for the Fed to feel comfortable in pausing rates.

Find out about

Pendal Focus

Australian Share Fund

Crispin Murray,

Head of Equities

But it indicates inflation is moving in the right direction.

As of March 23, the market was implying a peak in rates of 4.9% in May 2023, with rates at 4.1% by the end of 2023.

This is down from a March 8 reading of a 5.7% peak in September and 5.5% at year-end.

Markets

The S&P/ASX 300 end up 3.3% for the first quarter of 2023, courtesy of a rebound in the last week.

The S&P 500 was up 7.5% and the NASDAQ 17.1% for the quarter.

Bond yields rose as confidence improved last week, with US two-year yields up 26bps. They end the quarter 40bps lower, while 10-year Treasuries are 41bps lower than they started, at 3.47%.

The Safeguard Mechanism legislation was passed last week, requiring most facilities directly producing more than 100,000 tonnes of annual CO2-equivalent emissions to reduce their pollution significantly by 2030.

This poses a challenge for the mining sector, given its heavy reliance on diesel and the potential for higher costs.

Last week resource companies led the market, on the back on stronger commodity prices and M&A activity. The lithium sector rebounded sharply following US giant Albemarle’s all-cash $A5.5 billion bid for local lithium miner Liontown (LTR, +73.2%).

About Pete Davidson and Pendal Focus Australian Share Fund

Pete is Pendal’s head of listed property and a portfolio manager in our Aussie equities team. For more than 35 years, he has held financial markets roles spanning portfolio management, advisory and treasury markets.

Pendal Focus Australian Share Fund is Crispin Murray’s . Find out more about Pendal Focus Australian Share Fund here.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

This year Australian investors should be aware of government influence in four areas, says Pendal’s head of equities, Crispin Murray.

- Government policy poses risks for investors

- Wages, banks, energy, climate

- Find out about Pendal Focus Australian Share fund

- Watch Crispin’s latest Beyond The Numbers webinar

A GROWING trend toward government policy intervention in business is becoming an issue for investors, says Pendal’s head of equities, Crispin Murray.

Murray was speaking at his biannual Beyond The Numbers webinar.

“As investors our focus is on the practical reality of market environment we are operating in,” he says.

“One key shift we have seen is the number of companies referencing the growing influence of government policy on their outlook.”

Investors should be aware of government influence over the companies in their portfolios from four perspectives:

- Determining award wages

- Industrial policy, including regulating the big banks

- Power and gas policy

- The carbon reduction pathway

Below, Crispin goes into detail:

Award wages

Higher wages will impact the profitability of companies with a high share of domestic labour costs like the supermarkets and there are signs the government will push for a real wage increase.

A decision on the minimum wage and award wages is due mid-year, in a process that is normally tied to inflation in the March quarter.

“Will the government push for real wages to be protected? Which could lead to wage increases of 6 or 7-plus plus percent?” says Murray.

Midcaps on

the move

Hear from lithium industry pioneer

Ken Brinsden and Pendal’s

Brenton Saunders

On-demand webinar

“The challenge is that maybe inflation is set to fall over the course of this year and may head back towards 4 or 5 per cent — and so perhaps a 5 to 6 per cent wage increases is more appropriate.

“This is a battle that will need to be determined.”

Industrial policy

Industrial policy is also an emerging risk for investors.

“Our recent meetings with the banks had a very different tone,” says Murray.

“The banks have moved from being reasonably relaxed about the fact that rising interest rates were going to help support their margins.

“Now, they’re much more concerned about the backlash that this is creating in the community and from government.

“What we’re seeing, I believe, is anticipation of potential intervention by the government.”

Early intervention in the banks’ interest rate settings is already occurring, he says.

The Australian Competition and Consumer Commission is investigating how banks set interest rates for savers and some banks have already lifted savings rates to head off the inquiry.

“We also may see potentially an increase in the bank levy”, which is a quarterly tax on the largest banks calculated as 0.015 per cent of liabilities.

“The signal that sends to other companies is [to be] very mindful about using their pricing power.

