IN AUGUST 2022 we announced plans to bring together Australia’s two leading asset management businesses, Pendal and Perpetual.

We continue to believe this proposal would create Australia’s pre-eminent global asset manager, with clients benefitting from greater scale across customer service, distribution, technology, infrastructure and ESG leadership.

Since then Pendal and Perpetual have been working together constructively to finalise the details of this proposal.

On November 17, Pendal and Perpetual both publicly confirmed in separate ASX statements that the proposed merger is proceeding.

You can read Pendal’s statement here and Perpetual’s statement here.

The proposal remains strongly supported by our fund managers, given Perpetual’s commitment to preserving our culture of investment independence and the autonomy of our investment management teams.

The NSW Supreme Court provided further clarity to enable the two businesses to come together. You can read more here.

On December 23, Pendal shareholders overwhelmingly voted in favour of the proposed acquisition by way of a scheme of arrangement. You can read about the details on our shareholder website.

The scheme remains subject to court approval on January 11.

In the meantime, I want to reiterate that Pendal will continue to manage your investments to the best of our ability, as we have always done.

We look forward to doing so for many years to come.

I warmly thank you for your support and trust. Please do not hesitate to call or contact your Pendal account manager.

Please do not hesitate to call or contact your Pendal account manager.

– Richard Brandweiner

CEO, Pendal Australia

Some investors might be surprised to find countries such as South Korea and Taiwan classed as emerging markets. There’s usually a good reason explains Pendal’s JAMES SYME

- Read more: Why some EM investors may benefit more than others as the tide turns

- Find out about Pendal Global Emerging Markets Opportunities fund

SOUTH Korea is one of the few countries in the world to develop its own supersonic jet fighter.

It’s a stable and mature democracy — and home to some world-leading technology companies.

So some investors might be surprised to find it’s classed as an emerging market, along with Taiwan and wealthy Gulf countries such as Saudi Arabia and the United Arab Emirates.

What is an emerging market? Who decides the definition of emerging equity markets?

It’s an enduring controversy. Some countries at the more advanced end of the emerging markets (EM) spectrum could arguably be classified as developed markets.

It’s useful for investors to understand how countries are classified as emerging markets as opposed to frontier (or pre-emerging markets) and developed markets.

The origin of emerging markets

The term “emerging markets” dates back 40 years.

The International Finance Corporation (an arm of the World Bank) first began tracking stockmarket returns in 10 developing countries such as Argentina, Brazil and India in 1980.

The IFC came up with “emerging markets” as a way of describing these countries after rejecting dated terms such as “third world”.

The IFC based its definition on economic development, as measured by Gross National Product per capita (the annual value of a country’s goods and services divided by its population).

These days the definition used by the largest index provider, MSCI [PDF], is based around economic development, market size, liquidity and accessibility.

Under MSCI’s methodology four wealthy Gulf economies — Saudi Arabia, the United Arab Emirates, Kuwait and Qatar — are emerging markets, as are the highly successful economies of South Korea and Taiwan.

The case for South Korea

The question is often asked: is South Korea really an emerging market?

Events in the Korean domestic bond market since the end of September show why it probably still is.

The full series of events are too long to go into here.

But in short, a newly-elected provincial governor decided — for political rather than economic reasons — to push the local developer of a Legoland Korea theme park into bankruptcy and to renege on a government guarantee of the development company’s bonds.

The effect on domestic bonds was rapid and serious.

New issuance by local government development and housing companies proved impossible through October. Some major borrowers with investment grade credit ratings were unable to place bonds.

The bonds that the development and housing companies issue are called Project Finance Asset-Backed Commercial Paper (PF-ABCP).

They are the main funding source for Korea’s private-sector property developers, who saw their bond yields spike and began scaling back finance for new projects. In what very much looks like contagion, a mid-size life insurer delayed exercising a call option on some of its perpetual bonds.

Find out about

Pendal Global Emerging Markets Opportunities Fund

This was the first time this had happened since the financial crisis in 2009.

Despite the specific cause, this has come at a time of rising global interest rates and bond yields, a stronger US dollar, and a slowing Korean economy.

The conditions were in place for financial stress, but the combination of volatile politics and weak institutions acted as a trigger.

Dramatic move

The overall effect has been a dramatic move in the whole Korean commercial paper market.

Three-month Korean commercial paper typically has yields 0.25-0.5% higher than policy interest rates, but the gap at the end of November had reached 2.3% and still looked to be increasing.

So, despite generally tightening monetary policy through higher interest rates this year, Korean authorities have had to engineer a repurchase program to stabilise the market.

At the time of writing, this was KRW 2.8trn (USD 2.1bn) — but its size and scope have been steadily increased and more may well be required.

Ultimately, the creditworthiness of these instruments has not changed.

This is a shock to confidence — a market panic in the style of the nineteenth century.

The Bank of Korea and the Ministry of Finance are responding in the right way and they have the monetary firepower to settle the market at some point.

But there must be some resulting drag on Korean GDP growth and corporate earnings.

And this is why South Korea remains an emerging market.

Long-term excess returns

The long-term excess returns of emerging market equities over developed market equities compensates investors for the extra risk and volatility of emerging markets.

That risk can come in many forms. But it definitely includes a single provincial politician pushing the local Legoland into default and blowing up the entire domestic commercial paper market.

About Pendal Global Emerging Markets Opportunities Fund

James Syme, Paul Wimborne and Ada Chan are co-managers of Pendal’s Global Emerging Markets Opportunities Fund.

The fund aims to add value through a combination of country allocation and individual stock selection.

The country allocation process is based on analysis of a country’s economic growth, monetary policy, market liquidity, currency, governance/politics and equity market valuation.

The stock selection process focuses on buying quality growth stocks at attractive valuations.

Find out more about Pendal Global Emerging Markets Opportunities Fund here

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Here are the main factors driving the ASX this week according to our head of equities Crispin Murray. Reported by portfolio specialist Chris Adams.

A LOW point in the VIX volatility index last week proved to be the signal for a correction in the recent rally.

There was no specific macro news to prompt this. The weight of buying faded and the market shifted to a cautious position ahead of this week’s Fed meeting.

US ten-year government bond yields rose 9bps and the S&P 500 fell 3.4%.

Brent crude oil fell 11.1% and is now down for the year to date, as the market worries about a downturn in demand.

China’s re-opening appears to be happening faster than expected.

The iron ore price rose 9.6% as a result, and is helping underpin the Australian equity market. The S&P/ASX 300 was down 1% for the week. It has outperformed the S&P 500 by about 17% in 2022.

