Historically high valuations don’t mean markets cannot keep going up. CRISPIN MURRAY explains what’s driving markets – and the risks to watch for

- Large parts of US market not excessively over-valued

- Potential risks: stagflation, retail slowdown, fading AI theme

- Find out about Pendal Focus Australian Share fund

- Watch Crispin Murray’s new Beyond The Numbers bi-annual ASX outlook

EQUITY markets are trading at historical highs – but can continue grinding higher if key risks facing the US economy remain contained, says Pendal’s head of equities Crispin Murray in a new webinar.

In the US, the S&P 500 is trading at about 23 times earnings, while the NASDAQ is around 28 times.

“That’s right at the high end of those historic ranges,” says Murray in his latest Beyond The Numbers bi-annual ASX outlook.

“It means markets are vulnerable if there is a dramatic change – whether it’s earnings or the economy.”

That said, valuations are not uniform across the market.

Excluding the five-biggest names reduces the S&P 500’s PE to about 21 times – still high, but not extreme – while an equal‑weighted S&P 500 sits closer to 17 times, near historical averages, says Murray.

“That’s telling you that a large part of this US market is not excessively valued, and it’s very much a concentration in those tech-related names.”

Meanwhile Australian shares powered 11 per cent higher over the six months to September, despite dipping into correction territory during that period as growth and liquidity outweighed policy uncertainty.

(Scroll down for Crispin’s take on ASX reporting season.)

“It’s certainly been a roller coaster … that just highlights how the market is not particularly efficient in pricing,” says Murray.

“At Pendal, we believe you make money by anticipating change and taking advantage of a market that has become very focused on the short term.”

The risks to watch

Risks to the current market rating include:

- The looming threat of stagflation driven by policy headwinds

- Market concerns about US fiscal sustainability

- A risk that the AI boom fades

- Any potential removal of liquidity if retail flows slow or corporations reduce stock buy-backs

US government policy is at the core of the challenges.

Lower immigration is curbing population growth – a key driver of GDP – while tariffs are feeding through to prices, with roughly 40 per cent of their impact already visible in consumer prices, says Murray.

Meanwhile, monetary policy remains very tight.

“What that means is the outlook for the economy is quite different today than where it was at the beginning of this year.

“Looking into the fourth quarter, US growth is set to be below 1 per cent, inflation heading towards 4 per cent.

“It does look a lot like stagflation – and clearly, if we did have that tipping point in the economy, earnings go down, and the market won’t sustain its current multiple.”

Positive drivers remain in place

Still, that scenario appears unlikely.

“Corporate profitability continues to be good,” points out Murray.

“This is important, because it means companies still have the ability to invest, and it also means that they’re less likely to undertake substantial job-cutting programs.

“There’s been enormous growth in the data centre and the power area of the economy – and that is helping prop up growth.

“Consumers have seen their net worth rising dramatically over the last few years, and that’s estimated to support growth by between half and 1 per cent.

“And the final issue, which I think is probably the most important for now, is that the policy environment – which has been negative – is turning more constructive for growth.

“Five rate cuts are priced into the market, fiscal stimulus from the budget Bill next year is estimated to be close to 1 per cent positive, and clearly the US has been set up to the electoral cycle and ensuring the economy is in good shape ahead of the mid-terms.

“So, we don’t think we do cross that tipping point, but it’s clearly a major risk.”

Lessons from ASX reporting season

In Australia, several themes stood out in the recent full-year ASX earnings season, including high levels of post-result volatility.

Somewhat unusually, the best-performing sectors during reporting season were not correlated to earnings.

Resources stocks were buoyed by optimism around China, while gold stocks lifted on concerns about government financing and central bank buying.

On the negative side, earnings were a driver of underperformance – led by building materials and steel where ASX companies with exposure to the US suffered weakening demand.

“Overall, earnings revisions weren’t that exciting but when you dig down into it, most of the negatives were quite stock specific.

Pendal Focus Australian Share Fund

Now rated at the highest level by Lonsec, Morningstar and Zenith

“It was companies that were not necessarily executing as well as they should [or] those exposed to the US.

“Outside of those names, though, most companies were either reasonably comfortable with the outlook or actually quite positive.

“So generally speaking, I think the outlook for earnings is stable to slightly positive as a result of what we saw in that earnings season.

“We still get mid-single-digit earnings growth, which means returns aren’t exciting in Australia, but we still get a reasonable outcome.”

Data centres a good way to play AI

One question on investors’ minds is the prospect of the AI boom continuing.

“There is scepticism that the money being spent is not generating a return – and it’s something we’re watching carefully,” Murray says.

“But one thing I’ll emphasise is that the spend is real – and the people who are investing have the money.

“These hyper scalers – Amazon, Google, Microsoft, Meta and Oracle – have the financing to spend this money, and they believe they are getting a return.

“Consumers are also increasingly using these products.”

Murray says the world has a shortage of “compute” – an industry term for the processing power, memory and storage needed to perform calculations and run applications – and this is an opportunity for Australia and particularly local data centres.

“One of the challenges with investing and building data centres in Australia is access to land, access to capability, getting planning approval and getting power access.

“These things mean that there is a structural under-supply of capacity in Australia, and the companies that can deliver it are very well positioned.

“We still believe the market underestimates the confluence of not just AI demand, but the requirement for companies to move to the cloud to enable themselves to take part in utilising AI to run their businesses better.”

About Crispin Murray and the Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia. Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions.

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

Bond markets are reflecting a narrowing gap between developed and emerging market fundamentals. That could mean opportunity, argues Pendal’s Global Emerging Markets Opportunities team

- Historically narrow gap between emerging and developed market fundamentals

- Bond markets are paying attention

- Find out about Pendal Global Emerging Markets Opportunities fund

EMERGING markets are thought of as the riskier end of the equity asset class.

This risk is perceived to come from a variety of interlinked causes:

- Weaker governance and more volatile politics

- Lower economic resilience

- More extreme economic and financial cycles

Certainly the history of the asset class is one of booms and busts, while emerging debt markets have an unenviable history of defaults.

Looking at the world in 2025, though, we think the gap between the fundamentals of developed markets end emerging markets is historically narrow – perhaps narrower than it has ever been.

Developed markets face tighter conditions

The UK, where we are based, is seeing long bond yields gap higher in the face of chronically slow economic growth and a yawning fiscal deficit.

Real disposable income has grown at an annualised rate of only 0.6% since 2008. Despite extremely loose monetary and fiscal policy, GDP growth for 2025 is forecast at only 1.2%.

France is about to lose its third prime minister in 18 months, with no political consensus on how to address excess government debt (currently 114% of GDP) and a large fiscal deficit.

In Japan, inflation has eased pressure on government debt in the short term, but national finances remain extremely strained in the big picture.

The US, of course, is the ultimate developed market from a currency point of view.

But the inflationary effects of tariffs and doubts about the government’s commitment to inflation targeting monetary policy are also stressing markets.

The pattern across major developed markets is one of long bond yields pushing higher even as growth expectations deteriorate.

Bond investors are watching EMs

Meanwhile, many emerging markets have either lower growth and inflation, or higher growth and inflation but with a clear commitment to inflation targeting.

Bond investors are paying attention.

The JP Morgan EMBI Global index of USD-denominated emerging market government bonds is trading at its lowest spread over developed market bonds since 2013.

Borrowers are also reacting. Some more-indebted frontier markets are seeking to refinance USD denominated debt into Chinese RMB to take advantage of lower yields.

Equity investors, meanwhile, are taking a different view.

The 12-month forward price/earnings ratio of MSCI World (the developed markets equity index) has expanded to 21.6x, while MSCI EM Index is priced at only 14.3x.

Find out about

Pendal Global Emerging Markets Opportunities Fund

This EM valuation discount of 33.9% is well below the long-term historical average discount of about 20%.

This is despite the IMF’s GDP growth forecasts for the G7 falling to the lowest non-crisis level since 2002.

