Here are the main factors driving the ASX this week according to our head of equities Crispin Murray. Reported by portfolio specialist Chris Adams.

Find out about Crispin’s Pendal Focus Australian Share Fund

Find out about Crispin’s sustainable Pendal Horizon Fund

FOUR major issues are influencing markets at the moment:

- Rising rates and the withdrawal of liquidity

- The disruptive effect of the Omicron wave

- The potential for conflict between Russia and Ukraine

- Chinese policy easing

Of these, only the fourth is positive. As a result we have seen equities weaken in the year to date.

At this point the outlook for rates and inflation is the most important issue.

As the broad equity market has fallen, the growth stocks have underperformed. In the US, the S&P 500 fell 5.7% last week while the NASDAQ was down 7.6%.

The Australian market also fell, but less so given a skew to banks and resources over growth sectors. The S&P/ASX 300 fell 2.9%.

The S&P 500 and NASDAQ broke down through their 200-day moving averages for the first time in the post-March 2020 bull market.

This does not mean the market’s run is over. But it is the first meaningful correction, coinciding with a shift in monetary policy and highlighting the importance that liquidity has played in the Covid era.

Pendal Focus Australian Share Fund

Now rated at the highest level by Lonsec, Morningstar and Zenith

It is a well-understood principle that if rates, oil and the US dollar are all rising, equities are likely to drop. Oil and the US dollar index have been rising for a few months. The move higher in rates has been the final piece.

The Fed’s meeting this week will be an important near-term signal. The market has adopted a very hawkish view on policy in the past three weeks. Some see potential for Quantitative Easing (QA) to end immediately; the risk of an immediate rate hike; or signs that an expected hike in March could be 50bps rather than 25bps.

We think that those moves are unlikely. The Fed may seek to assuage the more hawkish concerns, which could actually see a relief rally.

Despite a sharp sell-down in markets and the possibility of soothing words from the Fed, the underlying challenge of inflation remains.

As a result we do not see this as a time to be re-loading on some of the sold-down names.

Rates outlook

The drop in the overall market and the correction in growth has been caused by two factors: the market moving to price in rates rising to around 2% by end of next year and the realisation that liquidity will start drying up.

The market is considering four broad scenarios:

- The bull case: 2% rates do the job, inflation eases, economic growth slows but remains solid, earnings continue to grow and the market valuation rating holds

- Central banks over-tighten like we saw in 2018 as the pandemic makes gauging the economy hard. The economy and earnings roll over in response and the market sells off.

- Rates continue to rise – possibly above 2% – but this does not derail the economy. This is a traditional scenario similar to the mid-to-late 1990s. Earnings continue to grow, supporting markets and offsetting an equity de-rating

- The bear case: inflation proves persistent. Central banks have to engineer a hard landing to re-anchor expectations. This would hit earnings hard and see markets sell off

The key point is that we are looking at a very disparate outcomes, creating more uncertainty for markets

Inflation outlook

The key underlying question is what will limit and bring down inflation.

This could be a combination of:

- Higher prices choking off demand and slowing the economy, ie inflation curing itself

- Debt and high leverage meaning the economy is sensitive to small rate changes and modest hikes working to bring down demand

- Demographics and aging populations suppressing demand and credit growth

- Technological disruption continuing to act as a deflationary force

On the flip side, arguments for persistent inflation include:

- Excess stimulus continuing to support demand

- Structural decline in labour market supply underpinning wage growth

- Transition to clean energy leading to higher fuel costs and investment spending

- China shifting away from export model to dual circulation

- The policy imperative as governments suppress real rates to manage debt

We don’t know the outcome. But it is clear that inflation presents more an issue today than at any time in the past couple of decades.

Liquidity a significant issue

The withdrawal of liquidity is potentially as significant an issue for equities as the debate around rates.

The shift in the liquidity environment is likely to make this a tougher year for equities. In our view, persistent growth in equities since March 2020 with no material correction is due to the surplus liquidity evident in money supply data.

QA is unwinding faster than expected. US money supply growth has slowed from just shy of 30% per annum at its peak to just above 10% now. This means less surplus liquidity to be funneled into financial assets.

Sustainable and

Responsible Investments

Fund Manager of the Year

Early warnings signals have been evident for some time in the more speculative parts of the market.

Some, such as the ARK Innovation ETF and Chinese tech indices peaked a year ago and are off about 60% since then. Others such as crypto and the solar and IPO ETFs tracked sideways through to October/November and are off 30-50% since then. Tesla and the broader Electric Vehicle and battery sector have proven more resilient, but are showing signs of rolling over.

The overall market has held up better – particularly the growth indices – due to the performance of the mega-caps. But this appeared to be changing last week, as they also started to underperform.

The US earnings season is expected to be decent and could help offset recent weakness. But there have been some disappointments in early results, notably Netflix. There is also risk that the market focuses on near-term uncertainty from Omicron’s disruption.

Credit spreads have not budged. This, along with resilient commodity prices, suggests the market is not yet at the point where it believes policy will derail the cycle.

That said, there is a view that we will need to see credit spreads widen to help tighten financial conditions sufficiently to restrain inflation. In this context, low spreads may not be as unambiguously positive as is usually the case.

It is important to note that the Australian market is more defensive and better protected in this environment due to the index mix. It is also less extended on valuation.

Covid and economic disruption

The good news is that global cases may be peaking.

New daily case data is increasingly convoluted and hard to measure. US waste water analysis suggests this wave was five times the size of the previous one, but is now rolling over.

It is becoming clear that Omicron is less severe than previous strains, though there is no consensus on why.

Regardless, health systems are coping, albeit under a lot of strain. In NSW the proportion of hospitalised patients needing to go into ICU is less than half the previous wave.

Omicron’s sheer transmissibility is still creating a lot of disruption. Some companies have seen more than 30% of their workforce unable to work, leading to businesses effectively shutting down. This is a risk to supply chains, particularly if the strain becomes established in China.

Real-time surveys in the US highlight how consumers have become more cautious. Anecdotally this is also true in Australia, which could have a bearing on company outlooks in the upcoming earnings season.

All that said, the market has tended to look through near-term numbers and we suspect this will continue.

There are signs we are entering the phase of learning to live with Covid. This should help some of the oversold re-opening stocks.

Russia/Ukraine threat

The odds of a Russian invasion of Ukraine have risen considerably in recent weeks. This adds to market uncertainty and is a risk for energy markets and gas supply. This is an issue to keep watching.

About Crispin Murray and Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia. Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Pendal’s head of equities Crispin Murray today challenged BHP’s proposal to collapse its dual-listed company (DLC) structure.

