The outlook for major ASX-listed miners is looking positive again. But investing in resources is now more nuanced with issues such as ESG and China. Pendal’s BRENTON SAUNDERS explains

- Outlook for miners is mixed and heavily dependent on China

- But conditions should be right for a rebound next year

- ESG issues come to the fore in AGM season

WITH a combined market cap of $190 billion, BHP, Fortescue and Rio Tinto are all top 15 companies and key pillars of the ASX.

They’re hard to avoid if you’re investing broadly in the ASX.

Iron ore is the major export of all three. When the price of the ore was above $US230 a tonne, the big three miners were reaping the benefits, and all three paid shareholders a special dividend this year.

But iron ore prices have dropped back to around $US100 a tonne and the share prices of the big three have underperformed in recent months.

So what’s ahead?

“The landscape for resources is pretty dynamic at the moment,” says Saunders, an experienced geologist and manager of Pendal’s natural resources portfolio.

“Investing in resources is now much more nuanced and that has to do, in large part, with how the Chinese economy has evolved.

“The outlook is also dependent on how demand and supply evolves for some of the major commodity groups, particularly energy.

“To that extent, the outlook for the large cap miners is looking more positive again, in part because they have sold off as much as they have, as has their principal commodity, which is iron ore.”

Improved outlook for 2022

“I think it’s reasonable to think that in the first half of next year — and probably the second quarter — that the sector will improve again, albeit off a highly eroded base,” Saunders says.

The next few months could still be bumpy though.

Pendal Focus Australian Share Fund

Now rated at the highest level by Lonsec, Morningstar and Zenith

Chinese demand for iron ore and steel is low and could get worse, Saunders says. But most of the negative sentiment is priced in.

“Also, this time of year is difficult for China from a pollution perspective as the country heads into winter and generates a large temperature inversion layer across the big metropoles, making pollution worse,” Saunders says.

“Typically at this time of year, there are restrictions on production. Then we move into Chinese New Year and after that there’s normally a rebound.”

But 2022 will be different with the Winter Olympic Games being held in Greater Beijing in February and the government determined to keep pollution levels down.

“The Beijing region does host a large percentage of the country’s steel production, so that will probably be depressed until the end of February,” Saunders says.

“Then as we move into spring, we could see an aggressive rebound that could be concurrent with stimulus and a lightening of some of the regulatory imposts on the property sector.

Follow The Point podcast: Actionable insights from Pendal portfolio managers

“There should also be a partial restocking of the steel value chain that’s been quite heavily denuded.”

ESG issues come to the fore in AGM season

It was an interesting AGM season for the major miners — in large part thanks to the evolution of environmental, societal and governance (ESG) concerns, votes on remuneration and the emergence of vocal, activist investors.

Faced with volatile commodity prices, ESG challenges and plenty of activist investors, two of the big three — BHP and Fortescue Metals — have fronted shareholder in recent weeks. Rio’s AGM is later in the year.

One of the key benefits of Fortescue’s AGM is that it allows shareholders to learn more about what Fortescue Future Industries (FFI), the company’s green offshoot, is doing, says Saunders.

2021 Money Management of the Year Awards

Pendal Australian Shares Portfolio

Winner – SMA Australian Equities

Pendal Property Investment Fund

Winner – Australian Property Securities

“It’s been a bit frustrating for shareholders because there isn’t a lot of transparency in FFI,” he says.

“The FFI business is evolving fast and it’s difficult to keep track of,” he says. “But at AGMs we learn more about it and this year was no exception.”

Two weeks ago, at the Fortescue meeting, chief executive Elizabeth Gaines revealed FFI had an unspent allocation of funds from last year, and the offshoot plans to spend $US600 million on clean energy projects this year.

BHP’s AGMs have demonstrated how the company has evolved and has been paying more attention to ESG issues.

“Over the last three years at its AGM, BHP has faced at least one quite controversial ESG proxy, or proposal,” Saunders says. “And over those three years they have become much more embracing of them because BHP’s ESG process in the background has evolved.

“BHP has actually approved some of these proposals, though when these issues first emerged several years ago the approach from them initially was to throw their hands up in the air and say that’s not feasible, or it’s unrealistic.

“There’s been quite a big evolution along the ESG lines specifically for BHP to become more aligned with some of the objectives of these action groups.”

About Brenton Saunders and Pendal MidCap Fund

Brenton is a portfolio manager with Pendal’s Australian equities team. He manages Pendal MidCap Fund, drawing on more than 25 years of expertise. He is a member of the CFA Institute.

Pendal MidCap Fund features 40-60 Australian midcap shares. The fund leverages insights and experience gained from Pendal’s access to senior executives and directors at ASX-listed companies. Pendal operates one of Australia’s biggest Aussie equities teams under the experienced leadership of Crispin Murray.