The RBA hiked rates 25bps, as expected, and struck a more cautious tone on inflation.

We also saw the federal government launch a new energy policy which at first glance looks under-prepared. The policy introduces price controls that would likely make the power problem worse in the future.

There are six big macro issues going into next year:

- The persistence of inflation — and how tight financial conditions will need to be in response

- The scale of economic slowdown in the US and developed markets. (Real-time signals are benign, but the yield curve is a very negative signal)

- The earnings leverage to that downturn — and whether nominal growth buffers earnings

- Whether markets have already priced in economic downturn. The bear view is that markets bottom during recession, not before. Bulls point to a falling oil price, a weaker US dollar and lower bond yields as evidence of lessening headwinds for equities

- What China’s economy does as it exits zero covid

- Whether the RBA can engineer a soft landing in Australia

US inflation outlook

Inflation signals were marginally negative last week.

Adviser Louise is invested

in making our world

A better place.

Louise meets a woman who

turned her life around thanks

to responsible investing

After average hourly earnings surprised on upside — which market founds reasons to dismiss — the Atlanta Fed wage tracker indicated wage growth was staying elevated at 6.5%. (Though the series is believed to overstate by around 1%, relating to career progression effects.)

When measured against the Employment Cost Index, this suggests limited relief on the wage front.

The Producer Purchasing Index was also higher than expected, rising 0.3% month-on-month and 7.4% year-on-year, versus 8.1% in October. Core PPI was +0.3% and 4.9% year-on-year. The trend is still lower.

There is a view that if you hold good inflation flat and factor in the real-time rent inflation number (which is now close to zero), you can make a case for inflation tracking to 3.2%.

The question is whether this is sufficient for the Fed.

Since this number may still drag inflation expectations up, it may be seen as still too high, requiring a weaker economy and tighter monetary policy to bring it below 3%.

The Fed and the economy

The Fed meets this week, with the market clearly primed for a 50bp hike in rates.

There will be a few key issues to watch:

- Whether the Fed signals any further slowing in the trajectory for rates at the next meeting. (This is unlikely given it’s not until the end of January)

- Where the dot plots have moved to in terms of peak rates and duration

- Any messaging on the long-term real rate assumption. (Again, we think this unlikely)

- The tone of the Fed press conference, given Powell’s recent shift from a hawkish to a more benign stance.

The market is now expecting the Fed rate to reduce relatively soon after hitting its peak.

Total financial conditions — a measure of changes in key indicators such as mortgage rates, credit spreads, equity markets and currency moves — have eased considerably since October.

This has reduced the risk of the Fed over-tightening. But it may also result in the Fed thinking they need to do more.

One thing to note is that real US money supply (M2) has plunged from more than 20% a year ago to -7.2% in December. This is its lowest point in more than 50 years.

This is prompting a view in some quarters that policy is already more than tight enough.

The US yield curve is more inverted than at any point in 40 years, providing further fuel for the bears

Job openings are coming down — indicating a cooling labour market — but there remains a fair way to go.

Elsewhere, developed-market ISM manufacturing indices are deteriorating and moving into contractionary territory. This indicates a slowing global economy.

China

Beijing continues to move faster than expected on re-opening, with zero covid effectively dead as a policy from December 7.

The retreat from PCR testing means we won’t see a headline surge in case numbers. The issue will be hidden until it is potentially evident through pressure on the hospital system.

This suggests we are tending towards the “quicker re-opening” or “chaotic re-opening” scenarios.

This may not be good for the economy in the near term if it leads to absenteeism and possible supply disruptions,

Oil

The oil market continues to weaken despite crude inventories continuing to fall.

Inventories of diesel and petrol products built meaningfully last week. Some saw this as a sign that end demand is falling in the US. But it may just reflect a seasonally stronger production period for refineries.

One concern for the oil market is that the time spreads for oil futures in the front months have moved into “contango” (an upward sloping curve, indicating futures contracts are trading at a premium to the spot price). This means trading oil becomes harder and less profitable, which reduces demand.

Adviser Sam is invested

in making our world

A better place.

Watch as Sam meets a

mum rebuilding her life

thanks to responsible

investing

It may also signal weakness in the physical market, indicating softer demand.

We suspect oil will continue to be under pressure in the near term.

But the fundamentals relating to supply should underpin the medium-term outlook — as will demand recovery from China and when the market begins to look through any downturn in developed markets.

Australia’s power intervention

There appears to be two elements to the Albanese government’s new energy policy.

The first is a near-term, stop-gap solution to try to get electricity prices lower. The second is draft legislation providing new powers for regulators and governments in the electricity and gas industry.

The near-term measures involve the government putting in a $12/GJ cap on uncontracted gas. It is unclear whether this is well-head or end-market including transport. There is also a A$125/ T cap on thermal coal, both contracted and uncontracted.

This means coal-fired power generation would break even at $60-65/MWH and gas power at $70/MWH.

The government is also committing to no coal or gas in the “capacity mechanism” — the structure that pays providers to have plants available to produce power when required.

The resulting lack of “firming capacity” — flexible supply to be called on when renewables are not functioning — would almost certainly lead to power cuts in the future.

In an effort to push it through before Christmas, the draft legislation is subject to only three days of consultation.

It involves a long-term price regime where gas is treated as a regulated utility.

Providers would be allowed an undefined “reasonable” price, based off an assessment of a fair return on the investment made.

The major flaw in this approach is that developing gas has a very different risk profile than traditional utility investment. The cost of developing gas projects can be a lot higher than planned. There are substantial operating risks and long-term pay-backs.

This means uncertainty around the pricing environment is likely to deter further investment in gas production and LNG import terminals, leaving Australia strategically short in gas.

The government is indicating it will introduce powers compelling companies to develop gas — effectively forcing private capital to invest against its will.

Unless changed, this demanding proposition could evolve into a battle like that over the mining tax under the Rudd government a decade ago.

From a stock point of view this may jeopardise the takeover offer for Origin (ORG).

It will also put pressure on AGL’s earnings, hampering its investment in the clean-energy transition.

Markets

Resource stocks continued to outperform on the China re-opening theme. Fortescue Metals (FMG, +8.7%) was the best performer in the ASX 100 last week.

All other sectors lost ground and there was a clear defensive tilt. Tech and energy were the worst-performers sectors.

About Crispin Murray and Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia. Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Emerging markets should benefit as sentiment turns on interest rates and the US dollar.