What it means for investors

As a team of EM investors with experience going back to the 1990s, we are very aware of the international and domestic political and policy risks in emerging markets.

The last year we saw a coup attempt in Korea, military conflict between India and Pakistan, challenging headlines everywhere around tariffs and trade, and the court-ordered removal of a prime minister in Thailand after less than a year in office.

Still, we believe the political and governance risk gap between emerging and developed markets is narrower than at any time we have seen.

Bond markets are paying attention.

Equity markets are not yet.

We remain very positive on the outlook for emerging market equities.

About Pendal Global Emerging Markets Opportunities Fund

James Syme, Paul Wimborne and Ada Chan are co-managers of Pendal’s Global Emerging Markets Opportunities Fund.

The fund aims to add value through a combination of country allocation and individual stock selection.

The country allocation process is based on analysis of a country’s economic growth, monetary policy, market liquidity, currency, governance/politics and equity market valuation.

The stock selection process focuses on buying quality growth stocks at attractive valuations.

Find out more about Pendal Global Emerging Markets Opportunities Fund here

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

Here are the main factors driving Australian equities this week, according to portfolio manager JACK GABB. Reported by head investment specialist Chris Adams

- Watch now: Crispin Murray’s bi-annual Beyond The Numbers webinar

- Find out about Pendal Focus Australian Share Fund

US inflation data and soft employment figures are amplifying expectations for rate cuts and supporting equity markets.

Bullish statements from software giant Oracle on demand for cloud-based services helped drive US indices to a record high last Thursday, before a slight easing.

The S&P 500 ended up 1.6% for the week, while the NASDAQ gained 2.1%.

Chinese equities – and the yuan – continued to rally with the Hang Seng up 4%. Japan’s Nikkei rose 4.1%.

European equities were quieter. The Euro Stoxx 50 gained 1.4% as the European Central Bank held rates steady. An easing cycle appears over for now.

Australian equities were also muted, with the S&P/ASX 300 gaining 0.1%.

Bonds rallied – particularly at the long end – with the key US 10-year falling briefly below 4%. That helped drive US mortgage rates lower.

However it’s worth recalling parallels with 2024.

Back then the 10-year yield hit a low point on September 16 – the eve of a Fed rate-cut decision.

(The Fed will announce its latest rates decision this week, early Thursday morning Australian time).

US macro and policy

Markets are fully pricing in a 25bp cut this week.

Another two-to-three consecutive cuts are also expected – despite current policy settings arguably providing little in the way of restrictive policy.

The Fed argues neutral rates are lower, but financial flows are rampant and consumer spending data belies perceived weakness in the jobs market.

Implied rates for December hit their lowest level since May and now sit at 3.629% versus 3.772% this time last week.

Softer jobs data drove the change, while inflation data was regarded as tame.

Six-month Treasury notes are now at 3.83% – 50 basis points below current implied rates. However a repeat of 2024’s 50-point September cut is seen as unlikely.

Inflation data

The producer price index (PPI) was lower than expectation, but the core consumer price index (CPI) accelerated to +0.35% in August (+4.2% annualised). Year-on-year core CPI rose to 3.1%.

Markets focused more on the job revisions. But by itself the CPI print does not appear to support a cut, let alone three-to-four in quick succession.

That leaves a risk of a repeat of 2024 when the Fed cut by 100 points and inflation expectations jumped.

The 10-year yield subsequently rose by 118 points, sending mortgage rates higher.

That risk is arguably amplified this year by perceptions of Fed independence, with a cut potentially interpreted as politically driven.

In good news for the Fed, the PPI (and jobs) data was weak.

PPI Final Demand fell to -0.12% month-on-month, versus +0.3% expected and 0.7% prior. Within that, services (which dominate the index) fell 0.16%.

By itself, the data is supportive of a cut. But data has tended to yo-yo and September or October’s print seems likely to see pricing rebound higher.

While the data does not measure import pricing (hence not tariffs directly), PPI for finished core good rose to 0.3% (3.8% annualised).

Jobs data

Besides CPI and PPI data, the labour market provided the key economic data of the week.

Initial jobless claims were a touch higher (263k versus 235k expected and 237k prior), but payrolls for the 12 months to March were revised down 911k.

This was well above most estimates and not far from the feared 1 million mark.

To put this in context, the monthly data estimated job growth of 2.35m over the 12-month period, an average of 196k/month. The reality was 1.44m, or 120k/month.

This is still ‘preliminary’ – the final monthly accounting isn’t due until February next year.

Based on what happened in February this year, the final revisions will again be revised materially – but to a less negative position.

All in all, it isn’t exactly confidence-inspiring.

Other data

Other economic data was limited.

The University of Michigan sentiment index did weaken/miss at 55.4, versus 58 expected and 58.2 prior.

Five-to-ten-year inflation expectations also rose to 3.9% from 3.5% prior (3.4% expected), which isn’t likely to be the message from the Fed on Thursday morning (Australian time).

Tariffs

For those keeping score (and revisions and volatility aside) the PPI and jobs data count for the doves at the Fed, while the CPI arguably counts against.

Outside of political interference, the other key consideration is the potential loss of tariffs once the Supreme Court rules (tariffs are supposedly the exclusive purview of Congress) – albeit hearings will run through to November.

Monthly tariff receipts are now running at $US30 billion, versus $7 billion before April.

This is a significant amount. It materially reduces the amount of debt issuance that needs to be absorbed, which is important given US debt levels.

To put it in context, over ten years the tariffs are worth over $US3 trillion of debt and potentially significantly more. US Treasury boss Scott Bessent says $750 billion to $1 trillion could be collected by June 2026.

A large chunk (though not all) of the tariffs are subject to a Supreme Court review, which is due before the end of the year.

To quote one commentator: “lose the case and Treasuries will throw a fit”.

Australia macro and policy

There was little meaningful Australian economic data last week with rate expectations largely unchanged ahead of a Reserve Bank meeting later this month.

Markets are pricing in a 12% chance of a cut. November is odds-on to deliver the only additional cut we see this year.

We did get some survey data on consumer confidence which showed a 3.1% drop versus August – mostly on expectations around unemployment and future economic conditions.

However, the latest CommBank Household Spending Insights data continues to show strong spending. The index was up 0.3% in August (versus +0.7% in July and +0.5% in May and June).

Find out about

Pendal Focus

Australian Share Fund

Crispin Murray,

Head of Equities

Spending growth has been consistently positive since the RBA began cutting in February.

China

Total financial flows passed the value of goods and services in China for the first time last week – a historic moment.

Financial account flows have grown rapidly over the past five years, driven by loosening of capital controls.

But the shift is arguably more impressive given China has also continued to dominate trade in global goods.

While it still lags developed economies such as the US and Japan (where the ratio is more like 10-15 to 1) the move is illustrative of the growing importance of the yuan.

It also serves as an important reminder of Beijing’s goal of globalising its currency.

Illustrative of this was the recent discussion by the People’s Bank of China to create a better mechanism for issuing sovereign debt overseas.

This would help feed growing demand for alternatives to US Treasuries and arguably add to pressure on long-dated yields.

Nearer term, the yuan has continued to strengthen relative to the USD.

With US rate cuts looming, and the Trump Administration happy to see the currency weaken, the likely direction of travel is for further strength.

That’s good news for commodities and the AUD.

Elsewhere it was relatively quiet on the economic front outside of a slight improvement in deflation trends.

August PPI landed at -2.9% year-on-year versus -3.6% in July.

While prices remain negative, the improvement was seen as a sign that anti-involution policies are having an impact.

Core CPI also rose to 0.9% (from 0.8%), the highest level since 2024.

Positively, last week Beijing also began plans to tackle the significant backlog of debts owed to the private sector by local government.

Up to 1 trillion yuan (US$140 billion) will potentially be earmarked in the first phase of a longer-term initiative.

Commodities

While energy stocks fell, it was a better week for oil, with Brent Crude +2.3% despite US Commodity Futures Trading Commission data showing the smallest long oil market position since 2010.