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

Higher interest rates will eventually work, but they’re not working just now, argues Pendal’s OLIVER GE. That could mean bonds become even better value next year

- Inelastic demand and supply mean rates work differently

- In likely scenario, bonds a good place to invest

- Find out about Pendal fixed interest capabilities

WHAT if higher interest rates worked against cutting inflation?

Or at least had little effect on demand — making rate hikes ineffective in the fight against inflation?

“I want to talk about the idea that in an environment where demand is still reasonably strong, interest rate hikes effectively do nothing,” says Oliver Ge, an assistant portfolio manager with Pendal’s income and fixed interest team.

“Rather than cooling things down, they might be pushing them back up,” Oliver says.

The idea comes down to the notion of elasticity of demand – a measure of the change in the demand for a product in relation to the change in its price.

Elastic demand means there’s a big change in quantity demanded when there’s a change in price.

Inelastic demand is the opposite – little change in demand no matter what the change in price.

“When households are in decent shape, as they are today – when you have wages growth at decade highs and unemployment at near record lows, and savings are still plentiful – you end up with an environment where people are much less sensitive to price changes,” Ge says.

Covid lowered our price sensitivity

“During lockdowns, people were happy to pay for a whole range of goods like laptops, gardening tools, toilet paper,” notes Ge. “Consumer demand collectively channelled its momentum into household items.

“Suppliers jacked up prices but there was still plenty of demand.

“While we have moved on from Covid, we haven’t moved on from this sort of low-price sensitivity environment.

“The money has only moved on from chasing goods to instead chasing services.

“The bottom line is that the elasticity of demand is very, very low. It’s basically inelastic.”

Services are labour intensive – hospitals, hotels, cafes, restaurants, airlines employ hundreds of thousands of people, Ge says.

“Even though we’ve added a million people to the workforce since 2020, businesses are still experiencing labour shortages.

Find out about

Pendal’s Income and Fixed Interest funds

“It’s a Covid hangover. People want to go out. They don’t want to be the people serving everyone else.”

“As a central banker you see inflation rising and your natural instinct is to raise rates. But the usual transmission mechanism is broken,” he says.

Transmission breakdown

Previously lifting interest rates would trigger tighter lending and refinancing, and companies would cut back on costs, including staff, says Ge. That would lead to higher unemployment and that would dampen inflation.

“But today, businesses aren’t really cutting back on staff. They’ve struggled to find and retain the right people, and thus don’t’ now want to lose them,” Oliver explains.

“Instead what they’ve chosen to do is compromise in other areas – say reduce the quality of ingredients if they are a restaurant.

“Or they are just passing the cost through to the consumer. And people are happy, at present, to pay the higher prices. Until they’re not.”

This process demonstrates an inelasticity of supply, as well as demand.

“So you have this relationship where higher rates are hurting businesses and to cope, they’re lifting prices, which consumers are paying.

“There’s a breakdown in the transmission of monetary policy to the employment market. In a very counterintuitive way, hikes are making things worse, not better.”

What it means for fixed interest investors

Higher interest rates will eventually work, but they’re not working just now, argues Ge.

“It will be the straw that breaks the camel’s back. It’s hard to see the stresses today but when it comes, it will come suddenly.

“I think there will be a fairly aggressive breaking point around the middle of next year. The Reserve Bank could realise too late, and then desperately try to reverse the rate rises.

“At which point bonds could become very good value. They are already good value, but that’s when the have the potential to become even better value.”

About Oliver Ge and Pendal’s Income and Fixed Interest boutique

Oliver Ge is an assistant portfolio manager with Pendal’s Income and Fixed Interest (IFI) team.

Oliver works on developing and running key quantitative investment models, and acting as trading support for the team. Oliver received his Bachelor of Commerce (Finance) from the University of Sydney and is also a CFA Charterholder.

Pendal’s IFI boutique is one of the most experienced and well-regarded fixed income teams in Australia. In 2020 the team won the Australian Fixed Interest category in the Zenith awards.

The invests across income, composite, pure alpha, global and Australian government strategies.

Find out more about Pendal’s fixed interest strategies here

About Pendal Group

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

Despite noise about another inflation surge and higher rates, central banks look to have price rises well under control, argues Pendal’s OLIVER GE

- Fears of 70s inflation rerun unfounded

- Why bonds, why now? Pendal’s income and fixed interest experts explain

- Find out about Pendal fixed interest capabilities

FOR or all the recent headlines about rising costs, oil prices and interest rates, there’s little to suggest inflation is anything other than under central bank control, argues Pendal’s Oliver Ge.

US inflation numbers came in higher than expected for August, marking the first acceleration in price rises since February.

The data sparked a number of news reports extrapolating the monthly figures to warn of a second wave of inflation and a new round of interest rate rises.

But a closer look reveals that the global economy is a long way from the narrative the news media are pushing, says Ge, a portfolio manager with Pendal’s Income and Fixed Interest team.