But some investors are better placed than others. Here’s why

- Economic outlook improving for Emerging Markets investors

- Country-level analysis an important factor in identifying opportunities

- Find out about Pendal Global Emerging Markets Opportunities fund

HIGHER US rates and a US dollar have recently curbed Emerging Markets returns, since they tend to depreciate other currencies, weaken US demand and draw capital out of EM economies.

As inflation comes under control, it’s expected that rate rises will decelerate and the US dollar will eventually weaken.

That’s good news for EM investors.

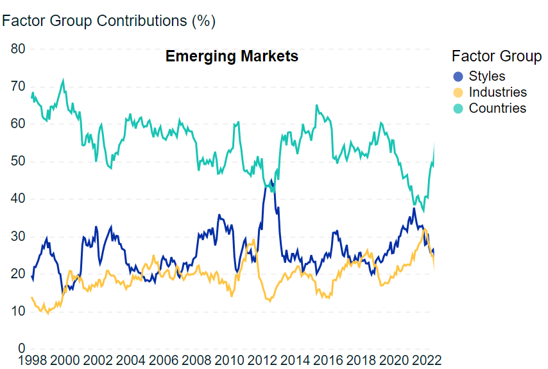

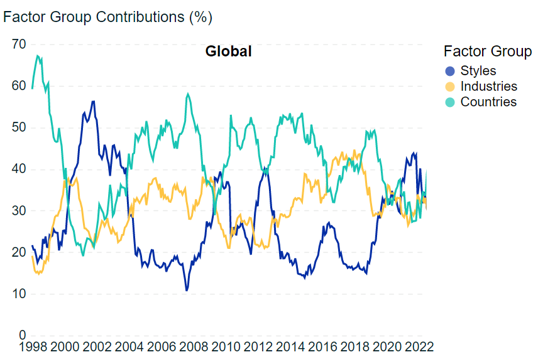

But there is another change that may benefit some emerging markets investors more than others: country-level factors are again becoming a powerful indicator of potential returns.

Investment managers that focus on top-down, country-level analysis should be able to take greater advantage of the changing conditions.

Why?

Country factors typically dominate style and industry factors in driving emerging markets returns.

This contrasts with developed markets which tend to have more features in common.

Emerging markets feature a wider range of political systems, demographic trends, industrial composition, resource endowments and economic development.

That’s where Pendal’s Emerging Markets team starts its analysis.

As you can see from these charts, most of the time it pays off:

But these charts also show that during the Covid period extraordinary monetary policy settings and falling bond yields drove the importance of style and industry factors.

This is reversing now and we are seeing country factors reassert traditional dominance.

This has coincided with a strong relative performance with the Pendal Global Emerging Markets Opportunities fund (GEMO), as you can see below:

| % | 3 Months | 1 Year (pa) | 3 Years (pa) | 5 Years (pa) | Since inception (pa) 01/04/2005 |

|---|---|---|---|---|---|

| Total return (after fees) | 9.71 | 31.55 | 11.37 | 12.41 | 9.80 |

| Benchmark: S&P/ASX 300 Accumulation Index | 8.53 | 28.72 | 10.10 | 10.22 | 7.96 |

| Performance over / (under) benchmark | 1.18 | 2.83 | 1.27 | 2.19 | 1.84 |

Source: Pendal, Pendal Global Emerging Market Opportunities Fund – Wholesale, after fees and before taxes. Past performance is not a reliable indicator of future performance. Inception date Nov 7, 2012.

Performance drivers and positioning

This performance has been driven the fund’s strategy of holding countries that are well suited for a given investment environment — and avoiding those that are not.

The fund currently holds only nine of the 24 countries in the index.

These include countries such as Brazil, Mexico and Indonesia which have bucked the trend of broader emerging market weakness.

All three made positive returns in 2023.

Fund managers James Syme, Paul Wimborne and Ada Chan (pictured below) each draw on more 20 years of experience in emerging market investing,

They see clear signals that these markets are shifting into a virtuous circle of upswings in domestic demand which typically drive multi-year periods of outperformance.

A similar environment drove the last surge in investor demand for Latin America (prior to the GFC).

These economies have taken more than a decade to rebalance and repair.

Now another opportunity emerges.

The fund’s performance has also been helped by the team’s decisions on China.

The fund has been underweight in China as multiple headwinds — including Covid-zero and regulatory pressure on the property sector — weighed on markets.

James, Paul and Ada are keeping a close eye on Beijing, however.

There are signals of a shift in policies that have weighed on the economy and market.

It is too soon to overweight this market. Economic growth, the liquidity and credit environments and the currency outlook all remains negative.

But if policy becomes more supportive this could — in combination with historically cheap valuations — drive an opportunity.

Find out about

Pendal Global Emerging Markets Opportunities Fund

Pendal Global Emerging Markets Opportunities fund’s emphasis on liquidity — and the agility to shift quickly between markets — will be a key factor in taking this opportunity when the time is right.

Emerging Markets outlook

High US rates and a strong US dollar are traditional headwinds to emerging markets as a whole — though as noted above there are countries bucking this trend.

It will take a shift in expectations around the US Fed’s hiking cycle to remove this headwind.

So far Pendal Global Emerging Markets Opportunities fund has been able to preserve capital relative to the benchmark. The fund has returned 0.73% annualised over the last two years, while the market is down 5.88% annualised.

This puts the fund in a relatively good place when the rebound in the asset class comes through.

We expect that, as always, owning the right countries will be important for performance in that period.

This is reinforced by the reestablishment of country factor dominance.

It is also aligned with our country-driven strategy, which has driven long-term outperformance.

About Pendal Global Emerging Markets Opportunities Fund

James Syme, Paul Wimborne and Ada Chan are co-managers of Pendal’s Global Emerging Markets Opportunities Fund.

The fund aims to add value through a combination of country allocation and individual stock selection.

The country allocation process is based on analysis of a country’s economic growth, monetary policy, market liquidity, currency, governance/politics and equity market valuation.

The stock selection process focuses on buying quality growth stocks at attractive valuations.

Find out more about Pendal Global Emerging Markets Opportunities Fund here

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Here are the main factors driving the ASX this week according to our head of equities Crispin Murray. Reported by portfolio specialist Chris Adams.

JEROME Powell struck a more nuanced tone in a speech about US inflation and jobs last week.

The chair of the US Federal Reserve told a Washington DC thinktank that the central bank was mindful of overtightening as well as potential distortions in the CPI calculation.