Gold also posted 1.6% gains on USD weakness – a trend that looks set to continue.

The PBOC also announced plans to ease licensing rules for gold imports and exports, potentially flagging further purchases.

In lithium, spodumene fell 5.5% on reports a large CATL lepidolite mine in China may restart sooner than expected. CATL reportedly held an internal mobilisation meeting on restarting, triggering a decline in spodumene prices back to c.$800/t.

Uncertainty remains regarding the outcome of the current lepidolite resource audit, due for completion end September. Pricing has now given back half of its recent rally.

Iron ore fell 1.1%, but pricing has so far proved resilient to typical seasonal weakness.

China steel production and exports remain strong while iron ore inventories are flat. USD weakness/RMB strength also helps.

There has been a pick-up in steel inventory and a recent decline in steel margins.

But iron ore is likely to remain rangebound while uncertainty persists regarding anti-involution policies and potential steel cuts.

Markets

Flows and AI remain supportive

Interest rates aside, two key trends continue to support equities: market flows and growth in AI.

On the former, in the US 1% of GDP is being directed into index funds every month, “regardless of valuations, sentiment or macro”.

That (along with strong consumer spending) appears incongruent with restrictive Fed policy.

AI also remains a key foundation for markets.

Tech is now more than a third of the S&P 500. That’s akin to the financial sector on the ASX.

Tech led gains last week in the US with headline AI-infrastructure agreements reshaping cloud compute dynamics.

Oracle was key, surging to a record following an incredibly bullish outlook for its cloud business.

Its deal with OpenAI to supply some 4.5GW of computing capacity beginning in 2027 is expected to require $300 billion of computing power over five years.

That took Oracle’s forward book to $455 billion, up $317 billion. Its market cap was up US$170 billion for the week.

Cloud Infrastructure revenue is now forecast to grow from US$18 billion in 2026 to US$144 billion by 2030. That was way in excess of sell-side estimates.

Meanwhile Microsoft struck a major contract with Dutch data centre company Nebius –potentially worth $20 billion over five years – to secure graphics processing units (GPU) capacity.

The utilities sector was not far behind tech, with increasing power demand from AI a growing tailwind.

Data centre power demand was estimated at 1.5% of global electricity demand in 2024.

By 2030, its share is forecast to double. In the US, demand is forecast to grow by 130% (at least).

Australian equities were flat last week, but under the surface there were big gains for gold, tech and property.

On the negative side, lithium and energy stocks fell.

About Jack Gabb and Pendal Focus Australian Share Fund

Jack is an investment analyst with Pendal’s Australian equities team. He has more than 14 years of industry experience across European, Canadian and Australian markets.

Prior to joining Pendal, Jack worked at Bank of America Merrill Lynch where he co-led the firm’s research coverage of Australian mining companies.

Pendal’s Focus Australian Share Fund has an 18-year track record across varying market conditions. It features our highest conviction ideas and drives alpha from stock insight over style or thematic exposures.

The fund is led by Pendal’s head of equities, Crispin Murray. Crispin has more than 27 years of investment experience and leads one of the largest equities teams in Australia.

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

Conditions look good for both bonds and equities right now, but one asset class should come out ahead. AMY XIE PATRICK explains

- Learn more about Pendal’s income and fixed interest capability

- Find out about Amy Xie Patrick’s Pendal Monthly Income Plus fund

US two-year bond yields have slipped from 3.95% to 3.54% since the start of August.

Over the same period, the S&P 500 clocked multiple new highs.

On the surface, that feels like a contradiction. Aren’t bonds supposed to rally when growth looks shaky, and equities move ahead when conditions are strong?

The story I’m hearing goes like this: softer labour market data plus Jay Powell’s Jackson Hole nod toward prioritising jobs over inflation equals imminent Fed cuts.

Bonds markets like this, because lower rates usually lifts bond prices. Equities like it because lower rates boost valuations.

Goldilocks achieved.

But if history teaches us anything, it’s that labour markets rarely weaken just enough to ease inflation pressures while staying benign (see figure 1 below).

Once unemployment inflects up, it usually keeps going.

If that’s the case, then one side of this rally is wrong. Either labour weakness proves more serious than equities are willing to admit, or not serious enough to justify the bond market’s enthusiasm for a rapid return to neutral.

Figure 1: Is this time different? US unemployment rate (%)

Here’s where I think the narrative misses a beat: it’s not just about jobs – it’s about tariffs.

This week’s US Producer Price Index (PPI) data surprised to the downside.

Companies hit by tariffs are swallowing the cost instead of passing it through to customers (see figure 2). That’s why inflation has stayed tame enough for bonds to rally.

Figure 2: US producers report higher costs through the ISM survey but aren’t passing it on US ISM prices index and US producer price index

Normally, margin compression would spell bad news for equities.

But tariff-sensitive stocks make up just 1% of S&P 500 market cap, 2% of earnings and 4-to-5% of revenues.

In other words, even if some corporates are hurting, it barely dents the index.

That’s the real reason bond and equities can both be in a happy place.

They’re being driven by different forces.

Bonds aren’t “slaves” to equities, and their correlation isn’t programmed to always be negative.

What it means for investors

For investors, the lesson is two-fold.

First, don’t let the surface-level story of “Fed cuts = everything rallies” fool you into thinking bonds and equities are in perfect harmony. They’re not.

Second, don’t over-index on tariffs either.

Both markets are effectively telling us to move on.

What will matter next is how growth and unemployment actually unfold.

It’s hard to see both asset classes continuing to benefit equally from that story.

For now, I’m positioned lightly in both bonds (via duration) and equities/riskier assets.

Dry powder matters more than chasing today’s consensus. When the next shoe drops – whichever side it lands on – that’s when the real opportunity will open up.

If you’d like to hear more, Pendal’s Income & Fixed Interest team would welcome an opportunity to chat.

You can contact us through the client account team here.

About Amy Xie Patrick and Pendal’s Income and Fixed Interest team

Amy is Pendal’s Head of Income Strategies. She has extensive expertise and experience in emerging markets, global high yield and investment grade credit and holds an honours degree in economics from Cambridge University.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia. The team oversees some $20 billion invested across income, composite, pure alpha, global and Australian government strategies.

Find out more about Pendal’s fixed interest strategies here

About Pendal Group

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

Here are the main factors driving Australian equities this week, according to portfolio manager JIM TAYLOR. Reported by head investment specialist Chris Adams

- Register for Crispin Murray’s bi-annual Beyond The Numbers webinar on Sep 12

- Find out about Pendal Focus Australian Share Fund

US ECONOMIC data continues to reinforce the narrative of a cooling employment environment providing scope for the Fed to keep cutting rates.

This was reflected in a US bond rally over the course of last week, with two-year yields reaching their lowest point in four years.

The market is now largely pricing consecutive cuts for the September, October and December meetings.

The US economy is best described as “slowing slowly”. Pundits have the risk of a recession sitting at about 30 per cent.

Conversely, Australian economic data is slightly hotter than expected, drawing a comment from RBA governor Michele Bullock that a continuation in this vein could see a curtailed rate cutting cycle.

This perspective was more in-line with our views coming out of reporting season: that the domestic economy is performing pretty well and does not require a significant cutting cycle to juice it up.

Elsewhere, the Saudis continue to hold up their end of the “lower is better” oil price deal with Trump.

OPEC+ commentary continues to support increased supply. Traders are jumping on the surplus supply bandwagon, with bullish oil bets at an 18-year low.

The iron ore price continues to hold up well, supported by renewed optimism for China’s prospects.

Equity market returns were subdued globally last week, in line with a historical trend of September as the poorest-returning month of the year.

The S&P 500 gained 0.4% and the S&P/ASX 300 shed 0.7%.

Tariffs

A US court of appeals upheld a lower-court ruling that President Trump’s use of tariffs under the International Emergency Economic Powers Act (IEEPA) was illegal.

