Australia is as good a place as investors can be in this tough environment, says Pendal’s head of equities CRISPIN MURRAY

A UNIQUE collision of global challenges is clouding the outlook for equities in the near term, but Australia remains well-positioned to outperform, says Pendal’s head of equities Crispin Murray.

Four major challenges are hitting markets simultaneously, says Murray: the crisis triggered by Russia’s invasion of Ukraine, impending interest rate rises, the pandemic and the re-emergence of inflationary pressures (though Australia doesn’t face the same inflation challenges as other parts of the world).

“It’s not a great short-term message — we think markets are going to continue to struggle,” says Murray, speaking to investment professionals this week in his bi-annual Beyond the Numbers webinar.

Watch a replay of Crispin’s webinar here (registration required):

“There are however, two silver linings,” he says.

“The first one is that Australia is perhaps the most defensive market in the environment we’re in.

“And the second one is that when you see this sort of drawdown in financial markets, there tends to be an indiscriminate nature to those sell offs and they often lay the foundations for some of the best investment opportunities that we will be able to take advantage of over the next few years.”

Reliance on Russian commodities

Russia’s unprovoked invasion of Ukraine has first and foremost led to a terrible humanitarian disaster.

But it has also exposed the West’s reliance on Russia’s commodity exports and demonstrated that while Russia may be a mid-sized economy, it plays an outsized role in the global economy due to its commodity exports, says Murray.

Europe’s oil and gas purchases from Russia are in the order of 1 billion euros a day.

But government sanctions over the invasion are only part of the story of the global economy’s reaction.

Instead, widespread self-sanctioning is seeing companies avoiding trading with their Russian counterparts for fear of being seen to support the invasion.

Pendal Focus Australian Share Fund

Now rated at the highest level by Lonsec, Morningstar and Zenith

“What the Western governments were thinking would be minimal disruptions to these key commodities is turning into major disruptions,” says Murray. Estimates are that half of Russia’s 5 million barrels a day of oil exports is failing to find its way to market.

The result is a commodity price melt-up — prices are soaring.

This leads to the second big pressure point for markets in inflation.

Recent spikes in inflation have been driven by short term issues like COVID-related supply chain disruption, a tightening labour supply driving real wages higher and commodity capacity constraints, says Murray.

But now longer-term issues are taking over as the core inflation drivers, including rebuilding supply chains, declining working age populations, the investment required to build a clean energy economy and China’s shift away from exports to a domestic self-sustaining economy.

“The challenge we’ve see over the last few months is that a lot of these inflationary pressures are becoming self-reinforcing,” says Murray.

“History will look back and judge policy decisions in 2021 as some of the worst that we’ve seen in many decades.

“The reason is that we had a supply shock brought about by the pandemic and the policy response was to continue to stimulate demand and that’s led to this inevitable inflationary pressure.”

Murray says it’s important to remember that inflation can choke itself off: “Prices of goods go up high enough, chokes off demand, people don’t have the spending power, economy slows and inflation goes away.”

But inflation can become sustained if it is underpinned by rising wages.

“We’re at effectively full employment in the US, and that’s leading to higher wages.”

Outlook for rates

The question of how far interest rates will need to rise to combat inflation is key to the outlook for markets.

Murray says there are two schools of thought for how rates will play out.

One school believes rates will not need to be lifted as much as the market fears, due to deflationary forces and excess debt.

Sustainable and

Responsible Investments

Fund Manager of the Year

That would lead to markets briefly correcting before rotating back quickly to long duration growth stocks, he says.

The second school of thought is that rates will need to rise and stay higher for a sustained period of time, similar to the period pre-GFC when the economy ran strong for years before slowing.

“If that is the model we’re looking at, then interest rates will have to go up materially more perhaps than the markets are thinking,” says Murray.

“This is the key debate from a macro point of view that we need to track,” he says.

Ironically, in the past, policymakers would likely respond to a geopolitical crisis by easing monetary policy, but that is highly unlikely this time.

“So, this is why near term we’ve got this irreconcilable conflict between these conflicting goals for policymakers.”

Where Australia fits

So, where does Australia fit in all this?

Surprisingly well, says Murray.

“Australia is as good a place as you’re going to be in this tough environment,” he says.

Partly this is because of the old-world make-up of the Australian stock market, dominated by finance, mining and energy companies.

But also, Australian companies are performing quite well.

Murray says Australian equity markets are declining despite improved earnings as a de-rating of prices due to higher interest rates and rising risk aversion is outweighing a good underlying earnings performance.

“So, what we’re seeing in markets so far is a reduction in the valuations rather than any earnings effect — if that remains the case, that would suggest that this is a correction within a longer term bull market, rather than the beginnings of a bear market.”

About Crispin Murray and Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia. Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Expect to see a lot more mentions of stagflation this year. TIM HEXT explains what it means for investors

WE’VE talked a lot recently about the easy days of central banking ending.

Russia’s invasion of Ukraine has sent this into overdrive.