The market interpreted this as a less prescriptive — and less hawkish — stance on rates than previously feared.

As a result, the S&P 500 gained 1.2% and US 10-year government bond yields fell 19bps. The S&P/ASX 300 was up 0.2%.

This outweighed the negative news of another firm payroll and average hourly earnings print.

There were reminders that the Fed may have to hold rates higher for longer than the market is expecting.

Optimism around China continues to support mining stocks and help underpin a rise in commodity prices.

It would not surprise us to see the market pause in the short term, given a) the equity market is approaching technical resistance levels, b) volatility has fallen to the low point of its range this year and c) key inflation data points are yet to come.

The depth of any economic downturn — and its effect on earnings — is the key swing factor for the medium-term outlook.

An important signal

Powell’s speech to the Brookings thinktank was an important signal.

There was not anything specifically new. He is still flagging a deceleration to 50bp in December and notes that the ultimate peak in rates may be higher than they expected in September.

The importance lay in the speech’s tone — which was far more balanced than his previous hawkish statements.

There were fears he would reprise the Jackson Hole speech, talking down markets after a strong rally.

Adviser Louise is invested

in making our world

A better place.

Louise meets a woman who

turned her life around thanks

to responsible investing

Instead, his speech implied he did not feel the need to drive Total Financial Conditions higher in the near term.

(Total Financial Conditions indices try to pull together changes in key indicators — such as mortgage rates, credit spreads, equity markets and currency moves — as an early indicator of the market impact of stimulus or tightening).

Powell introduced a sense of both upside and downside risks. He noted several key points:

- The view that peak rates may need to go higher than September expectations was his own opinion, and wasn’t necessarily shared by members of the Federal Open Market Committee (the Fed’s chief monetary policy body)

- The probability of an economic soft landing was “very plausible”

- The Fed could slow the pace of rate hikes as a “risk management” technique, to reduce risk of over-tightening

- Taking rates beyond the expected peak would not be his “first choice”. He would prefer to hold rates at high levels for longer

- Goods inflation is coming down

- Housing inflation is mechanically higher due to low turnover; rents on some new leases are now dropping and will flow through with a lag

- Services inflation was driven by wages, which have been affected by lower immigration and the great resignation

Without overstating its significance, this suggests the Fed is not looking to micromanage near-term financial conditions.

This more nuanced assessment of inflation — and the policy response — suggests the market does not need to react so violently to each individual data print.

The caveat, of course, is that Powell’s stance may change depending on the data.

US economic data insights

Jobs

Non-farm payroll data, while decelerating, continues to be stronger than expected with 263,000 jobs added.

Headline layoffs are still not countering broader employment gains across the service sector.

But the reaction was not as negative as might be expected.

There were seasonal elements at play, which may be subsequently revised down. The household survey showed a 138,000 fall in jobs and unemployment stable at 3.7%.

It was interesting to note that job leavers as a percentage of unemployed fell for the second consecutive month. This suggests people are more reluctant to leave jobs, which may be an indicator of a softening labour market.

Wages data remains incompatible with inflation falling below 3%. Private workers saw a 0.6% gain in hourly earnings. The three-month moving average stepped up as a result.

Powell highlighted a key challenge for the labour market: the section of the workforce that has not returned to work.

While the participation rate for 25-to-54-year-olds has rebounded, the same rate for over-55s has not recovered.

New job openings and labour turnover data was more positive for labour market softness as job openings continue to roll over.

However there is still a reasonable way to go here before the labour market has loosened up enough to lead to a step down in wage inflation.

Consumption

Earlier in the week we had the Personal Consumption Expenditures data — the Fed’s preferred inflation gauge.

It came in lower than expected, at 0.22% month-on-month versus a consensus expectation of 0.3%. The year-on-year figure is 4.98% versus 5% expected.

The issue here is while underlying inflation has decelerated, it remains too high.

Manufacturing

The Institute for Supply Management manufacturing index fell from 50.2 to 49, versus 49.8 expected.

This confirms slowing manufacturing.

There were constructive signs. The employment component continued to fall, indicating softer labour markets. Pricing was lower and the supply component indicated backlogs reducing, which will help on the inflation front.

When you pull all this together, we conclude that the economy remains relatively resilient. There are clear pockets of weakness — notably in housing and some manufacturing.

Adviser Sam is invested

in making our world

A better place.

Watch as Sam meets a

mum rebuilding her life

thanks to responsible

investing

But four factors indicate we still have a long path to sustainably lower inflation:

- Catch-up in service sector spending

- Real incomes holding up as a result of wage and employment growth and falling inflation

- Excess savings remain in place (roughly US$1 trillion of the peak US$2.2 trillion still in place)

- Lower participation rates

What’s changed is that earnings in the next couple of quarters may hold up better than feared — and the Fed is now more likely to hold rates higher for longer, rather than go for a higher, short-term spike.

This reduces some of near-term risk to markets. But it does not open the door to a more sustained rally.

We are likely to remain in something of a holding pattern.

China

Protests appear to have prompted a conciliatory policy response from Beijing.

Chinese vice premier Sun Chunlan avoided references to “dynamic clearing” (ie zero Covid) in a speech and said the virus was in a less dangerous phase.

Some lockdown measures were lifted in Guangzhou and Chongqing.

China is now aiming for vaccination of over-80s by the end of January.

However re-opening will be staggered and slow due to constraints such ICU capacity and desire to keep deaths low.

We may see more signals from the politburo and central economic work conference later this month.

Australia

Headline CPI data headline fell 40bp to 6.9% versus 7.6% expected. The trimmed mean fell 10bp to 5.3% (versus 5.7% expected).

Food prices fell more than 6% as the impact of floods receded. Holiday and travel prices fell 6.4%.

This is a short-term reprieve for the RBA which will help make the case for slowing rate increases.

However the firmness of the economy suggests inflation is unlikely to have been beaten yet.

Markets

Volatility — as measured by the VIX index of market expectations for near-term price changes — has fallen back to its lowest levels for 2022.

Historically, this has been a signal that markets are near a local high point.

This prompts caution. (Though it may also signal lower expectations of a significant policy mistake from the Fed and the market is getting more comfortable with the 2023 outlook.)

Overall, markets remain hostage to the inflation data and the degree the economy will slow.

Bears note that markets historically bottom three-to-six months after a recession has begun — and after rates peak, not before.

The Australian market was broadly flat last week, led by miners. A recovery in growth stocks and small caps indicates risk appetite has picked as bond yields have fallen.