This could affect 70 per cent of tariffs now in place. But enforcement has been delayed until mid-October to allows an appeal to the higher-level US Supreme Court.

A Supreme Court decision is not expected before early 2026.

If the original ruling is again upheld, the Trump administration could employ Section 122 of the 1974 Trade Act, which allows the imposition of up to 15% tariffs (versus the current weighted average of 16%) for 150 days.

Beyond that, Trump can look to use sectoral tariffs under Section 232 and 301.

The upshot is it looks likely that some form of tariffs remain in place.

If the IEEPA tariffs are deemed illegal, importers would need to file an action to have those tariffs repaid.

Tariff collection is running at US$370 billion annualised.

Macro and policy US

Consumer confidence

A key US confidence index dropped nearly 6% in August, driven by respondents with income in the $US50,000 to $100,000 range. Confidence for people with incomes above and below that remains resilient.

This “middle class squeeze” was noted by several companies in dining, retail, fashion and air travel during the recent US reporting season, according to the University of Michigan survey.

The survey reported more US consumers were dialling down spending now, than during the 2022 inflation spike.

More than 70% of those surveyed planned to tighten their budgets for items with large price increases in the year ahead.

Manufacturing

Messages were mixed in the latest survey of purchasing executives at US manufacturing companies.

The ISM manufacturing index rose from 48 in July to 48.7 in August. This was slightly below consensus expectations at 49.

New orders were at the strongest levels since January, whereas manufacturing output dropped back to November 2024 levels and the payrolls component fell, suggesting a sharp near-term fall in manufacturing sector payrolls.

Labour Data

Labour data continues to point to a cooling US employment market, according to the latest Job Openings and Labor Turnover Survey (JOLT) from the US Bureau of Labor Statistics.

There were 7.18 million US job openings in July, down from 7.36 million in June – with the latter also revised down by 80,000 and below consensus expectations of 7.37 million.

Openings are now about 80,000 above the September 2024 low and – assuming the usual level of revisions – could end up below that for August.

The retail sector was the weakest, probably reflecting an attempt to mitigate the cost impost of tariffs.

Find out about

Pendal Focus

Australian Share Fund

Crispin Murray,

Head of Equities

Health care – which had been strong previously – was weak for the second month and is now below the pre-Covid rate.

In contrast, federal job openings rose from 117,000 in June to 135,000 in July. But this was still slightly below last year’s range, consistent with a further gradual decline in federal payrolls ahead.

The ratio of openings to unemployment fell from 1.05 in June to 0.99 in July. This was the first time the number of unemployed had exceeded the total number of openings since April 2021.

However the ratio remains above the 0.93 average ratio of the second half of the 2010s.

The private sector “quits rate” was unchanged at 2.2% in July. This continues to suggest slower wage growth ahead.

This data saw bond yields fall 4bps and equity markets up on the day of its release, as it underscored the case for near-term rate cuts.

Other data points:

- Initial jobless claims increased to 237K in the week ending August 30, from 229K, marginally above the consensus, 230K. The increase was broad based across states and is an 11-week high.

- Continuing claims fell to 1,940K in the week ending August 23, from a downwardly revised 1,944K, below the consensus, 1,959K.

- The unemployment rate ticked up to 4.3%, from 4.2% in July, in line with the consensus. Stricter migration policies are likely to have kept this increase modest.

- Average hourly earnings rose by 0.3% for the month and 3.7% year-on-year, in line with the consensus. This is consistent with the Employment cost index (ECI) 3.6% year-on-year.

August payrolls rose by 22K, well below the consensus expectation of 75K. The two-month net revision was -21K. This is likely to see the Fed cut rates in September and suggest that further action before year end is required to stabilise the labour market.

- Federal payrolls fell by 15K, accompanied by a small fall in state and local government payrolls, resulting in a 16K drop in government jobs, about 20K weaker than the year-to-date trend

- Healthcare rose 47K, though this was the weakest print since January 2022.

- Manufacturing payrolls fell by 12K as uncertainty about tariffs bites.

Expectations of lower retail sales are weighing on distribution sector jobs.

- Construction payrolls fell by 7K, the third straight monthly fall.

- Professional and business services payrolls fell for a fourth straight month.

The August employment data showed the U.S. has added less than 600,000 jobs so far this year. Excluding the Covid period in 2020, that is the fewest for the first eight months of the year since 2009, when the economy was exiting the GFC downturn.

The Fed

Federal Reserve Governor Christopher Waller noted that “when the labour market turns bad, it turns bad fast … so for me, I think we need to start cutting rates at the next meeting”.

He added that “people are still worried about tariff inflation” but that he was not.

St Louis Fed President Alberto Musalem said the labour market still looked relatively healthy, while inflation concerns loom, especially given the impact of President Trump’s tariffs.

He also said “recent data have further increased my perception of downside risks to the labour market”, which could be seen as signalling openness to a rate cut soon.

Atlanta Fed President Raphael Bostic did not think it was “unambiguously clear” that the labour market was weakening materially.

He was more concerned with risks on inflation than labour market weakness. As a result he saw one cut as necessary this year, but was ready to pivot.

Macro and policy – Australia

Australian GDP increased 0.6% in the June quarter, with growth accelerating 40bps to 1.8% year-on-year.

This was slightly ahead of consensus and RBA expectations of +0.5% for the quarter and 1.6% for the year.

This marks the third consecutive quarter of recovery in annual growth since the cycle low in Q3 2024.

Notably, household consumption increased 0.9% for the quarter, versus consensus at +0.65%, with year-on-year growth accelerating 120bps to 2.0%. This is consistent with growth in real household incomes.

Growth was driven by higher discretionary spending across recreation, hotels and restaurants. Spending also rose firmly across health and food. The household savings rate declined 100bps to 4.2%.

Business investment fell 0.4% for the quarter, with broad-based weakness across non-dwelling construction (-0.9%) and engineering construction (-2.4%).

Growth in dwelling investment decelerated following a strong increase in the prior quarter but remains positive at +0.4%.

Household spending was up 0.5% month-on-month in July, in line with expectations, with the year-on-year rate accelerating 50bp to 5.1%.

This paints a pretty resilient picture of spending levels and the trends noted are pretty consistent with the company commentary coming out of reporting season.

RBA Governor Bullock’s remarks on the better-than-expected Australian Q2 GDP and consumption figures leaned somewhat hawkish.

She noted consumption growth was a bit stronger than the RBA thought and that if the trend continues there may not be that many rate cuts left in the current easing cycle.

“We are seeing it (consumer spending) come back, and that’s welcome,” she said.

“We’re seeing the private sector start to demonstrate a little bit more growth now, which I think is positive… That’s good, but it does mean that it’s possible that if it keeps going, then there may not be many interest rate declines yet to come. But it all depends.”

Macro and policy – China

Beijing is reportedly looking at some measures to cool the stock market, which is up US$1.2 trillion since August.

It is suggested these include the removal of some short selling curbs, and follows China Securities Regulatory Commission Chair Wu Qing signalling in late August his intention to consolidate the market’s positive momentum, while still promoting long-term value and rational investment.

Markets

Foreigners bought US$163 billion worth of US equities in June – a record monthly inflow, perhaps suggesting fears of the end of US exceptionalism are overdone.

June’s inflow was nine times the magnitude of the US$18 billion outflow seen from US equities in April at the height of the tariff worries.

With US equities seeing $285 billion of foreign buying in the first half of 2025, cumulative net foreign purchases of US equities are easily back at record levels.

All Things AI

AI-exposed stocks have driven a considerable portion of the market’s overall strength for the last few years.

AI-exposed equities have returned 50% in 2023, 32% in 2024 and 17% year-to-date in 2025, according to Goldman Sachs.

That compares with S&P 500 returns of 26%, 25% and 11% respectively.

Notwithstanding this share-price strength, current valuations of the largest stocks at 28x price/earnings is lower than their peak in 2021 of 40x.