“The government is saying ‘inflation is an issue — real wages have gone down — the corporate sector should absorb some of these inflationary pressures themselves.

“‘And if you’re not prepared to do it, we might find a way of intervening to make you do it’.”

Power and gas policy

Electricity and gas policy is also an area of intervention for the federal government.

“Clearly there’s been issues with policy in Australia for many, many years.

“But right now, we’ve got a real challenge — like it or not, we’re going to need gas for the next 10 years to help firm renewables.

“That is the lesson that the rest of the world has learned as a result of the Ukraine invasion.”

Australia is beginning to wake up to the fact that if there is no reliable domestic gas supply at a reasonable price, power prices have to go up, he says.

But the government’s attempt to cap gas prices is just leading to a breakdown in the marketplace: “There are no contracts being signed. And as a result of that, no one’s going to look to develop gas.

“This is again a key issue for companies in that sector.

“We’re hopeful that perhaps a little shifting of positions can occur that will solve this problem.

“If it doesn’t, then power costs will be going up, and it will hit households and it will hit corporate profits.”

Carbon reduction

The carbon reduction pathway and the safeguard mechanism is another area of government influence on business.

The safeguard mechanism requires companies that emit more than a certain amount of greenhouse gases to reduce their emissions each year or face financial penalties.

Export exposed companies get favourable treatment to ensure they are not put at a competitive disadvantage.

(Pendal’s ESG credit analyst Murray Ackman explains more here.)

“It is still in consultation phase. The government is seeking feedback.

“But as it stands today, what we’re hearing is certain companies are saying ‘we’re not going to qualify for being export-exposed’.

“For example, steel — because of the way it’s been measured — is not being considered export sensitive.

“Which means for those companies, they’re going to have to be reducing the carbon emissions between 4% and 5% a year through to 2030.

“Their current plans are maybe around 1%.”

The challenge is that the technology to solve for that kind of accelerated reduction pathway does not exist anywhere in the world, says Murray.

“That may mean that they start having to think about not investing in their businesses,” he says.

“We need to be very clear on that and make sure that we’re not caught out by that in our investments.”

About Crispin Murray and Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia. Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions.

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

Here are the main factors driving the ASX this week according to portfolio manager Jim Taylor. Reported by portfolio specialist Chris Adams

THE US Fed has discovered that when you push harder and faster than ever before, it’s likely something will break.

It’s taken time, but the market has found the weakest link in the form of shortfalls in bank asset-liability matching.

Bank asset-liability matching is when a bank ensures it has enough money to cover its obligations by balancing its assets and liabilities.

The likelihood of a full-blown banking crisis is relatively low, given better capitalisation of the US banks and relatively low loan-to-value ratios of US mortgages.

A “Goldilocks” scenario is also possible, where growth slows due to credit tightening as a result of pressure on banks – meaning rates don’t need to go to 6%.

But the full implications of this issue are yet to be seen, and the market last week was looking for guidance from treasury secretary Janet Yellen.

Her mixed messaging prompted some sharp market reactions.

The Fed raised rates by 25bps, largely in line with expectations (which ranged from 50bps to no hike at all).

Midcaps on

the move

Hear from lithium industry pioneer

Ken Brinsden and Pendal’s

Brenton Saunders

On-demand webinar

Fed chair Jay Powell signalled that peak rates were close, but he maintained the mantra of “higher for longer”. The market says otherwise, with rate cuts baked into implied pricing for the back end of 2023.

Overall equity markets have performed reasonably well over the past couple of weeks, given what has been thrown at them. The bears would certainly be feeling quite short-changed.

The S&P/ASX 300 was off 0.58% last week and is down 3.36% for the month to date. The S&P 500 gained 1.41% for the week and is up 0.16% for the month.

Notwithstanding all the postulating over the course of the week, we have three open questions on the US banking issue:

- The outcome for First Republic Bank

- The FDIC’s sale of Silicon Valley Bank

- Congressional action on deposit insurance

US banking

After delivering a 25bp hike in rates, Powell acknowledged that “recent developments are likely to result in tighter credit conditions for households and businesses and to weigh on economic activity, hiring, and inflation. The extent of these effects is uncertain.”