“As BHP Ltd (Australia) shareholders, we are not in favour of BHP’s proposal for the collapse of its DLC structure,” Mr Murray said.

On December 8, BHP announced a final board decision to end the DLC structure and unify its corporate structure under the existing Australian parent company, BHP Group Limited.

BHP Group Limited and BHP Group Plc shareholder meetings are expected to take place on January 20 with unification due to be complete by January 31.

“This proposal is transferring value from Australian Limited shareholders to offshore PLC shareholders. This value transfer has been evidenced by the material decline in the Australian multiple of earnings that BHP Ltd trades on,” said Mr Murray, who leads one of the Australia’s biggest Australian equities teams for independent asset manager Pendal Group.

“We appreciate that the main reason for the proposal is the greater flexibility it provides to do large M&A deals in the future. However, there are two questions we have around this. Firstly, BHP has had a poor track record in this regard historically. There is a risk that Australian shareholders pay the price for the unified corporate structure and then see more value destruction overtime. Secondly, while a unified corporate structure will make doing scrip-based M&A easier, the decline in multiple potentially negates this.”

Pendal expects that should the proposal not go through the long-term premium of the Australian listed company to PLC would return.

Below, Mr Murray outlines Pendal’s main issues with the proposal:

What has been the value destruction borne by Australian shareholders to date?

The BHP Ltd share price fell 14% in the two days (17th-18th August 2021) following the announcement of the DLC collapse.

The premium of BHP Ltd’s (ASX) share price to BHP PLC’s (LSE) share price — which had existed almost since the inception of the DLC — fell from more than 20% to around 5% after the announcement.

Even with the more recent recovery in resources, the stock has underperformed the market by about 15%, in line with the reduction in the Ltd premium to PLC.

This premium is likely to erode further if the vote goes through.

In our view, this represents a substantial, permanent and unnecessary value transfer from Australian to PLC shareholders.

BHP management expected the UK share price to re-rate to a multiple in line with the Australian listing.

In fact, the opposite has occurred.

The charts below show the absolute PE of BHP Ltd vs the ASX200 is at a 10-year low, despite the overall rise in market rating.

Relative to industrials, the stock is almost half the rating it was 10 years ago.

If a key motivation is to enable scrip-based M&A, the reduction in multiple makes any potential acquisition less appealing.

Has the dual listed structure impacted BHP’s ability to do M&A?

In our view, none of the reasons BHP is proposing as rationale for the collapse of the DLC structure would stand in the way of BHP executing its strategy.

The DLC structure was consciously put in place by BHP, at its discretion, at the time of the Billiton merger. It has now been in place for 20 years and through this time BHP has had no issue implementing its strategy or accessing capital.

BHP has a strong balance sheet and access to debt and equity capital markets across multiple geographies and listings.

In the preamble to the US Onshore petroleum stake in 2017 — and under activist shareholder pressure — BHP vigorously defended the DLC structure and concluded it was too expensive to unwind.

Most of the costs associated with the DLC collapse have increased in the interim and are expected to be $350mln to $450mln.

But M&A is not always a good thing…

We respect the BHP Board and management. However, we do note how difficult it is to execute effective, large-scale deals in the resources sector.

To highlight this, there are a number of examples of unsuccessful transactions under former BHP management. These include:

- The merger with Billiton. After 15 years, BHP chose to demerge most of the Billiton assets into South 32 (S32), since they did not meet BHP’s standards of being low cost and long life. The demerger resulted in de-rating of the S32 earnings of about 33%, which persists today.

- The 2011 acquisition of PetroHawk and Fayetteville for U$15.1bn and US$4.8bn respectively. An additional US$18.9bn was spent on the assets during ownership. Ultimately these assets were sold for US$10.8bn in FY18 after an attributable EBIT loss of US$5bn during ownership.

- The 2005 acquisition of WMC Resources. This includes Olympic Dam and Nickel West. Neither asset has fulfilled the original expectation of returns.

- There was also the failed attempted acquisition of Potash of Saskatchewan (Canada) in 2011 at a price that subsequently fell away materially.

BHP has had cumulative write-downs of $22.9bn since 2001. Much of this relates to assets bought at too high a price.

M&A in the resource sector is difficult. The likelihood is that value accrues to the acquired company’s shareholders.

That Australian shareholders wear the current value destruction from the collapse of the DLC just to simplify M&A in the future is challenging to accept.

Isn’t this really about the de-merger of the petroleum business?

In our view, reassessment of the DLC structure is tied to the decision to de-merge the petroleum business.

While BHP has stated it would go ahead with the demerger even if the DLC was not collapsed, the company has highlighted that it would make the process simpler.

We believe these two strategic decisions need to be evaluated separately.

And, again, we are not sure it is in the interests of Australian shareholders to accept the value destruction of the DLC collapse for a simpler demerger that may or may not go ahead.

Are there broader implications for the market?

The consolidation of BHP on the ASX will see its ASX 200 index weight rising from about 5.8% to about 9.6%.

While this is not the concern of BHP management, taking a macro view highlights that such a concentration of index weighting is not ideal for Australian broad market investors. It reduces diversification and impacts expected risk-adjusted returns.

It certainly will, however, lead to an increase in ‘non-discretionary holdings’ from index funds and those managing benchmark risk. This could reduce active shareholder pressure on management. We would strongly argue that this is not in the long-term interest of BHP shareholders.

Conclusion

We appreciate the company’s motivation for seeking to collapse the DLC structure in terms of simplifying management of the organisation.

BHP PLC shareholders will also benefit from this one-off gain, though many of those with current PLC stock may not ultimately be long-term holders. This is why there is very little push-back on the proposal.

But in our view, as detailed above, this proposal is clearly not in the interests of Australian BHP Ltd shareholders.

Given the clear value destruction and the questionable benefits accruing from the change, Pendal will be voting shares under its management against the proposal.

Here are the main factors driving the ASX this week according to our head of equities Crispin Murray. Reported by portfolio specialist Chris Adams.

Find out about Crispin’s Pendal Focus Australian Share Fund

Find out about Crispin’s sustainable Pendal Horizon Fund

This is the final weekly note from Pendal’s Australian equities team for 2022. We wish our clients and readers a well-deserved rest after a very busy year. Our weekly note will return early in the new year.

COVID and inflation have been the two big issues to watch all year. Both have taken significant turns in recent weeks, leaving the outlook for 2022 as uncertain as ever.

This does not mean that the outlook is necessarily negative.