“This kind of stuff is going to get a lot of clicks.

“Thirteen consecutive months of disinflation in the US and now we’ve had the first tick up, and somehow the media is extrapolating that the Federal Reserve is on the case and it’s all going to end in the crapper.”

Ignoring noise created by business media is an important lesson for investors, says Ge.

“There’s a lot of commentary on a possible ’70s-style, second wave of inflation. And how if that were to happen, central banks would need to react.

“But I don’t believe we’re going down that path. We’re not even close to a rerun of the 70s.”

The dual inflation shocks of the 70s and 80s have gone down in investing folklore as a tumultuous period of skyrocketing prices, spiralling wage rises and damaging unemployment.

“Some people are concluding that we’re on the path to repeat the 70s/80s experience when inflation hit almost 15 per cent in the US.

“But there are a few reasons why we’re not likely to get a re-run of what happened 50 years ago.”

Ge says the 70s crisis was unique and brought about in part because the US economy was running very hot.

“In 1973, the US economy was growing at 7.6 per cent — three times higher than what it is today.

“It also had a highly unionised labour force. And then it got whacked with two major oil shocks.

“The difference is that back then, the US was highly oil dependent, and it also was experiencing a massive devaluation of its currency. Put the two together and it triggered a big wave of inflation.

“At the same time, the US was home to a sizeable manufacturing sector, which was very highly unionised. They had explicit mandates in contracts that matched pay to inflation.”

Find out about

Pendal’s Income and Fixed Interest funds

But he says the environment today is very different.

“The US is no longer energy dependent — in fact it is an exporter of oil. Unionisation is no longer widespread. There are none of the original catalysts that prompted the blowout.”

The central banks also play a different role today, says Ge.

“Central banks today have a very explicit inflation fighting objective — they are not going to suddenly drop rates because inflation is coming down like they did in the 70s.

“They will choose to err on the side of caution. That means we’re going to see an environment where rates are going to be higher for longer.

“The picture I’m painting isn’t sexy — but it’s real. And it should comfort investors.”

About Oliver Ge and Pendal’s Income and Fixed Interest boutique

Oliver Ge is an assistant portfolio manager with Pendal’s Income and Fixed Interest (IFI) team.

Oliver works on developing and running key quantitative investment models, and acting as trading support for the team. Oliver received his Bachelor of Commerce (Finance) from the University of Sydney and is also a CFA Charterholder.

Pendal’s IFI boutique is one of the most experienced and well-regarded fixed income teams in Australia. In 2020 the team won the Australian Fixed Interest category in the Zenith awards.

The invests across income, composite, pure alpha, global and Australian government strategies.

Find out more about Pendal’s fixed interest strategies here

About Pendal Group

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

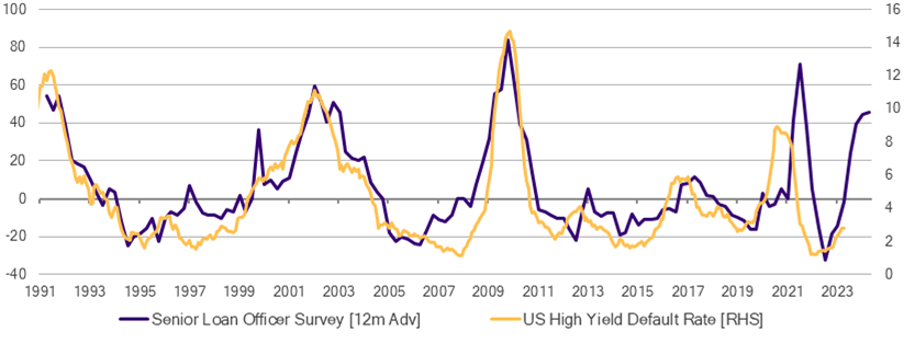

The risk of recession appears to be sidelined for now, but investors may be overlooking one factor, argues Pendal’s OLIVER GE

- Tightening credit threatens business viability

- Bonds best protection from recession

- Find out about Pendal fixed interest capabilities

A NUMBER of US banks and analysts have walked back their recession predictions in recent weeks.

But there are still worrying signs in the business sector, cautions Pendal’s Oliver Ge.

Much of the discussion about higher interest rates has focused on the impact of bigger mortgage repayments for homeowners.

But tightener credit conditions and stricter collateral requirements for business are likely to have a more significant impact on the economy, argues Ge, an assistant portfolio manager with Pendal’s income and fixed interest team.

“There’s a growing narrative that the economy can navigate through this tightening cycle without derailing growth and causing havoc to the jobs market.

“It can be hard to argue against this. Despite 400 basis points in hikes from the RBA, economic activity remains reasonably robust and domestic employment is incredibly strong.

“But the economic brakes applied via interest rates is very gradual.