As a result, it was too soon to determine the effects and how monetary policy should respond.

He noted that the rate-setting Federal Open Market Committee (FOMC) had considered a pause. But the hike was supported by a “strong consensus” with a change in guidance around additional hikes.

The “dot plots” graph which outlines future expectations continues to suggest higher for longer.

When quizzed on the market’s implied 125bps of rate cuts due to the banking issues, Powell said the Fed didn’t see rate cuts this year. (Though this was based on how the Fed now sees the economy evolving).

There was greater focus on Secretary Yellen’s comments.

On Monday she said US regulators might act to protect bank depositors if smaller lenders were threatened.

The government was ” resolutely committed” to mitigating financial stability risks where necessary. But she did not address the issue of whether Federal Deposit Insurance Corporation (FDIC) coverage could be expanded to cover all deposits.

Find out about

Pendal Horizon Sustainable Australian Share Fund

On Wednesday, Yellen said she had “not considered or discussed anything having to do with blanket insurance or guarantees of all deposits” in response to a question on whether Treasury would circumvent Congress and insure all deposits.

The market took exception to this and on Thursday Yellen walked this back, saying:

“We have used important tools to act quickly to prevent contagion. And they are tools we could use again. The strong actions we have taken ensure that Americans’ deposits are safe. Certainly, we would be prepared to take additional actions if warranted.”

Meanwhile the Fed’s balance sheet continued expanding (though at a slower rate than the previous week), as banks move to shore up funding.

The total balance sheet grew US$94 billion, on top of US$300 billion the previous week. This included (among other items):

- $37 billion in guaranteed lending to the FDIC (vs +$143 billion the previous week)

- $42 billion drawn from the new Bank Term Funding Program (vs +$12 billion)

- $43bn decrease in discount window borrowing (vs +$148 billion)

Breaking down growth by the 12 Federal Reserve banks is instructive.

Growth in Fed assets is concentrated in the New York and San Francisco regions, which are up US$35 billion and US$24 billion for the week, respectively. There were modest increases across most other banks. But the continued concentration in just two districts gives the market some comfort around the risk of wider contagion.

There is still a clear and significant shift in deposits from smaller to bigger banks.

There is also a reduction of about US$100 billion in net deposits, which is feeding into some US$120 billion of flows last week into money market funds, on top of a similarly strong week before.

US interest rates

The FOMC statement and press conference suggest the Fed now sees risks to the economic outlook as more balanced than earlier in the month.

Find out about

Pendal Focus

Australian Share Fund

Crispin Murray,

Head of Equities

Banking sector stress adds downside risks to growth, employment and inflation.

But despite already tightening conditions, recent data shows inflation has not yet cooled sufficiently to be consistent with Fed targets.

The real interest rate (nominal rates minus inflation) is now near 0.9%, which is nearing the 1% that Powell previously indicated was “restrictive territory”.

The Fed is navigating a fine line by raising rates 25bps (versus the 50bps some were expecting prior to Silicon Valley Bank’s collapse) and keeping the terminal rate consistent at 5.1%.

It recognises that inflation remains too high, but also accepts the economic outcome from the current banking crisis has a long way to unfold, with obvious risks to the downside.

Prior to the Fed’s meeting, markets were pricing an 82% chance of a 25bps hike – with cuts starting in November.

During Powell’s post-announcement press conference, the probability of a June cut increased from 55% to 80%.

US macro data

Existing US home sales surged 14.5% in February, the most since mid-2020.

The median selling price of a pre-owned home fell 0.2% from a year earlier.

The jump in February sales follows 12 straight months of decline, but still leaves monthly sales 27.8% below the peak in January 2022.

The rate on a new 30-year conventional mortgage was 6.18% at the start of February – nearly 100bp lower than the recent peak in October. But it’s since risen sharply to 6.71% last week.

Mortgage payments for a new purchaser of a median-priced existing single-family home was equal to 51% of disposable income in February.