Similarly, the valuations of the ten biggest largest technology, media and telecom (TMT) stocks at a median of 31x is still well below the 41x seen at the peak of the dotcom bubble in 1999.

So far, the spoils have gone mainly to the AI infrastructure companies in the semi-conductor, electrical component, power, tech hardware and industrials sectors, as opposed to companies expected to see productivity or revenues boosted by AI.

The trend in capex by “hyper-scalers” such as Amazon Web Services, Google Cloud and Microsoft Azure in the next few quarters will be one of the key drivers of sentiment for AI stocks in the back end of 2026.

In this vein, the question is whether we will see hyper-scaler capex intentions increase as the year progresses, as we saw in 2025 when 20% expected growth at the start of the year morphed into 54% growth. There were similar trends in 2024.

The market is grappling with how AI is going to affect software companies.

Is it an opportunity for sales growth in the medium term? Or will it reduce barriers to entry and prove disruptive to business models, pricing structures and ultimately compress profit pools of the software-as-a-service (SaaS) players?

There is little evidence of value creation in enterprise software applications so far. Until some evidence is shown, the market is discounting first and looking to see how things pan out.

The recent share price performance of software maker Salesforce is an example of how this is playing out – down almost 10% in the last three months.

It was also evident in the company’s earnings call where the very first question was whether the SaaS cycle was coming to an end due to the rise of AI.

The company noted in response that “the software industry is going through a tremendous transformation” but that AI large-language models are providing “a new platform that we can build on and extend our applications”.

In terms of productivity we are clearly at the very early stages of the AI rollout with the highest level of adoption in larger firms and concentrated in finance and technology.

AI-related commentary on earnings calls continues to ramp up, with 58% of S&P500 companies mentioning it in the most recent quarterly results season.

While the detail on the use case for AI technology is compounding, very few companies are actually directly linking the use of AI with EBIT or profit margins, though there are increasing instances of companies quantifying time or productivity benefits.

About Jim Taylor and Pendal Focus Australian Share Fund

Drawing on more than 25 years of experience investing in top-performing Australian companies and a background in accounting, Jim manages our Long/Short Fund and co-manages our Imputation Fund. He is a Chartered Accountant with membership of the Australian Institute of Chartered Accountants.

Pendal Focus Australian Share Fund is managed by Crispin Murray. The fund has beaten its benchmark in 14 years of its 18-year history (after fees), across a range of market conditions. Find out more about Pendal Focus Australian Share Fund here.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

The latest GDP data shows Aussies are spending again. Pendal’s head of government bond strategies TIM HEXT explains what it means for interest rates

AUSSIE consumers are spending again – that’s the main message from the latest quarter GDP numbers for Australia released today.

Overall, growth was slightly higher than expected at 0.6% versus a 0.5% forecast.

Annually we are 1.8% stronger than a year ago.

Increased consumer spending comes through as a clear trend in the June-quarter national accounts.

Despite last year’s tax cuts and February’s rate cuts, for a while it seemed consumers were more interested in saving than spending.

We estimated around 70% of the extra income was being saved.

However, in the June quarter household spending rose 0.9%, led by a 1.4% rise in discretionary spending.

It’s not quite boom-time out there in retail land, but it’s the first real positive sign since early 2022 when inflation and rate hikes hit consumers hard.

As a result, the household saving rate fell from 5.2% to 4.2%.

Overall GDP would have been stronger had public investment not fallen by 3.9%, albeit from very high levels.

State governments may be finally showing some fiscal restraint.

GDP per capita positive again, but labour cost pressures remain

Since mid-2022 we have had nine quarters of negative GDP per capita growth and only two quarters of positive growth.

Today makes a third at 0.2%, so good news.

Less welcome, by the RBA at least, was a rise in real unit labour costs of 0.7% for the quarter, after a 0.2% fall in the previous quarter.

The RBA is expecting wages to grow by 3.3% this year and 3% next year, as measured by the Wage Price Index. Without going into a detailed description of the pros and cons of various wage measures, the RBA would like to see real wages closer to productivity.

Any signs that wages are settling down nearer 3.5% than 3% would mean a very cautious RBA.

Market reaction and what’s next

Although there are the usual caveats in GDP numbers, the market viewed today’s numbers as a positive sign for growth, moving three-year yields around 10 basis points higher (3.55% from 3.45%).

Rate-cut expectations have moved from 100% chance of one cut by November to 90%.

Terminal cash expectations are now 3.15% from nearer 3% last week.

It does all feed into the idea that the RBA has time and optionality on its side.

If the consumer gets more confident from here, some may ask if any more rate cuts are needed.

If you’d like to hear more about how Pendal’s Income & Fixed Interest team is positioning for this environment, please contact us through our accounts team

About Tim Hext and Pendal’s Income & Fixed Interest boutique

Tim Hext is a Pendal portfolio manager and head of government bond strategies in our Income and Fixed Interest team.

Tim has extensive experience in banking, financial markets and funding including senior positions with NSW Treasury Corporation (TCorp), Westpac Treasury, Commonwealth Bank of Australia, Deutsche Bank, Bain & Co and Swiss Bank Corporation.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia.

Find out more about Pendal’s fixed interest strategies here

About Pendal

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

In 2023, Pendal became part of Perpetual Limited (ASX:PPT), bringing together two of Australia’s most respected active asset management brands to create a global leader in multi-boutique asset management with autonomous, world-class investment capabilities and a growing leadership position in ESG.

A softer US dollar is setting up a turning point for emerging markets – but not all countries will benefit equally. Pendal’s Global Emerging Markets Opportunities team explains

- Dollar weakness supports EM relative returns

- Deficit countries do best

- Find out about Pendal Global Emerging Markets Opportunities fund

A WEAKER US dollar is creating a supportive backdrop for emerging-market equities, says Pendal’s Global Emerging Markets Opportunities (GEMO) team.

The US Dollar Index – which measures the USD against other major currencies – is down about 10 per cent so far this year

Emerging market returns have historically been strongest when the US dollar is weak, because servicing US-dollar debt becomes cheaper; domestic purchasing power in EMs improves; and cheaper imports help keep inflation under control, creating room for rate cuts.

The prospect of a lower US dollar over coming years suggests EM equities are potentially at an inflection point, creating conditions for a multi-year outperformance of their developed market peers, argues the GEMO team.

“We see the classic conditions in place for an extended period of EM outperformance helped by potential US dollar weakness,” the team has told Pendal investors.

US dollar under pressure

Pressure from policy shifts could place continued downward pressure on the US dollar.

The US Federal Reserve is signalling further rate cuts, while the Trump administration has shown a preference for a weaker dollar through public statements and by raising currency concerns in tariff negotiations.

At the same time, investors are questioning the Fed’s commitment to its inflation target and weighing the risk of greater policy volatility – a loss of confidence that is adding to downward pressure on the dollar.

How dollar weakness boosts EM

Pendal’s GEMO team believes the level of the US dollar affects the performance of businesses in emerging markets in several important ways.

A weaker dollar improves balance sheets and creditworthiness at EM companies by making it cheaper to service US dollar debt.

EM consumers benefit because they can buy more imported goods, which get cheaper as local currencies strengthen. This puts a dampener on prices across EM economies, containing inflation and opening opportunities for rate cuts.

Similarly, because commodities are often priced in US dollars, a weaker dollar means they become cheaper in other currencies, lifting demand and prices. Many EM economies are commodity exporters.

And lower US interest rates leave investors searching globally for higher returns, adding capital flows to EM equities and bonds.

“A weaker US dollar environment has historically been better for emerging market equities,” says the team.

Some EMs are better placed than others

Still, while EM performance lifts as the US dollar weakens, the effect is uneven and investors should be discriminating in stock selection, says the GEMO team.

The Pendal team strongly believes in a top-down, country-level approach to emerging markets investing.

Economies with a current account deficit – common in Latin America and South-East Asia – benefit most from cheaper borrowing, lower imported inflation and stronger consumer demand.

