Valuation dispersion in emerging markets exudes opportunities

As active investors, we hold the fundamental belief that markets are inefficient and that, through the application of a well-considered and well-tested investment process it is possible to outperform over the longer term. As top-down investors, we believe that a lot of that inefficiency can be found at the country level, through excessive optimism or pessimism about growth prospects, sustainability of growth, currency outlook or the political and governance environment in that country. As growth-at-reasonable-price investors, we pragmatically believe that markets will, at times, misprice part of the growth-value spectrum in the asset class.

Current concerns: the aggressive and excessive re-rating of growth

We believe that anomalies currently exist within the emerging markets equity asset class in the pricing of growth and fundamentals in both top-down and sector/stock-specific dimensions. Following are some examples…

Chinese internet stocks

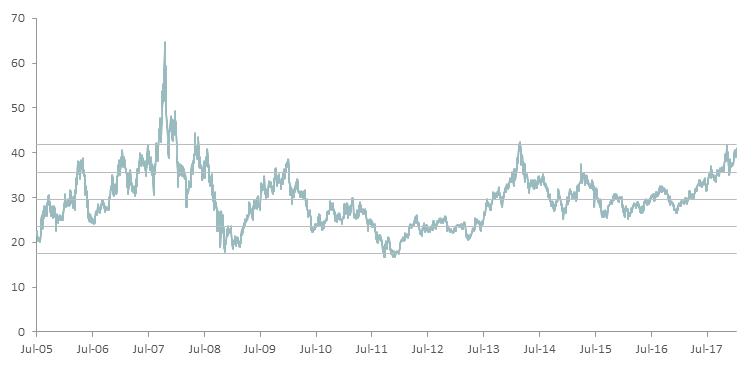

Chinese internet stocks soared in 2017. One of the biggest winners was Tencent, a colossus of the Chinese technology landscape, in large part because of its ubiquitous WeChat messaging app which has one billion users. At the time of writing, Tencent is valued on a dizzying multiple of 37 times its 12-month forward price/earnings ratio (P/E). This represents over one standard deviation above the historic mean 12-month forward P/E ratio for the stock, which is statistically material. Previous occasions when the stock has been valued at this elevated level have been followed by de-ratings back to its average price. Should Tencent finish 2018 at its long-term average valuation (29.7 times 12-month forward P/E), the stock would finish the year below its current level, assuming it achieves consensus 2019 earnings. And this assumes that Tencent continues to grow its revenues by greater than 50% for the foreseeable future in an economy growing at an estimated 11% in nominal terms.

Tencent’s toppy valuation

Source: Bloomberg

Other Chinese internet names have lower but still demanding valuations, arguably weaker business models and more challenging governance aspects. Of particular note is the re-rating of Alibaba, which has just enjoyed three very strong quarters in terms of growth in revenue per active user within China and from international revenue, but which seems to have been factored into the share price (the share price has more than doubled since the start of 2017).

An additional component of our growing caution on Alibaba is the firm’s use of cash flow. Since the end of 2015, the company has generated RMB 196 billion in cash flow from operations. This might not seem much over eight quarters for a company with a market cap of RMB 3 trillion (US$482 billion), but of that cash flow, RMB 117 billion was used to fund acquisitions in everything from e-commerce in other emerging markets to luxury malls, newspapers and supermarkets. It remains to be seen whether all of those assets will attract the 29 times 12-month forward P/E multiple that Alibaba currently trades on over the longer term.

Beyond Tencent and Alibaba, other Chinese internet names have experienced similar performance, reacting to strong operational growth with very large share price rises over the past year. The space has enjoyed growth, price momentum and significant investor interest, but it remains our view that share prices cannot outstrip earnings indefinitely.

Lofty valuations in some segments

It is not just in the Chinese internet sector where valuations have exploded far beyond levels supported by underlying earnings fundamentals. There are a number of companies within emerging markets that are challenging even the most generous of assumptions to arrive at the market’s lofty valuations. A few notable examples include Mercado Libre, the operator of an online trading site in Latin America; Celltrion, the largest of a group of related Korean biotechnology companies; and HDFC Life, the life insurance subsidiary of a leading Indian financial services firm, HDFC. By way of example, HDFC is trading on a price/book value of 25 times (no, the decimal point is not missing!) Compare this valuation to industry-leading regional insurer, AIA, which trades at a price/book value of 2.4 times and China Life Insurance trades which trades at 1.7 times and the degree of exacerbation becomes apparent.