That’s down from the recent peak of 55% in October, but significantly above the 30% to 35% before Covid.

Rates are likely to remain elevated for some time, so a meaningful improvement in affordability will need to come via a decline in home prices.

Layoffs continue to grow without any reflection in unemployment claims. This probably reflects generous severance packages and ease of regaining alternate employment.

Australian macro

Growth in advertised rents in Australia has significantly outstripped growth in the CPI measure of rents for all rental housing since the onset of the pandemic in 2020.

So, unlike in the US where leading indicators are improving, there seems to be no relief coming domestically in the rent component of CPI.

European macro

The Bank of England pushed ahead with another rate hike, increasing by 25 bps to 4.25% – the highest since 2008.

The central bank believes UK living standards will remain flat this year and left the door open to further increases.

Further details were hammered out for the Swiss government’s solution to the Credit Suisse issue.

European Central Bank president Christine Lagarde ensured there was no ambiguity in her message regarding impact from the Credit Suisse crisis on policy.

“In such an environment, our ultimate goal is clear. We must – and we will – bring down inflation to our medium-term target in a timely manner,” she said.

In this regard, she has been helped by the fact that EU gas prices continue to fall and are down 45% this year.

Markets

Bonds yields fell in the aftermath of the Fed meeting.

The two-year and 10-year curve has steepened, with short-term yields falling more than long. But the cash rate/10-year curve has become even more inverted.

In US equities, large-cap technology and defensives have outperformed, while leveraged exposures like banks and property trusts have underperformed.

The US dollar has weakened. Commodity sector performance has been rather mixed.

The S&P/ASX 300 saw reasonable performance over the week. There was an expected weakness in REITs and financials while gold companies performed well.

There was limited company news.

About Jim Taylor and Pendal Focus Australian Share Fund

Drawing on more than 25 years of experience investing in top-performing Australian companies and a background in accounting, Jim manages our Long/Short Fund and co-manages our Imputation Fund. He is a Chartered Accountant with membership of the Australian Institute of Chartered Accountants.

Pendal Focus Australian Share Fund is managed by Crispin Murray. The fund has beaten its benchmark in 14 years of its 18-year history (after fees), across a range of market conditions. Find out more about Pendal Focus Australian Share Fund here.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

The Fed has finally signalled it’s ready to pause rate hikes. Meanwhile we’re all watching for the next signs of stress after almost 5% in a year, says Pendal’s head of government bond strategies TIM HEXT

IT’S now been a year since the US Federal Reserve started hiking rates.

Since then the pace has been relentless, with a total of 4.75% of hikes in nine meetings.

At every opportunity, the Fed’s message has been “more are coming” and “rates need to be higher to contain inflation”.

Finally, the Fed today gave some hope the end of hikes is getting close, leaving the door open to a pause shortly.

As expected, the Fed today hiked 25 basis points to a target range of 4.75% to 5%.

The accompanying statement also featured a softening of language.

Future hikes no longer “will” be needed but now “may be appropriate”. Finally, the door is ajar for a pause.

The rest of the statement contained the usual language around a strong commitment to returning inflation to the 2% objective.

The “dot plot” – which shows where the 11 members of the rate-setting Federal Open Market Committee think rates are going – suggests one more hike this year, peaking at 5.125%.

The consensus is 4.4% for the end of next year and 3.25% at the end of 2025. Neutral is viewed as 2.4%.

Find out about

Pendal’s Income and Fixed Interest funds

Economic projection revisions were small. GDP was lowered slightly to 0.4% for this year despite a strong Q1.

No wonder recession risks and concerns remain high.

Response to banking wobbles

Chair Jay Powell’s press conference contained some interesting insights.

Despite maintaining a brave face, it seems this month’s banking wobbles did rattle the Fed.

We learned a pause was on the table for this meeting amid potentially tighter credit conditions.

The European Central Bank’s logic in hiking 50 basis points last week – that to resist would suggest lack of confidence in the banking system – was not at play here.

Market response

Bond markets rallied modestly on the FOMC statement but were given a decent boost by Powell’s comments.