Stagflation — a stagnating economy combined with rising prices — is a central bank’s worst nightmare. Should they risk sending the economy into recession to tackle inflation?

It is a scenario they haven’t had to face for about 40 years.

Inflation has reared its head since then, but it was always demand led. Slowing the economy was seen as responsible and investors were generally doing well.

Last week US Fed chair Jerome Powell was asked by Senator Richard Shelby if he was “prepared to do what it takes without any reservation” to tackle inflation.

Senator Shelby referenced former Fed chair Paul Volcker who aggressively tackled stagflation in the early 1980s — just before the US moved into a recession.

It was clearly a dig at Powell’s so far muted response to rising inflation.

If taken at face value US rates may need to go far higher than the current 2% factored in by markets.

In Australia, Governor Philip Lowe is still living in 2020, claiming inflation is not yet clearly sustainable within the 2-3% band.

He is sort-of correct — just the wrong way around.

It looks like inflation will be sustainably above 3% this year and next, potentially hitting 5% on an annual basis. No doubt he will be forced to change the narrative soon.

Stagflation will get a lot more mentions this year.

Powell said a clear “yes”.

Find out about

Pendal’s Income and Fixed Interest funds

We will have to dust off the textbooks, having not lived or at least invested through it.

Suffice to say it is bad news for most of us, seeing not only our investments but also our spending power go backwards.

Another complicating factor for super funds is that stronger commodities may end up meaning a stronger AUD.

Since more than a third of assets sit offshore unhedged, super funds normally rely on risk-off moves driving a weaker AUD, somewhat reducing the negative performance.

A stronger AUD but weaker risk markets will increase the drag on asset returns.

As long as wages don’t lock in with inflation shocks — creating the vicious circle we saw in the 1970s — supply will eventually return to commodity and goods markets.

It just may not be a 2022 story — or even 2023.

Meanwhile will rate hikes assure another downturn as the cycle lives on?

A Pendal statement on Russia’s invasion of Ukraine

During these tragic times, Pendal’s sympathy lies with the people of Ukraine in their struggle to maintain their freedom.

As responsible investors, Pendal Group and its affiliates J O Hambro Capital Management, TSW and Regnan have taken decisive steps to reduce our already minimal exposure to Russian securities.

We are limiting direct risk in client portfolios and taking decisive steps to comply with evolving sanctions and restrictions. We will refrain from investing in Russian and Belarusian securities for the foreseeable future.

The situation is evolving rapidly and we continue to monitor the emerging risks, which may take an unexpected form as the consequences ripple through the financial and economic systems.

As active managers, our purpose is to navigate our clients through a world in flux to protect their interests during uncertain times.

About Tim Hext and Pendal’s Income & Fixed Interest boutique

Tim Hext is a Pendal portfolio manager and head of government bond strategies in our Income and Fixed Interest team.

Tim has extensive experience in banking, financial markets and funding including senior positions with NSW Treasury Corporation (TCorp), Westpac Treasury, Commonwealth Bank of Australia, Deutsche Bank, Bain & Co and Swiss Bank Corporation.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia.

Find out more about Pendal’s fixed interest strategies here

About Pendal

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

In 2023, Pendal became part of Perpetual Limited (ASX:PPT), bringing together two of Australia’s most respected active asset management brands to create a global leader in multi-boutique asset management with autonomous, world-class investment capabilities and a growing leadership position in ESG.

Be wary about holding growth assets right now — and consider some rotation to bonds says Pendal’s OLIVER GE

RUSSIA’S unprovoked invasion of Ukraine continues to attract sanctions aimed at limiting the terrible human toll in that part of the world.

The financial implications of those sanctions are of course reverberating far and wide in markets around the globe — and few investors would argue against such action.

But what does it mean in terms of asset allocation? Especially if the sanctions cause Russia to default?

“There is an increasing chance that Russia might default and that has implications for Europe,” says Oliver Ge, a portfolio analyst with Pendal’s Income and Fixed Interest team.

“That in turn hurts the United States and the rest of the global economy.”

“The average investor might take a cursory glance at what’s happening in Ukraine, but I’d argue it’s going to have major ramifications.”

“Russia has about $US640 billion of reserves of which $US400 billion is frozen in central banks around the world. On conservative estimates, it costs about $US1 billion a day to run the war so the impact to Russian coffers is material.”

“Even though energy products haven’t been sanctioned, many global buyers are staying away from Russian energy. If the war is protracted and the sanctions remain in place, pressure on the Russian economy will build.”

“It is also going to be a very challenging environment for neighbouring countries in Europe — not only through the energy channel and its effect on business margins but also through second-order effects via the banking sector in the form of bad debts.

“This will take time to fully play out but we are already seeing the cracks form.”

Financial impact in Australia

“At the start of the year, the consensus forecast for Aussie equities was for growth of about 5 per cent. Not a huge amount but a nice little bump. And that’s driven by the fact that we are in recovery mode.

“That hasn’t happened, predominantly because of Russia’s invasion of Ukraine. It doesn’t matter how much direct exposure our big companies have to Russia — once markets become concerned the effects spread around the world.