Rather, the potential paths we head down next year look very different:

- On Covid: We could be in the early phases of the largest wave. This could put substantial strain on healthcare systems, prompting renewed restrictions which could drag on the economy and escalate supply chain problems.

Alternatively we may discover the effects of the vaccines, anti-virals and potential lower virulence of Omicron mean the virus becomes more benign — to be handled without restrictions.

- On inflation and rates: We could see economic strength and a tight labour market sustain inflationary pressures. This could prompt both the Fed and markets to realise that higher real rates are needed, prompting a sell-off in equities and growth stocks in particular.

Alternatively, we may see inflationary pressures ease as supply chains resolve themselves, people re-enter the labour force and structural factors such as tech and debt re-assert. In this scenario growth and earnings are good and we see bonds and equities rallying, with growth resuming leadership.

Now is not the time for betting the house on one of these directions.

We should have a far better understanding of the Omicron issue within three weeks, while the rates issue will take much of next year to play out.

Our portfolios are low on thematic risk. Instead we are looking for features such as good cash flow, strong stock-specific stories and good franchise strength.

We are maintaining a tilt to re-opening plays given the poor sentiment right now. But we are mindful of the near-term path, given the potential for more negative short-term news flow.

Markets were down last week. The S&P/ASX 300 fell 0.7% and the S&P 500 lost 1.9%.

Pendal Focus Australian Share Fund

Now rated at the highest level by Lonsec, Morningstar and Zenith

Concerns about central bank policy and the degree to which rates need to rise to contain inflation weighed. So too did uncertainty over Covid due to contradictory research on Omicron risks and increasing government restrictions heading into Christmas.

Covid and vaccines outlook

Surging case numbers in a number of countries — notably the UK and Denmark — are fanning concerns about healthcare systems coming under strain.

The interplay between Delta and Omicron waves is complicating an assessment of the situation and government reactions. For example The Netherlands has reimposed lockdowns despite material falls in new cases, fearing that an Omicron wave will see new cases hurtle higher again.

The risk of Omicron breakthrough infections — ie vaccinated people catching the virus — is 5.4x higher than it was for Delta, according to research from the Imperial College in London.

The key question concerns the disconnection between cases and hospitalisations.

South African data is hard to interpret because it is subject to large backward revisions. For example, the number of people in hospital with Omicron was revised up 61%. Many of these patients are in hospital for other reasons and have incidentally tested positive. This is leading some to conclude that there have been far more asymptomatic cases than first thought.

The number of new daily cases in Gauteng Province — home to more than a quarter of South Africa’s population — is falling.

This has happened within a month of the wave’s start — rather than the usual two to three months in previous waves.

There are a number of theories to explain this:

- Case numbers are being significantly understated due to a higher proportion of asymptomatic cases

- Changes in social behaviour — people self-isolating more quickly — may have a containing effect

- Better medical treatment

- A portion of the community is not susceptible to the variant

- A significant portion of the population is transient and has left the province as we approach Christmas

Each of these explanations have quite different interpretations.

The other issue is a disconnection with hospitalisations. Does this reflect lower severity or is it a function of the younger demographics in Gauteng?

A study from Imperial College — not yet peer-reviewed — claims there is no reason mutations in Omicron should lead to less severity. If there are lower case numbers it is because of vaccinations, the study says.

Nevertheless, the proportion of people needing critical care — as well as the length of hospitalisations — are materially lower than the last wave. This suggests there is some factor helping reduce severity.

Covid in the UK and US

The UK will provide an acid test. It is too early to draw conclusions on hospitalisation rates. But we are seeing a high incidence of positive tests among British patients hospitalised for other reasons. This suggests a high rate of asymptomatic cases.

The UK will provide the lead for US, which will be the key driver of market sentiment.

US cases overall are still not rising quickly. They are up 3% week-on-week. But this was held down by declining numbers in the Midwest. Lead indicators suggest a material acceleration with the New York testing positivity rate doubling in three days.

The most effective response to Omicron is the third jab. This reloads the number of immune antibodies, materially reducing risk of breakthrough infection.

The case growth has triggered an acceleration of boosters in most affected countries, though capacity to administer shots at this time of year is constrained.

Sustainable and

Responsible Investments

Fund Manager of the Year

The key issue for markets is the policy response to this wave of cases.

The near-term risk is that markets fear the worst and governments feel the need to act, reimposing restrictions. We are already seeing this come through with US Q4 GDP forecasts moderating to 6%, down from 7-8%.

This could see a sentiment-driven sell-off in markets. But it is important to note the strength of nominal GDP growth, which means earnings should remain firm.

Economics and policy

The Fed came in at the hawkish end of the expected range, doubling the rate of Quantitative Easing tapering. QE should now end in March. The Fed’s “dot points” now indicate three hikes in 2022.

The market was initially positive because there was no escalation of inflation concerns. It is worth noting that the expected terminal value of rates did not budge, remaining at 2.1% by the end of 2024.

There are two disconnections worth noting.

First, the market does not currently believe the Fed will need to raise rates in 2023. It sees rates peaking around 1.5%, reflecting confidence in inflation fixing itself.

Second, the Fed and the market both believe inflation can be fixed without real rates ever going positive.

There is a school of thought that believes this is not credible because of key differences between this cycle and previous examples:

- Household balance sheets are far stronger

- Fiscal stimulus is far greater

- The degree of QE has been much higher

- Changes to the labour market and supply chains

- The impact of greenflation

- Real rates have been far lower for longer

There are small signs that the Fed’s pivot is already prompting inflation expectations to moderate and that we may have passed through peak fear on this front.

There are also signals that people are returning to the labour market in the US, with the participation rate edging up.

Outside the US, the Bank of England raised rates from 0.1% to 0.25%, surprising a market that expected them to hold steady given the risk from Covid. This was seen as a negative, suggesting the BOE sees inflation as a key risk.

The ECB was more balanced, announcing the end of its pandemic program of QE but putting in place a transition program. This is designed to prevent fears that early rate rises put peripheral bond markets under pressure. Inflation is less of an issue in the EU currently, which gives them more latitude.

US fiscal policy took a twist today with Senator Joe Manchin announcing he will not support the current Build Back Better package in its current form.

This likely means the current model, which was to put in programs for one, three and five year periods to reduce their apparent cost, is dead.

Rather Biden will need to reduce the programs he wants to commit to and ensure they are fully funded. This still looks likely, given Manchin’s relationship with Biden. But it will take time and will be a set-back for renewable energy-related stocks.

Markets

Overall we believe the market environment is still reasonably constructive.