“What often gets overlooked is that there is another transmission mechanism — the tightening of lending standards — that carries perhaps more importance to the business cycle.”

As interest rates lift, banks will increase the perceived credit risk of all borrowers. To mitigate these risks they will impose stricter income and collateral requirements on their borrowers.

Small businesses are generally more reliant on bank loans given that they have fewer alternative sources of funding.

“It’s not the cost but access to credit that matters,” says Ge.

“Small business owners rely on a flow of working capital to pay their suppliers and employees. At the moment, the banks are happy to supply that. But should lenders’ outlook on the economy turn, they may have to cut off those lines of credit”.

“That’s when businesses will be forced to pare back on labour and supplies. That spills over into the rest of the ecosystem — that’s when you get that pain.

Tighter lending in the US

As you can see below, there’s evidence that banks are already tightening lending in the US, where the Federal Reserve conducts a quarterly survey of the biggest banks to assess lending terms.

“Lending standards have tightened significantly, comparable to historic highs,” says Ge.

“Business cash buffers are running out and you’ll likely see a wave of defaults over the course of the next six-to-nine months.

“Ultimately, that is where we’re headed. But it’s not something people are factoring into their forecasts.”

A tightening of lending standards has real potential to push the global economy into recession, says Ge.

“Whatever happens in the US will filter through to the rest of the world. There’s no way that Australians can somehow insulate themselves.

“At the start of the year, people were tossing up between a soft and hard landing. The hard landing scenario has faded from people’s memories.

“But the prospect of recession is still very much out there.”

Find out about

Pendal’s Income and Fixed Interest funds

About Oliver Ge and Pendal’s Income and Fixed Interest boutique

Oliver Ge is an assistant portfolio manager with Pendal’s Income and Fixed Interest (IFI) team.

Oliver works on developing and running key quantitative investment models, and acting as trading support for the team. Oliver received his Bachelor of Commerce (Finance) from the University of Sydney and is also a CFA Charterholder.

Pendal’s IFI boutique is one of the most experienced and well-regarded fixed income teams in Australia. In 2020 the team won the Australian Fixed Interest category in the Zenith awards.

The invests across income, composite, pure alpha, global and Australian government strategies.

Find out more about Pendal’s fixed interest strategies here

About Pendal Group

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

The current yield curve inversion — where short-dated bonds yield more than long-dated bonds — may not mean a recession is imminent, argues Pendal’s OLIVER GE

- Yield curve inversion traditionally predicts recession

- But transitory inflation could be an alternative explanation

- Find out about Pendal fixed interest capabilities

THE prospect of stagflation has been the talk of markets in recent weeks as rising short-term interest rates push the bond yield curve into inversion, flagging a sign of impending recession.

An inverted yield curve — where shorter-dated bonds yield more than longer-dated bonds — is an important indicator for investors.

Longer-dated bonds usually pay higher interest rates to compensate for their increased risk over time. But right now short-term interest rates are moving closer to — and even higher than — long term rates.

That’s important because it’s traditionally a harbinger of recession.

But with a strong global economy, low unemployment and benign equity market conditions, analysts have been looking for an alternative explanation for the inversion other than a surprise descent into stagflation and recession.

Oliver Ge, a portfolio manager with Pendal’s Income and Fixed Interest team, says the yield curve inversion may also be explained by expectations that current inflationary pressures are only short term.

“There are two ways this can be interpreted,” says Ge.

“In one sense you can see it as a sign of recession. But I don’t think that’s the case”.

“Instead, what we’re seeing in the market is that short-dated bond yields are higher because they carry a premium to their longer-dated counterparts to compensate investors for bearing higher near-term inflation risk. That’s what’s driving the inversion”

Stagflation is a worry for markets because it means a toxic combination of rising prices and lower economic growth.

Find out about

Pendal’s Income and Fixed Interest funds

But Ge says the conditions for stagflation are not present in the global economy.

“There’s 1.8 jobs available for every person who wants a job in the US,” he says.

“That’s more jobs per person than there has ever been.

“In Australia, the workforce is in a stronger position than it was pre-pandemic. We’ve recovered all the job losses we had in the pandemic and created more and there are still labour shortages.

“Some say it’s about borders and immigration — but this is a global phenomenon. The overriding theme across the world is employment is fantastic. There are jobs for everyone.”

Ge says in such a strong economic environment, it’s difficult to believe that a few interest rate hikes will stop businesses hiring.

Returning to recession so soon after the global pandemic downturn would also be surprising from an historical view, he says.

“Looking back, you see a recession every eight to 10 years or so. The yield curve is telling us there is a recession around the corner but that’s almost never the case historically.

“Maybe you get a bit of a slowdown, but you don’t get the end of days that some people are calling for.”