About Crispin Murray and Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia. Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Here are the main factors driving the ASX this week according to our head of equities Crispin Murray. Reported by portfolio specialist Chris Adams.

A CONTINUED drop in bond yields, a weaker US dollar and lower oil prices helped markets squeeze higher last week in a relatively quiet period on the macro front.

The S&P 500 rose 1.6% and the S&P/ASX 300 lifted 1.5% last week.

The key question is whether we are seeing the US economy slow enough to relieve inflationary pressure via labour markets and commodity prices.

This would allow the market to conclude the forward pricing of rate increases had peaked, regardless of Fed rhetoric.

The other related issue is how weak the economy gets and what this means for earnings.

There are several possible scenarios:

- A softer economy leads to falling bond yields and commodity prices. Earnings weakness is limited, allowing equities to continue rallying — potentially back to August highs (about 7% above current levels)

- A softer economy is followed by a significant earnings downturn, which after a near-term rally sees the market reverse to prior lows

- Inflation remains stubbornly high, meaning the rate path needs to stay higher for longer despite a softening economy. This creates greater risk for economic and earnings downside and sees the market fall to new lows. All scenarios are plausible at this stage.

Adviser Louise is invested

in making our world

A better place.

Louise meets a woman who

turned her life around thanks

to responsible investing

Equity markets are tied to the US dollar, the oil price and bonds yields.

It will be important to watch how oil performs following the OPEC meeting on December 4 and any potential Moscow reaction to price caps.

Bond yields are hostage to the outlook for inflation. The US dollar would likely weaken on signs of a softer economy and the rate outlook easing off — but would bounce back on signs of persistent inflation.

US Economics and policy

Minutes from the Fed’s last meeting suggest it is likely to pause rate hikes, reflecting the need to weigh up the lagged and cumulative effects of rate increases so far.

There was a reference to some members seeing the ultimate peak as higher than previously thought. This was the point Powell used in his press conference to try to contain any easing in total financial conditions.

Fed speakers continue to emphasise a lack of consistent evidence that inflation is coming down.

They continue to see embedded inflation as the key risk — and as a result prefer to err on the side of over-tightening.

A variety of lead indicators such as shipping prices, import prices, crude oil prices and surveys of expectations are moving in the right direction.

Two issues continue to underpin inflation:

- Supply chain shortages in certain areas. Several companies have recently flagged difficulties in obtaining certain parts. Part of the problem is that some industries re-tooled to different functions during the pandemic, prompting a structural decline in the number of suppliers of some industries.

- Labour. Wages remain stubbornly high, underpinning service inflation which is not yet showing signs of falling.

There are some anecdotal signs of softening in labour demand.

The US National Retail Federation — the world’s biggest retail trade association — expect seasonal hires of 525,000 versus 670,000 last year. This week’s US employment data will be an important test of this.

Initial reports for Black Friday weekend indicate strong retail sales (partly due to inflation.

Mastercard data suggest in-store purchases increased 12%, e-commerce sales rose 14%, apparel sales climbed 19%, restaurants jumped 21% and electronics lifted 4%.

China

There are widespread reports of protests about Covid lockdowns. Whether this leads to more loosening or harsher clampdowns is unclear.

It is hard to get a near-term read on China.

Covid cases are rising as the country goes into winter with limited hospital ICU capacity and no new vaccines yet approved.

The resources sector has remained largely resilient. The market is choosing to look through near-term weakness to focus on the re-opening trade.

As expected, the People’s Bank of China further reduced its bank reserve ratio requirements by 25bp to 11%.

This is part of an effort to bolster the economy in the face of rising cases and lockdowns.

Markets

The ASX has now recovered back above its August highs.

Financials, energy and resources have led the way. Staples, property and small caps have lagged.

Stocks expected to benefit from lower bond yields led the market higher last week. REITs, industrials and banks were the strongest sectors.

Miners lagged, driven mainly by weaker lithium stocks.

Chinese spot lithium prices have been falling. Monthly sales of electric vehicles (EVs) fell 21% in October, though there was some seasonality and impact from lockdowns.

EVs made up 19.4% of new registrations in October, versus 21.8% in September. There is some concern of excess lithium inventory in the channel. This is a volatile sector with a lot of momentum and is prone to sizeable drawdowns. Unlike other commodities the outlook for demand remains very strong and supply is likely to be constrained. Any inventory issue is likely to be short lived.

Adviser Sam is invested

in making our world

A better place.

Watch as Sam meets a

mum rebuilding her life

thanks to responsible

investing

About Crispin Murray and Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia. Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

A turning point for emerging markets may be approaching as the drivers of recent weakness dissipate, argues Pendal’s James Syme.

- US dollar outlook key to EM

- China emerges from downturn

- Find out about Pendal Global Emerging Markets Opportunities fund

A TURNING point for emerging markets equities is approaching as the drivers of recent weakness rapidly dissipate, says Pendal’s James Syme.

Emerging markets equities have faced headwinds in an environment of rising rates, a higher US dollar and China’s economic troubles and restrictive government policies.

But with the end of the US rate cycle starting to come into view and a newly engaged China starting a process of restoring growth, it is increasingly likely that stronger returns from emerging markets stocks are imminent.

“The two big drivers of the difficult environment in emerging markets in the past 21 months all seem to be improving,” says Syme, who co-manages Pendal’s Global Emerging Markets Opportunities fund.

“And that’s coming at a time of year when emerging markets have historically performed well.”

There is a long-established relationship between the performance of emerging markets equities and the US dollar.

“Since emerging markets came into existence as an asset class in the 1980s, virtually all the money that has been made has been during periods of dollar weakness, says Syme.

“Return on equity in strong-dollar periods is somewhere around zero.”

Find out about

Pendal Global Emerging Markets Opportunities Fund

How the USD affects emerging markets

There are a few reasons for this relationship.

First, emerging market countries tend depend on external financing to grow their economies.

Some use external financing to build manufacturing export capacity — Japan, Hong Kong, Korea and Taiwan all took this route. Others export commodities — like Saudi Arabia, Brazil or South Africa.

“Either way, external flows of capital — bond investors, equity investors or foreign direct investment — is a huge driver of what happens,” says Syme.

“Exchange rates are just ratios. When someone is selling dollars, they are buying something else.

“Are we into a weak dollar environment yet? No. And it’s premature to call it with US inflation still at 7.7 per cent.

“But when we do get to the point of a weaker dollar, the implications will be very powerful. You will want to own emerging markets when we get there.”

