When rates start going up, how far will they go? It’s a question Pendal’s head of government bond strategies TIM HEXT has been thinking about a lot lately

WE have just released our latest Income and Fixed Interest Quarterly Report (contact a Pendal business manager for a copy) and I have spent my time recently questioning market pricing.

Right now nearly everyone is focused on the timing of RBA rate hikes versus market expectations.

The near-term performance of funds we manage is all about solving that one.

But the issue that’s been occupying my mind — and I write about in the Quarterly — is the long-term question of the terminal rate of a hiking cycle.

In other words, when rates do start going up, how far will they go?

I think rates will move up to 1.5% in 2023. Inflation will peak around 3% in early 2023 before tapering off back to 2.5%, led by modest goods price deflation kicking in.

This will see the RBA happy to leave cash rates there for at least a year or more.

Find out about

Pendal’s Income and Fixed Interest funds

Consensus is that 1.5% cash rates will see out the rate-hike cycle. The logic is that a 2% rise in mortgage rates would hit the economy hard.

But as the decade unfolds and investment remains strong, real yields could move modestly positive once more.

That would mean cash rates closer to 2.5% than 1.5% and bond rates nearer 3% than 2%.

I doubt markets will factor this in for some time, but it’s a risk to consider for long-term asset allocators.

Of course in the meantime — with cash stuck near zero — it is expensive to be too underweight fixed interest.

Now rates have backed up, fixed interest is once again playing its part as a defensive asset.

For those of us managing portfolios, we must play the short term while keeping in mind the medium term.

We’ll leave long term to the custodians of superannuation funds whose time horizons allow for it.

About Tim Hext and Pendal’s Income & Fixed Interest boutique

Tim Hext is a Pendal portfolio manager and head of government bond strategies in our Income and Fixed Interest team.

Tim has extensive experience in banking, financial markets and funding including senior positions with NSW Treasury Corporation (TCorp), Westpac Treasury, Commonwealth Bank of Australia, Deutsche Bank, Bain & Co and Swiss Bank Corporation.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia.

Find out more about Pendal’s fixed interest strategies here

About Pendal

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

In 2023, Pendal became part of Perpetual Limited (ASX:PPT), bringing together two of Australia’s most respected active asset management brands to create a global leader in multi-boutique asset management with autonomous, world-class investment capabilities and a growing leadership position in ESG.

What’s the role of fixed income in portfolios right now? Here’s a quick snapshot from Pendal’s head of income strategies AMY XIE PATRICK

IT’S been a tough year for fixed income.

Fuelled by bouts of inflation tantrum, a rise in yields drove one-year total returns on most major fixed income benchmarks into the red by early November.

Only high-yield benchmarks delivered positive returns — mostly due to the recovery of credit spreads that took place at the start of the year.

Though this doesn’t help the average fixed income allocation much, since the risk-and-return profile of global junk debt is more akin to equities than fixed income.

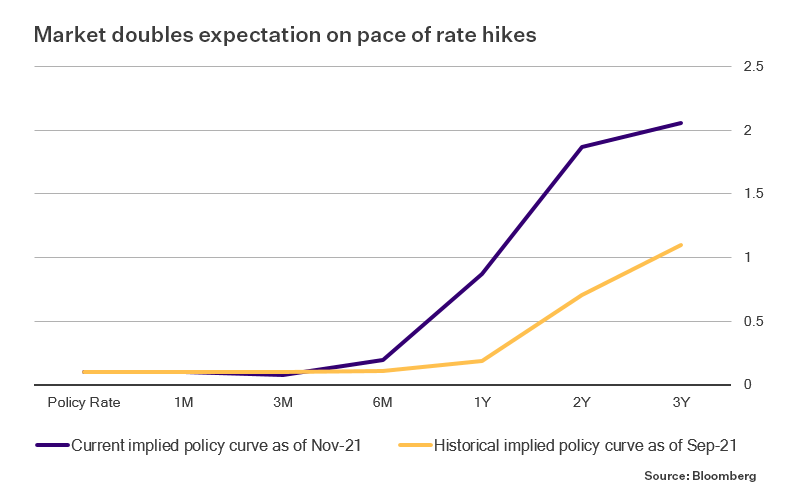

The market currently out-hawks all central banks, pricing in a steeper path of normalisation than policy makers are willing to concede.

As you can see in the below chart, since the end of September the market has doubled its expectation around the pace of rate hikes in Australia.

That leaves a decent buffer for central banks to get “pulled-to-market” if they are wrong — and a lot of room for yields to fall if they are right.

Such a steep path of rate hike expectations leave little room for error. The latest Omicron Covid variant is a case in point.

Let’s also not forget the efficiency of markets that run ahead of hiking cycles.

From 2004 to 2006, Alan Greenspan’s Fed raised policy rates by 425bps. Over the same period, yields on US 10-year Treasuries rose a mere 33bps.

Any hiking cycle now would be hard pushed to even match half of Greenspan’s pace.

Even with inflation still rising, fixed income has an important role to play.

Its negative correlation to equity markets delivered a poor return outcome for the asset class in 2021.

But overall, portfolios have benefited from the tear that risk assets have been on.

In times of market stress that negative correlation will prove invaluable.

Compared to a year ago, 10-year government bonds in Australia now provide 85bps more yield.

There is now a fatter cushion to absorb any macro stumbling blocks lurking on the horizon.