About Oliver Ge and Pendal’s Income and Fixed Interest boutique

Oliver Ge is an Assistant Portfolio Manager with Pendal’s Income and Fixed Interest (IFI) team.

Oliver works on developing and running key quantitative investment models, and acting as trading support for the Income & Fixed Interest team. Oliver received his Bachelor of Commerce (Finance) from the University of Sydney and is also a CFA Charterholder.

Pendal’s IFI boutique is one of the most experienced and well-regarded fixed income teams in Australia. In 2020 the team won the Australian Fixed Interest category in the Zenith awards.

The invests across income, composite, pure alpha, global and Australian government strategies.

Find out more about Pendal’s fixed interest strategies here

About Pendal Group

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Bonds have the potential to provide a positive investment return even during central bank rate-hiking cycles. Pendal’s OLIVER GE explains how

RATES go up, bonds go down. It’s an investing truism that has become ingrained in our thinking.

But what if, in fact, bonds had the potential to provide an investment return during central interest rate hiking cycles?

That’s the finding from research by Oliver Ge, a portfolio manager with Pendal’s Income and Fixed Interest team.

Monetary policy tightening cycles are actually kinder on bonds than people believe, Ge says.

“The key is that it depends on how much is priced into the bond market at the point central banks start lifting rates.

“Looking at history, an investor who buys bonds at the moment of the first rate hike in a cycle and sells at the last rate hike actually gets quite a substantial return.”

The finding demonstrates that there is a lot more nuance to the classic doctrine of “rates go up, bonds go down”, says Ge.

Since the 1990s there have four rate hiking cycles in Australia, each averaging an increase of 2.25 per cent to the RBA’s policy rate, he says. The annualised bond return over the same period was more than 4 per cent.

“The compelling story is don’t ignore bonds when rates are rising — they can still give you mid-single digit returns.

“That’s quite significant in a market where equities are negative.”

Find out about

Pendal’s Income and Fixed Interest funds

The explanation for why bonds had positive returns over those times is based on two factors, he says.

First, rate hikes do not materialise unannounced. The RBA broadcasts its decisions in advance and a considerable portion of future hikes are already in the price of the bonds before the first hike.

This means a 25 basis points move higher rarely translates into a direct one-for-one change in the yield of a bond, says Ge.

“During the 2009-2010 cycle, the RBA moved the policy rate up by 175 basis point from 3 per cent to 4.75 per cent. Over the same horizon, a five-year Commonwealth government bond moved up by around only 35 basis points,” he says.

The second thing is the pace of rate hikes. In principle, the more gradual a central bank tightens, the more income a bond can accrue to offset would-be losses, says Ge.

By magnitude, the largest tightening cycle over the last 30 years was 300 basis points, but it occurred over a six-year window, allowing bonds to maintain mid-single digit returns per annum despite the absolute quantum of moves.

“Right now, the market expects the RBA to kick off their hiking cycle in June, ending in mid-2024 at a peak rate north of 3 per cent.

“This puts the expected bond experience somewhere between the last two hiking cycles, both of which resulted in a positive outcome for fixed income investors.

“While a negative shock can’t be ruled out, the likelihood of further inflation surprise is diminishing.

“There’s already a lot priced into bonds. And it’s reasonable to say that we’re closer to the end of this higher rates move than we are at the start.”

About Oliver Ge and Pendal’s Income and Fixed Interest boutique

Oliver Ge is an Assistant Portfolio Manager with Pendal’s Income and Fixed Interest (IFI) team.

Oliver works on developing and running key quantitative investment models, and acting as trading support for the Income & Fixed Interest team. Oliver received his Bachelor of Commerce (Finance) from the University of Sydney and is also a CFA Charterholder.

Pendal’s IFI boutique is one of the most experienced and well-regarded fixed income teams in Australia. In 2020 the team won the Australian Fixed Interest category in the Zenith awards.

The invests across income, composite, pure alpha, global and Australian government strategies.

Find out more about Pendal’s fixed interest strategies here

About Pendal Group

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Ultra-loose monetary policy is creating exceptions to risk and reward – and bringing opportunities for investors seeking better returns for their cash. OLIVER GE explains

- Bonds paying better returns than bank deposits

- 4x returns when held to maturity

- Find out more about Pendal fixed interest funds

THE link between risk and reward is a staple of investment theory.

But ultra-loose monetary policy as the Reserve Bank of Australia seeks to support the economy’s pandemic recovery is creating some exceptions to that age-old rule.

Investors who choose the safety of a government bond (held to maturity) are now offered better returns than a nominally higher-risk bank term deposit, says Oliver Ge, a portfolio manager with Pendal’s Income and Fixed Interest team.

“If you’re willing to hold government bonds for a year — just like you would with a bank term deposit — you’ll get four-to-six times more money than you’ll get from a bank,” says Ge.

Cash is an important asset for many investors. It provides security and flexibility, and importantly it offers protection from being forced to sell assets in a downturn.