China’s impact on EMs

The other big driver of emerging markets opportunity is China.

This is partly because it is the largest part of the asset class, accounting for about a third of value in the emerging markets index.

“It has the most number of companies in the index so what happens in China drives returns for the emerging markets asset class as a whole,” says Syme.

“But it is also a tremendous consumer of raw materials and manufacturing products.

“In the last 20 years, emerging markets as a whole do better when China is strong and accelerating.”

But what’s the right way to play the opportunity in emerging markets over the coming year?

“It’s too simplistic to just go and buy back beaten down tech holdings like Alibaba and TSMC that were the leaders of the last bull market. Maybe they will do well – but you can’t just assume.

“The world has moved on. We’ve seen Armageddon in the crypto space, a lot of pain in VC-funded start-ups and significant cutbacks in the global mega tech players. That includes China.

Syme says instead the drivers of the next leg of growth will more likely be old world companies like Anhui Conch Cement, Tsingtao Brewery and Hong Kong Exchanges and Clearing.

But he says the key for most investors is simply to review their portfolios and ensure their emerging markets weighting has not been thrown out by the recent declines.

“Right now, you don’t want to be too underweight EM and you don’t want to be too underweight China.”

About Pendal Global Emerging Markets Opportunities Fund

James Syme, Paul Wimborne and Ada Chan are co-managers of Pendal’s Global Emerging Markets Opportunities Fund.

The fund aims to add value through a combination of country allocation and individual stock selection.

The country allocation process is based on analysis of a country’s economic growth, monetary policy, market liquidity, currency, governance/politics and equity market valuation.

The stock selection process focuses on buying quality growth stocks at attractive valuations.

Find out more about Pendal Global Emerging Markets Opportunities Fund here

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Here are the main factors driving the ASX this week according to portfolio manager Jim Taylor. Reported by portfolio specialist Chris Adams

THE question of when and where US rates will peak remains uncertain. There were no clear, new signals in the past week.

US economic data was mixed.

Housing, manufacturing and producer-purchasing index (PPI) prints were all weaker. Retail sales were stronger than expected.

The head of one of the 12 US federal reserve bank districts did his best to dampen positive sentiment. St Louis Fed President Jim Bullard noted the importance of avoiding the policy mistakes of the 1970s, when rates were dialled back too quickly.

(Bullard soon changes from a voting to non-voting member of the Federal Open Market Committee, the Fed’s chief monetary policy body).

The US yield curve inverted further and commodities were mixed. There were no further signals from Beijing after positive moves on Covid-zero and the property sector last week.

Equity markets held on to most of the gains from the previous week. The S&P 500 fell 0.6% and the S&P/ASX 300 gained 0.13%.

In the US we are seeing more caution creep into management statements around current conditions and the outlook.

This is a necessity — and ultimately a positive — since it indicates tighter rates are slowing the economy.

US rates

Bullard made the case that rates need to be between 5% and 7% to slow inflation.

His dovish outlook is for a 5% to 5.25% rate.

Find out about

Pendal Focus

Australian Share Fund

Crispin Murray,

Head of Equities

He expects rates to be kept high for an extended period, to avoid the monetary policy mistakes of the 1970s when rates were eased too early and inflation came roaring back.

“We’re going to have to see very tangible evidence that inflation’s coming down meaningfully toward target,” he said. “I think we’re going to want to err on the side of staying higher for longer in order to get that to happen”.

US economy

Producer Price Index

The producer price index — a measure of US inflation at the wholesale level — rose 0.2% in October versus 0.4% expected.

This was the smallest increase since July 2021. It’s now running at 8% year-on-year, well below March’s peak of 11.7%.

Core PPI (ex-food and energy) fell 0.1%. It’s now 5.4% year-on-year versus the 9.7% peak in March.

This reflects a broad-based slowdown in goods prices.

Evidence continues to build that corporate margins are coming under pressure as supply chains loosen and consumer spending shifts from goods to services.

The Fed continues to watch corporate margins closely as a lead indicator for inflationary pressure.

Manufacturing

The Philadelphia Fed manufacturing index declined by 11 points to -19.4 in November, against consensus expectations for an increase.

It now stands at the lowest level since May 2020.

The underlying composition was weak as new orders, shipments, and employment components all declined.

Housing

The US housing market remains dire. New housing starts fell 4.2% and are now down 21% from the April peak. Building permits fell 2.4% in October. (Both results were slightly better than expected, however).

Find out about

Pendal Horizon Sustainable Australian Share Fund

A key measure of US homebuilder activity and sentiment — the National Association of Home Builders index — plunged from 38 to 33 in November. This was below a consensus of 36.

Sales of existing homes fell 5.9% in October. This was above consensus, but it’s now down about 32% from the January peak.

The supply of new homes in the last data for September stood at 9.2 months of sales.

Mortgage rates have now peaked so demand is unlikely to fall much further. But it will remain extremely depressed for some time yet.

The fall in new housing starts is concentrated in single-family dwellings. Multi-family starts have remained steady for much of the year, but leading indicators such as building permits suggest a small decline in coming months.

Volume activity has been very weak.

The question now becomes: how much do house prices fall from here?

Retail sales

Retail sales data stands in stark contrast to the data points above which support the notion of a cooling economy.

October retail sales rose 1.3% versus 1% expected. Sales (excluding autos) were 1.3%, versus consensus of +0.4%.

It seems clear that consumers are happy to run down the strong savings buffer accumulated during Covid.

This buffer has declined, but still remains in positive territory versus pre-Covid.

Consumption remains on course for a strong end to the year.

One potentially positive sign is retailers offering greater discounts to support sales.

For example, in October Amazon held its second “Prime Day” sale for 2022. These usually only happen once a year.

US retail chain Target noted they would need further markdowns to shift excess inventory by the end of the Christmas period if recent trends persisted.

The EVRISI Retailers survey suggests retail pricing power has collapsed back to pre-Covid levels. This is another requirement for bringing inflation to heel.

Australian economy

The labour market remains resilient with the unemployment rate falling to 3.4%. Unemployment and under-utilisation rates are at a 40-year low.

Employment grew 32,000 in October versus 15,000 expected. The participation rate held steady at 66.5%.

The gains were made in full-time employment (+32,000) while part-time jobs fell 15,000.

Hours worked rose 2.3% for the month, driven mainly by fewer workers taking sick and annual leave.

NSW job growth remains strong, while we are seeing weakening labour conditions in Western Australia.