About Amy Xie Patrick and Pendal’s Income and Fixed Interest team

Amy is Pendal’s Head of Income Strategies. She has extensive expertise and experience in emerging markets, global high yield and investment grade credit and holds an honours degree in economics from Cambridge University.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia. The team oversees some $20 billion invested across income, composite, pure alpha, global and Australian government strategies.

Find out more about Pendal’s fixed interest strategies here

About Pendal Group

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

Pendal’s head of equities Crispin Murray and his team have access to Omicron analysis from a variety of leading virologists and epidemiologists. Here are Crispin’s observations so far.

NEAR TERM, the emergence of Omicron is concerning because the sheer number of variations in the virus — notably the spike protein which the vaccines target — are very likely to render vaccines less effective in preventing the spread of the virus.

The Moderna CEO said as much in the Financial Times this week.

The transmissibility of Omicron is likely to be greater than previous variants, but it is still unclear to what extent.

Although the number of reported cases in South Africa has accelerated far faster than Delta, it’s unknown how long the variant was already seeded in the community or subject to super-spreading events.

The datasets are still too small to be more definitive.

We believe comments that Omicron may be less virulent — that it will lead to fewer hospitalisations — are premature.

Pendal Focus Australian Share Fund

Now rated at the highest level by Lonsec, Morningstar and Zenith

This view is based on observations in South Africa rather than data from a trial. It can be influenced by a variety of factors such as age and the number of previous infections a patient person has had.

Mitigating this uncertainty are a number of observations:

1. Thanks to South African scientists we’ve identified this variant at an earlier phase than Delta. This limits the level of seeding in other countries, containing the spread and buying time for a scientific response

2. While vaccines may no longer be as effective in stopping transmissibility, there is a reasonable expectation they will continue to be effective in lessening the effects of the virus through the response of B and T cells — which play an important role in our body’s Covid defence system

3. The advent of anti-viral medicines should reduce the health consequences of those infected

4. The impact of each subsequent wave has been less material on the economy as responses become more targeted and people become more attuned to the risks

5. We are seeing accelerating economic momentum globally. This is different to what we saw when the Delta wave began to emerge in May and June.

Corporate responses to date have been along similar lines: they will wait until we have more data and a better understanding before taking any potential responses to the new variant.

What if current vaccines prove to be ineffective against Omicron?

The mRNA suppliers say they have already been working on new versions of the vaccine.

They indicate it could take 100 days to develop an Omicron vaccine — and about six months to become available at a mass level, subject to regulatory approvals.

About Crispin Murray and Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia. Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Find out more about Pendal Focus Australian Share Fund here.

Here are the main factors driving the ASX this week according to portfolio manager Jim Taylor. Reported by portfolio specialist Chris Adams

THE emergence of Omicron halted a week of positive news flow in its tracks.

Before Thanksgiving in the US, the market had been gaining confidence that the Chinese government was taking steps to underpin economic growth and stem the risk of a sharper slowdown.

News that Jay Powell would be appointed for a second term as Fed Chair — coupled with talk of faster tapering —bolstered the view that the US central bank was not falling behind the curve on inflation.

Then Friday saw a sharp risk-off trade after the WHO flagged the Omicron mutation as a variant of concern.

As a result the S&P 500 ended the week down 2.18% and the S&P/ASX 300 lost 1.64%.

Stocks related to the re-opening fell far further. Commodities were generally down (except iron ore), and US 10-year government bond yields fell 7bps.

COVID and vaccines

Prior to the WHO announcement, Covid concerns remained centred on Europe.

Austria re-entered full lockdowns, though other countries resisted this move. Hospitalisations continue to remain very low.

Although the health outcomes in Europe remain encouraging, this wave is being felt in stock prices. Even prior to the Omicron news, re-opening stocks in Europe were under pressure from the latest wave and consequent mobility restrictions.

Find out about

Pendal Focus

Australian Share Fund

Crispin Murray,

Head of Equities

The risk with Omicron is that it may make vaccines less effective.

It has a spike protein dramatically different to the original variant on which the vaccines were based. The spike protein is the component of the virus that binds to cells. Because of these mutations Omicron could have increased resistance to vaccines — plus greater transmissibility and severity compared to other variants.

The WHO said it will take weeks to better understand the efficacy of current vaccines as well as Omicron’s severity in terms of health outcomes and hospitalisation.

Vaccine maker BioNTech said initial lab results on the variant could come within two weeks. Pfizer indicated a variant-tailored vaccine could be available about 100 days after genetic sequencing.

In Australia mobility rates continue to rebound at a similar rate in Victoria and New South Wales. This is despite the fact that new daily cases in Victoria have plateaued at a far higher rate than NSW.

Macro and policy

Jerome Powell was reappointed for a second term as chair of the US Federal Reserve. Lael Brainard replaced Richard Clarida as vice chair.

The markets welcomed this news. Powell’s more hawkish bent (compared to Brainard) is seen as reducing the risk that the Fed would be too loose in the face of inflationary pressure.

This narrative was reinforced by signals from other Fed members that it could withdraw support more quickly from the economy to deal with rising inflation.

Vice Chair Clarida noted they will be watching data between now and the December meeting closely and may have a discussion about accelerated tapering if warranted.

Fed Governor Christopher Waller called for tapering to be possibly done by April, making way for a possible interest rate hike in Q2.