But big exporters that run a surplus such as Taiwan and Korea can face headwinds as their products become more expensive in US-dollar terms.

“EMs differ from each other in fundamental ways,” says the team.

“That means that any given macro environment is going to suit some EMs and perhaps be a headwind for others.

Find out about

Pendal Global Emerging Markets Opportunities Fund

“This is grounded in the observation that emerging markets go right or wrong at the country level.

“Country factors – such as the current account deficit/surplus dynamic – dominate EM returns in a way that they do not in developed markets.”

How Pendal is positioned

The Pendal GEMO portfolio reflects this selectivity, holding just nine of the 24 MSCI EM countries.

Overweights include Brazil, Indonesia, Mexico and South Africa – economies with current account deficits, inflation under control, scope for rate cuts and attractive valuations.

Taiwan and Korea are underweight in the fund, with the team citing earnings pressure in semiconductors, autos and steel from tariffs.

In China, GEMO favours selective exposure to domestic-demand names and Hong Kong listings, avoiding tariff-exposed sectors.

About Pendal Global Emerging Markets Opportunities Fund

James Syme, Paul Wimborne and Ada Chan are co-managers of Pendal’s Global Emerging Markets Opportunities Fund.

The fund aims to add value through a combination of country allocation and individual stock selection.

The country allocation process is based on analysis of a country’s economic growth, monetary policy, market liquidity, currency, governance/politics and equity market valuation.

The stock selection process focuses on buying quality growth stocks at attractive valuations.

Find out more about Pendal Global Emerging Markets Opportunities Fund here

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

Here are the main factors driving the ASX this week, according to Pendal’s head of equities CRISPIN MURRAY. Reported by portfolio specialist Chris Adams

- Find out about Pendal Focus Australian Share fund

- Live webinar: Register for Crispin Murray’s bi-annual Beyond The Numbers update on Sep 12

THINGS remain relatively quiet on the macro front and US economic growth is holding up reasonably well – though it’s still below trend.

We’re seeing early signs of improvement in other economies, possibly as tariff uncertainty begins to diminish at the margin.

US rates are falling in the absence of a dramatic rise in US employment growth. All this remains a supportive context for equity markets.

Overall Australia’s reporting season was okay.

We did not get the kicker to earnings that was seen in the US – and valuation is at the top end of the range.

But the local market remains supported by signs of an improving domestic economy and impending rate cuts from the Reserve Bank.

Volatile price reactions continued last week – notably Coles, NextDC and Qantas to the upside and Woolworths and Wisetech to the downside.

Equity markets were flat in aggregate last week, failing to build on gains made after recent dovish comments from the Federal Reserve chair.

The S&P 500 retreated 0.1% while the S&P/ASX 300 gained 0.2%.

The US yield curve steepened with short-end yields falling as confidence on rate cuts built.

But the 10-year remained anchored by ongoing concerns over supply of Treasuries and the Fed’s potential to shift focus from inflation to growth as the composition of voting members changes.

Metal prices continue to rise on signs the global economy is experiencing a small improvement in growth rates, along with supply discipline in China.

AI chipmaker Nvidia’s result had enough for both bulls and bears to feed off, resulting in a relatively muted reaction.

The key swing factor has been China sales, which is more a stock-specific issue than a reflection of the need to invest in AI.

Nvidia earnings

There were two negatives in the result:

-

- The data centre (DC) division, which is the bellwether for the AI thematic, saw sequential sales fall 1%. However this was due to China, where shipments dropped from $US4.6 billion in Q1 to $0.6 billion in Q2 due to the US government restricting sales. While the restriction has been lifted, the Chinese themselves are now discouraging purchases of Nvidia chips as they look to diversify supply chain.

- Op-ex growth guidance was lifted from the mid-30% to high-30% range.

Offsetting this were positives:

- Excluding China, underlying sequential DC revenue growth was 12%. Shipment of Blackwell ultra chips reached $US10 billion – NVDA’s fastest product-ramp ever.

- The networking unit within DC grew revenue 46% quarter-on-quarter (QoQ). This is becoming a key area for investor interest as it drives the efficacy of chipsets.

- Overall revenues were 1.5% better than expected at +6% quarterly and +55% year-on-year.

- Gross margins surprised to the upside, helping drive 4% EPS revisions.

There is nothing in this result to reinforce the negative AI sentiment mentioned last week.

Locally, data centre manager NextDC’s result highlighted significant demand for DC capacity in Australia and the broader Asian region.

A lot of this is driven by the need to prepare for AI by moving data to the cloud. Cloud service providers Amazon, Microsoft and Google have seen 39% yearly growth in cloud bookings in aggregate.

Australian economy

July’s consumer price index (CPI) was higher than expected, rising 0.9% for the month and 2.8% for the year (compared to expected annual growth of 2.3%).

The market largely shrugged this off though, since the first month of the quarter is seen as the least reliable of the inflation data points.

The specific explanation was government electricity subsidies rolling off.

The core, trimmed-mean measure was also higher than expected at 2.7%, though that was still consistent with RBA expectations.

This does highlight a risk to the pace of the easing cycle in Australia.

Pendal Focus Australian Share Fund

Now rated at the highest level by Lonsec, Morningstar and Zenith

Credit growth is accelerating, which suggests policy is not that restrictive. We have seen a number of Australian companies reporting improved sales in July and August.

Markets

The ASX was flat last week but the Australian market rose 3.2% in August (+12.4% calendar YTD), with small caps leading at +8.4% (+18.7% calendar YTD).

Small caps were helped by three factors:

- More leverage to the China anti-involution theme

- Better-performing tech names

- Greater exposure to domestic discretionary

Resources were the best-performing sector, up 10.3% for the month, which was tied to:

- A rally in rare earths as western countries look to underwrite capacity with a guaranteed floor pricing well above spot

- Moves in China to reduce lithium supply

- Resilience in the iron ore price

Consumer discretionary, utilities and domestic REITS all outperformed in August, partly due to signals from results but helped also by rates. Banks also outperformed on resilient margins.

Health care underperformed, partly on a global rotation away from defensive sectors but also due to stock-specific issues at CSL, Sonic Healthcare and Telix Pharmaceuticals.

Technology also lagged. There was significant divergence within the sector, but the biggest names drove the downside: Wisetech had a poor result; Xero was caught up in the “AI-may-kill-software” narrative; and there was an overhang from the cap raise for the Melio deal.

Five major ASX reporting season themes

Here is an overview of five themes Pendal’s team identified during reporting season:

1. Overall earnings were okay

Earnings overall were reasonable, with similar overall trends to February in terms of misses and beats.

A third of companies beat by 5% or more and 22% missed.

FY26 revisions came down more than they did in February, mainly driven by issues at offshore-exposed companies.

Consensus EPS growth for FY26 dropped marginally through August and is now indicating around 6% higher than FY25.

This was in contrast to the US where FY26 expectations rose. But Australia does not have the same drivers from tech and financials.

2. Stock responses were volatile

Stock price volatility on the day of results reached new highs, driven by the tone of messaging and revisions.

Some 30% of companies experienced stock moves more than three standard deviations away from their average on reporting day.

It’s interesting that the strength of reaction was almost as material for earnings variances of 2.5% away from consensus, as for 5% away.

This means volatility is not tied to greater unpredictability in reporting. Rather it is a new market feature linked to an acceleration of investors shifting position in response to events.

This has become somewhat circular. Quant strategies and high-turnover investment pods led the way, but are now reinforced by long-only investors who anticipate such moves and are beginning to reinforce them.

Of the biggest downside daily moves, James Hardie (-28%), Woolworths (-15%) and South32 (-7%) were tied to earnings. But most of the other underperformers such as CSL (-16%), SGH (-9%) and JB Hi-Fi (-9%) were due to valuation de-rating, reflecting a lack of confidence in the business or management.