But for investors seeking income, it can offer very poor returns.

Find out about

Pendal’s Income and Fixed Interest funds

“You go to one of the big banks and they’re offering about 0.25 per cent interest rates on a one-year term deposit — $25 on a $10,000 investment. That’s not a lot.

“But if you’re happy to lock your money away for a year, why not try a government bond? A one-year Australian government bond is paying 1 per cent, so you’re getting four times as much money.

“Unless you think the Australian government is going to default — and as long as you hold to maturity — you’re better off giving them your money.”

Ge points out that state government bonds can offer even better returns, with the Western Australian semi-government bonds offering returns as high as 1.6 per cent.

Protection against downturn

Bonds provide a further advantage over term deposits because alongside guaranteed income and capital protection, they offer protection against an economic downturn.

“If there was a catastrophic event like a Covid version two and the RBA decides not to lift rates, these bonds could return a lot more as they will rise in value,” says Ge.

“Bonds are just insurance policies that always pay you — and when things blow up, they pay you even more.”

Ge says the anomaly exists because the RBA is providing very cheap funding to the banks, meaning they do need to compete for deposits in the market and can keep deposit rates artificially low without affecting the financing of their lending businesses.

“They have so much money they can afford to do this,” he says.

By contrast, government bonds are issued into a competitive global market and rates are set by investor demand.

Ge says the anomaly is likely to stay in place as long as the banks have access to cheap funding.

“This is a genuine opportunity to get a lot more juice with the same or better safety – assuming you hold to maturity,” says Ge.

About Oliver Ge and Pendal’s Income and Fixed Interest boutique

Oliver Ge is an Assistant Portfolio Manager with Pendal’s Income and Fixed Interest (IFI) team.

Oliver works on developing and running key quantitative investment models, and acting as trading support for the Income & Fixed Interest team. Oliver received his Bachelor of Commerce (Finance) from the University of Sydney and is also a CFA Charterholder.

Pendal’s IFI boutique is one of the most experienced and well-regarded fixed income teams in Australia. In 2020 the team won the Australian Fixed Interest category in the Zenith awards.

The invests across income, composite, pure alpha, global and Australian government strategies.

Find out more about Pendal’s fixed interest strategies here

About Pendal Group

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Could Russia’s invasion of Ukraine prompt Chinese action in Taiwan? That’s not likely in the medium term argues Pendal’s OLIVER GE

ALARM bells are ringing in the East.

As fighting intensifies in Ukraine’s urban core, Chinese jets have entered Taiwan’s air defence zone, leading some to speculate that it’s only a matter of time before we see People’s Liberation Army boots on the ground.

At times like this it’s understandable that investors pondering their exposure to Russia’s invasion of Ukraine might also think harder about the China-Taiwan stand-off.

Pre-election positioning among Australian politicians pulls the China-Taiwan situation into even sharper focus for local investors.

However a Chinese invasion of Taiwan is a very low probability event in the short and medium term.

Near term, the Chinese Communist Party has other priorities at stake.

President Xi has promised to rectify growing domestic discontent over diminished living standards. Housing affordability and employment opportunities are key focal points for the CCP leadership.

They do not have time for major external distractions.

In the medium term, Taiwan’s support from the US remains crucial. Remember that Taiwan (but unfortunately not Ukraine) is of great strategic importance to Washington.

Its proximity over major shipping lanes and dominance in semiconductor manufacturing has seen consecutive US administrations pledge Taiwan military support in the event of a war.

China has no appetite for a direct confrontation with the US.

In the longer term these reasons above do not negate the possibility of a future conflict.

A unified China is arguably the biggest political objective of the CCP. China’s dominance in the region and military capacity continues to build.

But for now the carrot of economic cooperation remains the preferred policy over brute force.

About Oliver Ge and Pendal’s Income and Fixed Interest boutique

Oliver Ge is an Assistant Portfolio Manager with Pendal’s Income and Fixed Interest (IFI) team.

Oliver works on developing and running key quantitative investment models, and acting as trading support for the Income & Fixed Interest team. Oliver received his Bachelor of Commerce (Finance) from the University of Sydney and is also a CFA Charterholder.

Pendal’s IFI boutique is one of the most experienced and well-regarded fixed income teams in Australia. In 2020 the team won the Australian Fixed Interest category in the Zenith awards.

The invests across income, composite, pure alpha, global and Australian government strategies.

Find out more about Pendal’s fixed interest strategies here

About Pendal Group

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Even with the promise of meeting bond interest payments, the risk of contagion from Evergrande has increased as investors rotate away from equities and high yield credit. Pendal’s Oliver Ge explains what’s next

CHINESE property giant Evergrande has staved off default on the first of many payments covering some $US300 billion in debt.

But investors are still holding their breath to see whether Beijing will step in and what happens next.