The key argument remains that a combination of easing supply bottlenecks, slowing wage gains on the back of rising labour participation and faster productivity growth ought to bring inflation down without the Fed having to act more aggressively.

Three to six months ago an acceleration of tapering would have been met with great concern by the markets.

But rhetoric from the Fed governors will be priming the market for just such a move. Tapering could be over by mid-March. Rate rises in 2022 are now baked in by the market — perhaps as early as June.

US data prints were generally positive. US Initial Jobless Claims came in at 199,000, well below consensus. It is expected to reverse to about 250,000 before resuming a downward trend to pre-Covid levels of about 210,000.

A re-rebound in existing homes sales continues, rising from 6.2 million to 6.34 million. Consensus expectations were 6.2 million.

The percentage of cash buyers — as opposed to mortgages — has risen from 19% to 24% year-on-year.

Low inventory means prices are still soaring, up 18% annualised in the three months to October. This ensures the rent component of the CPI will continue to rise for some time yet.

Markets

There have been some notable developments in commodity markets.

Over the weekend Peruvian Prime Minister Mirtha Vasquez announced her government planned to close four gold and silver mines that have had conflicts with local communities.

Peru is the world’s second-biggest copper producer after Chile, accounting for about 10 per cent of 2021 global production.

OPEC+ has indicated they see the release of strategic reserves by countries such as the US as unjustified in current conditions and they may respond with higher production when they meet next week.

Sustainable and

Responsible Investments

Fund Manager of the Year

Bonds had been selling off very calmly and modestly over the course of the prior week, rallying very strongly on Friday with US 10-year government yields up 15bps.

More generally the underperformance of the non-mega cap tech stocks in the US continued last week.

There was very little in the way of stock-specific news for the Australian bourse.

Materials continued their recent strength with increasing comfort that China was addressing the growth problem they have engineered.

The iron ore miners were among the week’s best performers. Fortescue Metals (FMG) was up 11.12%, Mineral Resources (MIN) +5.20%, Rio Tinto (RIO) +4.66% and BHP (BHP) +4.33%.

AMP (AMP, -11.89%) was the weakest on the ASX 100 after management flagged impairment charges.

Tech names were generally weaker. Friday’s Omicron news saw re-opening stocks such as Qantas (QAN, -8.76%) hit hard.

About Jim Taylor and Pendal Focus Australian Share Fund

Drawing on more than 25 years of experience investing in top-performing Australian companies and a background in accounting, Jim manages our Long/Short Fund and co-manages our Imputation Fund. He is a Chartered Accountant with membership of the Australian Institute of Chartered Accountants.

Pendal Focus Australian Share Fund is managed by Crispin Murray. The fund has beaten its benchmark in 12 years of its 16-year history (after fees), across a range of market conditions. Find out more about Pendal Focus Australian Share Fund here.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

A monthly insight from James Syme and Paul Wimborne, managers of Pendal’s Global Emerging Markets Opportunities Fund

WE have seen high inflation prints across the world in recent months.

Meanwhile, volatility in interest rate expectations and sell-offs in government bond markets are testing the resolve of central banks — which have mostly been sticking to the view that the current inflation spike will prove to be transitory.

In some developed markets there has been significant pressure on central banks, including those of the UK, Australia and Canada.

The governor of the Bank of England said their monetary policy committee would “have to act” if inflation in the prices of consumer goods and energy fed through to inflation expectations.

The Reserve Bank of Australia had to abandon its yield curve control policy (which had pegged 2024 government bond yields at 0.1%).

The bank had stopped supporting the policy as fears about inflation were priced into bond markets through October, with yields on the April 2024 government bond rising from 0.05% at the start of October to 0.78% at the end of the month.

Similarly, October saw the Bank of Canada catch rates and bond markets by surprise, ending its government-bond purchase program and accelerating expectations for when it might start hiking policy interest rates.

Find out about

Pendal Global Emerging Markets Opportunities Fund

Emerging market central banks have not been immune from this shift.

Many emerging markets have variously seen inflation data that is high or above expectation, and sharp shifts in central bank policy.

Brazil

Brazil has seen an aggressive sell-off of government bonds in recent months, which intensified in October. Inflation data has been difficult with both September and October CPI printing above 10% YoY.

Inflation expectations continue to increase, with the five-year breakeven inflation rate now over 6%, despite the central bank (the BCB) sticking to its 2024 CPI target of 3%.

More fundamentally, fears of a water crisis (which would have inflationary implications for power pricing) or a relaxation of fiscal discipline ahead of the October 2022 presidential election have undermined confidence in BCB’s inflation-fighting credibility.

This has happened despite BCB hiking rates and the bond market pricing in continued aggressive policy rate increases.

Year-to-date, BCB has hiked the policy interest rate from 2% to 7.75%. But the shorter end of the yield curve has also moved higher by 3% or more, leaving the BCB much to do.

As we have discussed in previous commentary, this is very much driven by the inflationary outlook. The Brazilian real looks to us fundamentally cheap and the external financial position of Brazil remains very strong.

That does not, however, prevent the drag on economic activity and corporate earnings from a one-year real interest rate (adjusted for inflation expectations) of over 6%.

Central and Eastern Europe

Another region where, for different reasons, there has been a sharp shift in inflationary and interest rate expectations is Central and Eastern Europe.

The greatest shift has been in Poland, where an Australia-style move in the front-end of the yield curve forced the central bank to hike rates from 0.1% to 0.5% in the October meeting (when a hold had been expected) and then to hike again from 0.5% to 1.25% in the November meeting (when a much smaller hike had been expected).