Tasmania and South Australia are on an uptrend. Queensland and Victoria have flat-lined.

Hourly wage rates (ex-bonuses) in Australia rose +1% q/q and +3.1% y/y in Q3. This was stronger than consensus, which was looking for a 0.9% q/q outcome.

Headline wages growth was the strongest in quarterly terms since Q1 2012.

Quarterly growth in private-sector wages (+1.22% q/q) was the strongest since Q2 2008 (+1.24% q/q) and the second strongest since the WPI series began in 1997.

Private-sector wage rates (includingbonuses and commissions) rose 4.1% y/y.

All this is consistent with feedback from private-sector companies, which are flagging wage growth expectations in the mid-to-high 3% range.

This is a critical factor to watch given the more dovish tack taken by the RBA compared to other central banks.

About Jim Taylor and Pendal Focus Australian Share Fund

Drawing on more than 25 years of experience investing in top-performing Australian companies and a background in accounting, Jim manages our Long/Short Fund and co-manages our Imputation Fund. He is a Chartered Accountant with membership of the Australian Institute of Chartered Accountants.

Pendal Focus Australian Share Fund is managed by Crispin Murray. The fund has beaten its benchmark in 14 years of its 18-year history (after fees), across a range of market conditions. Find out more about Pendal Focus Australian Share Fund here.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

The super-high inflation battle of 2022 may be won, but the outcome of the war is still uncertain says Pendal’s head of government bond strategies TIM HEXT.

THE market had been looking for US inflation to moderate for several months.

Forward indicators of goods prices had pointed this way since Q3.

Last week the US Consumer Price Index finally delivered a much slower pace of increase than expected.

Stocks surged, which was surprising given it wasn’t entirely unexpected.

Then again, markets were looking for any relief from this year’s constant inflation woes to jump on a positive narrative.

Doers this start an ongoing trend? Or will this month’s CPI join earlier false dawns such as July?

As always with inflation the breakdown is important.

Headline was 0.4% against consensus 0.6%. Core was 0.3%, below the consensus of 0.5%.

Leading the way down was used car prices, which fell 2.4%. Leading indicators show further weakness ahead. After a Covid-led 68% rise there is plenty of room to fall.

Apparel prices fell 0.7%. Inventory overhangs in a number of retail areas may see further discounting ahead.

The surprise contributor to lower inflation was health insurance.

This had been increasing by 2% per month for the past year. It fell 4% in October — and the way it’s calculated means it will keep falling for the next year.

Find out about

Pendal’s Income and Fixed Interest funds

Finally, rents showed some slowing in the pace of rises. They were still up 0.6%, but it was the smallest increase in six months. Again, forward indicators point to continued moderation in rent (and owner equivalent rent) in the CPI.

These changes all point to further moderation in the months ahead.

Although not entirely unexpected, lower inflation will continue to provide some encouragement to markets that the Fed can slow the pace of hikes.

December still seems a lock for a hike of 50 percentage points. But in 2023 they could moderate to 25 points or even none.

What’s next

So the super-high inflation battle of 2022 may be won. But the outcome of the war is still uncertain.

Getting from 9% to 4% next year will be the easy part.

The globe is a now a different place post-pandemic.

A combination of commodity shocks from Russia and tight labour markets globally will likely see inflation get sticky around 4%. Any rate cuts by then may be wishful thinking.

Unless we tip into a steep recession the US Fed will remain wary about calling victory on inflation any time soon.

Investors should continue to view any decent rallies as an opportunity to de-risk portfolios for the challenges ahead.

About Tim Hext and Pendal’s Income & Fixed Interest boutique

Tim Hext is a Pendal portfolio manager and head of government bond strategies in our Income and Fixed Interest team.

Tim has extensive experience in banking, financial markets and funding including senior positions with NSW Treasury Corporation (TCorp), Westpac Treasury, Commonwealth Bank of Australia, Deutsche Bank, Bain & Co and Swiss Bank Corporation.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia.

Find out more about Pendal’s fixed interest strategies here

About Pendal

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

In 2023, Pendal became part of Perpetual Limited (ASX:PPT), bringing together two of Australia’s most respected active asset management brands to create a global leader in multi-boutique asset management with autonomous, world-class investment capabilities and a growing leadership position in ESG.

Chinese policy has shifted in recent few weeks, impacting emerging markets investors. Pendal’s JAMES SYME outlines how our EM team is responding

This is a monthly insight from James Syme, Paul Wimborne and Ada Chan, co-managers of Pendal’s Global Emerging Markets Opportunities Fund

- China’s economy has lots of potential to recover but has been constrained by extremely negative policies in key areas.

- Chinese stocks steadily sold off as investors became more pessimistic about the prospects for more market-friendly policies.

- This month Beijing made major policy moves on Covid re-opening and real estate industry debt. Investors should broadly see this as a buying opportunity for the best-positioned Chinese companies. We have very significantly reduced our underweight position in China.

- Some parts of China’s equity market remain unattractive, include state-owned banks, private-sector real estate developers and tech giants with very poor corporate governance.

ONE of the characteristics of emerging markets is volatility.

Things can turn very quickly — positively or negatively.

Our investment process is designed to accommodate this. We are constantly alert to market drivers, change and trend, positive and negative surprises and changing forecasts and surveys.

The past two weeks have seen significant shifts in Chinese policy, which put some market drivers into a new context.

Our process emphasises a disciplined and repeatable country-based analytical process.

As always, we follow our core five-point framework in reviewing the outlook for Chinese equities (in USD terms) over the next two years.

These are:

- Growth

- Liquidity and credit environment

- Currency

- Management and politics

- Valuation

Here is our latest thinking on these market drivers in relation to China:

1. Growth

Growth in China is weak by historic standards, with strong exports offset by very weak domestic investment and consumption.

Third-quarter GDP was up 3% year-on-year. Industrial production lifted 6.3% and exports grew 10.7%.

But retail sales were up only 2.5% and property sales (for the 31 main listed players) lost 29%.

The crippling effect of the Three Red Lines restriction on lending to property developers continues to have a devastating effect on the sector. Meanwhile ongoing Covid lockdowns hurt confidence-hit consumers.

The outlook does not seem to be improving either. PMI surveys for October weakened to 48.7 for non-manufacturing and 49.2 for manufacturing.

Can fiscal policy drive growth?

Next month’s Central Economic Work Conference can shift the emphasis of fiscal policy while keeping to agreed policy parameters.

Probably the most effective change would be to directly support households, given the current downturn in domestic consumption.