“The message to advisers is that if you were told at the start of the year that you’d get 5 to 7 per cent growth, that’s not going to play out in the current state of affairs.”

“So, you should be very wary about holding growth assets and potentially think about some rotation to bonds. Bonds will keep paying,” he says.

“It shouldn’t be a massive rotation, but investors should be more mindful around the expectations of growth assets.”

A Pendal statement on Russia’s invasion of Ukraine

During these tragic times, Pendal’s sympathy lies with the people of Ukraine in their struggle to maintain their freedom.

As responsible investors, Pendal Group and its affiliates J O Hambro Capital Management, TSW and Regnan have taken decisive steps to reduce our already minimal exposure to Russian securities.

We are limiting direct risk in client portfolios and taking decisive steps to comply with evolving sanctions and restrictions. We will refrain from investing in Russian and Belarusian securities for the foreseeable future.

The situation is evolving rapidly and we continue to monitor the emerging risks, which may take an unexpected form as the consequences ripple through the financial and economic systems.

As active managers, our purpose is to navigate our clients through a world in flux to protect their interests during uncertain times.

Find out about

Pendal’s Income and Fixed Interest funds

About Oliver Ge and Pendal’s Income and Fixed Interest team

Oliver is an assistant portfolio manager with Pendal’s Income and Fixed Interest team.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia. In 2020 the team won the Australian Fixed Interest category in the Zenith awards.

With the goal of building the most defensive line of funds in Australia, the team oversees A$22 billion invested across income, composite, pure alpha, global and Australian government strategies.

Find out more about Pendal’s fixed interest strategies here

About Pendal Group

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Here are the main factors driving the ASX this week according to our head of equities Crispin Murray. Reported by portfolio specialist Chris Adams.

Find out about Crispin’s Pendal Focus Australian Share Fund

Find out about Crispin’s sustainable Pendal Horizon Fund

RUSSIA’S invasion of Ukraine is creating second-order effects which the market is struggling to read, leading to dislocations.

We can see two ends of the spectrum in commodities which are “melting up” and European equities (banks in particular) which are plunging.

The markets are facing a four-way collision: the pandemic, a geopolitical crisis, an interest rate tightening cycle and an inflation shock. This is a unique combination.

Historically a geopolitical crisis such as Ukraine and the resulting supply side shock would be partly managed through a reduction in interest rates — as was the 1998 Russian default.

But last week we saw Fed Chair Powell deliver as hawkish a testimony as we have seen in decades.

The market’s saving grace has been the strength of the economy and corporate earnings. But this degree of uncertainty and risk is likely to drive markets lower in the near term.

European markets are bearing the brunt at the moment, but the consequences could spread.

Australia is proving to be the most defensive of markets, with the S&P/ASX 300 up 1.8% last week. It is down 3.5% so far in 2022 compared to -8.2% for the S&P 500 and -13.4% for the NASDAQ. It has also done much better than European or Japanese equities.

We expect this to continue given our combination of commodity exposure, geographic distance, less need to tighten policy and strong economic growth.

Ukraine crisis

Sanctions are becoming more severe, though many are subject to a grace period and so may not yet be fully biting.

There is a notable degree of self-sanctioning, where companies are refusing to buy Russian products. Trade and shipping companies are finding it difficult to insure Russian cargos, or unload them.

In the oil market it is estimated that 2-3 million barrels a day of the 5 million that Russia produce have been effectively removed from the market as a result, creating a squeeze.

Shell has been criticised for purchasing a cargo of Russian oil at a US$28.50 discount to spot. This highlights the public opinion that underpins self-sanctioning.

Shell’s statement — that they could not secure an alternative and had no option other than to stop producing refined products — highlights the growing complexity of supply chains in this environment and the risk of economic disruption.

Debate around potential solutions emphasises the uncertainty and unintended consequences that could eventuate from various courses of action.

For example, there is a view that there needs to be some face-saving scenario for Putin, such as the permanent deployment of troops and nuclear weapons to Belarus. This would result in a higher state of risk for European security than we have seen for some time.

At this point a clean resolution looks unlikely. While current market risk premiums will fall away, there will be a significant strategic shift in the West.

This is likely to see a significant rise in defence spending, an acceleration of the move to renewables, substantial investment in gas storage and the need for reinvestment in strategic commodities.

Pendal Focus Australian Share Fund

Now rated at the highest level by Lonsec, Morningstar and Zenith

In combination, this means substantially more investment spending and less optimised supply chains.

This underpins a higher level of inflation.

Implications for commodities

Oil

Russia’s 5 million barrels a day account for about 12 per cent of global supply. This is already disrupted and hardening public opinion may see the US ban imports of Russian oil, with other countries likely to follow.

The political problem for the West is that at current prices Europe is paying an estimated 1 billion euros a day to Russia.

The question is whether this can be sustained in the face of growing public opposition. We may even see Russia ban exports as a reaction to sanctions. The situation is highly unpredictable.