The Czech central bank has also shocked markets with the speed and scale of rate hikes, with a tightening phase that began with a move from 0.25% to 0.5% in June 2021 accelerating to leave policy interest rates at 2.75% at the time of writing.

Sustainable and

Responsible Investments

Fund Manager of the Year

It is not clear that Russia has serious inflationary problems, but the central bank, the CBR, has a reputation as one of the most orthodox and hawkish central banks in EM and has steadily hiked ahead of expectations through the year.

But there are bright spots…

Amid this pattern of central banks potentially getting behind the inflationary expectations curve and having to then hike rates aggressively to catch up, there are bright spots.

Some emerging markets, despite seeing higher fuel prices and economic recoveries, have seen moderate increases in inflation and have even been able to leave policy interest rates on hold at levels that are overall stimulative.

This group absolutely includes India, which has seen inflation tick lower in recent months (to 4.35% in the year to September), allowing the Indian central bank to remain on hold, with policy rates at 4%.

Other markets have also been able to remain on hold, including Indonesia (on hold at 3.5% with inflation to October of just 1.7%), and South Africa (on hold at 3.5% with inflation to September of 5.0%).

US monetary policy impact

Clearly the overall direction of financial conditions in emerging markets will also be driven by the direction of US monetary policy.

The US Federal Reserve has kept short-term interest rates near zero. But bond markets are steadily pricing in interest-rate increases in 2022, with futures suggesting the most likely increase is two 0.25% increases next year.

As those have been priced in, with shorter-dated bond yields rising, the longer-dated part of the yield curve has been falling.

Interestingly, this is the opposite of what occurred during the taper tantrum in 2013, when the long end sold off in response to reduced asset purchases by the Fed.

Emerging markets respond well to higher growth and higher commodity prices — and poorly to higher US interest rates and increased volatility.

With global growth strong and the Fed still committed to easy monetary policies, emerging economies and emerging markets are well placed.

But we’ll need to see the volatility in rates and yields calm down before investors can be more confident about the asset class.

About Pendal Global Emerging Markets Opportunities Fund

James Syme and Paul Wimborne are senior portfolio managers and co-managers of Pendal’s Global Emerging Markets Opportunities Fund.

The fund aims to add value through a combination of country allocation and individual stock selection.

The country allocation process is based on analysis of a country’s economic growth, monetary policy, market liquidity, currency, governance/politics and equity market valuation.

The stock selection process focuses on buying quality growth stocks at attractive valuations.

Find out more about Pendal Global Emerging Markets Opportunities Fund here

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

GLOBAL fixed income markets have been marching to a common theme lately.

Inflation data have been on an upward trend and there seems to be consensus that inflation will climb higher still.

Market pricing for rate rises from major central banks is outpacing what the policy makers themselves are saying.

Inflation will be going higher over the next couple of quarters. That theme is global since the driving forces behind the trend are global.

Supply chain disruptions coupled with higher goods demand have affected us all. As lockdowns lift and consumption normalises, there will be a handover from goods inflation to services inflation.

There is an assumption that rising wage pressures will be an equally global theme.

That is not the case. As RBA Assistant Governor Lucy Ellis pointed out this week, market fixation with labour market patterns offshore is leading to an overly optimistic outlook for wage developments in Australia.

Labour force participation rates in the US have been slow to recover since the depths of the pandemic. That same degree of sluggish return to work need not apply to Australia.

Initiatives such as JobKeeper have been instrumental in maintaining a link between employers and workers.

In the US, the fiscal response was aimed at generous unemployment benefits. So generous at first, in fact, that many workers chose to quit their jobs so they could access a better income stream.

Find out about

Pendal’s Income and Fixed Interest funds

Another difference is the health policy response in handling the pandemic.

In the US, despite attempts at various lockdown measures, Covid has unfortunately run rampant in the community. In Australia, a zero-Covid strategy until very recently has produced a far better population health outcome.

While the US vaccination rate seems to have stalled around the 60% mark, Australia’s vaccination rates continue to climb. New South Wales passed 92% this week.

For the US, this translates to slower re-entry into the labour force by workers who are still legitimately fearful of contracting the virus.

The resulting picture differs for wage pressures in Australia and the US.

Sure, both central banks are willing to let things run hotter for longer. But the heat is far more intense in the US.

Nevertheless, the market prices a matched pace of rate hikes for Australia and the US in 2022. Either the Fed will need outpace the market, or the RBA will prove the market wrong.

Higher yield prospects bring on more corporate issuance

Likely driven by the fear of rate hikes translating into higher refinancing rates next year, the pace of corporate issuance has been heavy so far this month, especially offshore.

European and US credit markets have seen higher-than-typical new issuance volumes in the past two weeks.

Despite continued inflows into both sectors, the supply deluge has been weighing on credit spreads — and hence the secondary market performance of many of these new deals.

In Australia the new issue pipeline has also been solid — about $3.5 billion of benchmark deals hit the market this week.

Issuers have ranged from utilities and banks to commercial and industrial real estate investment companies.

Contrary to the offshore credit climate, however, demand appetite remains very robust in Australia. Most deals have been able to price at the tighter end of price guidance and perform well in the secondary market.

Emerging market volatility

The higher yield environment would usually be a particular headache for emerging markets, especially accompanied by a climbing greenback and slowing China.