US 10-year yields are back below 3.5% and near the lows from last week’s turmoil, despite the banking crisis having passed (for now).

Markets are now well ahead of the Fed, pricing in almost 1% of cuts by year end.

US two-years are sub 4%, indicating rates nearer 3% than 5% next year.

What’s next?

We are now all on “break watch”.

Where will we see the next signs of stress after almost 5% of hikes in a year?

The field is wide open. Commercial property, private equity and the non-bank financial sector are a few of the areas that thrived in the zero-rate environment.

A largely fixed-rate loan market in the US has dampened the impact of the hikes so far – but that will end.

Equities have largely taken it all in their stride. Stresses may be offset by lower rates, meaning it may be a case of picking the sector winners and losers more than the overall market direction.

About Tim Hext and Pendal’s Income & Fixed Interest boutique

Tim Hext is a Pendal portfolio manager and head of government bond strategies in our Income and Fixed Interest team.

Tim has extensive experience in banking, financial markets and funding including senior positions with NSW Treasury Corporation (TCorp), Westpac Treasury, Commonwealth Bank of Australia, Deutsche Bank, Bain & Co and Swiss Bank Corporation.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia.

Find out more about Pendal’s fixed interest strategies here

About Pendal

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

In 2023, Pendal became part of Perpetual Limited (ASX:PPT), bringing together two of Australia’s most respected active asset management brands to create a global leader in multi-boutique asset management with autonomous, world-class investment capabilities and a growing leadership position in ESG.

Here are the main factors driving the ASX this week according to our head of equities Crispin Murray. Reported by portfolio specialist Chris Adams.

NEWS headlines are full of bank runs and bailouts, emergency weekend policy-maker meetings and record declines in short-end yields.

These are signs of the system stress that often accompanies periods of financial tightening.

Last week this was reflected in dramatically lower bond yields as US two-year government bond yields fell 75bps. Brent crude oil was off 11.9% and gold gained 5.8%.

The S&P 500 gained 1.4%, while Australia (S&P/ASX 300 -2.8%) and European equities (EuroSTOXX 50 -3.8%) lost ground.

The common thread was a market view that financial shocks would trigger a recession, requiring central banks to reverse course quickly.

Concerns over economic growth and an expectation of lower rates saw a rotation away from resources and cyclicals to growth and bond sensitives.

The consequences for financial markets are too early to call.

Policy makers face a complex challenge of balancing the apparently conflicting objectives of preserving financial stability and fighting inflation.

The impact on equities will be determined by the ability of policy makers to contain risk and the flow-on effects on rates and economic growth.

Potential scenarios

Potential outcomes range between two poles:

- Moderate additional financial tightening, which helps reverse the economy’s stronger momentum this year. This scenario could see economic growth fall by 25bps to 50bps and take out a rate hike without derailing the soft-landing story. Equities therefore hold up in current trading range.

- A substantial credit crunch as capital flees smaller banks, removing liquidity for small businesses and commercial real estate. This could trigger a significant recession, affecting earnings and forcing central banks to dramatically cut rates. Under this scenario equities make new lows, though we would likely see a rotation to growth.

It is natural to compare this situation with the Global Financial Crisis, but there are significant points of difference, which suggest far less risk for markets.

Bank capital ratios and liquidity buffers are far greater than they were in the GFC.

Banks generally are profitable and have scaled back their more volatile business streams.

Policy makers have the available tools and playbooks to respond and there is far better transparency over the interconnected exposures of financial institutions.

There will be companies with weak or more vulnerable franchises. We are likely to see more of these flushed out in coming weeks.

But that does not equate to a systemic crisis.

The key for markets is whether the policy response can restore confidence beyond just patching up funding in the short term, as has so far been the case.

Two key issues

There are two separate financial issues, occurring simultaneously: 1) Credit Suisse and Europe and 2) US banking issues

1. Credit Suisse and Europe

In Europe, pressure on Credit Suisse culminated in a takeover by rival UBS in a government—brokered deal at the weekend.