Russia is believed to have enough storage to house surplus production for 2-3 months. Beyond this they would need to rein in production. Once done, this is hard to unwind. This would present a medium-term constraint on oil supply.

The potential for a deal between the US and Iran adds further complexity.

There is clearly motivation to get a deal done, which could see Iran’s roughly 1 million barrels a day return to global markets. (Although how much is already being sold via other channels is unclear).

This could provide some relief, but this would be short-lived if Russian volumes continue to disappear.

Gas

Russia produces about 8% of global LNG supply (roughly 30 million tonnes per year). Again, this may become hard to replace.

In addition Russia relies on Western technology and companies for infrastructure servicing and repairs. This could lead to further decreases in supply if withheld for an extended period of time.

Another 20 million tonnes of capacity are under construction in partnership with western firms. The latter’s withdrawal could see these projects delayed substantially.

Sustainable and

Responsible Investments

Fund Manager of the Year

In the medium term, Australian gas projects potentially become more attractive given the security of supply and Europe’s desire to reduce reliance on Russian volumes.

Coal

Like oil and natural gas, coal prices are surging on tighter markets.

Russia provides 17% of the world’s thermal coal and 9% of metallurgical coal. This may drive more interest in Australian coal as a reliable alternative, though in the near term it means coal prices are likely to rise to the point where it chokes off demand.

Soft commodities

Russia and Ukraine together supply 25% of the world’s wheat, 24% of its barley, 14% of corn and 58% of sunflower oils.

History suggests agricultural supplies are not disrupted during wars. But clearly there is risk given reliance on the region.

Planting season is from late March into April. The question is whether there will be access to seeds and fertiliser to allow a proper planting. The wheat price rising 50% in 10 days reflects the risk here.

There are also potential second-order effects. A surge in food prices has historically been the catalyst for civil unrest in some countries.

China will also be mindful of their exposure, especially since issues with swine flu are affecting pork supply. Beijing has apparently moved to withhold fertiliser exports to ensure domestic supply to support their crop yields.

Economics

We are seeing unprecedented disruption in the supply of critical commodities.

The longer the invasion continues, the more pressing this issue becomes, underpinning inflation and damaging global growth.

In the US, food accounts for just over 20% of the after-tax income for the lowest quintile of income earners, with gas another 7% or so.

Sustained increases in prices will start to drag on consumption and become more politically sensitive given the disproportionate effect on lower-income workers.

In terms of headline inflation, the average oil price was about US$75 in Q4 2021. Even if it comes back to $100 we are still looking at a 60-80bps increase in headline inflation.

The threat to growth has been the catalyst for a rally in bonds as the market moves to assume less central bank tightening will be required.

For example JP Morgan have cut Q4 2022 global GDP growth by 0.8% to 3.1%, driven largely by a downgrade in the outlook for Europe.

The most protected economies in terms of growth are those with their own domestic commodity supply and self-reliance. The US is in a reasonable position, as is Australia.

So the market is pricing in less rate hikes.

This, along with safe haven flows, continues to push the US dollar higher against most currencies — the Australian dollar being a notable exception.

While this market reaction is understandable, it is worth highlighting Powell’s comment to Congress last week.

The Fed Chair’s comments looked like a clear commitment to bring down inflation regardless of the political consequences.

Powell did not shy away from comparisons to Paul Volcker – notable for draconian measures to bring inflation under control in the 1980s – and agreed he was prepared to “do what it takes without any reservation” to protect price stability.

While the Fed was likely to hike only 25bp in the March meeting, Powell inferred it may need to lift 50bp in subsequent ones.

This highlights the collision between inflation pressure — tied to strong growth, supply chain issues and commodity disruption — and hawkish monetary policy.

There are two major view on how this unfolds over this year, based on two different phases of history:

- The first is that we will see a replay of the 12 years post-GFC, when the market kept anticipating rate rises that did not eventuate until 2018. When they did, they were quickly reversed because the debt burden in the economy meant it could not handle the rise. We suspect the majority of the market still believes this is the world we operate in. This implies a broad expectation that this tightening cycle will not be too severe.

- The counter view is that we revert to the pre-GFC era, when the market was more accurate in predicting rates and extended cycles of increases were needed to slow the economy down. A combination of better household balance sheets thanks to the Covid stimulus; the need for substantially more investment in defence and decarbonisation; the move to shorten and build redundancy into supply chains; and the lack of investment in carbon-emitting industries (notably commodities) could mean we return to something like the pre-2008 environment.

This is currently the key call for markets and positioning.

The latest US payroll data was strong, with 678,000 new jobs versus 423,000 expected. Average hourly earnings grew 5.1%, versus 5.8% expected, which did lend some respite to inflation concerns.

The US has returned to full employment and pre-Covid levels in terms of hours worked, in contrast to the long trough that followed the GFC.

There are only 2.1 million fewer jobs than pre-pandemic. These can be accounted for by lower participation, given the leisure and hospitality sector is still 1.5 million jobs below February 2020 levels — and there is still a lot of tightness in the labour market.