On the whole, emerging market hard currency sovereign debt has been resilient in the face of yield climbs so far this month, with yield-related widening in spreads broadly in line with global high yield.

This is because most emerging market central banks have been proactive and keenly aware of inflation pressures.

They have no desires to invite an ugly currency-inflation spiral. Moreover, the global economy is still in good shape, in spite of China’s property-driven slow-down.

The key driver of volatility for emerging market sovereign risk has been the volatility in Turkey and in particular around the currency.

This volatility stems from the Turkish’s president’s unorthodox views on the relationship between inflation and interest rates — and hence the high turnover of the leadership of the Turkish central bank.

A noteworthy improvement now versus the last Lira crisis in 2018 is the composition of the country’s external debt rollover risk.

A lot of the maturing debt is held by the government or institutions that have historically exhibited high roll-over rates even in times of crisis.

Our portfolios currently have no exposure to the Turkish Lira — or any other high-beta local emerging market risk.

Our income strategies employ a tactical allocation to the USD emerging market sovereign index. Turkey is a component of that.

We expect political developments in Turkey to continue punctuating sovereign credit spreads with bouts of volatility, but current market pricing is also compensating investors for that volatility.

Our exposure remains highly liquid and our investment process tunes into left-tail risks.

These are aspects of our investment philosophy that will help us to de-risk promptly and efficiently out of emerging markets when warranted.

About Amy Xie Patrick and Pendal’s Income and Fixed Interest team

Amy is Pendal’s Head of Income Strategies. She has extensive expertise and experience in emerging markets, global high yield and investment grade credit and holds an honours degree in economics from Cambridge University.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia. The team oversees some $20 billion invested across income, composite, pure alpha, global and Australian government strategies.

Find out more about Pendal’s fixed interest strategies here

About Pendal Group

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

Pendal Sustainable Australian Fixed Interest Fund – Class R (APIR: BTA0507AU, ARSN: 612 664 730)

On 25 November 2021, the existing units of the Pendal Sustainable Australian Fixed Interest Fund (Fund) were reclassified as ‘Pendal Sustainable Australian Fixed Interest Fund – Class R’. The name of the Fund did not change and there were no changes to the terms of the class or your rights as an investor.

What do you need to do?

No action is required. You will be able to continue to invest or withdraw from the Fund.

An updated Product Disclosure Statement (PDS) was issued on 25 November 2021 and made available on www.pendalgroup.com.

Economics rather than environmentalism can explain much of the global renewables boom, says Regnan’s head of research, Alison George.

- Pollution, consumer preferences driving shift to renewables

- Economics are clear: renewables now cheapest in all key regions

- Pursuit of net zero would turbo-charge this trend

THE transition to a renewable energy system is a mega-trend that will drive investment returns for decades.

Renewables are expected to account for 70 per cent of the $US530 billion spent on all new generation capacity in 2021, says the International Energy Agency.

But with almost every part of the global economy touched by the transition, picking investment opportunities can be daunting.

Successful investing in the transition is made even more difficult by noisy debate and political point-scoring about the best path to net-zero carbon emissions.

But beyond the noise, much of global shift to renewable energy can be explained by underlying forces that are with us today and offer some quite understandable and investable opportunities, says Alison George, head of research at Regnan, a global leader in sustainable investing.

“There’s a whole lot of change happening in energy systems — all from three key drivers,” says George.

“Emissions are important, but in developing countries it’s air pollutants that are key to changes happening now, with climate concerns coming up behind.”

Then there’s changing consumer preferences and technological advancement.

Sustainable and

Responsible Investments

Fund Manager of the Year

“The shifts that are occurring in the energy system are a combination of those three factors playing out over time.”

Focusing on these three drivers can give investors a much clearer understanding of how the transition will affect their portfolios.

“In China and India, they are much more concerned with the very real problem of air pollution, which is causing significant numbers of extra deaths right now,” says George.

“Similarly, Australia’s love of home solar panels is not just about incentives — it’s about people liking the idea of being in control of their own power, playing to a personal independence narrative.

“It’s not just a decarbonisation preference — it’s a consumer preference.

“Historically energy was a low-engagement purchase, then all these apps came along so you can see how much power you are generating and connect it all up.”

George says the advancement in technology, which will ultimately allow households to trade energy the same way they trade stocks, via an app on their phone, will further drive the interest in renewables.

‘It’s not environmental, it’s economic’

Even global scale changes like the phasing out of coal-fired power stations can be explained by underlying economic drivers.

“Even without new commitments from governments, energy coal is already on the way out.

“It’s not environmental – it’s economic.

Find out about

Regnan Global Equity Impact Solutions Fund

“In the US there has been a huge changeover from coal to gas that was entirely economically driven because of the shale gas revolution.

“Suddenly the US had an abundant source of cheap gas and that has led to a lot of very economically rational coal to gas switching.”

This combination of an energy transition being driven by factors other than climate change allows investors to think differently about how they play the transition.

One implication is that the policy debate and regulatory overlay is perhaps less important than traditional economics.