Growth is strong, companies have pricing power, rates remain very low and sentiment is not over-confident.

In the near term the Covid case spike could hold the market back. The early read on Omicron suggests any further sell-off would be an opportunity for bombed-out cyclicals.

The medium term issue is that the market seems to be underestimating the policy response required to contain inflation.

In this environment a focus on higher-returning, good-quality franchise positions is an important part of the portfolio.

It is also worth noting the continued rebound in iron ore.

This is partly driven by inventory re-stocking, but also reflects improved sentiment on China. Beijing continues to signal a more pro-growth policy shift, albeit with no major stimulus yet announced.

About Crispin Murray and Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia. Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Here are the main factors driving the ASX this week according to our head of equities Crispin Murray. Reported by portfolio specialist Chris Adams

MARKETS rebounded as volatility subsided last week. This was due more to a lack of bad news on Covid or the US rates outlook rather than any specific good news.

The S&P ASX 300 rose 1.65% and the S&P 500 gained 3.85%. However the US rebound was not led by the sectors hit hardest in recent weeks. Energy and technology were up on the week, but less so than the overall market.

This week should provide important markers for the two main issues currently driving markets:

- There are a number of central bank meetings — including the Fed which will update its quarterly rate plot. This should give greater guidance on the outlook for tighter rates.

- We should begin to get a clearer view on Omicron trends and more research on the effectiveness of vaccines.

It is also worth noting the People’s Bank of China cut its reserve ratio requirement (RRR) last week.

This signals policy easing, though we suspect it will help stabilise recently slowing growth, rather than stimulating a new leg higher.

Covid and vaccines

Renewed waves of Delta — and potentially Omicron — mean markets are wary of the potential for lower growth into Q1 2022.

On Delta, we are seeing a sharp drop in new cases in Austria, which shows restrictions are working and demonstrates that each subsequent wave is having a lower impact.

The UK looks to be the first developed-market country seeing Omicron emerge. The government has reinstated some restrictions, fearing of the impact of a surge in cases off an already high base.

Omicron data out of South Africa has been encouraging. Case growth rate has been slowing in Gauteng province. The testing positivity rate is dropping and hospitalisations are not significantly accelerating. That said, the data can be volatile. The picture is looking more positive than a week ago, but it is still too early to draw conclusions.

Initial Omicron studies confirm the view that existing vaccines provide a lower degree of immunity. But we are yet to understand their effect on severe Covid.

Pendal Focus Australian Share Fund

Now rated at the highest level by Lonsec, Morningstar and Zenith

A UK study (yet to be peer reviewed) indicated a patient with two Pfizer doses had 35% immunity from Omicron 25 weeks after the shots, versus 50-60% from Delta. This rose to 75% with the booster, but it remains unclear how long that will last. Booster dose penetration will play a key part of supressing the spread of Omicron.

The risk to markets is that even a milder variant of Covid can put pressure on hospital systems through sheer weight of numbers if it breaks through vaccine protection.

The positive scenario would be that vaccines remain effective in providing immunity to severe Covid and the disconnection between cases and hospitalisations remains high.

It is still too early to make a call on which way this breaks due to the younger age profile of current Omicron clusters and the time it will take to assess data on hospitalisations.

Economics and policy

US rates

US inflation data came in slightly higher than expected. Headline CPI rose 0.8% in November versus consensus expectations of 0.7%. It is running at 6.9% year-on-year. Core inflation rose 0.5%, in line with consensus, and is running at 4.9% year-on-year.

Autos were a strong component of the rise. But even adjusting for this, inflation pressures are broadening. The rental component did not accelerate, which was a small positive.

The data should not affect the Fed decisions this week.

The key issue for the pace of tightening next year is the durability of inflation.

This will be driven by whether supply chain issues ease and by tightness in the labour market, which depends on the participation rate.

If inflation remains persistent and starts to flow through to wages, real rates will need to move higher.

Sustainable and

Responsible Investments

Fund Manager of the Year

This would weigh on the valuation premiums in growth stocks. We have seen evidence of this in recent weeks in the underperformance of the more speculative growth stocks.

China

Property developer Evergrande effectively defaulted on public debt for the first time. We expect to see the government manage the liquidation, enabling the transfer of unfinished projects to other developers that have the resources to complete them.

Policy makers continued to signal an easing through a reserve ratio requirement cut.

The key debate for China next year is whether policy easing is aimed at accelerating growth, or to prevent a further slowdown while leaving the growth rate at a subdued level.

At this point we lean more to the latter.

The Covid-zero policy and need to manage inflation constrain Beijing’s ability to use traditional measures to promote growth.

Markets and stocks

Equity market volatility last week fell from the extreme highs of the previous week, underpinning a recovery.

But the more speculative high-growth names did not bounce back as much as the broader market.

This suggests the potential for higher real rates is weighing on these names. Larger-cap tech names have been less affected by this issue, given they are seen as higher quality.

Australian equities did not bounce back as hard as the US. Resources and energy saw a limited recovery despite the bounce back in commodity prices.

About Crispin Murray and Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia. Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Find out more about Pendal Focus Australian Share Fund here.

Here are the main factors driving the ASX this week according to our head of equities Crispin Murray. Reported by portfolio specialist Chris Adams

OMICRON concerns and a pivot from US Fed chair Jerome Powell on inflation triggered a risk-off move in markets last week.

Equities fell — the S&P/ASX 300 lost 0.62% and the S&P 500 was off 1.17%. Longer-dated bond yields fell, as did the oil price. The VIX volatility index spiked above 30% for the first time since February.

In equities we saw a sell-off in more speculative tech stocks and a rotation towards more defensive value names.

The market has moved quickly to price in a great deal of fear over Omicron and the pace of rate hikes. There is a reasonable chance these concerns may be overdone – though there are still a lot of questions around Omicron.

However a combination of falling volatility, a strong rebound in the US economy supporting earnings, easing concerns over Quantitative Easing tapering, and receding uncertainty around Omicron could very well see markets rally through to January.

Covid and vaccines

The market has two current concerns around Covid.

The first is the Delta variant’s ongoing winter wave in the northern hemisphere. The second is the potential implication of the Omicron variant.

Delta wave

On the latest Delta wave, there are signs leading countries in eastern and central Europe are seeing the usual peaking of cases two-to-three months in. This is positive, suggesting that targeted restrictions can be effective.

But we are also likely to see this wave roll into other parts of the continent. Cases are rising rapidly in France and southern Europe. The UK is moving back towards the top end of its range of cases. US data is distorted by Thanksgiving, but early indicators suggest a renewed wave is building there.