The jury is still out on whether the signal from average hourly earnings represents a turning point.

The numbers have been affected by mixed effects, more growth in lower paid workers and volatility in hours worked due to unwinding of the Omicron disruption.

Markets and ASX reporting season

US equities struggled to follow through on their rally at the end of last week, but have held up relatively well in the face of the poor news.

The S&P 500 fell 0.5% last week. It continues to face the triple headwind of rising oil prices, rising rates and a stronger US dollar.

The Euro STOXX 50 fell 10.4%. The European economy is much more vulnerable to the challenges highlighted above. But it is unusual for markets to disconnect to this degree in the short term and the relative moves need to be watched to see if acts as a lead indicator.

Australia’s bounce reflected a “catch-up” on the US for the prior week. It also reflects the higher weighting in mining and energy companies.

There has been huge dispersion this year on the ASX. The Energy sector is up 25.4% versus a 10.2% fall in the bond-sensitive AREIT sector. Nevertheless, this move remains small in a historical context, suggesting there could be plenty more to go.

The key conclusion from reporting season is that the underlying performance of Australian companies is in good shape, with the number of positive revisions almost double the long-term average.

One theme was that lower multiple stocks saw better revisions, reflecting an improved outlook for the domestic economy and higher rates helping financials.

Overall earnings per share (EPS) for the market is set to grow 13.8% for the financial year, versus 11.5% expected in January. This leaves the price/earnings ratio on 15.4x. At this point FY23 is expected to see flat EPS growth.

Looking at the market’s components:

- Industrials: EPS for FY22 rose to 5.8% from 4.8% and the sector trades on 27x PE. FY23 EPS growth is now expected to be 13%, down from 14% previously.

- Banks: EPS growth for FY22 increased to 13% from 11.2% previously and it trades on 13x P/E. FY23 expectations shifted from 6.8% EPS growth to 6.1%.

- Miners: The market is expecting 10% EPS growth in FY22, then -17% in FY23. It trades on 9.3x PE.

- Energy: EPS expected to be +77% for FY22 and +6% in FY23. Trades on 11x P/E. Clearly both energy and mining could see material changes to these numbers.

The earnings shifts within the market mean the unwinding of the growth premium has not been as material as price movements would indicate.

There was not too much to report at a stock level post reporting season.

Resource and energy stocks saw strong rotation last week as commodity prices rose.

Insurance stocks were hit by the floods, although they all have a lot of protection from reinsurance contracts and the price reaction is substantially overstating the cost.

About Crispin Murray and Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia. Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

During these tragic times, our sympathy lies with the people of Ukraine in their struggle to maintain their freedom.

As responsible investors, Pendal Group and its affiliates J O Hambro Capital Management, TSW (Thompson, Siegel & Walmsley) and Regnan have taken decisive steps to reduce our already minimal exposure to Russian securities.

We are limiting direct risk in client portfolios and taking decisive steps to comply with evolving sanctions and restrictions.

We will refrain from investing in Russian and Belarusian securities for the foreseeable future.

The situation is evolving rapidly and we continue to monitor the emerging risks, which may take an unexpected form as the consequences ripple through the financial and economic systems.

As active managers, our purpose is to navigate our clients through a world in flux to protect their interests during uncertain times.

Stocks that could benefit from inflation, the role of carbon credits in portfolios, what’s driving India in EM, two events to watch closely next week.

Amid all the disheartening news this week there was a bright spot in Australia’s GDP numbers. ANNA HONG explains in our weekly Income and Fixed Interest note

IT HAS been a tough week filled with geopolitical and humanitarian tensions, as well as the flood crises impacting us.

Clearly there is plenty of bad news to go around and our thoughts are with everyone impacted.

Market volatility is making portfolio positioning challenging — we still believe rate hikes and rising yields are on the agenda in the medium-term.

But this week’s Australian GDP numbers brought a much-needed pleasant surprise.

A bright spot for a once hard-hit industry reminded us of the general resilience of the wider economy.

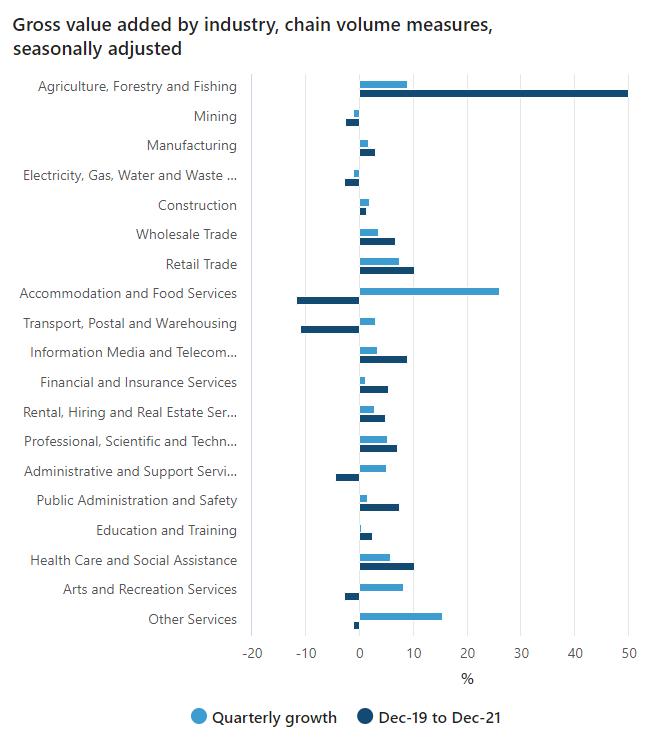

The Farm sector posted a 9 per cent growth in the last quarter and a whopping 50 per cent growth since the 2019 droughts as you can see below:

While March 2020 will always be associated with the outbreak of Covid globally, that month was significant in Australia for other reasons.

At that time Australia suffered through hailstorms, cyclones and bushfires to cap off a horror run of droughts from 2017 to 2019. That led to Farm GDP declining 22% in that period.

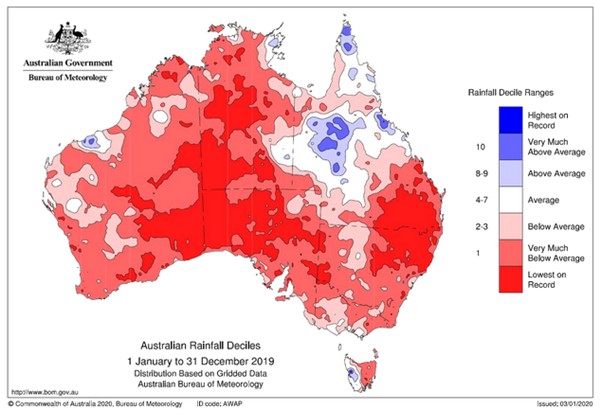

Australia experienced its warmest and driest year on record in 2019. Large areas were affected by high temperatures and well-below-average rainfall.

Those conditions contributed to one of the worst bushfire seasons on record.

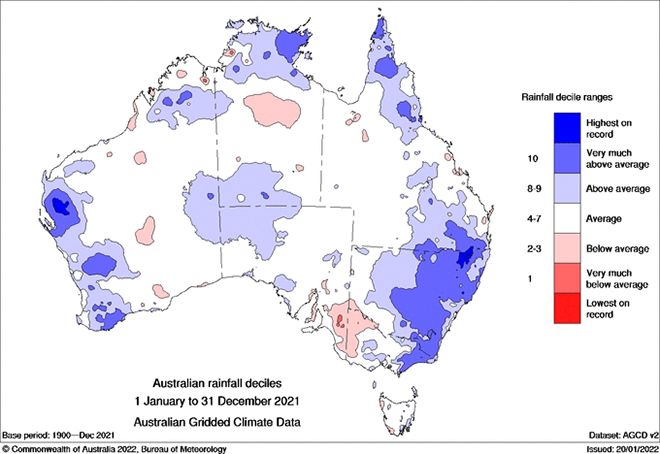

Fast forward to 2021-22 and the cooler La Nina weather pattern is painting a very different picture, as these maps from the Bureau show:

Outlook

This recovery demonstrates the resilience of the Australian society and economy.

Growth has rebounded, unemployment is down, prices are higher.

The agriculture industry presents the same thematic as the broader economy. It’s now running close to full capacity with labour shortages a significant constraint, leading to rising prices.

Despite geopolitical issues and setbacks from the flood, we are now firmly in a rate hike cycle globally as central banks stay focused on tackling inflation.

Until the dust settles, it remains to be seen if demand-led inflation or stagflation (covered by our head of government bonds Tim Hext in last week’s weekly note) will emerge as the front-runner.

Find out about

Pendal’s Income and Fixed Interest funds

About Anna Hong and Pendal’s Income and Fixed Interest team

Anna Hong is an assistant portfolio manager with Pendal’s Income and Fixed Interest team.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia. In 2020 the team won the Australian Fixed Interest category in the Zenith awards.

With the goal of building the most defensive line of funds in Australia, the team oversees A$22 billion invested across income, composite, pure alpha, global and Australian government strategies.

Find out more about Pendal’s fixed interest strategies here

About Pendal Group

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

What economic conditions would make the RBA happy? Pendal’s head of government bond strategies TIM HEXT has some answers

I SPOKE last week about central banks needing tighter conditions to help limit inflation in our Income and Fixed Interest Weekly note.

I mentioned the term a “hawkish hike” which prompted a number of readers to ask: “aren’t all hikes by definition hawkish?”

The answer is that they are… but the accompanying statement is a chance to influence expectations of future hikes.

This is especially so in countries where longer term fixed rate home loans are predominant – no point hiking and seeing them go nowhere. We expect the Fed to do this in their March hike, possibly pushing up the terminal level of rates as well. This will not be bond friendly.