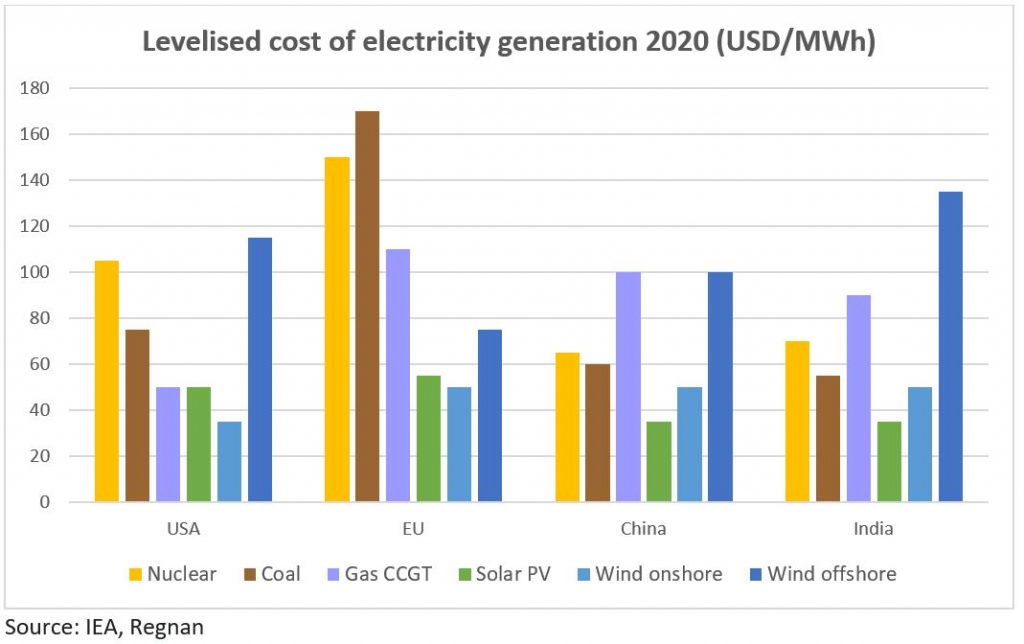

The International Energy Agency says renewable energy is now the cheapest way to lift energy production in all key regions.

“If you need more supply, the next megawatt will be renewable.

As the graph below shows, solar is the cheapest option in China and India. In the US and EU, it’s onshore wind.

The nuclear option

Economics also explain why nuclear is being left behind renewables, despite being low carbon, George says.

“Nuclear is expensive in relative terms, even in developing economies where input costs like labour and land are lower.”

That’s why nuclear doesn’t get much of a boost, even under the most ambitious decarbonisation scenarios.

“Renewables are already the best bet. It doesn’t matter what scenario we look at, renewable investment is a runaway car — it’s happening of its own accord.

“That is the key expectation that people should have.”

“Pursuit of net zero would only accelerate these trends, while also bringing hydrogen into the picture.

“There is a still a big gap between current policies and what is needed to achieve the net zero commitments being made by countries around the world.

“This represents a huge investment opportunity – worth a cumulative US$27 trillion by 2050 according to the IEA.

“Solar, wind and especially batteries would all be winners from increased environmental ambition, turbo charging current trends as more energy comes from electricity and renewables get a larger share of an even bigger electricity pie.

“Electricity networks would also require substantial increased investment.”

About Alison George

Alison George is Regnan’s head of research. She has deep experience in ESG, responsible investment and active ownership. Alison oversees Regnan’s research frameworks, processes and outputs, ensuring it remains at the forefront of industry practice and meets evolving clients needs.

About Regnan

Regnan is a responsible investment leader with a long and proud history of providing insight and advice to investors with an interest in long-term, broad-based or values-aligned performance.

Building on that expertise, in 2019 Regnan expanded into responsible investment funds management, backed by the considerable resources of Perpetual Group.

The Regnan Global Equity Impact Solutions Fund invests in mission-driven companies we believe are well placed to solve the world’s biggest problems.

The Regnan Credit Impact Trust (available in Australia only) invests in cash, fixed and floating rate securities where the proceeds create positive environmental and social change. Both funds are distributed by Perpetual Group in Australia.

Find out about Regnan Global Equity Impact Solutions Fund

Find out about Regnan Credit Impact Trust

For more information on these and other responsible investing strategies, contact Head of Regnan and Responsible Investment Distribution Jeremy Dean at jeremy.dean@regnan.com.

There are plenty of so-called ‘climate-aware’ companies to invest in — some 60 per cent of the ASX300 (by market cap) now have net zero commitments. But how do you judge the right ones? EDWINA MATTHEW explains

- Not all net zero commitments are the same

- Strategy and governance, disclosures and analysis of targets are critical, plus transition implications for workers

- Red flags include board sceptics, indirect impact from value chains and lack of progress

Some 60 per cent of the ASX300 (by market cap) now have net-zero commitments.

That’s a reflection of accelerating global progress on climate change.

Almost 90 per cent of global emissions are now covered by net-zero commitments from nations — up from about 75 per cent before the recent COP26 climate change conference.

Financial institutions are also forming initiatives — such as the Glasgow Financial Alliance for Net Zero announced at COP26 — to accelerate the transition away from fossil fuels.

So Australian investors have plenty of opportunity to invest in “climate-aware” companies.

The question is: how do you judge which companies are best placed to deliver on their net-zero commitments?

“Investors and the public are sceptical about the credibility and veracity of many net-zero commitments,” says Edwina Matthew, Head of Responsible Investments at Pendal Group.

“Investors need to ensure the companies they invest in are walking the talk.

“That means having a clear and credible climate strategy in place that is based on delivering actual real-world decarbonisation, and not just ‘virtual’ reductions from carbon offsets and asset divestment.”