So far hospitalisations remain contained in the higher-vaccinated countries.

Omicron

Omicron adds a new level of complexity to the outlook.

South Africa had extremely low case levels prior to Omicron’s emergence. A new wave had been expected, similar to what we’re seeing in Europe. But this low level of existing cases has allowed Omicron to become the dominant strain relatively easily.

The question is whether it can also become dominant in countries where Delta cases are already more prevalent.

Pendal Focus Australian Share Fund

A high-conviction equity fund with 16 years of strong performance in a range of market conditions

We also don’t know whether Omicron will lead to a different pattern to Covid waves — extending them or increasing the amplitude.

We continue to wait for the data on Omicron. There are three areas to watch for:

1) Ability to bypass vaccines

Data on the difference in immune antibodies could be available within a week. It seems likely existing vaccines may be less effective at preventing infection, while still conferring some immunity.

It may mean booster jabs are needed sooner than expected. Imminent data is unlikely to show the degree of protection against a severe Covid infection. Actual observations of hospitalisations will likely provide the indicator on this.

2) Transmissibility

There are suggestions from a number of scientists that Omicron has a substantially higher “R0” (rate of transmissibility) than Delta. There are a number of reasons why it may be too early to definitively conclude this. These include the low level of previous cases in South Africa, the fact that Omicron is easier to detect than Delta and heightened focus on the new variant which means testing levels are far higher.

There are also suggestions it has been around for longer than a month, so we are seeing some catch up in cases reported. It may be that we need to see how Omicron spreads in a country where Delta is already prevalent to reach a conclusion.

3) Severity

We will be watching the proportion of Omicron patients that require hospitalisation and for how long. There has been speculation based on observations in South Africa that hospitalisations rates are lower than Delta. These reports say hospitalised patients are experiencing fewer respiratory issues and are able to leave hospital sooner. More data is needed.

Observations on Omicron severity are prompting speculation that Covid may be evolving into a more endemic-like virus. This might enable the world to build immunity without severe health implications and possibly signal the beginning of the end of the pandemic.

We believe it is far too early to buy into this thesis.

For one thing, cases reported so far have been in younger, healthier people who are more social and have lower vaccination rates. As cases spread into more vulnerable age cohorts we may see higher hospitalisations — so it is too early to make this call.

The upshot is that there are a lot of unknowns and potential outcomes.

The difference in reaction to Omicron and the pandemic’s beginning is notable.

In early 2020 governments and markets were slow to recognise the threat. Now we are seeing a sharp negative reaction with governments re-imposing travel restrictions and markets turning risk-off.

The risk scenarios can cut both ways here. There is a reasonable chance the outcome won’t be as bad as feared. Therefore we are mindful of not becoming overly cautious.

Follow Pendal podcast

The Point on ![]()

Quick, actionable insights for investors

The US could be the key country to watch. Case numbers have been low, potentially making it easier for Omicron to establish itself as the dominate strain. Half of Americans are either unvaccinated or had their second shot more than six months ago, with fading immunity.

The final issue to keep in mind is the durability of the booster shot. We are watching Israel’s experience to see if immunity proves more durable after the booster.

Economics and policy outlook

Powell’s pivot and inflation

In his testimony to Congress, Fed Chair nominee Powell said Quantitative Easing (QE) could finish “a few months sooner” than previously indicated. He also said it was time to retire the term “transitory”. The market has moved to expecting QE to be over by end of March.

The bond yield curve flattened materially as a result. The spread between 10-year and two-year US government bonds dropped from above 100bps to about 75bps as the longer-dated yields fell.

Is it no coincidence that Powell has become more hawkish on inflation a week after his nomination for a second term as Chair.

He will need Republican votes to be confirmed by Congress — a hawkish tone on inflation helps this. Inflation is also a factor in Biden’s waning popularity and dealing with it has become a policy imperative.

We are therefore mindful of the political angle to this shift and cautious on reading too much into it.

Powell pushed rates higher in 2018 on concerns over Trump’s fiscal stimulus and almost flattened the yield curve — though he shifted quickly after equities fell sharply in response.

The great irony is that in the week “transitory” was retired, inflation expectations – reflected in the pricing of two-year forward inflation swaps — dropped materially. This partly reflects confidence that the Fed will not be complacent. Omicron concerns and some supply chain improvements are also factors.

This meant real interest rates actually rose on the week – bond yields were down, but inflation expectations were down further. This may explain the decline in tech growth stocks – particularly at the more speculative end – given the correlation with real rates.

Economic outlook

Faster tapering means reduced additional easing, not tightening. QE has not really been a driver of the Main Street economy beyond the effect on confidence of rising share prices. As a result faster tapering should not have a material impact on the economy.

However it could see rotation away from the more speculative end of markets towards more predictable and yield sensitive stocks.

It is also important to note that faster tapering does not necessarily mean rates go up sooner. The market is pricing two-to-three hikes in CY22. This may prove too many. Powell has always been very clear that the pace of tapering and rate hikes should not be connected.

Finishing QE earlier gives the Fed optionality. If the economy is slowing and inflation easing it is unlikely to go hard on hiking rates. The lesson of 2018 is to be wary of being too hawkish.

Payrolls

Payroll data was disappointing. The US economy added 210,000 new jobs in November — well below consensus expectations of 550,000.

However there are a number of offsetting factors which means this does not necessarily signal a definitive change in the labour market trajectory.

Sustainable and

Responsible Investments

Fund Manager of the Year

There were material, positive revisions for previous months and the latest household survey reported 1.1 million new jobs.

There were also possible early signs of workers returning to the market with the participation rate among 25-54 year olds rising 0.5%. Again, it is too soon to get too excited by this. About half the 5 million drop in workers in the last two years remains unexplained.

Headline wage growth slowed to 0.3% month on month. But underlying measures indicate it stayed at the 5-6% level, so this remains a live issue.

Markets

Concerns over tighter US monetary policy and Omicron saw de-risking in equities, exacerbated by a seasonally illiquid period in the market.

Equity market volatility, as measured by the VIX, spiked into the 99th percentile of readings. It is hard to see it moving much higher unless we see a major adverse development on Covid.

There has been a high correlation between spikes and the VIX and market corrections this year.

On this basis markets could recover into the year’s end as volatility falls. However lingering caution may see large cap and rate sensitives lead, rather than more speculative growth names.

The latter’s sell-off continues, as reflected in the relative performance of the ARK Innovation ETF as well as the BNPL, cloud, gaming and cyber security sectors versus the broader NASDAQ.

Resources are interesting — they have been tied to China growth revisions where news may be becoming slightly more positive.