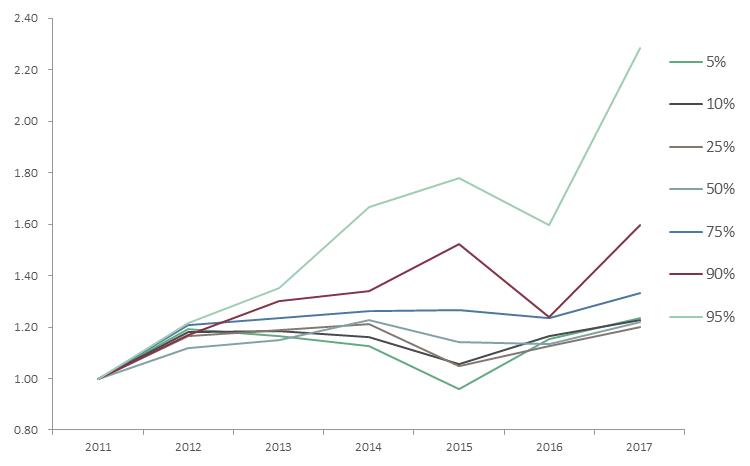

To illustrate the degree of dispersion across emerging market companies we have created a composite value measure of index constituents to track their valuation over the past five years. The chart below highlights the degree of dislocation in valuations.

The most expensive emerging market stocks have become far more expensive

Source: JOHCM. Composite value measure of MSCI Emerging Markets Index constituents, based on price/book, price/earnings and inverse dividend yield, 2011 = 1.0. Data as at 23 January 2018.

Looking into the top and bottom quartiles (by composite valuation), we find some interesting trends. The top quartile is dominated by China (based on benchmark weight), with India and Indonesia over-represented. At a sector level, information technology, consumer staples and consumer discretionary make up over 70% of the top quartile. The bottom quartile sees South Korea, China and Russia over-represented at a country level while financials is the dominant sector.

There is no natural limit to the premium to which growth stocks can trade at over other stocks. Nonetheless, we certainly feel that parts of the asset class (Chinese internet, consumer growth stocks in parts of Asia) will experience valuation headwinds from these levels.

It is clear that these companies very much represent the growth end of the growth spectrum, and this aggressive rerating of growth stocks is borne out in the index-wide data. By constructing a composite valuation measure (using price/book ratio, price/earnings ratio and the inverse of dividend yield), we can look at the re-rating of the most expensive stocks. The chart above clearly shows that the top-quartile of stocks has re-rated away from the rest of the asset class.

A distorted index: no time for a passive approach

One further impact from the aggressive re-rating of growth over the last two years has been its effect on the valuation of the overall asset class, as calculated by market cap-weighted or free-float-weighted indices. As these larger growth stocks have performed and re-rated, they have driven the overall valuation of the MSCI Emerging Markets Index higher. Some of these growth stocks now dominate the benchmark. At the time of writing, Tencent represents 5.6% of the Index, Alibaba 3.8% and the Chinese internet sector in total represents 12.6%. Naspers (a portfolio holding) has significant exposure to Chinese internet stocks and is a further 2.2%. Collectively, this 15% weighting is slightly larger than the index weight represented by the whole of Latin America plus Turkey plus Poland.

This really matters when one considers passive investing in emerging markets equity. An investor putting US$100 to work in a passive, MSCI Emerging Markets Index-based fund is putting the first US$15 into Chinese internet exposure and only about US$11 in total into the long-term growth stories of India, Pakistan, Indonesia and Egypt. Seen from another perspective, this hypothetical investor is putting over US$27 into information technology exposure and just over half of that into energy and materials.

Naspers – market-leading internet exposure at a discount

The portfolio retains a large position in Naspers, a South African-listed consumer stock. Naspers is a media holding company, with the single largest asset being 33% of Tencent. It also owns 28.7% of Russian internet company, Mail.ru (also listed). Naspers also has substantial investments in pay TV, e-commerce, online classifieds and online marketplaces.

“Passive flows, factor investing and active momentum investing are causing an increasing deviation between valuation and fundamentals”

By subtracting the current market value of the Tencent and Mail.ru stakes from Naspers’ market cap, it is possible to calculate the net value of Naspers’ other assets (including net debt and central costs). This stub has historically had a small positive value, but in 2016 it began to fall as Tencent outperformed Naspers, finishing the year with a valuation US$13.4 billion less than its stakes in Tencent and Mail.ru. In 2017, the stub value fell substantially (touching -US$50 billion and finishing at -US$42.3 billion) despite some very positive operational and financial developments in the stub. We see this as a major mispricing and as a further indication that passive flows, factor investing and active momentum investing are causing an increasing deviation between valuation and fundamentals in parts of the emerging market equity space.

Active opportunities

None of this is to call for a crisis in emerging markets. Global economic conditions remain robust. For about the last two years, exports and manufacturing purchasing manager surveys (PMIs) across the world have been robust, while an absence of inflation has allowed central banks to tighten slowly while longer-dated bond yields remain benign. This environment of stronger global growth but supportive global monetary policy is an ideal one for emerging economies. We believe this will create exciting investment opportunities in the emerging markets equity asset class. We are particularly positive on opportunities within India, South Korea and Taiwan.