Below Edwina lists some key things to look for.

Sustainable and

Responsible Investments

Fund Manager of the Year

Examine a company’s net zero targets

A company needs targets that span the life of its transition plan – including intermediate (typically 2030) and long-term (2050) targets. They need to be science-based and aligned to the Paris Agreement.

Companies should also be clear in their disclosures about whether their targets are across “scope 1, 2 and 3 emissions” — and what percentage of its assets and emissions are covered by those targets.

What are Scope 1, 2 and 3 emissions? They are the three factors an organisation should consider to understand its carbon footprint.

- Scope 1 greenhouse gas emissions come directly from sources controlled by a company

- Scope 2 are indirect emissions associated with the purchase of electricity, steam, heat or cooling

- Scope 3 result from assets not controlled by a company, but indirectly impacted by its value chain

Investors also need to look out for how carbon offsets are used in their net zero plan and also whether there is reasonable consideration of transition implications for their workforce and communities.

To mitigate risks of ‘green-washing’, investors need to not just look at the company’s targets but also look at the governance and incentive structures and disclosure practices.

Is there clear evidence that a company’s climate transition plan is incorporated into its corporate strategy and risk management systems?

Red flags to watch out for

There are also red flags for investors, Matthew says.

“One is having net zero implementation responsibilities sitting solely in a sustainability or ESG role rather than being incorporated into relevant executive and business line responsibilities.

Also look out for climate sceptics on boards or lobbying against change via industry associations.

“Investors should also assess whether scope 3 emissions are sufficiently considered. While it’s an iterative process that should be refined over time, there should be demonstrable evidence of progress.”

Find out about

Pendal Horizon Sustainable Australian Share Fund

Climate transition plan

Companies should have a climate transition plan with detailed analysis of material risks and opportunities.

There should be evidence the analysis is used to inform business decisions (including relevant capital allocation), resourcing and expertise and sometimes links to remuneration.

Investors should ask themselves if the board has sufficient skills. Is there stakeholder engagement? What is the track record of achieving previous transition strategies and targets?

Disclosures

Investors need to also pay close attention to disclosures.

Does a company produce reporting in line with the Task Force on Climate Related Financial Disclosures (TCFD)? How regular and comprehensive are they?

Does a corporate clearly outline the most material climate-related risks and opportunities for its business? How robust is the analysis that sits behind these views?

“We want to make sure their net zero plan is credible. It should be practical but adequately ambitious to align with key stakeholder expectations,” Matthew says.

“Without doubt the private sector on the whole is stepping up to the net zero call to action and this is a very important development.

“As investors, the onus is now on us to pay attention to the detail and progress of individual net zero plans.

“Through company engagements, we are working with companies to address any shortfalls and accelerate real economy decarbonisation.”

About Edwina Matthew

Edwina Matthew is Pendal’s Head of Responsible Investments. Edwina is responsible for maintaining our leadership position in the provision of sustainable and ethical investment products.

Edwina is actively involved in the implementation of the UN-supported Principles for Responsible Investment. She also represents the company in working groups with a number of industry associations and initiatives relating to responsible investment.

About Pendal Group

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

We believe sustainability considerations ultimately drive higher and more stable investment returns over the long term.

Pendal Group has a proud heritage in responsible investing, extending back decades. Our specialist responsible investing business Regnan includes highly experienced ESG research and engagement experts and offers a growing range of investment strategies.

Some of our responsible investing strategies

Here are the main factors driving the ASX this week according to our head of equities Crispin Murray. Reported by portfolio specialist Chris Adams

The market is focused on two issues right now.

- First there is increasing scrutiny on signals from the US Federal Reserve. Expectations are building that rates will need to rise sooner rather than later. The idea that the Fed could be comfortable with higher inflation as a “catch-up” from the previous period of low inflation is in question

- The second issue is the new wave of Covid in Europe, the extent to which this will be replicated in the US and the potential economic impact.

Both issues have the potential to depress bond yields. Confidence that the Fed will take action to control inflation can support the bond market. So too can another Covid wave if it suppresses economic growth.

This is reflected in the equity market with a rotation from cyclicals to growth and defensives.

Equity market returns were muted last week. The S&P/ASX 300 fell 0.47% and the S&P 500 gained 0.36%.

We think sentiment on these two issues presents a risk to markets — but more in the way of driving material rotation rather than a sustained sell-down.

Abundant liquidity, decent economic growth and stimulatory policy all remain supportive of the overall market.

Covid and vaccines

Unfortunately the pandemic has escalated again. A surge in central European cases has culminated in a nationwide lockdown in Austria and the potential for other countries to follow suit.

Only about two-thirds of Austrians are fully vaccinated. But even in The Netherlands, where almost 74% of people are fully vaccinated, there is a surge in new cases.

The acceleration highlights the seasonal element of Covid (as the northern hemisphere heads into winter) and the importance of increasing vaccine penetration.

Pendal Focus Australian Share Fund

Now rated at the highest level by Lonsec, Morningstar and Zenith

In the US, both new cases and hospitalisations have increased.

The market is concerned a new wave will result in a repeat of the economic hit in June and July.

At this point we think two factors can support a less severe outcome:

- Each successive wave has resulted in less economic impact. We think this should continue to hold true. Continued penetration of vaccines since mid-year — coupled with boosters and better treatments — should reduce risk of broad-based lockdowns. There is also a question about the degree to which some communities would tolerate additional blanket lockdowns.