On the outperformers, Qantas (+9%), Stockland (+7%) and Westpac (+6%) can be understood on the basis of earnings. But most of the rest reflected a company establishing itself as a safe haven in a challenging environment. For example, Brambles (+12%) was one of the few international industrial stocks not seeing downgrades.

3. Ratings changes drive returns

Reinforcing point two, rating changes were the most material driver of returns, and the beta to earnings changes has risen.

The biggest re-ratings were generally either:

- Stocks beginning to stabilise or turn the corner after a tough period (eg Guzman Y Gomez, IDP Education, Tabcorp, ARB Corporation, Seek, Kelsian, Worley), or

- Stocks that established or reaffirmed their status as relatively predictable safe havens (eg CAR Group, Coles, REA Group, Brambles)

On the downside there were a few significant de-rates tied to earnings (eg Dominos Pizza, Reece, Amcor). But most reflected large sentiment shifts, particularly on higher value stocks (eg CSL, HUB24, Netwealth, Woolworths, Commonwealth Bank).

4. Disappointing large caps hit harder than small caps

The average two-day relative return for industrial large caps which missed consensus EPS by more than 5% was -7.2% for the ASX 100, versus -3.8% for small caps.

This probably reflects the facts that higher active trading is concentrated in the more liquid stocks.

5. Domestic outperforms international

This reporting season, domestic stocks generally performed better than internationally-exposed companies.

Australian-focused consumer discretionary names Tabcorp, Nick Scali, Super Retail, Qantas and Scentre all signalled the consumer was stabilising and showing signs of improvement.

Financials (excluding insurers) outperformed, with bank margins better than expected as they pulled the deposit pricing lever.

Contractors such as Ventia, Downer, Monadelphous and Worley also saw gains, with an improved industry structure leaving the environment for pricing as good as it has been for many years.

Residential housing sector names such as Aspen, Stockland and Lifestyle Communities did well, boosted by the declining interest rates and the early extension and broadening of the federal government’s First Home Buyer Scheme –now uncapped in volume and with increased price caps.

Global industrials such as James Hardie, Amcor, Reliance Worldwide, Reece and BlueScope Steel underperformed.

Sentiment around the resilient domestic consumer was reflected in ratings changes.

The consumer discretionary sector saw a 3.8x P/E expansion in August, beating energy (3.2x) and materials (2.5x). Healthcare was the only sector to see a multiple contraction (0.3x).

Stepping back and looking at the ASX valuation, we are now at the top end of our historic range, leaving the market largely reliant on earnings for further support.

Earnings growth is expected to be mid-single digit.

This all leaves the market vulnerable in the event of an economic shock.

However the picture at the moment looks benign, particularly with interest rates likely to come down.

About Crispin Murray and the Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia. Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions.

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

A shift in focus from inflation to employment hints at a likely rate cut in September. Pendal’s head of income strategies AMY XIE PATRICK explains

- Learn more about Pendal’s income and fixed interest capability

- Find out about Amy Xie Patrick’s Pendal Monthly Income Plus fund

SINCE December 2018, we’ve known Fed chair Jay Powell is not afraid to pivot.

Back then the Fed hiking cycle was forced to an abrupt halt when the US economy came under the strain of the first round of Trump’s trade tariffs.

By the following October, the Fed had cut rates by 75 percentage points to 1.75%.

Powell’s latest comments at last weekend’s Fed’s annual gathering in Jackson Hole, Wyoming, may prove to be another example.

In his speech, Powell acknowledged downside risks to employment, suggested further easing from the current “restrictive” policy stance may be appropriate and – for the first time in months – did not make this conditional on the inflation outlook.

Since these remarks, the US bond market has priced in an 85% chance of a cut at the next Federal Open Market Committee meeting in September.

This would take the upper bound of the Fed Funds target rate to 4.25%.

Sceptics view the move as Jay Powell bending to political pressure from President Trump.

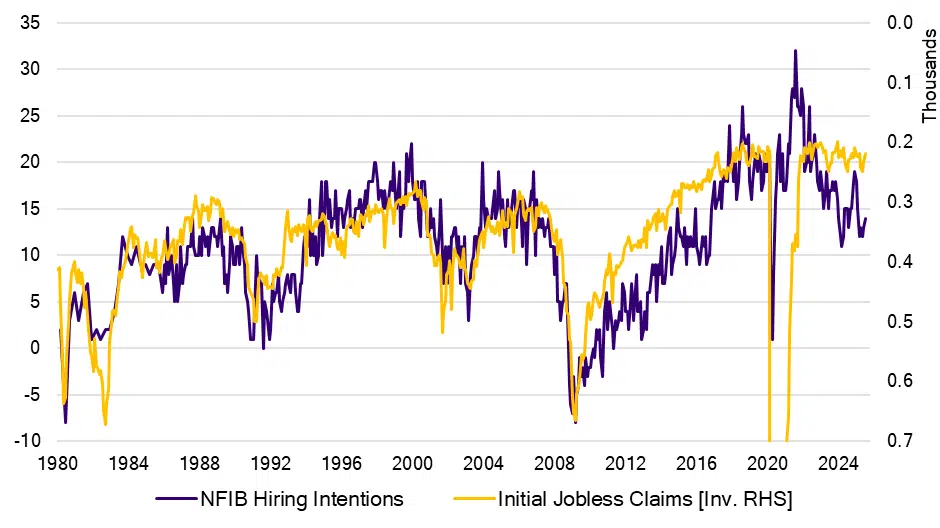

The chart below suggests the Fed ought to be getting a little more worried.

US hiring and firing: NFIB Hiring Intentions and Initial Jobless Claims

Source: Bloomberg

The purple line shows the hiring intentions of US businesses, according to a monthly survey by the National Federation of Independent Business.

The yellow line is an inverted series of US initial jobless claims – a weekly series to reflect new joblessness.

The long-standing relationship between the purple and yellow lines is clear to see, and intuitive to grasp.

When businesses stop hiring, they eventually have to start firing. And vice versa.

When businesses feel the bottom is in, they stop firing, and then they start hiring.

This relationship seems to have dislocated of late. We need more time to see whether this is an actual dislocation, or one of those blips in the long-run data.

A possible explanation?

Perhaps businesses sense the slowdown and have paused hiring, but burned by the post-Covid labour shortages, are not yet willing to let people go.

A likely rate cut

September will likely bring a rate cut from the Fed.

Pendal’s analysis of the long-term decision-making bias of the Fed leans heavily on market pricing.

In other words, the Fed doesn’t like to surprise or disappoint (unlike some other central banks we know). That analysis also shows how sensitive the Committee is to labour-market dynamics.

If the Fed has now pivoted its focus from inflation to employment, we too should be looking at the best leading indicators for where labour markets are headed.

If you’d like to hear more about what those lead indicators might be, Pendal’s Income & Fixed Interest team would welcome an opportunity to chat.

You can contact us through the client account team here.

About Amy Xie Patrick and Pendal’s Income and Fixed Interest team

Amy is Pendal’s Head of Income Strategies. She has extensive expertise and experience in emerging markets, global high yield and investment grade credit and holds an honours degree in economics from Cambridge University.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia. The team oversees some $20 billion invested across income, composite, pure alpha, global and Australian government strategies.

Find out more about Pendal’s fixed interest strategies here

About Pendal Group

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

Here are the main factors driving the ASX this week, according to Pendal’s head of equities CRISPIN MURRAY. Reported by portfolio specialist Chris Adams

- Find out about Pendal Focus Australian Share fund

- Live webinar: Register for Crispin Murray’s bi-annual Beyond The Numbers update on Sep 12

MARKETS are seeing renewed momentum on the back of US Fed Chair Jerome Powell’s dovish message on rates late last week.

This offset earlier weakness, nudging the S&P 500 forward 0.3% while the S&P/ASX 300 gained 0.5%.

Unless there’s a significant strengthening in next week’s labour data, US rates should fall at the September 17 meeting.