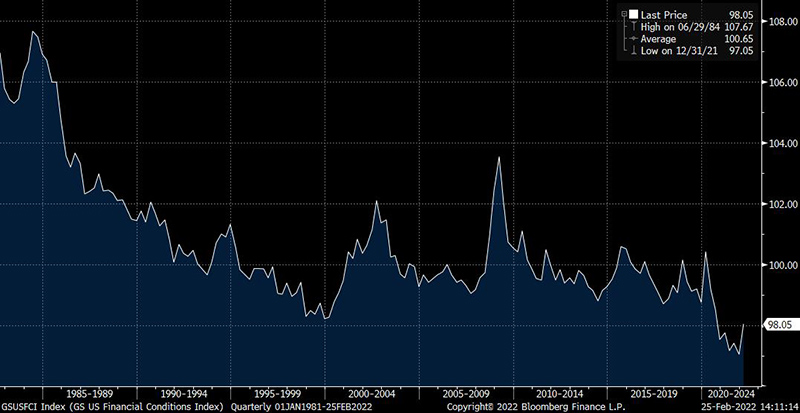

In the US Goldman Sachs produces a Financial Conditions Index (FCI) to try and capture this wider view.

The FCI is largely made up of 10-year nominal Treasury yields and Corporate Bond spreads (as measured by non-financial BBB bonds 15+ years). They also include equities, the TWI and the Fed Funds rate — though these are much smaller.

The important point is that moving Fed Funds — while other indicators stay put — does not tighten financial conditions.

Find out about

Pendal’s Income and Fixed Interest funds

They need to see a measured sell-off in term rates. Wider credit spreads help. Lower equities also help, provided they don’t go into a tailspin.

Any Fed ‘put’ for markets (where they jump in to protect them) is a very long way from here.

What would make the RBA happy

In the Australian context, the RBA would be extremely happy if by the end of 2022 inflation is at 3.25%, unemployment sub 4%, wages 3.5%, equities 10% lower, 10-year bonds 2.75% and cash rates 1%.

It is not the RBA’s job to make sure superannuation balances have positive performance in any given year. Or to protect house prices.

Given the massive rises in 2021 a negative year for assets is not a major setback. A year where labour outperforms capital is long overdue.

Of course, the Ukraine disaster will have an impact. But prospects of higher inflation will mean the Fed will need to get on with its hiking path, even if near-term risk markets are unsettled.

About Tim Hext and Pendal’s Income & Fixed Interest boutique

Tim Hext is a Pendal portfolio manager and head of government bond strategies in our Income and Fixed Interest team.

Tim has extensive experience in banking, financial markets and funding including senior positions with NSW Treasury Corporation (TCorp), Westpac Treasury, Commonwealth Bank of Australia, Deutsche Bank, Bain & Co and Swiss Bank Corporation.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia.

Find out more about Pendal’s fixed interest strategies here

About Pendal

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

In 2023, Pendal became part of Perpetual Limited (ASX:PPT), bringing together two of Australia’s most respected active asset management brands to create a global leader in multi-boutique asset management with autonomous, world-class investment capabilities and a growing leadership position in ESG.

Here are the main factors driving the ASX this week according to our head of equities Crispin Murray. Reported by portfolio specialist Chris Adams.

Find out about Crispin’s Pendal Focus Australian Share Fund

Find out about Crispin’s sustainable Pendal Horizon Fund

MARKET reaction to Russia’s invasion of Ukraine was more subdued than many would have expected, though there has been underlying volatility.

The S&P500 actually ended up last week, gaining 0.8%. This is possibly because the market had already priced in a high probability of conflict – alongside the underlying issue of higher rates.

Sentiment was cautious as a result. The view that sanctions would not cover key commodities and NATO forces would not engage on the ground tempered perceived near-term impact on the broader global economy.

A spike in gold, oil, wheat and other commodities unwound in the space of a few hours. This was a catalyst for recovery in parts of the market that initially fell the most.

The domestic market was hit harder than the US with the S&P/ASX 300 off 2.4%. This seems mainly due to anticipation of a more negative reaction in offshore equities.

This sentiment-driven fall overwhelmed a reasonably positive final week of reporting season, which underpinned the consistent message that the domestic economy looks set to recover well while cost pressures are building in certain areas.

Recent market caution could mean the late-week bounce continues, likely led by growth stocks.

But we remain wary this will persist given liquidity withdrawal has not yet started. Economic strength will probably also continue to underpin inflationary pressures, which could be exacerbated by the geopolitical risks triggered by Russia last week.

This makes the policy response even more challenging.

Pendal Focus Australian Share Fund

Now rated at the highest level by Lonsec, Morningstar and Zenith

This will be combined with a reappraisal of energy policy in the West. Significant sums will need to be invested to accelerate the energy transition and build resilience in the supply of energy and other critical commodities.

This reinforces this long-term theme of far higher levels of investment which underpin commodity demand.

Economics and policy

Some are questioning whether central banks will delay rate hikes in response to the Ukraine crisis.

This is unlikely in our view — the level of inflation is just too high to delay action. The only small shift is that the probability of the Fed hiking rates 50bp in March has fallen.