- Economic growth was starting to slow from the second quarter peak when the last wave hit the US. This time the economy is accelerating. So while the latest surge may constrain economic improvement, it would not be reinforcing an already declining trend.

That said, the market will need convincing — and trends are likely to be negative in the next few weeks. This would support continued rotation from cyclicals to growth and defensives.

The key will be whether countries such as Germany and the US follows a UK-like path, where cases are at moderately high levels, but hospital numbers are manageable.

Economics and policy

Japan’s US$500 billion stimulus package and the passage of the Biden US$1.2 trillion infrastructure bill emphasise that fiscal policy will remain supportive.

We’ve also seen agreement at US agricultural equipment maker John Deere and Co, which experienced its first strike for wage growth in 30 years.

Workers agreed to a six-year deal including a 10% rise in the first year, sign-on bonuses and a return of cost-of-living adjustments. Yet another sign of the wage pressure coming through.

Inflation

There is a view building that the Fed is likely to signal a more hawkish shift on rates in its next meeting on December 14-15.

Previously, the Fed’s line has been that it was comfortable with higher inflation because there had been a period of lower-than-target inflation. This could act as a buffer for inflationary pressure.

No matter how transitory you believe current inflation to be, this buffer has now gone.

The Fed can continue to argue it is tolerating higher inflation to support employment goals. But the notion that inflation can run hotter to offset previous muted inflation no longer holds.

The market is also increasingly aware that some of the more structural drivers of inflation are flowing through and will be difficult to hold back. For example, leading indicators of housing rents suggest this will pick up materially over the next 12 months.

At the same time, the outlook for growth remains reasonably strong, despite the potential for another Covid wave, as discussed earlier.

To put some context around the combination of growth and inflation on nominal GDP, we are set to see levels in Q4 not seen since the early 1980s.

Nominal GDP is a reasonable proxy for corporate revenue and should underpin corporate earnings growth into CY22.

The risk comes if it also forces central banks to apply the brakes more aggressively.

This combination of higher growth and the flow-through of property-related inflation saw three members of the Fed signalling last week that the topic of faster tapering will be discussed at the December meeting.

There are two broad schools of thought on inflation at the moment:

- Current inflation is a function of temporary factors relating to the mismatch of supply and demand. Supply chains were unprepared for the rebound in demand as consumers came out of lockdown. There have been episodes of this before, such as in the early 1950s at the start of the Korean War. The lesson then was that inflation quickly fades as it begins to eat into the spending power of consumers and leads to demand destruction.

- The alternative view is that while the initial rise of inflation was induced by these temporary factors, it now becomes entrenched due to issues around labour supply, shortening supply chains, the impact of de-carbonisation (greenflation) and a lack of adequate response from central banks.

In this regard, the two key issues to monitor in upcoming months are US labour market participation and how prepared central banks are to anchor inflation expectations.

On the latter point, a decision to replace Fed Chair Powell or appoint him for a second term with be important. Lael Brainard is seen as an alternative. Powell remains the favourite, but his odds have fallen in recent weeks.

China

There have been signs in recent weeks that Beijing is looking to ease policy in response to slowing growth.

This is not straightforward. The same cocktail of factors dragging on growth also make an effective response difficult. These include:

- Beijing’s zero-Covid approach

- Power constraints

- High raw-material prices

- Weak housing sentiment

- High debt, leading to constraints on local government financing

- A strong currency

Recent statements from Premier Li Keqiang and the People’s Bank of China suggested an emphasis on constraining credit was diminishing and there was a need to safeguard exports.

A shift in policy direction will help limit the slowdown. Concerns around the Evergrande issue have also receded. However we do not see this as the time to be too bullish on China-sensitive stocks.

Beijing faces headwinds in its effort to combat slowing growth. Covid remains a challenge. So, too, do poor consumer sentiment towards property, rising inflation, weakening exports and constraints on local government funding for infrastructure due to falling land sales.

Meanwhile China has imposed environmental-based constraints on growth ahead of the Winter Olympics in March.

Sustainable and

Responsible Investments

Fund Manager of the Year

While we are likely to see cuts in reserve ratio requirements for the banks, increased credit growth and some fiscal measures, these will probably be incremental in nature.

They will also take time to flow through.

We can reasonably expect concerns over China’s growth to remain in place for the first quarter of 2022.

Markets

Rising Covid, combined with a stronger US dollar, has led to a rotation away from cyclicals and back towards growth.

It’s worth noting that within tech, large cap is performing better than small cap in the US. This reflects rising volatility in the macro environment, which favours the more stable names with stronger earnings.

Oil prices were weaker as the US released some strategic energy reserves. There was talk that Washington was lobbying China to do likewise to help ease energy prices, though this is unlikely to work in the medium term.

In Australia the banks have given up their market leadership for 2021 (year-to-date) on the back of an update from Commonwealth Bank (CBA, -9.54%). Financials have returned 26.09% YTD, versus 33.33% for Communication services and 27.91% for Consumer Discretionary.

Growth names did best last week. Technology (+3.08%) and Health care (+2.82%) led. Financials fell 3.22%, Energy was down 1.57% and Materials lost 1.48%.

About Crispin Murray and Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia. Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Find out more about Crispin Murray’s Pendal Focus Australian Share Fund

Find out about Crispin’s sustainable Pendal Horizon Fund