In terms of sentiment we are watching credit spreads. The high yield spread over investment grade bonds has shifted up from 80bps to 130bps on recent concerns.

Oil is another indicator to watch. A combination of recent reserve releases and Omicron has seen West Texas Intermediate fall back to August’s levels — when Delta concerns peaked. If the market believes we’ll get a continuation of the global economic recovery next year we should see this bounce.

Sentiment in equity markets is softening with around 50% of stocks in the S&P 500 hitting a 20-day low. However it is not signalling capitulation.

We see scope for a recovery into January, on a combination of:

- Lower volatility

- Omicron concerns receding

- Falling 10-year bonds

- Continued strong economic environment, particularly in US

- Expectations of easing policy in China

- Still good liquidity

- A seasonally illiquid market

Covid remains the main caveat to this view.

About Crispin Murray and Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia. Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Find out more about Pendal Focus Australian Share Fund here.

When rates start going up, how far will they go? It’s a question Pendal’s head of government bond strategies TIM HEXT has been thinking about a lot lately

WE have just released our latest Income and Fixed Interest Quarterly Report (contact a Pendal business manager for a copy) and I have spent my time recently questioning market pricing.

Right now nearly everyone is focused on the timing of RBA rate hikes versus market expectations.

The near-term performance of funds we manage is all about solving that one.

But the issue that’s been occupying my mind — and I write about in the Quarterly — is the long-term question of the terminal rate of a hiking cycle.

In other words, when rates do start going up, how far will they go?

I think rates will move up to 1.5% in 2023. Inflation will peak around 3% in early 2023 before tapering off back to 2.5%, led by modest goods price deflation kicking in.

This will see the RBA happy to leave cash rates there for at least a year or more.

Find out about

Pendal’s Income and Fixed Interest funds

Consensus is that 1.5% cash rates will see out the rate-hike cycle. The logic is that a 2% rise in mortgage rates would hit the economy hard.

But as the decade unfolds and investment remains strong, real yields could move modestly positive once more.

That would mean cash rates closer to 2.5% than 1.5% and bond rates nearer 3% than 2%.

I doubt markets will factor this in for some time, but it’s a risk to consider for long-term asset allocators.

Of course in the meantime — with cash stuck near zero — it is expensive to be too underweight fixed interest.

Now rates have backed up, fixed interest is once again playing its part as a defensive asset.

For those of us managing portfolios, we must play the short term while keeping in mind the medium term.

We’ll leave long term to the custodians of superannuation funds whose time horizons allow for it.

About Tim Hext and Pendal’s Income & Fixed Interest boutique

Tim Hext is a Pendal portfolio manager and head of government bond strategies in our Income and Fixed Interest team.

Tim has extensive experience in banking, financial markets and funding including senior positions with NSW Treasury Corporation (TCorp), Westpac Treasury, Commonwealth Bank of Australia, Deutsche Bank, Bain & Co and Swiss Bank Corporation.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia.

Find out more about Pendal’s fixed interest strategies here

About Pendal

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

In 2023, Pendal became part of Perpetual Limited (ASX:PPT), bringing together two of Australia’s most respected active asset management brands to create a global leader in multi-boutique asset management with autonomous, world-class investment capabilities and a growing leadership position in ESG.

What’s the role of fixed income in portfolios right now? Here’s a quick snapshot from Pendal’s head of income strategies AMY XIE PATRICK

IT’S been a tough year for fixed income.

Fuelled by bouts of inflation tantrum, a rise in yields drove one-year total returns on most major fixed income benchmarks into the red by early November.

Only high-yield benchmarks delivered positive returns — mostly due to the recovery of credit spreads that took place at the start of the year.

Though this doesn’t help the average fixed income allocation much, since the risk-and-return profile of global junk debt is more akin to equities than fixed income.

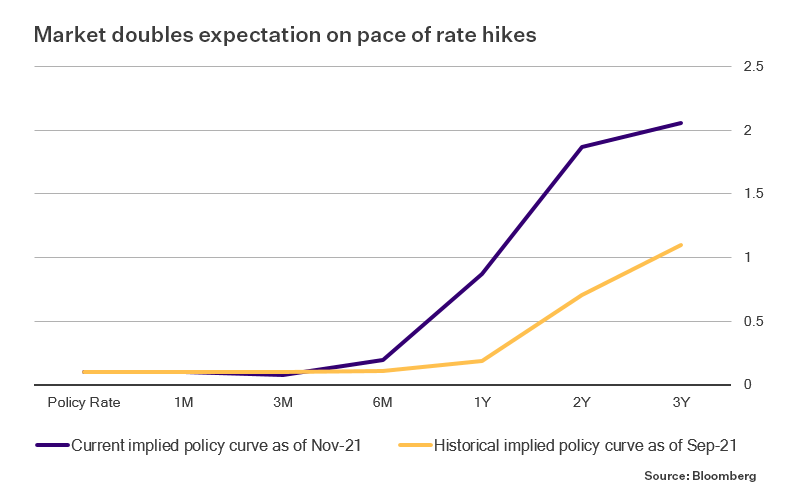

The market currently out-hawks all central banks, pricing in a steeper path of normalisation than policy makers are willing to concede.

As you can see in the below chart, since the end of September the market has doubled its expectation around the pace of rate hikes in Australia.

That leaves a decent buffer for central banks to get “pulled-to-market” if they are wrong — and a lot of room for yields to fall if they are right.

Such a steep path of rate hike expectations leave little room for error. The latest Omicron Covid variant is a case in point.

Let’s also not forget the efficiency of markets that run ahead of hiking cycles.

From 2004 to 2006, Alan Greenspan’s Fed raised policy rates by 425bps. Over the same period, yields on US 10-year Treasuries rose a mere 33bps.

Any hiking cycle now would be hard pushed to even match half of Greenspan’s pace.

Even with inflation still rising, fixed income has an important role to play.

Its negative correlation to equity markets delivered a poor return outcome for the asset class in 2021.

But overall, portfolios have benefited from the tear that risk assets have been on.

In times of market stress that negative correlation will prove invaluable.

Compared to a year ago, 10-year government bonds in Australia now provide 85bps more yield.

There is now a fatter cushion to absorb any macro stumbling blocks lurking on the horizon.

About Amy Xie Patrick and Pendal’s Income and Fixed Interest team

Amy is Pendal’s Head of Income Strategies. She has extensive expertise and experience in emerging markets, global high yield and investment grade credit and holds an honours degree in economics from Cambridge University.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia. The team oversees some $20 billion invested across income, composite, pure alpha, global and Australian government strategies.