Targeted fiscal measures have been successfully used to support consumption in previous downturns. Examples include subsidies for rural purchasers of home appliance in 2008 and support for car buyers in 2014-15.

But given the weight of real estate and adjacent sectors in the economy, this is unlikely to do more than help specific industries.

2. Liquidity and credit environment

The liquidity and credit environment will need to do some of the lifting.

But monetary stimulus is constrained by weak private credit demand and concerns about the exchange rate.

The capacity certainly exists. Despite global inflationary pressures the Chinese economy is heading into deflation.

PPI inflation dropped into negative territory in October after a September print of just +0.9%. Household and corporate excess deposits continue to collect in the commercial banking system.

The liquidity and credit metrics we track look very promising.

Total outstanding credit grew 10.5% in the year to October, while M2 money supply growth in October was 11.8%.

These represent a continuing pick-up in credit and money growth and a return to the more stimulative measures of early 2020 and in 2016-2017.

However deeper changes are needed for this to work.

There are two reasons:

Firstly, private sector credit demand is extremely weak. Simply making it cheaper and more available is unlikely to change that.

This is a classic crisis of confidence in which the central bank can end up “pushing on a string”.

Either policies change to create confidence or fiscal policy must do the work. Secondly, while the three red lines restrictions on private sector property developers are still in place, the key sector that isn’t borrowing will remain unable to do so.

Find out about

Pendal Global Emerging Markets Opportunities Fund

3. Currency

Thecurrency was at its all-time real effective exchange rate in the first quarter of 2022.

Though it is notionally supported by net exports — and protected by capital controls — it is likely to weaken relative to the US dollar.

This is partly because of interest rate differentials and partly because policymakers among east-Asian exporters must keep their currencies reasonably in-line with the depreciating Japanese yen.

4. Management and politics

The previous drivers are important, but management and politics are the key.

This month President Xi Jinping was appointed for an unprecedented third term.

In an overhaul of the Politburo Standing Committee, market-friendly reformers (including Premier Li Keqiang) were removed and replaced with Xi loyalists.

State media have begun referring to Xi Jinping as “Core” leader and establishing his political views (“Xi Jinping Thought”) as doctrine.

This marks a move away from the “Collective Leadership” system of Chinese politics which has been in place since the 11th Party Congress in 1978.

The economic focus on technology and quality of life adopted at the 2017 Congress remains in place.

The main changes at this congress were around governance and national security, with emphases on international relations, geopolitics and reunification with Taiwan.

What does this mean for the economy, and for a market looking for some political and policy relief?

The policies that have dramatically undermined growth — real estate restrictions and zero Covid — remain key.

As do the political developments that have hugely increased investor perception of risk in China — clampdown on tech companies, support for Russia, cold conflict with the West.

We essentially believe China’s policy choices in the past two years have broken its economy and equity market. We may now be seeing the beginning of changes that are needed to fix this.

On November 11, the People’s Bank of China and the banking regulator extended the end-of-2022 deadline for banks to limit their property and mortgage loans.

This major step is likely to substantially ease a credit crisis in the Chinese real estate sector.

Leading banks must reduce the share of total loans made to property companies to 40% and the share made to mortgages to 32.5%. But the deadline has been indefinitely extended.

This is likely to restore confidence in the property sector — particularly for homebuyers — though the most leveraged developers still face a difficult future.

On the same day we saw changes in China’s Covid policies — though officials stressed these were a refinement, not a relaxation.

The 20 new Covid policies include shorter compulsory quarantines, reduced testing and less latitude for local officials to impose their own restrictions.

Rising cases suggest this is not likely to lead to a rapid full re-opening of the economy.

But Beijing’s health commission said the government would keep advancing “in small steps”.

Markets have taken these steps as a sign that the Chinese economy — and Chinese companies — are on a path to the same post-lockdown, mini-booms we saw in other economies.

Then on November 14 President Xi met President Biden in Indonesia.

Officials from both sides said substantial differences remained between the two.

But the face-to-face meeting appeared cordial. The discussions are a sign that China is not Russia.

5. Valuation

Valuation is the only one of these five factors that are unambiguously supportive.

But valuation alone is not a buy case.

For any market, ongoing economic growth and corporate earnings disappointments undermine the fundamentals to which valuation multiples are applied.

Worsening liquidity conditions justify lower valuation multiples. A poor currency outlook will reduce expected US dollar returns.

Most significantly, the downside to valuation multiples when politics goes bad is always much, much more than you think.

The MSCI China forward price/earnings ratio (based on consensus 12-month forward estimates) has declined from a peak of 18.5x in February 2021 to 8.3x at the end of October.

This compares to a recent average of 11.3x.

Other valuation metrics have similar patterns. Cheap, but cheap alone is not enough.

Remain alert to opportunities

Our investment process has a monthly review of the key top-down drivers of USD equity return for all countries.

We take no strategic views. No market is an automatic overweight and no market is automatically excluded.

We do not think Chinese equities — whether A-shares, H-shares or overseas listings — are “uninvestable”. We remain alert to opportunities.

Some parts of the Chinese equity market do look very difficult to invest in.

Public sector banks remain mere policy tools and investor mistrust here is very high.

The more leveraged private sector developers are still unlikely to survive their debts coming due.

Corporate governance at some big technology companies — most notably Alibaba — is very poor and hard to look past.

Some Chinese state-owned companies remain sanctioned by the US Treasury and are literally uninvestable for most foreign investors.

But China is a huge market. It is the biggest emerging market by market capitalisation and by number of listed securities.

Since the end of October we have very significantly reduced our Chinese underweight.

The great bulk of this move happened before the policy changes were announced. Since those announcements, Chinese assets have moved sharply higher.

We will continue to follow our process and react to both the level of these market drivers — as well as change, trend, surprise, forecasts and surveys.

A mix of positive and negative drivers continue to influence China.

But the outlook is much better than a month ago.

And it is always a mistake in emerging market investing to assume that any trend — up or down — will continue forever.

About Pendal Global Emerging Markets Opportunities Fund

James Syme, Paul Wimborne and Ada Chan are co-managers of Pendal’s Global Emerging Markets Opportunities Fund.

The fund aims to add value through a combination of country allocation and individual stock selection.

The country allocation process is based on analysis of a country’s economic growth, monetary policy, market liquidity, currency, governance/politics and equity market valuation.

The stock selection process focuses on buying quality growth stocks at attractive valuations.

Find out more about Pendal Global Emerging Markets Opportunities Fund here

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.