US bonds rallied through the curve and the US dollar weakened on the new information.

This is constructive for risk assets and was reflected in a rotation to US small caps, which have been lagging the market.

Sentiment towards AI stocks took a hit from a Massachusetts Institute of Technology report indicating companies can’t deploy it effectively and OpenAI CEO Sam Altman referring to AI “overexcitement”.

The Nvidia result this week will determine whether sentiment recovers.

Australian results season continues to be mildly constructive for the market.

Domestically focused stocks are outperforming. REITs are up on renewed interest in property assets, banks higher on better margins and other stocks such as Seek, Downer and Super Retail all able to deliver good profit outcomes.

Volatility continues with severe negative reactions to results from James Hardie, CSL and Sonic Healthcare.

Markets generally remain constructive with the economy seen as holding up and liquidity supportive with interest rates expected to come down.

US rate expectations

The focus has been on Jay Powell’s Jackson Hole speech, and the signals he would give regarding the potential for a September rate cut.

Last week the market began to fear Powell would be cautious and seek to dampen expectations. This led to the probability of a September rate cut dropping into the 60% range.

But Powell struck a dovish tone and markets latched onto his remark that “with policy in restrictive territory, the baseline outlook and the shifting balance of risks may warrant adjusting our policy stance”.

The key signal is the Fed does need to see another weak employment data point to act, because they see policy settings as restrictive while risks on inflation and employment are balanced.

Powell dropped references to the labour market as “solid” and noted that a slowdown in payroll growth was “much larger than assessed” in the July meeting.

He also flagged that labour demand and supply had weakened together. While there was limited evidence of labour market slack, this was “an outcome we want to avoid”.

The RBA cites this view as well: once the labour market tips over it can gather momentum and this can create a structural issue as extended periods of unemployment see people fall out of the labour market.

Powell noted the inflationary effects of tariffs would “accumulate over coming months” and there was a risk it became protracted. But he also said second-round effects created by wages did “not seem likely”.

He has left himself an out should next week’s payroll data shows a dramatic firming of the labour market, but this is a low probability.

The washout is that the market is now pricing in around a 90% chance of a rate cut in September.

Powell appeared be sending a soft signal that the next rate moves may be limited (ie perhaps two 25bp total moves rather than a 100bp), partly through his point that the labour market was in balance.

There also appears to be a shift in the longer-term policy; the approach of allowing inflation to overshoot has effectively been dropped.

It is somewhat irrelevant what Powell thinks about rates medium term though, since he will have stepped down as Chair.

The pressure on the Fed from the Trump Administration continues to build. Fed governor Lisa Cook faces calls from the President to resign over allegations she had been misleading on a mortgage application form.

This adds to speculation that the Fed will move a lot more dovish next year.

This may help drive short-end yields lower, but could also lead to a steepening of the yield curve as the long end begins to question the inflation target commitment.

The market is expecting four rate cuts by June next year.

AI sentiment shift

The other key thematic issue last week was a negative shift in AI sentiment. This was due to:

- An MIT report that found 95% of AI pilot programs in companies are not hitting performance targets. This was because AI tools were too generic and did not adapt to workflows established in the corporate environment.

- Sam Altman from Open AI said: “Are we in a phase where AI investors as a whole are overexcited about AI? My opinion is yes.” We note he followed that up by saying: “Is AI the most important thing to happen in a very long time? My opinion is also yes.” Nevertheless, this adds to the weight of AI-bubble calls from the likes of Ray Dalio and Alibaba co-founder Joe Tsai.

- Meta was reported to have instigated a hiring freeze on AI developers. This comes after a months-long hiring binge, including poaching three people from OpenAI on rumoured packages of US$100 million over four years.

- There was talk that Nvidia had asked Taiwanese multinational Foxconn – which makes chip components – to suspend work on the H20 chip, which is specifically made for Chinese customers, due to a lack of demand.

This news also came on the back of a disappointing release of ChatGPT5 and Meta’s Llama 4.

Given the strength of AI names – eg Nvidia is up 80% from April lows and 40% over 12 months – the sector is vulnerable to consolidation.

The issues raised are real ones, and the question for our portfolios is the implications for data centre providers such as NextDC and Goodman Group.

As always there is nuance, such as:

- Our conversations with management teams suggest that applying AI is problematic for organisations. One of the biggest challenges is access to data and whether this is set up in way which can be utilised. Many companies need to resolve this, requiring investment and further migration to the cloud. So this may not have a bearing on datacentre demand.

- The bubble talk is inevitable, given some of the valuations being applied to private companies and the salaries being offered to attract staff. Much of this speculative activity has not translated into domestic data centre providers, with Goodman’s stock flat on twelve months and NextDC down. We continue to expect material contract announcements to underpin good growth for these companies.

Our final observation is that in the US market large-cap mutual funds and hedge funds are still materially underweight the technology sector.

Tariffs

The US Federal Circuit Court is soon due to rule on the Trump Administration’s appeal against the Court of International Trade’s ruling that tariffs imposed under the International Emergency Economic Powers Act (IEEPA) were not legal.

Experts believe the ruling will be upheld and therefore this will go to the Supreme Court.

The market appears ambivalent about this, though there may be some risk to long bond yields as there is a complexity surrounding whether money already raised needs to be refunded, which would aa pressure to the fiscal position.

We also note that inbound containers to the Port of Los Angeles, which collapsed a few months ago, has also rebounded. This suggests trade flows are normalising, so we do not to expect any disruption to supply.

Markets

Powell’s dovish message fuelled US markets to new highs on Friday, led by airlines, homebuilders, banks and consumer discretionary stocks – all rate-sensitive sectors – while consumer staples, insurers and healthcare lagged.

We note the US small cap Russell 2000 index rose 4% on Friday.

It has lagged the larger-cap indices and is more leveraged to domestic stocks, highlighting how the market sees these rates cuts as underpinning growth rather than being reactive to a more significant slowdown.

As explained last week, the technicals for markets remain supportive. Japan continues to make new highs and China – another lagging market – is breaking out of a 10-year range.

Pendal Focus Australian Share Fund

Now rated at the highest level by Lonsec, Morningstar and Zenith

Australia

We are roughly 80% of the way through earnings season with some key bellwethers yet to report – notably the supermarkets, Wesfarmers, Qantas, Medibank Private, Scentre Group and Wisetech.

Volatility remains as high as we have ever seen in terms of stock-price reaction on the day of the result.

This, we believe, is creating some significant distortions in terms of value.

It highlights the growing importance of management’s role in setting their cost of capital.

Those who communicate well, are predictable and earn the trust of the market command substantial “sleep-at-night” premiums over other companies – even where the earnings growth is lower.

We see this in the divergence in price/earnings ratio between Wesfarmers and CSL, which reached extremes last week on a poorly-communicated CSL result.

CSL is now rated the same as Westpac.

The former is expected to deliver ~22% EPS growth pa over the next two years, while Westpac is expected to grow EPS 1%.

This reflects how earnings momentum, flow and narrative drives prices in the short term.

Themes to highlight from last week include:

- Banks performed strongly as both Westpac and National Australia Bank delivered positive surprises on margins.

- Consumer discretionary also performed well with Super Retail Group beating expectations on performance and outlook.

- Domestic businesses are holding up better despite subdued economic conditions. Seek is seeing improved performance in Australia driven by yield and Downer is improving its margins.

- Most US-exposed industrials continue to struggle with BlueScope Steel, Reliance Worldwide and James Hardie disappointing last week. The exception here was Brambles, which disappointed on revenue but was able to make up for this with lower costs and provisions.

- Traditional REITs outperformed as they talk to improving valuations and a pickup in interest in property assets.

- Other rate sensitive defensives such as Transurban and The Lottery Corporation also outperformed as the market rotated to predictable domestic stocks with some rate leverage.

With a week to go the revisions signal is similar to the last few years, with a skew to positive revisions. Some 28% of companies have beaten EPS by 5% or more, while 20% have missed.