Find out more about Pendal’s fixed interest strategies here

About Pendal Group

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

Pendal’s head of equities Crispin Murray and his team have access to Omicron analysis from a variety of leading virologists and epidemiologists. Here are Crispin’s observations so far.

NEAR TERM, the emergence of Omicron is concerning because the sheer number of variations in the virus — notably the spike protein which the vaccines target — are very likely to render vaccines less effective in preventing the spread of the virus.

The Moderna CEO said as much in the Financial Times this week.

The transmissibility of Omicron is likely to be greater than previous variants, but it is still unclear to what extent.

Although the number of reported cases in South Africa has accelerated far faster than Delta, it’s unknown how long the variant was already seeded in the community or subject to super-spreading events.

The datasets are still too small to be more definitive.

We believe comments that Omicron may be less virulent — that it will lead to fewer hospitalisations — are premature.

Pendal Focus Australian Share Fund

Now rated at the highest level by Lonsec, Morningstar and Zenith

This view is based on observations in South Africa rather than data from a trial. It can be influenced by a variety of factors such as age and the number of previous infections a patient person has had.

Mitigating this uncertainty are a number of observations:

1. Thanks to South African scientists we’ve identified this variant at an earlier phase than Delta. This limits the level of seeding in other countries, containing the spread and buying time for a scientific response

2. While vaccines may no longer be as effective in stopping transmissibility, there is a reasonable expectation they will continue to be effective in lessening the effects of the virus through the response of B and T cells — which play an important role in our body’s Covid defence system

3. The advent of anti-viral medicines should reduce the health consequences of those infected

4. The impact of each subsequent wave has been less material on the economy as responses become more targeted and people become more attuned to the risks

5. We are seeing accelerating economic momentum globally. This is different to what we saw when the Delta wave began to emerge in May and June.

Corporate responses to date have been along similar lines: they will wait until we have more data and a better understanding before taking any potential responses to the new variant.

What if current vaccines prove to be ineffective against Omicron?

The mRNA suppliers say they have already been working on new versions of the vaccine.

They indicate it could take 100 days to develop an Omicron vaccine — and about six months to become available at a mass level, subject to regulatory approvals.

About Crispin Murray and Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia. Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Find out more about Pendal Focus Australian Share Fund here.

Here are the main factors driving the ASX this week according to portfolio manager Jim Taylor. Reported by portfolio specialist Chris Adams

THE emergence of Omicron halted a week of positive news flow in its tracks.

Before Thanksgiving in the US, the market had been gaining confidence that the Chinese government was taking steps to underpin economic growth and stem the risk of a sharper slowdown.

News that Jay Powell would be appointed for a second term as Fed Chair — coupled with talk of faster tapering —bolstered the view that the US central bank was not falling behind the curve on inflation.

Then Friday saw a sharp risk-off trade after the WHO flagged the Omicron mutation as a variant of concern.

As a result the S&P 500 ended the week down 2.18% and the S&P/ASX 300 lost 1.64%.

Stocks related to the re-opening fell far further. Commodities were generally down (except iron ore), and US 10-year government bond yields fell 7bps.

COVID and vaccines

Prior to the WHO announcement, Covid concerns remained centred on Europe.

Austria re-entered full lockdowns, though other countries resisted this move. Hospitalisations continue to remain very low.

Although the health outcomes in Europe remain encouraging, this wave is being felt in stock prices. Even prior to the Omicron news, re-opening stocks in Europe were under pressure from the latest wave and consequent mobility restrictions.

Find out about

Pendal Focus

Australian Share Fund

Crispin Murray,

Head of Equities

The risk with Omicron is that it may make vaccines less effective.

It has a spike protein dramatically different to the original variant on which the vaccines were based. The spike protein is the component of the virus that binds to cells. Because of these mutations Omicron could have increased resistance to vaccines — plus greater transmissibility and severity compared to other variants.

The WHO said it will take weeks to better understand the efficacy of current vaccines as well as Omicron’s severity in terms of health outcomes and hospitalisation.

Vaccine maker BioNTech said initial lab results on the variant could come within two weeks. Pfizer indicated a variant-tailored vaccine could be available about 100 days after genetic sequencing.

In Australia mobility rates continue to rebound at a similar rate in Victoria and New South Wales. This is despite the fact that new daily cases in Victoria have plateaued at a far higher rate than NSW.

Macro and policy

Jerome Powell was reappointed for a second term as chair of the US Federal Reserve. Lael Brainard replaced Richard Clarida as vice chair.

The markets welcomed this news. Powell’s more hawkish bent (compared to Brainard) is seen as reducing the risk that the Fed would be too loose in the face of inflationary pressure.

This narrative was reinforced by signals from other Fed members that it could withdraw support more quickly from the economy to deal with rising inflation.

Vice Chair Clarida noted they will be watching data between now and the December meeting closely and may have a discussion about accelerated tapering if warranted.

Fed Governor Christopher Waller called for tapering to be possibly done by April, making way for a possible interest rate hike in Q2.

The key argument remains that a combination of easing supply bottlenecks, slowing wage gains on the back of rising labour participation and faster productivity growth ought to bring inflation down without the Fed having to act more aggressively.

Three to six months ago an acceleration of tapering would have been met with great concern by the markets.

But rhetoric from the Fed governors will be priming the market for just such a move. Tapering could be over by mid-March. Rate rises in 2022 are now baked in by the market — perhaps as early as June.

US data prints were generally positive. US Initial Jobless Claims came in at 199,000, well below consensus. It is expected to reverse to about 250,000 before resuming a downward trend to pre-Covid levels of about 210,000.

A re-rebound in existing homes sales continues, rising from 6.2 million to 6.34 million. Consensus expectations were 6.2 million.

The percentage of cash buyers — as opposed to mortgages — has risen from 19% to 24% year-on-year.

Low inventory means prices are still soaring, up 18% annualised in the three months to October. This ensures the rent component of the CPI will continue to rise for some time yet.

Markets

There have been some notable developments in commodity markets.

Over the weekend Peruvian Prime Minister Mirtha Vasquez announced her government planned to close four gold and silver mines that have had conflicts with local communities.

Peru is the world’s second-biggest copper producer after Chile, accounting for about 10 per cent of 2021 global production.

OPEC+ has indicated they see the release of strategic reserves by countries such as the US as unjustified in current conditions and they may respond with higher production when they meet next week.

Sustainable and

Responsible Investments

Fund Manager of the Year

Bonds had been selling off very calmly and modestly over the course of the prior week, rallying very strongly on Friday with US 10-year government yields up 15bps.