Credit Suisse had pre—existing issues. It was undergoing a turnaround plan established late last year alongside a capital raising.

There were continuing outflows from the private bank and asset management business. Clients were losing confidence and shifting assets to other groups or into government bonds.

This reduced profitability, crimping Credit Suisse’s ability to wear losses likely to come from running down the troubled investment bank (which was the source of its issues).

The question is now whether the takeover deal restores confidence or whether we begin to see concerns over UBS.

It’s worth noting that UBS is far more profitable and has a much smaller investment bank.

It is important to note that this is not currently being viewed as a broader European banking crisis.

Capital and liquidity requirements are far stronger than they were in the GFC.

After years of restructuring, banks are less exposed to financial market volatility and are more profitable.

There is an estimated EUR400 billion equity buffer in the system compared to requirements.

As a result, credit default swap (CDS) spreads for big global banks have not surged in tandem with Credit Suisse’s.

At this point we don’t expect the Credit Suisse issue to trigger a systemic problem in Europe, leading to a recession.

This could change, but it would require a significant policy failing.

2. US banking issues

The second issue is in the US and has potentially more structural implications.

The issue is a fundamental weakness in the US banking system relating to a high reliance on uninsured deposits for funding and a lower level of regulation on sub-$250 billion balance sheet banks.

The US banking system is highly fragmented.

The biggest banks — those with more than $100 billion in assets — account for about half the asset base.

Then there are about 100 regional banks with $10 billion to $100 billion in assets and some 3500 community banks with less than $10 billion.

The issue is that smaller banks are not heavily regulated. Just over half of all US deposits are insured under a Federal Deposits Insurance Corporation (FDIC) scheme that promises to cover up to $250,000 of a depositor’s funds.

The fundamental problem is that corporate treasurers and high net worth individuals who are “uninsured” are now being far more careful with who they leave their money.

As a result, we have seen substantial deposit runs, with withdrawals continuing even after the FDIC announced that all deposits would be protected.

This is evident in money market funds which saw US$116 billion in inflows this week. It was the fifth-biggest week on record (dating back to 1992).

It can also be seen in use of the Fed discount window, which is the way the Fed provides a liquidity backstop to the financial system.

Last week banks borrowed $153 billion — an all—time record. The week before it was $4.6 billion.

This reflects depositors withdrawing funds and banks needing to seek alternative funding.

The Fed has announced emergency funding to backstop depositors at Silicon Valley Bank and Signature Bank and the creation of a Bank Term Funding Program (BTFP).

This shouldn’t be seen as quantitative easing. It isn’t creating new money and technically it’s lending — not buying.

It should help stabilise markets, but illustrates that the Fed balance sheet is proving hard to shrink.

Treasury secretary Janet Yellen has tried to calm concerns by drawing on provisions that enable the Fed to act in the face of a systemic financial crisis and by insuring SVB and Signature depositors.

This requires a super majority of the FDIC, Federal Reserve, the Treasury Secretary and the President to agree.

This is clearly meant to represent an implicit guarantee on all depositors in banks with more than $120 billion on their balance sheet.

The challenge is they do not have the authority to make that an explicit guarantee. This can only come from Congress.

Adviser Sam is invested

in making our world

A better place.

Watch as Sam meets a

mum rebuilding her life

thanks to responsible

investing

That is unlikely to happen any time soon. It would probably come with new rules on regulation and be a complex process to legislate.

The problem is no one knows how far potential support from policy makers would extend.

Yellen got tied up in knots in congressional testimony while explaining why depositors in community banks should not move their money to big banks.

The pressure on these smaller banks is likely to prevail, which leads them to draw on the discount window and the new Fed facility which uses par value (not market value) in assessing collateral.

This is not a sustainable solution.

The next bank in the firing line is First Republic which received a $30 billion deposit influx from the largest US banks, which were effectively recycling the deposits they were receiving as First Republic’s customers were leaving.

This is an effort to demonstrate that they believe the deposit guarantee is there.

At this point we are waiting to see which form the solution takes.

What does this mean for the US?