Economic momentum appears to be building, particularly in the US. We have seen incomes remain strong, unemployment claims hit 52-year lows, Covid cases decline and strong capital goods shipments and house prices accelerate.

US personal income growth has now cycled through all the additional hand-outs people were receiving.

While it fell marginally below the growth in outlays for the first time since Covid struck, the savings rate remains in normal territory. This indicates households have been able to maintain spending without dipping into the excess savings built up over the past two years.

Sustainable and

Responsible Investments

Fund Manager of the Year

The Citi Economic Surprise Index is on the rise again. This measures the difference between reported economic data and consensus expectations (it rises when the data is better than consensus).

Unlike the 2018 rate raising cycle when the Fed raised four times while data was starting to disappoint, this is not the case currently.

This will be a signal to watch as rates rise.

Markets

The combination of high volatility and a growing use of short-dated options by retail and institutional investors has exacerbated recent market moves.

This year we have seen rising volatility force investors to sell down risk. This can have a self-reinforcing effect due to the technical nature of options.

The sharp bounce at the end of last week shows this trend can operate in reverse — which may be supportive in the near term, particularly if volatility starts to subside.

Current volatility levels signal daily moves of 1.5% in US equities, so it is plausible this subsides. However in our view this would be a technical bounce and we are still working through a correction as liquidity becomes a headwind.

That said, we note that sentiment indicators remain at the more pessimistic end. US domestic equity fund inflows have still not reversed — though this will be something to watch as liquidity is withdrawn.

In terms of other assets oil is very hard to call in the near term.

There is still a potential for a deal between the US and Iran, which is probably worth $10-15 off the price in the near term. There is also the threat of releasing strategic reserves. But the medium-term fundamentals are supportive given low inventory, improving demand and potential supply disruption.

Soft commodities are the other key sensitive area to watch given the political consequences of high food prices. Wheat traded almost identically to oil.

Aussie stocks

Domestic market moves were dominated by the Ukraine news, which muted reactions to positive results such as NEC and exaggerated negative reactions.

Banks underperformed after a good run on initial concerns that the rise in rates may be slowed given geopolitical uncertainty. That narrative has quickly unwound.

The 32% bounce back in Block(SQ2) (formerly Afterpay) on Friday highlighted the potential for a positioning unwind in this market.

The underlying themes for reporting season have been constructive with regard to the domestic economy. Rising costs are an issue, the ability to price for it is key.

About Crispin Murray and Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia. Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

A weekly comment from Pendal’s head of government bond strategies, Tim Hext

WHEN it comes to bonds, some things are easy to read.

Strong data normally means inflation pressure which means yields sell off. And vice versa.

But events such as this week’s Ukraine crisis are less clear.

Do you jump on risk off and buy bonds? Or do you fret that already high inflation pressures are going to worsen, forcing central banks to tighten more?

This is a glimpse into the complicated world of stagflation.

Even career central bankers such as RBA governor Phil Lowe have only distant memories of stagflation.

Like most, he has largely operated for 30 years in a world of solid growth but low inflation.

Policy could be cautiously eased, unemployment falls and asset prices boom. Life is great for central bankers.

Hit the reverse button though and choices become very hard.

Now is such a time.

The US Fed needs to get financial conditions tighter in the US — they remain near all-time lows despite very high inflation, as you can see in the Goldman Sachs Financial Conditions Index below:

The Ukraine events may hit sentiment in Europe and even globally, but sanctions will push commodity prices even higher.

There is a left tail risk it worsens. But logic (and hope) suggest Putin’s aim is to install a Russia-friendly (or at worst neutral) buffer between him and NATO, rather than to expand further.

We think the US Fed may tip its hat to events by only going 25bp in March. But it will be a hawkish hike — that is, they need long-end yields to move higher to tighten conditions and rein in inflation.

This is especially so in an economy where mortgages are tied more to long-term, not short-term rates.

We saw such a thing from the RBNZ this week, which went out of its way to increase forward expectations despite only hiking 25bp not 50bp.

Find out about

Pendal’s Income and Fixed Interest funds

This week’s events have not fundamentally changed our view that equities drift lower and bond yields higher over 2022.

After all that’s how you get tighter financial conditions.

What central banks want they can engineer — at least short term.

The 2021 halcyon days for asset markets are fading fast.

About Tim Hext and Pendal’s Income & Fixed Interest boutique

Tim Hext is a Pendal portfolio manager and head of government bond strategies in our Income and Fixed Interest team.

Tim has extensive experience in banking, financial markets and funding including senior positions with NSW Treasury Corporation (TCorp), Westpac Treasury, Commonwealth Bank of Australia, Deutsche Bank, Bain & Co and Swiss Bank Corporation.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia.

Find out more about Pendal’s fixed interest strategies here

About Pendal

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

In 2023, Pendal became part of Perpetual Limited (ASX:PPT), bringing together two of Australia’s most respected active asset management brands to create a global leader in multi-boutique asset management with autonomous, world-class investment capabilities and a growing leadership position in ESG.