More generally the underperformance of the non-mega cap tech stocks in the US continued last week.

There was very little in the way of stock-specific news for the Australian bourse.

Materials continued their recent strength with increasing comfort that China was addressing the growth problem they have engineered.

The iron ore miners were among the week’s best performers. Fortescue Metals (FMG) was up 11.12%, Mineral Resources (MIN) +5.20%, Rio Tinto (RIO) +4.66% and BHP (BHP) +4.33%.

AMP (AMP, -11.89%) was the weakest on the ASX 100 after management flagged impairment charges.

Tech names were generally weaker. Friday’s Omicron news saw re-opening stocks such as Qantas (QAN, -8.76%) hit hard.

About Jim Taylor and Pendal Focus Australian Share Fund

Drawing on more than 25 years of experience investing in top-performing Australian companies and a background in accounting, Jim manages our Long/Short Fund and co-manages our Imputation Fund. He is a Chartered Accountant with membership of the Australian Institute of Chartered Accountants.

Pendal Focus Australian Share Fund is managed by Crispin Murray. The fund has beaten its benchmark in 12 years of its 16-year history (after fees), across a range of market conditions. Find out more about Pendal Focus Australian Share Fund here.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

A monthly insight from James Syme and Paul Wimborne, managers of Pendal’s Global Emerging Markets Opportunities Fund

WE have seen high inflation prints across the world in recent months.

Meanwhile, volatility in interest rate expectations and sell-offs in government bond markets are testing the resolve of central banks — which have mostly been sticking to the view that the current inflation spike will prove to be transitory.

In some developed markets there has been significant pressure on central banks, including those of the UK, Australia and Canada.

The governor of the Bank of England said their monetary policy committee would “have to act” if inflation in the prices of consumer goods and energy fed through to inflation expectations.

The Reserve Bank of Australia had to abandon its yield curve control policy (which had pegged 2024 government bond yields at 0.1%).

The bank had stopped supporting the policy as fears about inflation were priced into bond markets through October, with yields on the April 2024 government bond rising from 0.05% at the start of October to 0.78% at the end of the month.

Similarly, October saw the Bank of Canada catch rates and bond markets by surprise, ending its government-bond purchase program and accelerating expectations for when it might start hiking policy interest rates.

Find out about

Pendal Global Emerging Markets Opportunities Fund

Emerging market central banks have not been immune from this shift.

Many emerging markets have variously seen inflation data that is high or above expectation, and sharp shifts in central bank policy.

Brazil

Brazil has seen an aggressive sell-off of government bonds in recent months, which intensified in October. Inflation data has been difficult with both September and October CPI printing above 10% YoY.

Inflation expectations continue to increase, with the five-year breakeven inflation rate now over 6%, despite the central bank (the BCB) sticking to its 2024 CPI target of 3%.

More fundamentally, fears of a water crisis (which would have inflationary implications for power pricing) or a relaxation of fiscal discipline ahead of the October 2022 presidential election have undermined confidence in BCB’s inflation-fighting credibility.

This has happened despite BCB hiking rates and the bond market pricing in continued aggressive policy rate increases.

Year-to-date, BCB has hiked the policy interest rate from 2% to 7.75%. But the shorter end of the yield curve has also moved higher by 3% or more, leaving the BCB much to do.

As we have discussed in previous commentary, this is very much driven by the inflationary outlook. The Brazilian real looks to us fundamentally cheap and the external financial position of Brazil remains very strong.

That does not, however, prevent the drag on economic activity and corporate earnings from a one-year real interest rate (adjusted for inflation expectations) of over 6%.

Central and Eastern Europe

Another region where, for different reasons, there has been a sharp shift in inflationary and interest rate expectations is Central and Eastern Europe.

The greatest shift has been in Poland, where an Australia-style move in the front-end of the yield curve forced the central bank to hike rates from 0.1% to 0.5% in the October meeting (when a hold had been expected) and then to hike again from 0.5% to 1.25% in the November meeting (when a much smaller hike had been expected).

The Czech central bank has also shocked markets with the speed and scale of rate hikes, with a tightening phase that began with a move from 0.25% to 0.5% in June 2021 accelerating to leave policy interest rates at 2.75% at the time of writing.

Sustainable and

Responsible Investments

Fund Manager of the Year

It is not clear that Russia has serious inflationary problems, but the central bank, the CBR, has a reputation as one of the most orthodox and hawkish central banks in EM and has steadily hiked ahead of expectations through the year.

But there are bright spots…

Amid this pattern of central banks potentially getting behind the inflationary expectations curve and having to then hike rates aggressively to catch up, there are bright spots.

Some emerging markets, despite seeing higher fuel prices and economic recoveries, have seen moderate increases in inflation and have even been able to leave policy interest rates on hold at levels that are overall stimulative.

This group absolutely includes India, which has seen inflation tick lower in recent months (to 4.35% in the year to September), allowing the Indian central bank to remain on hold, with policy rates at 4%.

Other markets have also been able to remain on hold, including Indonesia (on hold at 3.5% with inflation to October of just 1.7%), and South Africa (on hold at 3.5% with inflation to September of 5.0%).

US monetary policy impact

Clearly the overall direction of financial conditions in emerging markets will also be driven by the direction of US monetary policy.

The US Federal Reserve has kept short-term interest rates near zero. But bond markets are steadily pricing in interest-rate increases in 2022, with futures suggesting the most likely increase is two 0.25% increases next year.

As those have been priced in, with shorter-dated bond yields rising, the longer-dated part of the yield curve has been falling.

Interestingly, this is the opposite of what occurred during the taper tantrum in 2013, when the long end sold off in response to reduced asset purchases by the Fed.

Emerging markets respond well to higher growth and higher commodity prices — and poorly to higher US interest rates and increased volatility.

With global growth strong and the Fed still committed to easy monetary policies, emerging economies and emerging markets are well placed.

But we’ll need to see the volatility in rates and yields calm down before investors can be more confident about the asset class.

About Pendal Global Emerging Markets Opportunities Fund

James Syme and Paul Wimborne are senior portfolio managers and co-managers of Pendal’s Global Emerging Markets Opportunities Fund.

The fund aims to add value through a combination of country allocation and individual stock selection.

The country allocation process is based on analysis of a country’s economic growth, monetary policy, market liquidity, currency, governance/politics and equity market valuation.

The stock selection process focuses on buying quality growth stocks at attractive valuations.

Find out more about Pendal Global Emerging Markets Opportunities Fund here

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.