The key issue here is not so much contagion risk, as the other banks are receiving extra liquidity and there are not large direct credit exposures to these banks.

Instead, it is the transmission mechanism to the broader economy, since smaller banks are major providers of credit.

Banks with less than $250 billion in assets provide around half of total commercial and industrial loans and 80% of commercial real estate lending. Smaller banks also dominate residential lending.

The concern is these funding pressures could trigger a credit crunch on top of existing tighter financial conditions — driving the economy into recession.

A more benign outlook may be that this credit tightening equates to 25-50bps of a slowdown in GDP growth, helping deal with an economy that has been running too hot. In this scenario the flow-on effects might be limited given tight labour markets.

This could mean that one of the expected 25bp rate hikes from the Fed is removed.

A more bearish view seems to be dominating at the moment given the sharp drop in two-year US government bond yields.

This move was greater than that seen in the GFC and around 9/11. It’s seen by many as a warning bell for recession.

The consensus for US rates now implies no more rate hikes and 100bps of cuts by year’s end.

A number of other signals support a more bearish view:

- As measured by the “Move” index, bond market volatility is back to levels not seen since the GFC.

- Historically, the first cut in a rising rate cycle has been a poor near-term indicator for the economy or for equity markets, though the latter generally recovers relatively quickly.

- Once it starts steepening from a point of maximum inversion, the yield curve is often a signal for upcoming recession.

The exception to a number of recessionary signals is the most recent one — where there would not have been a recession if it were not for Covid.

A lot of people are wary of betting against history.

It is worth stepping back and thinking about why these historical relationships apply.

Essentially, it is a function of the Fed raising rates too hard for too long, effectively over-tightening and creating a recession and large earnings drop.

Initial rate cuts are therefore a reflection of the weakness rather than a positive for the market.

This cycle is somewhat unusual as we have an overlay of the pandemic, excess savings, extremely tight labour market and a recovering China.

While a recession is probably more likely than not, it is still a more complex issue than some traditional indicators would suggest.

The other — more bearish — complexity in this cycle is that the Fed still has not dealt with inflation.

Historically, Fed pivots have usually come when inflation was running between 1 and 2% — not above 4% as it is today.

US inflation and the Fed

The latest US CPI data — lost in the noise last week — did not provide relief.

Headline CPI is better at 6% year-on-year as energy declines and three-month annualised is 4%.

But monthly core CPI was firm at +0.45%, underpinned by +0.6% monthly growth — the highest since September 2022.

If you overlay lead indicators on rents, it’s possible to see inflation falling to 4% — but remaining sticky there. That is just not low enough for the Fed to declare victory.

So, this week’s meeting is lineball on a 25bp move. There is a view that deferring a potential hike to May costs very little on the inflation side but could make a big difference on the financial stability side.

For the equity market, the banking issues are bad for financials, but the prospect of fewer rate hikes is good for growth stocks, helping prop up the market last week.

Central banks

The ECB’s expected 50bp rate hike also got lost in the noise.

It was notable that the forward guidance moved from saying rates need to rise significantly higher for an extended period, to now being data dependent.

In China, the PBOC sneaked in an unexpected cut to the bank reserve ratio requirement on Friday as well. This is seen as an important signal towards supporting growth

Finally, in Australia rate expectations have stepped down materially from 4.15% to 3.40% at the end of 2023, implying no more hikes.

Markets

Credit spreads have been widening out, but not yet signalling something more concerning.

There are pockets of stress emerging in some areas, notably commercial mortgage-backed securities (CMBS).

In terms of equities the US, the S&P 500 has held the 3800 support, but still does not look too healthy.

Commodity Trading Advisers — which are used as an indicator of marginal players in equities — have moved quite underweight in US equities, with potentially more to go into quarter end.

The other feature of the market worth noting is the rotation back to growth as expectations have shifted on the risk of recession and the path of rate hikes.

The S&P/ASX 300 underperformed the US due to the fall in resource and energy stocks on global growth concerns.

About Crispin Murray and Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia. Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions.