Pendal’s Oliver Ge says the fallout on the domestic Chinese market would be minimal in the event of a controlled default.

Evergrande — which owns 1300 projects in 280 cities according to Bloomberg — represents a small 0.2% portion of China’s loan system, says Ge, an assistant portfolio manager with Pendal’s Income and Fixed Interest team.

“Right now Beijing has not been materially vocal on a rescue package, preferring instead that the company quietly sells down its assets and makes investors, suppliers and homeowners whole before quietly exiting the industry.

“But the issue is that Evergrande is unable to deliver on the ‘quietly’ part since they have no credibility in the financial system.

“No one will lend them any money. The only way they can quickly raise cash is to mark down their existing inventory of apartments.”

Find out about

Pendal’s Income and Fixed Interest funds

Markdowns as a high as 25% have been quoted, says Ge.

But going down this path means the rest of Evergrande’s peer group would have its asset book revalued too –prompting the sell-off we’ve seen so far.

Broader impact for investors

Until recently the contagion was limited to Asia and resource names such as BHP and Rio Tinto, which supply the iron ore for Chinese property projects.

Today, even with the promise of meeting bond interest payments, the risk of contagion has increased as people rotate away from equities and high-yield credit altogether, Ge says.

And the market implication for offshore USD bonds is significant.

“Right now Evergrande USD bonds are trading around 20-25c to the dollar (yuan).

“Default is almost guaranteed at those levels and other domestic peers will invariably get dragged into the sell-off.

“The current Asian high-yield default rate is around 3%. This could rise to 9% if Evergrande and its subsidiaries officially miss their debt obligations going forward.

“In lieu of a policy u-turn from the Federal Reserve, government bonds will likely thrive in this regime.”

Evergrande is just the tip of a large iceberg in China right now, says Ge.

“There is an ongoing vicious cycle that won’t stop until Beijing decides to scale back their social inequality reforms.

“Loose monetary and fiscal can help but it won’t be enough to offset existing headwinds.”

About Oliver Ge and Pendal’s Income and Fixed Interest boutique

Oliver Ge is an Assistant Portfolio Manager with Pendal’s Income and Fixed Interest (IFI) team.

Oliver works on developing and running key quantitative investment models, and acting as trading support for the Income & Fixed Interest team. Oliver received his Bachelor of Commerce (Finance) from the University of Sydney and is also a CFA Charterholder.

Pendal’s IFI boutique is one of the most experienced and well-regarded fixed income teams in Australia. In 2020 the team won the Australian Fixed Interest category in the Zenith awards.

The invests across income, composite, pure alpha, global and Australian government strategies.

Find out more about Pendal’s fixed interest strategies here

About Pendal Group

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

The Strait of Hormuz blockade wasn’t an isolated shock. Understanding what was already in motion is the key to reading what comes next, argues Pendal’s AMY XIE PATRICK

- Sticky inflation persists; central banks must stay hawkish

- Oil disruption, not conflict, drives market risks

- Find out about Pendal Dynamic Income Fund and Pendal Monthly Income Plus fund

STICKY and rising inflation was already a problem before the global economy encountered the most recent oil shock.

In the US, core Personal Consumption Expenditure — the Fed’s preferred measure of underlying inflation — has been stuck around 1% above the Fed’s 2% target since mid-2024.

Core PCE itself hasn’t been at 2% for five years.

In Australia, reflation was already underway, causing the RBA to initiate a new hiking cycle.

Markets are now pricing a peak cash rate of around 4.75%, roughly 40 basis points above the peak of the entire 2022-23 hiking cycle.

Demand has been running ahead of supply in both the US and Australia.

By the RBA’s own estimates, the output gap – the difference between how much the economy could produce without creating inflation and how much it is producing – is positive and accelerating in Australia.

Meanwhile, consumer demand in the US has remained resilient while a new cap-ex cycle is in full swing, led by AI and technology.

Higher oil prices never guarantee higher core inflation, but this robust demand backdrop gives businesses the pricing power to pass on higher costs to customers.

The job of central banks is to ensure that the inflation coming over the next few months doesn’t embed itself into persistent expectations.

Separate the conflict from the oil disruption

It’s easy to conflate the geopolitical conflict with the economic disruption, but they can – and likely will – diverge.

Ceasefire talks could extend indefinitely (just as the Ukraine conflict did), and at some point markets move on regardless.

What matters for economies is whether oil and energy supply chains normalise.

That could happen through alternative shipping routes or new sources of supply coming online, independent of diplomatic moves.

In a scenario where the conflict drags on but oil logistics recover, we can expect a higher-for-longer oil price.

At the same time, a severe demand-destruction scenario, where fuel shortages cause genuine economic contraction, becomes a much smaller tail risk.