India – a coiled spring

India has been a serial economic underperformer despite its potential to be one of the world’s fastest-growing economies. It has struggled recently with below-trend growth, but the conditions are in place for growth to explode over the next two years. In the short term, a general election to be held by 2019 at the latest means we can expect plenty of fiscal stimulus by the Modi Government to ensure that India’s economy is firing on all cylinders going into the polls.

On a more long-term structural note, last year saw two major developments in India that only add to our optimism towards India’s economy and, by extension, Indian equities. The first was the announcement of a recapitalisation of the state-owned banks of approximately US$32 billion over the next two years. This was by far the most significant move of any recent Indian Government to tackle the under-capitalisation of the state-owned banks.

The second was the announcement of a US$105 billion five-year road building plan to improve transport infrastructure to allow the economy to benefit fully from the liberalising effects of the national goods and services tax (GST). These steps are indicative of a government keen to ensure that the positive effects of its reforms are felt before the election.

We believe India’s economy resembles a coiled spring waiting to be released. Moreover, it is a growth story that should materialise irrespective of developments in the China and US economies. While India’s equities are not cheap in an absolute sense, the premium they attract over the average for emerging markets is slightly below its normal level, and we feel that the very strong growth opportunity and the prospects for further reforms justify current valuations.

South Korea – a winner on corporate governance

We believe South Korea stocks are cheap for corporate governance, not geopolitical reasons. Korea’s companies are rich in cash, yet Korea has the lowest payout ratio of any major market in the world. This is explained by a lack of effective oversight that allows company managers to simply hold cash back from shareholders, however this practice is changing. The behaviour of corporate Korea and the related lack of dividends has become a growing issue in Korea’s politics, as an ageing population needs income from its investments. We feel that both Korea’s public’s response to a recent corruption scandal and the resulting election of a left-wing administration will put huge pressure on Korea’s companies to reform. This will be the catalyst to unlock much of the hidden value in Korea’s equity market.

Taiwan – a play on global growth and rising yields

Taiwan is currently our third large overweight country position in the portfolio. As a heavily export-oriented economy with a large tech sector, it is an obvious beneficiary of the synchronised recovery in global economic growth. But it’s not just the export growth story that attracts us here. Taiwanese financials such as Cathay Financial Holding stand to profit from rising interest rates and bond yields, especially insurance names with large, established policy accounts.

Active on country and intricate on company

The multitude of economic, political, industrial and social factors that interplay in developing countries present many risks and opportunities for astute investors. Furthermore, the companies operating either within or across these markets can present their own set of interesting dynamics. Remember that these companies aren’t immune to the rapid shifts emanating from competitive forces and technological evolution that are more commonly related to companies in developed markets. However, focusing on either the country or the company in isolation can lead to overlooking a sizeable intersection of these two realms. It is what makes investing in emerging companies truly interesting and truly rewarding for investors who can appreciate the convolutions and the intricacies in tandem.

This article has been prepared by Pendal Fund Services Limited (PFSL) ABN 13 161 249 332, AFSL No 431426 and the information contained within is current as at April 18, 2018. It is not to be published, or otherwise made available to any person other than the party to whom it is provided.

PFSL is the responsible entity and issuer of units in the Pendal Global Emerging Markets Opportunities Fund (Fund) ARSN: 159 605 811. A product disclosure statement (PDS) is available for the Fund and can be obtained by calling 1800 813 886 or visiting www.pendalgroup.com. You should obtain and consider the PDS before deciding whether to acquire, continue to hold or dispose of units in the Fund. An investment in the Fund is subject to investment risk, including possible delays in repayment of withdrawal proceeds and loss of income and principal invested.

This article is for general information purposes only, should not be considered as a comprehensive statement on any matter and should not be relied upon as such. It has been prepared without taking into account any recipient’s personal objectives, financial situation or needs. Because of this, recipients should, before acting on this information, consider its appropriateness having regard to their individual objectives, financial situation and needs. This information is not to be regarded as a securities recommendation.

The information in this article may contain material provided by third parties, is given in good faith and has been derived from sources believed to be accurate as at its issue date. While such material is published with necessary permission, and while all reasonable care has been taken to ensure that the information in this article is complete and correct, to the maximum extent permitted by law neither PFSL nor any company in the Pendal group accepts any responsibility or liability for the accuracy or completeness of this information.

Any projections contained in this article are predictive and should not be relied upon when making an investment decision or recommendation. While we have used every effort to ensure that the assumptions on which the projections are based are reasonable, the projections may be based on incorrect assumptions or may not take into account known or unknown risks and uncertainties. The actual results may differ materially from these projections.