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

Should we be concerned about the knock-on effects of the Silicon Valley Bank collapse? Pendal’s AMY XIE PATRICK explains

COCKROACH theory refers to the belief that problems affecting one company may indicate similar problems with other similar companies.

After the collapse of California’s Silicon Valley Bank (SVB), the market and the media are on the lookout for more cockroaches.

The good news is that SVB was an unusual cockroach. The bad news is that other creepy crawlies lie in wait.

Two main issues led to SVB’s fall.

The first was an unusual decision not to hedge interest rate exposure or mismatch between its assets (long-dated fixed income instruments) and liabilities (deposits).

Most banks face this mismatch. Few would leave it unhedged.

Bloomberg’s US Treasury index returned -12.3% in 2022. This gives an indication of the mark-to-market damage that would have hit SVB’s long-dated fixed income assets.

The second factor was the concentration risk in its customer base.

The Silicon Valley tech sector formed almost the entirety of the bank’s borrower and depositor base.

Ultra-low interest rates going into and coming out of the pandemic were a huge boon to this sector.

At the time, money was virtually free and poured into high-growth sectors hungry for returns. But by the end of 2022 – after 425 basis points of interest rate hikes – that was no longer the case.

Higher discount rates needed to be applied to potentially speculative future earnings in the sector.

All at once, SVB found its customers calling on their deposits.

The need to satisfy these liquidity demands caused SVB to start realising some of those steep mark-to-market losses in their assets.

SVB is the 16th largest lender in America, but its $200 billion of assets still sat below the $250 billion threshold at which banks need to report unrealised losses.

This helped hide the stress before a classic run on deposits in early March.

Are there more cockroaches?

There could be other lending institutions with similar red flags, but the bank’s problems were largely self-made.

Many regional US banks go under every year.

Most often, it is due to the poor quality of their loan books. Not because of poor risk management.

That is perhaps the most heartening takeaway from the SVB crisis.

Unfortunately, other risks have been uncovered by the bank’s collapse.

Here are the main lessons:

1. Easy money a thing of the past

The first is that easy money is a thing of the past.

The SVB crisis reminds us that the promise-heavy tech sector needs much more diligence now that money-good T-bills pay between 4.5% and 5%.

Similarly, in Australia cash and near-cash investments yield 4% or more.

This naturally pushes up the bar for going further out along the risk curve and down the liquidity ladder.

When money was virtually free, illiquid and opaque investments such as private debt and equity seemed attractive.

Just as had been the case with SVB until now, unrealised losses within these investments have yet to come to light. That flood of money is reversing.

2. Hurdles for mortgage-backed securities

A second risk is highlighted by the mortgage-backed securities (MBS) losses on SVB’s asset portfolio.

Find out about

Pendal’s Income and Fixed Interest funds

Mortgage-backed securities allow investors to own part of a bundle of home loans that have been packaged together.

Interest rates were not the only blame factor here. So was the quality of the underlying assets.

Like clockwork, a global synchronised housing downturn is following the synchronised global rate hiking cycle.

Australian credit portfolios heavily invested in illiquid residential mortgage-backed securities (RMBS) face significant hurdles this year.

The value of RMBS portfolios will be affected by the house price correction we’re already experiencing, as well as payment delays from stressed borrowers.

In addition, the RMBS issued by non-major banks are of poorer quality, leading to more accidents waiting to happen.

As Pendal’s senior credit analyst, Terry Yuan, says: “Set-and-forget credit portfolios often rely on the AAA rating of RMBS to raise the average portfolio rating of their holdings, giving them more room to veer into the low-BBB space.

“Both ends of the ratings spectrum will experience a lack of liquidity should something go wrong”.

That is not what true fixed income is supposed to feel like for the end investor.

3. The information factor

The third risk unveiled by the SVB crisis is that of information. Unlike the GFC, and thanks to technology, rumours can become truths in the space of a few tweets.

Adviser Sam is invested

in making our world

A better place.

Watch as Sam meets a

mum rebuilding her life

thanks to responsible

investing

The reality is that SVB depositors are likely to be made whole. The shame is they could have got there without going through this mess first.