That’s why at Pendal we are less focused on ceasefire odds and more on the following data:

1. Vessel flows: Limited, but not zero

While commercial traffic through the Strait of Hormuz is still down sharply since February, it has started to recover.

The Bloomberg graph below shows rolling 7-day transits rising at the end of April (compared to 758 on February 28).

2. Tanker indices: Elevated, but coming off the boil

The next graph below shows baltic dirty (crude oil) and clean (LNG) tanker indices.

Tanker indices are market price benchmarks for hiring oil and gas tankers. They act as a real‑time barometer of stress or recovery in the global energy supply chain.

This data suggests early signs that oil logistics are beginning to normalise from the peak of disruption.

Shortages will still be felt in parts of the world, but the probability of severe demand destruction is falling as supply chains adapt.

Our view: Inflation above recession

With demand resilient and the worst supply scenarios becoming less likely, we believe the dominant risk is inflation running higher for longer — not a growth collapse.

The positive output gap that existed before the shock means businesses can protect margins. Corporate profitability should therefore hold up reasonably well in the near term.

We expect the uncertainty of inflation data in coming weeks and months to drive episodes of bond-market volatility.

However, as long as corporate profitability and economic activity remain healthy, equity markets should be able to confidently weather this volatility.

Indeed, once tail risks become the central case, risky assets tend to stabilise and move on.

Fuel inventories are the key variable to watch for when the scales tip from inflation to growth concerns.

Inventories have also not changed meaningfully yet due to the lag between when oil leaves the Middle East to when it reaches Australia in the form of ready-to-use fuel.

In-bound shipments of fuel have also been supported by Asian refining nations running down their own excess reserves to capture higher margins.

However, those refining nations will turn towards protecting their own supplies over supernormal profits if the shortfall of global oil supply persists.

Portfolio positioning: Minimal duration, selective on credit, tactical on equities

The Pendal team has cut portfolio duration back to minimal levels.

With growth resilient and inflation elevated, duration doesn’t offer compelling risk-reward.

The market is pricing two more hikes from the RBA, and no policy change from the Fed.

We’d rather preserve flexibility and add duration when either inflation fears are more meaningfully priced into yields, or the data mix shifts enough to suggest that bond markets have already discounted the worst.

On credit, we made an active decision to de-risk in early March – not on a prediction of what would happen, but because the asymmetry was clear.

If markets normalised, we could replenish exposures from primary issuance, likely at more attractive levels than pre-war.

If conditions deteriorated sharply, the additional cash gave us the flexibility to either protect liquidity or selectively buy into forced selling.

As it turns out, credit markets have remained functional and primary activity has picked up. We’ve used that window to rebuild some exposures, but we’re being deliberate about it.

Australian credit markets have been well supported in recent weeks due to the higher all-in yield that corporate bonds now offer.

However, most of that rise in yields is due to risk-free rates reflecting inflation concerns, rather than credit spreads reflecting higher credit risks from corporate borrowers in a more uncertain macro environment.

It’s vital to treat the interest rate-setting and the credit exposure of the portfolio as two separate and intentional choices.

The two can behave very differently depending on the economic and market backdrop.

When adding corporate bonds to our portfolios, we want to ensure that we are being compensated specifically for taking on extra credit risk.

On equities, fundamentals remain reasonably supportive in the near-term.

Positive demand conditions, the ability to pass through costs, and the stabilising effect of tail risks being well-flagged all point in the same direction.

The key watch item remains the consumer tipping point.

If demand destruction comes from fuel shortages or the cost of living itself, the equity story changes. We’ll be watching the data carefully for early signs of that transition.

Find out about

Pendal Dynamic Income Fund

Amy Xie Patrick,

Head of Income Strategies

Bottom line: Higher for now, with eyes on demand

As we can see, the oil shock met with pre-existing economic trends that were bond-bearish: sticky inflation above central bank targets and resilient economic growth.

This backdrop does not afford the RBA the luxury to “look through” the supply-side shock, and in line with market predictions has again raised interest rates by 25 basis points to 4.35%.

While we want to see greater bond market discounting of inflation headwinds, we continue to monitor the ability of both businesses and consumers to deal with rising costs.

In the meantime, our income portfolios continue to access core income through Australian credit markets, as well as having the option to tactically engage in return boosters such as Australian equities as market sentiment recovers from recent volatility.

In a cycle where the inflation and growth mix can shift quickly, preserving the option – rather than the obligation – to add interest rate exposure is one of the most valuable tools that we have.

About Amy Xie Patrick and Pendal’s Income and Fixed Interest team

Amy is Pendal’s Head of Income Strategies. She has extensive expertise and experience in emerging markets, global high yield and investment grade credit and holds an honours degree in economics from Cambridge University.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia. The team oversees some $20 billion invested across income, composite, pure alpha, global and Australian government strategies.

Find out more about Pendal’s fixed interest strategies here

About Pendal Group

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.